1 Introduction

The nature of income dynamics and the distribution of idiosyncratic shocks are crucial for behavioral choices of consumption, savings, and leisure, and influence the design of optimal social insurance and taxation. While the early literature studying idiosyncratic income fluctuations focused mostly on linear and symmetric models of risk, recent contributions have explored nonlinearities and nonnormalities (e.g., Arellano et al. (2017); Guvenen et al. (2014); Guvenen et al. (2019)). In particular, this literature has documented that the persistence of innovations is not uniform but exhibits systematic asymmetries—for example, that large negative earnings shocks are less persistent than positive changes—and that the distribution of innovations to income displays strong left skewness and excess kurtosis relative to normally distributed shocks. Much of this literature has focused on fluctuations in individual annual earnings. However, many questions in economics, such as optimal taxation and consumption-savings choices, require that one studies the dynamics of disposable household income rather than individual labor earnings before taxes. Moreover, it is important to also understand the dynamics of each of the components that labor income comprises: hours worked and hourly wages.1

This paper decomposes earnings shocks into changes in hours and changes in wage rates and studies the extent to which the nonlinear and non-Gaussian aspects of male earnings dynamics are driven by hours, wages, or their interactions. 2 We also examine the role of specific sources of large earnings shocks such as job changes. Finally, we examine the extent to which the non-Gaussian aspects of male earnings changes are passed through to household earnings and household disposable income. We study these questions using nonparametric methods building on Guvenen et al. (2014); Guvenen et al. (2019), which enables us to detect the sources behind the nonnormalities and nonlinearities in a descriptive and intuitive way. To this end, we use panel data from a combination of administrative registers (e.g., annual tax records and employment registers), covering the entire population in Norway. Furthermore, we link the Norwegian Labor Force Survey (AKU) data set to these administrative records to derive a high-quality measure of hours worked. Specifically, we employ machine learning techniques to estimate a model for the actual annual hours in the AKU as a function of observables available in the registry data. We then apply this model to the entire workforce to impute a similar labor hours measure. This imputation procedure is an independent contribution of our paper.

We start by decomposing earnings growth into hours and (hourly) wage components conditional on workers’ age and past earnings. For workers in the middle of the earnings distribution, hours and wage growth are about equally important in accounting for large changes in earnings, whereas small earnings changes are mainly driven by wage growth. Low and high earners exhibit different patterns, however. For individuals with low past earnings, hours changes account for a larger fraction of earnings growth than does wage growth. For high earners, this pattern is reversed, with wage growth accounting for most of their earnings fluctuations. The main events associated with large negative or positive earnings shocks are transitions in and out of long-term sickness, transitions between full-time and part-time work, and job changes.

We next document that the persistence of earnings changes in Norway is highly asymmetric, a finding broadly consistent with other studies for U.S. and Norwegian workers (c.f., Arellano et al. (2017); Guvenen et al. (2019)). Small shocks and large increases are essentially permanent, whereas large declines are transitory for most workers. The exception is the high earners, for whom negative changes are highly persistent and positive ones are more transitory. Exploiting the administrative nature of our data—which includes even those who drop out of the workforce—our methodology allows us to study effects working through both the intensive and the extensive margins of labor supply.

We investigate the dynamics and mean reversion patterns of hours worked versus hourly wages in order to understand the drivers of the nonlinear persistence of earnings. We uncover a sharp dichotomy between hours and wages. Changes in wage rates are highly persistent. This holds true for both positive and negative changes, and for small and large changes alike. In contrast, the persistence of changes in hours worked turns out to be highly nonlinear: moderate and large reductions in hours worked tend to be transitory and have mostly disappeared five years after an initial fall, whereas increases in hours worked are permanent. This holds true for all workers except for those with the highest recent earnings. We conclude that the nonlinear persistence of individual earnings changes in Norway is mainly driven by hours worked and not hourly wages. Namely, large earnings declines for the majority of workers are transitory because they are, to a larger extent, driven by hours declines, which are transitory. Again, the exception is the high earners, for whom declines have a somewhat larger persistence because earnings reductions for these workers are primarily driven by wage declines, which are persistent.

We then turn to the distribution of individual earnings changes in Norway. A first observation is that its higher-order moments and their variation over the life cycle and between income groups are qualitatively remarkably similar to those reported for U.S. workers (see Guvenen et al. (2019)). In both countries, the variance of earnings growth declines in age and in recent earnings, although the volatility is larger in the U.S. than in Norway. Earnings growth is not symmetric but negatively skewed, and the left skewness becomes more pronounced as individuals get older or their earnings increase. Moreover, this distribution is highly leptokurtic and even more so for the high-income or older worker. We conclude that, despite the differences between Norway and the U.S. in their welfare state and labor market institutions, the nonnormalities and nonlinearities in earnings dynamics are very similar, which might reflect similar underlying economic mechanisms (see Karahan et al. (2019); Hubmer (2018)).

We study the distributions of hours and wage growth and their role in driving the higher-order moments of earnings growth and find that both hours growth and wage growth display non-Gaussian features. Both are left skewed, albeit less so than earnings growth. Moreover, both display excess kurtosis, with hours growth having higher kurtosis than earnings growth. To quantify the importance of hours and wage growth in the higher-order moments of earnings growth, we apply an exact statistical decomposition where the skewness (kurtosis) of log earnings growth is a weighted sum of the skewness (kurtosis) of log hours and wage growth plus a residual co-skewness (co-kurtosis) term that broadly captures whether large hours and wage changes coincide. All terms contribute to the negative skewness of earnings growth, with co-skewness being the main component (i.e., workers experience large declines in hours and wages simultaneously). Similarly, the co-kurtosis term is the largest contributor to the excess kurtosis.

We also investigate the role of job changes—one of the main events associated with large earnings changes—in driving the skewness and kurtosis of earnings changes. We find that the distribution of earnings growth for job switchers exhibits weaker negative skewness and less excess kurtosis compared to the distribution for job stayers. Furthermore, there are very few job switchers relative to the number of job stayers. Therefore, the skewness and kurtosis of earnings growth tend to be driven by job stayers.

