1 Introduction

Large differences in lifetime earnings (LE) are evident among workers in the U.S. (Guvenen et al. (2017)). Even though inequality starts early in life, the striking differences in earnings growth over the life cycle are key for understanding the LE distribution. In this paper, we study these differences using administrative balanced panel data by focusing on heterogeneities in two important forces that the previous literature has deemed important for earnings growth: the ability to i) accumulate human capital (Huggett et al. (2011)) and ii) climb the job ladder (Topel and Ward (1992)). We aim to quantify the importance of each of these mechanisms throughout the LE distribution by identifying and investigating different types of career paths.1

We use a confidential employer-employee matched panel of the earnings histories of male workers between 1978 and 2013 from the U.S. Social Security Administration (SSA). Using a 10% sample of workers born between 1953 and 1960, we first compute workers’ total wage and salary income over the ages of 25 to 55 and rank them into 50 LE quantiles. Top 2% group earns about 7.5 times that of median LE workers, who earn 3.5 times that of bottom earners. The vast majority of these differences are a result of earnings growth heterogeneity: top LE individuals see their incomes rise by more than 17-fold between the ages of 25 and 55, median LE workers experience more than twofold increase, and those at the bottom see essentially no earnings growth.

We employ a job ladder model with two-sided heterogeneity in the spirit of Cahuc et al. (2006) and Bagger et al. (2014) as a measurement device to quantify the relative roles of latent heterogeneity in job ladder dynamics and human capital accumulation throughout the LE distribution. The model features learning on the job, on-the-job search, employer competition, and idiosyncratic shocks to worker productivity. To bring the model closer to data, we add to this framework a life-cycle structure in the form of perpetual youth. Importantly, we allow for rich ex-ante worker heterogeneity in unemployment risk, the job finding rate, and the contact rate for employed workers, as well as the ability to learn on the job. Finally, the model also features recalls for unemployed workers by their last employers (Fujita and Moscarini (2017)).

The key insight for identifying the importance of human capital and job ladder risk throughout the LE distribution relies on differences in job switching patterns and earnings changes of job stayers and switchers. In the data, about 30% of the bottom LE workers stay with the same employer in two full consecutive years, compared to around 60% above the median. Relatedly, bottom earners work for about 12 employers between the ages of 25 and 55, more than twice as many as those above the median.

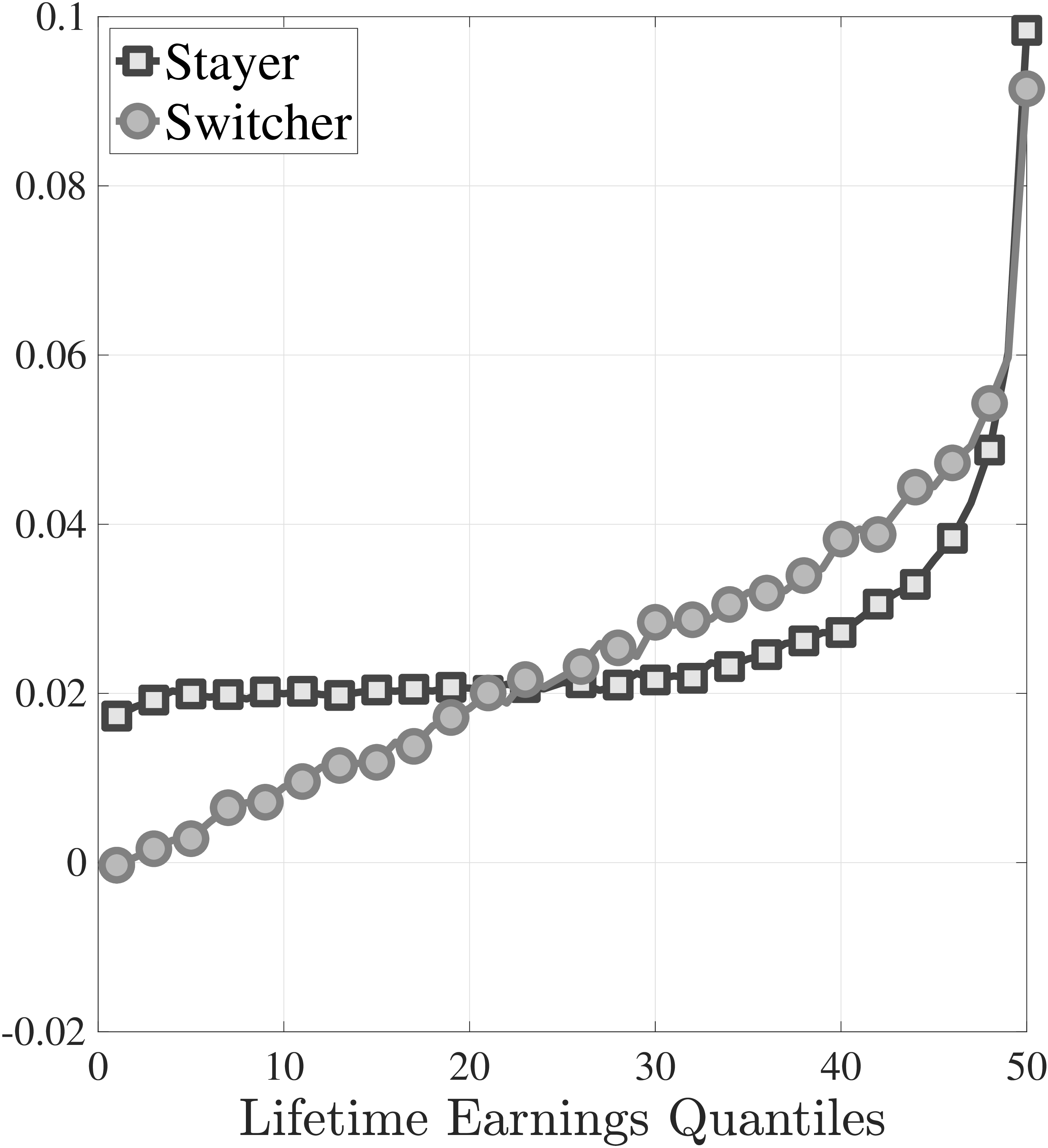

Our key novel empirical finding is that average annual earnings growth for job stayers is surprisingly similar, around 2% in the bottom two-thirds of the LE distribution, whereas for job switchers it rises almost linearly from 0% for the bottom earners to around 3% for those in the 65th percentile.2 This large heterogeneity indicates that the nature of job switches is very different across the LE distribution. By exploiting the distribution of earnings changes for job switchers, we argue that more than 35% of job switches are a result of a significant unemployment spell for bottom earners, compared to only around 15% in the top tercile. Finally, earnings growth of job stayers and switchers increases steeply in the top tercile, reaching around 10% for the highest earners.

These facts imply that differences in earnings growth in the bottom half of the LE distribution are coming from growth differences of job switchers, suggesting strong heterogeneity in job ladder risk among them. Job stayers’ growth differences, however, should be the main culprit in the upper half, as high LE workers rarely switch employers, hinting at differences in returns to experience. Inference is more complicated, because, for example, wage growth of job stayers is also affected by outside offers and a higher incidence of unemployment can stem from higher ex-ante risk or bad ex-post luck. We estimate our model with this rich set of facts to obtain an exact quantitative assessment of the importance of different economic forces. Specifically, we target the fraction and average earnings growth of job stayers and switchers as well as the higher-order moments of their earnings changes by LE groups and over the life cycle.

One of our major contributions is to quantify the vast ex-ante heterogeneity in job ladder risk. We estimate a quarterly job loss risk of 9% for bottom LE workers, compared to 2% above the median. Quarterly job finding rates also display large differences, ranging from 30% at the bottom to 50% above the median LE. Given the annual nature of the SSA data, we cannot directly test these estimates. Instead, we use the Survey of Income and Program Participation (SIPP) to document large differences in job loss and job finding rates across workers with different past earnings and over the life cycle that are quantitatively consistent with the estimated model. Turning to the contact rate for employed workers, we find that bottom LE workers have a 30% probability of being contacted in a quarter, relative to a 55% probability at the top. However, the SIPP data show that high earners are less likely to make job-to-job transitions. Our model matches this feature of the data as well: Despite getting more outside offers, high LE workers tend to work for more productive firms and can rarely be poached. We directly test this mechanism using data from the Survey of Consumer Expectations (SCE) and find more contacts for people with higher past earnings, consistent with our estimates.

The estimated model provides a good account of the career trajectories of workers by LE groups, so we use it to decompose the differences in lifetime earnings. First, we find that wage—rather than employment—differences explain the vast majority of LE inequality. The only exception is inequality at the bottom half, where employment differences also play some role: bottom LE workers work about 25% less than those at the median. A higher ex-ante job loss rate and—to a lower extent—a lower job finding rate for bottom LE workers explain almost all of these employment differences. Employment differences among those above the median are negligible in comparison.

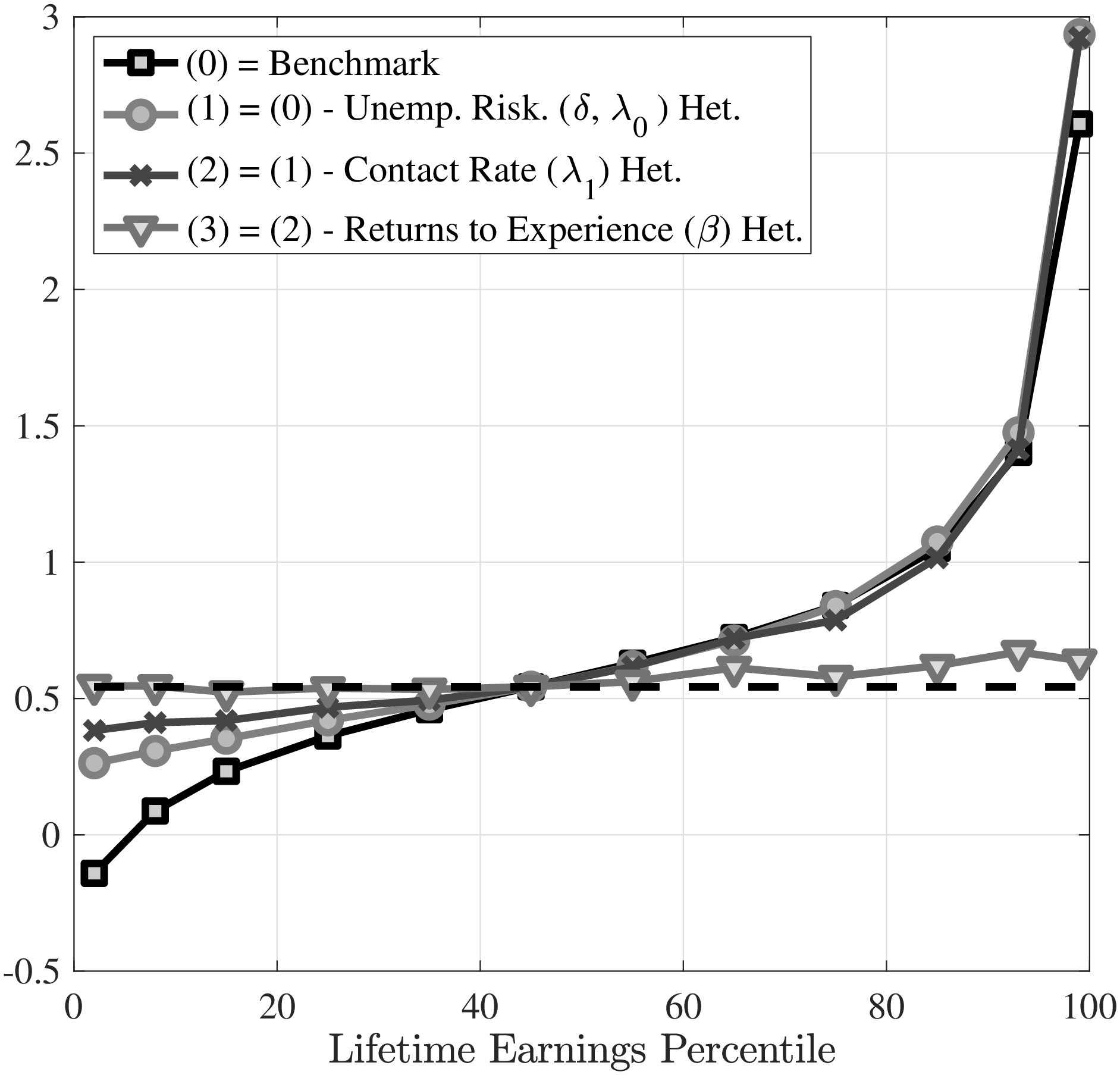

Turning to differences in lifetime wages, we find them to be mainly driven by wage growth over the life cycle, resonating with our empirical findings on earnings inequality and earnings growth. In a series of experiments, we isolate the relative roles of ex-ante differences in job ladder risk and the returns to experience. Heterogeneity in unemployment risk accounts for more than 50% of the wage growth differences between workers in the bottom and the median. High unemployment rates among low LE workers reduce wage growth by preventing these workers from accumulating human capital and from climbing the job ladder; the former channel accounts for about 70% of the total effect. Differences in contact rates also have a nonnegligible effect on wage growth heterogeneity. Eliminating them closes an additional 20% of the wage growth gap between workers in the bottom and the median by allowing low LE workers to move to better firms.

While ex-ante heterogeneity in job ladder risk is important at the bottom half of the LE distribution, it explains very little of the differences above the median. In contrast, heterogeneity in learning ability drives almost all earnings growth differences above the median but only about 20% of these differences among the lower half. This is because learning ability is Pareto distributed, which implies that average returns to experience is relatively similar in the bottom half and increases steeply toward the top of the LE distribution, essentially mirroring average stayer earnings growth. For workers who enjoy high wage growth regardless of job switching—the top LE group in the data—the model assigns a high level of returns to experience.

A key conclusion of our study is that different economic forces are driving the inequality in different parts of the LE distribution. While bottom LE workers experience low wage growth relative to the median throughout their working life, primarily because of poor labor market experience (i.e., high unemployment risk and fewer outside offers), workers at the top see high wage growth, mainly because they enjoy a very high level of returns to experience. These quantitative findings resonate with the empirical patterns of job mobility and income growth of job stayers and switchers across the LE distribution.

Our findings also shed new light on the relative roles of initial conditions and ex-post shocks in determining lifetime inequality (Keane and Wolpin (1997); Huggett et al. (2011)). In our model 81% of the variation in lifetime earnings is a result of ex-ante heterogeneity in initial conditions, which is substantially higher than the corresponding 61% figure Huggett et al. (2011) find from a similar exercise. They use a calibrated Ben-Porath (1967) human capital model that features ex-ante heterogeneity in initial human capital and learning ability but not job ladder dynamics. Thus, the higher role for initial conditions stems from the rich worker heterogeneity in job ladder risk in our estimation, which can more precisely capture the source of inequality in the bottom half.

Related literature and our contributions. The broad contribution of our paper is to quantify the heterogeneity in economic forces across the income distribution. Recently, Guvenen et al. (2021) and Guvenen et al. (2014b) use the SSA data to document the nature of idiosyncratic risk, with a focus on higher-order moments, across the income distribution and over the life cycle and business cycle, respectively. Both papers are mostly descriptive and estimate reduced-form income processes. We use moments similar to those in Guvenen et al. (2021) along with new ones we document to structurally estimate a job ladder model and identify the economic forces behind earnings growth.

Hubmer (2018) shows that a reasonably calibrated job search model as in Burdett and Mortensen (1998) can capture the higher-order moments of earnings growth documented in Guvenen et al. (2021). We make use of these insights for estimation, but our focus is on quantifying the latent heterogeneity in job-ladder risk and the ability to learn and their roles in lifecycle earnings growth differences, all of which are absent in Hubmer (2018). Another closely related paper is Bagger et al. (2014), which estimate a job ladder model similar to ours for Denmark. They investigate educational differences, while we study the entire LE distribution. Finally, they use information on firm productivity to estimate their model, which we lack in our dataset. Instead, we develop an identification scheme that exploits the earnings growth distributions of job stayers and job switchers.

Finally, there is a growing body of research that estimates the latent heterogeneity in job ladder risk (e.g., Ahn and Hamilton (2020); Morchio (2020)). Most recently, Gregory et al. 2021 employ k-means clustering to group workers according to their job ladder risk in the Longitudinal Employer-Household Dynamics data. Hall and Kudlyak (2022); Ahn et al. (2022) use the Current Population Survey data to estimate a hidden-state Markov model of labor force transitions. All three papers reach similar conclusions to ours.

The rest of the paper is organized as follows. Section 2 presents the data and the stylized facts. Section 3 describes the model, Section 4 discusses its estimation, and Section 5 presents the estimation results. Section 6 provides the decomposition of lifetime earnings, and Section 7 discusses policy implications of our findings and concludes.

2 Empirical Analysis

In this section, we document several stylized facts that motivate and guide our analysis of lifetime earnings inequality. Our aim is to identify the heterogeneities in the ability to accumulate human capital and climb the job ladder by investigating the career paths of different LE groups over the working life. Our analysis is based on administrative annual data from the SSA. We support these findings using monthly panel data from the SIPP as well.

2.1 The SSA data and sample selection

Our data are drawn from the Master Earnings File (MEF) of the SSA records, which includes every individual with a Social Security number (SSN). Basic demographic variables available are date of birth, place of birth, sex, and race. The earnings data are derived from the employee’s W-2 forms. The measure of labor earnings is annual and includes all wages and salaries, bonuses, and exercised stock options as reported on the W-2 form (Box 1). The MEF has a small number of extremely (uncapped) high earnings observations, therefore, we winsorize observations above the 99.999th percentile in each year. We convert nominal earnings into real values using the personal consumption expenditure deflator, taking 2005 as the base year. See Panis et al. (2000) and Olsen and Hudson (2009) for detailed documentation of the MEF.

W-2 forms contain another crucial piece of information for our purpose, an employer identification number (EIN), which identifies firms at the level at which they file their tax returns with the IRS. We use this variable to follow each worker’s career path at an annual frequency. Note that an EIN is a different concept than an “establishment,” which typically represents a single geographic facility of the firm. Two caveats are worth mentioning regarding the use of EINs to identify firms. First, an EIN is not always the same as the parent firm, because some large firms choose to file taxes at a level lower than the parent firm (see Song et al. (2018)). Second, firms may change their EINs, for example, due to ownership changes (see Haltiwanger et al. (2014)). As a result, we may be over counting the number of job switches.

Sample selection. We construct a 10% sample based on the randomly assigned last four digits of (a confidential transformation of) the SSN. We select individuals born between 1953 and 1960, for whom we therefore have data between ages 25 and 55 (referred to as a worker’s lifetime). Furthermore, we work with a sample of wage and salary workers with a strong labor market attachment because the mechanisms we investigate speak to labor market participants. One drawback is that the MEF does not have direct measures of labor force participation. We address this problem by excluding individuals with earnings below a time-varying minimum earnings threshold \(Y_{\text{min},t}\)—25% of a full-year full-time salary at half the minimum wage, e.g. \(\approx\)$1,885 in 2010—for i) at least one fourth of their working life, or ii) two or more consecutive years. These two criteria help us exclude early retirees, the disabled and those who are out of the labor force for other reasons.3 We also drop workers that are self-employed—those with self-employment income above the minimum earnings threshold \(Y_{\text{min},t}\) and more than 10% of his annual total earnings—(iii) for more than one eighth of their working life, or (iv) for two or more consecutive years.4 These restrictions exclude workers who choose self-employment as their career path, and yet keep those who rely on self-employment income during unemployment spells, as well as payroll workers with a small self-employment income on the side. This procedure reduces our sample from 1,845,640 individuals to 840,194 for whom we have at least 31 years of earnings data.5

2.2 Stylized facts on lifetime earnings inequality and growth

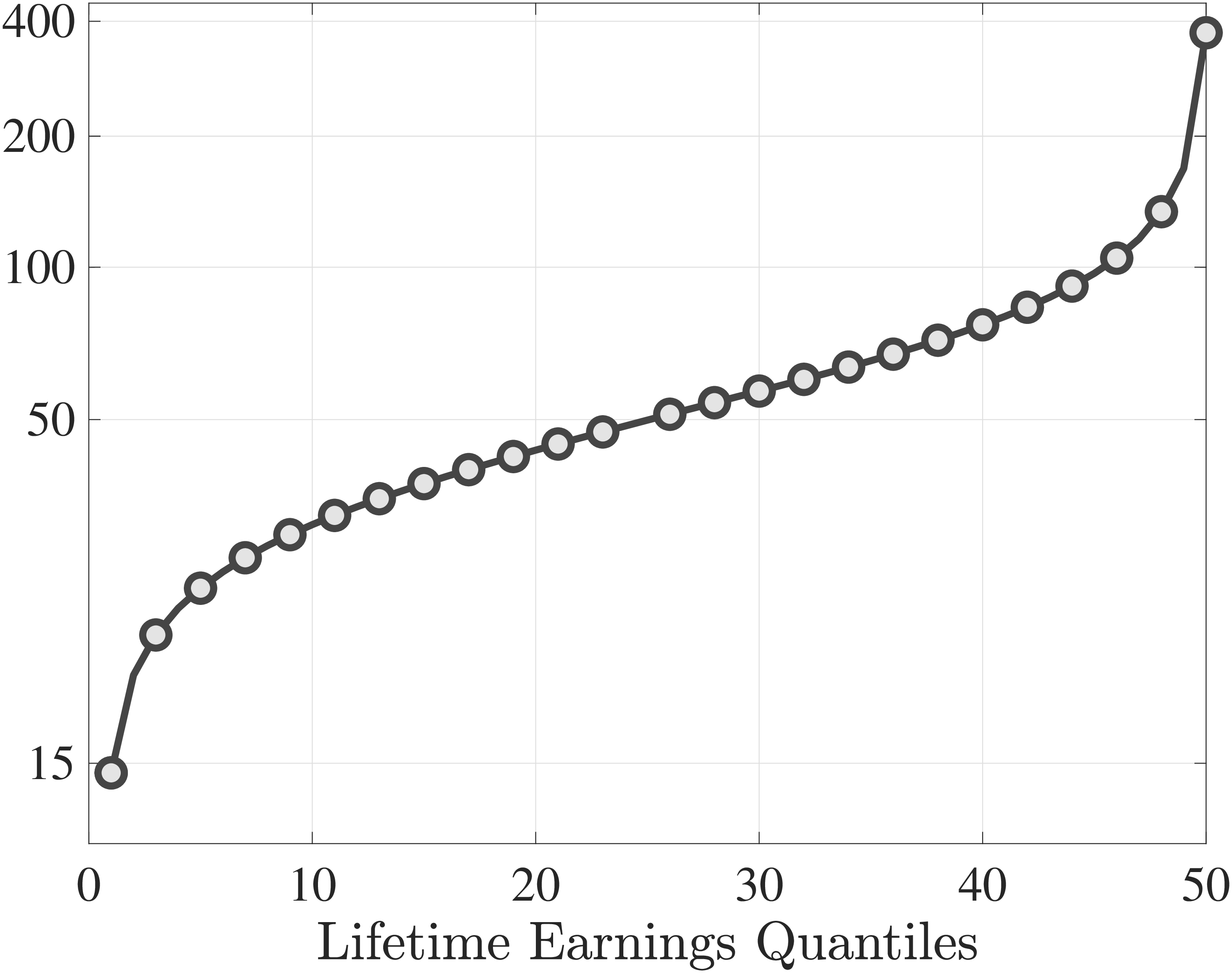

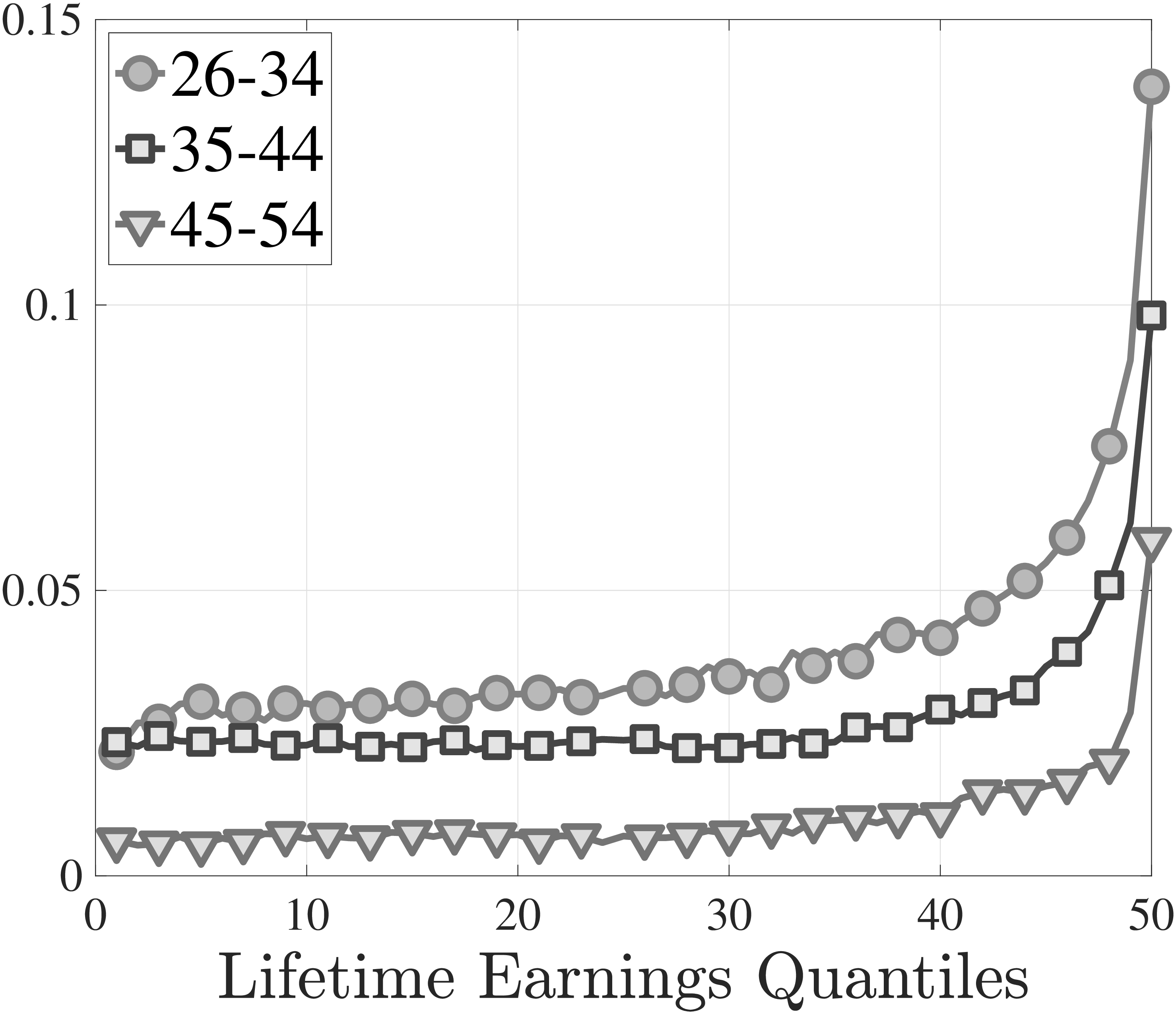

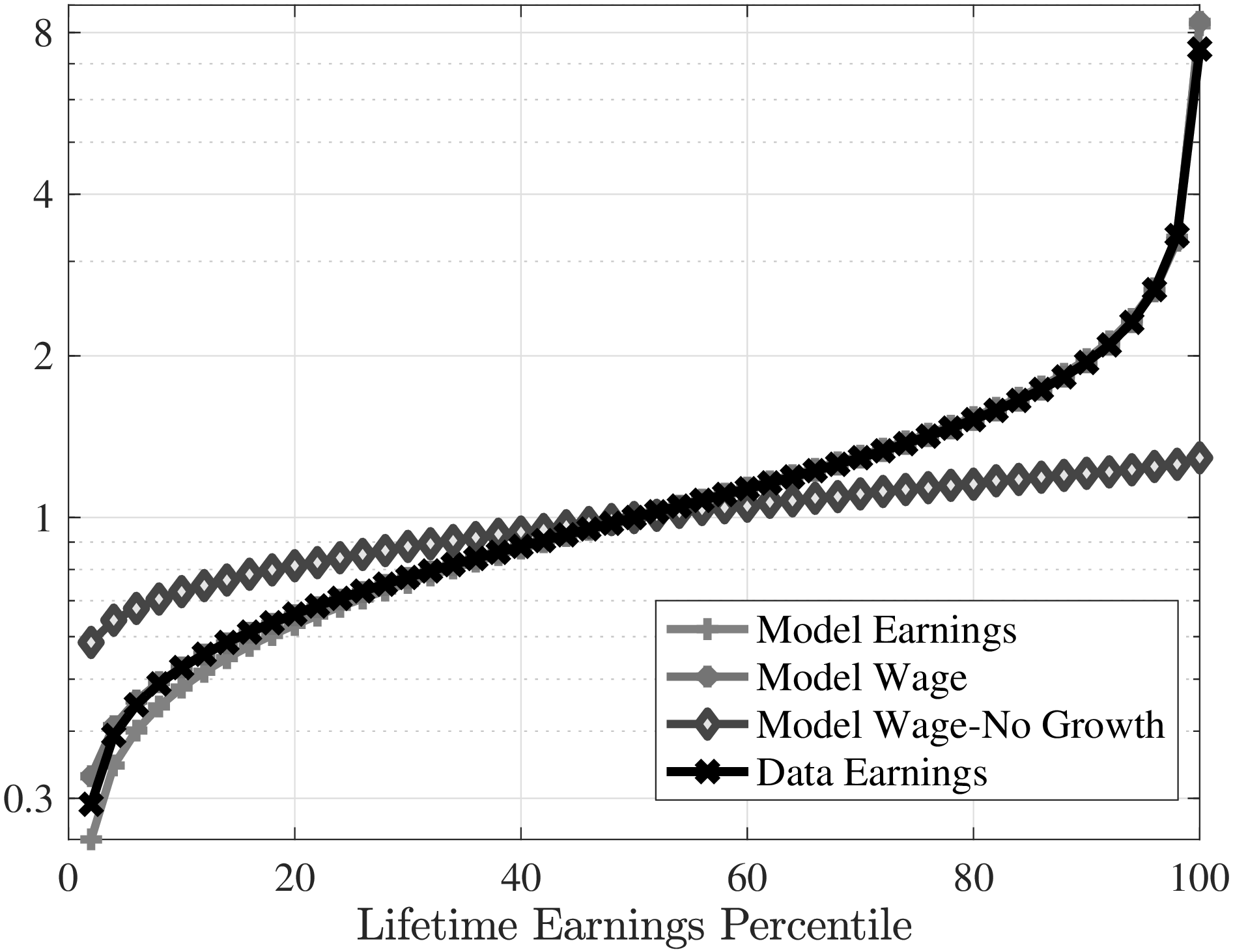

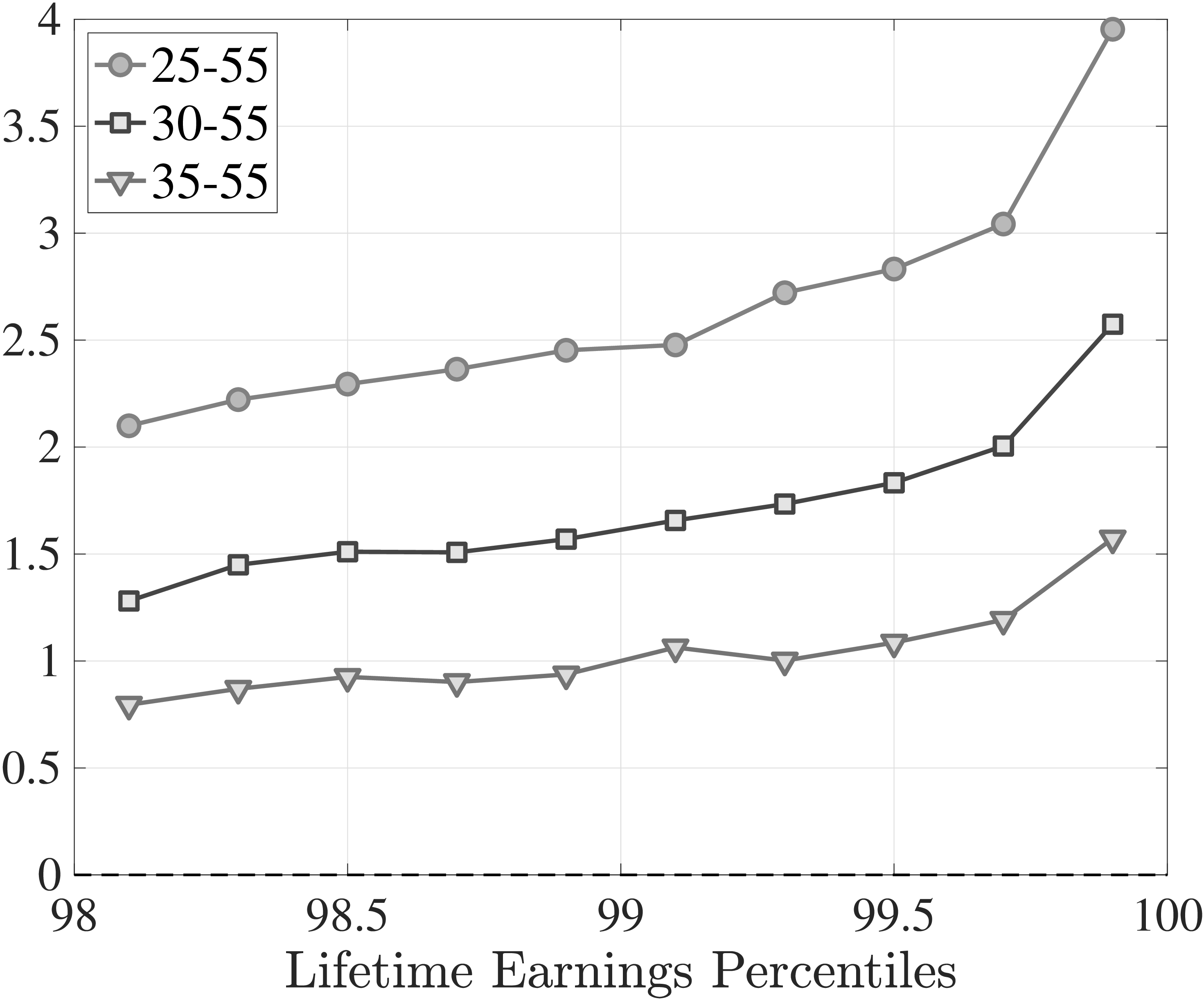

We compute lifetime earnings as the sum of individuals’ W-2 earnings from ages 25 to 55.6 This measure is then used to rank workers into 50 equally sized quantiles, \(LE_{j}\) for \(j=1,\ldots,50\). Individuals around the 90th percentile (\(LE_{45}\)) earn 3.7 times as much as those around the 10th percentile (\(LE_{5}\)) (see Figure 1a and Table A.2). This inequality is roughly half the annual earnings inequality, for which the ratio of the 90th percentile to the 10th percentile hovered around 8 throughout our sample period (Guvenen et al. (2014b)). Inequality is more pronounced at the top, with \(LE_{50}\) earning almost 4 times as much as \(LE_{45}\) versus \(LE_{5}\) earning almost twice as much as \(LE_{1}\).