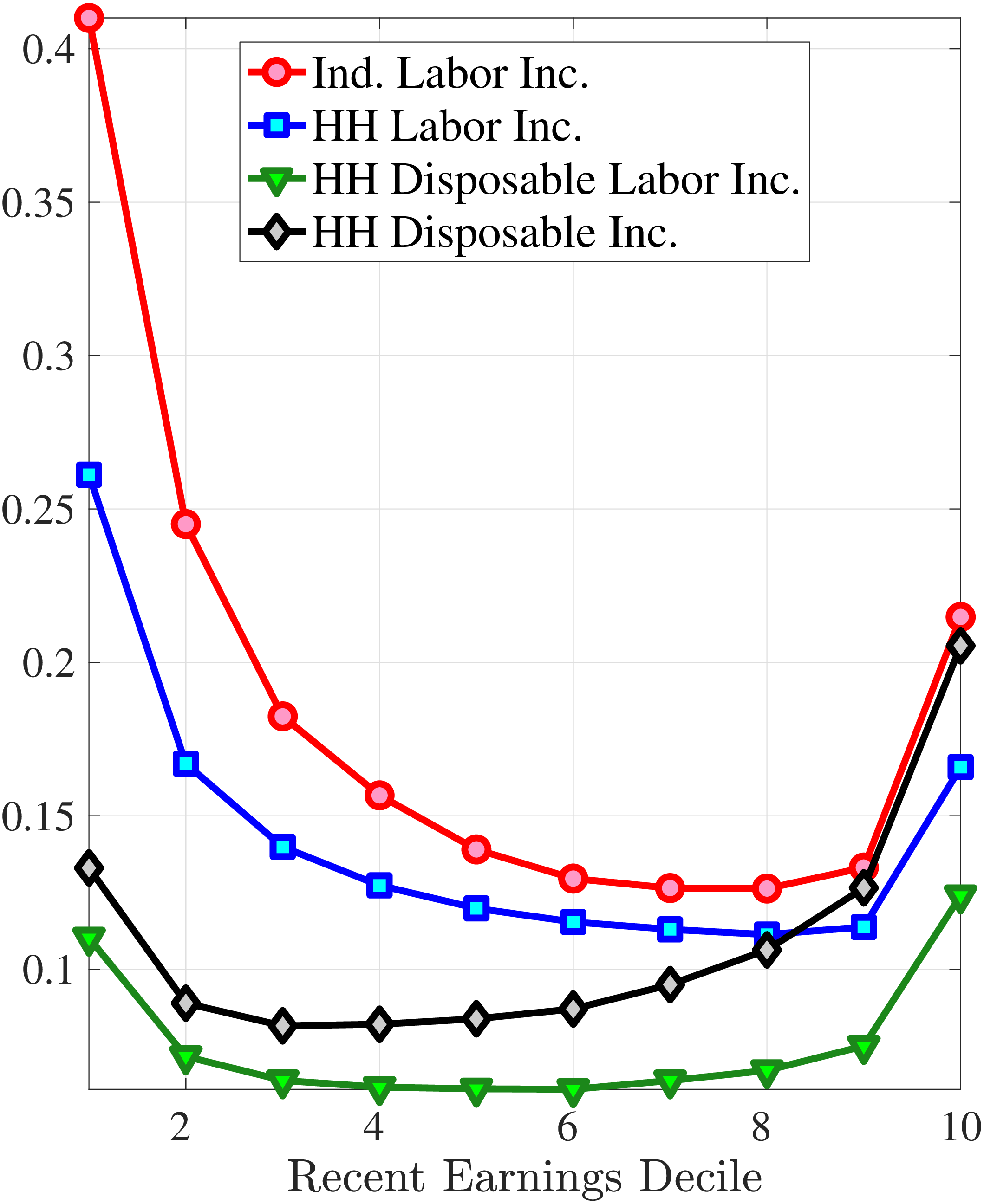

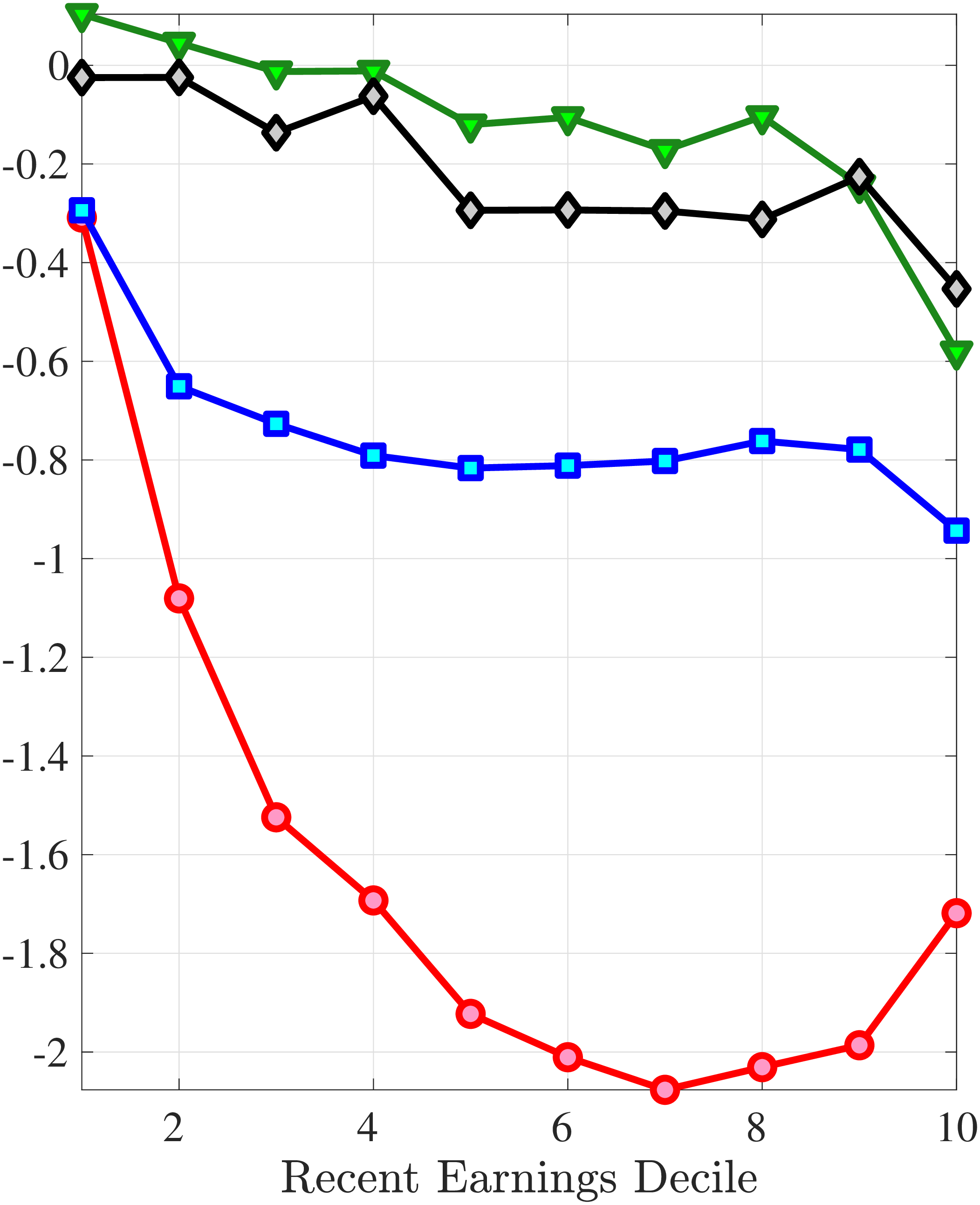

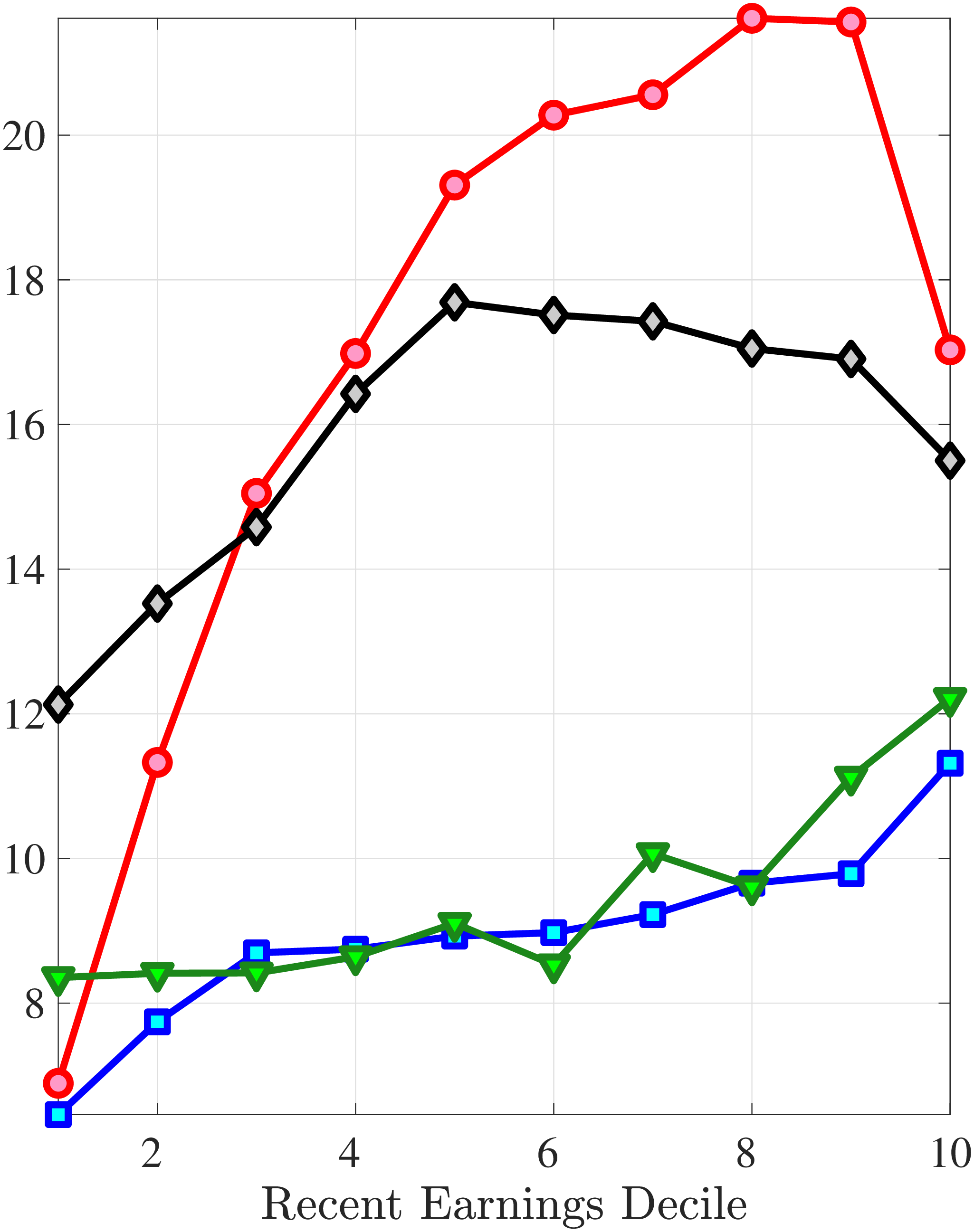

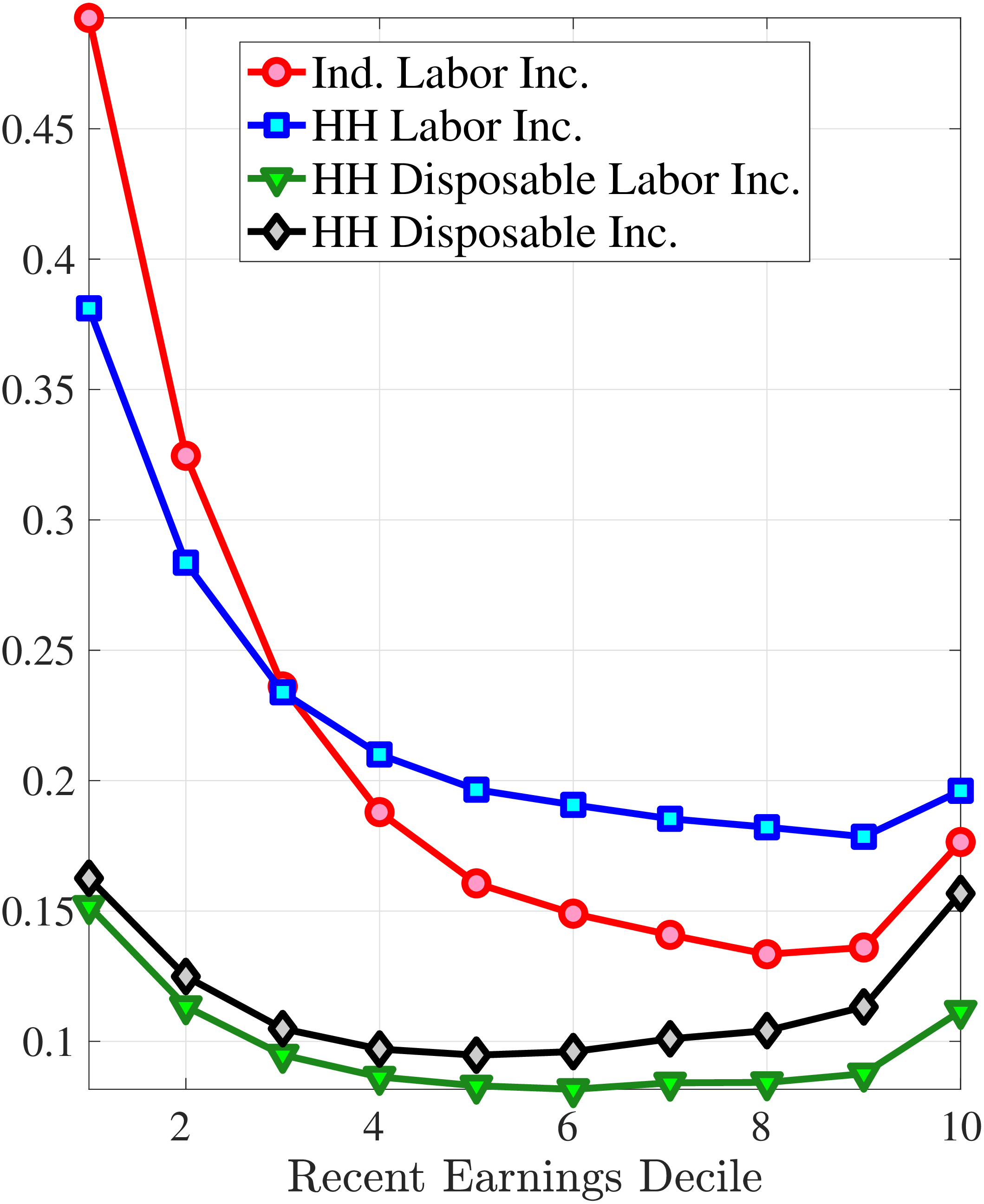

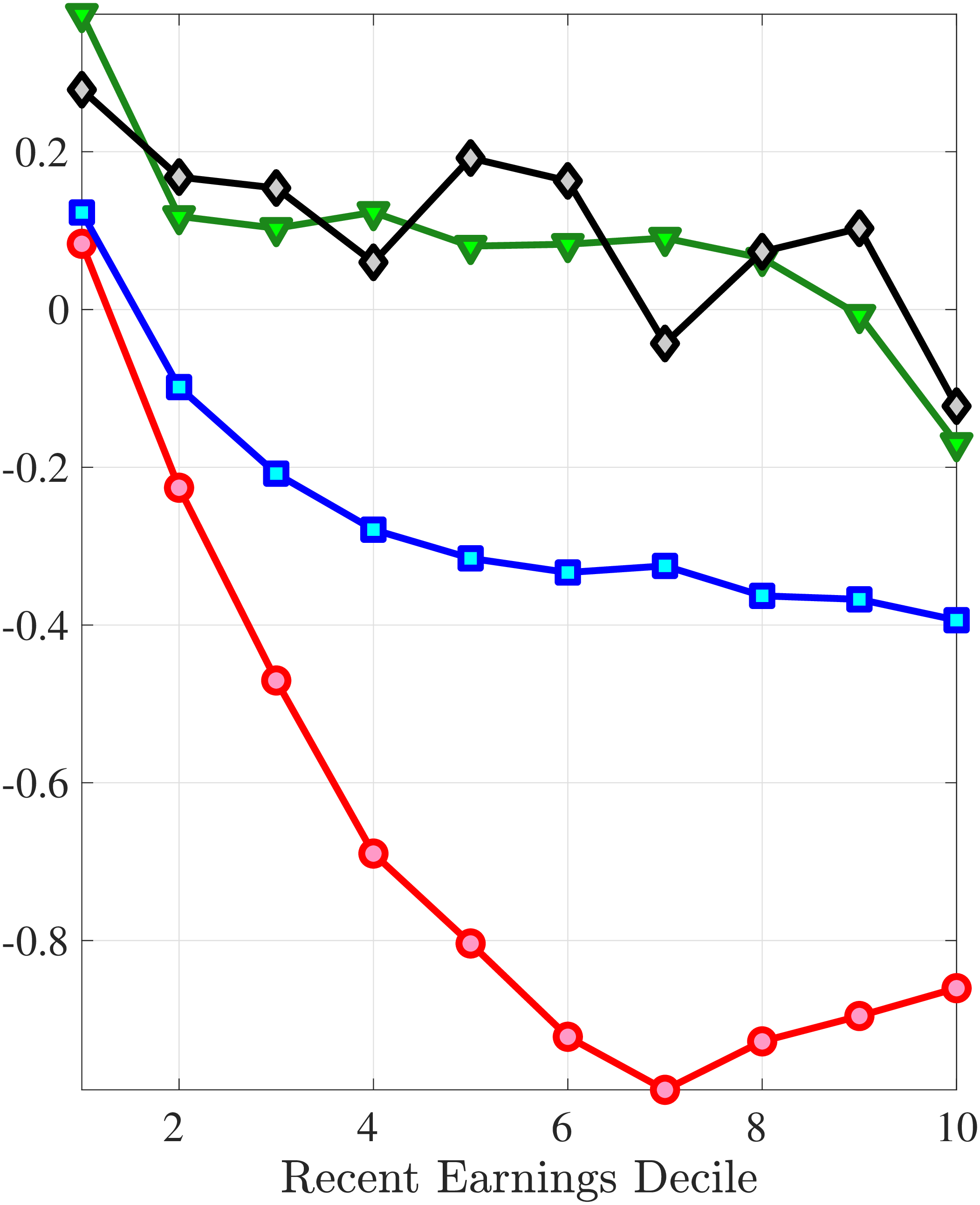

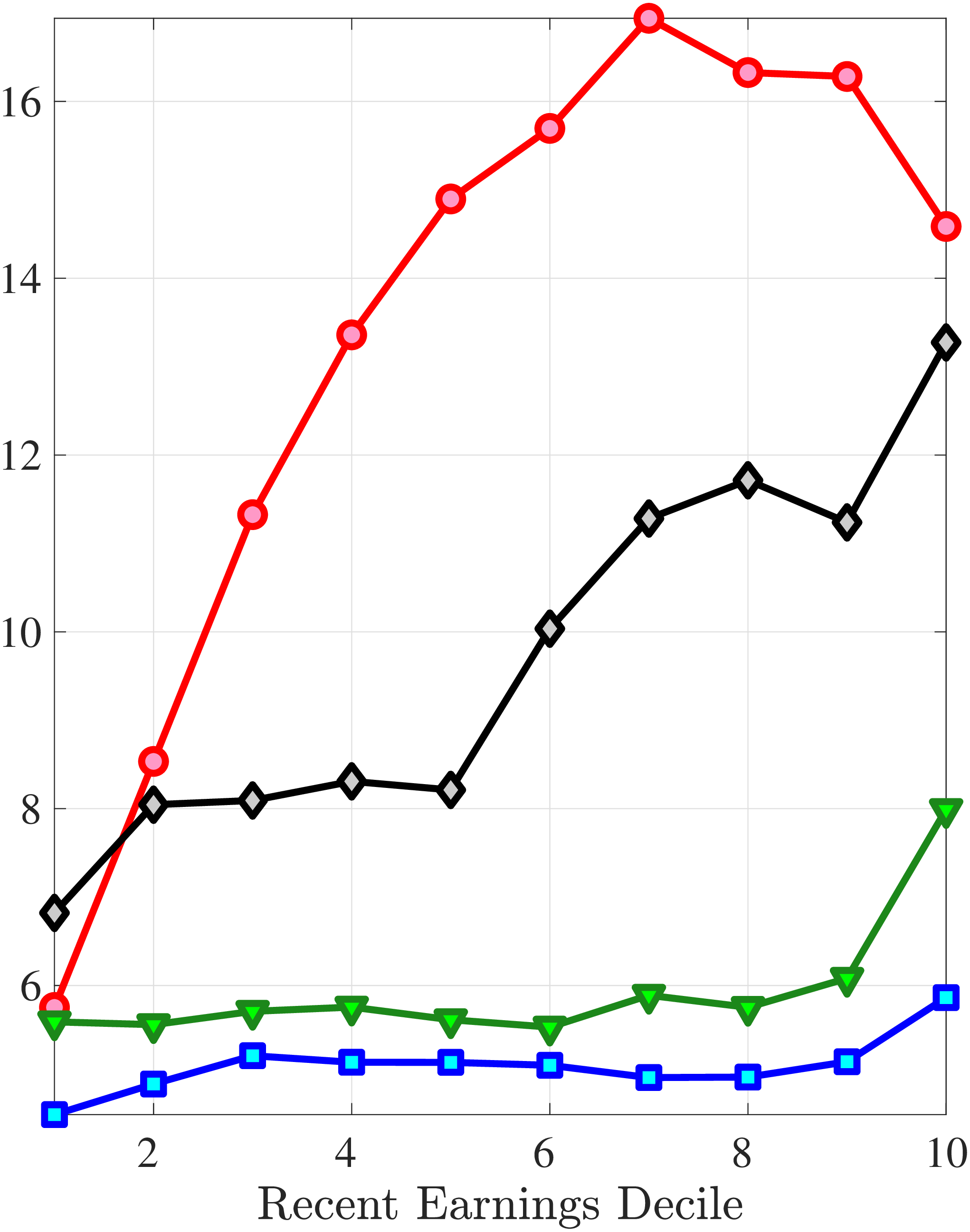

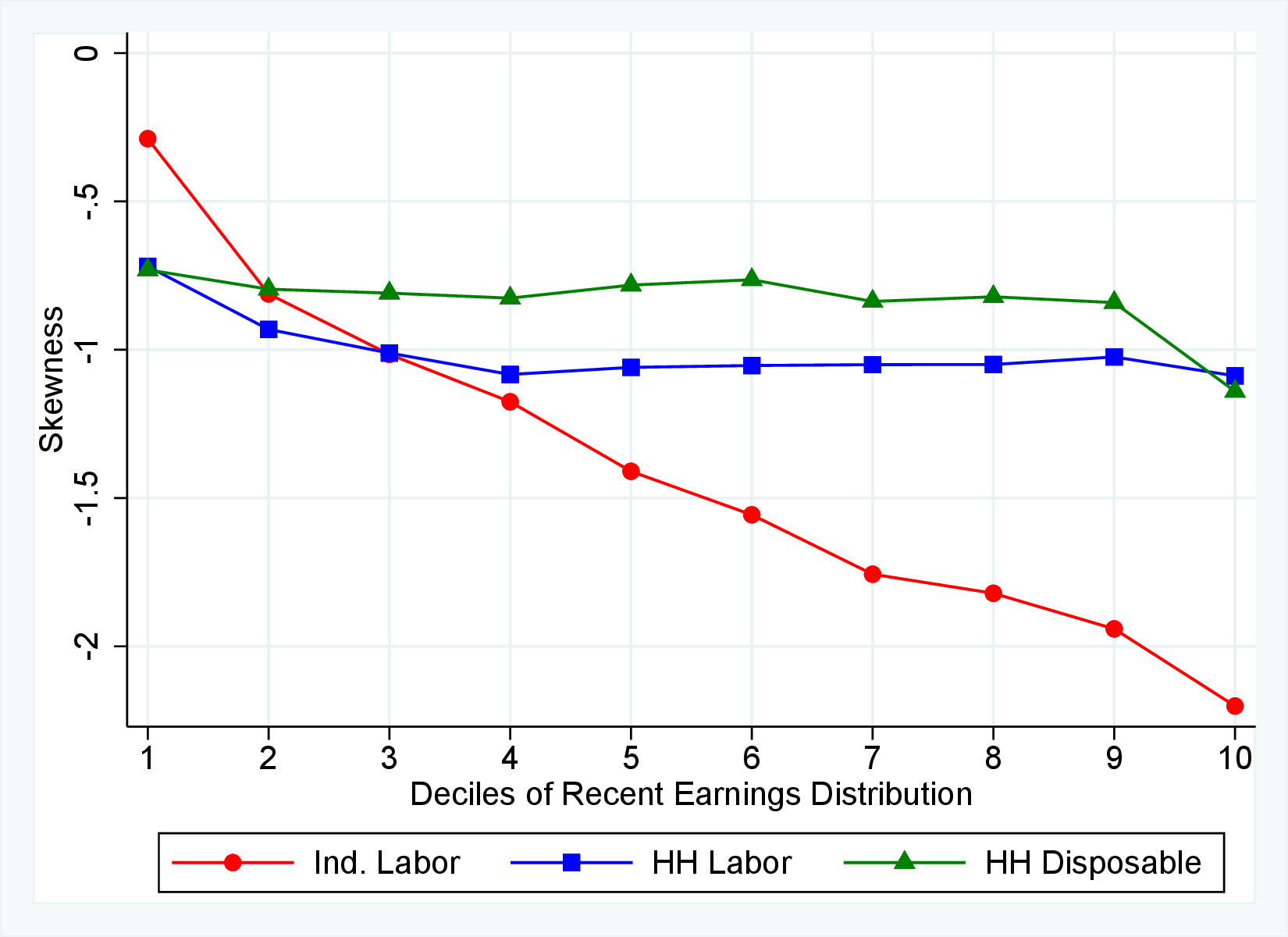

Finally, we examine how the dynamics of household earnings and disposable income differ from male earnings dynamics. Disposable income is substantially less volatile than male earnings because of spousal and public insurance. Relatedly, growth in household earnings and disposable income is less negatively skewed, with disposable income growth being approximately symmetrically distributed. Thus, we conclude that the Norwegian system of taxes and transfers provides substantial insurance against tail risk in income.

Our paper is structured as follows. We review some of the related literature on earnings dynamics in Section 2. Section 3 describes the data and empirical methodology. In Section 4, we decompose earnings risk into changes in hours and changes in wage rates and study their dynamics and contributions to earnings growth. Section 5 studies the higher-order moments of wage and hours growth and their contributions to the higher-order moments of earnings growth. It also examines how the higher-order moments are affected when going from male labor earnings to household earnings and household disposable income. We finally conclude in Section 6.

3 Data and Methodology

In this section, we describe our data sources and the machine learning algorithm we employ to impute actual work hours in the register data. We also lay out the empirical methodology for studying earnings, hours, and wage changes.

3.1 Data Sources on Income and Labor Supply

Our analysis uses data from four different data sources between 1993 and 2014. The first data set is Administrative Tax and Income Records, which contains a set of detailed information on income and taxes for the entire Norwegian population from 1993 onward. In addition, this register contains information on age, gender, household composition, country of origin, and education. Our measure of labor earnings is comprehensive and includes wages and salaries from all employment, including bonuses and other irregular payments. We exclude income from self-employment and also exclude individuals with significant self-employment income from the sample, mainly because we do not have data on labor supply for self-employed individuals.4

Tax records are of high quality because most information is third-party reported to the tax authorities, and very little is self-reported. Employers, banks, brokers, insurance companies, and any other financial intermediaries are obliged to report information on earnings payments, the value of assets owned by the individual and administered by the financial intermediary or employer, as well as information on the income earned on these assets. Capital income is measured as the sum of positive interest, dividends, and realized capital gains and losses but without deductions for interest expenses. Moreover, the tax records contain information on transfers and income taxes. Transfers include unemployment benefits, sickness benefits, paid parental leave, remuneration for participation in various government activity programs, disability benefits, public pensions, and other social welfare payments.