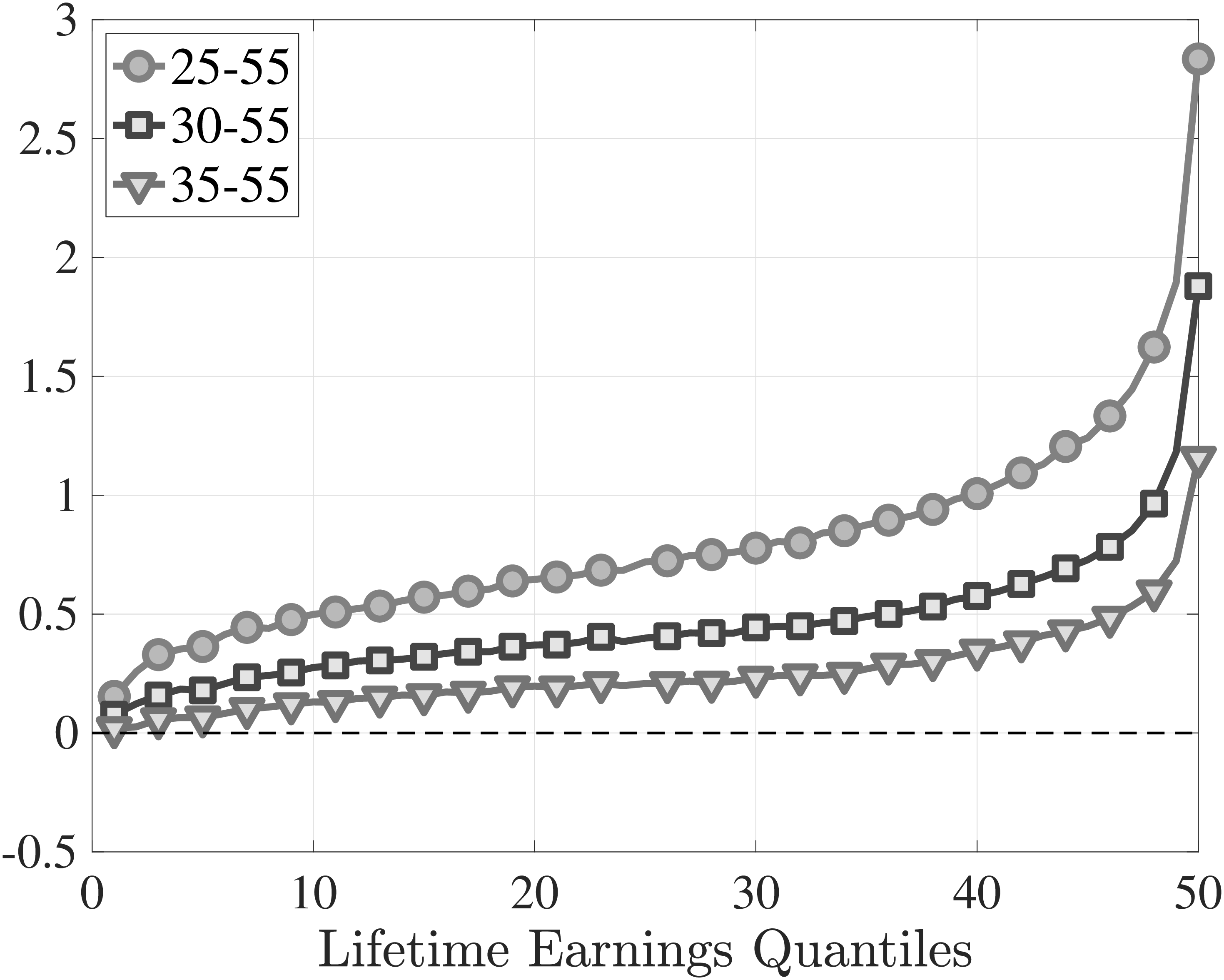

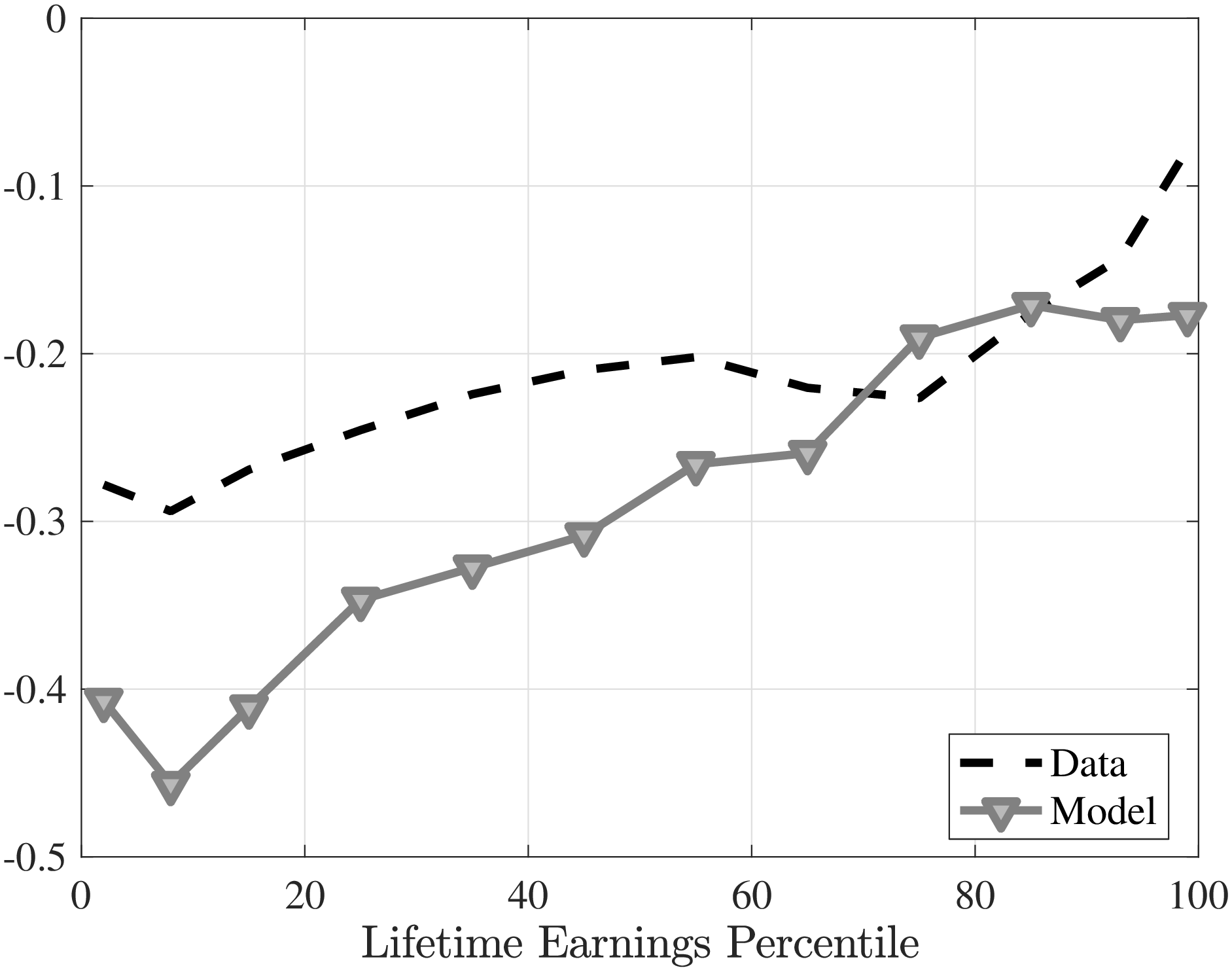

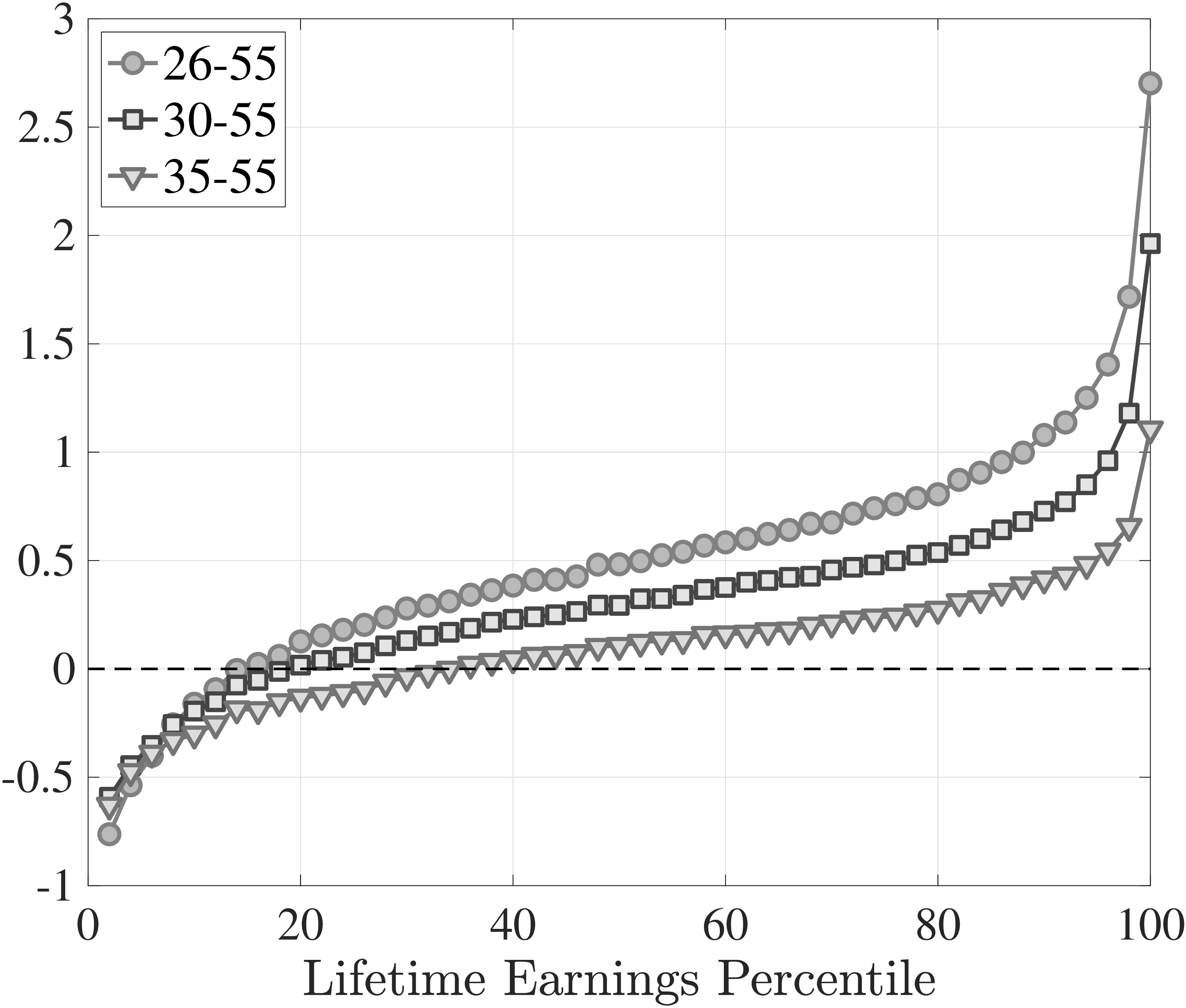

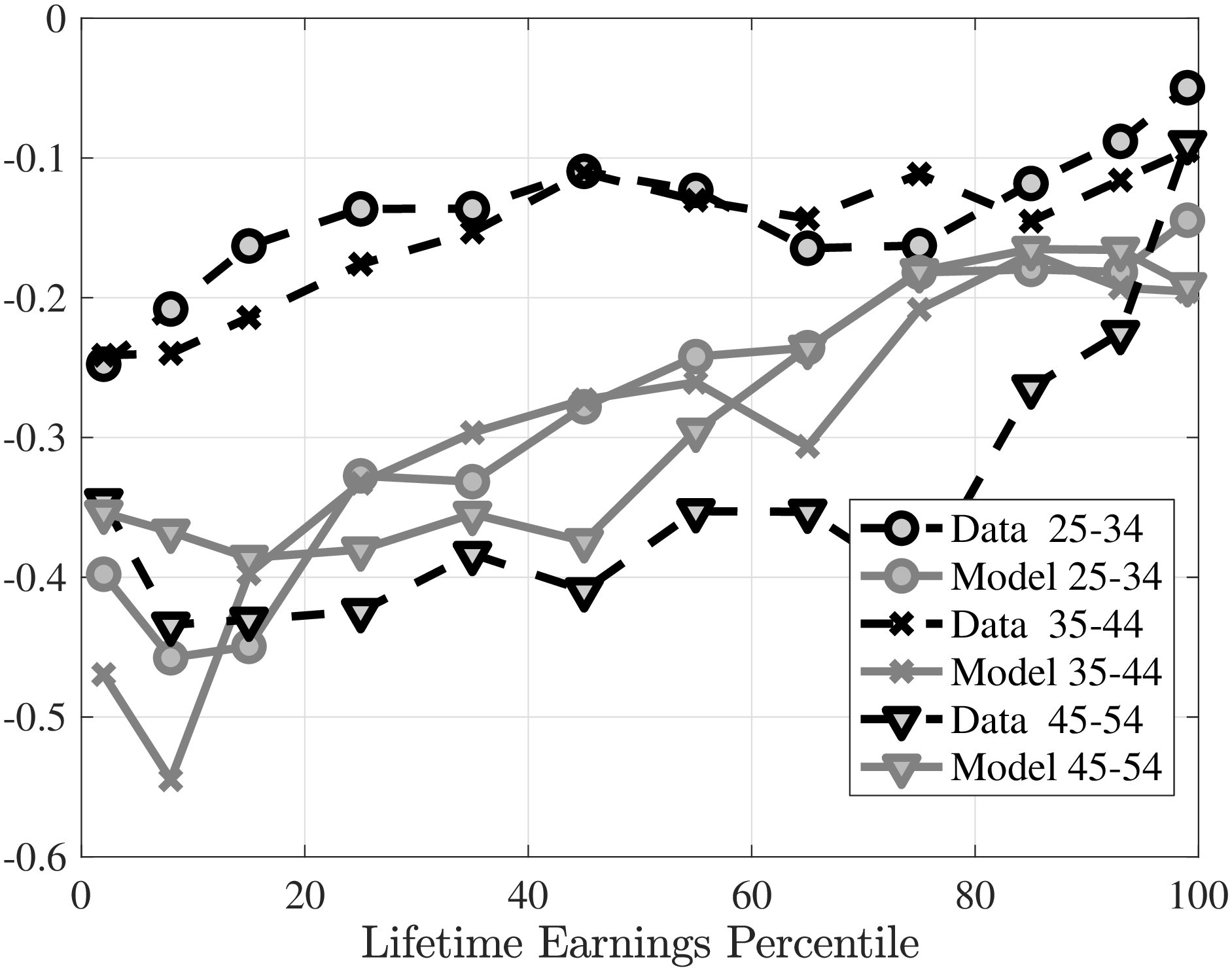

Notes: The left panel shows the average annual earnings over the life cycle by LE group. The right panel shows the log difference of average earnings \(\bar{Y}\) between age 55 and various ages over the LE distribution. For clarity we use one marker for every other LE quantile.

It is well known that in the U.S. differences in earnings growth over the life cycle are key for understanding the inequality in lifetime earnings (see, for example, Huggett et al. (2011) and Kaplan (2012)). To illustrate this point, Figure 1 shows the log growth of average earnings between different ages over the LE distribution; i.e., \(\log \overline{Y}_{h_{2},j}-\log \overline{Y}_{h_{1},j}\), where \(\overline{Y}_{h,j}\) is the average earnings of workers in LE \(j\) at age \(h\) (see Guvenen et al. (2021) for a similar figure from a broader sample). This growth measure allows us to include workers with zero earnings.7 Earnings growth is positively related to the level of lifetime earnings, which is not surprising, since, all else the same, one should expect the higher growth individuals to rank at the top of the distribution. However, the quantitative magnitudes are striking: The top LE earners (\(LE_{50}\)) see their earnings rise by more than 17-fold between the ages of 25 and 55, median workers experience a two-fold increase, whereas those at the bottom see little to no earnings growth (around 16%).8 As we quantify in Section 6, large differences in earnings growth make an unmistakable contribution to the lifetime earnings inequality.

Some of this steep rise in earnings growth at the top could simply be due to transition from school to employment in the labor market. For example, top LE individuals might be pursuing graduate degrees around earlier ages. While the lack of education data does not allow us to answer this question directly, Figure 1b plots earnings growth between the ages of 30 and 55 and 35 and 55 when schooling is unlikely to matter much. While the magnitudes change, we still find a steep profile of earnings growth with respect to LE, suggesting that low labor supply at age 25 is not the major driver of these patterns.

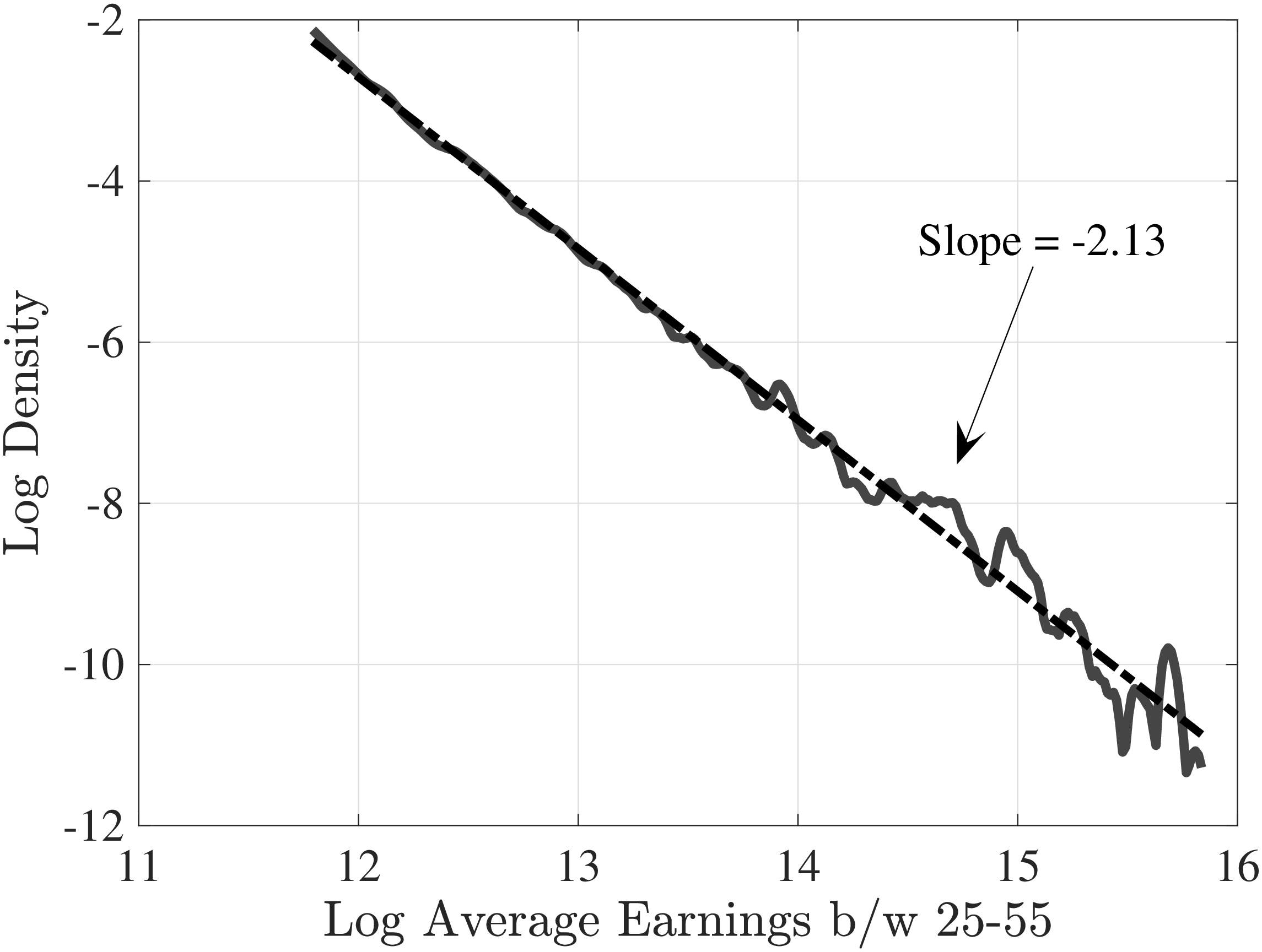

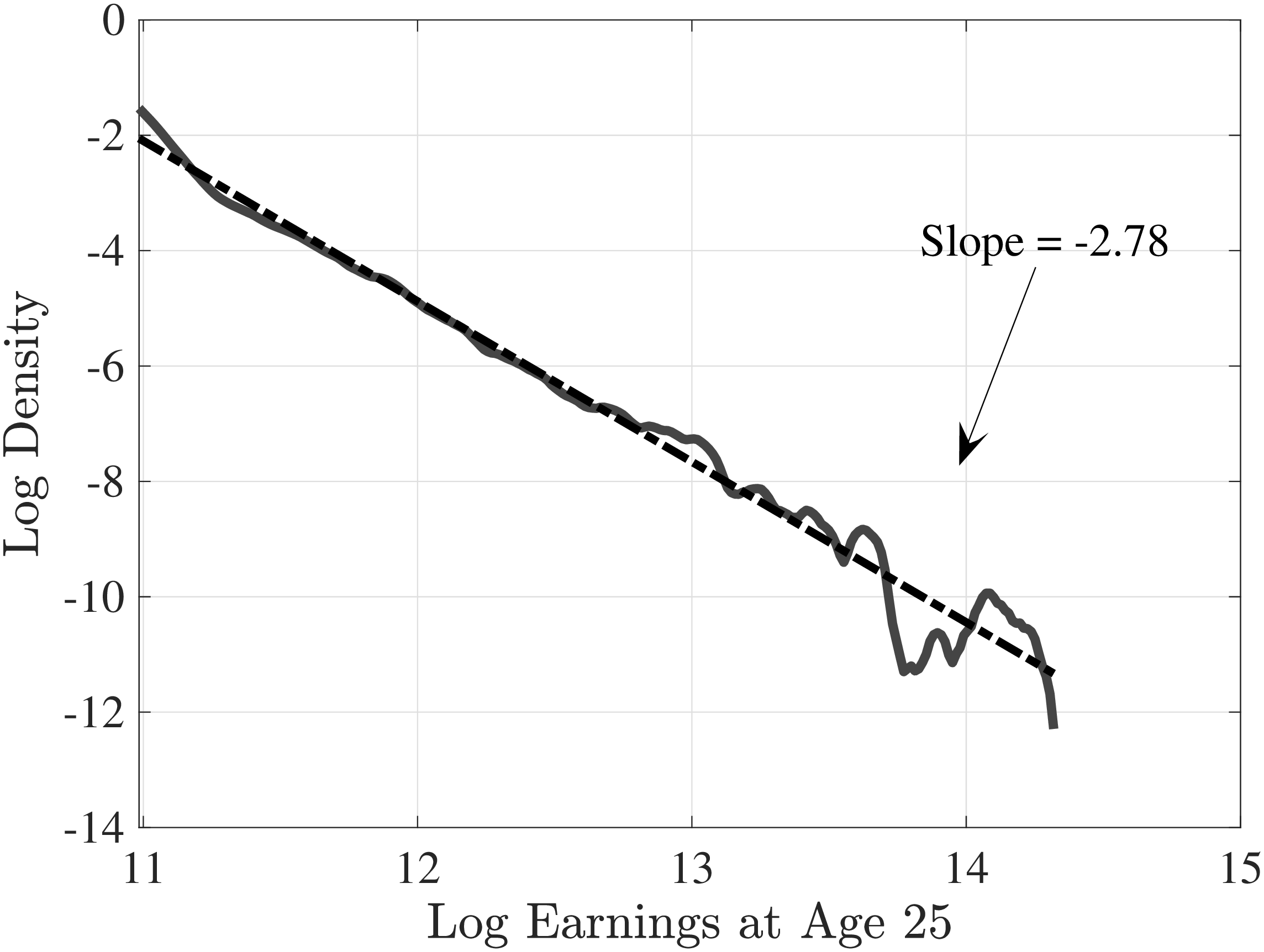

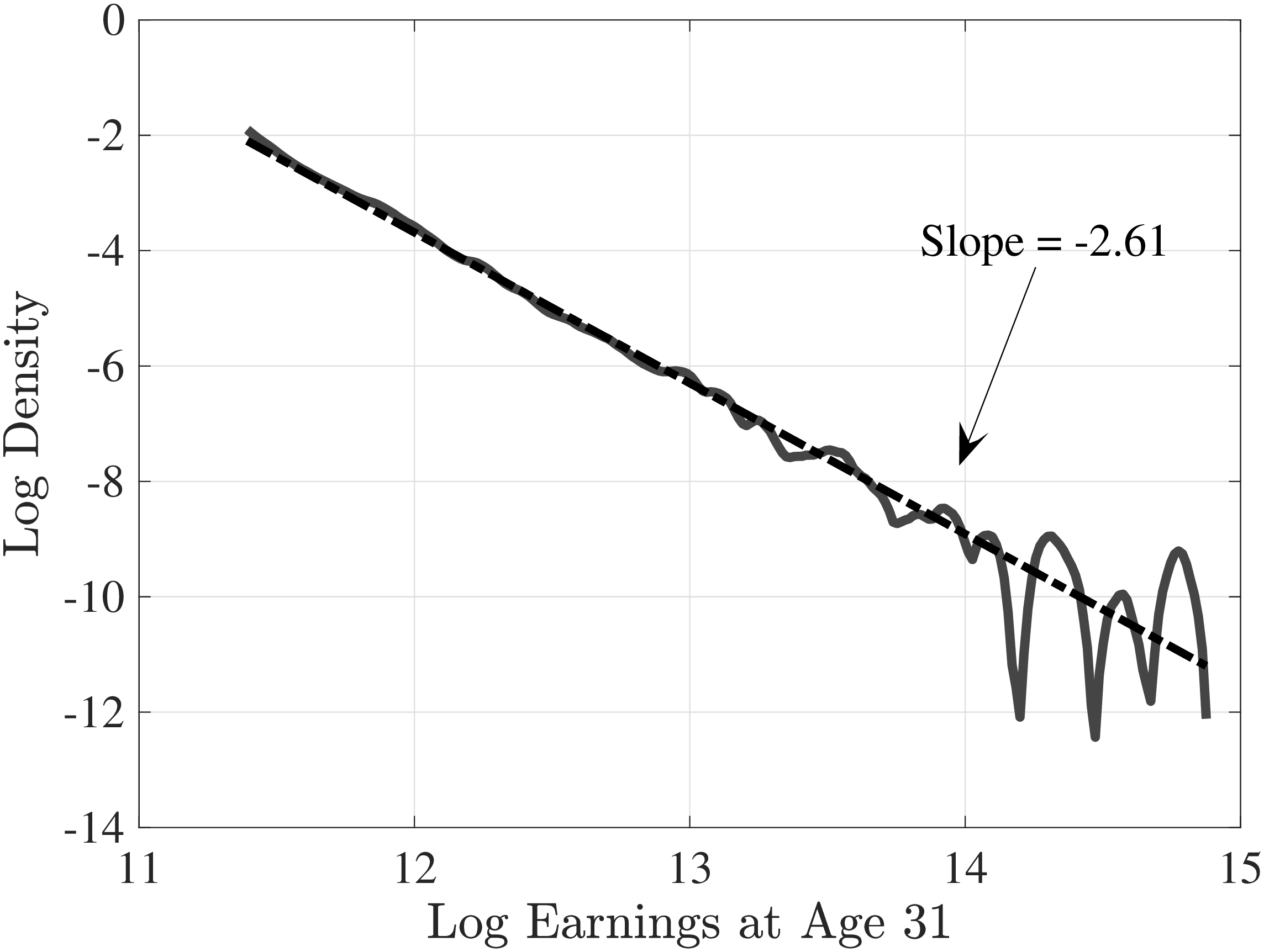

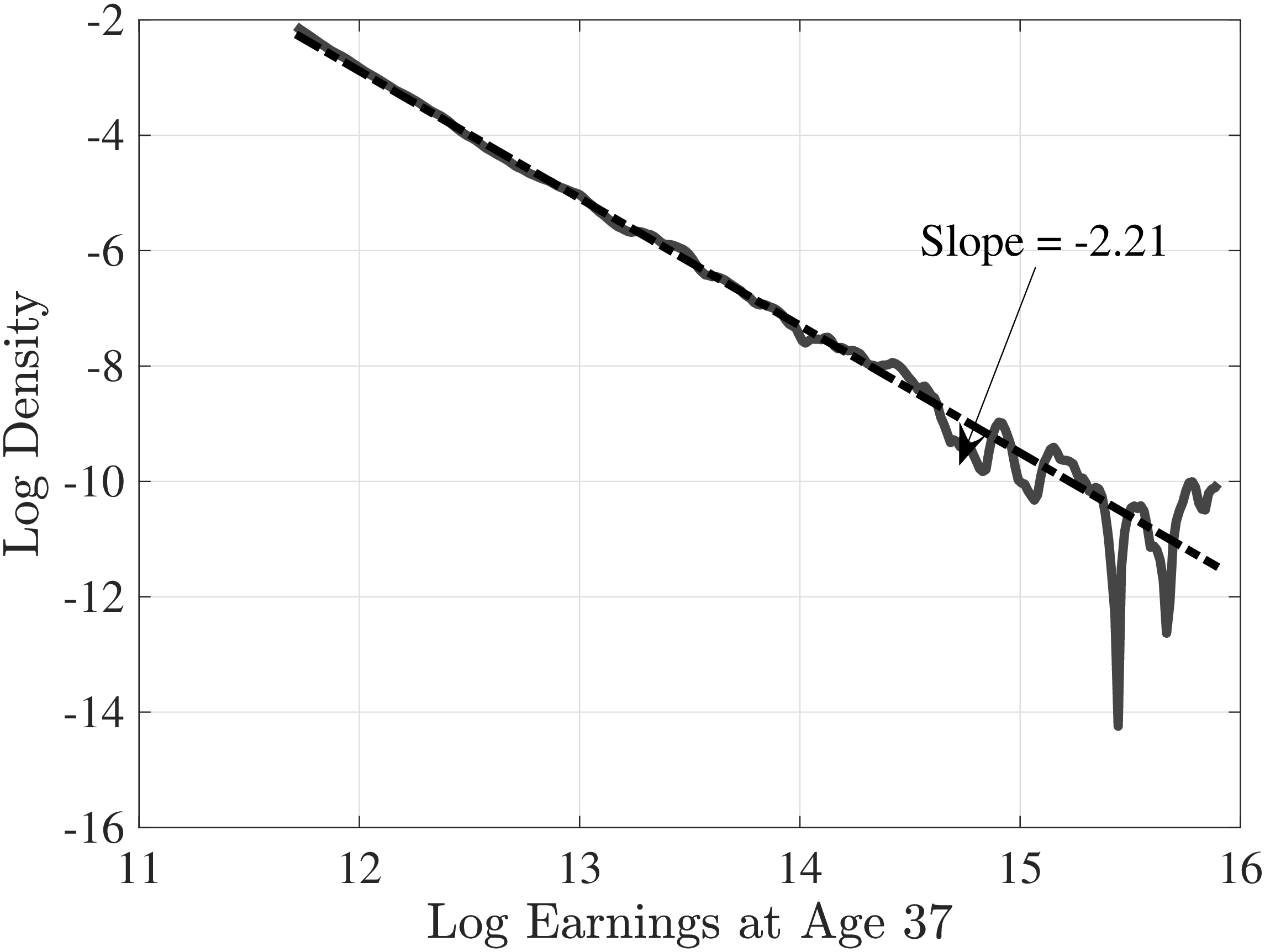

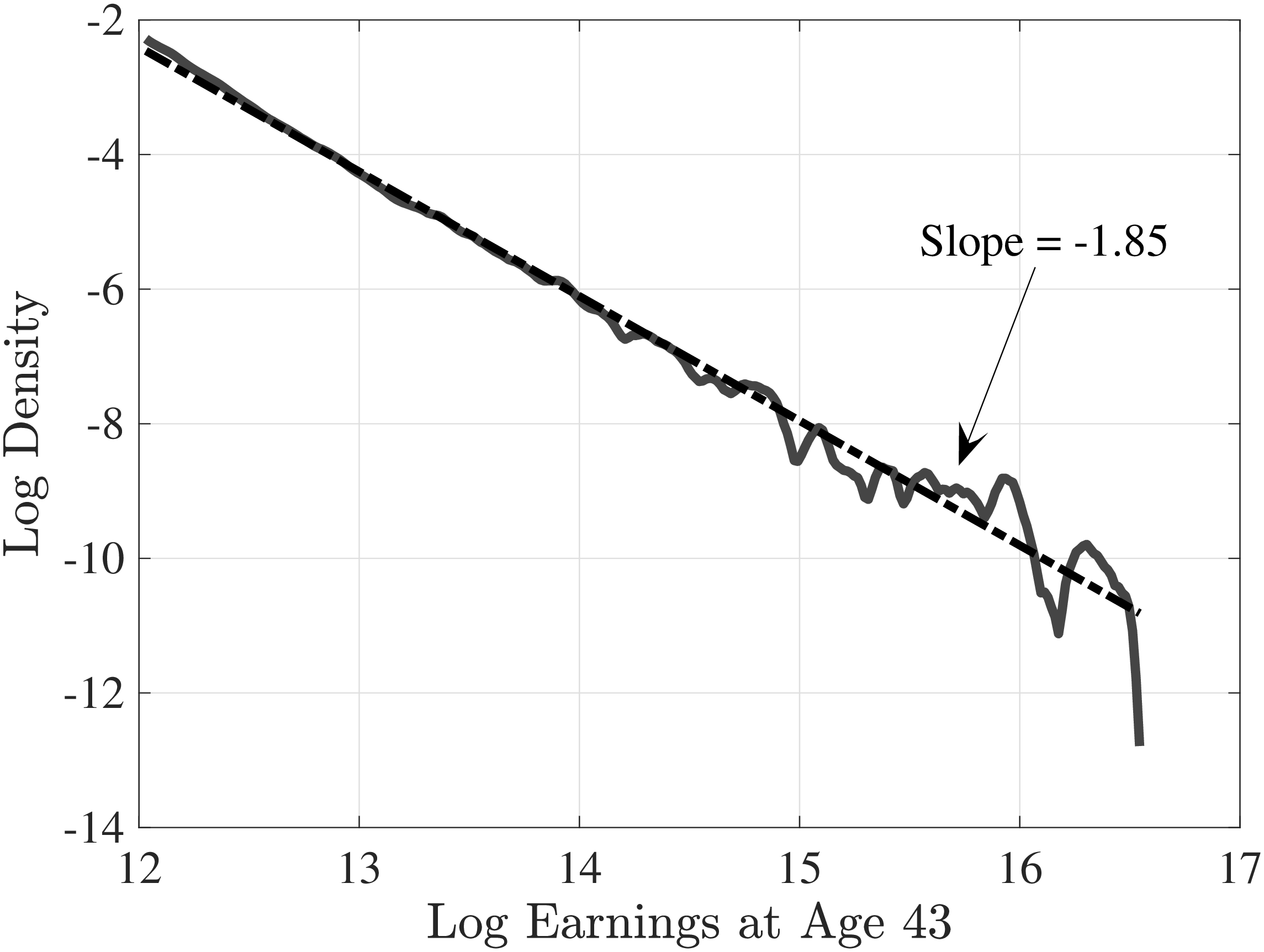

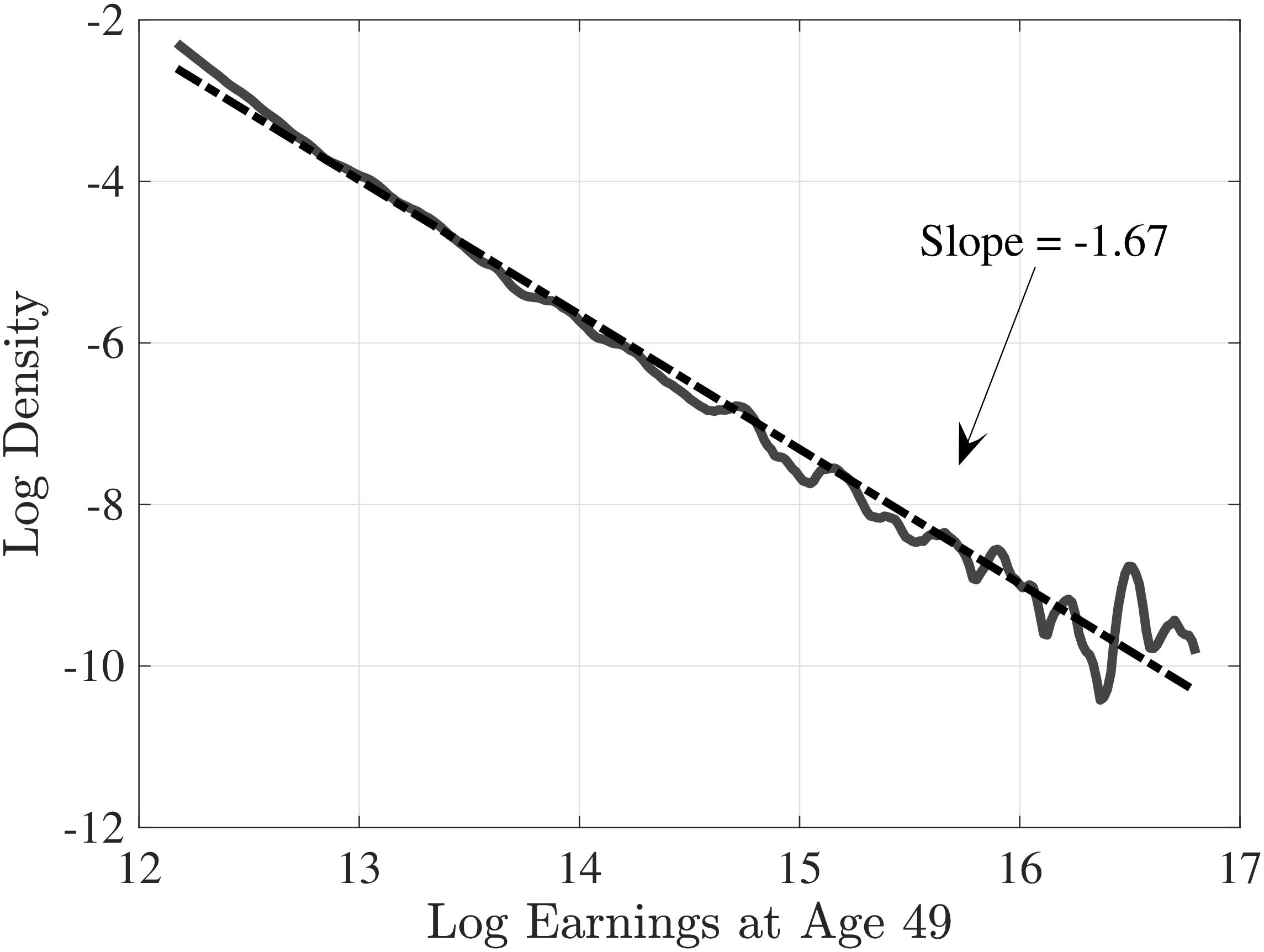

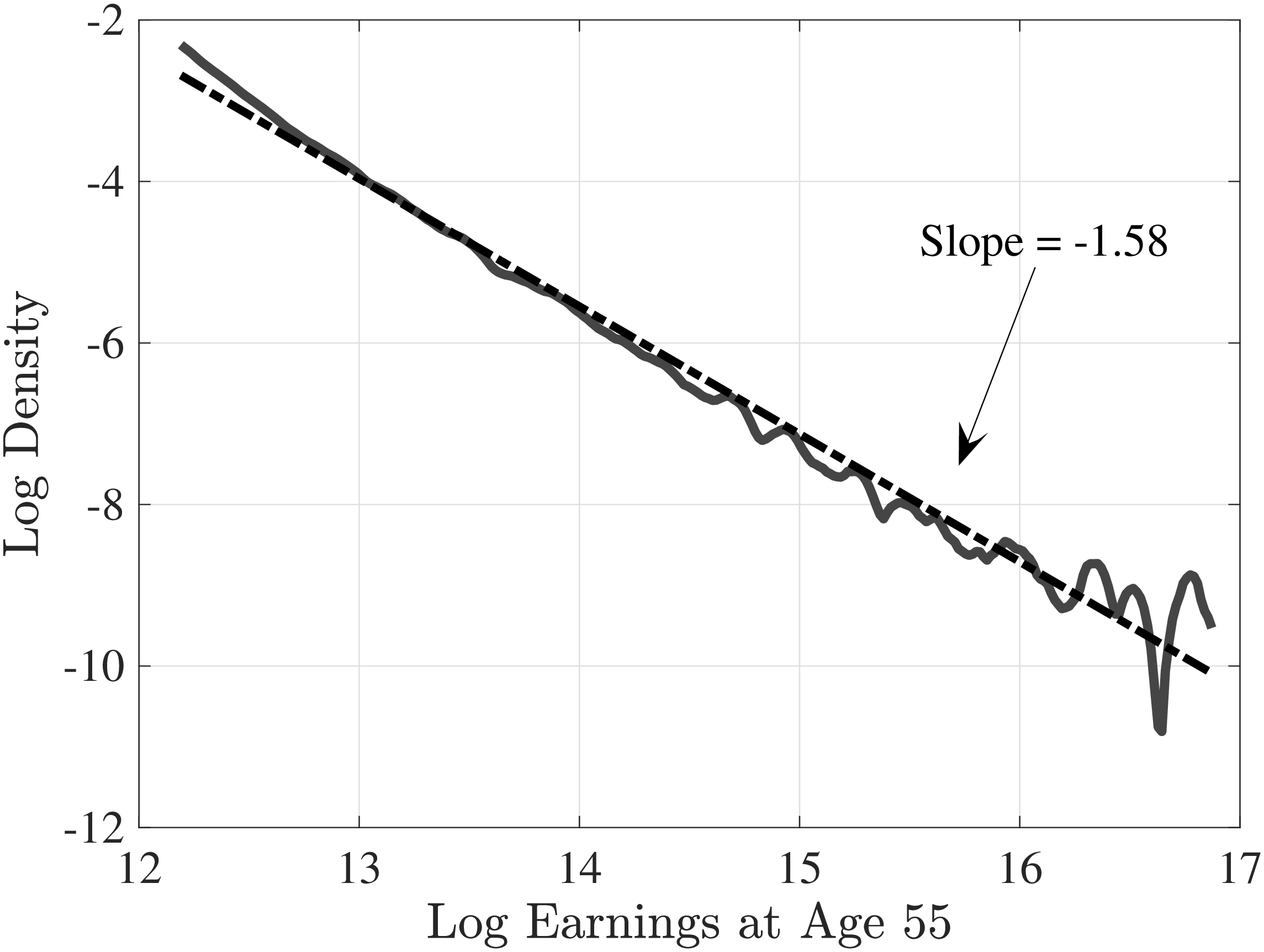

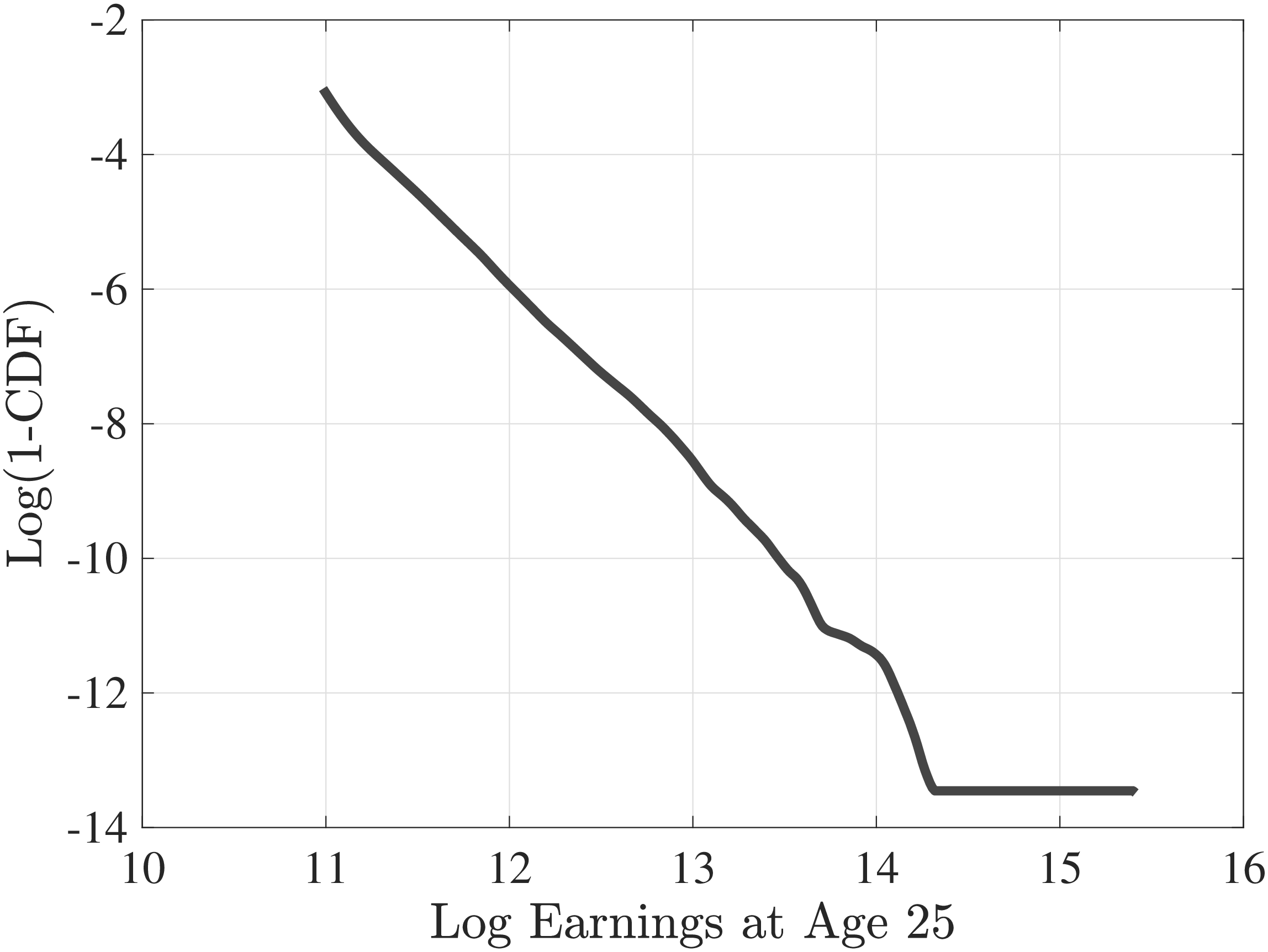

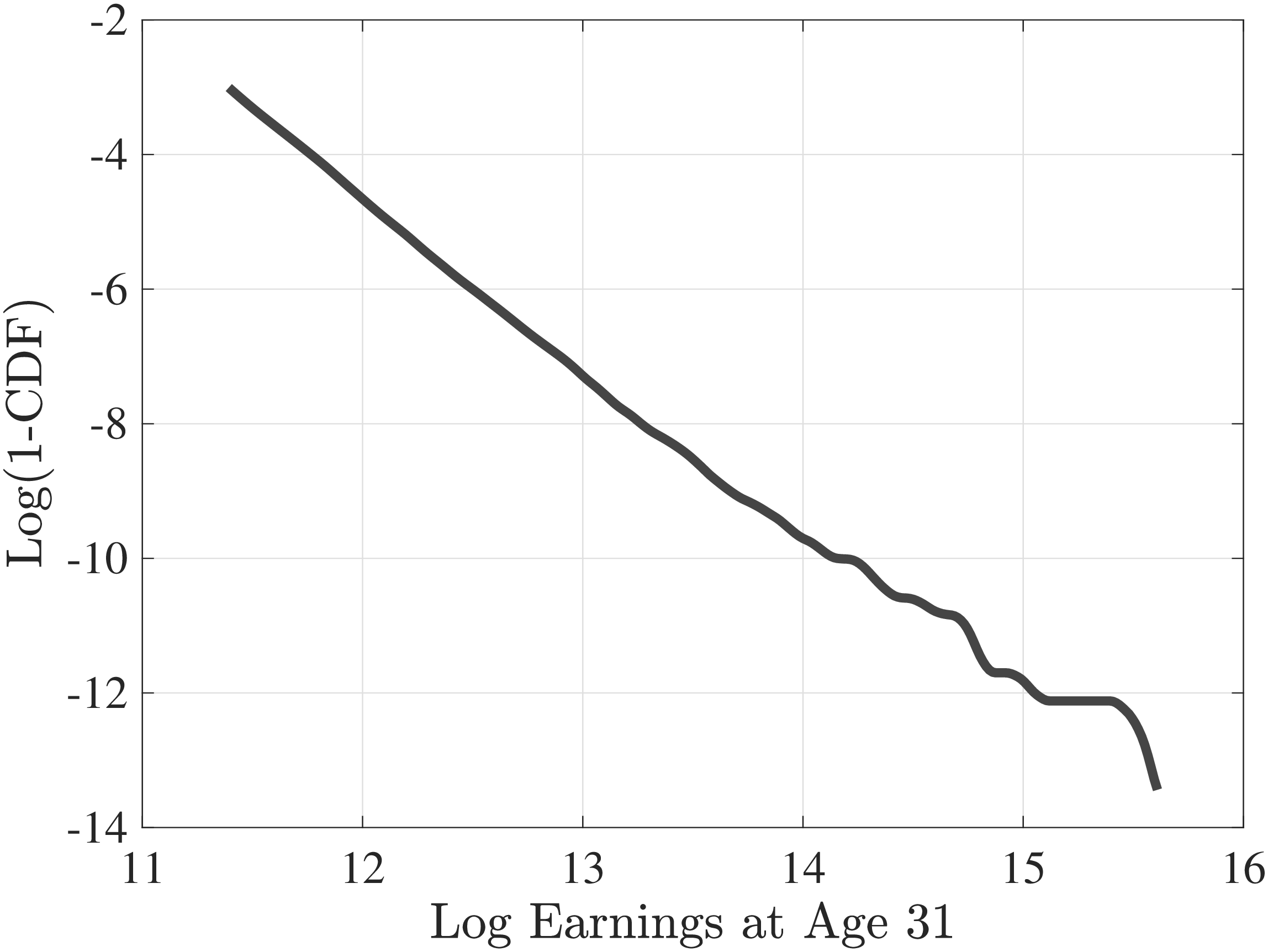

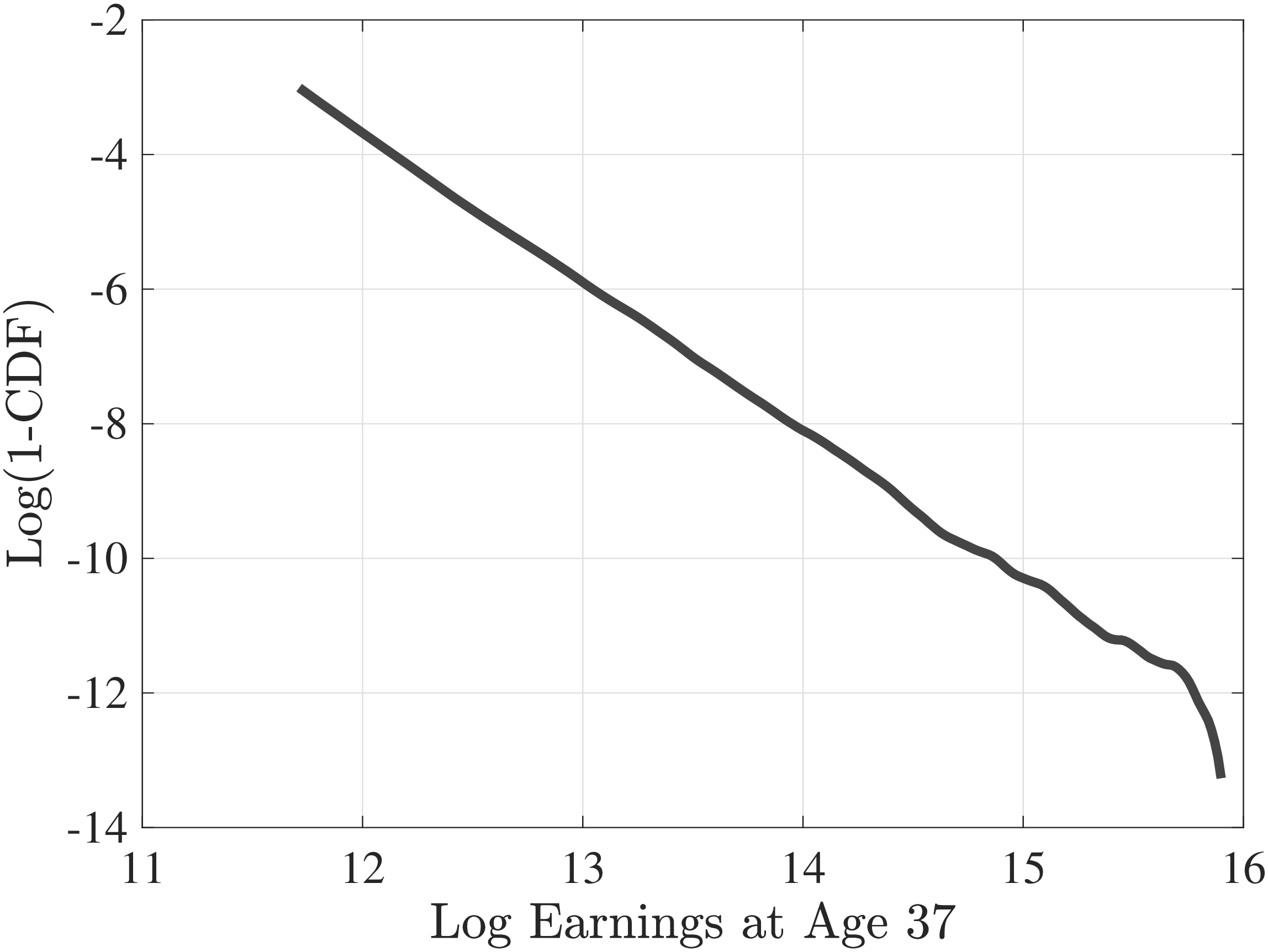

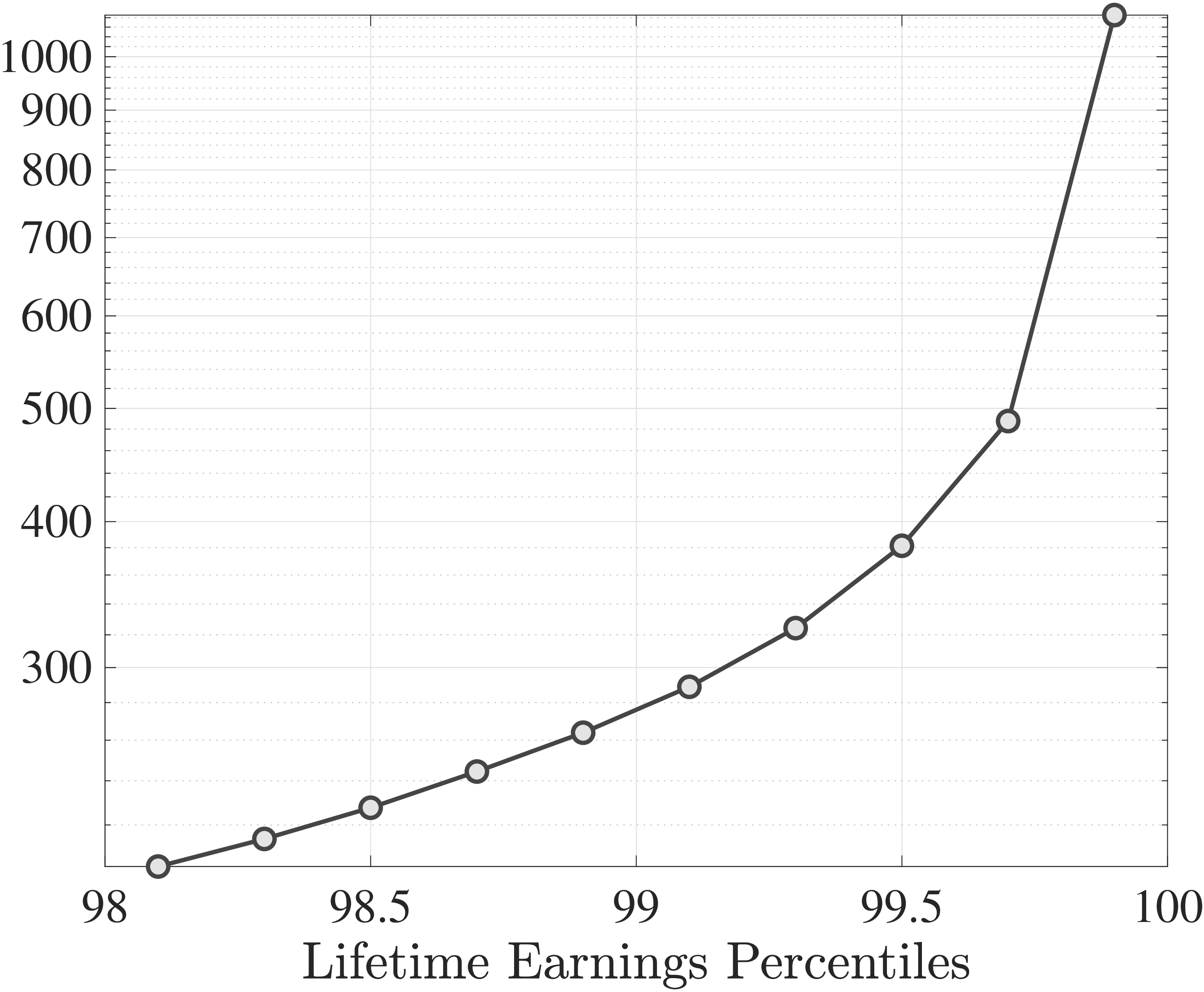

Top Earnings Inequality: A Brief Digression. As we discussed above, inequality is more pronounced at the top of the LE distribution. For example, the average annual earnings in the top 0.2% is over \(\$1,000,000\), compared to \(\$200,000\) for those around the 98th percentile. In fact, the right tail of the LE distribution follows a power law (Table A.2) with a a Pareto tail slope of –2.13 (Figure A.1). It is also already established that the population earnings distribution has Pareto tails (Piketty and Saez 2003; Atkinson et al. 2011). Importantly and interestingly, we find that this power law also holds in the cross-sectional distribution of earnings at each age (see Appendix A.2.1). Log density is linear in the tails at all ages and the slope gets closer to 1 in absolute value, which points to rising income concentration over the life cycle (Figures A.3 and A.4).

2.3 Career paths by lifetime earnings

A natural immediate question is: What accounts for the large differences in earnings growth? To this end, we investigate the differences in labor market experiences between LE groups. Earlier work has shown that job mobility is important for earnings growth over the life cycle (Topel and Ward (1992)). Therefore, we start by investigating how the number of (distinct) employers over the working life differs between LE groups.

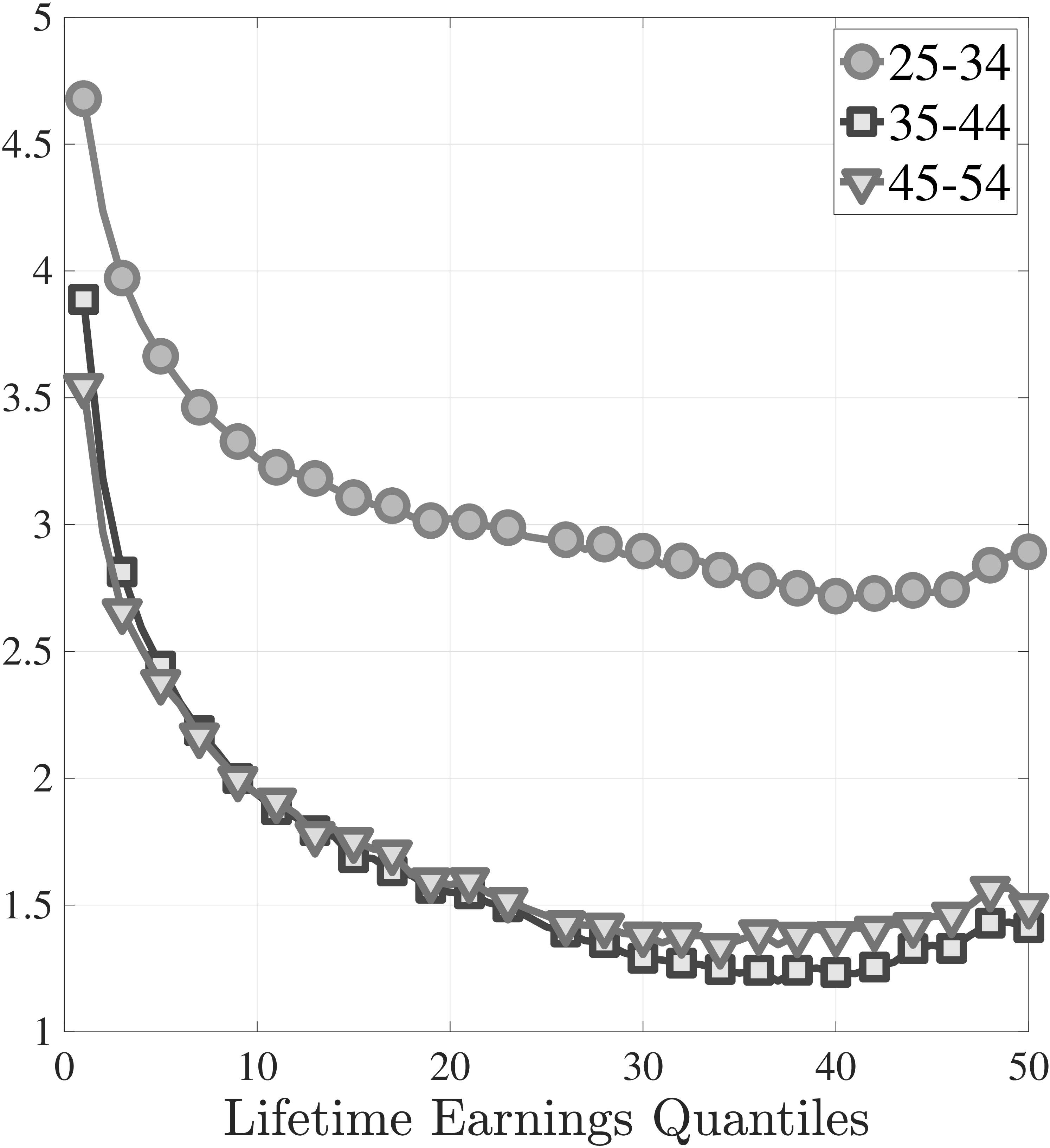

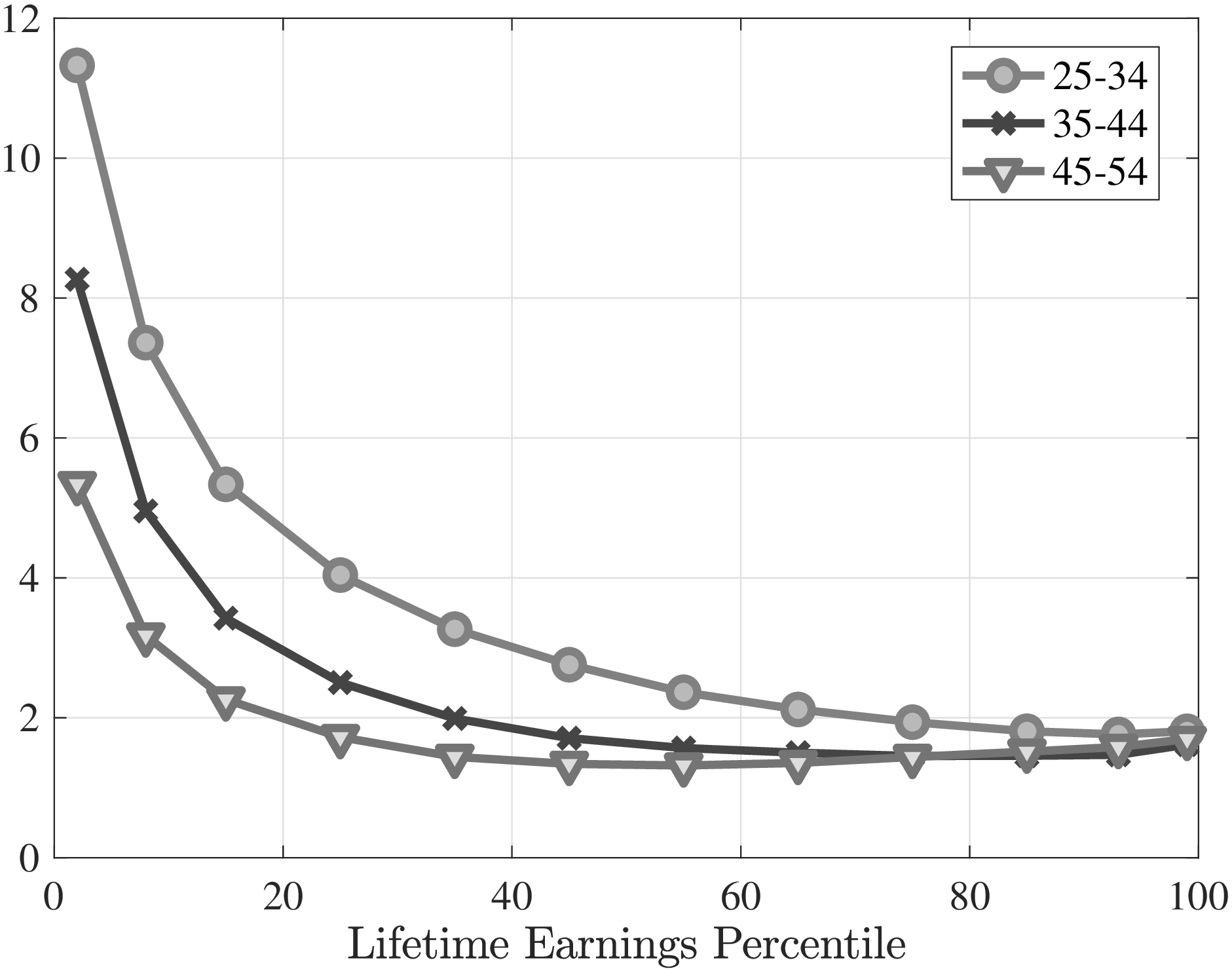

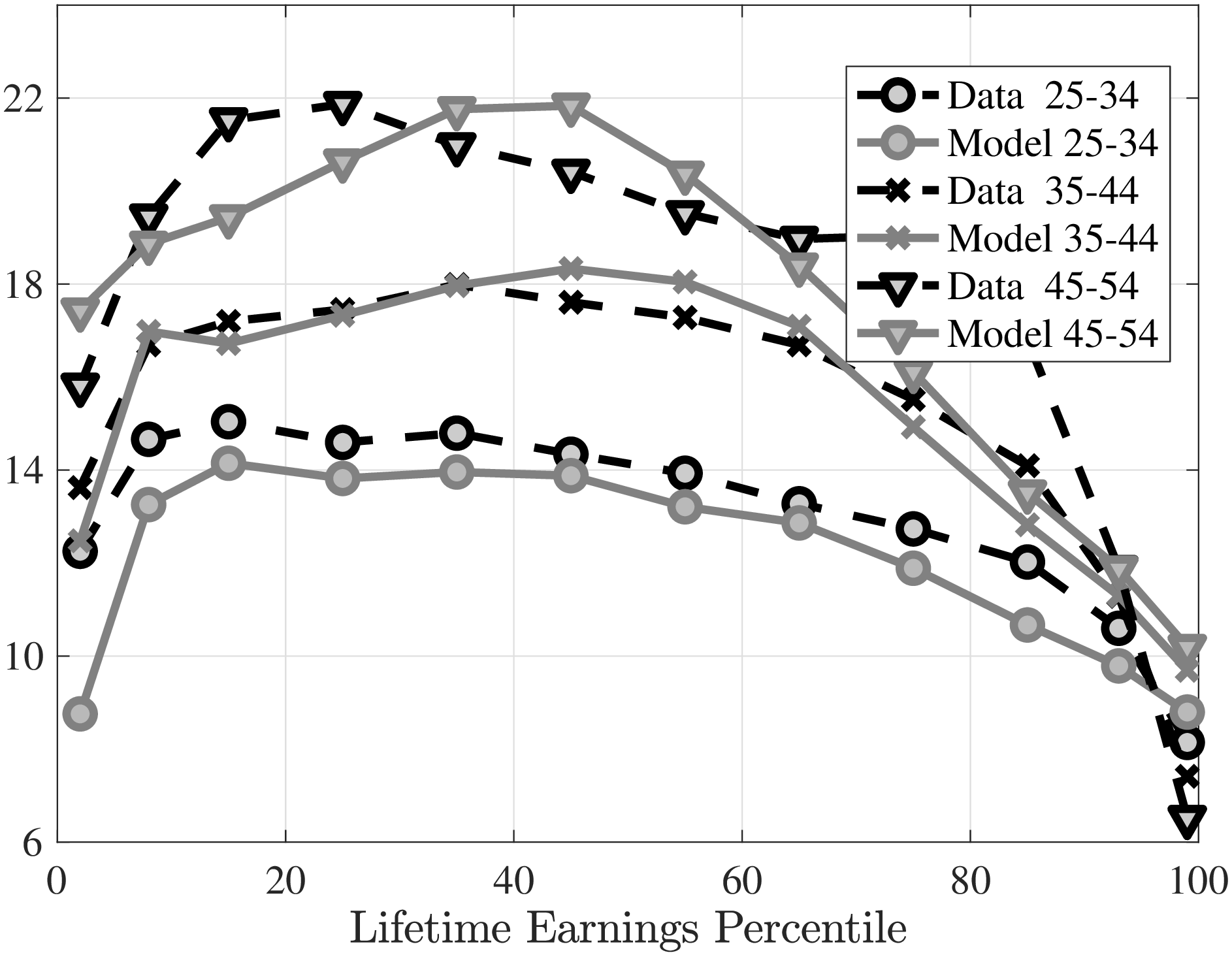

Individuals at the bottom of the LE distribution work for almost 5 different employers on average between ages 25 and 34, whereas the number of unique employers drops sharply to around 3 in the upper half of the LE distribution (Figure 2a). As workers age, job switching declines throughout the LE distribution but much more so in the upper half. While top workers work for around 1.5 different employers per decade after age 35, bottom workers still end up working for 3.5 employers on average, not much lower than the number of employers before age 35. At first glance, one might think that low LE individuals switch jobs very often and experience large earnings growth as a result. As we will see next, the nature of switches is very different across the LE groups.

We now document the average earnings growth across LE groups for workers who stay with the same employer and for those who change jobs. Given the annual frequency of the data, it is possible for job switchers to have more than one W-2 in a given year. Moreover, some workers may hold multiple jobs concurrently. These issues pose a challenge for a precise classification of job stayers and switchers. There is more than one plausible definition for a job stayer, and we opt for a conservative one. Specifically, we call a worker a job stayer between years \(t\) and \(t+1\) if i) he has income from the same employer in years \(t-1\), \(t\), \(t+1\), and \(t+2\); ii) his income in years \(t\) and \(t+1\) is above the minimum income threshold for that year; and iii) this employer accounts for at least 90% of his total labor income in years \(t\) and \(t+1\).9 This definition ensures that the main employer was the same firm in years \(t\) and \(t+1\). We label all other workers as job switchers. Note that according to this definition, switchers are a very heterogeneous group and consist of people who make direct job-to-job transitions, those who experience nonemployment, and those who come out of nonemployment. We return to this heterogeneity later.

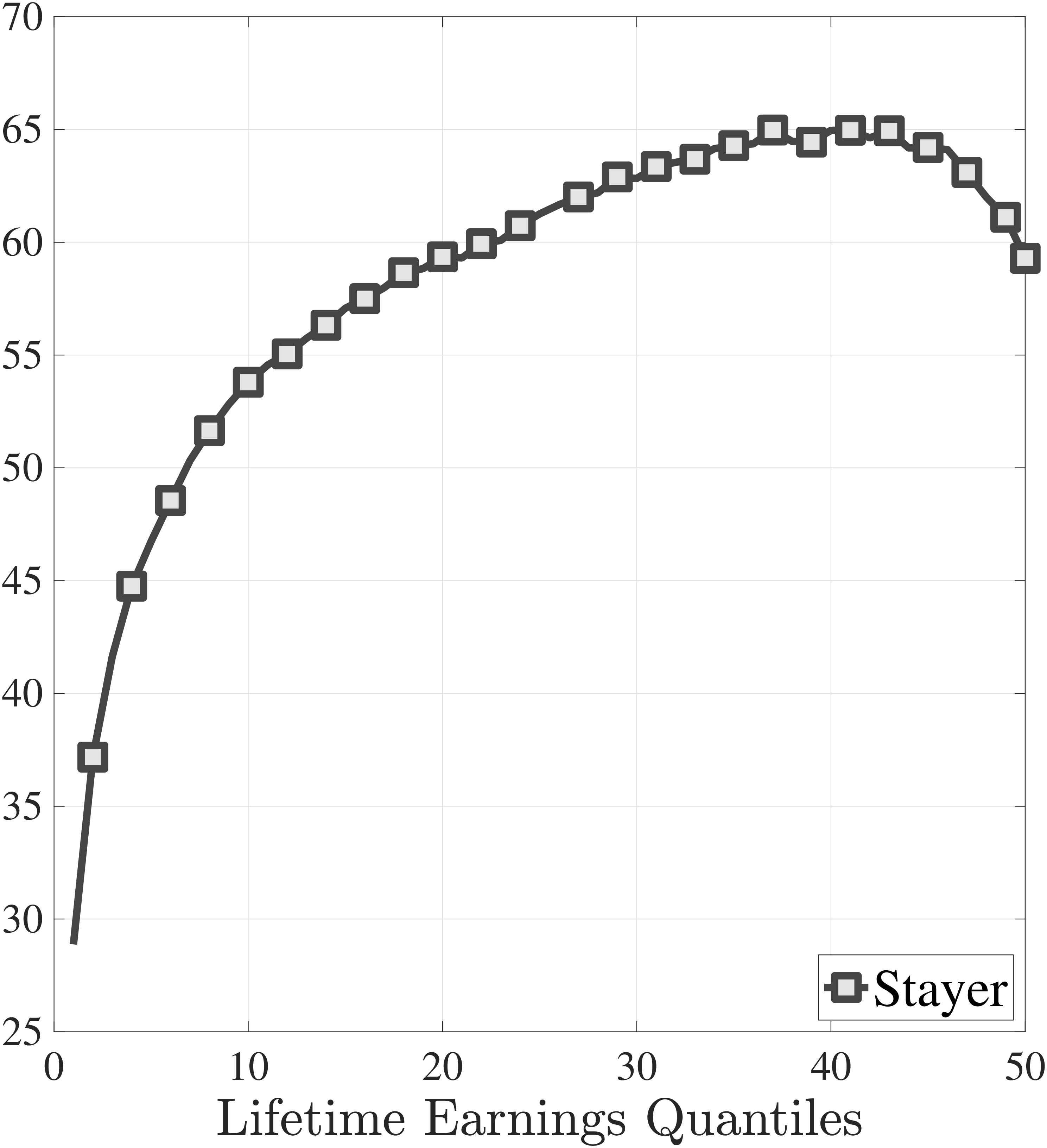

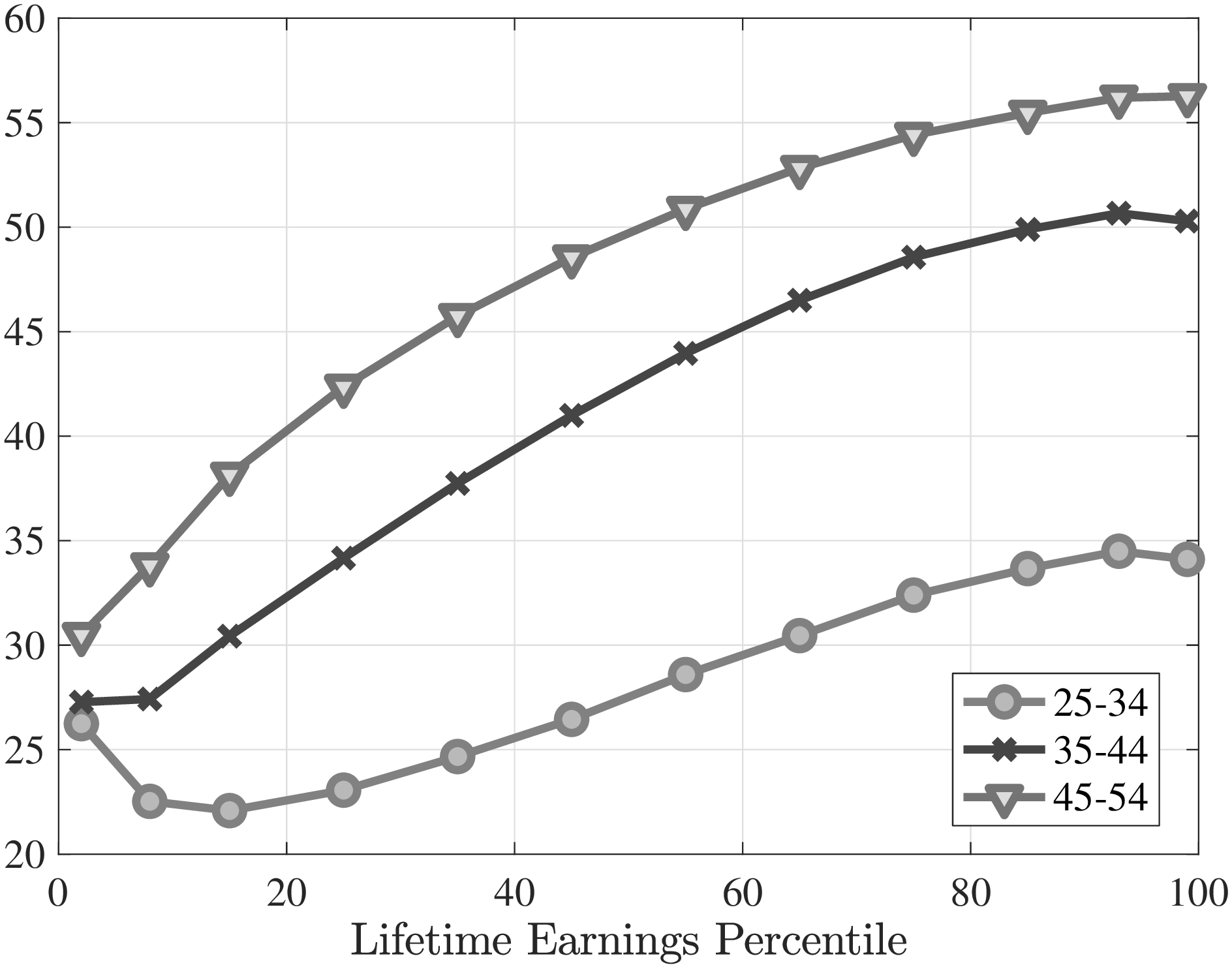

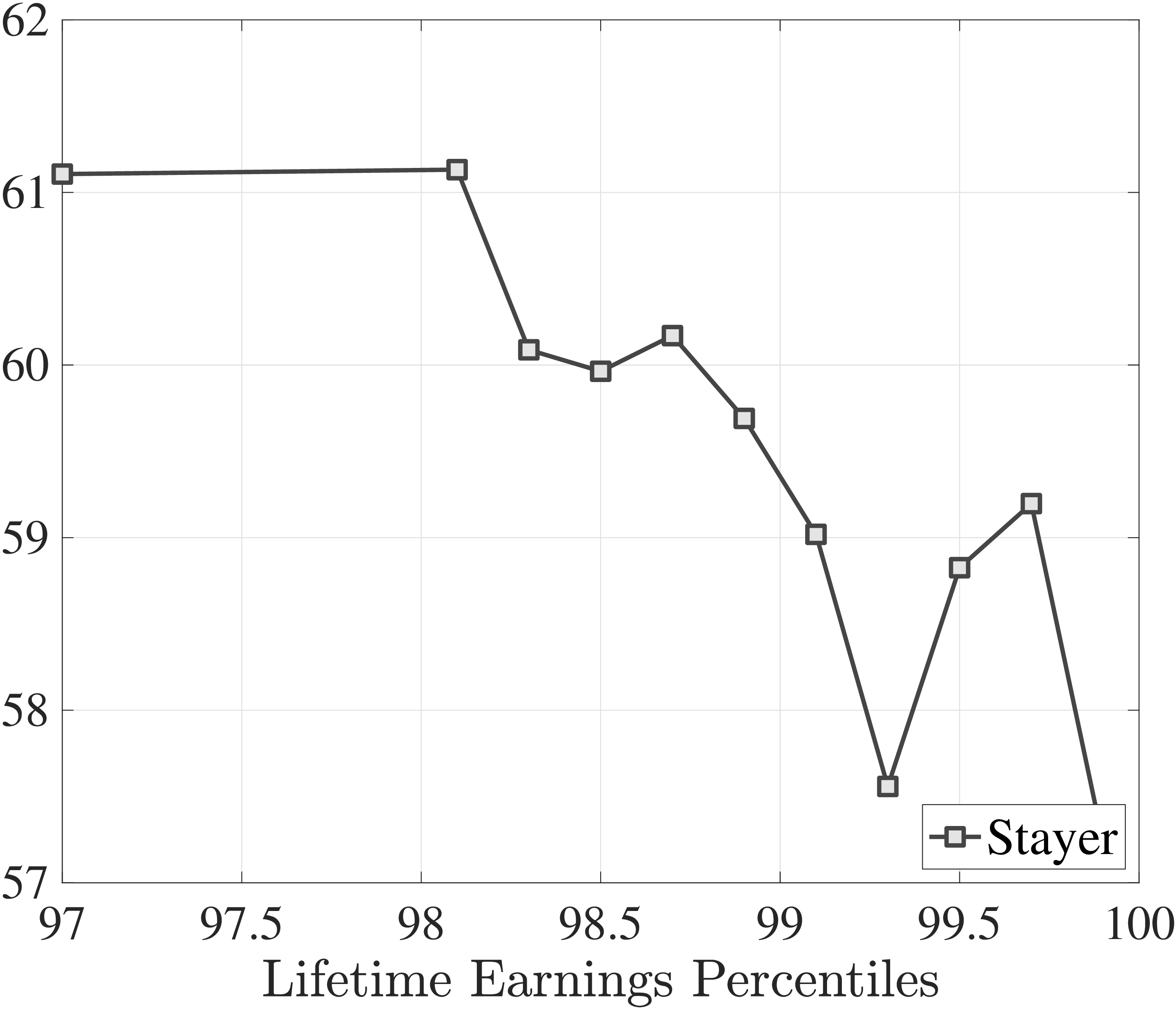

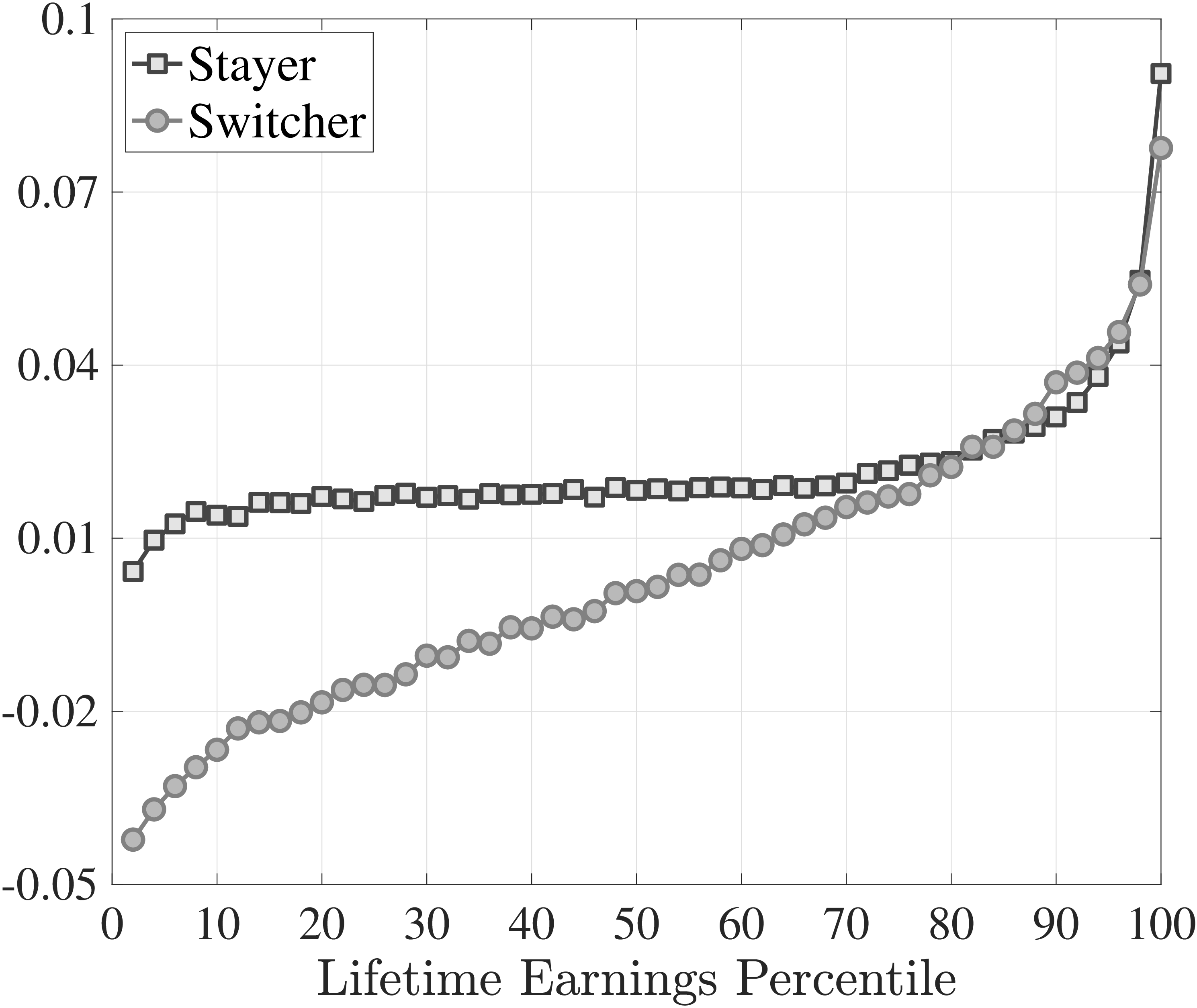

Notes: The left panel shows the number of distinct employers employers over the working life by LE. The middle panel shows the fraction of workers in each LE group who are job stayers according to our definition, calculated for each age and averaged over the working life. The right panel plots the log growth of average earnings \(\bar{Y}\) between \(t\) and \(t+1\) for job stayers and switchers separately by LE, again, averaged over \(t\) over the working life.