For most of our analysis, the basic tax unit is an individual. For our household-level analysis, we use family identifiers from the population register, pooling the individual incomes of spouses for both married and cohabiting couples to calculate household income. Household income is equivalized using the OECD equivalence scale. All values are deflated using the (Laspeyres) Consumer Price Index.

The second data set is maintained by the Norwegian Social Security Administration and contains the start and end dates of spells for unemployment, parental leave, sickness, and disability benefits at the daily level. We use this information in our impution model.

The third data set we use is the Employment Register, which is a matched employer-employee data set of the universe of employers and employees in Norway. All employers are required to report contractual hours, employment duration, sector, and industry to the government. Information about contractual hours of work is limited to the period from 2003 to 2014, since prior to 2003 only full-time and part-time hours was reported.5 The Employment Register covers the entire labor force, except for self-employed workers and freelancers. This amounts to 90% of the labor force and 77% of the prime-age population (25 to 60 years old). For individuals with multiple jobs during the year, we define main employment as the job that accounts for the largest share of annual earnings and measure annual “register hours” as the sum of contractual hours worked in all jobs.

Finally, to measure actual annual hours worked for the entire population, we use data from the Norwegian Labor Force Survey (AKU) in combination with register data. The next section lays out our measurement and imputation procedure and motivates why our approach provides a better measure of labor supply than the register hours.

3.2 Measuring and Imputing Actual Hours of Work

3.2.1 Measuring Annual Hours Worked in the AKU

The AKU is the basis of official Norwegian employment statistics, comparable to the Current Population Survey (CPS) for the U.S. It is a representative survey of all residents ages 15-74, covering 24,000 people each quarter. The sample is a rotating panel where each participant is interviewed for eight consecutive quarters. We focus on 2003-2014 and restrict the sample to individuals ages 25-60. We impute annual hours for individuals for whom we have at least three quarterly observations in a calendar year. This yields a final sample of 35,909 men and 35,175 women.

Survey participants report two measures of labor supply during the week preceding the interview: actual hours worked last week and regular (contracted) hours last week. By relying on remembering very recent events, the AKU measures of hours worked are robust to standard recall bias. The survey week is randomly drawn within the quarter.6 See Appendix A.3 for a more comprehensive description of the Labor Force Survey.

Given reported labor supply for four weeks in a year, we impute the total annual hours in year \(t\) as \(h_{t,j}^{LFS}=13\cdot \sum _{q=1}^{4}h_{t,q}^{LFS}\), where \(h_{t,d}^{LFS}\) is weekly hours in quarter \(q\) of year \(t\) and \(j\) represents either actual hours or contracted hours.7

The next subsection motivates why we use the actual hours variable in the AKU as our main measure of labor supply instead of the contractual hours measure in the administrative data. We also estimate m.e. for the contractual hours measure in the Employment Register using a similar variable from the AKU.

3.2.2 Actual Hours versus Register Hours

The measure of contractual hours in the Employment Register has significant weaknesses as a measure of actual hours worked, and we believe that the AKU actual hours variable offers a better measure of actual labor supply for four reasons. First, Statistics Norway uses this survey to calculate official statistics on aggregate employment and unemployment (instead of contractual hours information in the employment register). Therefore, it is conducted using modern survey techniques, designed to minimize m.e. and to provide a precise measure of actual hours worked.

Second, “contractual hours” measures the regular hours in the employment contact. This measure of labor supply is conceptually different from actual annual hours worked, which is what we need for our purposes. In particular, contractual hours do not include overtime because the Employment Register was originally administered by the Social Security Administration to calculate work-related benefits, which does not cover overtime. Moreover, the register does not cover employment that amounts to less than four hours per week or seven days per job spell.

Third, even as a measure of regular hours, contractual hours in Norwegian register data contain substantial m.e. because employers often fail to update changes in employment spells or contractual hours. While earnings and employment matter for taxes and transfers from the Norwegian government, neither hours worked nor contractual hours play any role for taxes and transfers. The Employment Register does, therefore, not have an incentive to enforce accurate reporting of contractual hours and misreporting does not have any repercussions for the employer.8 This m.e. can be quantified using the AKU measure of contractual hours. We interpret the variable contracted hours in the AKU survey as the respondents’ perception of register hours in the Employment Register. Moreover, all individuals surveyed in AKU can be matched to the register data. The availability of two independent measures of contractual hours—self-reported and reported by the employer, respectively—allows us to estimate the magnitude of the m.e. for contractual hours in the register data. Assume that m.e. in growth in (the log of) contracted hours in both AKU and register data is classical (i.i.d.). Then the variance of this m.e. can be estimated as the difference between the variance of log hours growth in the register data and the covariance between contracted log hours growth in AKU and the register data. This estimation procedure implies a variance of classical m.e. of 0.061 and 0.047 for young and old men, respectively. Thus, m.e. accounts for 65% and 83% of the variance of contracted hours growth for young and old men, respectively. For comparison, this is the same order of magnitude of m.e. that Heathcote et al. (2014) estimate for male hours growth in the PSID.9 We interpret this finding as an indication that contractual hours in AKU exhibit substantial m.e., of a magnitude comparable to that of the PSID.

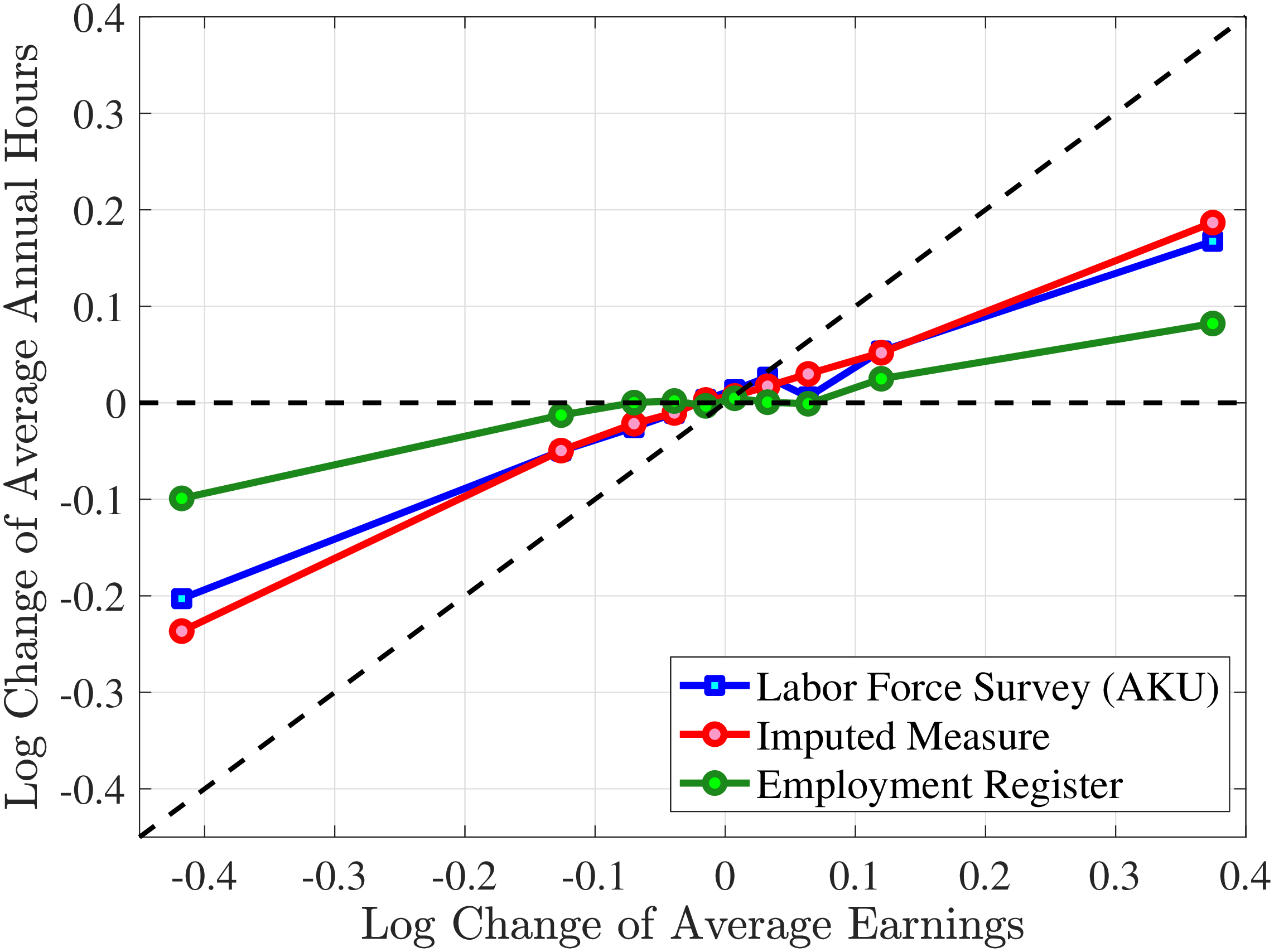

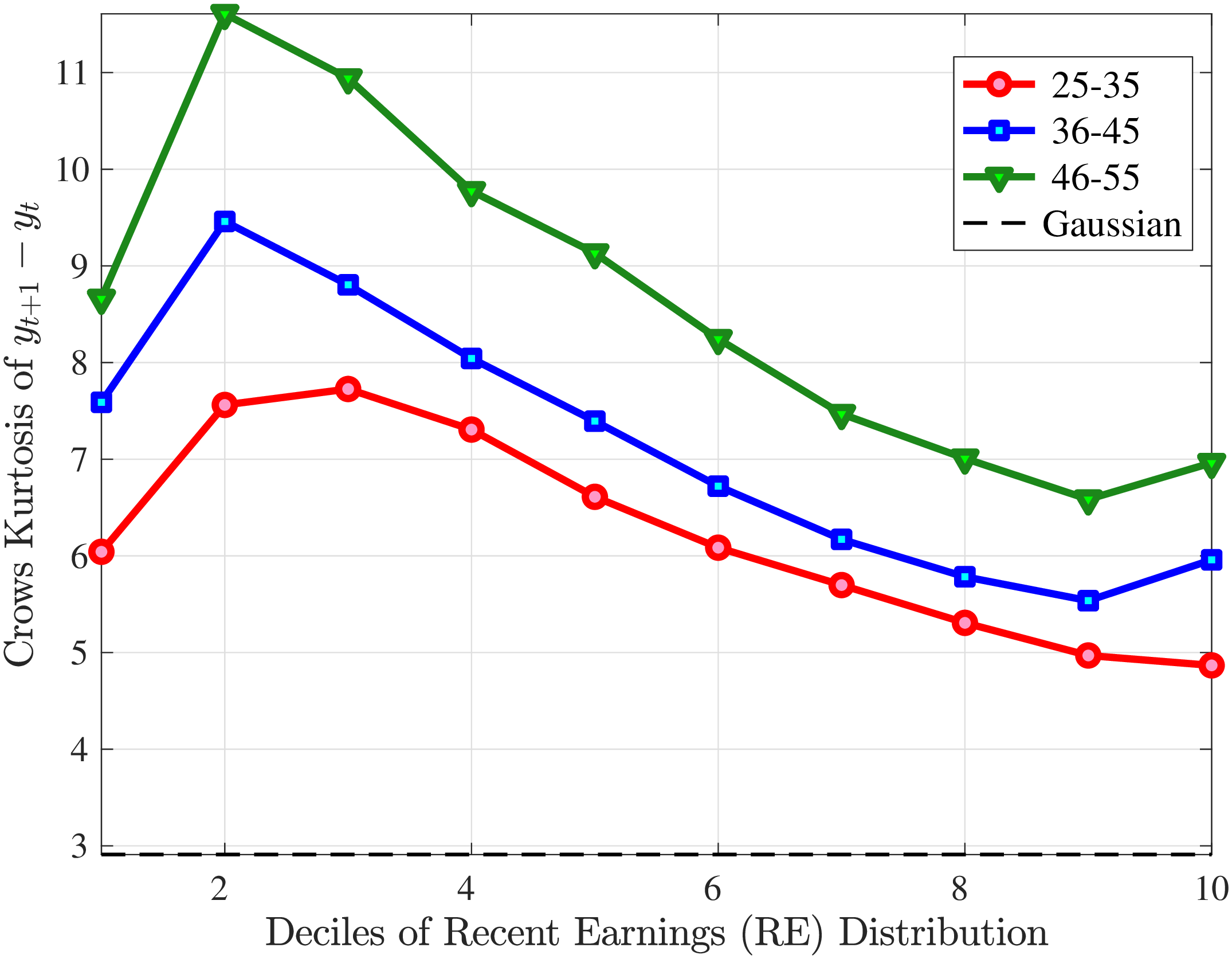

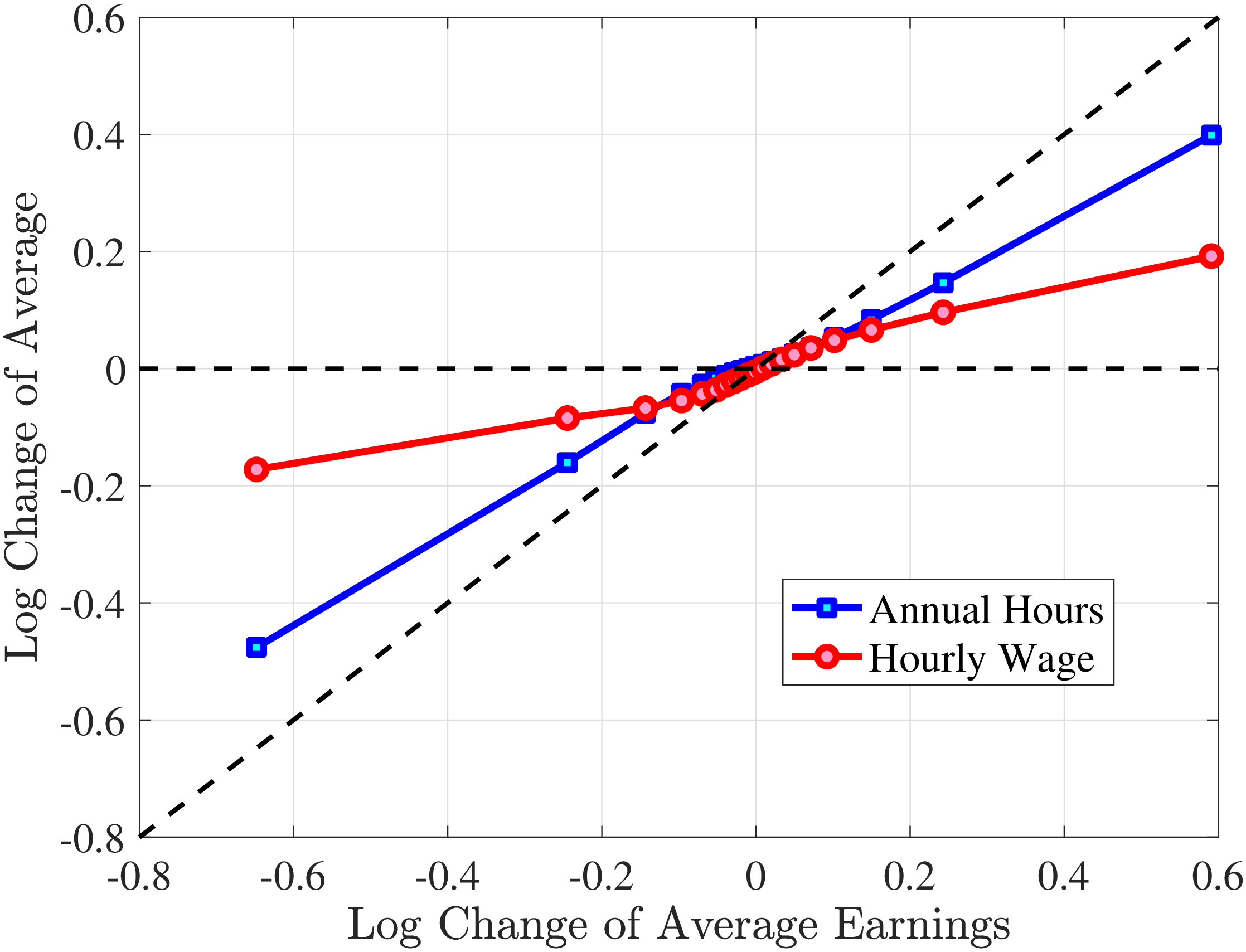

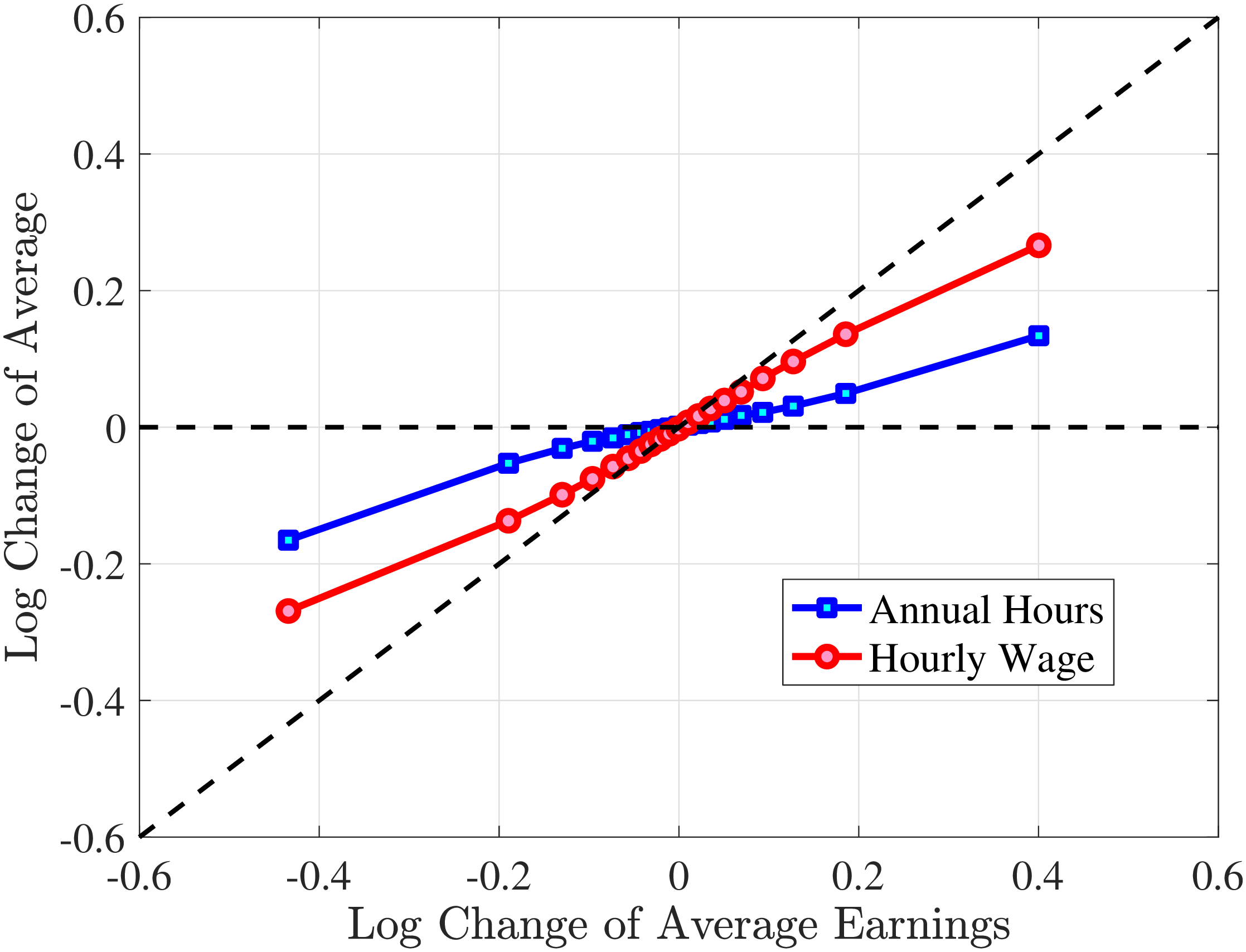

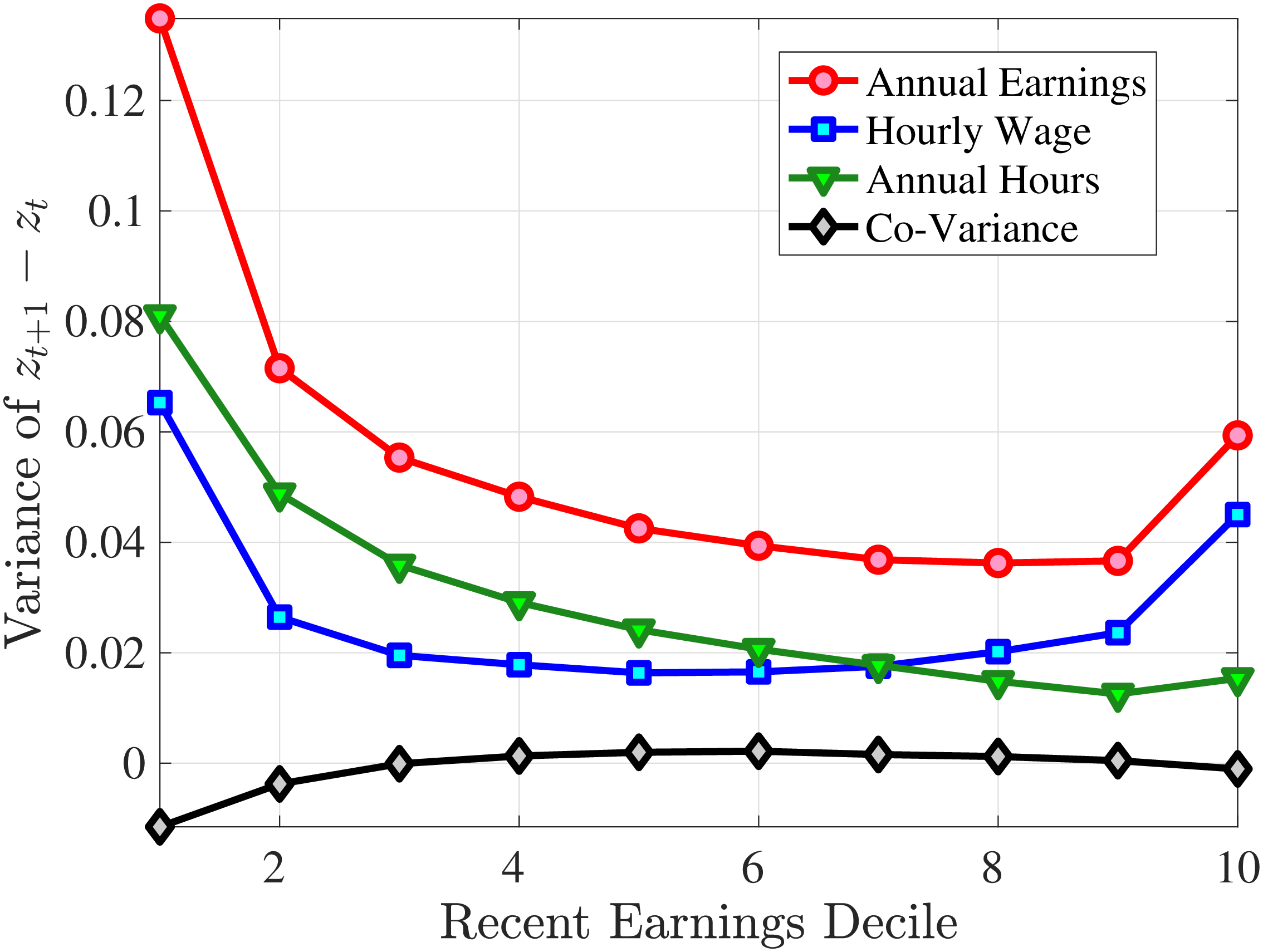

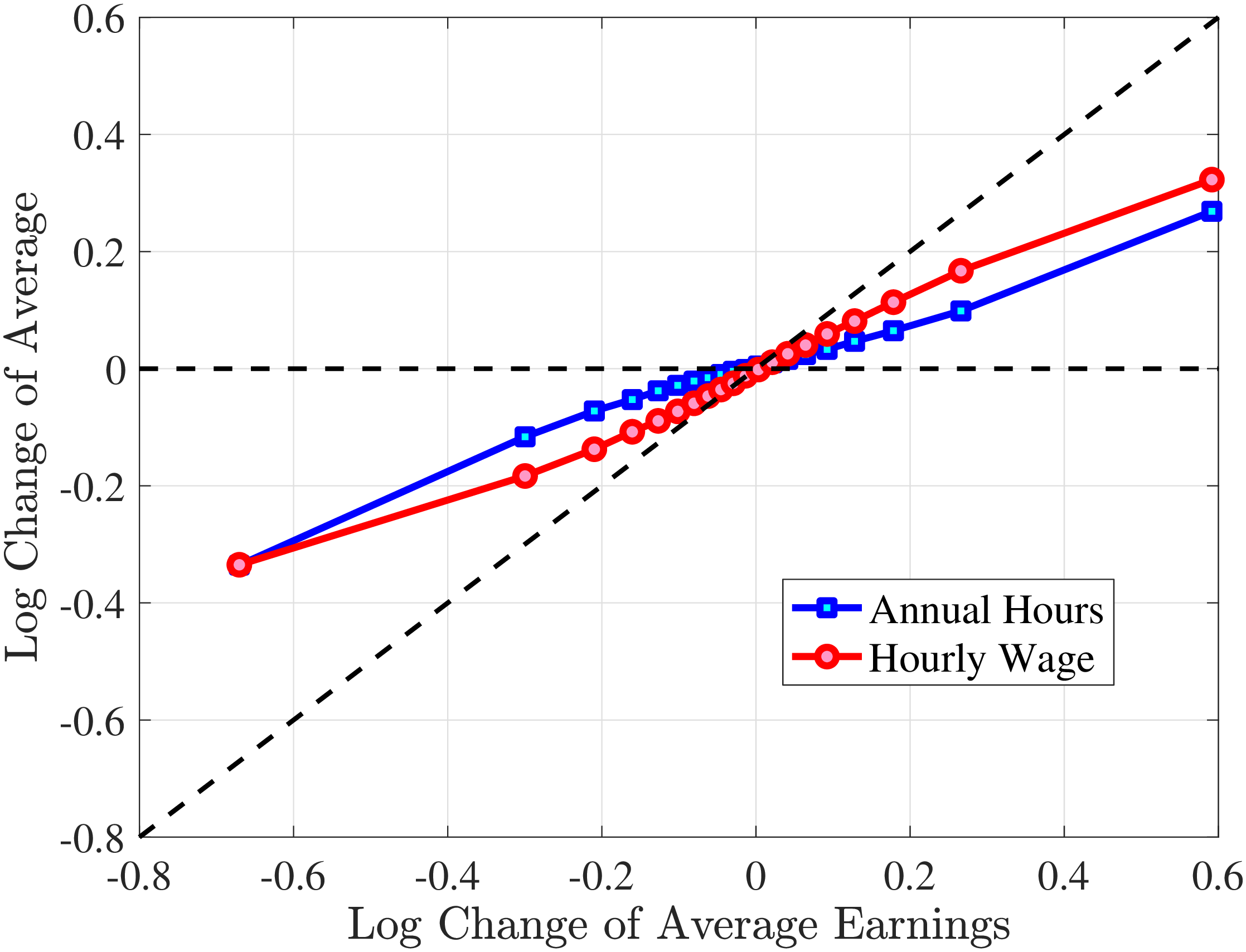

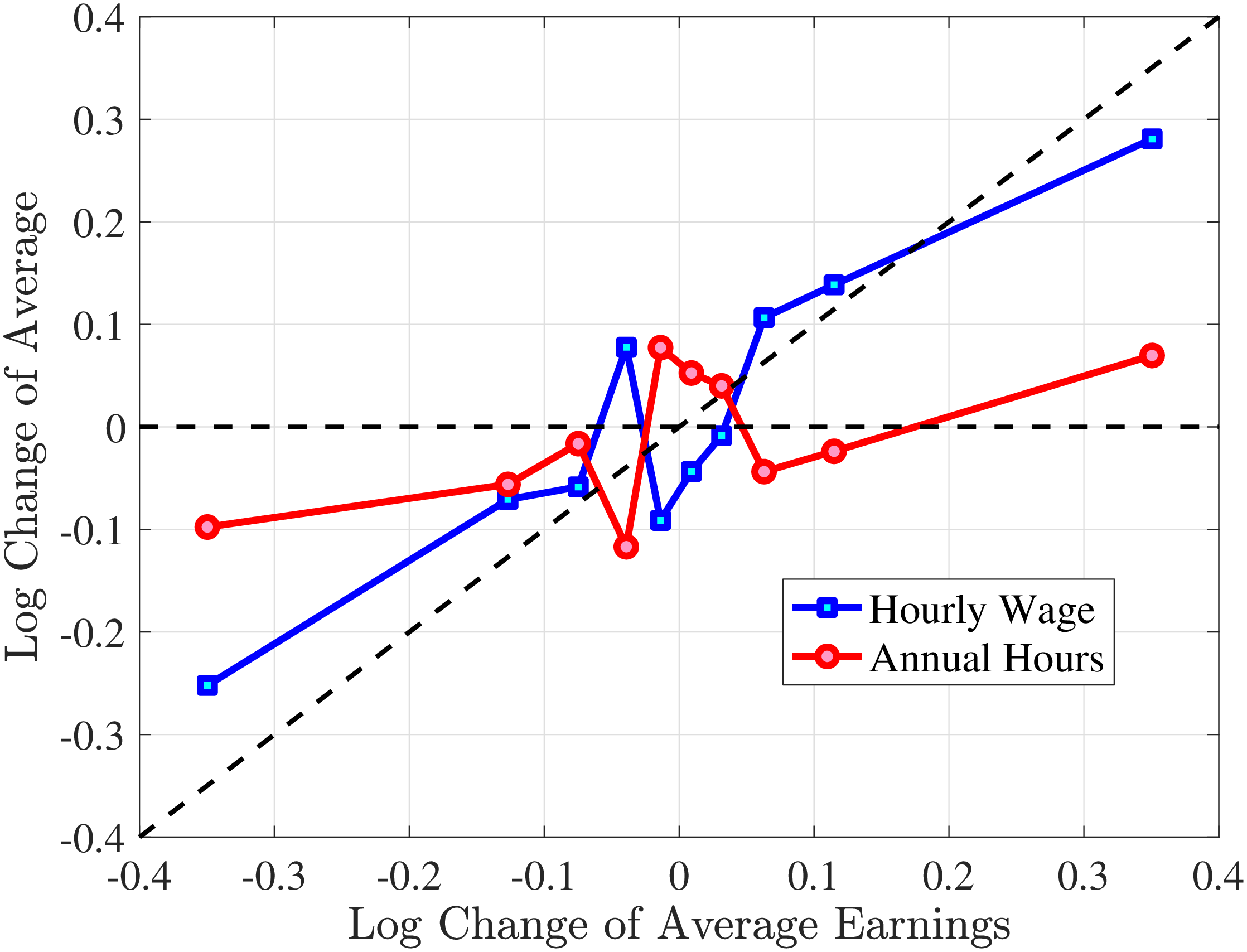

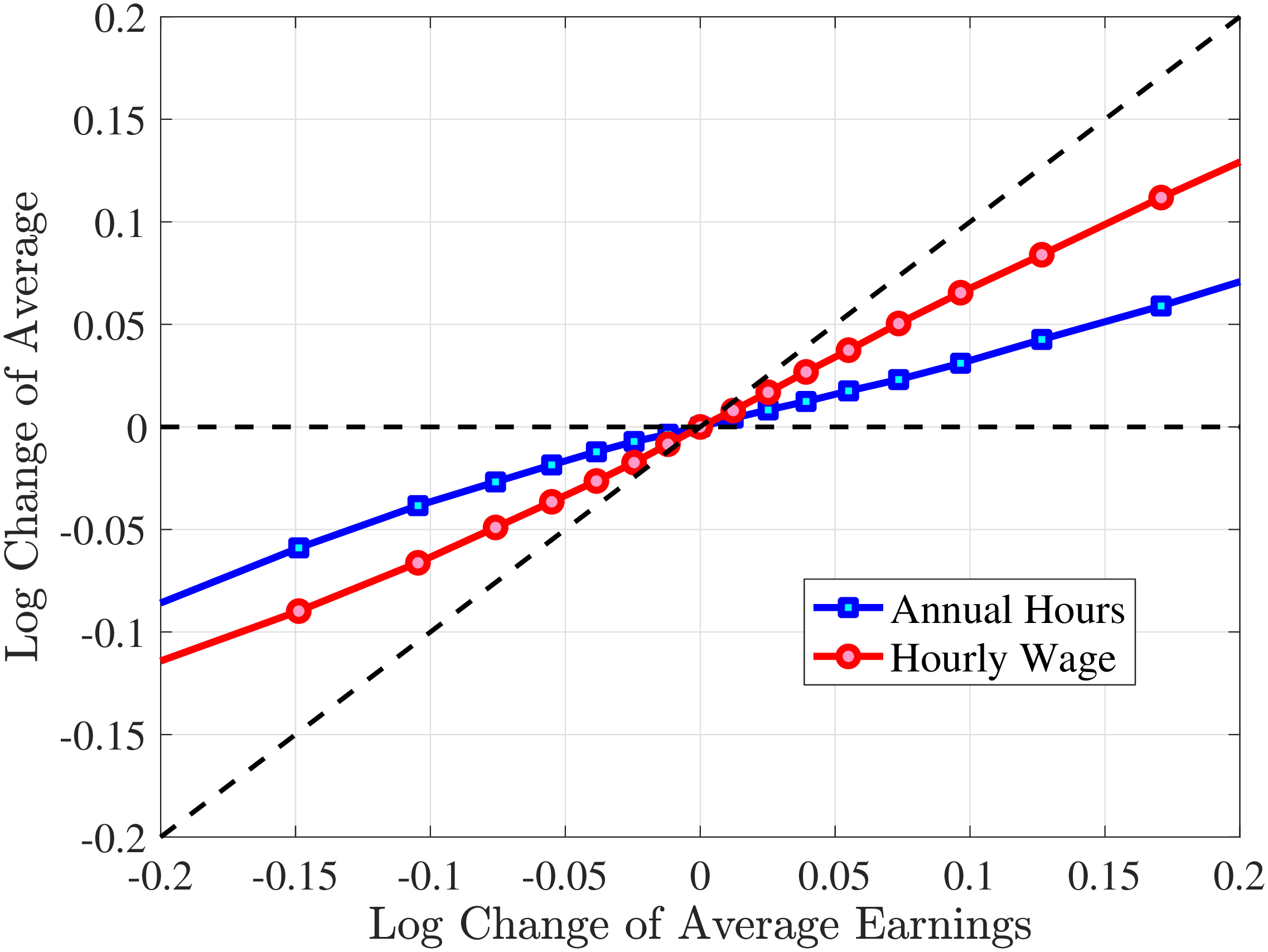

The fourth and most important reason for actual hours being a better measure than register hours is that observed earnings changes have a much stronger correlation with actual hours changes than with register hours changes. To show this, we rank individuals present in the Labor Force Survey into 10 bins based on their one-year earnings changes, where earnings data are from the register data. For each bin, we plot the log change of average earnings between \(t\) and \(t+1\) on the \(x\)-axis against the corresponding change in average annual hours on the \(y\)-axis for both actual hours in the AKU and contracted hours from the Employment Register (Figure 1). Changes in contracted hours (from the administrative data) are significantly smaller than those of the survey data. For example, for large earnings changes (positive or negative), the change in register hours is just one-half of the change in actual hours. And for small earnings changes, the elasticity of register hours is zero. Actual hours can therefore explain more of the changes in earnings. This observation provides direct evidence that contracted hours data contain systematic m.e. relative to survey data on actual hours.10 Moreover, Appendix Table A.1 illustrates that the higher-order moments of contractual hours in AKU are quite different compared to those of our measure of actual hours in the same survey. Since our aim is to decompose earnings changes into changes in hours worked versus hourly wages, we conclude that using actual hours is better than relying on contracted hours.

Figure 1

–

Response of Actual, Contracted, and Imputed Hours

Note: The figure displays the average one-year changes in contracted annual hours, imputed annual hours, and actual annual hours (as measured in the Labor Force Survey) for individuals with different one-year changes in annual earnings.

Figure: Figure 1 – Response of Actual, Contracted, and Imputed Hours

3.2.3 Imputing Actual Hours from Administrative Data

The downside of the Labor Force Survey data is that it has only a limited sample size, with our sample comprising about 71,000 individuals. As discussed above, all individuals present in the Labor Force Survey are also present in the register data. We merge the two data sources using individual identification numbers and design a novel imputation approach to infer actual hours worked for the entire population. We now lay out this imputation procedure, which is a contribution of independent interest.

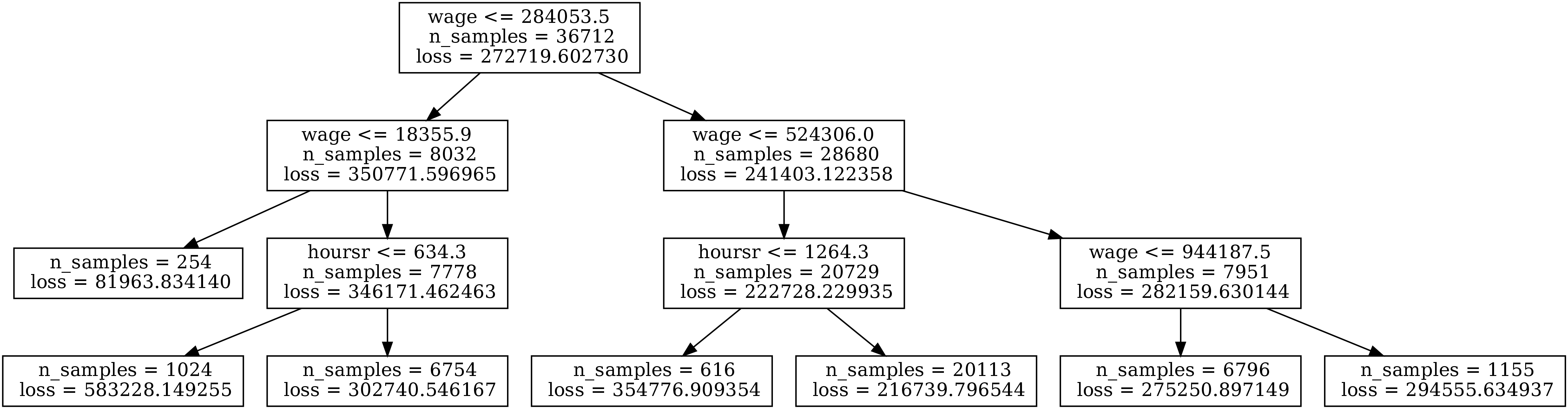

We employ a regression tree approach to estimate actual annual hours \(h_{it}^{LFS}\) from the Labor Force Survey using information from the various sources of register data as predictors. Classification and regression trees (CART) are widely used supervised machine-learning methods to develop prediction models because they are conceptually simple yet powerful.11 CART algorithms are capable of handling a large number of features and observations and are easy to use. They recursively partition the training data space according to feature (predictor) thresholds into subsets with homogeneous values of the dependent variable (for example, those with earnings or hours worked above or below a certain cutoff). In the terminal nodes, the algorithm fits simple prediction models to minimize the overall mean squared error. After the tree is grown large, the algorithm then prunes some of the nodes to minimize the cross-validated sum of squares (see, e.g., Hastie et al. (2009) and Loh (2011) for further details of the machine learning algorithm).

At the terminal nodes of the tree (the leaves), we use linear regression models to minimize the errors between the measured and predicted values:12

\[ h_{it}^{LFS}=\beta X_{it}+\epsilon _{it}. \]

We use a rich set of regressors, \(X_{it}\), from the register data (the Social Security Administration Register, the Administrative Tax and Income Records, and the Employment Register). In particular, we include contractual hours from the employment register, sickness days, parental leave days, and unemployment days reported in the Social Security Administration Register as well as their arc-percent change from last year as these are informative about total hours worked in the current year. To capture the differences in hours worked linked to job characteristics, we include indicator variables for part-time versus full-time and public versus private sector employment as well as their changes from the last year. Job change is an important predictor for labor supply (see Guvenen et al. (2019)); thus, we include indicator variables for job stayers in the current year and the last year. As is well recognized, labor supply varies over the life cycle and across education groups (see, e.g., Chakraborty et al. (2015), Bick et al. (2022)). We therefore include these variables in our set of regressors. We further include marital status and its change since last year as independent variables (see, e.g., Chakraborty et al. (2015) for variation in labor supply by marital status). Finally, we include average past earnings, current annual earnings, and arc-percent change in annual earnings as additional regressors.13 For details on how we construct our regressors, see Appendix A.4.14

To select the optimal regression tree structure, we experiment with various depths of the tree (up to five layers) and evaluate the goodness of fit in the training sample as well as an out-of-sample test sample. To do so, as is standard in the machine learning literature, we use 80% of our sample to fit the model and the rest to evaluate the performance out of sample. In general, choosing a deeper tree with finer categories will increase the in-sample fit, but this may come at the cost of overfitting, which will decrease the accuracy of out-of-sample predictions.

We estimate the model separately for men and women. Table I summarizes the \(R^{2}\) in the training sample and test sample for different depths of the tree. For men, a regression tree of level two gives the best goodness of fit in the test sample. However, a tree with a depth of three is a very close second and performs significantly better than that of level 2 for the training sample. For women, the optimal depth level is three for the test sample. We therefore choose the tree structure with a depth of three for both men and women. Figures A.1 and A.3 show these tree structures. The associated linear-regression coefficients are reported in Tables A.3 and A.4. We use these estimated models to impute actual work hours for the individuals that are not present in the Labor Force Survey.15

The two most important covariates are contractual hours and labor earnings. The algorithm splits the sample mainly according to annual earnings and register hours for both men and women. The number of days receiving benefits for sickness, parental leave, and unemployment is also an important predictive variable. This is not surprising since the number of days on benefits is very accurately measured—it is based on actual benefit payments—whereas the number of employer-reported contractual hours in the Employment Register often misses such benefits spells. The estimations show that our model has greater explanatory power for women than for men, partly because contractual hours and earnings have a higher correlation with actual hours for women than for men.