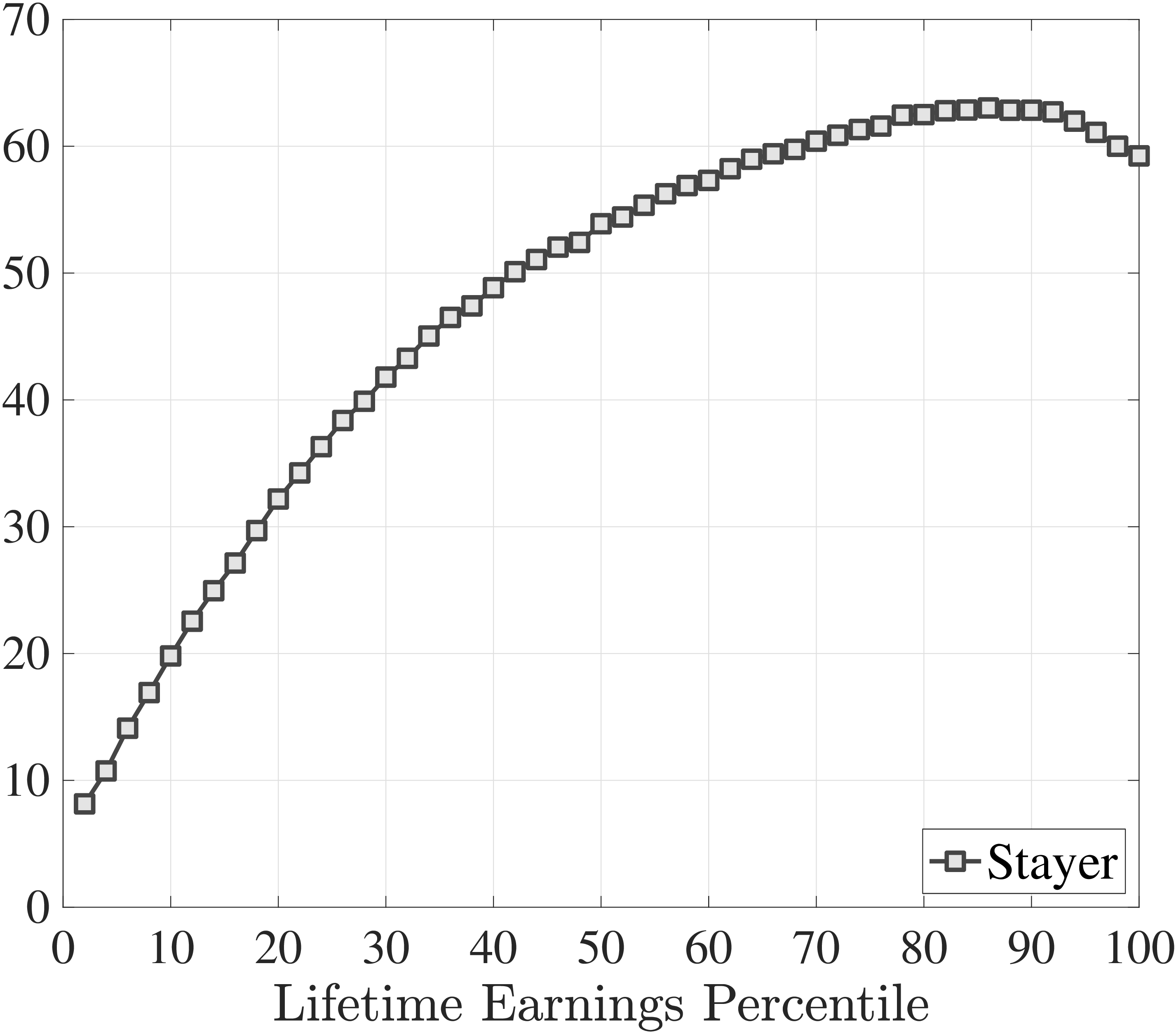

The middle panel of Figure 2 shows the fraction of job stayers within each LE group, averaged over the working life. Resonating with the large differences in the number of different jobs hold over the life cycle, bottom LE individuals stay with the same firm on average for 30% of their working life, compared to around 60% above the median.10

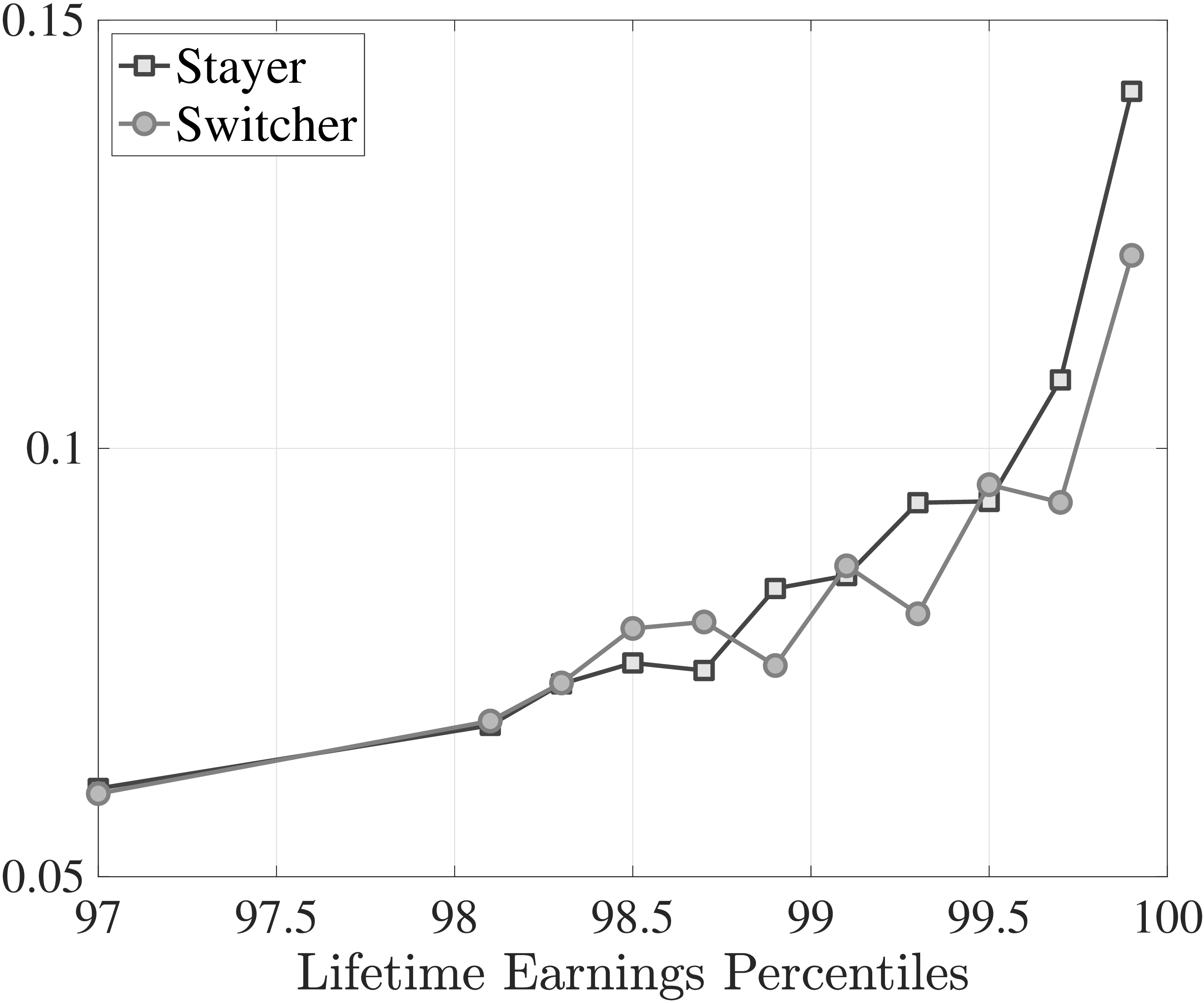

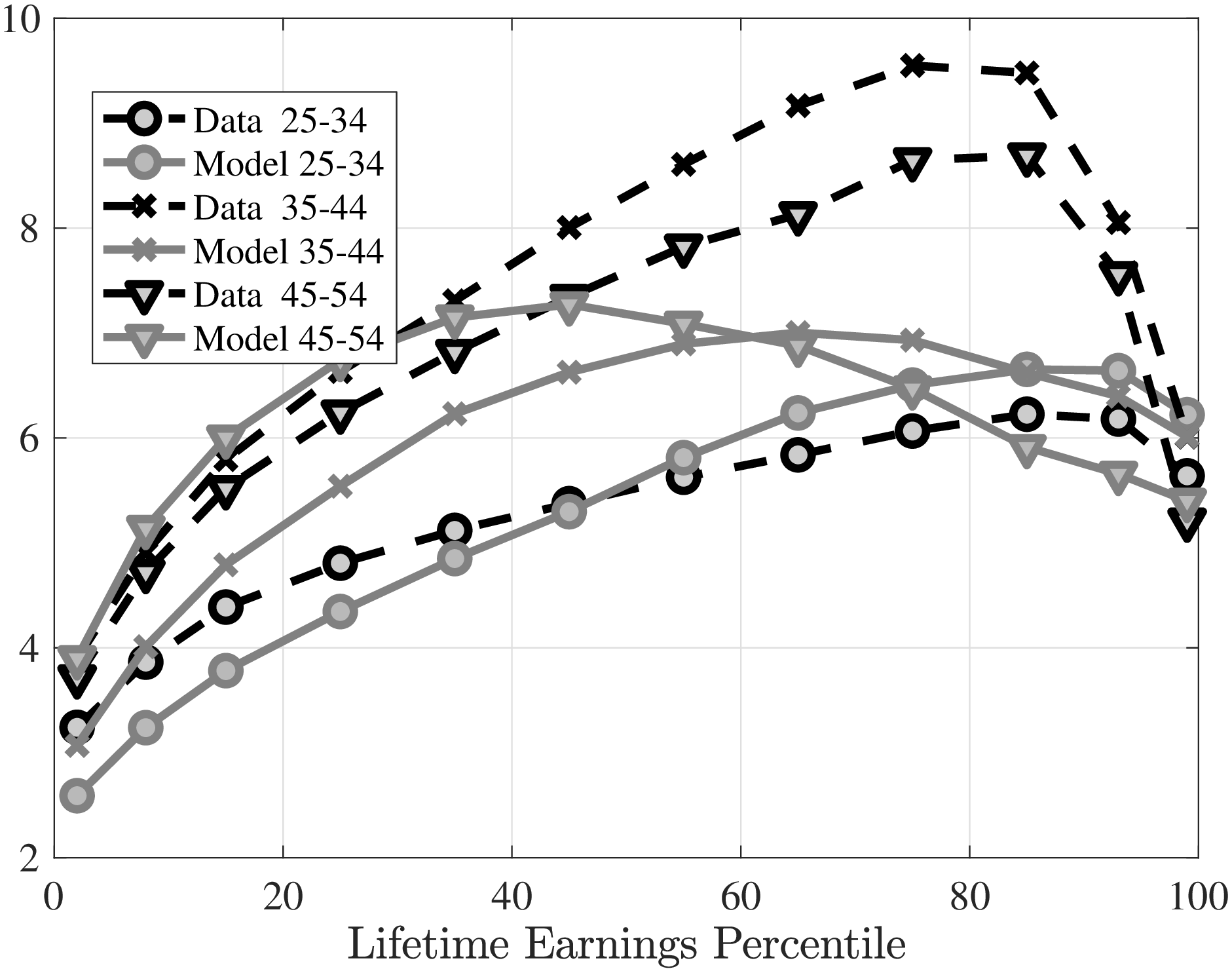

How much of an earnings growth does a worker experience when he stays with the same employer versus when he switches jobs? The answer differs widely across the LE distribution (Figure 2c). For job stayers log average earnings growth (between \(t\) and \(t+1\)) is surprisingly similar at around 2% in the bottom two thirds of the LE distribution. Whereas, average earnings growth for stayers increases sharply in the top LE tercile, reaching around 10% for \(LE_{50}\). Turning to job switchers, we find that average annual earnings growth is essentially zero at the bottom of the LE distribution and rises almost linearly to around 4% for \(LE_{45}\), after which it accelerates to 10% for the top LE individuals. This large heterogeneity indicates that the nature of job switches is very different throughout the LE distribution, which we will investigate shortly.11

These differences in earnings growth between job stayers and switchers are key for understanding the different forces behind the lifetime earnings growth over the LE distribution. For example, given the little heterogeneity among job stayers below the median LE, it is clear that the differences in lifetime earnings growth are due to the differences in the frequency and nature of job switches among these workers, suggesting large heterogeneity in job ladder risk for them. Whereas workers above the median LE are much more likely to stay with the same employer, therefore, large differences in earnings growth of job stayers should be the main culprit behind the lifetime earnings growth differences among them, suggesting large heterogeneity in returns to experience. Of course, wage growth of job stayers may also be determined by outside offers they do not accept or returns to experience is still a factor for earnings changes of job switchers. Thus, the exact decomposition of the importance of different economic forces requires a structural model estimated to match these salient features of the data (Section 3).

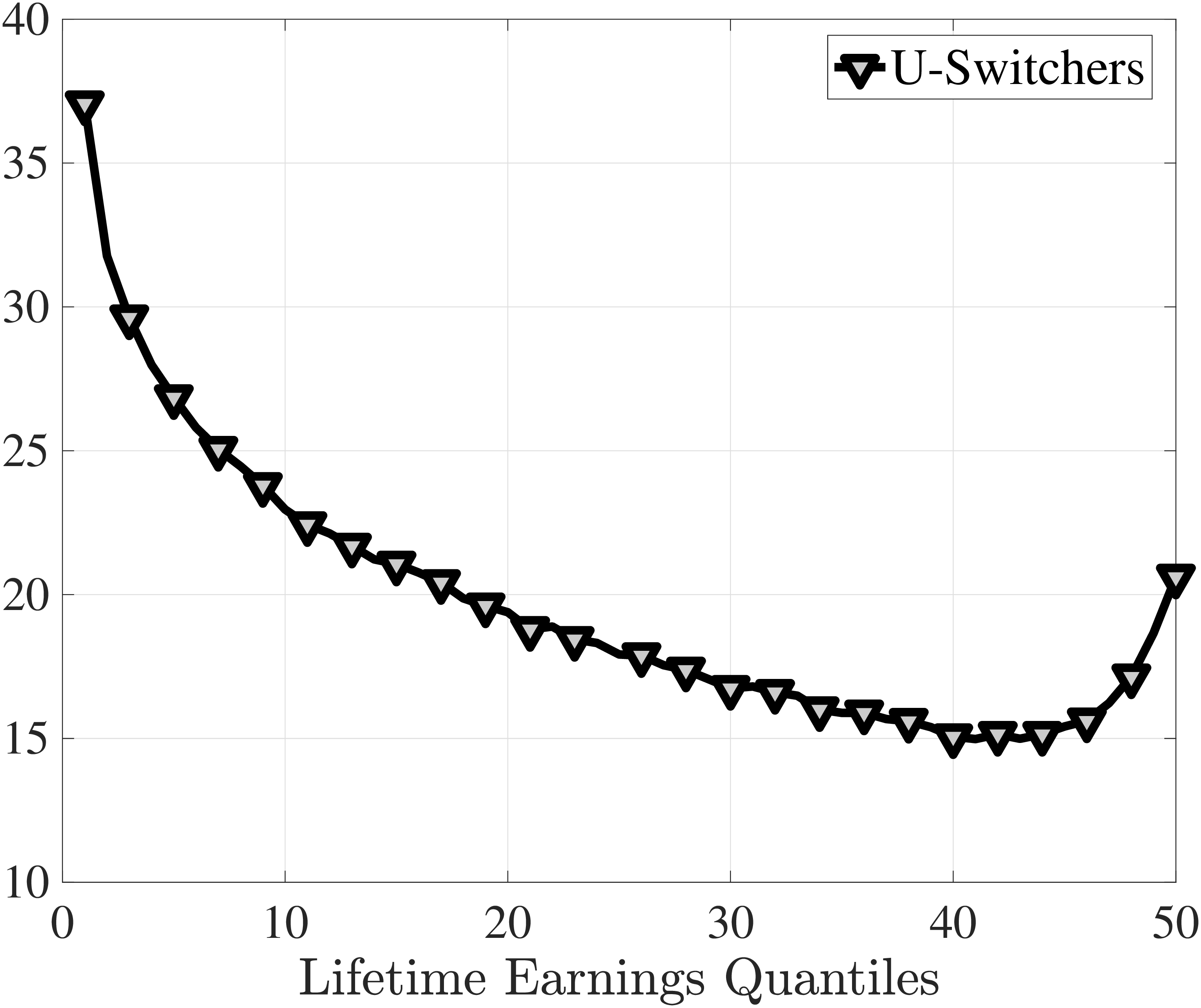

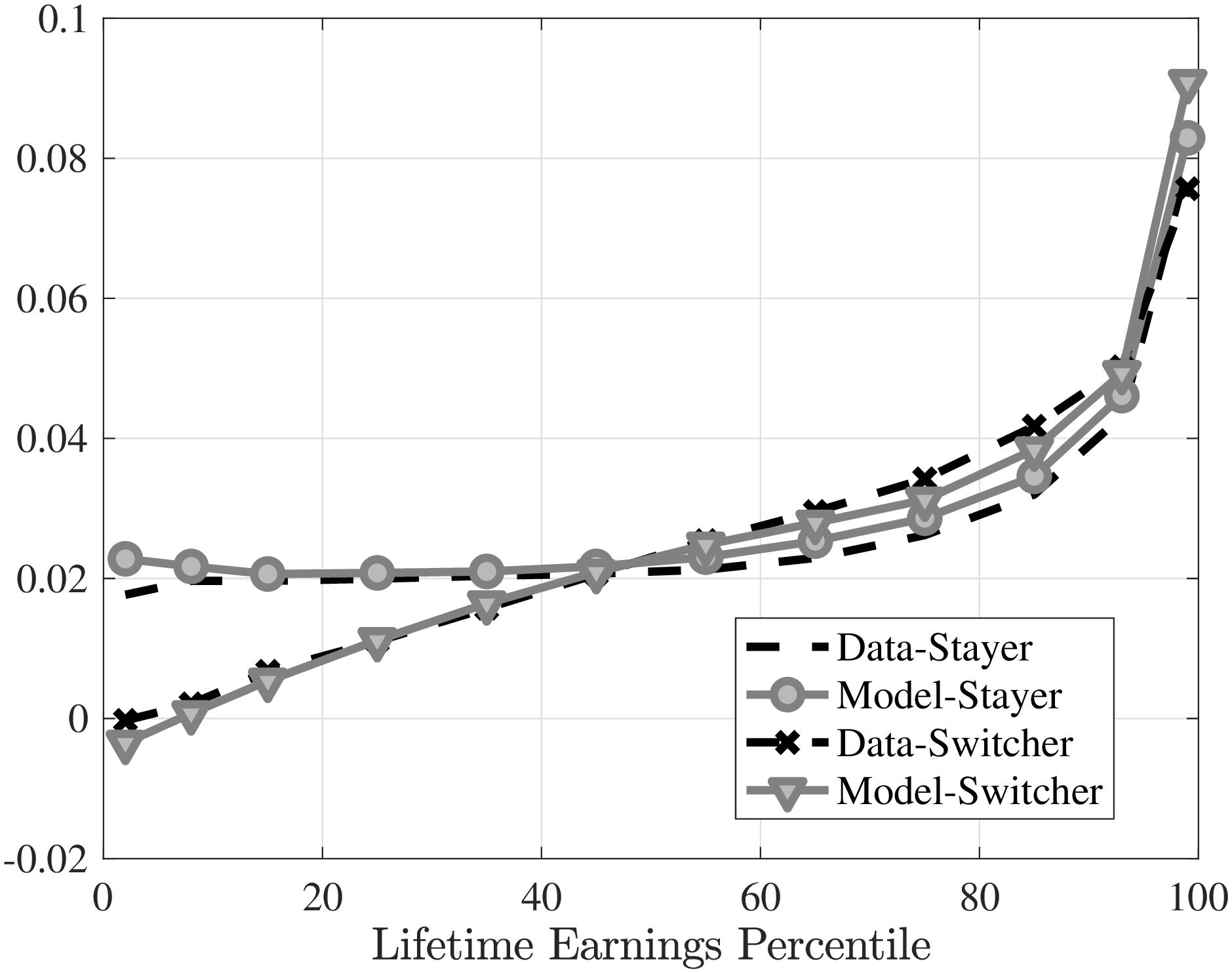

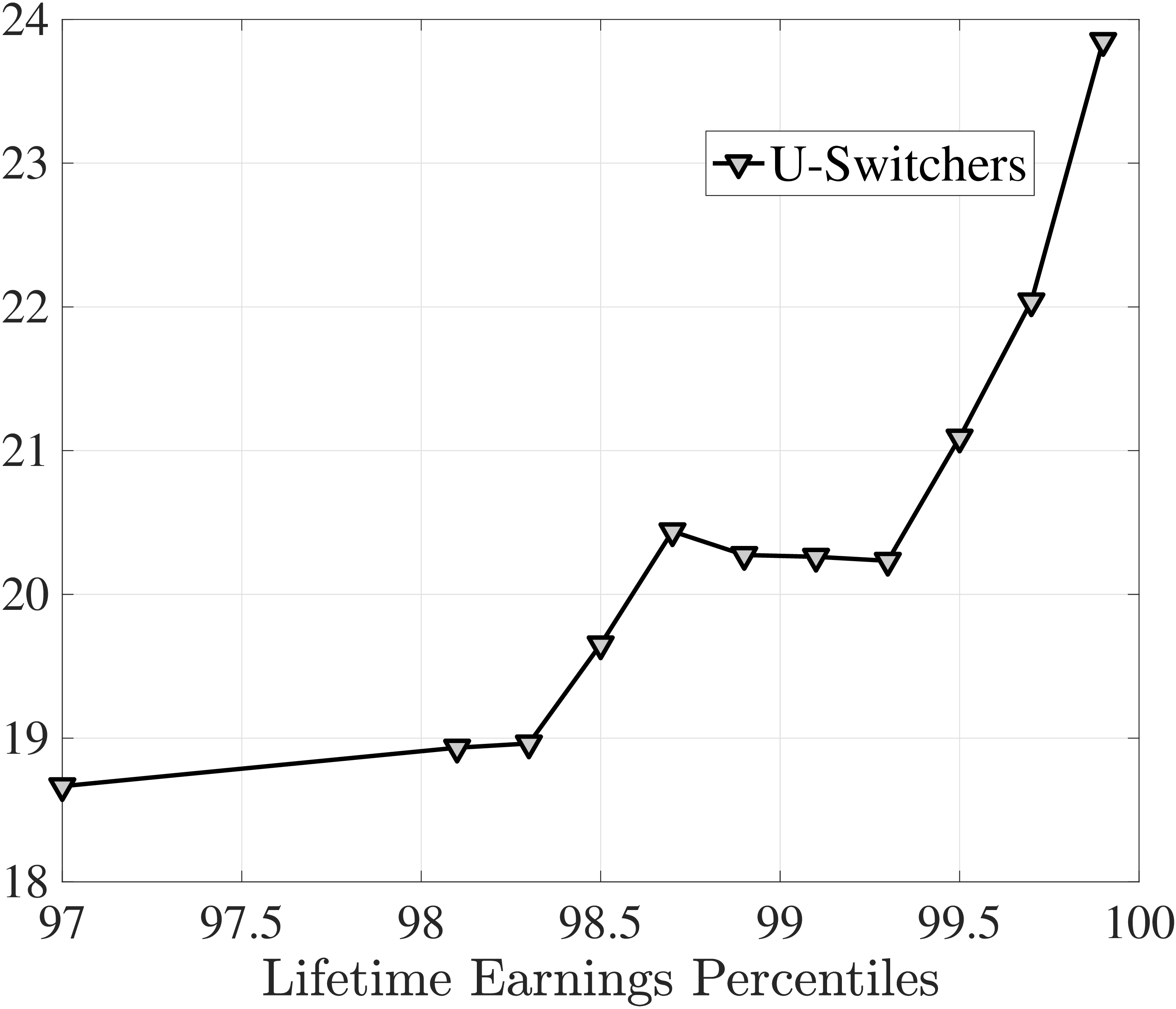

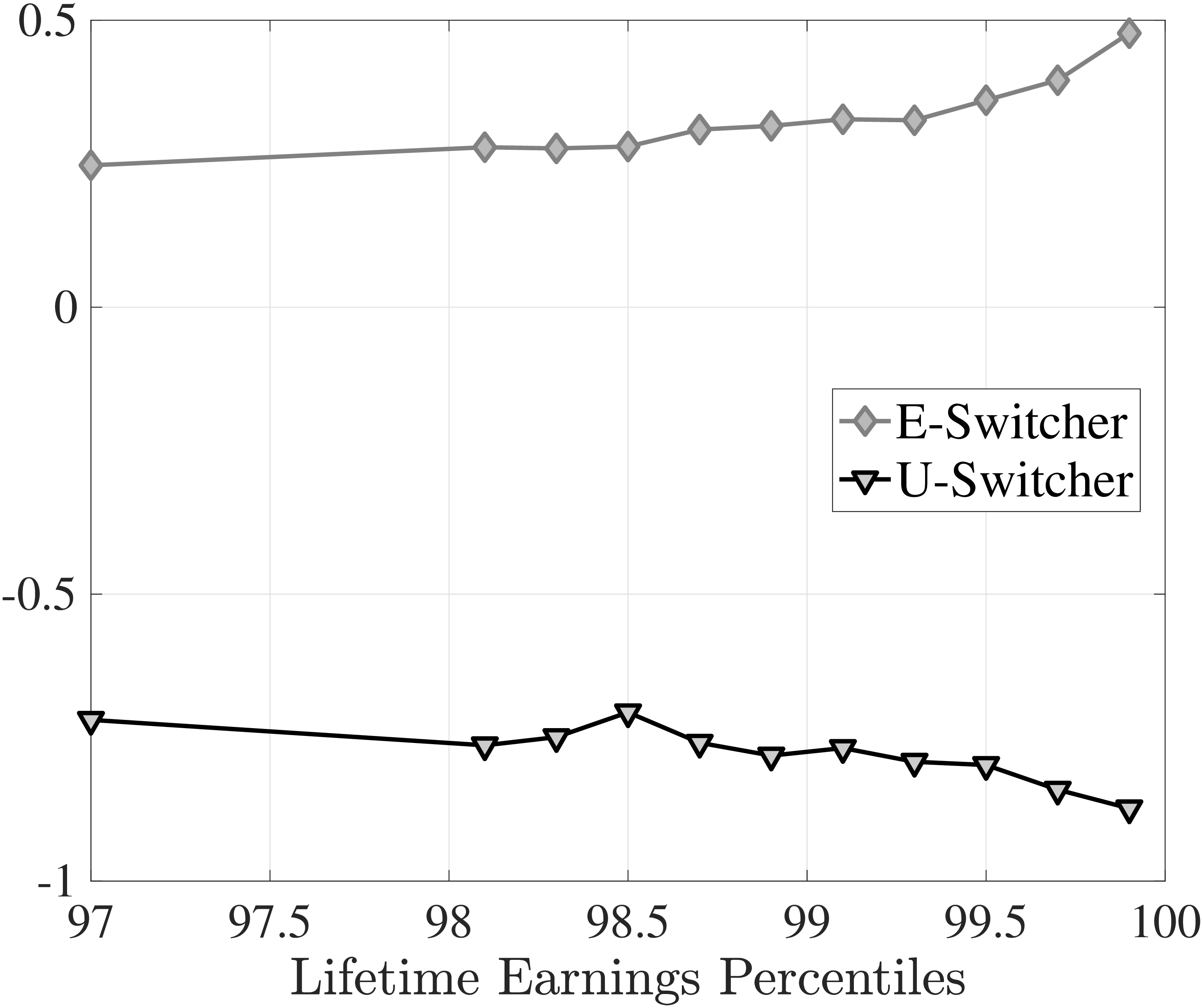

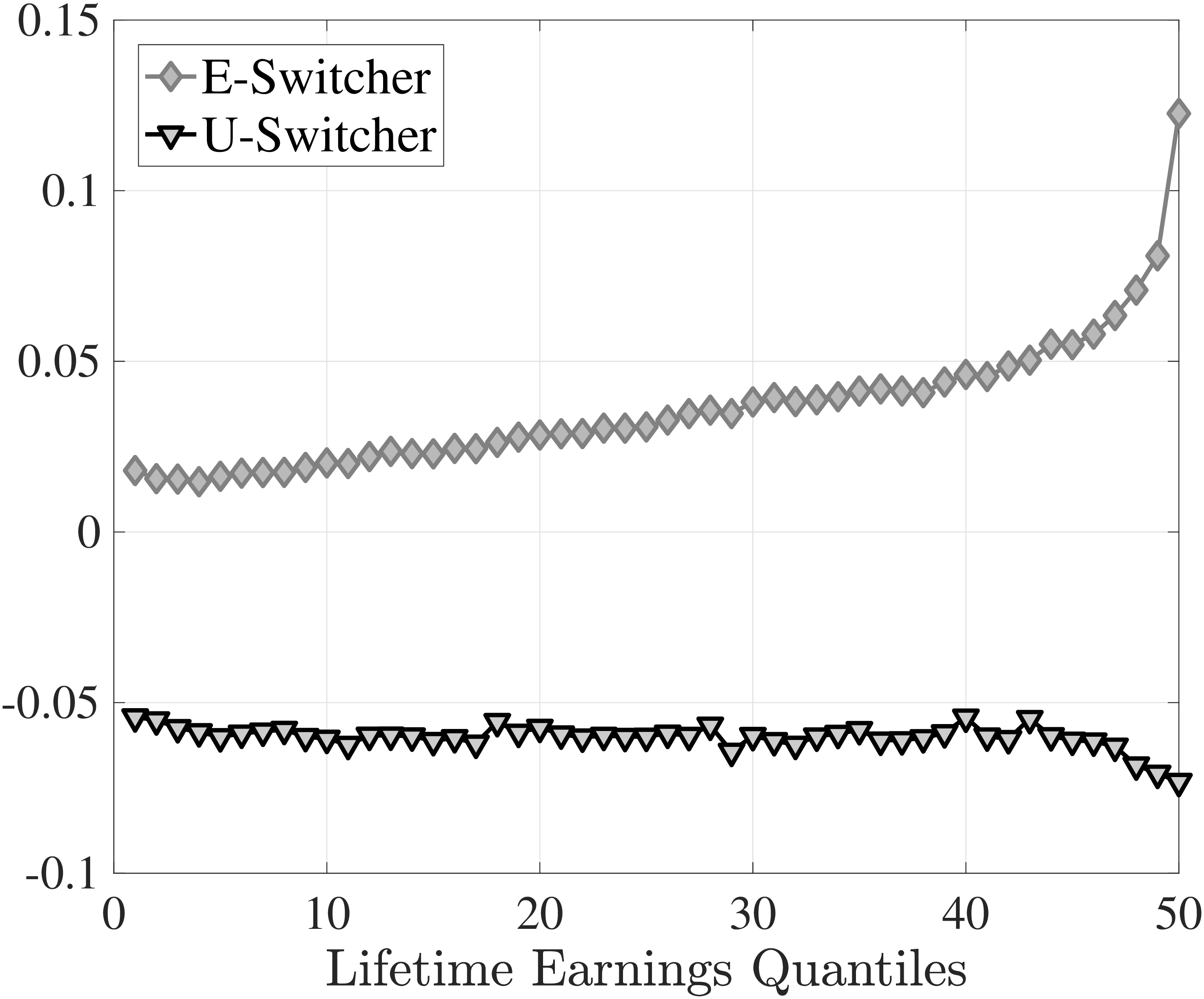

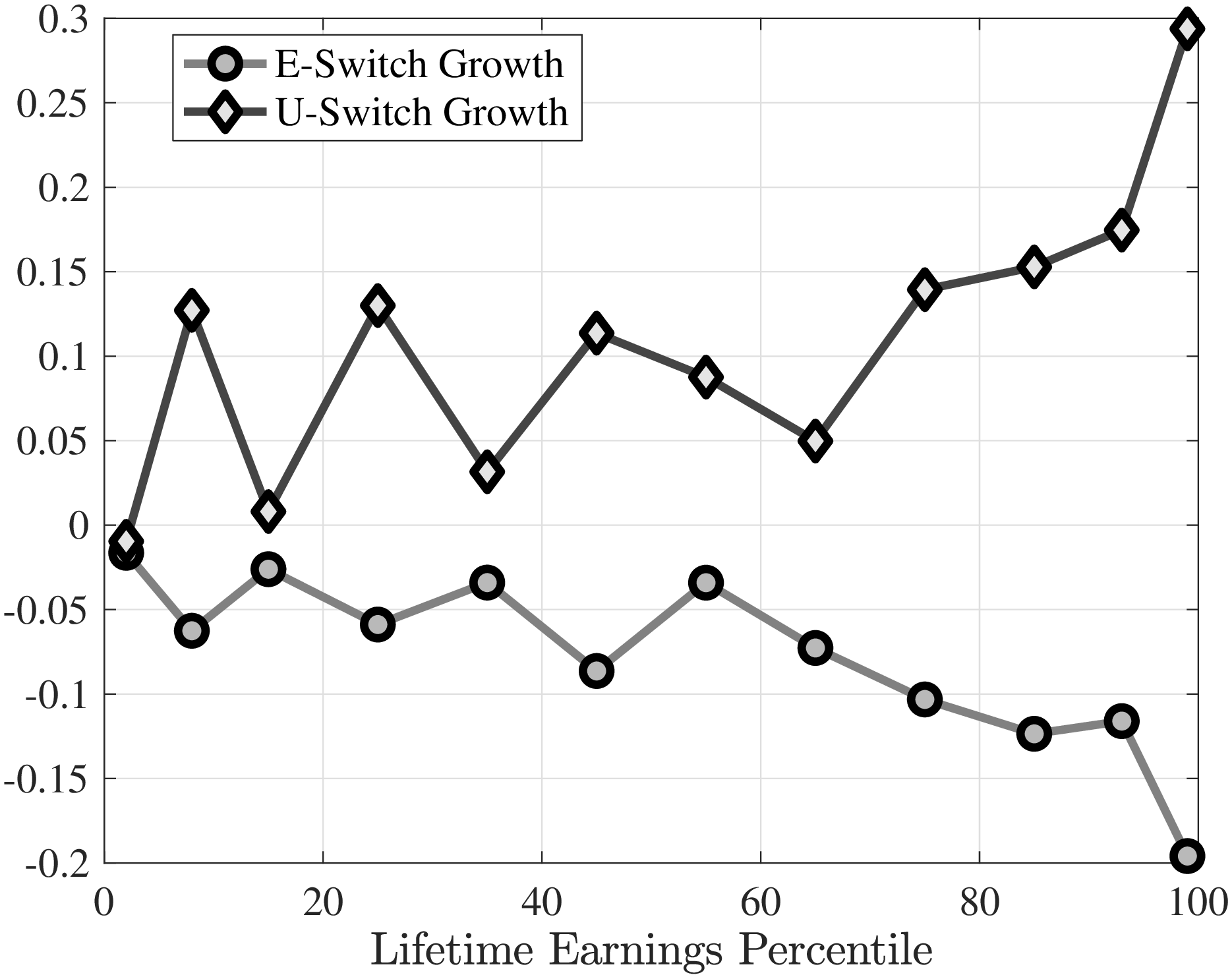

As we discussed before, job switchers are a very heterogeneous group as they include workers who switch jobs directly or due to a job loss (or a quit). The annual nature of the data does not allow us to separate these directly. Yet, we argue that the earnings growth distribution of switchers is informative about the nature of switches. For example, switchers who see their earnings decline by more than 25% have most likely experienced some nonemployment spell in \(t+1\). Thus, we classify such workers as “U-switchers,” and the remaining job switchers as “E-switchers.” The latter contains workers that make direct job switches as well as those coming out of nonemployment in \(t+1\).12

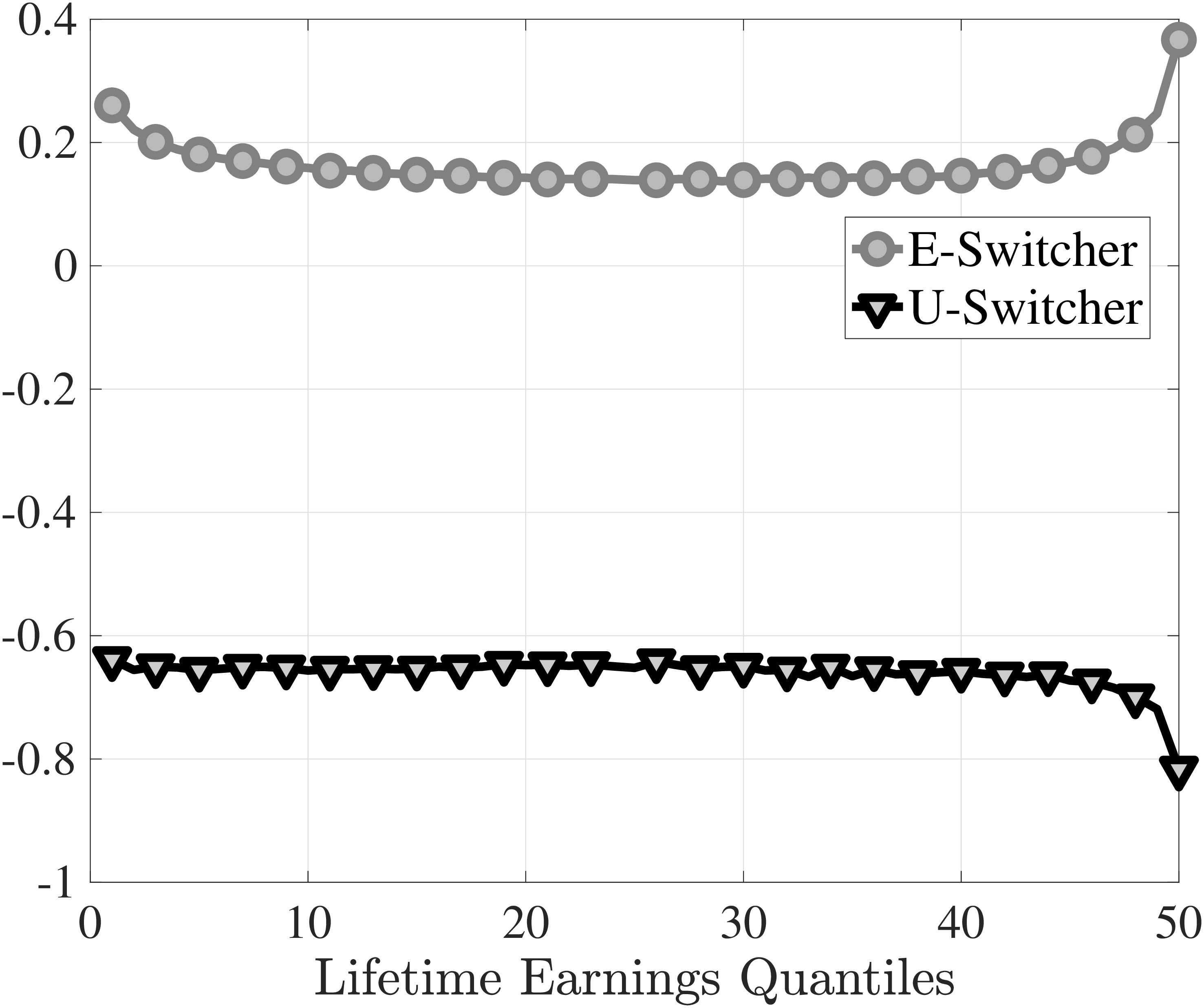

More than 35% of job switches are U-switches for bottom LE workers (Figure 3a). This share declines sharply over the LE distribution and reaches a low of 15% for \(LE_{40}\), before increasing to 20% for top LE workers. Thus, on average, higher LE individuals are more likely to make job switches involving earnings increases. Investigating the average earnings growth associated with each type of switch, we find large differences between E- and U-switches, but little variation across the LE distribution (except for the bottom and the top end). On average, an E-switch is associated with an earnings increase of larger than 15%, whereas a U-switch is associated with a decline of more than 60%.

The annual nature of our data limits the analysis of the earnings changes of job switchers.13 To investigate the role of annual aggregation in our results, we construct (normalized/average) earnings growth between the years when a worker is full-year employed in the same firm before and after the switch. Our substantive conclusions hold when we analyze this measure of earnings growth (Figure A.10). In addition, we investigate the monthly SIPP data, which allow us to construct direct measures of job loss (EU), job finding (UE), and job-to-job (EE) transition rates by income and age (see Appendix B for details). We find that low-income workers lose their jobs more often and the job finding rate is significantly lower for them (Figure B.1), therefore, they are more likely to make U-switches. In Section 5, we use these direct measures of quarterly job flow rates to quantitatively test our estimation results in an external validation exercise.

Notes: The left panel shows the share of U-switchers among job switchers averaged over the life cycle. The right panel plots the log growth of average earnings \(\bar{Y}\) between \(t\) and \(t+1\) for U- and E-switchers.

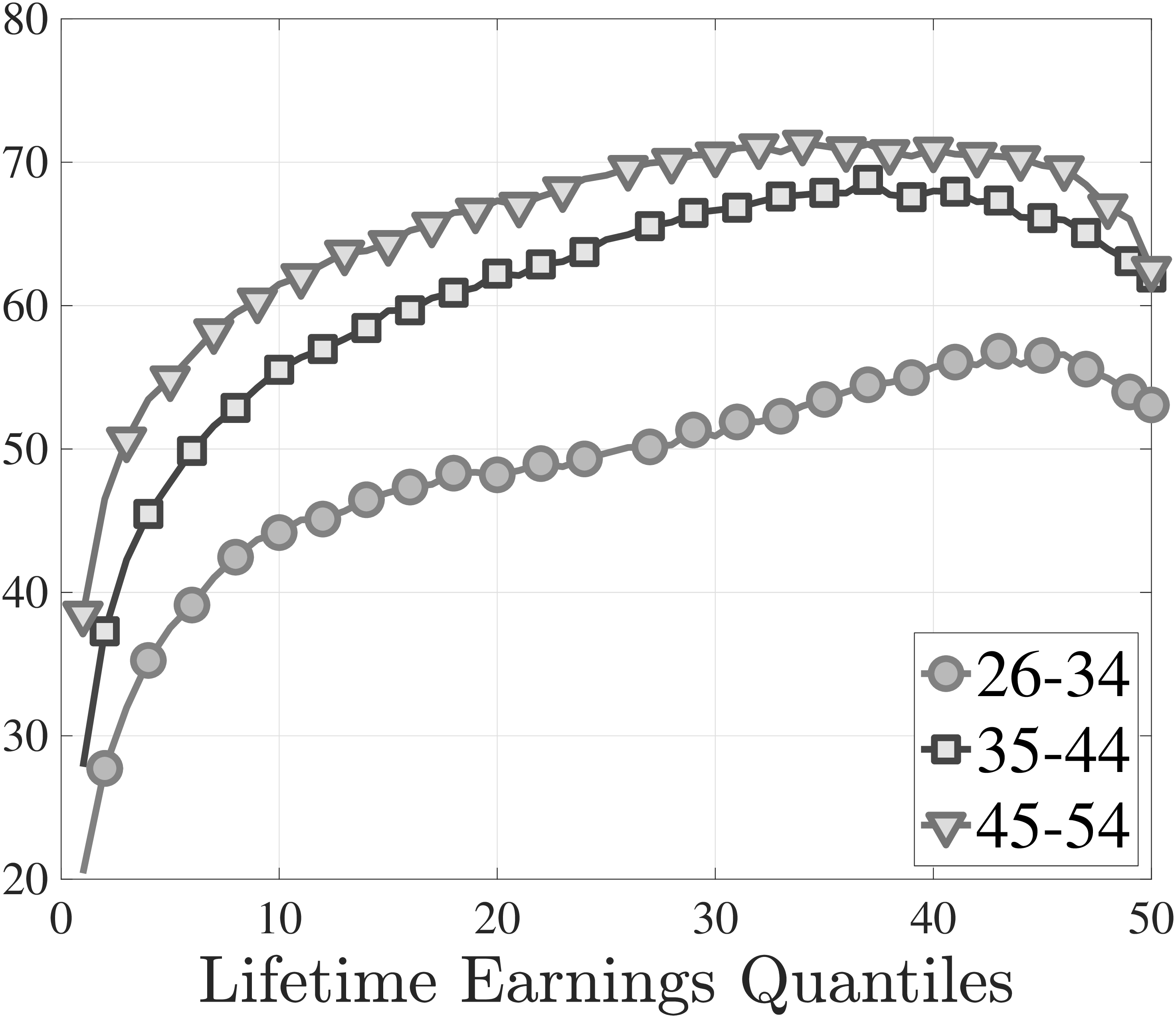

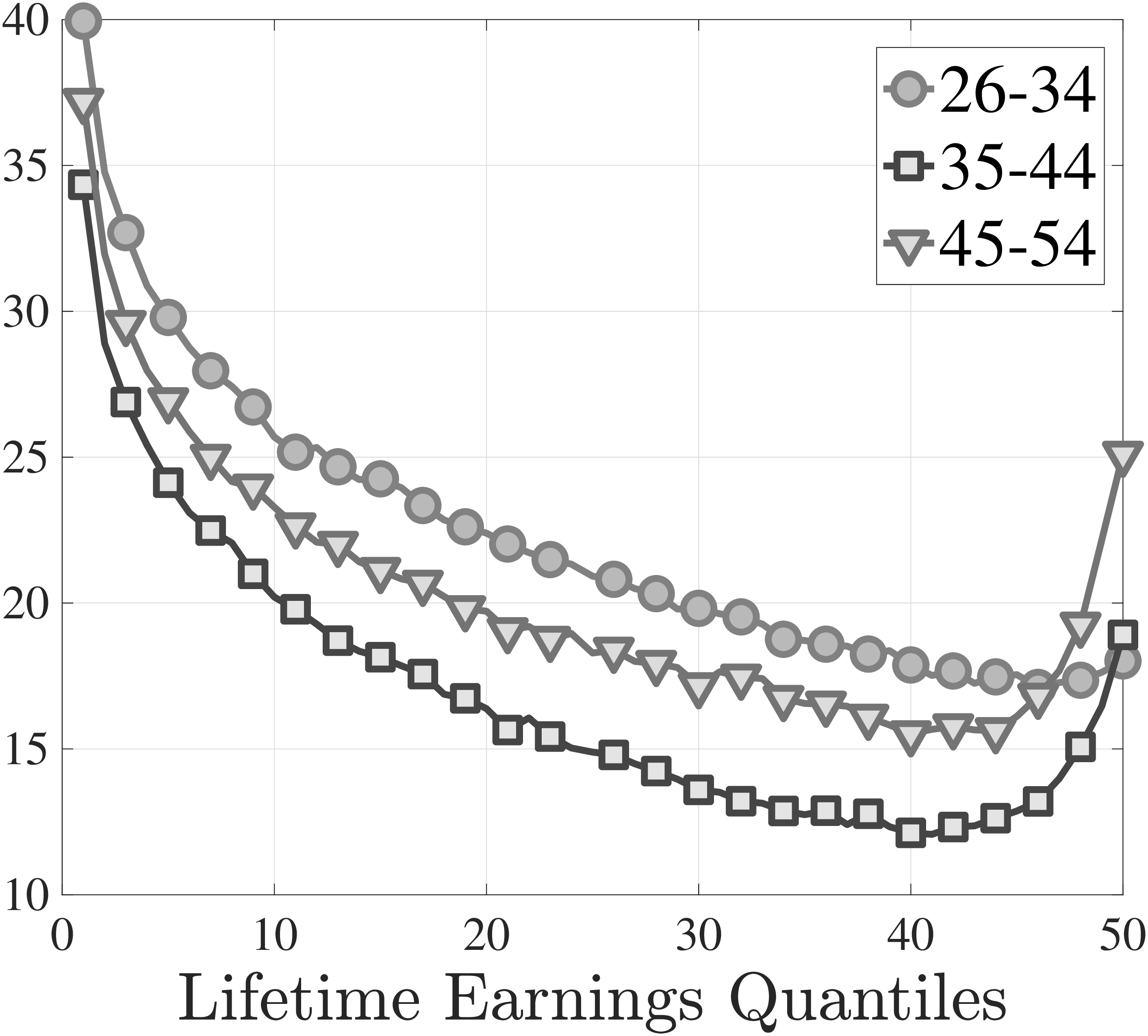

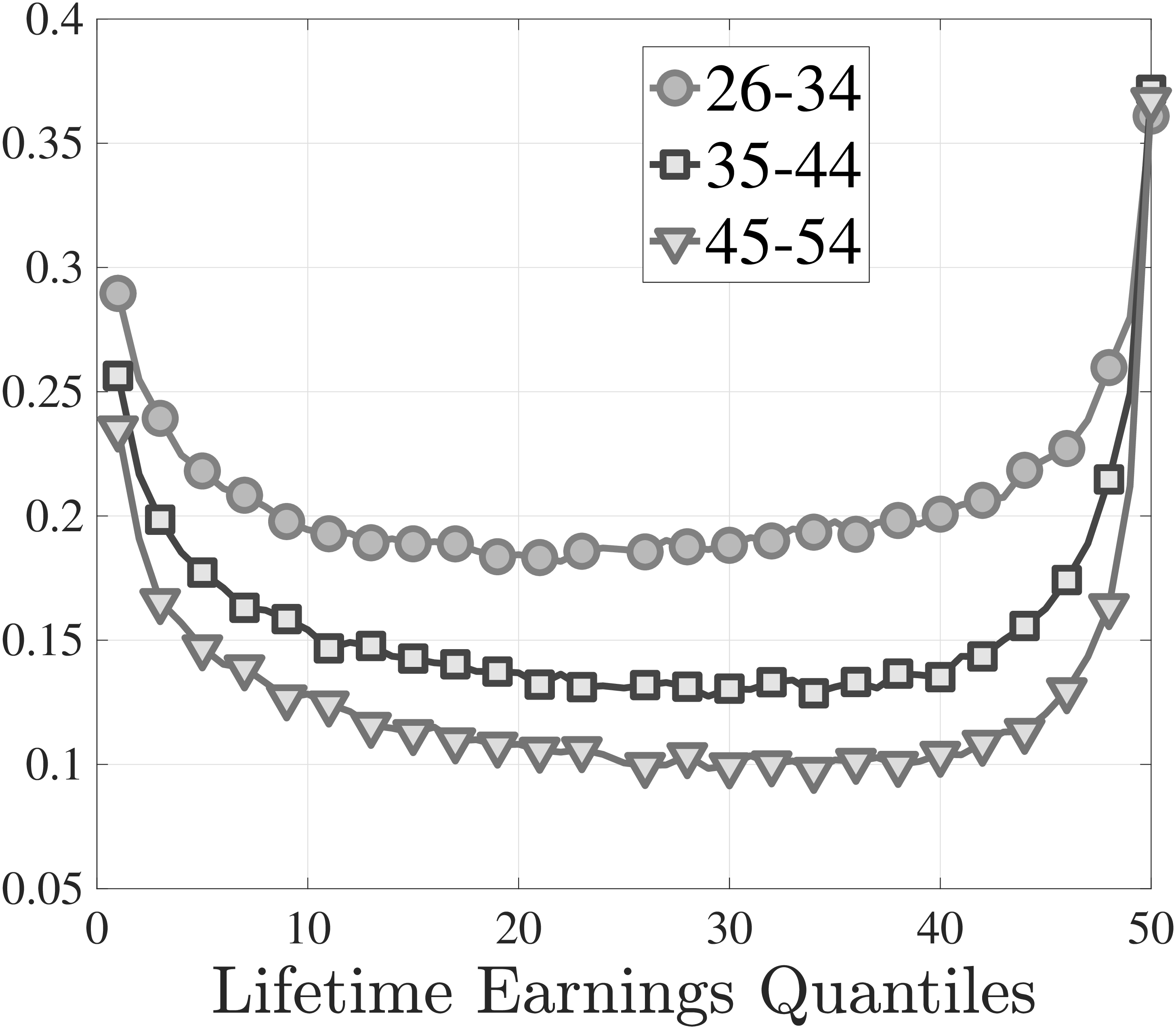

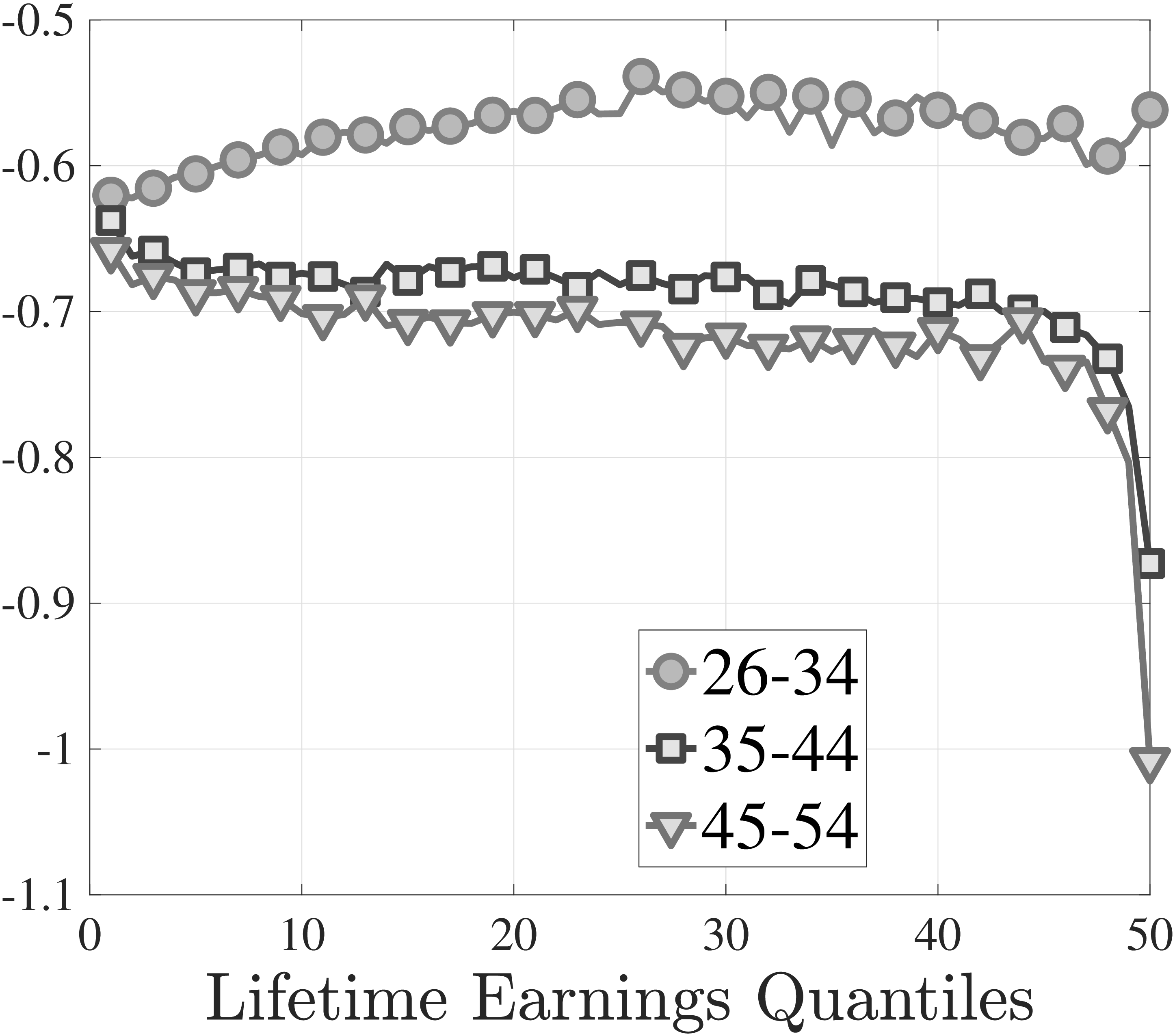

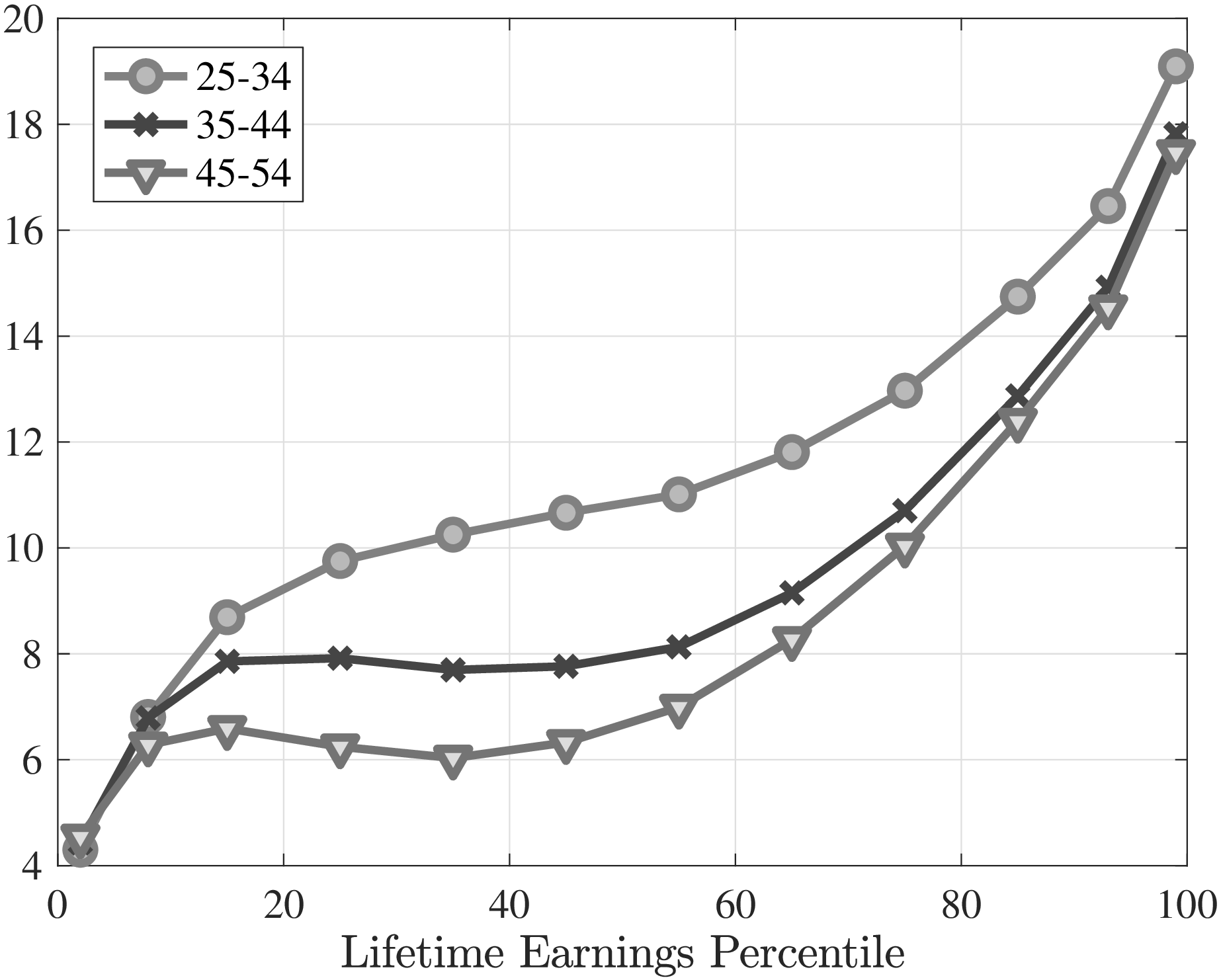

Life-cycle variation. Significant age variation in job switching and earnings growth rates has been extensively documented before (Topel and Ward (1992)). We contribute to this literature by investigating differences in these life-cycle profiles between income groups. Figure 4 plots the fraction of stayers and the earnings growth of job stayers and switchers for three stages of the working life over the LE distribution. The fraction of workers who stay with the same firm increases in a concave fashion over the life cycle for all LE groups. This increase is consistent with declining unemployment risk and job mobility documented before (Jung and Kuhn (2018)). Interestingly, the concavity is more pronounced above the median LE, resonating with larger decline in the number of distinct employers over the life cycle (Figure 2a).

Turning to the average earnings growth of job stayers, we find a flat profile below \(LE_{30}\) at all ages. Moreover, consistent with the existing literature, the rate of earnings growth declines with age. Similarly, the average earnings growth for job switchers also declines sharply over the life cycle, especially for higher LE workers, and becomes negative for oldest age group throughout the LE distribution (Figure 4c). Interestingly, being a job switcher or a stayer has limited effects on earnings growth of top LE workers before age 44, but it matters quite a bit for the oldest group. These individuals keep experiencing large earnings gains even after 44 when they stay with the same employer but their earnings decline if they switch jobs. In other words, in the top LE group earnings growth falls sharply for both job stayers and switchers over the life cycle but much more so for job switchers. This is because, first, U-switches become more likely among job switchers as the top LE workers get older. Second, and more importantly, average earnings growth for U-switches falls sharply for the oldest top LE workers (Figure A.8), which implies that unemployment spells become more costly for them. Our model is able to capture this feature of the data and we investigate it further in Section 5.

We have documented several facts regarding the careers of individuals who end up in different parts of the LE distribution. While these facts are useful for describing the various components of earnings growth heterogeneity, they do not suffice to provide an exact decomposition of the importance of the underlying economic forces or to separate ex-ante heterogeneity from ex-post luck. In what follows, we develop and estimate a structural model of wages and job turnover with heterogeneity in returns to experience and job ladder risk as well as ex-post productivity and job ladder shocks. In the end, this quantitative model will allow us to disentangle the various economic forces that shape the distribution of wage changes of job stayers and switchers.

3 Model

We build on Bagger et al. (2014) as it features a tractable framework to study the role of job search and learning on the job in generating wage growth.14 Despite endogenously generating some age variation in job mobility and earnings dynamics, this model falls short of capturing the magnitudes in the data. Thus, we incorporate stochastic aging to this framework à la Blanchard (1985). Furthermore, motivated by large negative earnings changes for job stayers, we also allow for recalls for unemployed workers by their last employers à la Fujita and Moscarini (2017). Next, we present our theoretical model and motivate each ingredient by linking them to specific empirical facts.

3.1 Environment

The economy is populated by heterogeneous workers and firms that produce a single consumption good sold in a competitive market. Workers can be employed or unemployed, and search for jobs in a frictional labor market, both on and off the job. They start life as young (\(y\)) and become old (\(o\)) with probability \(\gamma\). They have preferences with log per-period utility over consumption, and discount future periods at rate \(\rho\): U({c_{t}}{t=0}^{})={t=0}^{}()^{t}c_{t}. There is no inter-temporal savings technology that allows workers to smooth their consumption. This assumption along with the log preferences and log linear production function—which we introduce shortly—greatly simplifies computation.

Worker productivity. Each worker enters the labor market with no experience and accumulates human capital as he gains actual experience from employment. The human capital of worker \(i\) in period \(t\) is given by

\[ \begin{aligned} h_{it} & = & \tilde{h}_{it}+\epsilon _{it},\,\,\,\,\tilde{h}_{i0}=\alpha _{i}\\ \tilde{h}_{it} & = & \begin{cases} \tilde{h}_{it-1}-\varsigma & \text{if unemployed}\\ \tilde{h}_{it-1}+\beta _{i}+\zeta \left (\tau _{it}^{2}-(\tau _{it}-1)^{2}\right) & \text{if employed} \end{cases} \end{aligned} \]

Here, \(\tilde{h}_{it}\) denotes the deterministic component of human capital. Its level at \(t=0\), \(\tilde{h}_{i0}\), is determined by the worker’s type \(\alpha _{i}\), which reflects permanent heterogeneity in productivities due to differences in initial conditions such as innate ability, education, and labor market experience before \(t=0\). Human capital accumulates as the worker gains actual experience \(\tau _{it}\) through employment. Note that human capital is not specific to the firm, consistent with Gathmann and Schonberg (2010) who show labor market skills to be quite portable. Motivated by the large differences in average earnings growth for job stayers by LE, the rate of human capital accumulation has a worker-specific linear component \(\beta _{i}\), potentially correlated with \(\alpha _{i}\), and a common quadratic component \(\zeta\).15 In Huggett et al. (2011) individual-specific growth rates of human capital arise as a result of different investment choices due to the heterogeneity in productivities in the production of human capital. Our model captures this heterogeneity through exogenous differences in returns to experience. When a worker is unemployed, his human capital \(\tilde{h}_{it}\) depreciates at a constant rate \(\varsigma\).16 Finally, \(\epsilon _{it}\) is an idiosyncratic shock to worker productivity that captures the residual sources of variation in earnings not modeled in our framework, such as bonuses. Motivated by the large variation in the distribution of earnings changes for job stayers (Figure D.2), we assume that its distribution depends on worker type \(\alpha _{i}\) and age. We specify the process for \(\epsilon _{it}\) in Section 4 in detail.

Firm distribution and production technology. Productivity of a firm is constant over time and drawn from a distribution \(F(p)\) with a support of \(\left [\underline{p},\infty \right]\) common to all workers. A worker with human capital \(h_{it}\), who works for a firm with productivity \(p_{j(i,t)}\), produces a homogeneous good according to a log-linear production function, \(e^{y_{it}=p_{j(i,t)}+h_{it}}\).

3.1.1 Heterogeneity in search and matching

Unemployment risk. A job dissolves exogenously with probability \(\delta ^{a}(\alpha _{i})\), in which case the worker searches for a job. We model separation rates to be heterogeneous across workers of different types and ages. This heterogeneity is needed to capture the declining unemployment risk by the wage and age of workers discussed in Section 2.

Job finding rate. An unemployed worker of age \(a\in \{y,o\}\) with permanent ability \(\alpha _{i}\) meets a firm with probability \(\lambda _{0}^{a}(\alpha _{i})\), which captures ex-ante heterogeneity in job finding rates. This heterogeneity is motivated by our findings from the SSA and SIPP data and are potentially important for wage growth over the life cycle, as workers with a high job finding rate will work for more years, end up accumulating more human capital and, on average, work for more productive firms. To account for the sources of earnings growth, we explicitly model the differences in job finding rates. Furthermore, workers who are hit by separation shocks find a job immediately with probability \(\xi \lambda _{0}^{a}(\alpha _{i})\). As we discuss later, our model period is a quarter, and a nonnegligible fraction of laid-off workers find a job within three months (Abraham et al. (2016)). Moreover, there is evidence of transitions that look like direct job-to-job switches but are actually involuntary (Jolivet et al. (2006)). Thus, we allow for the possibility of finding a job within the same period.

Recalls. In the data, there are many job stayers who experience large declines in annual earnings. Strongly left-skewed idiosyncratic productivity shocks could in principle account for these large losses, in turn, we would have erroneously assigned a bigger role for ex-post productivity shocks especially for low-income workers (as opposed to their higher ex-ante unemployment risk). Instead, we allow for a recall option of unemployed workers by their last employers, which is fairly prevalent in the data (Fujita and Moscarini (2017)). Specifically, we assume that with probability \(\lambda _{r}\) the offers for unemployed workers come from their last employers. The recall option can alter the wages as it affects the value of a job to a worker. However, we assume that the option value of recall is not considered in the wage bargaining process.17 This assumption keeps the estimation computationally feasible as it allows us to derive the wage equation analytically.

Search on the job. While employed, workers search for better jobs and with probability \(\lambda _{1}^{a}(\alpha _{i})\) receive an outside offer from another employer, whose productivity is drawn from the distribution \(F(p)\), triggering a renegotiation between two firms that we explain below. As Figures 3a and B.1c have shown, workers differ in the types and rates of job switches. Our framework can generate qualitatively similar patterns without explicit differences in the contact rates: High-wage workers—employed on average by more productive firms—are less likely to get an offer that beats their current employer. This reduces their job-to-job transition rate even if they receive counteroffers at the same rate as low-wage workers. Similarly, as workers get older, they settle into higher paying jobs and are less likely to move. However, our estimation shows that this endogenous mechanism is insufficient to explain the quantitative differences in the data.

Timing of events. At the beginning of each period, the productivity shocks are drawn and workers’ human capital is updated according to equation 1. Next, output is produced and wages are paid. There is no inter-temporal savings device, so workers consume their wages. At the end of the period, search and matching shocks are realized: Unemployed workers who find jobs negotiate their wage, workers who receive an outside offer renegotiate their wages or switch employers, and employed workers that draw separation shocks become unemployed. They may find a job immediately or have to wait for the next period to search. Aging occurs stochastically at the end of the period with probability \(\gamma\) and is mutually exclusive from the labor market shocks.

3.2 Wage determination

We now briefly explain the bargaining protocol by focusing on the key equations and how the life-cycle structure affects them. See Appendix C for derivations.

Wages are specified as piece-rate contracts. In particular, if a worker with human capital \(h\) works for a firm of productivity \(p\) at a piece rate of \(R=e^{r}\leq 1,\) he receives a log wage \(w\) of \(w=r+p+h\). Here \(R\), the contractual piece rate, is determined endogenously. Upon meeting with a firm, the worker bargains over this piece rate \(R\), which is not updated until the worker meets with another firm.

We now describe how this piece rate is determined for workers with different labor market states. First, let’s define \(\mathbb{I}_{i}\equiv \{\alpha _{i},\beta _{i}\}\) as the vector of individual-specific state variables capturing ex-ante (fixed) heterogeneity. Note that as we discussed above, \(\mathbb{I}_{i}\) pins down the individual-specific worker flow rates as well as the firm distribution, i.e., \(\{\delta ^{y}(\alpha _{i}),\delta ^{o}(\alpha _{i}),\lambda _{0}^{y}(\alpha _{i}),\lambda _{0}^{o}(\alpha _{i}),\lambda _{1}^{y}(\alpha _{i}),\lambda _{1}^{o}(\alpha _{i})\}\). The value functions introduced below are individual specific and thus a function of \(\mathbb{I}_{i}\) in addition to other state variables.

Hires from unemployment. Let \(V_{0}^{a}\left (h;\mathbb{I}_{i}\right)\) and \(V^{a}\left (r,h,p;\mathbb{I}_{i}\right)\) denote the expected lifetime utility of an unemployed worker \(i\) with human capital \(h\) at age \(a\), and when he is employed at a firm with productivity \(p\) at piece rate \(e^{r},r<0\), respectively. We define \(V^{a}\left (r,h,p;\mathbb{I}_{i}\right)\) below and assume that the value of unemployment is equivalent to employment in the least productive firm of type \(p_{\min}\) extracting the entire match surplus, i.e., \(V_{0}^{a}\left (h;\mathbb{I}_{i}\right)=V^{a}\left (0,h,p_{\min};\mathbb{I}_{i}\right)\). This assumption—typical for this class of models and justified by the high empirical job acceptance rate of the unemployed (Van den Berg 1990)—implies that unemployed workers accept any job offer and simplifies the problem.

The wage bargaining protocol dictates that unemployed workers receive \(\theta\) share of the expected match surplus, where \(\theta\) captures the worker’s bargaining power.18 More specifically, the piece rate of a hire from unemployment, \(r_{0}\), solves

\[ \mathbb{E}V^{a}\left (r_{0},h',p;\mathbb{I}_{i}\right)=V_{0}^{a}\left (h;\mathbb{I}_{i}\right)+\theta \mathbb{E}\left [V^{a}\left (0,h',p;\mathbb{I}_{i}\right)-V_{0}^{a}\left (h;\mathbb{I}_{i}\right)\right]. \]

The worker’s surplus from the match is the increase in expected lifetime utility from unemployment to a state where he is paid his entire output (\(r=0\)). Thus, when an unemployed is hired, the firm offers a piece rate that increases his expected lifetime utility by \(\theta\) share of this surplus. In equation (2), the expectation is with respect to \(\epsilon _{t+1}\).

Poaching. When a worker is contacted by a firm with productivity \(p'\), the incumbent firm and the poacher compete. The more productive firm outbids the less productive one and hires the worker. We now discuss the wage that arises as a result of this competition.

There are several cases to consider. First, suppose that the poacher has higher productivity; \(p'>p\). Then, the poacher hires the worker by paying a piece rate \(r'\) that increases the worker’s value by \(\theta\)–share of the surplus generated by the match: \[ \mathbb{E}V^{a}\left (r',h',p';\mathbb{I}_{i}\right)=\mathbb{E}\left \{V^{a}\left (0,h',p;\mathbb{I}_{i}\right)+\theta \left [V^{a}\left (0,h',p';\mathbb{I}_{i}\right)-V^{a}\left (0,h',p;\mathbb{I}_{i}\right)\right]\right \}. \] Note that as Postel-Vinay and Robin (2002) have shown, job switches may result in workers accepting wage losses, as they anticipate faster wage growth in higher productivity firms. Wage losses upon job switches are a prominent feature of the data.

Second, let’s consider a case in which the poacher has lower productivity than the current employer. Bertrand competition implies that the incumbent firm retains the worker, possibly by adjusting the worker’s piece rate. This new piece rate offers the worker the maximum value he could attain working at firm \(p'\), i.e., the value associated with \(r=0\) (\(R=1\)), and a \(\theta\)–share of the additional surplus generated by the offer. In this case, the new piece rate \(r'\) solves the following equation: \[ \mathbb{E}V^{a}\left (r',h',p;\mathbb{I}_{i}\right)=\mathbb{E}\left \{V^{a}\left (0,h',p';\mathbb{I}_{i}\right)+\theta \left [V^{a}\left (0,h',p;\mathbb{I}_{i}\right)-V^{a}\left (0,h',p';\mathbb{I}_{i}\right)\right]\right \}. \] Note that in contrast to other models of on-the-job search such as Burdett and Mortensen (1998) and Hubmer (2018), this model generates potentially large and leptokurtic increases in wages for job stayers, which is prevalent in the data (Guvenen et al. (2021)).

In some cases, the productivity of the poacher may be so low that the new offer does not generate any additional surplus and therefore does not trigger a change in the piece rate. Then, the worker discards the offer. Let \(q^{a}(r,h,p;\mathbb{I}_{i})\) denote this threshold firm productivity such that offers from firms with \(p'\leq q^{a}(r,h,p;\mathbb{I}_{i})\) are discarded. \(q^{a}\) solves \[ \mathbb{E}V^{a}\left (r,h',p;\mathbb{I}_{i}\right)=\mathbb{E}\left \{V^{a}\left (0.h',q^{a};\mathbb{I}_{i}\right)+\theta \left [V^{a}\left (0,h',p;\mathbb{I}_{i}\right)-V^{a}\left (0,h',q^{a};\mathbb{I}_{i}\right)\right]\right \}. \]

4 Estimation

We now use this model to estimate the contributions of the heterogeneity in the worker flow rates and the ability to accumulate human capital to the differences in earnings growth over the life cycle. To this end, we first exogenously set four parameters: The quarterly discount rate \(\rho\) is set to 0.005 to match the annual rate of 2%; workers’ bargaining power \(\theta\) is set to 0.4 following Bagger et al. (2014); the quarterly aging probability \(\gamma\) is set to \(1/60\) so that a worker becomes old on average in 15 years; and the reallocation probability \(\xi\) is set to 0.4 following Abraham et al. (2016).

We estimate the remaining parameters using the simulated method of moments (SMM). We simulate quarterly data for 100,000 individuals and aggregate them to annual observations to create a matched employer-employee panel mimicking the SSA sample. Importantly, we subject the model to the same sample selection criteria in Section 2.1 and compute the model counterparts of targeted moments. Recall that our sample consists of workers between ages 25 and 55 (Section 2.1). However, estimation does not assume that workers start their careers at age 25. Instead, both in the data and the model we are agnostic about workers’ labor market experiences before age 25. Thus, previous labor market experience or time spent in school would show up as ex-ante heterogeneity in our estimation. In our simulations, each individual starts unemployed at the age of 23 and we discard the first two years to allow workers to find a job before age 25.

4.1 Targeted moments

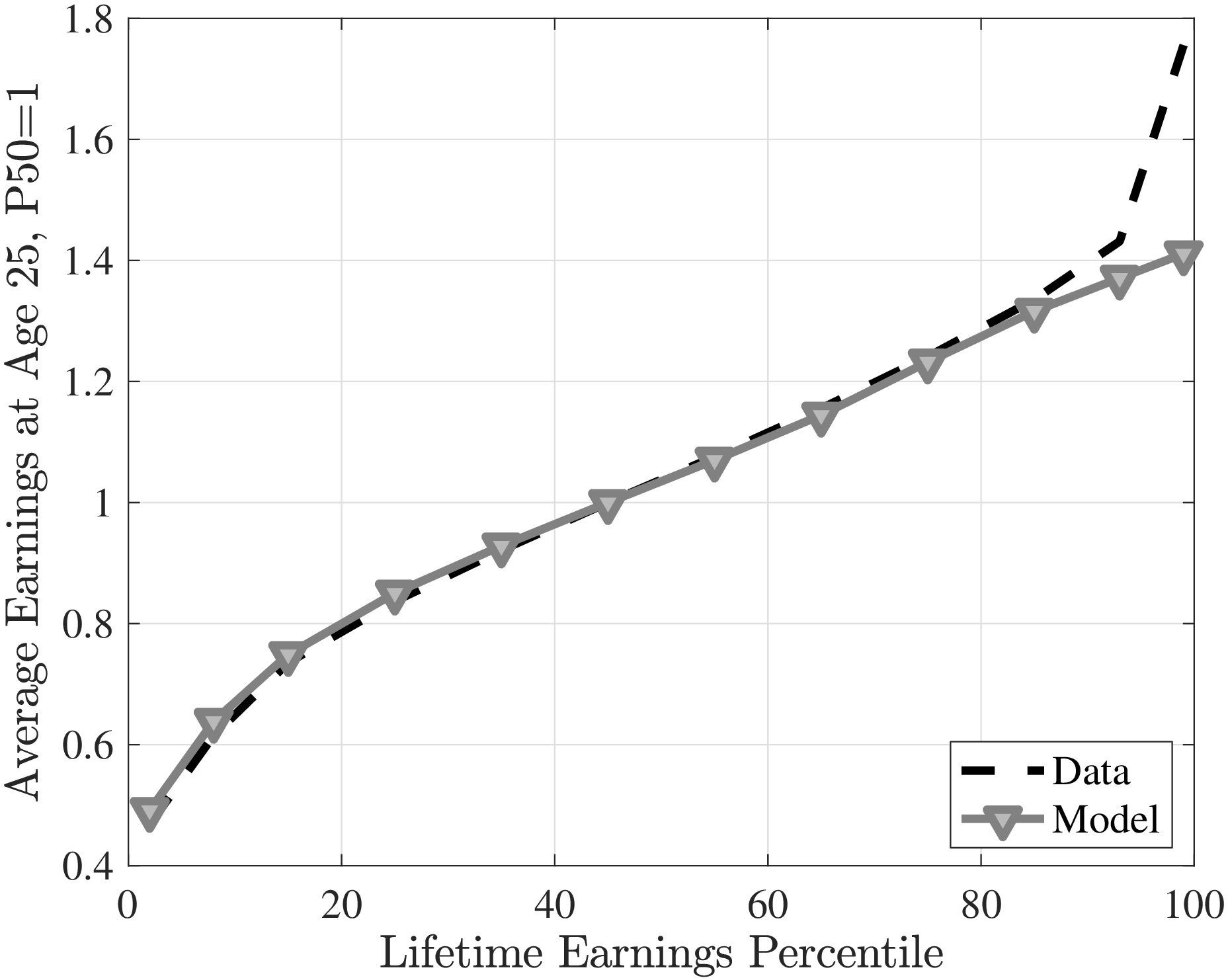

We target five sets of moments. The first two are about the cross-sectional distribution of earnings changes for job stayers and switchers. The third and fourth have to do with the fraction of job stayers, E–switchers, and U–switchers and their average annual earnings growth, respectively. Finally, we target average earnings at age 25 by LE group. We choose to not target the heterogeneity in lifetime income growth. As we argue in the next section, the model is already identified using these five sets of moments.

Grouping workers. We condition each targeted moment on LE and age groups. Specifically, we calculate workers’ lifetime earnings as in Section 2 and rank them into 12 percentile groups: 1–4, 5–10, 11–20,…, 81–90, 91–96, 97–100. Furthermore, we group workers into three age groups: 25–34, 35–44, 45–54.

Cross-sectional moments of earnings growth. As documented in Guvenen et al. (2021), earnings changes are highly leptokurtic and left skewed. This shape of the earnings change distribution is broadly consistent with job ladder models: Most workers see little change but a small share experience a large swing due to unemployment, a job-to-job transition or an outside offer, which in turn may lead to a left-skewed and leptokurtic distribution. Based on these insights, we target the mean, standard deviation, skewness, and kurtosis of annual earnings changes for job stayers and switchers separately.19 We also condition workers based on their lifetime earnings because of large variation in these moments by income (Guvenen et al. (2021)).

An issue when computing growth rates is dealing with zero earnings. Recall that in our sample, we drop workers with two or more consecutive years of zero earnings. However, there are still observations with no income in a given year. We would like to keep them as they contain information about the importance of search frictions. For this purpose, we use the arc percent growth measure defined as \(2(Y_{t+1}-Y_{t})/(Y_{t+1}+Y_{t})\), where \(Y_{t}\) is annual earnings. Targeted cross-sectional moments are shown in Figure D.2.

Average income growth moments. Next, we target the fraction and average income growth of job stayers, E–switchers, and U–switchers by three age and 12 LE groups. The details of how these moments are constructed are discussed in Section 2.3. Figures D.1 and D.3 show these moments by age and the targeted LE groups.

Average earnings at age 25. Finally, we target the average earnings by LE group at age 25. This moment of the data is shown in Figure D.4.

4.2 Identification

Below we provide an informal discussion of identification of our model. We acknowledge that all parameters are determined jointly within the SMM estimation as most parameters affect more than one aspect of the data. In this section, our goal is to show that each feature of the model has a pronounced effect on at least one unique moment targeted in the estimation. Namely, there is at least one unique feature of the data that informs each ingredient of the model. This identification discussion also justifies the selected targeted moments presented in the previous section.20

Ex-ante worker productivity (\(\alpha,\beta\)). The concave average life-cycle profile of earnings growth is informative about the average experience profile of worker productivity, driven in the model by the mean of the joint (\(\alpha,\beta\)) distribution and the common quadratic term \(\zeta\). The differences in the initial earnings levels of LE groups and their stayer earnings growth (Figure 2c) help us pin down the variance-covariance matrix of the joint distribution of \(\alpha\) and \(\beta\). Note that the distribution of firm productivities also has a first-order effect on the initial earnings dispersion as well as on the earnings growth of job stayers through outside offers. As we discuss next, we use other features of the data to identify the distribution of firm productivities.

Firm productivity distribution. In the estimation of job ladder models, identifying the distribution of firm productivities is a key challenge. There are several approaches to estimate this distribution using matched employer-employee data.21 For example, Postel-Vinay and Robin (2002), Cahuc et al. (2006) and Bagger et al. (2014) use data on firms’ value added or profitability to back out the firm distribution. We cannot implement this method as our dataset doesn’t contain any direct information on value added or profitability. Barlevy (2008) shows that under appropriate conditions the wage gains of job switchers could identify the offer distribution nonparametrically, even in the presence of unobserved worker heterogeneity. Bagger and Lentz (2014) use poaching patterns between firms to rank firms with respect to their productivity. More recently, Bonhomme et al. (2017) uses k-means clustering to classify firms into discrete groups.

The key insight for our approach of identifying the firm productivity distribution relies on differences in earnings growth between job stayers and switchers, with stayer growth exhibiting relatively little heterogeneity at the bottom two thirds of the LE distribution and switchers showing much larger differences throughout the LE distribution (Figure 2c). If there was no job ladder to be climbed (i.e., a degenerate firm distribution), then the average earnings growth of switchers and stayers would look very similar (especially in the upper half of the LE distribution) as they would both be mainly driven by the differences in \(\beta\). Job ladder dynamics through the shape of the firm distribution, on the other hand, help the model generate a different profile of earnings growth for stayers and switchers. We confirm this insight by investigating the sensitivity of \(\psi _{f}\) to switcher earnings growth moments à la Andrews et al. (2017) (see Appendix D.2).

Heterogeneity in worker flow rates (\(\delta ^{a}(\alpha),\lambda _{0}^{a}(\alpha),\lambda _{1}^{a}(\alpha),\lambda _{r}\)). Our strategy relies on identifying these flow rates separately for each LE and age group and then linking the LE groups to ex-ante worker type \(\alpha\). U–switches, those that involve a larger than 25% earnings loss (Figure 3b), are intimately linked to the job loss rate \(\delta\). Moreover, their frequency is not affected by the rate of job-to-job transitions, because such transitions result in either wage increases or wage losses smaller than 25%, and are therefore counted among E-switches.22 Turning to the job finding rate \(\lambda _{0}\), this rate determines how long a given unemployment spell lasts. Therefore, it has a pronounced effect on the average earnings loss of U–switchers along with the possible wage decline associated with falling off the job ladder. The latter is determined by the shape of the firm distribution, whose empirical underpinning is discussed above. Finally, the stayer probability is given by a combination of the job loss rate \(\delta\) and the offer arrival rate for the employed \(\lambda _{1}\) as well as the recall rate \(\lambda _{r}\). The key feature that identifies the recall rate is the left skewness of earnings growth for job stayers. In the model, stayer growth distribution is dramatically right skewed in the absence of recalls. Having already identified \(\delta\) and \(\lambda _{r}\), stayer probability can now be used to pin down \(\lambda _{1}\).

Idiosyncratic shocks (\(\epsilon\)). They are residuals of earnings growth not explained by the structural features of the model. Our simulations show that the endogenous mechanisms can explain well the earnings dynamics of job switchers. Thus, we use the higher-order moments of earnings changes for job stayers to identify the idiosyncratic risk.

Age dependence in parameters. Targeted moments identifying the flow rates and the distribution of idiosyncratic shocks have strong age variation in the data (see Section 2), which we exploit to identify the age dependence in these parameters.

4.3 Estimation methodology

In this section we first explain the functional form assumptions concerning the worker and firm distributions as well as the flow rates. While our identification strategy does not require specific functional forms, these assumptions allow us to have more statistical power and keep the estimation computationally feasible. Next, we describe the SMM objective function along with the computational method used for estimation.

Functional forms. The worker fixed-effect \(\alpha\) is normally distributed with mean \(\mu _{\alpha}\) and standard deviation \(\sigma _{\alpha}\). \(\beta\) is Pareto distributed with shape and scale parameters \(\chi _{w}\) and \(\psi _{w}\), respectively, and is correlated with \(\alpha\) by the coefficient \(\rho _{\alpha \beta}\). We also estimated a version of our model with Gaussian \(\beta\) and have found that a fat-tailed distribution such as Pareto helps the model better match the very large earnings growth of top LE groups relative to the median and the relatively smaller differences between the median and the bottom LE groups.23 We revisit this choice later in the context of estimation results in Section 5. Firm productivity is also assumed to be Pareto distributed with shape and scale parameters \(\chi _{f}\) and \(\psi _{f}\), respectively.24 We normalize the scale parameter \(\psi _{f}\) to 1, as one cannot separately identify \(\psi _{f}\) and the mean of the \(\alpha\) distribution.

We model the heterogeneity in worker flow rates as a function of worker type \(\alpha\) and age. In particular, we use a cubic spline to model unemployment risk, the job finding rate, and the contact rate as a function of \(\alpha _{i}-\mu _{\alpha}\) for each age group. We experimented with the number of points for each flow rate and concluded that three points for each age group was flexible enough for job finding and contact rates, whereas unemployment risk required 5 points for each age to fit the heterogeneity in the data.