How good is our imputation of hours worked? The explanatory power of our model is relatively high with an overall R-squared of about 0.23 for men and 0.49 for women in the out-of-sample test. This is comparable to the explanatory power of Mincer-type linear regressions on data from the PSID. Regressions on these data with annual hours worked as the dependent variable and standard covariates as explanatory variables (gender, education, a quartic in age, and, most importantly, annual earnings) yield an overall R-squared of 0.45 for women and 0.16 for men (see Online Appendix C for details).16

| Level | ||||||||

| Depth | 5 | 4 | 3 | 2 | 1 | 4 | 3 | 2 |

| Wage | Yes | Yes | Yes | Yes | Yes | No | No | No |

| Men | 28.09 | 26.82 | 25.69 | 24.73 | 23.41 | 22.63 | 21.67 | 20.80 |

| Test | 22.06 | 22.42 | 22.89 | 22.96 | 22.23 | 18.15 | 17.94 | 17.77 |

| Women | 50.65 | 49.65 | 48.79 | 48.08 | 47.21 | 42.79 | 42.06 | 41.31 |

| Test | 47.88 | 48.45 | 48.73 | 46.66 | 47.83 | 42.13 | 41.04 | 41.07 |

Given that our focus is to quantify the importance of hours changes for earnings risk, we investigate the average hours growth conditional on earnings changes from our imputation approach compared to those from the AKU and Employment Register data. To this end, Figure 1 plots the changes in imputed hours measure as a function of earnings changes, alongside changes in actual hours and contracted hours. Our imputed hours changes are remarkably close to the actual changes in the Labor Force Survey data. We conclude that the changes in imputed hours is a good estimate of the changes in actual hours. In the rest of the paper, we use imputed hours as our measure of annual hours worked.

We close this section with a discussion of measurement error (henceforth, m.e.) in AKU hours and imputed hours. Note first that actual hours in AKU is likely to contain m.e. both for standard reasons of survey misreporting and because our measure is constructed by multiplying hours worked in four random weeks by 13. We believe it is reasonable to assume that the m.e. in our hours variable is classical.17 Fortunately, classical m.e. in AKU hours would not affect the imputation model because it would by construction be independent of the right-hand regressors in equation (1). Second, any imputation procedure will induce some m.e. in the predicted hours relative to the true hours worked. However, we show in Section 5.2 that this m.e. in our context is of minor magnitude. Moreover, classical m.e. in imputed hours does not affect the analysis in Section 4 on nonlinear persistence because there we average over a large number of individuals, implying that the classical m.e. will wash out.18

Finally, we recognize that individuals who actually respond to any survey, including the AKU survey, will by construction be selected (as they are the ones who responded). Because we linked all AKU interviewees to the register data, we can assess the extent to which those who respond to AKU are selected relative to those who have incomplete or missing responses in AKU. Appendix Tables A.1 and A.2 document that the AKU sample has somewhat lower variance of growth in register hours and lower variance of earnings and earnings growth than the full population of men. The main reason for the lower dispersion of earnings and hours in the AKU sample is that the survey undersamples individuals with low earnings and individuals with large changes in earnings and register hours. The differences in skewness and kurtosis are small. Note that all the analysis in the paper is done on the full sample and the purpose of the AKU data is only to provide an imputation model of hours worked. We conjecture that our imputation model for hours is not significantly affected by the selection in AKU because our CART regression-tree model explicitly incorporates non-linearities associated with low earnings and low register hours. In particular, our CART model has separate branches and, hence, separate regressions at each node, for individuals with very low earnings and very low register hours.

3.3 Sample Selection and Empirical Methodology

We follow a nonparametric empirical methodology building on Guvenen et al. (2019); Guvenen et al. (2014). The idea is to group workers with similar observables at a sufficiently fine level so that they can be thought of as approximately ex ante identical. Then, for each such group, we investigate the properties of income changes as a proxy for the nature of idiosyncratic risk that individuals within that group are facing. This methodology allows us to uncover the heterogeneity in the nonnormalities and nonlinearities in earnings dynamics that different groups of workers face.

Base Sample

Our base sample is a revolving panel of 25- to 60-year-old workers with a reasonably strong labor market attachment. We first define an individual-year earnings observation as being admissible for that year if the individual (i) is between 25 and 60 years old and (ii) has labor earnings above \(Y_{\text{min},t}=5\%\) of median earnings and (iii) works more than 200 (imputed) hours per year.19 Then, for each year \(t\) between 2003 and 2013, we select individuals who are admissible in \(t-1\) and in at least two more years between \(t-5\) and \(t-2\). This condition ensures that the individual has a reasonably strong labor market attachment. Given these restrictions, our sample consists of 19.9 million individual-year observations in total, which is roughly 900,000 males and 800,000 females per year.

Worker Groupings

One of the key observables we sort workers on is their recent earnings (RE) between \(t-1\) and \(t-5\), \(\bar{Y}_{t-1}^{i}\). By requiring individuals to have at least three years of admissible income in the last five years, we ensure that we can compute a reasonable measure of each person’s average past income. We compute each individual’s RE \(\bar{Y}_{t-1}^{i}\) by summing his or her annual wages normalized by age effects between \(t-1\) and \(t-5\): \[ \bar{Y}_{t-1}^{i}\equiv \sum _{s=1}^{5}\frac{\tilde{Y}_{t-s,h-s}^{i}}{\text{exp}(d_{h-s})}, \] where \(\tilde{Y}_{t-s,h-s}^{i}\) denote the annual wage earnings of individual \(i\) who is \(h\) years old in year \(t\). The constants \(d_{h-s}\) are age dummies from regressing log individual earnings on a full set of age, gender, and cohort dummies. Next, we group workers by their gender and age in \(t-1\). Within each of these groups, we rank workers into 10 deciles with respect to their recent earnings \(\bar{Y}_{t-1}^{i}\).20

Growth Rate Measures

We use two types of measures of growth in the variables of interest \(Z\) where \(Z\) is earnings, income, hours worked, or hourly wages. The first measure focuses on growth in average \(\bar{Z}\) for a group of similar workers. In particular, for a group \(j\) of workers who have similar observable characteristics, \(V_{t+1}^{j}\) (namely, they are in the same age group, have similar recent earnings in \(t-1\), and have experienced a similar earnings change between \(t\) and \(t+1\)), we define the average growth between \(t\) and \(t+k\) as follows: \[ \Delta \mathrm{RA}_{t,t+k}^{Z}=\log (\bar{Z}_{t+k,h+k}^{j}\mid V_{t+1}^{j})-\log (\bar{Z}_{t,h}^{j}\mid V_{t+1}^{j}), \] where \(\bar{Z}_{t,h}^{j}\equiv \sum _{i=1}Z_{t,h,i}^{j}\) and \(Z_{t,h,i}^{j}\) is variable \(Z\) for individual \(i\) in group \(j\).

We refer to this as the representative agent (RA) change. One major advantage of this approach is that it incorporates the extensive margin when going forward. For example, even though a person drops out of the labor market, the impact of his or her (zero) earnings will be included through the average change for the group. Another advantage of the representative agent change is that the persistence of the original shock to earnings is identified in a nonparametric way. Assuming that future idiosyncratic shocks to individuals in the group are independent, the future idiosyncratic innovations will wash out across group members. Therefore, the evolution of the group mean \(\bar{Z}\) captures the expected evolution after the initial shock for the group. We study both short-term and long-term RA changes.