Finally, we assume that the i.i.d idiosyncratic shocks hit only job stayers once a year with some probability \(\pi (\alpha)\) (because endogenous mechanisms can explain well the earnings dynamics of job switchers). Innovations are normally distributed with standard deviation \(\sigma _{\epsilon}\) and \(\pi (\alpha)\) is modeled as a cubic spline separately for each age group.25

SMM objective function. Let \(d_{n}\) for \(n=1,...,N\) denote a generic empirical moment, and let \(m_{n}(\theta)\) be the corresponding model moment that is simulated for a given vector of model parameters, \(\theta\). The scales of the moments vary largely, thus we measure the distance between the data and the simulated moments by arc percentage deviation, \(F_{n}(\theta)=2\times \frac{m_{n}(\theta)-d_{n}}{m_{n}(\theta)+d_{n}}\). Our SMM estimator is then defined by \(\hat{\theta}=\arg \min _{\theta}\boldsymbol{F}(\theta)'W\boldsymbol{F}(\theta)\), where \(\boldsymbol{F}(\theta)=\left [F_{1}(\theta),...,F_{N}(\theta)\right]^{T}\). The weighting matrix \(W\) reflects our beliefs on the importance of each set of moments in identifying the economic forces behind earnings growth.26 We target a total of 380 moments to estimate 41 parameters.

Numerical method for estimation. We employ a multistart global optimization algorithm available by Guvenen and Ozkan (2021). In particular, we generate 15,000 uniform Sobol (quasi-random) points, compute the objective value for each of these, and select the best 1,000 (ranked by the objective value), each of which is used as an initial guess for the local minimization stage. This stage is performed with a mixture of Nelder-Mead’s downhill simplex algorithm and the DFNLS algorithm of Zhang et al. (2010). In the end, we pick the best parameter estimates out of 1,000 local minima.

5 Estimation Results

5.1 Parameter estimates

We first discuss the key parameter estimates by relating them to the moments that inform them the most. The full set of estimates are presented in Appendix D.

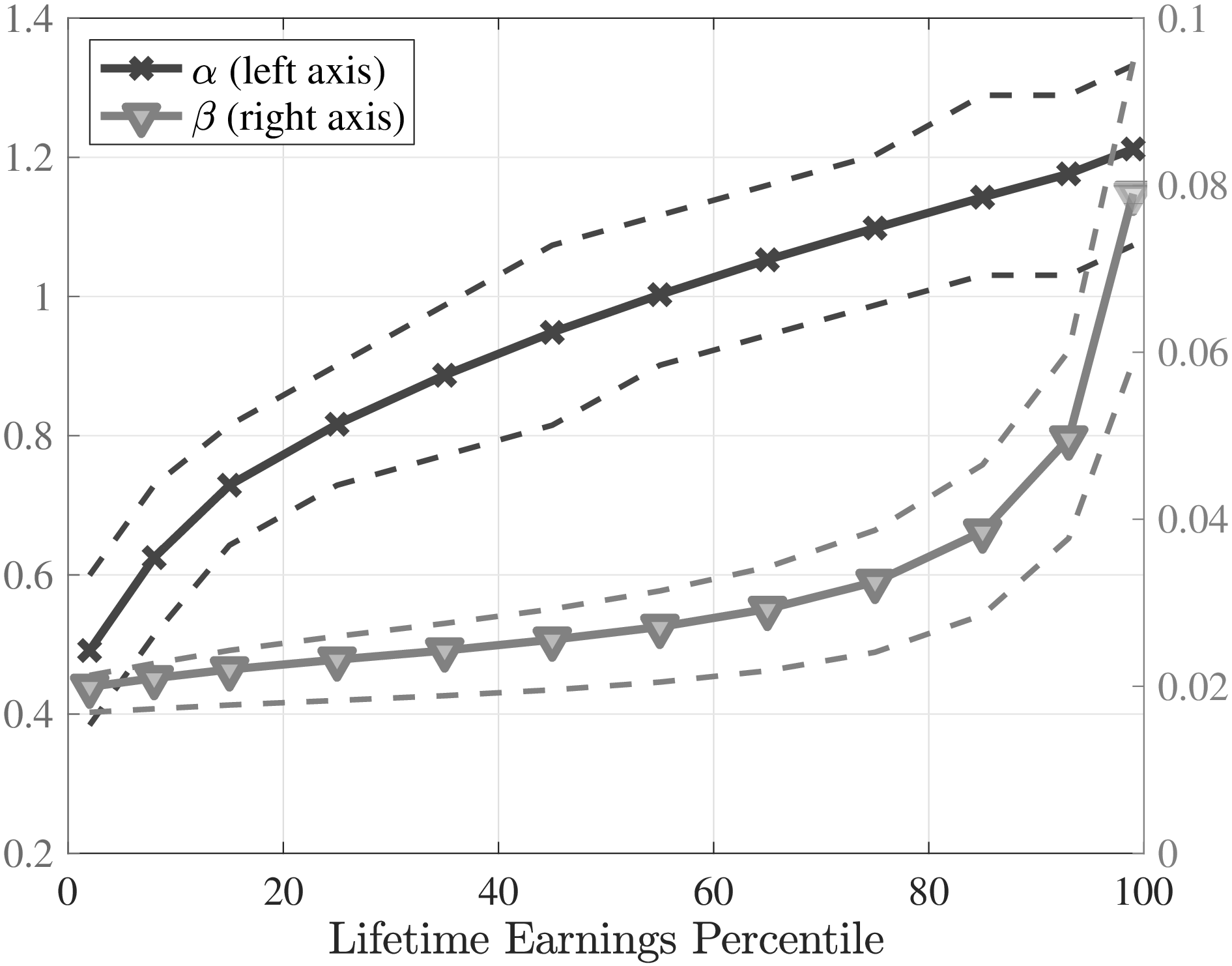

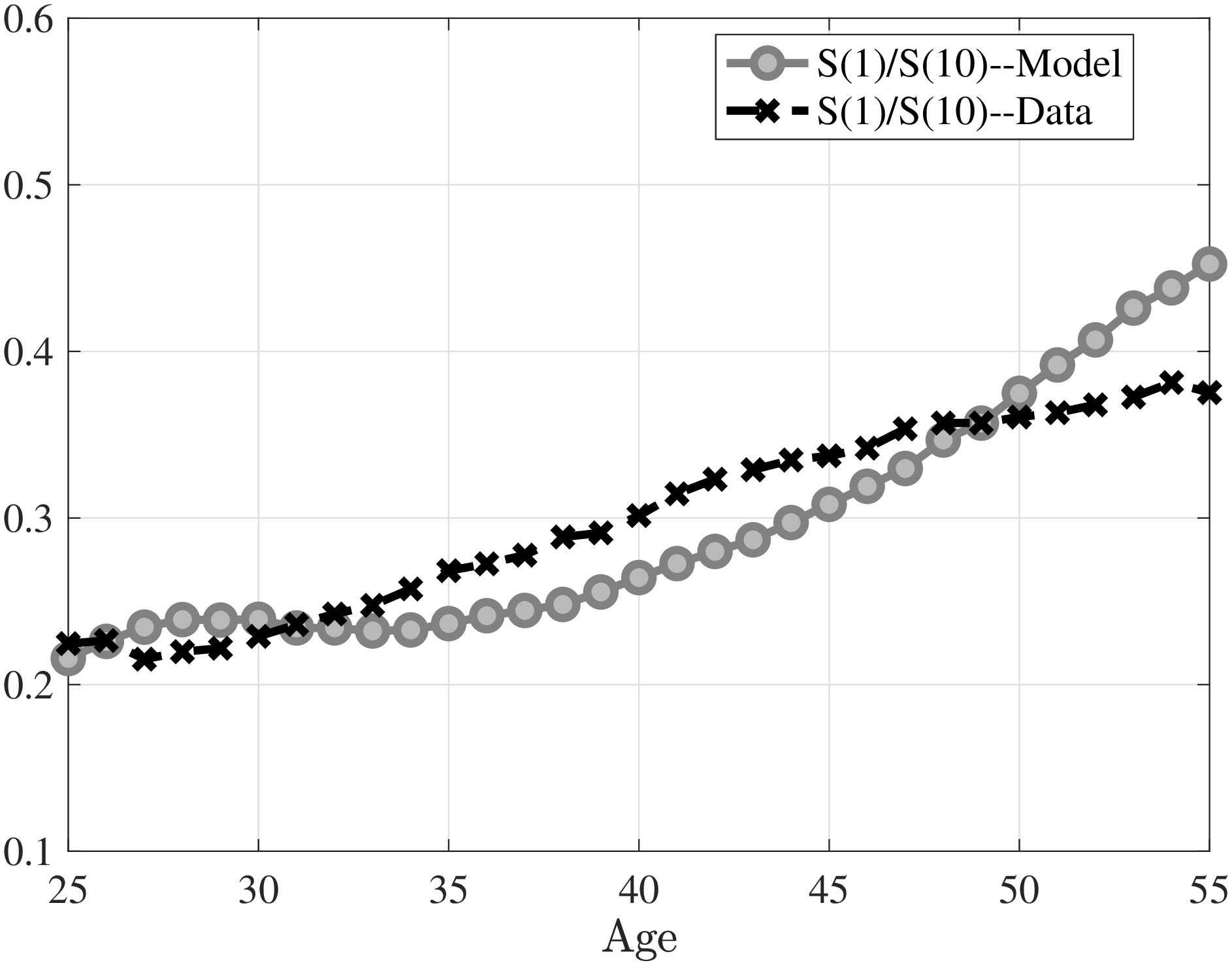

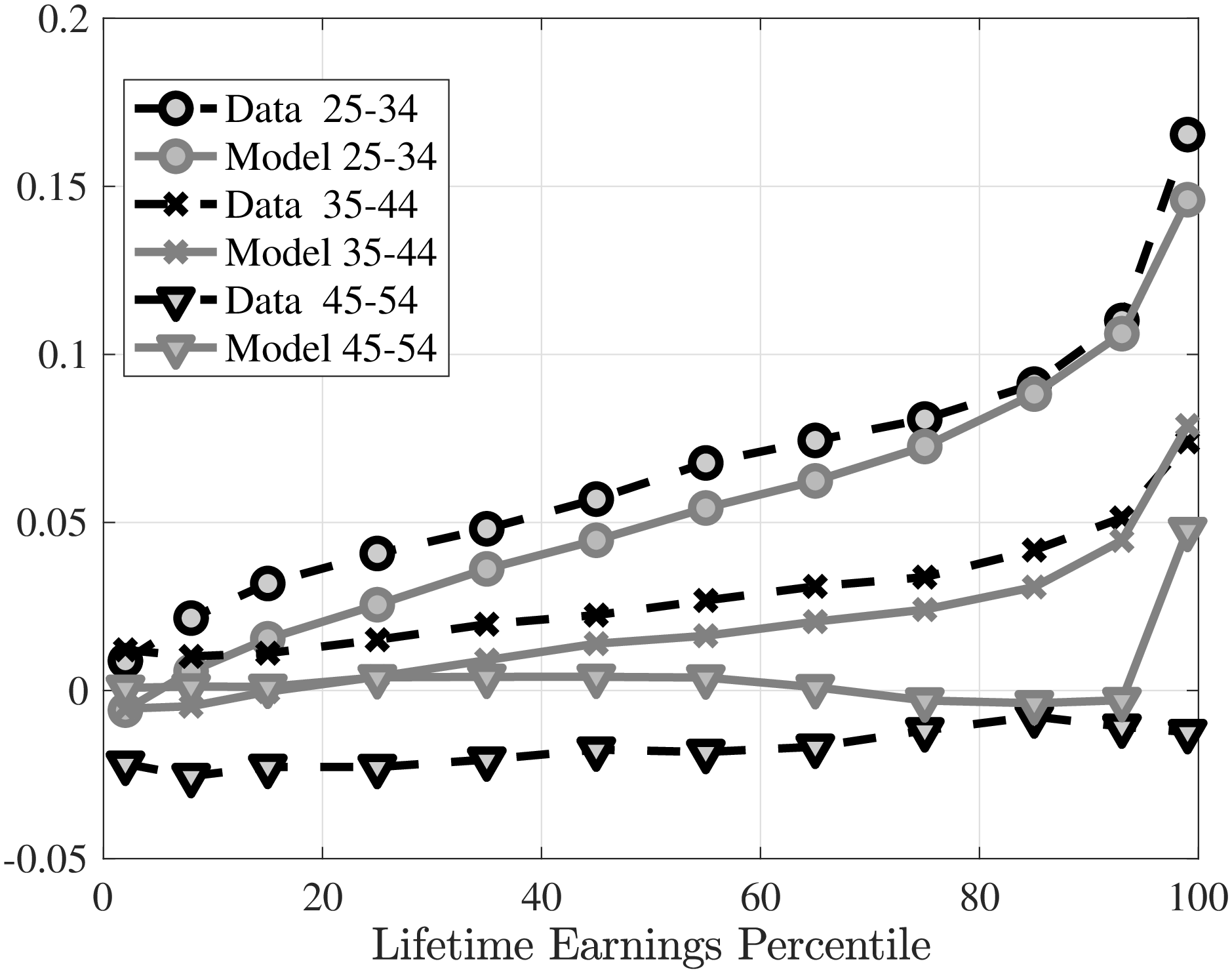

Notes: The left panel shows the mean of the distributions of \(\alpha\) and \(\beta\) by LE groups. Both distributions have been demeaned to have mean zero in the overall distribution. The right panel shows the ratio of incomes earned by the top 1% earners \((S(1))\) relative to the top 10% earners (\(S(10\))).

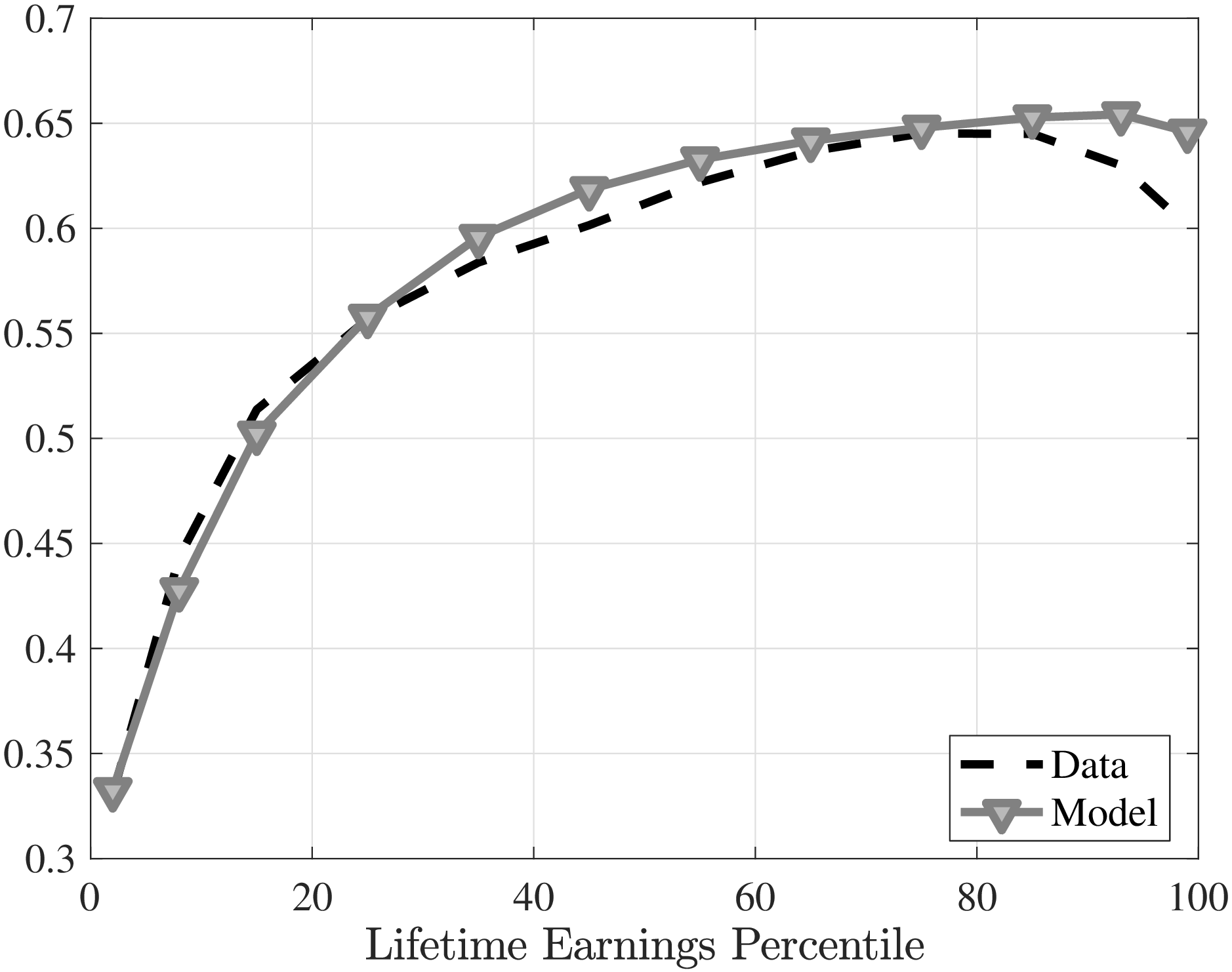

Distribution of \(\alpha\) and \(\beta\). We start by investigating the heterogeneity in permanent ability \(\alpha _{i}\) and the returns to experience \(\beta _{i}\) (Figure 5a). \(\alpha\) increases almost linearly throughout the LE distribution. Top LE individuals have an \(\alpha\) that is more than 60 log points larger than that of those at the bottom. Moreover, there is a sizable variation within each LE group. The interquartile range (dashed lines in Figure 5a) is around 10 log points. Together with this, the standard deviation of \(\alpha\) in the entire population is \(0.25\). Return to experience, \(\beta\), also increases with LE—not surprising given its positive correlation with \(\alpha\) of \(\rho _{\alpha \beta}=0.44\)—however with a different shape: \(\beta\) is relatively flatter in the bottom two-thirds and increases steeply towards the top.27 Clearly, this variation of \(\beta\) by LE is dictated largely by the shape of its distribution, which is assumed to be Pareto to match the average earnings growth differences of job stayers (Figure 2c).

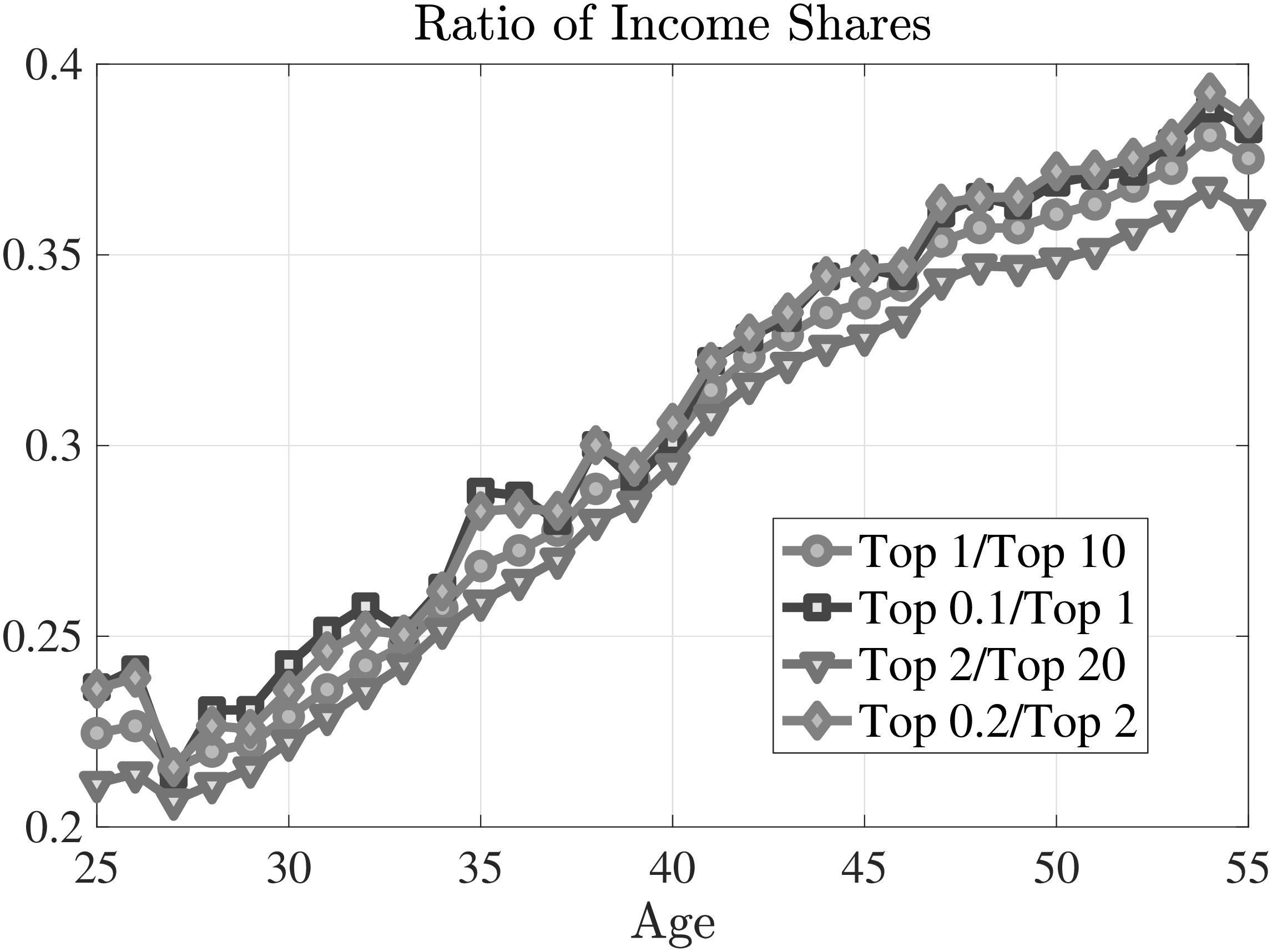

The Pareto distributed \(\beta\), along with a Pareto firm productivity distribution, implies that earnings distribution exhibits power law throughout the life cycle as in the data (Figure A.2). While not targeted in the estimation, the model tracks the relative earnings share of the top 1% in the top 10% fairly well from age 25 to 50, after which the relative share in the model increases faster, driven by the growing importance of the return heterogeneity (Figure 5b). Note that typical models of top income inequality deliver a Pareto distribution through the accumulation of random returns over long periods of time, therefore, log income is exponentially distributed in the entire population (e.g., see Gabaix et al. (2016); Jones and Kim (2018)). However, the distribution of log income within each age is Gaussian in the random growth setting or in a process with normally distributed “growth types” (see Guvenen et al. (2014a) who also argue that several other features of the MEF data are not consistent with this mechanism of top inequality).

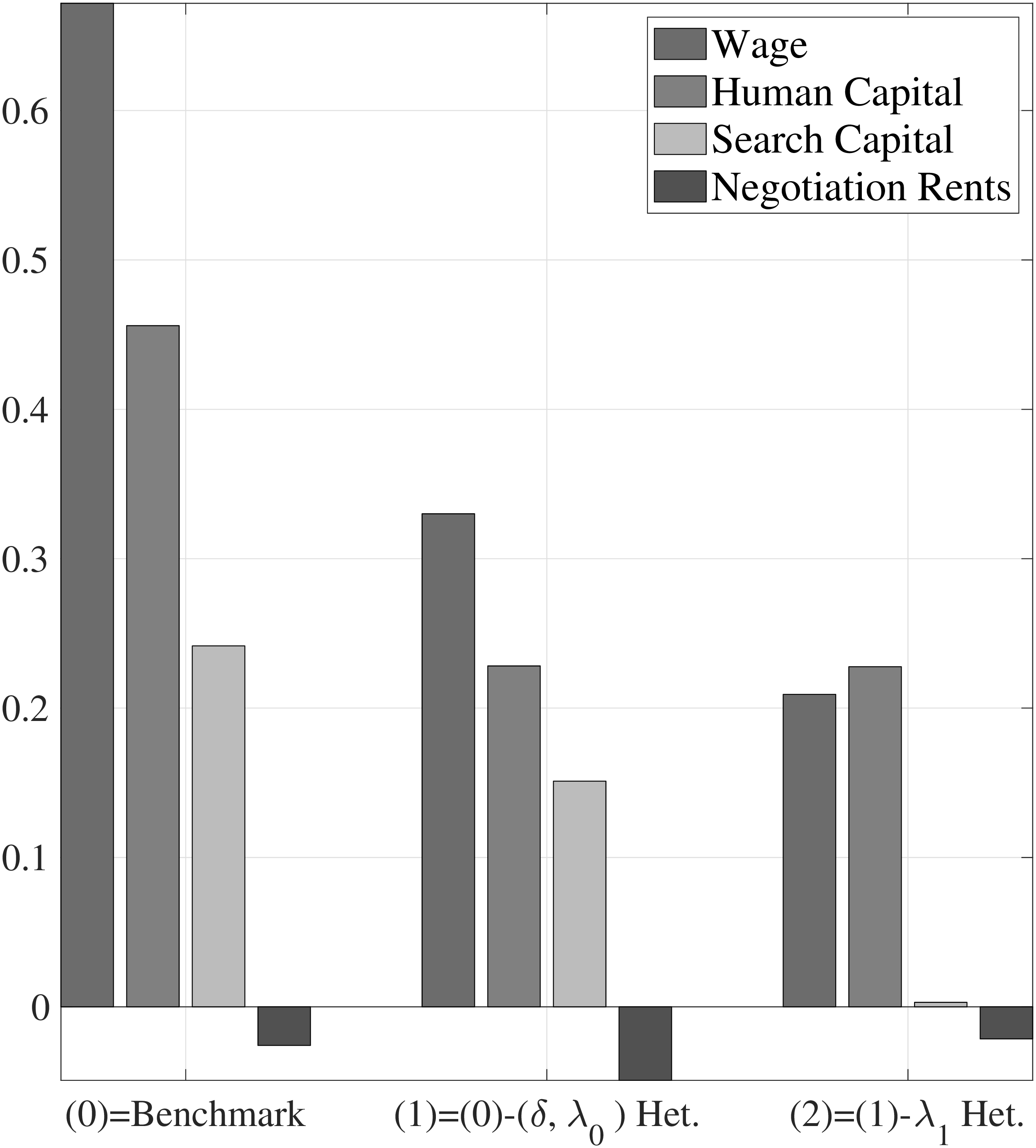

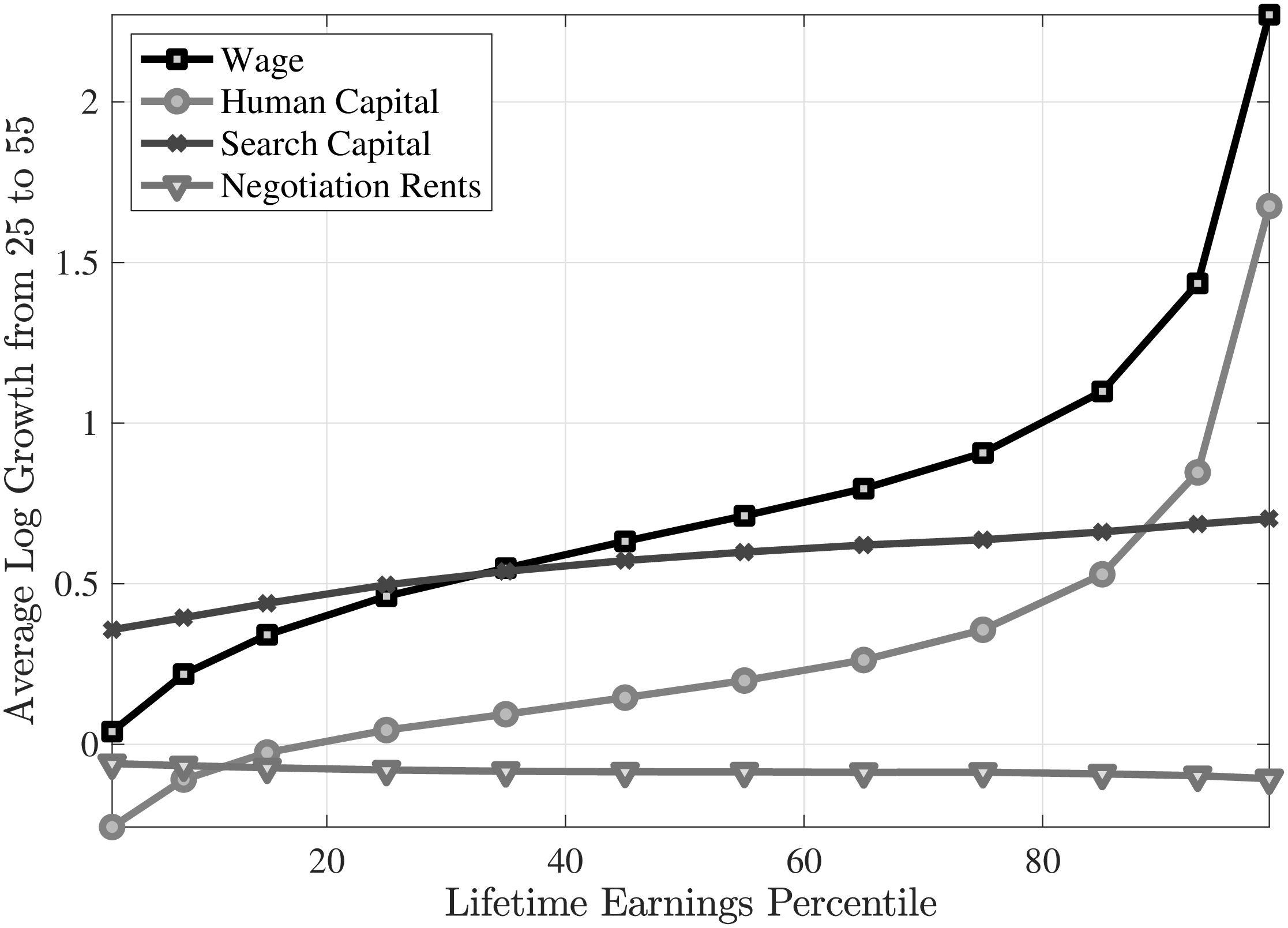

Human capital depreciation. We estimate human capital depreciation to be around \(1.5\%\) on a quarterly basis, larger in magnitude than estimated in Jarosch (2015) using German data. This is not the only channel in our model that contributes to scars from unemployment, which are large and persistent (Von Wachter et al. (2009), Krolikowski 2017). An unemployed worker also loses search capital, negotiation rents as well as the forgone opportunity of accumulating experience.

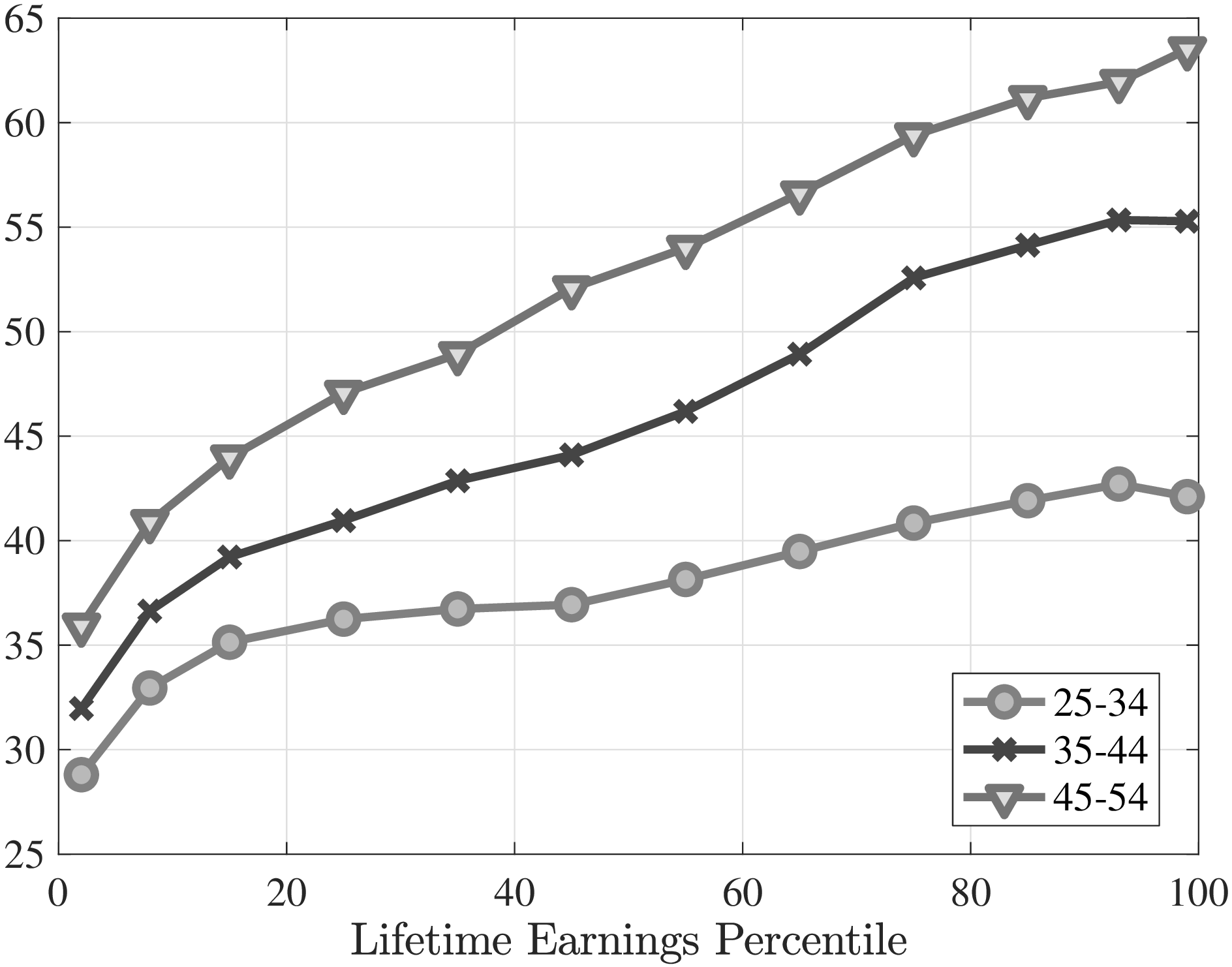

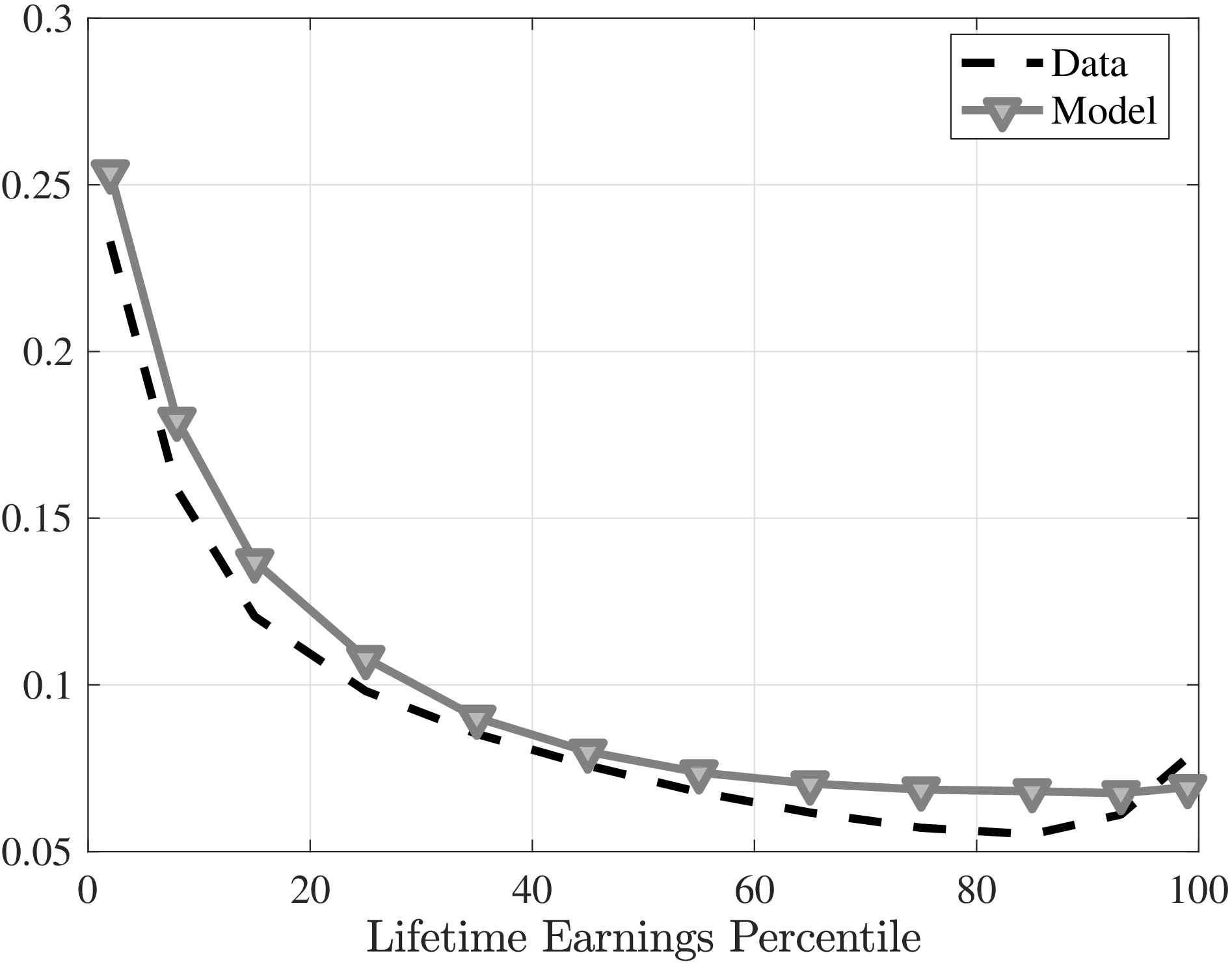

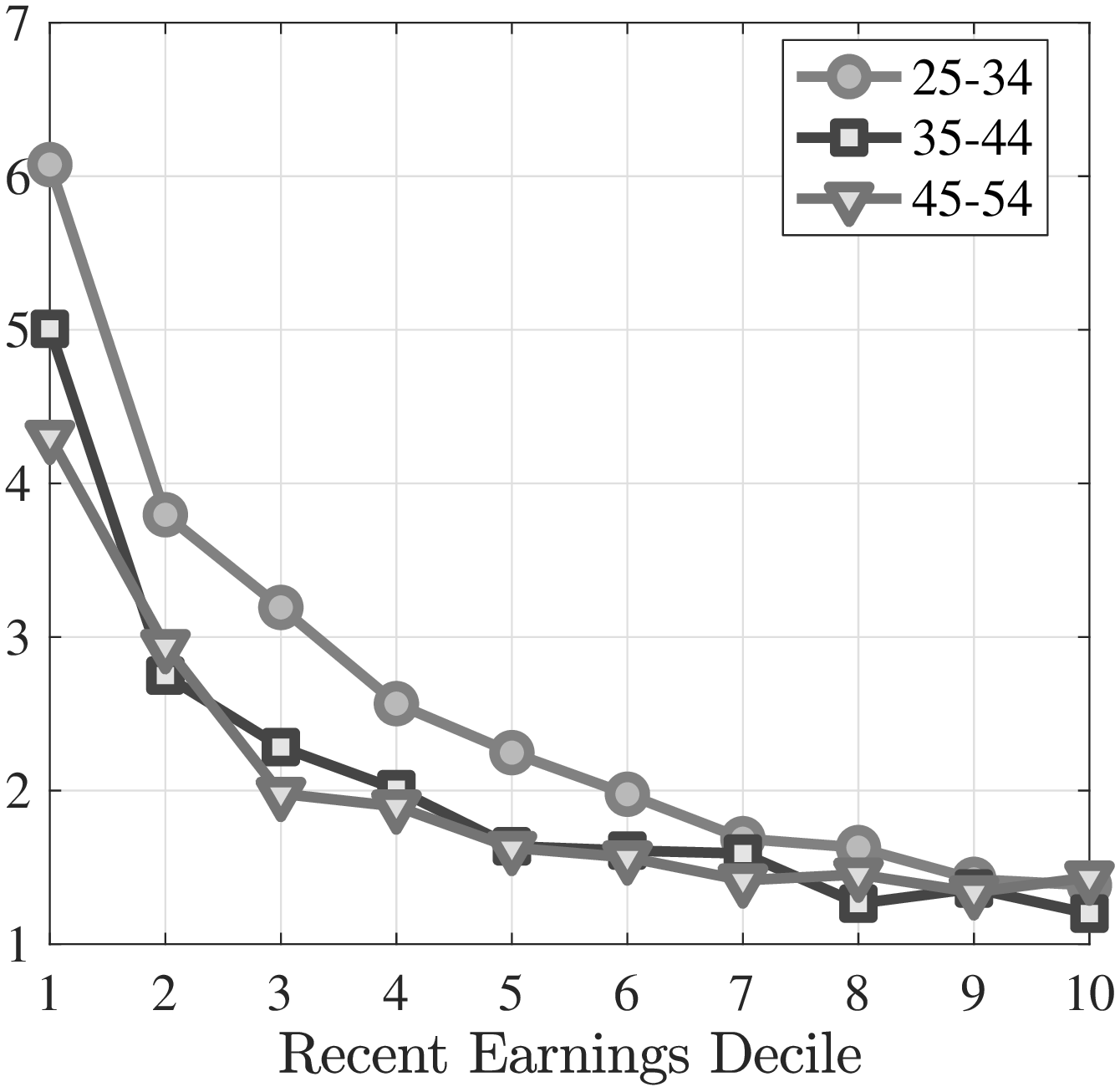

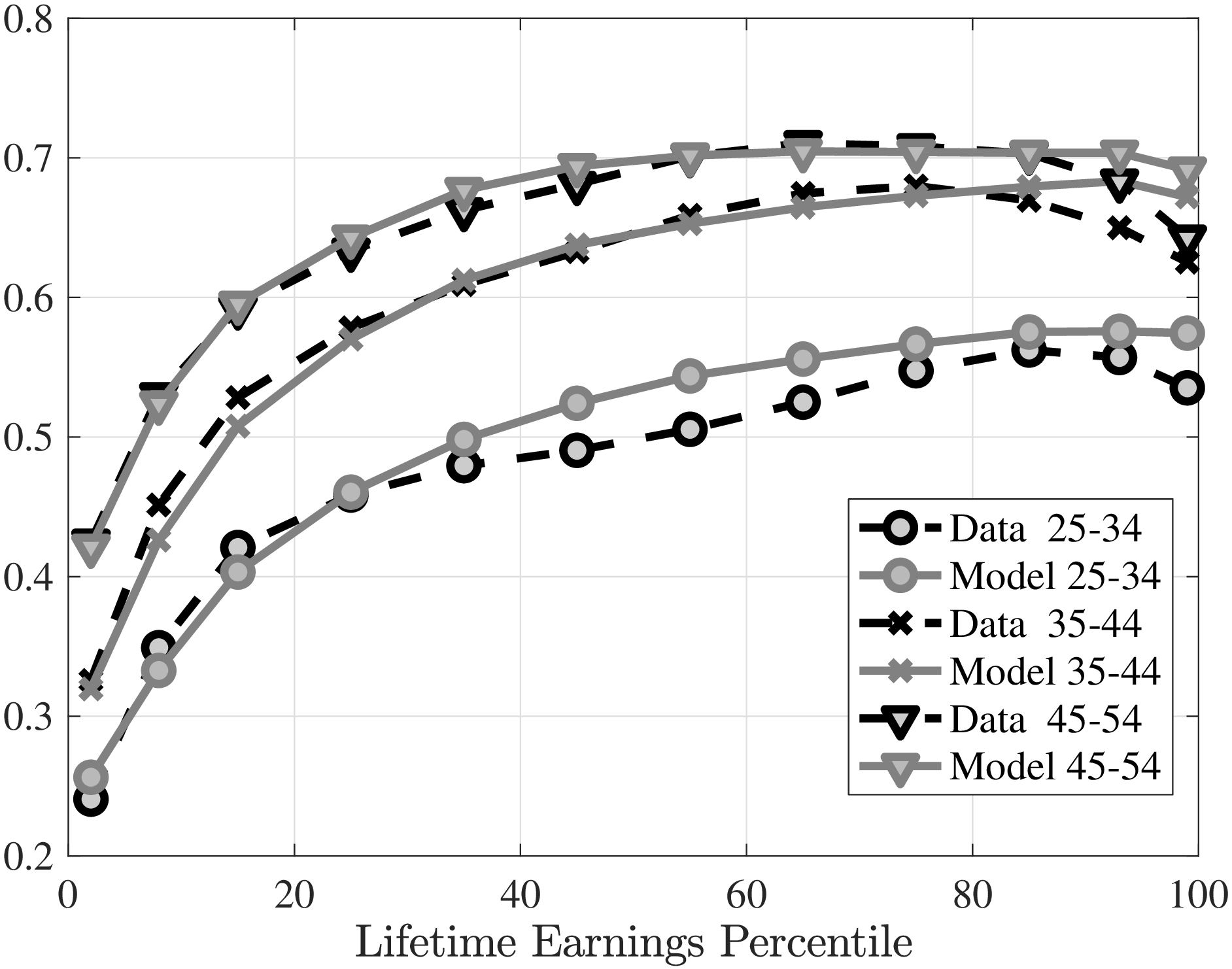

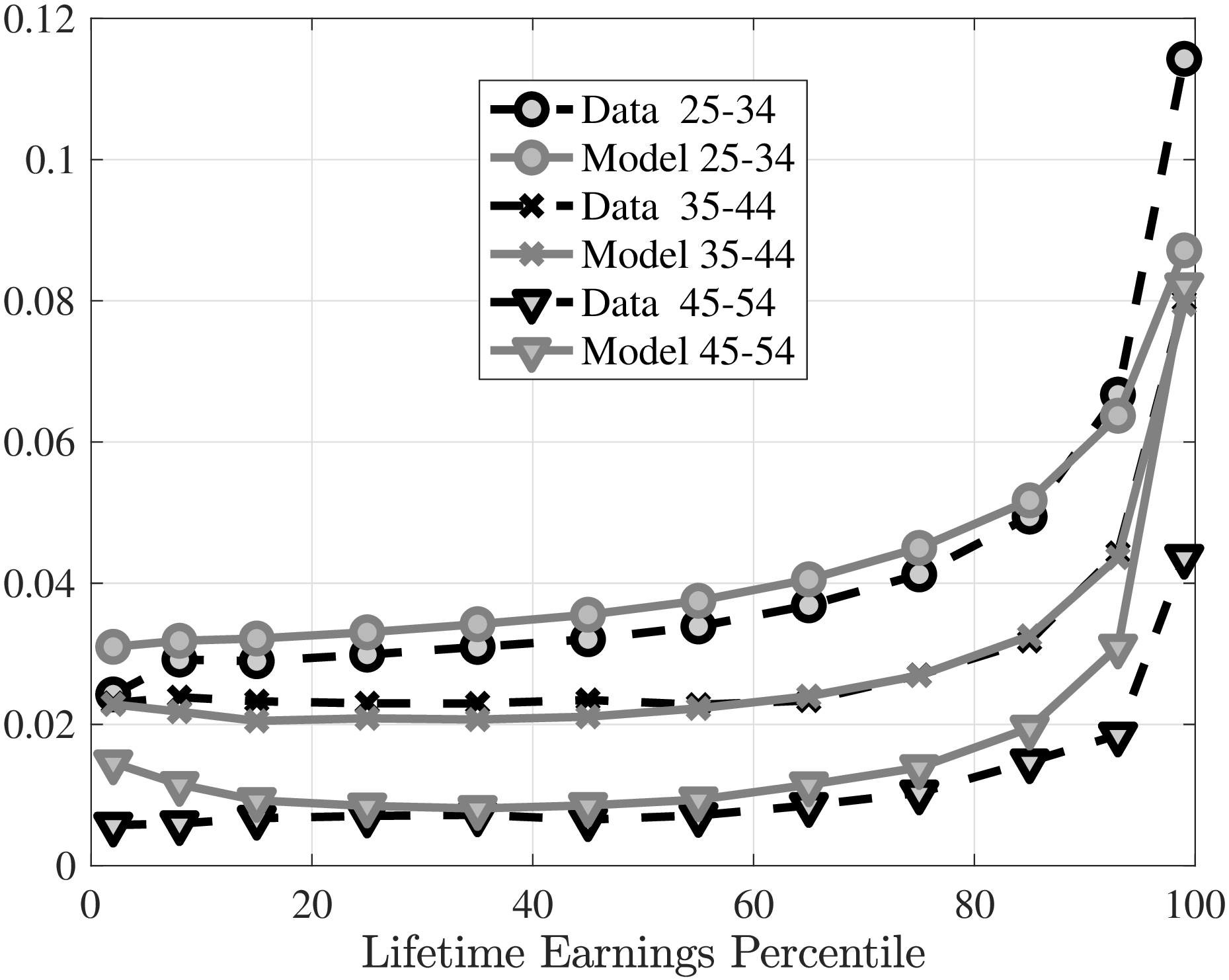

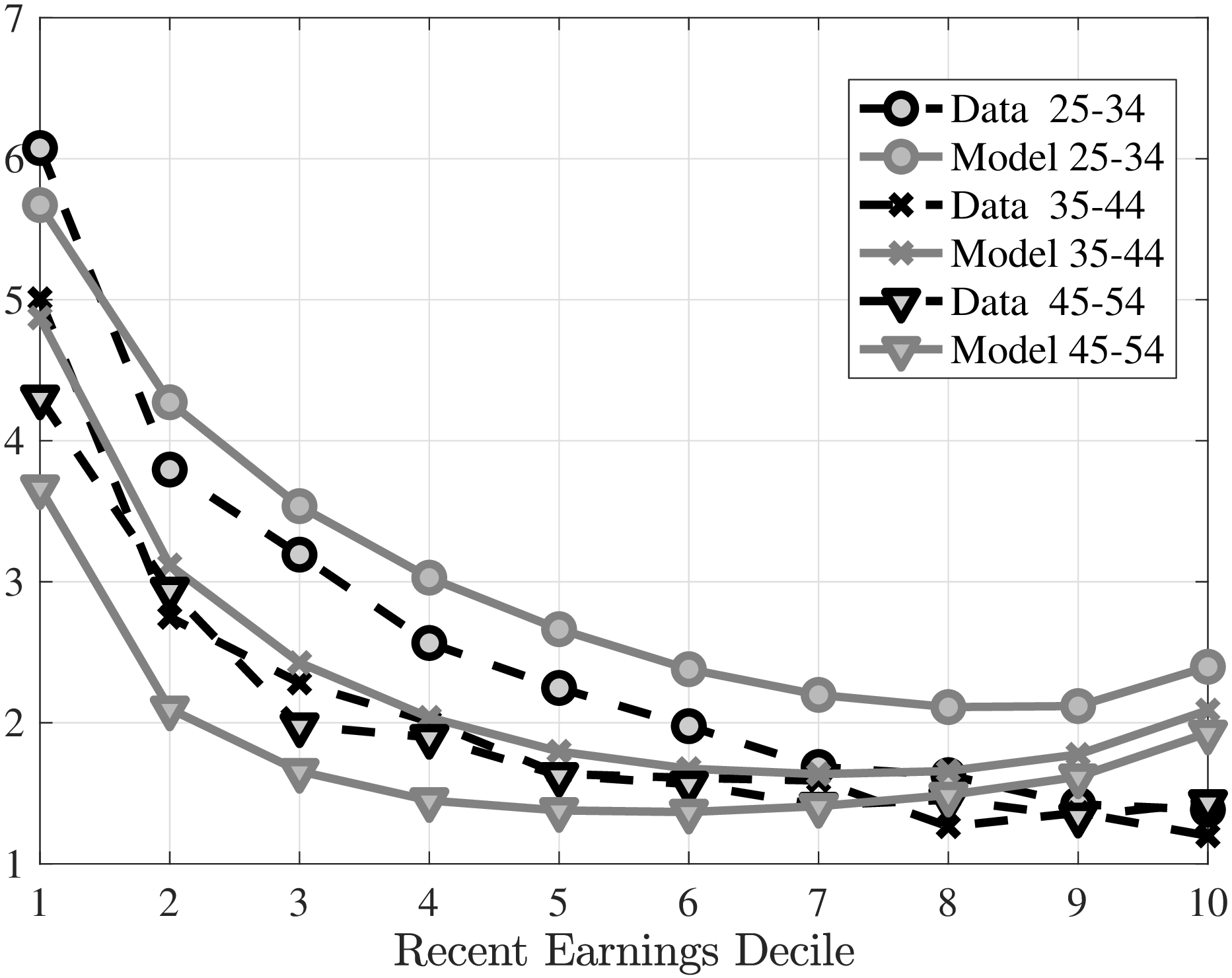

Heterogeneity in flow rates. Figure 6 plots in three panels how the quarterly unemployment risk, the job finding rate, and the contact rate vary with calendar age and LE groups.28 Unemployment risk, \(\delta ^{a}(\alpha)\), declines sharply with lifetime earnings up to median LE and is essentially flat for individuals above the median (Figure 6a). The job loss rate for bottom-LE workers is around four times as high as that for above the median workers. For example, for the youngest age group it declines from around 12% for the bottom earners to less than 3% for median workers. Consistent with previous work, we find the unemployment risk to be significantly higher for younger workers (see Shimer (1998) and Jung and Kuhn 2018). However, the life-cycle variation in unemployment risk is dwarfed by the differences between income groups, which we also observe in the SIPP data (Figure B.1).29 For example, for median workers job loss rate declines from around 3% to less than 2% over the life cycle. Furthermore, even though they see a significant decline in their job loss rate, bottom-LE workers never achieve the job stability above-median workers enjoy.

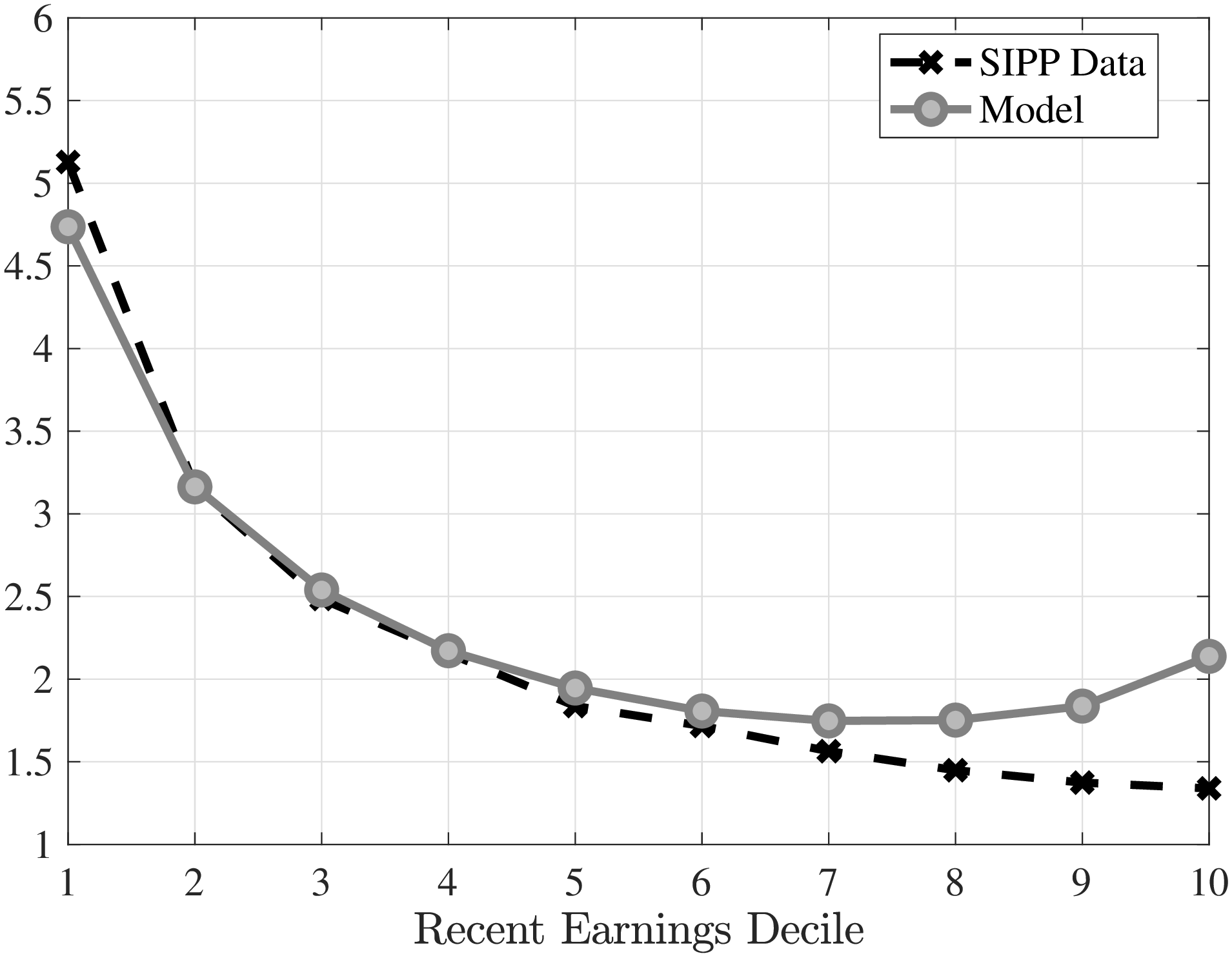

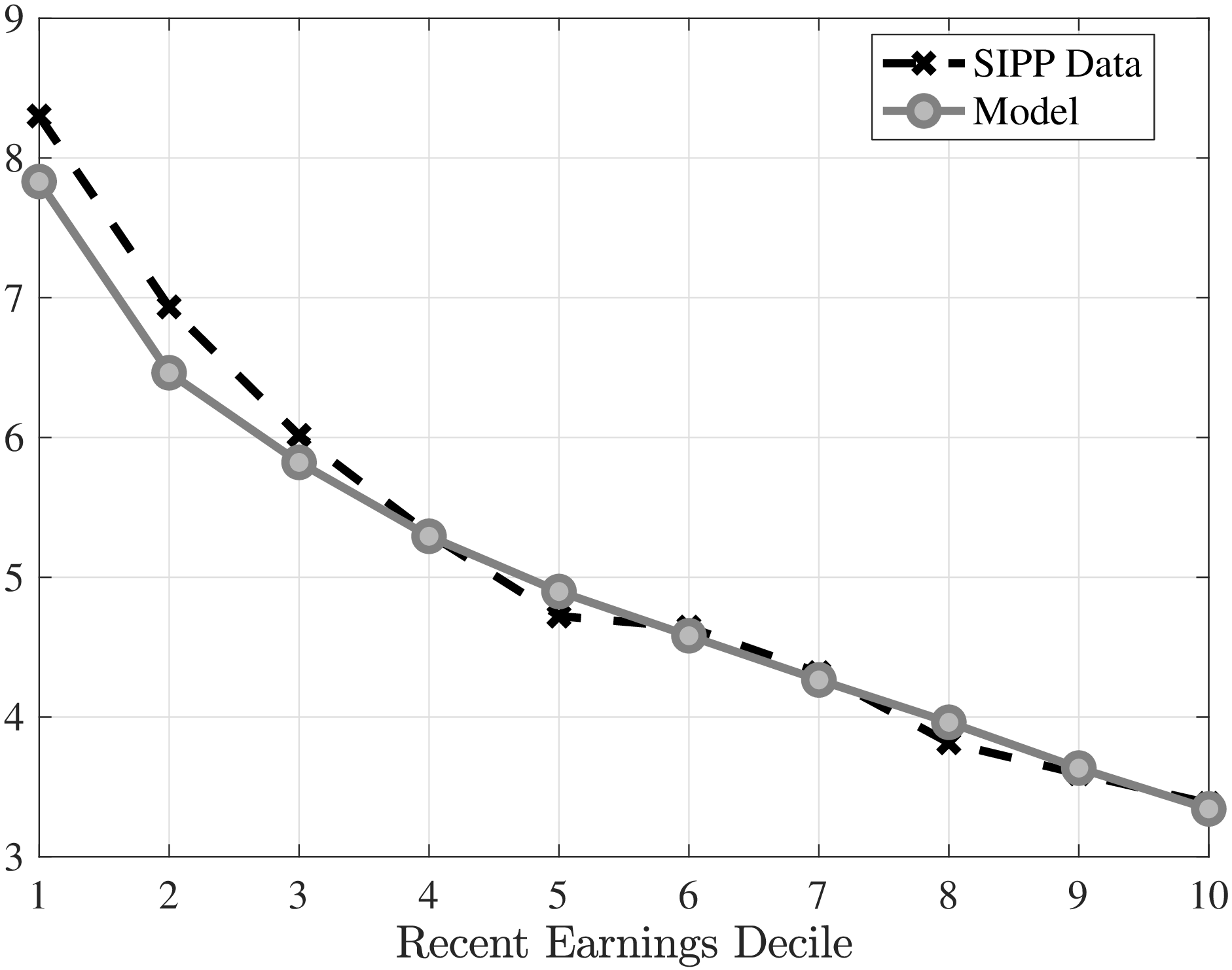

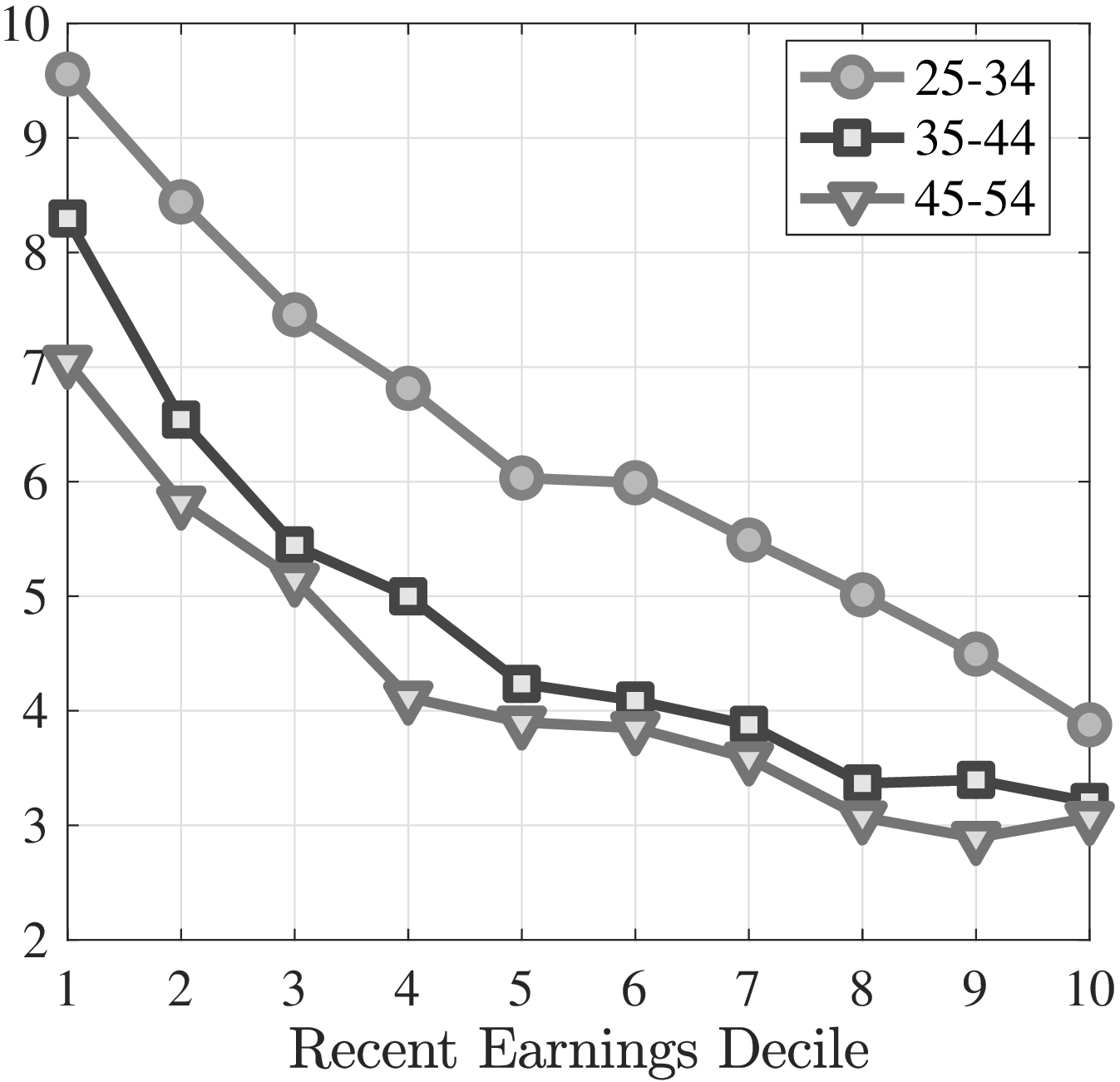

Given the annual nature of the SSA data, we cannot directly test these estimates. Instead, we investigate how the model fits the evidence on heterogeneity in job flow rates from the high-frequency SIPP data. SIPP contains monthly observations in overlapping panels with length between 2.5 and 4 years.We select a sample of males (ages 25–55) with strong labor force attachment (see details in Appendix B). We rank them into 10 equally sized deciles within each age group (25–34, 35–44 and 45–55) based on their recent earnings (RE) over the past three years. Next, we compute the EU, UE, and EE transition rates for each group over the next four months. We also follow the exact same sample construction in the model-generated data. Figure 6b shows how the unemployment risk varies with recent earnings in the SIPP data averaged over the life cycle along with its model counterpart (for separate age groups see Figure D.7). While not explicitly targeted in the estimation, the model captures remarkably well the extent of variation in the data, except for the top decile, where there is a slight uptick in the model-based EU rate but not in its empirical counterpart.

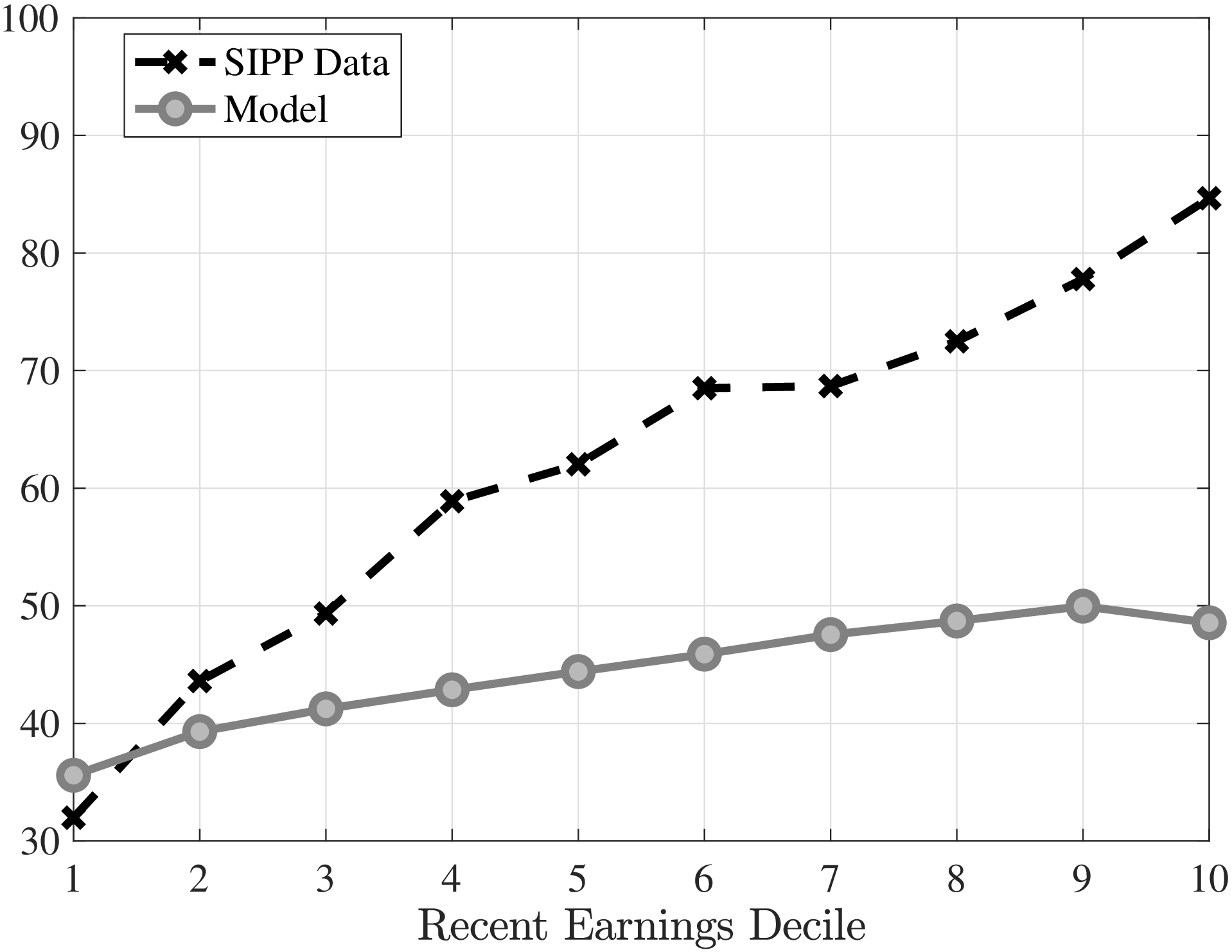

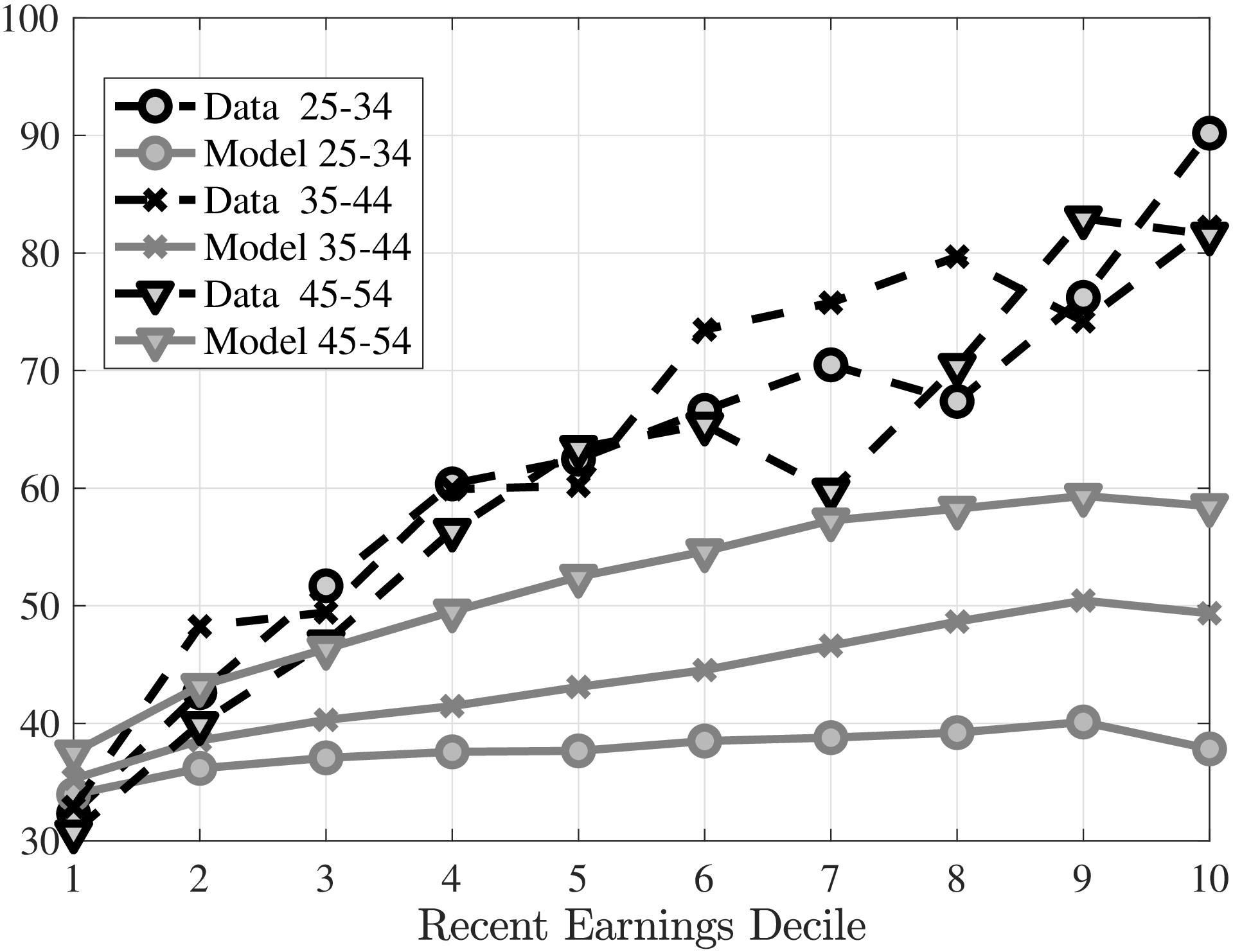

We estimate the job finding rate to be increasing with LE and age (Figure 6c). For example the quarterly job finding rate increases from around 30% at the bottom for workers ages 25–34 to above 60% at the top for workers ages 45–54. These estimates imply that the youngest bottom LE workers stay unemployed for around 3 quarters, compared to less than 2 quarters for the oldest top LE individuals.30 Coupled with an especially high unemployment risk for low LE workers, these estimates imply large differences in actual experience over the life cycle (Figure 9b). In particular, quarters worked over the working life range from 90 for low LE individuals to 120 at the top, which then have implications for earnings growth differences that we discuss later. The increasing job finding rate across the income distribution is qualitatively consistent with the evidence from the SIPP (Figure 6d), however, it does not increase as much as the data.31 There is also almost no age variation in the data in job finding rates, whereas the model estimates are systematically higher for older workers.

We estimate that 12.5% of unemployed workers are recalled back by their last employer (\(\lambda _{r}=0.125\)). This recall probability is lower than the 40% measured in Fujita and Moscarini (2017) for the US. They measure recalls directly using survey data from the SIPP, whereas we infer them indirectly to match the left tail of the earnings growth distribution of job stayers.

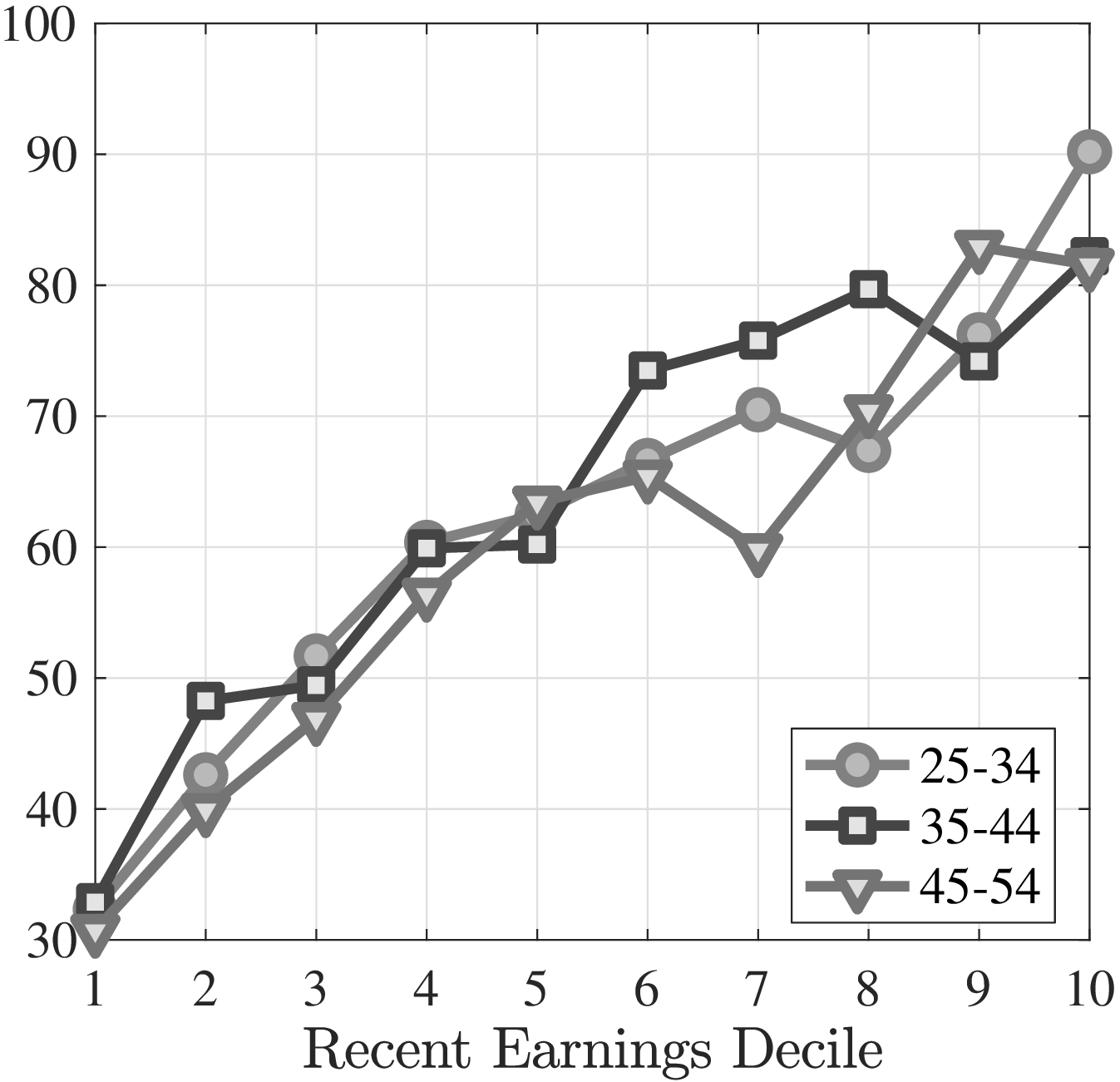

Turning to the contact rate for employed workers, we find this to be increasing with lifetime earnings and age, with a range between 25% and 55% (Figure 6e).32 While the increasing contact rate with LE and age seems contradicting with a declining job-to-job transition rate by RE and age in the SIPP data, the model actually captures both of these patterns well endogenously (Figures 6f and D.7).33 This is because high LE and older workers get more offers but they work for high-productivity firms that are hard to poach from. Therefore, they reject most of the contacts, whereas low LE or younger workers make EE switches more often with fewer offers.

To validate this finding, we analyze data from the SCE, which is a monthly, nationally representative survey of roughly 1,300 individuals that asks respondents about their expectations about various aspects of the economy as well as their employment status, prior work history and job search behavior (see Faberman et al. (2017) for more details). Importantly for our purposes, it asks about the number of employer contacts and job offers received. To keep the analysis similar, we take a sample of employed respondents between ages 25–55, and group them into five bins based on their wages over the last year. We find that contacts received from other potential employers increase in previous wages and are quite high at the top (Table 1). People in the highest group (workers above the 95th percentile) are contacted around 0.43 times per month versus 0.18 contacts per month for the lowest quartile, consistent with the underlying mechanism in the model. Moreover, inspecting unsolicited contacts, those that were not initiated by the employee, we find much larger differences. For top earners, contacts are almost five times more likely than for those at the bottom (0.43 vs. 0.09, respectively).

| Recent earnings groups | 1-25% | 26-50% | 51-75% | 76-94% | 95+% |

| Total Number of Contacts | 0.18 | 0.18 | 0.13 | 0.26 | 0.43 |

| Unsolicited Contacts | 0.09 | 0.02 | 0.04 | 0.11 | 0.43 |

Notes: Respondents between ages 25-55. Individuals who report 25 or more contacts in the last 4 weeks

are dropped from the sample. We assign zero contacts for those reporting a positive number of

contacts but none corresponding with either (i) an employer directly online or through email, (ii) an

employer directly through other means, including in-person, or (iii) an employment agency or career

center.

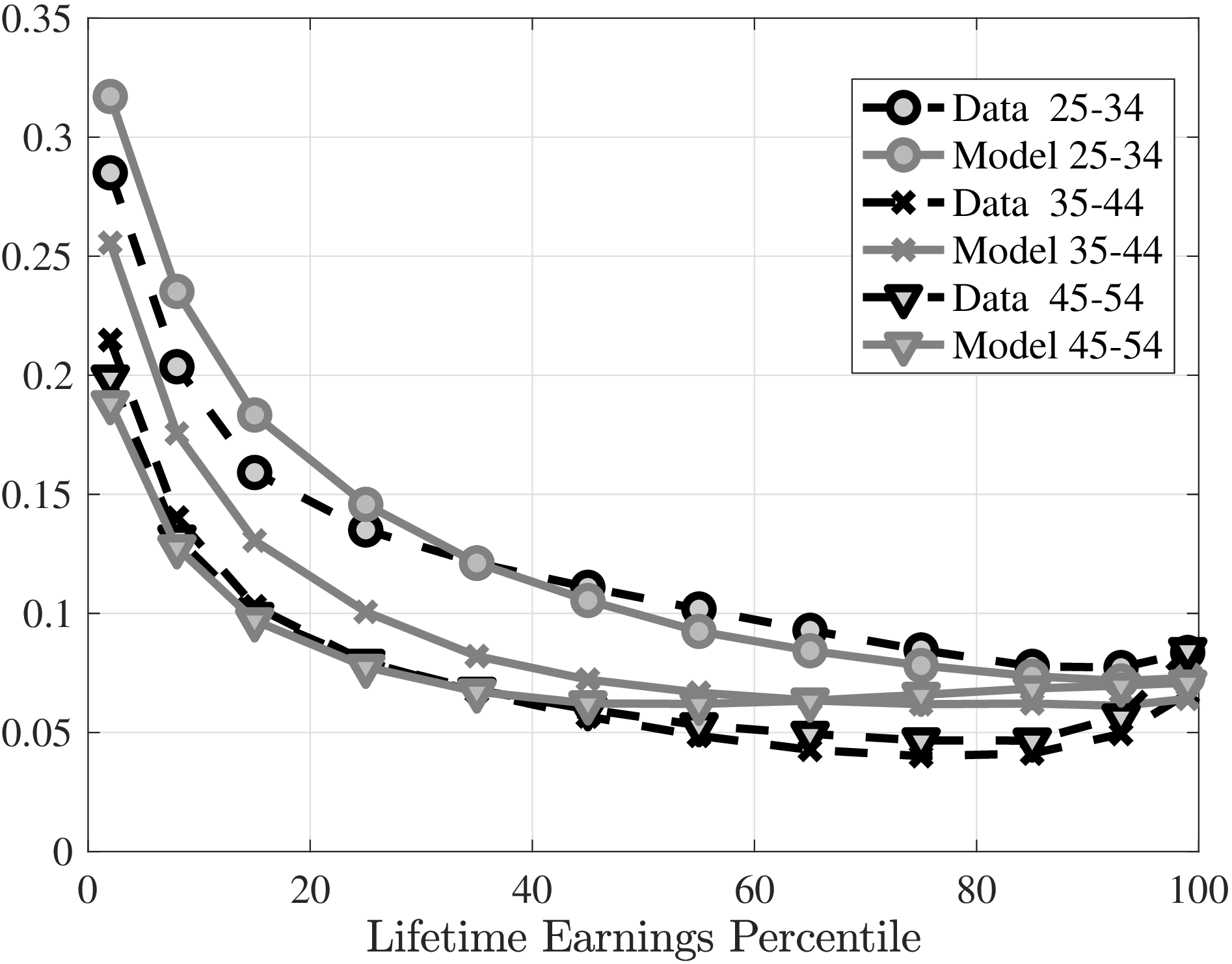

Idiosyncratic shocks. We estimate that the probability of experiencing productivity shocks, \(\pi (\alpha)\), increases with LE from around 5% to 20%. Recall that their distribution is identified from the second-to-fourth order moments of the earnings growth for job stayers. Figure 7 shows that the variance increases above the 20th percentile and kurtosis decreases above the 40th percentile of the LE distribution. These patterns require shocks to be more likely for higher-LE workers, whereas for low LE individuals the earnings dynamics for job stayers are mainly driven by the endogenous job ladder mechanisms, including recalls. This finding is consistent with evidence from Norway that for high earners large earnings changes are mostly driven by wage changes rather than movements in extensive margin of labor hours (Halvorsen et al. (2019)).