When investigating the distribution of (idiosyncratic) shocks (in Section 5), we focus instead on a measure of individual growth because we are interested in the higher-order moments of dynamics in outcomes for individuals. We work with the log growth rate in individual-specific variables between \(t\) and \(t+k\): {}{k}z_{t}{i}z{t+k,h+k}{i}-z{}_{t,h}{i}, where \(z_{t}^{i}\equiv \log Z_{t,h}^{i}-d_{h}^{z}\) denotes the log of variable \(z\) net of age effects of the same variable. This is a widely used growth rate measure, and its higher-order moments for a log-normal distribution are familiar to most readers (zero skewness and a kurtosis coefficient of 3). Recall that our sample includes observations with labor earnings above \(5\%\) of median earnings. Thus, when calculating \(\Delta _{\log}^{k}z_{t}^{i}\), we drop individuals from the base sample whose observations are below the cutoff in either \(t\) or \(t+k.\)21

4 Dissecting Earnings Dynamics

Changes in earnings are due to changes in hours worked, changes in the hourly wage rate, or joint changes. This section documents the extent to which earnings dynamics are driven by hours versus hourly wages. The answer to this question matters for many economic questions, including risk sharing and social insurance arrangements (see, e.g.,? and?). A large literature, dating back to seminal papers by Abowd and Card (1989), MaCurdy (1981), Altonji (1986), and Abowd and Card (1989), has studied the covariance structure of changes in wages and hours. Most of the focus has been on uniform relations between movements in wages and movements in hours. However, data restrictions have so far made it difficult to examine possible heterogeneity in the covariance structure of wage and hours growth. In this paper, we exploit the sheer size of our administrative data and our novel imputation of hours to document the heterogeneity in the co-movements of hours and wage growth across individuals who experience earnings changes that are small versus large, negative versus positive, and across workers with different earnings histories.

We first quantify the importance of hours and wage changes for earnings changes, and then document how hours versus hourly wages account for the asymmetries and nonlinearities in earnings dynamics.

4.1 Decomposing Earnings Changes to Hours and Wage Growth

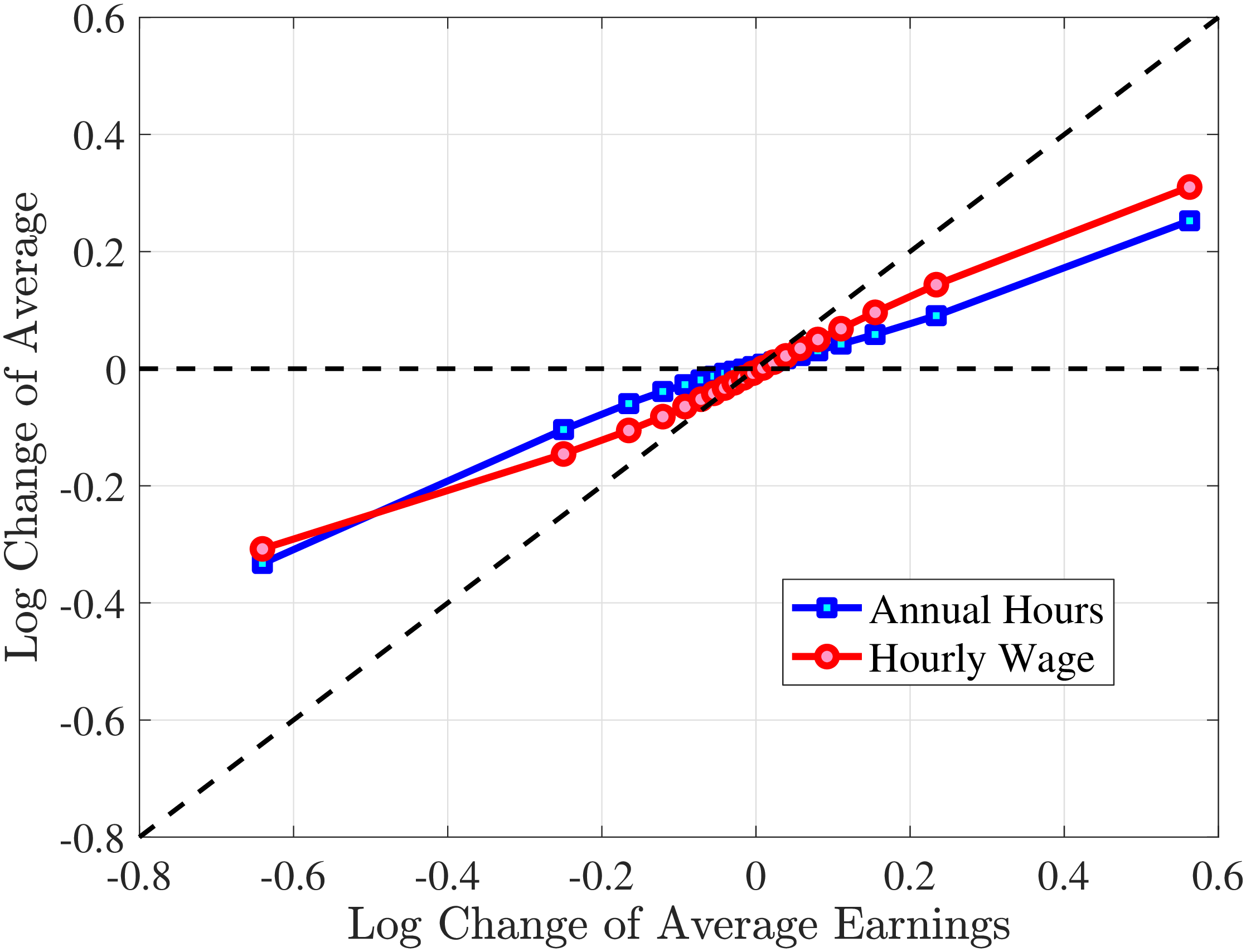

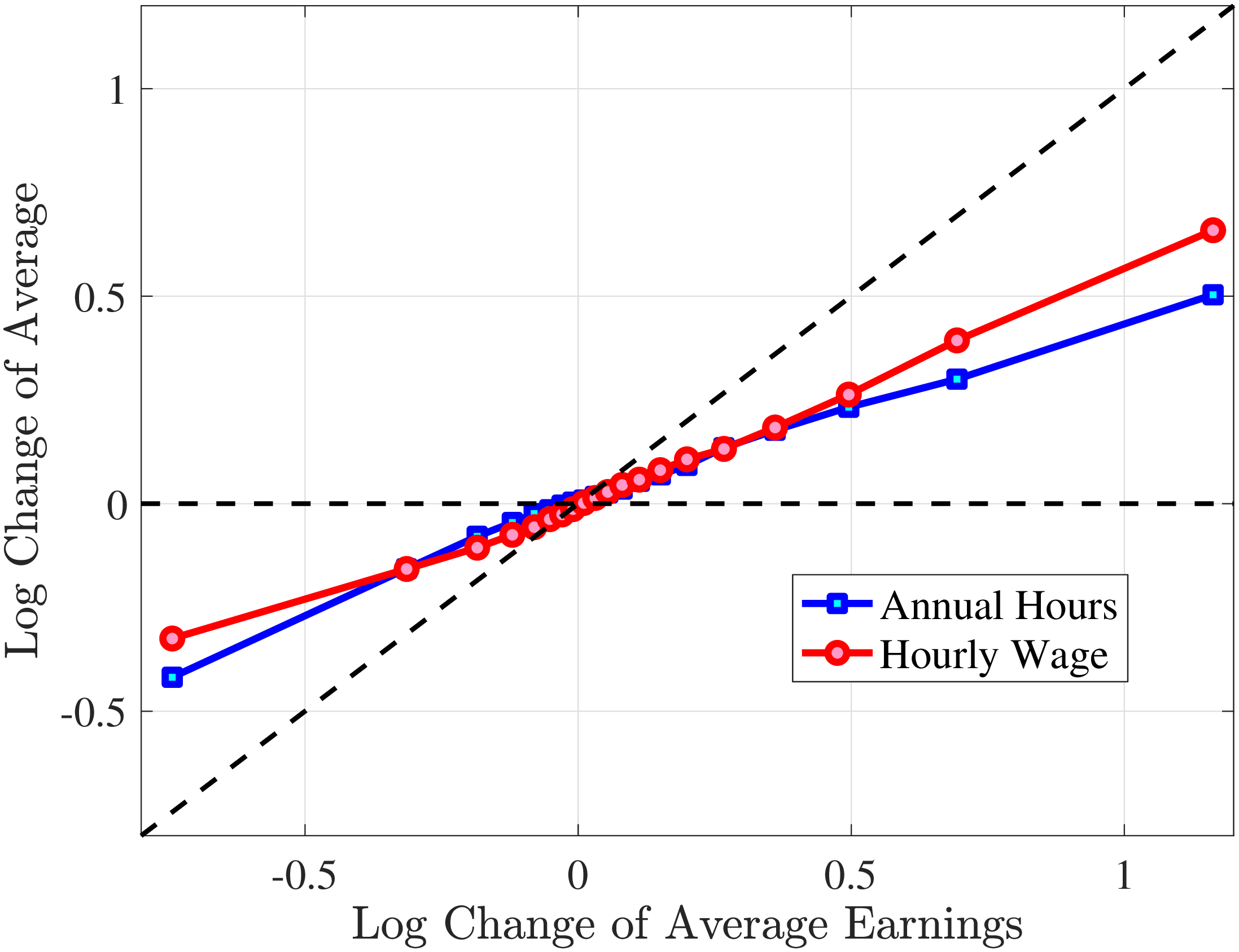

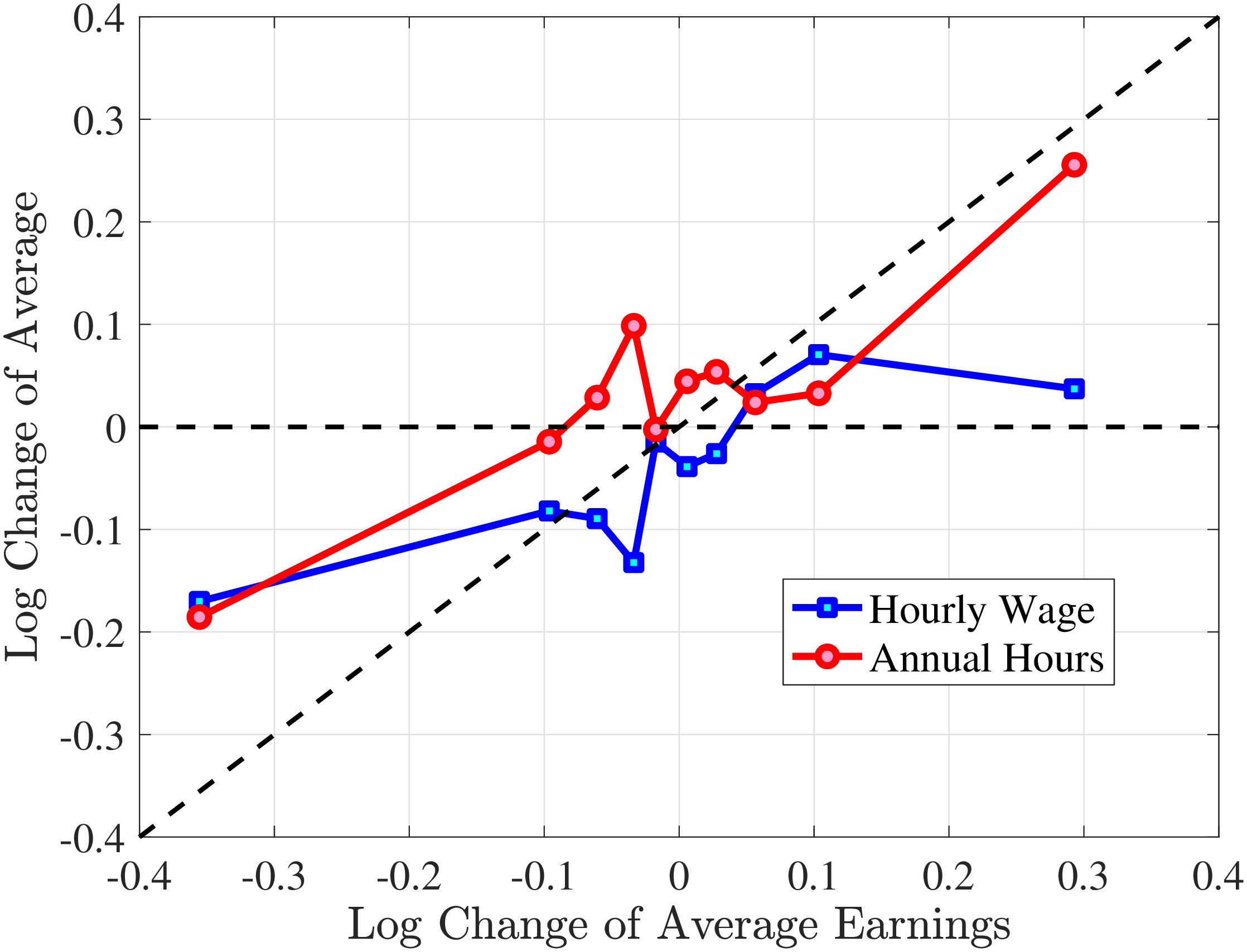

We measure the hourly wage rate as earnings/hours. This is the common approach in the literature (see, e.g., Heathcote et al. (2010a), Heathcote et al. (2014), Bick et al. (2022)) as wage rates are rarely directly observable in the data. We proceed by decomposing earnings changes into changes in hours worked versus hourly wages. To this end, we group them with respect to their earnings growth (in addition to conditioning workers with respect to age and recent earnings \(\bar{Y}_{t-1}^{i}\)).22 In particular, within each age and RE group, we rank workers on their earnings growth from \(t\) to \(t+1\) and sort them into 20 different quantiles. We treat each such finely defined group as homogeneous and plot the growth of their average hours and hourly wages on the y-axis conditional on their earnings growth between \(t\) and \(t+1\) on the x-axis.23 To control for age effects and differences in mean reversion between different groups of workers, we normalize changes on both the x- and y-axes such that their values at the median quantile cross at zero.

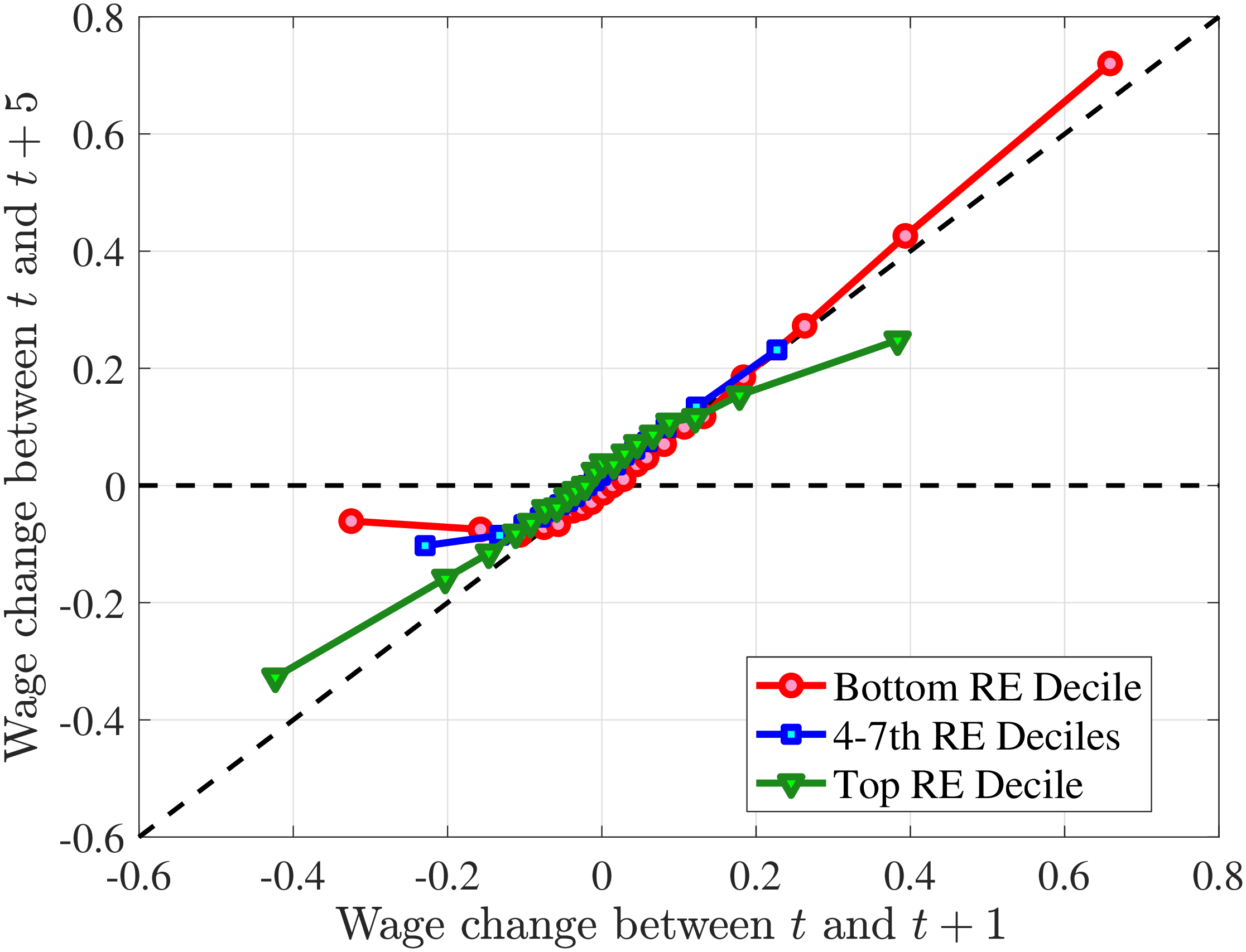

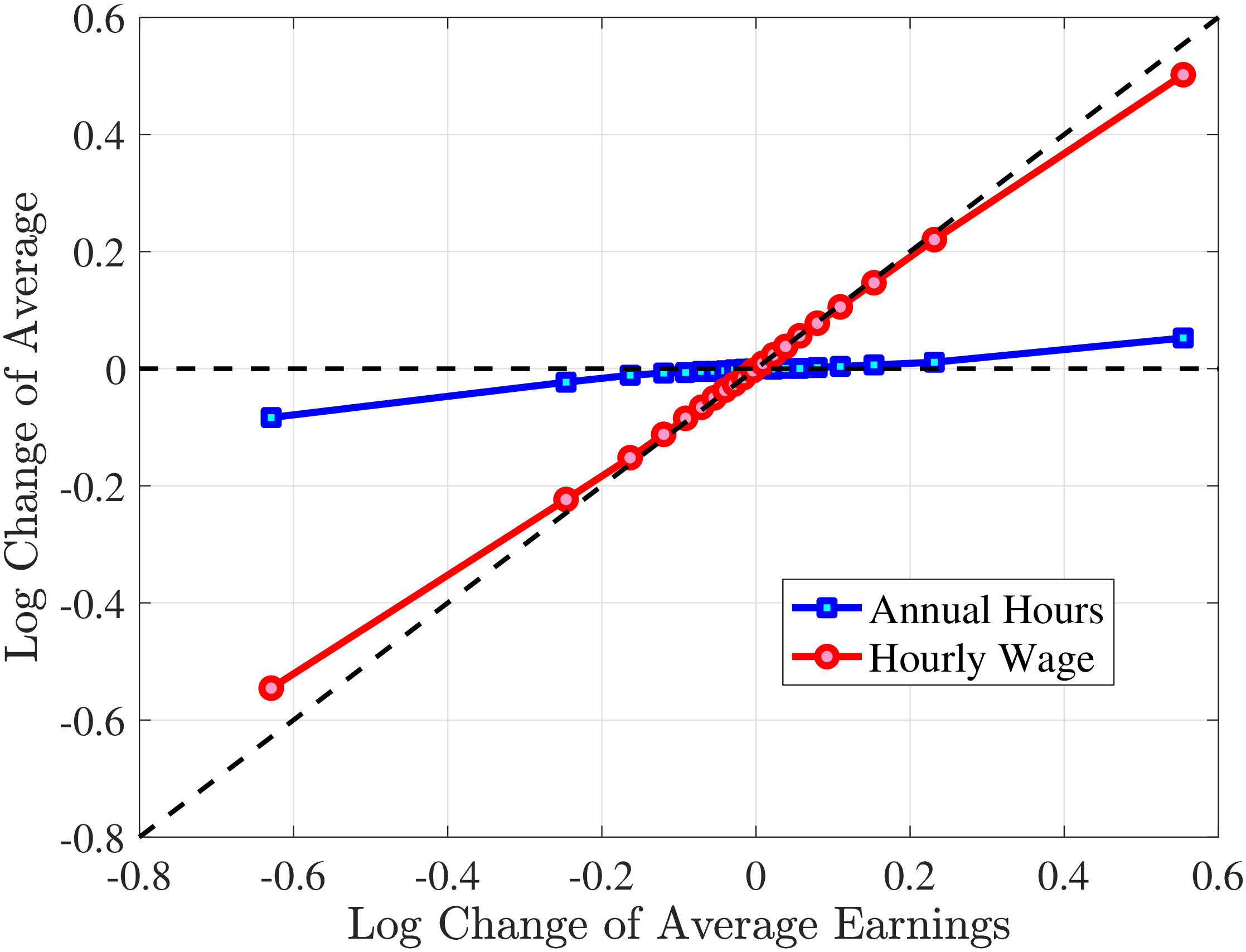

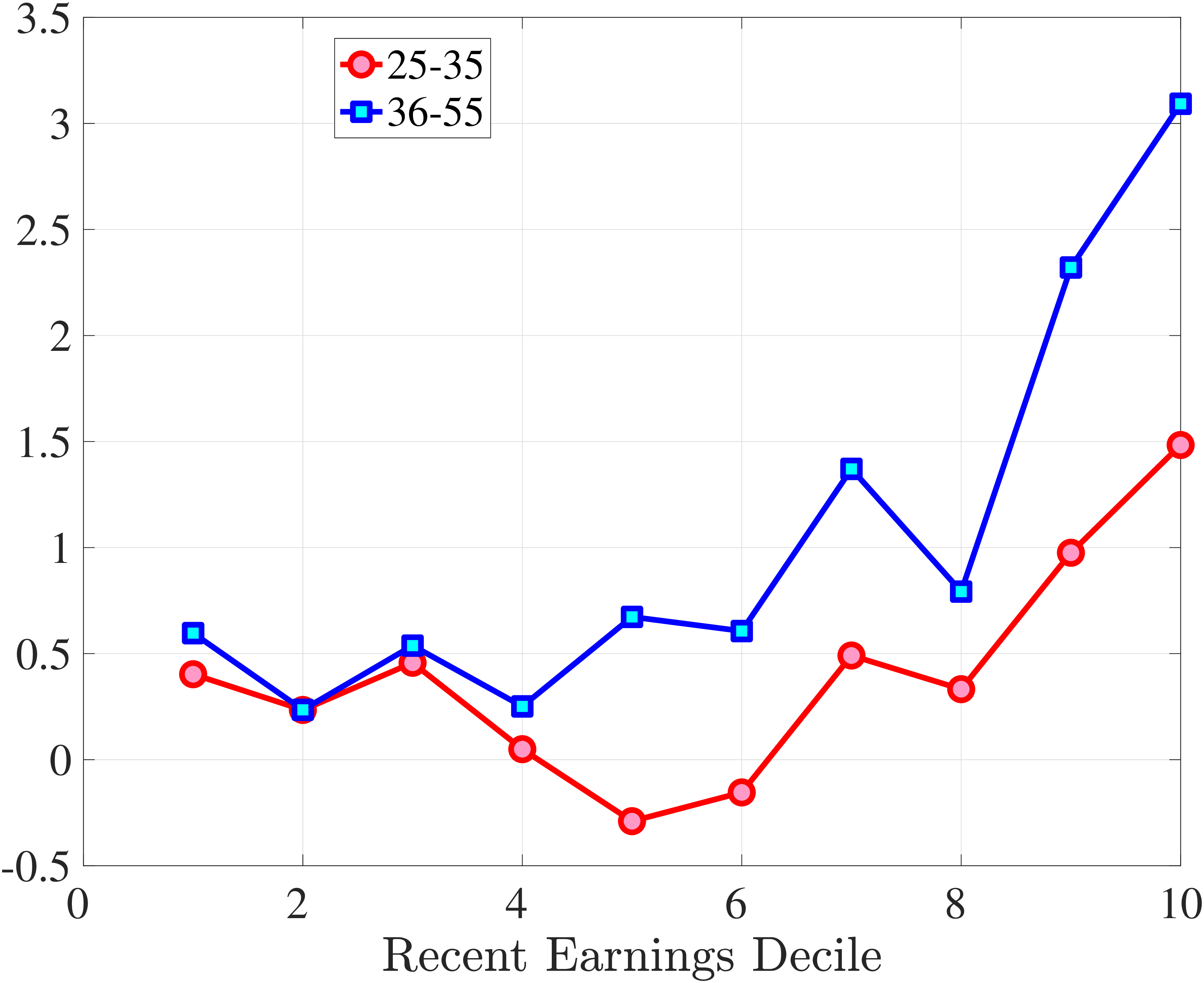

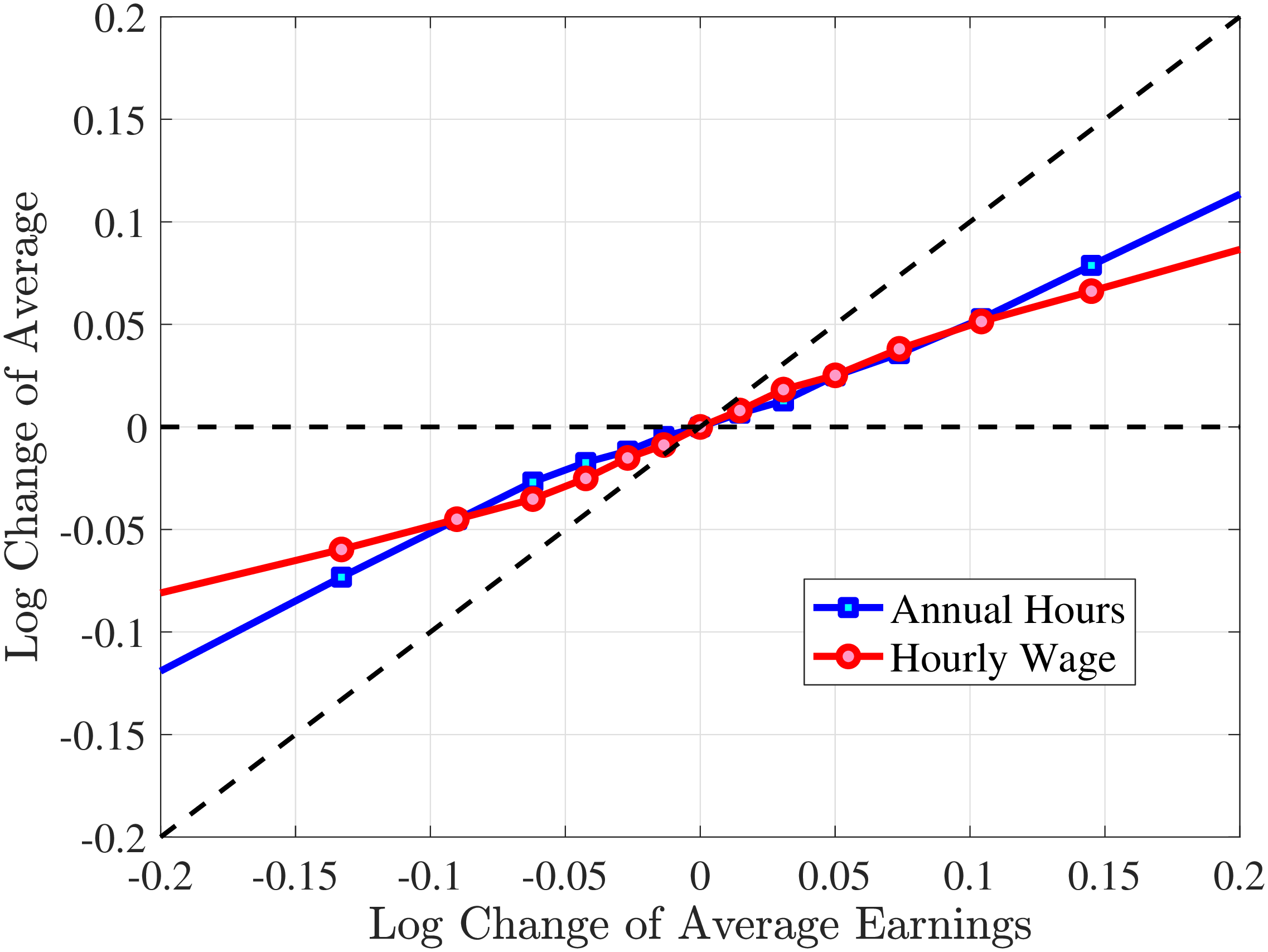

In Figure 2, we start with the 40% of prime-age males (36-55 years old) who are in the middle of the recent earnings distribution (i.e., the 4th to 7th deciles). The differences across these deciles are negligible. Note first that for large negative earnings changes, hours growth is roughly as large as wage rate growth. For example, the group of workers whose earnings decline around 60 log points on average experience a decline of about 30 log points in hours and a decline of 30 log points in wage rates. For large positive changes, the hourly wage rate increases slightly more than hours worked. Second, small earnings changes (both gains and losses) are mainly driven by wage changes. For example, for men who experience a loss of 10 log points in earnings, more than 70% of this loss is from a decline in wage rates. These results illustrate the heterogeneity in the covariance structure of wage and hours growth over the earnings change distribution.

Figure 2

–

Contribution of Hours and Wages to Earnings Shocks, 4th-7th RE Deciles

Note: The figure displays the one-year representative agent change (log change of averages) for imputed hours and imputed wage rates for 20 different groups of prime-age males (ages 36 to 55) in the 4th-7th RE deciles, plotted against their contemporaneous one-year log change in average annual earnings.

Figure: Figure 2 – Contribution of Hours and Wages to Earnings Shocks, 4th-7th RE Deciles