5.2 Model’s fit to the data

We now show the model’s performance in fitting the targeted moments. In doing so, we also discuss the economic forces behind the higher order moments of earnings changes as well as earnings growth patterns for job stayers and switchers.

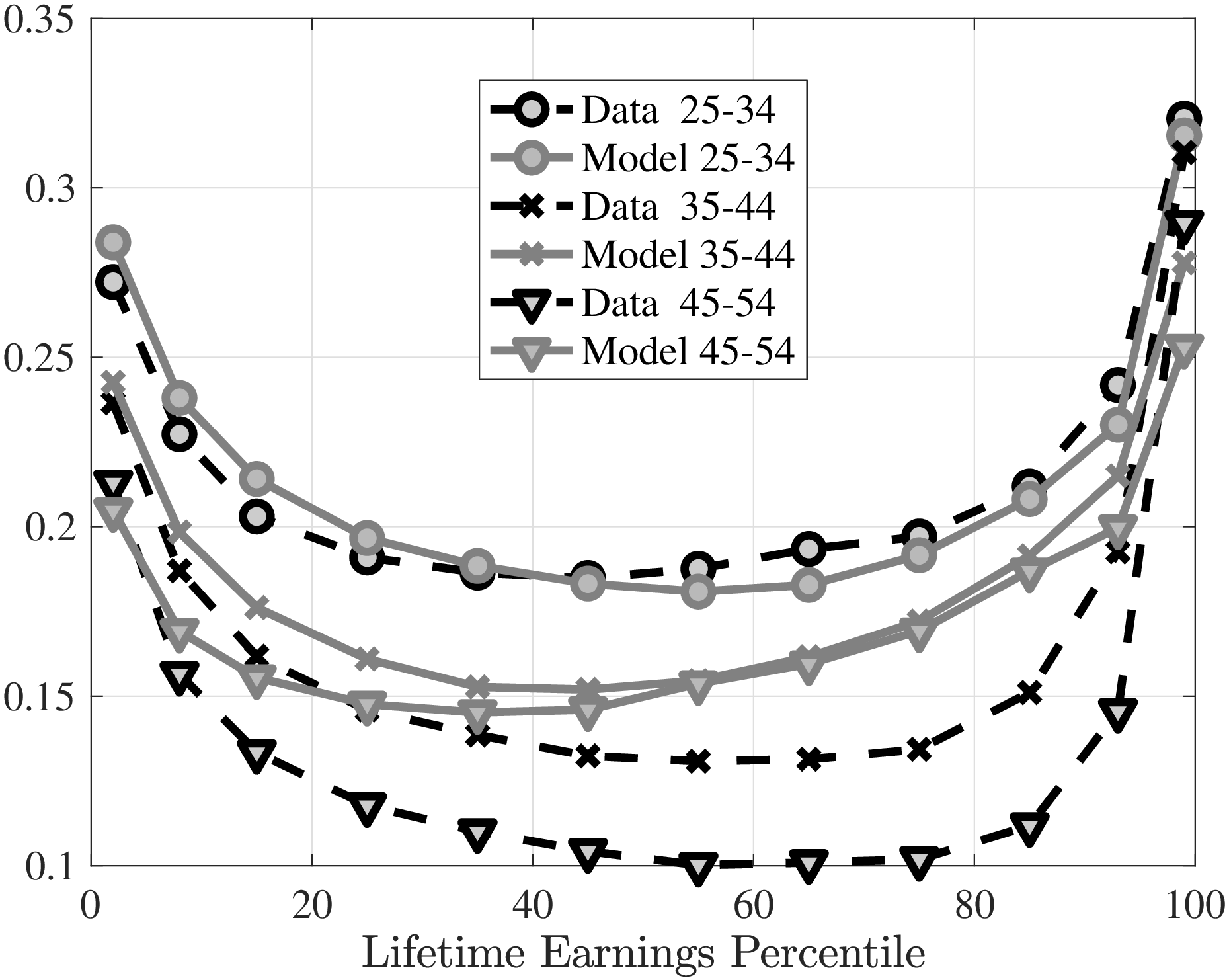

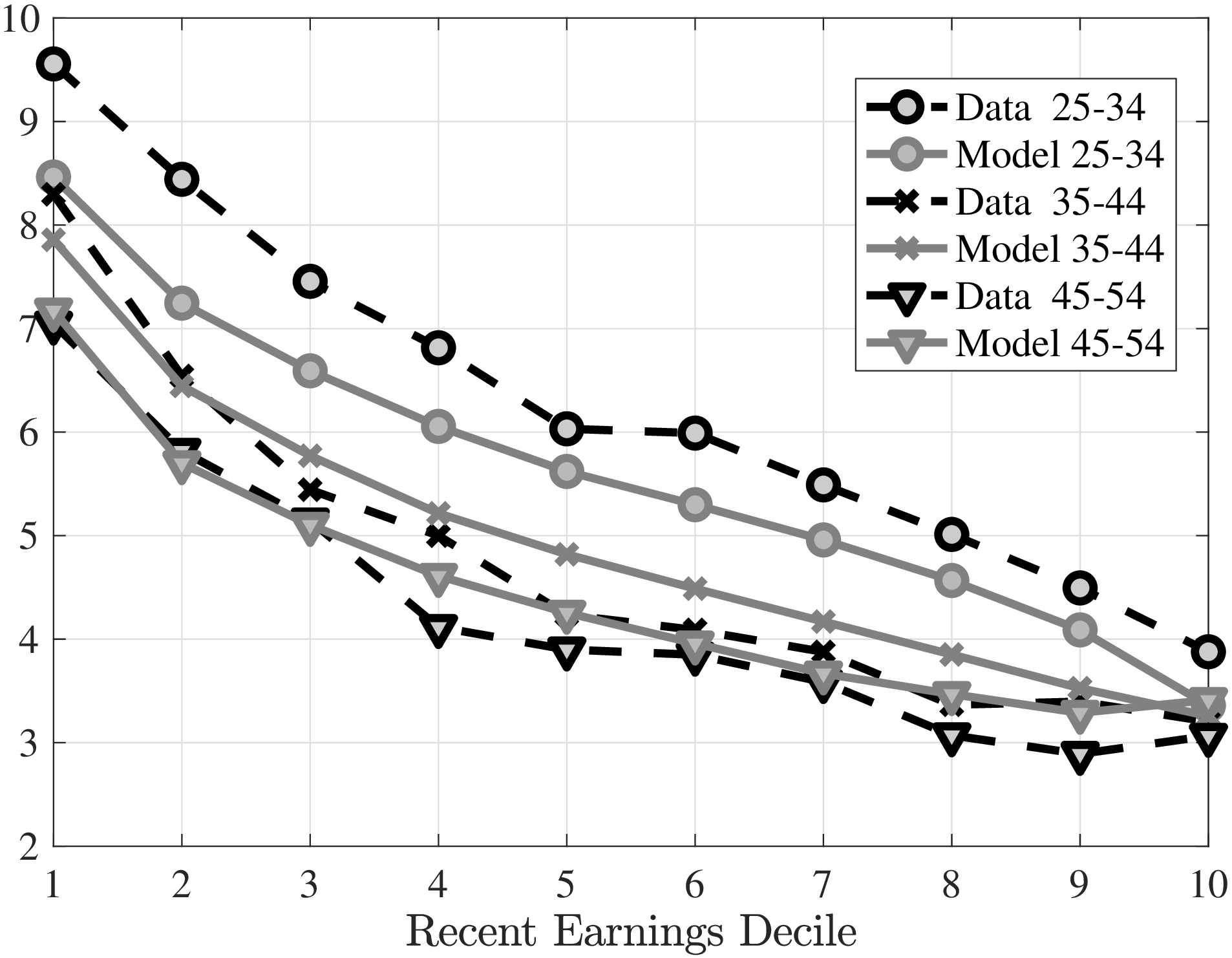

Cross-sectional moments. Figure 7 shows the fit of the model to cross-sectional moments. For the clarity of exposition, we suppress the life cycle variation and plot averages over three age groups. The fit along the life-cycle is shown in Appendix D.3.

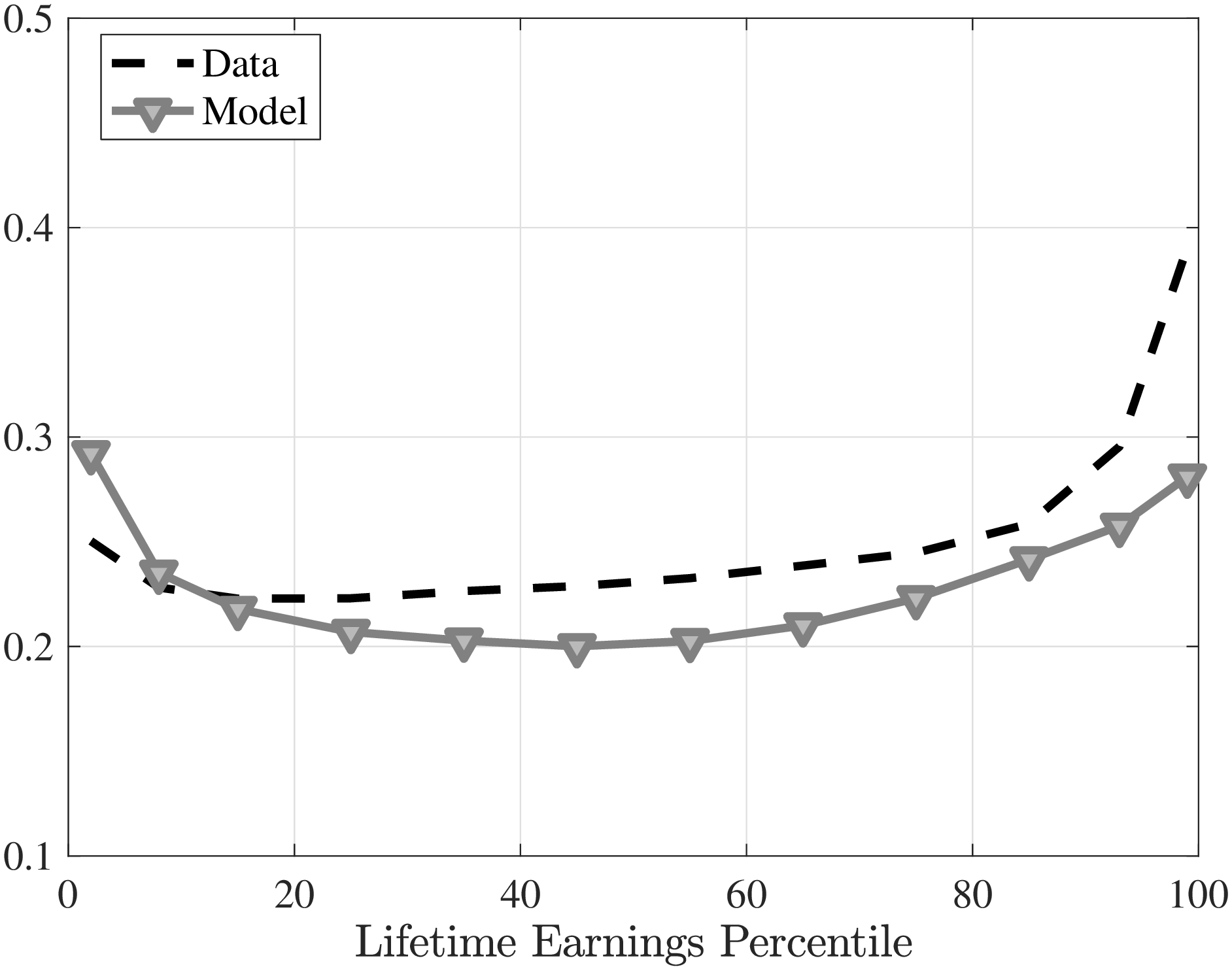

The model captures well the standard deviation of earnings changes for job stayers and switchers (Figure 7a). Both in the data and in the model, job switchers have a higher standard deviation throughout the LE distribution. In the model, big changes to earnings happen when people switch jobs because of a job loss. The declining unemployment risk (Figure 6a) combined with an increasing poaching rate (Figure 6e) implies that a higher share of job switchers at the bottom go through unemployment as opposed to direct job switches, and explains why the standard deviation is higher at the bottom compared to the rest of the distribution. The profile flattens out because there is much less variation in the unemployment risk above the median.

For job stayers, earnings changes are driven by job loss followed by a recall, an outside offer that leads to renegotiation, and idiosyncratic productivity shocks. Due to their high job loss rates, the share of recalls is highest at the bottom, which tends to push up the standard deviation at the bottom. As we move to the right along the LE distribution, unemployment risk fades, the prevalence of outside offers increases, and a larger share of such offers result in the worker staying with the same employer, and getting a large raise (Figures 6e and 6f). Moreover, idiosyncratic shocks become more frequent and contribute to the increasing standard deviation for job stayers above the median.

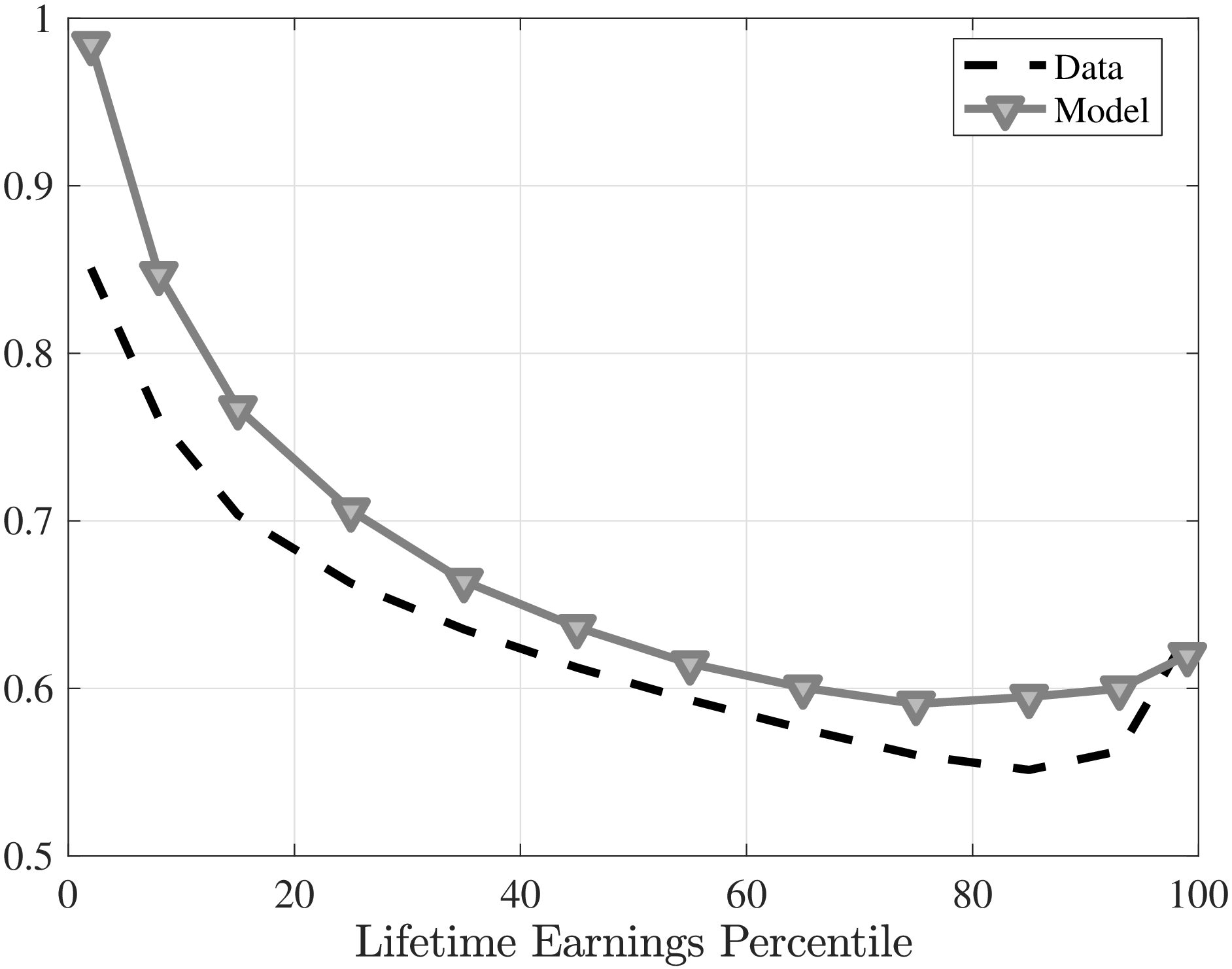

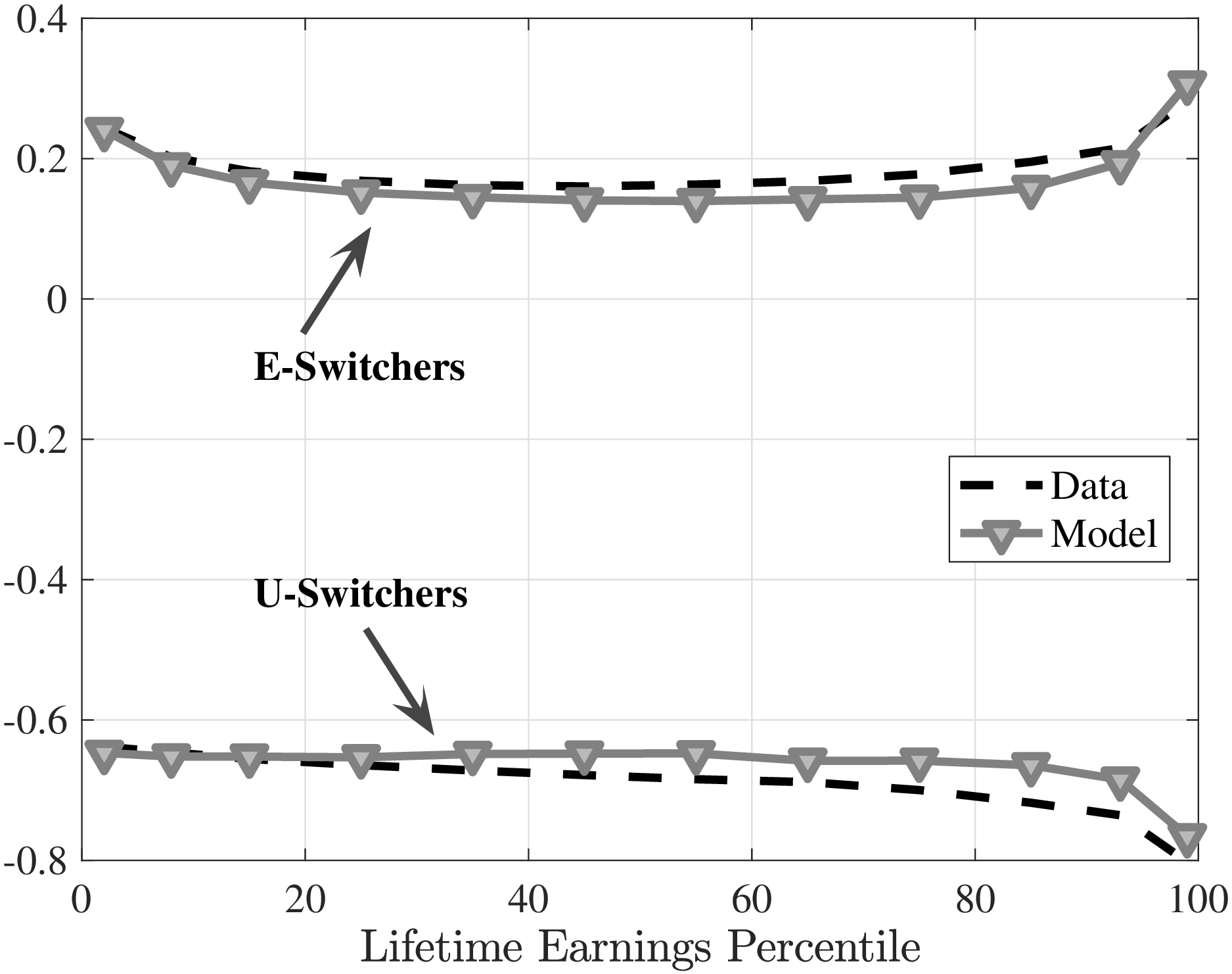

Turning to skewness, we find that the model captures well the essential features of the data (Figures 7c and 7d). First, earnings changes are negatively skewed for both job switchers and stayers. For switchers, the negative skewness is mostly a result of flows into unemployment, which result in the worker losing the position on the job ladder and human capital depreciation throughout the spell of unemployment. The decreasing profile of skewness (increasing negative skewness) is a result of two offsetting forces. On the one hand, human capital depreciation is stronger for low LE individuals due to longer unemployment durations, pushing skewness down at the bottom. On the other hand, job loss is less frequent but more costly for high LE individuals as they have more search capital and negotiation rents to lose. The latter force dominates and causes the skewness of earnings changes to be more negative for job switchers among high LE individuals.

As for job stayers, recalls generate large earnings declines within the same firm. In the absence of recalls, the model cannot generate a negative skewness for job stayers. As we move to the right of the LE distribution, the left tail shrinks as temporary layoffs become less frequent. The right tail expands, because outside offers arrive more often and are more likely to result in wage renegotiation. Both forces combined result in a milder negative skewness for job stayers at higher LE percentiles.

The model is quite successful in matching the extent of kurtosis and its variation over the LE distribution. Infrequent events that lead to large changes, such as outside offers and unemployment spells followed by recalls, are the leading sources of excess kurtosis for job stayers. In fact, they are so strong that without idiosyncratic shocks, earnings changes would be a lot more leptokurtic. The idiosyncratic shocks, despite being leptokurtic themselves, help the model bring down the kurtosis of job stayers closer to values in the data. Earnings changes of job switchers are also leptokurtic in the model and the data, but to a lesser degree compared to job stayers.

Finally, we investigate the model’s fit on cross-sectional moments along the life-cycle dimension. Figure D.2 shows how the higher-order moments of earnings changes for stayers and switchers vary between three age groups. As in the data, life-cycle variation in the model is less pronounced than the variation between LE groups. Overall, we conclude that the model does fairly well in capturing the essential moments of earnings changes for job stayers and switchers across the LE distribution and over the life cycle.

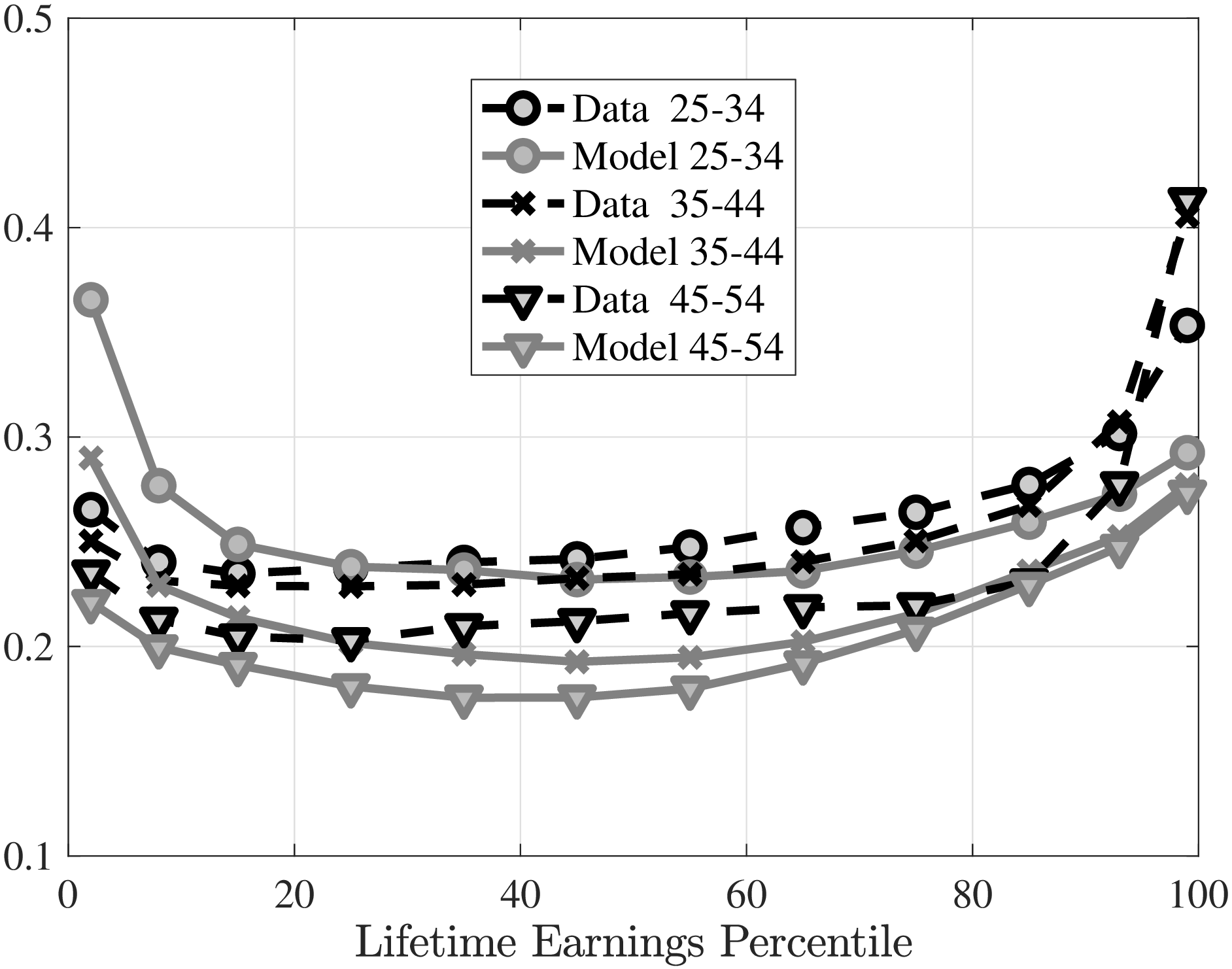

Income growth moments. Next, we study job stayers and switchers. The model reproduces remarkably well the increasing share of job stayers by LE quantile in the data (Figure 8). There are few job stayers at the bottom due to high flow rates into unemployment. The share of job stayers essentially follows the unemployment risk along the LE distribution, increasing up to around the 70th percentile and stabilizing thereafter.

The model also generates overall a realistic average earnings growth for job stayers and switchers throughout the LE distribution (Figure 8b). In particular, there is little heterogeneity among job stayers for the bottom two thirds of the LE distribution, which, as discussed before, is in part due to the relatively flat average profile of returns to experience (\(\beta\)) in each LE group. Earnings growth of job stayers has a component due to human capital accumulation, governed by \(\beta\), and a component due to the job ladder, through outside offers that lead to wage increases on the job. As Figure 5a shows, the former component is basically flat for two thirds of the distribution with a very small positive slope. Yet, the earnings growth of stayers in the model is higher at the low end of the distribution compared to the 20th percentile. This feature has to do with the second component, which is stronger at the low end. This result may seem surprising because bottom LE individuals have the lowest contact rates when employed. However, given their high unemployment risk, employed workers at the bottom tend to also have a lower piece rate as they frequently lose their job before they receive many outside offers and can negotiate a better piece rate. A lower piece rate implies that, conditional on staying with the same firm (which is the group we consider in Figure 8b), an outside offer is more likely to lead to wage renegotiation. Thus, there are two competing forces determining the effect of the job ladder risk at the bottom: a lower contact rate and a higher share of those contacts that lead to wage growth. It turns out that the latter is stronger at the bottom compared to the 20th percentile of the LE distribution.

Turning to job switchers, the model captures well their average earnings growth (Figure 8b). In particular, there is a large variation throughout the LE distribution, ranging from zero at the bottom to 9% at the top. Moreover, consistent with the data, most of this heterogeneity is due to compositional differences among job switchers. The share of E-switchers among all workers decline from 25% to around 5% over the LE distribution (Figure 8c). However, their share among only switchers increases sharply from around 65% at the bottom of the LE distribution to above 80%. These shares are slightly below those in the data but capture remarkably well the variation along the LE dimension. Finally, consistent with the data, there is much less between-group heterogeneity in the earnings growth of E-switchers and U-switchers (Figure 8d).

Recall that being a job switcher or a stayer has limited effects on earnings growth of top LE workers when younger than 44, but it matters quite a bit in the oldest age group (Figure 4). This is because both U-switches become more likely as they get older and, more importantly, average earnings growth for U-switches falls sharply for the oldest top LE workers (Figure A.8). Our model can capture this feature of the data (Figure D.3), thus we are able to investigate it further: Top LE workers have already climbed to the top of the job ladder in the oldest age group so they are less likely to make voluntary E-switches. Therefore, the relative likelihood for U-switches increase dramatically for them. Furthermore, since they are at the higher end of the job ladder, if they make a U-switch (e.g., lose a job), their earnings decline sharply because they lose search capital (a job in a high-productive firm), negotiation rents, and human capital.

Thus, we conclude that the estimated job ladder model captures quite well the key features of the careers of individuals in different parts of the lifetime earnings distribution.

6 Decomposing Lifetime Earnings Inequality

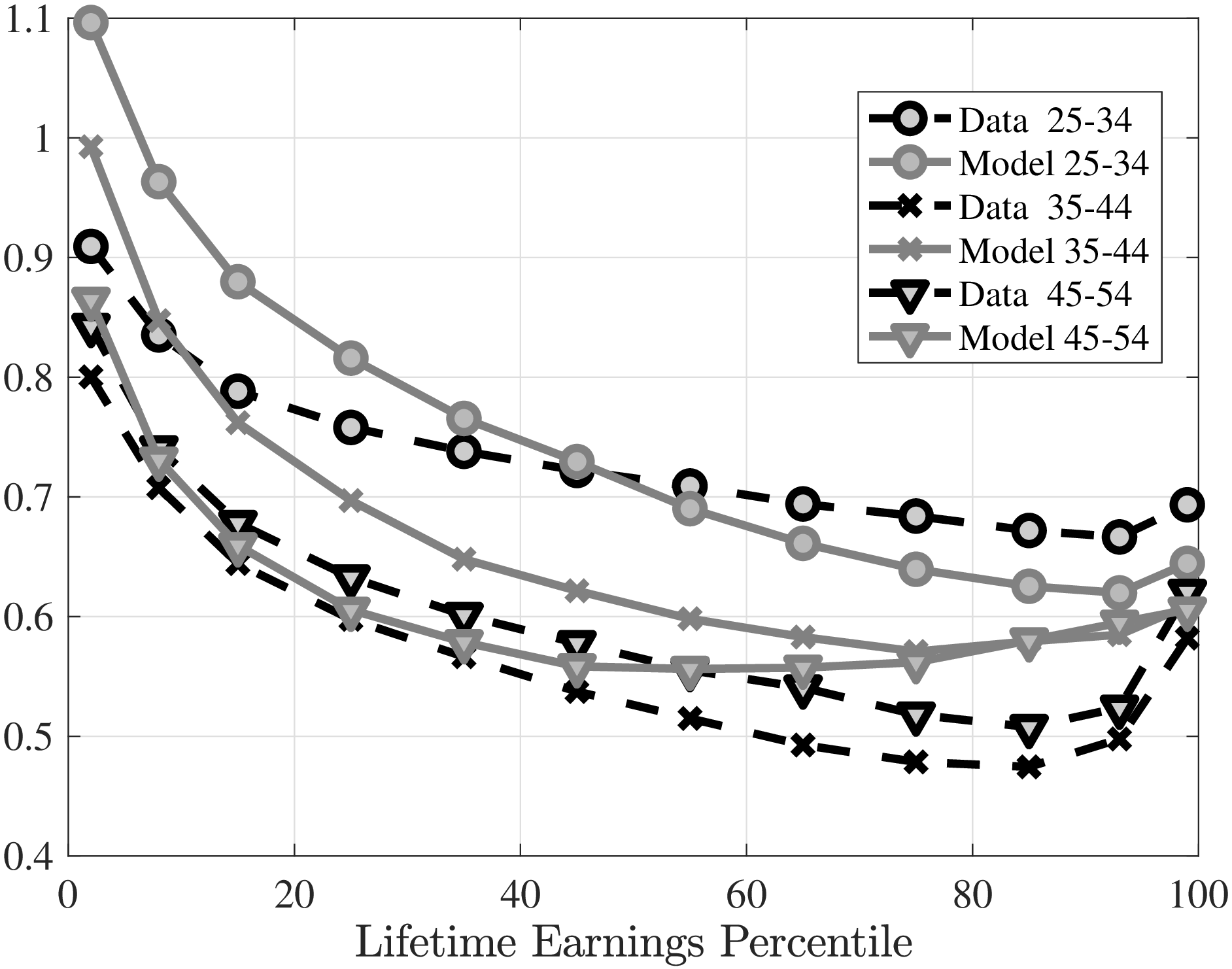

The model matches well the distribution of lifetime earnings (Figure 9a). At the top of the distribution, \(LE_{50}\) earns around 4.19 times as much as \(LE_{45}\) in the model, slightly overstating the data (3.83). The fit is much better below \(LE_{45}\): \(LE_{45}\) earns 1.97 times as much as \(LE_{25}\) in the model, compared to 1.94 in the data. Moreover, the ratio of \(LE_{5}\) to \(LE_{1}\) is 1.80 in the model, slightly below its empirical counterpart of 1.92 (Table 2).

| \(LE_{50}/LE_{45}\) | \(LE_{45}/LE_{25}\) | \(LE_{25}/LE_{5}\) | \(LE_{5}/LE_{1}\) | |

| Data | 3.83 | 1.94 | 1.90 | 1.80 |

| Model | 4.19 | 1.97 | 2.07 | 1.92 |

Notes:

\(LE_{i}/LE_{j}\)

is the ratio of average lifetime earnings of the individuals in

\(LE_{i}\)

to those in

\(LE_{j}\)

.

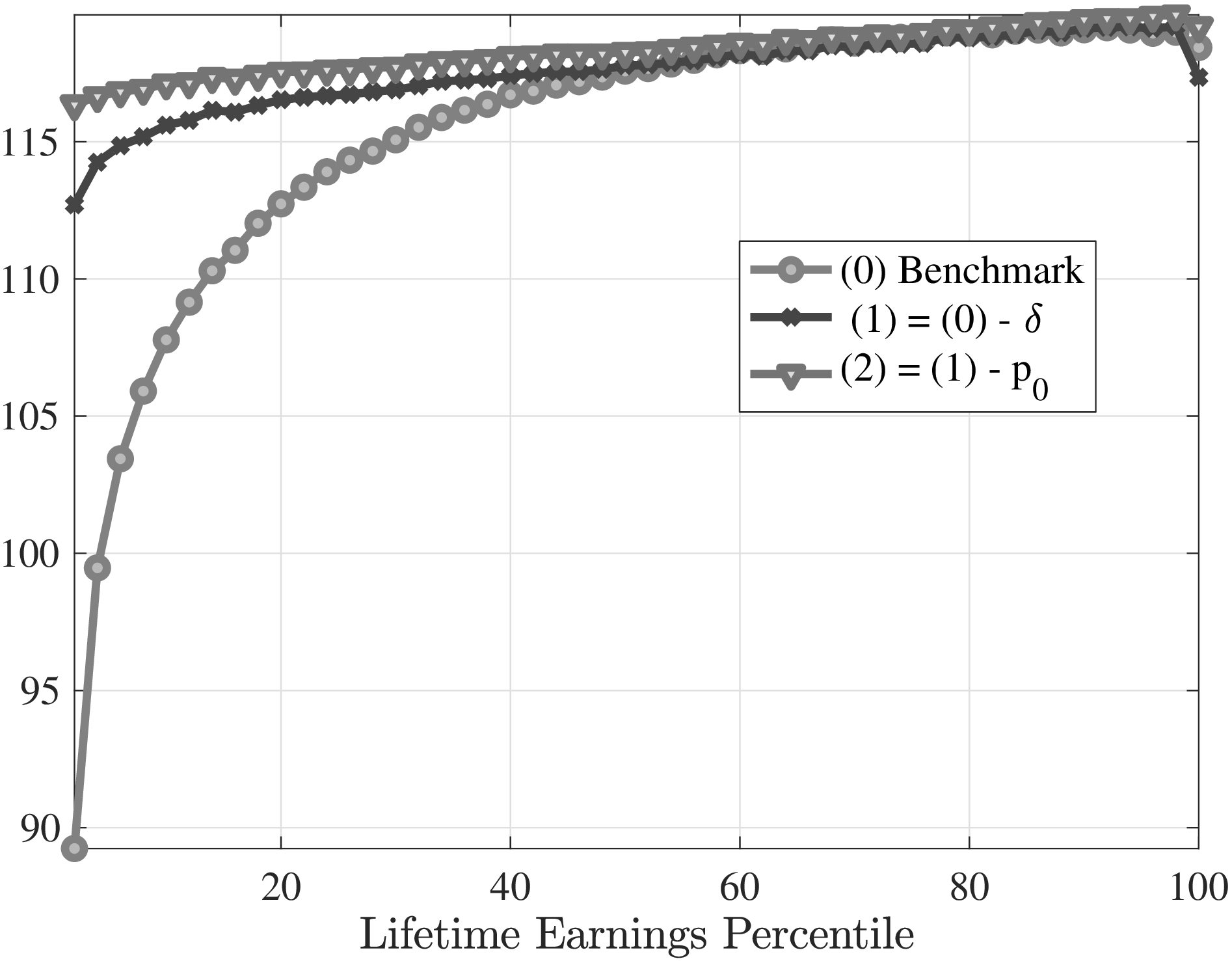

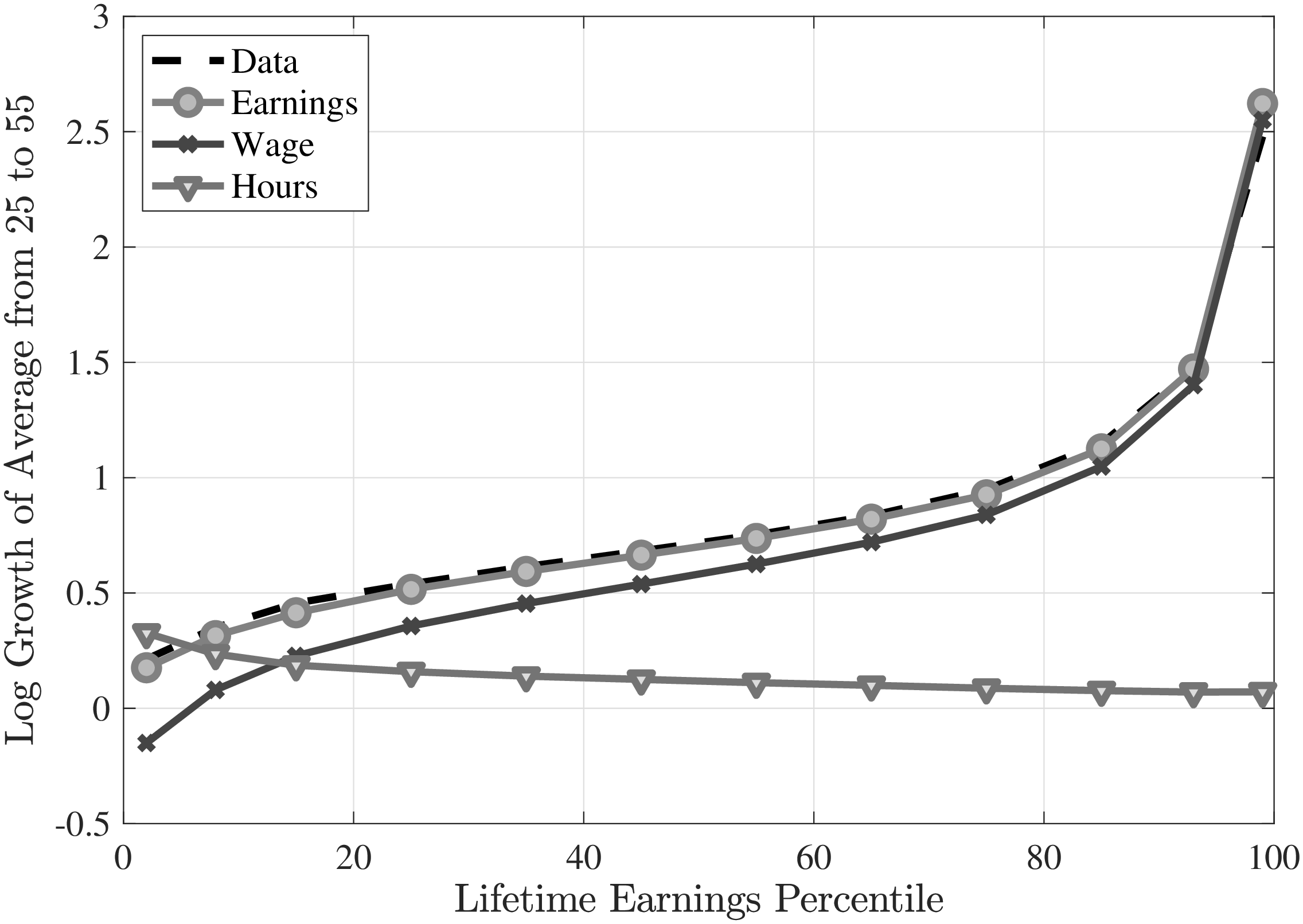

6.1 Earnings Differences: Wages versus Employment

To what extent are these large differences in lifetime earnings driven by differences in wages as opposed to differences in employment rates over the life cycle? Figure 9a plots the earnings and wage differences in the model by normalizing the median group to 1. This figure shows that wage—rather than employment—differences explain the vast majority of LE inequality. Differences in average wages over the life cycle are remarkably similar to the lifetime earnings differences, except below the 25th percentile, where differences in employment (measured as the number of quarters worked over the working life) play an important role. For example, employment of workers at the bottom of the LE distribution is about 25% lower than that of the median workers. Employment differences above the median are negligible in comparison (Figure 9b).