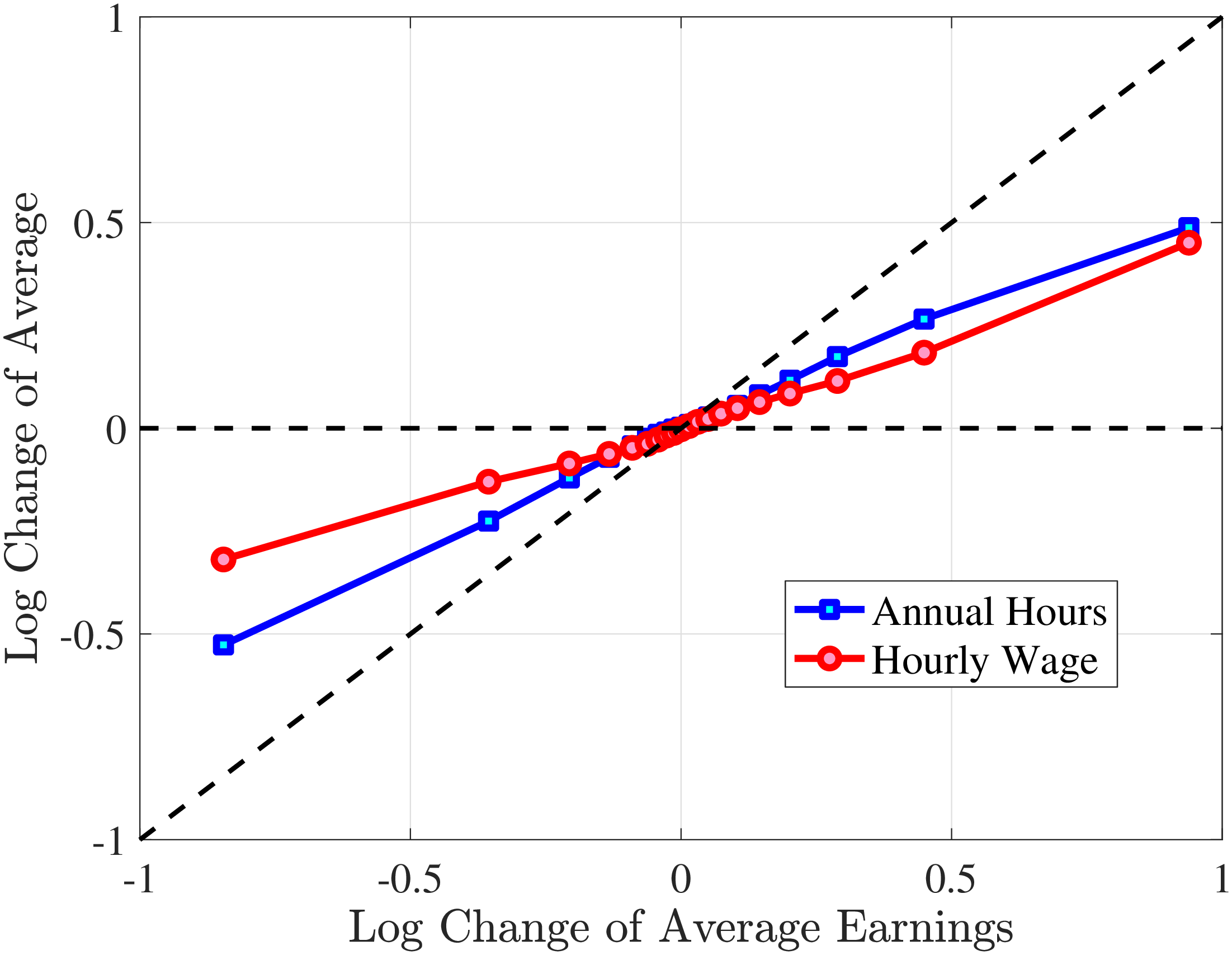

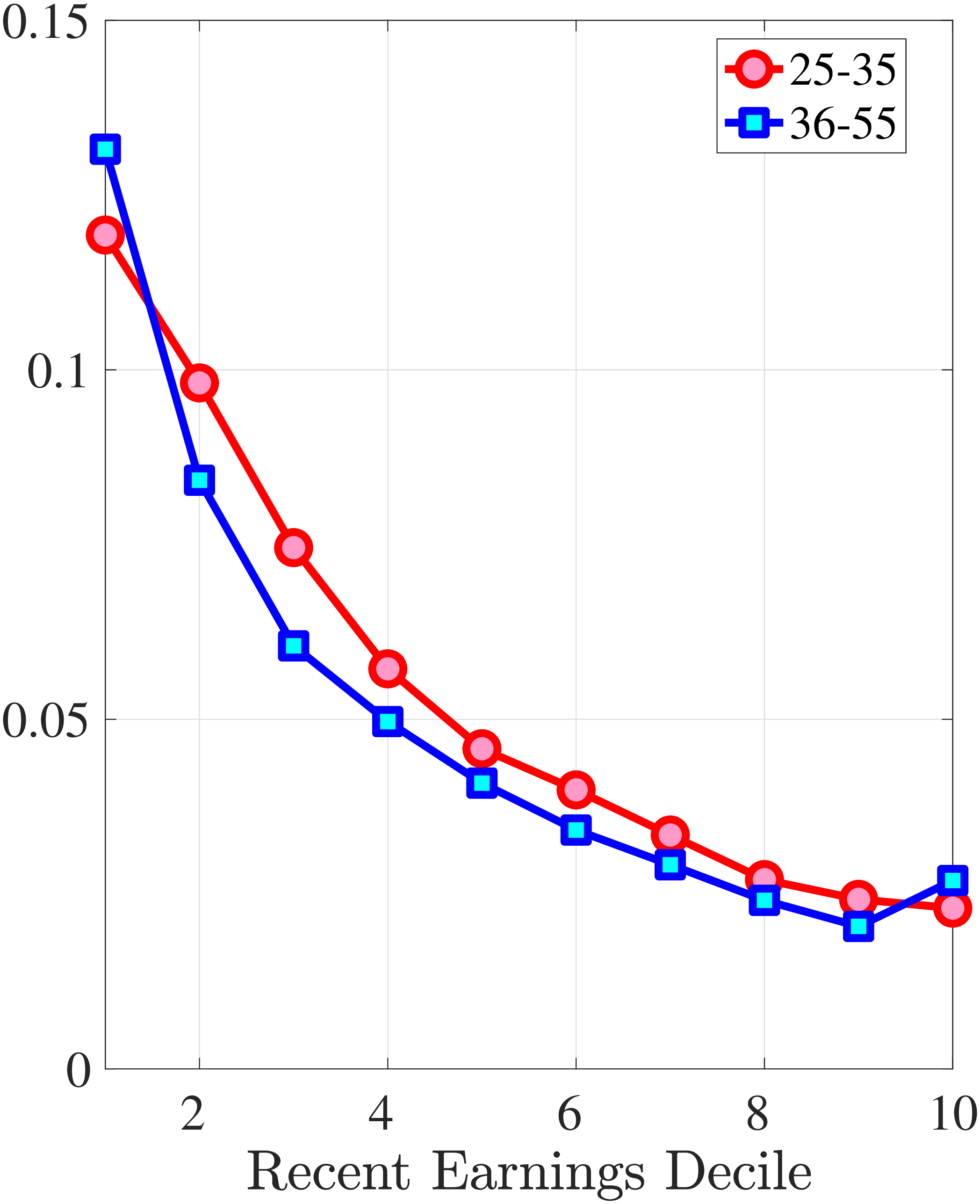

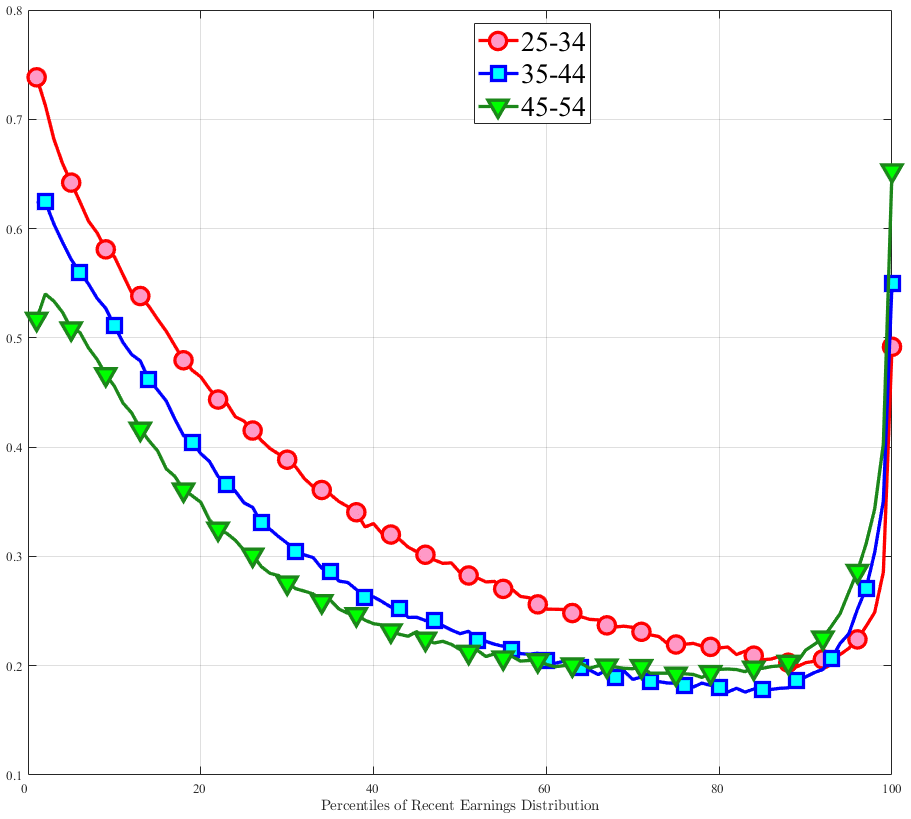

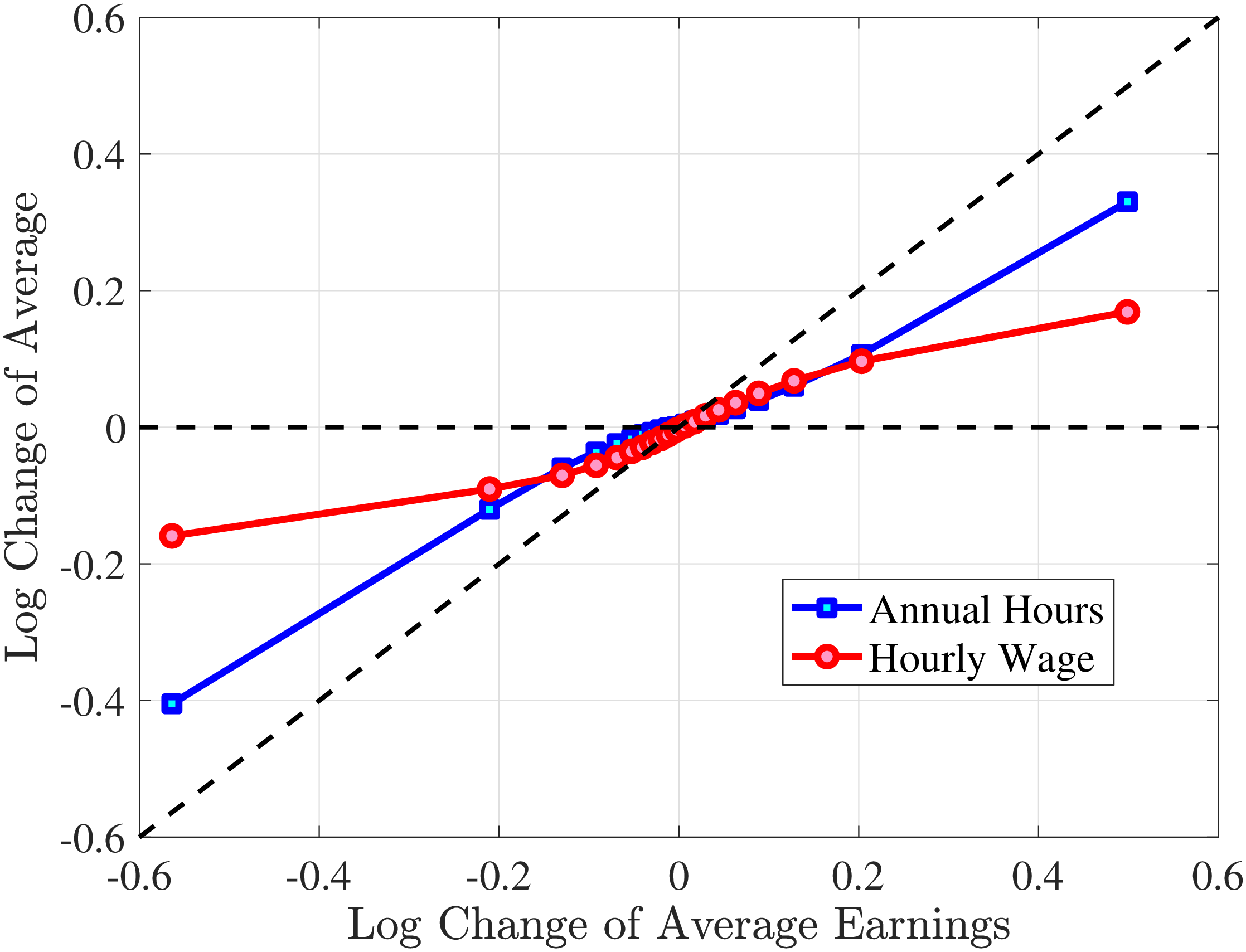

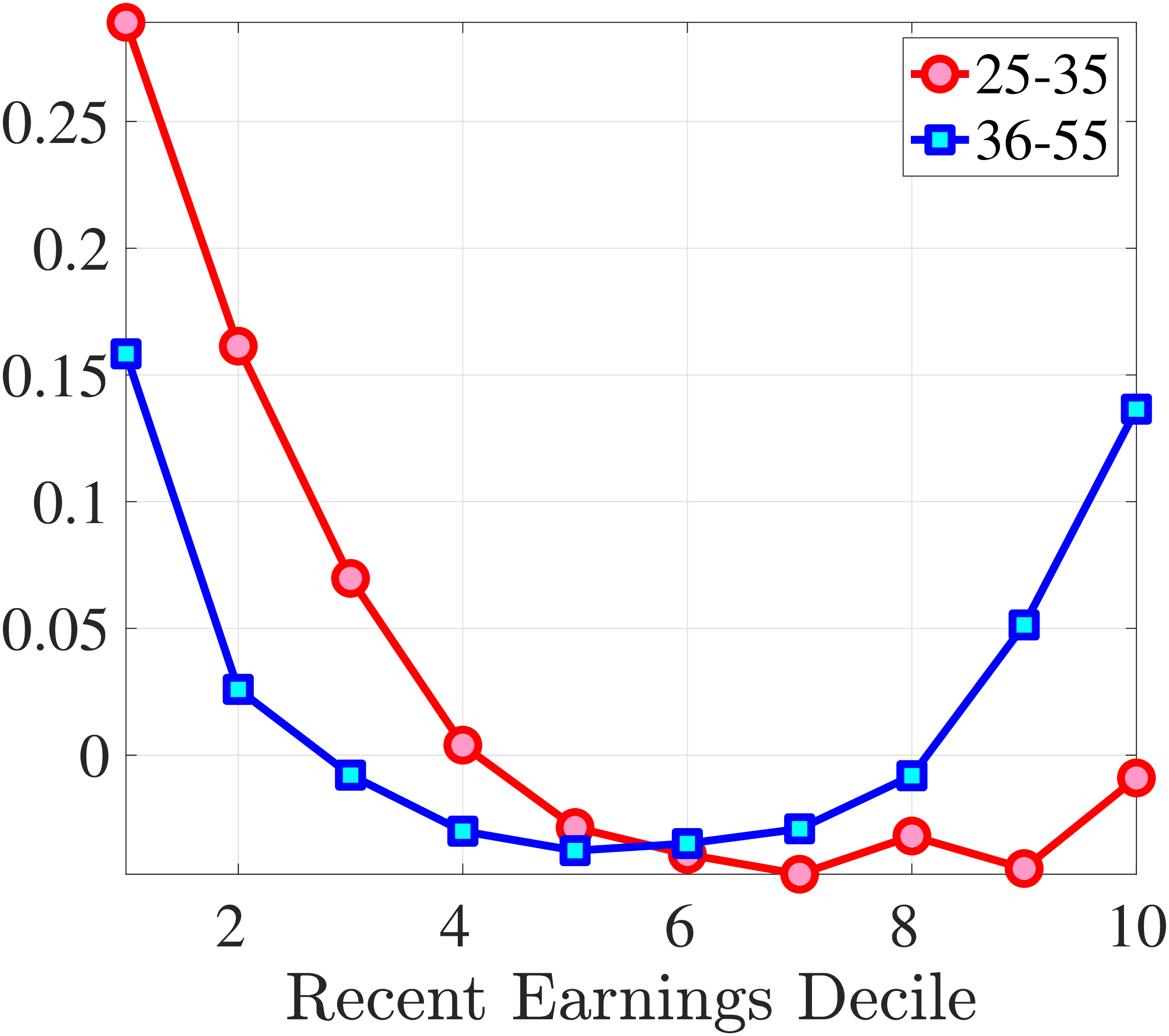

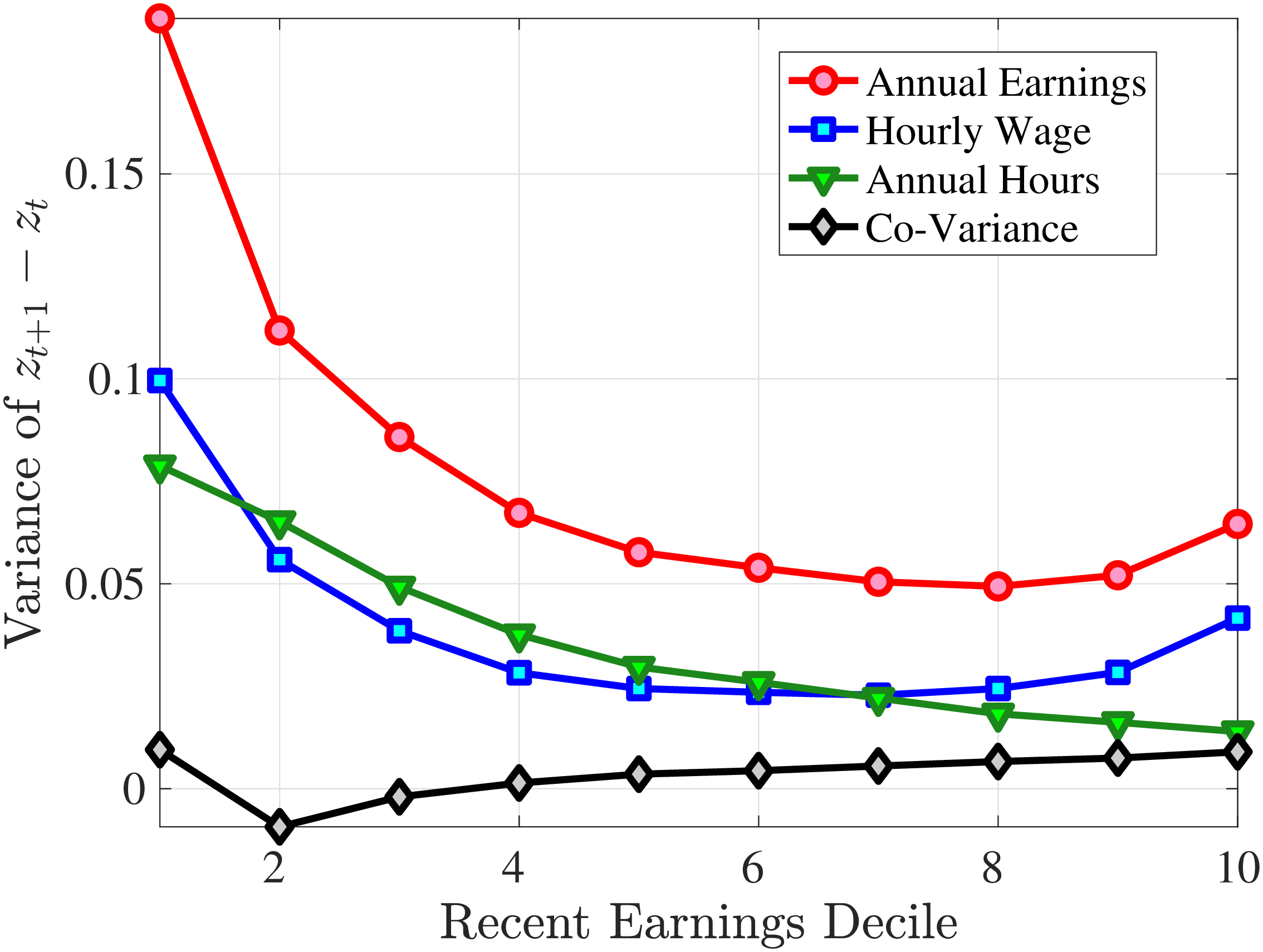

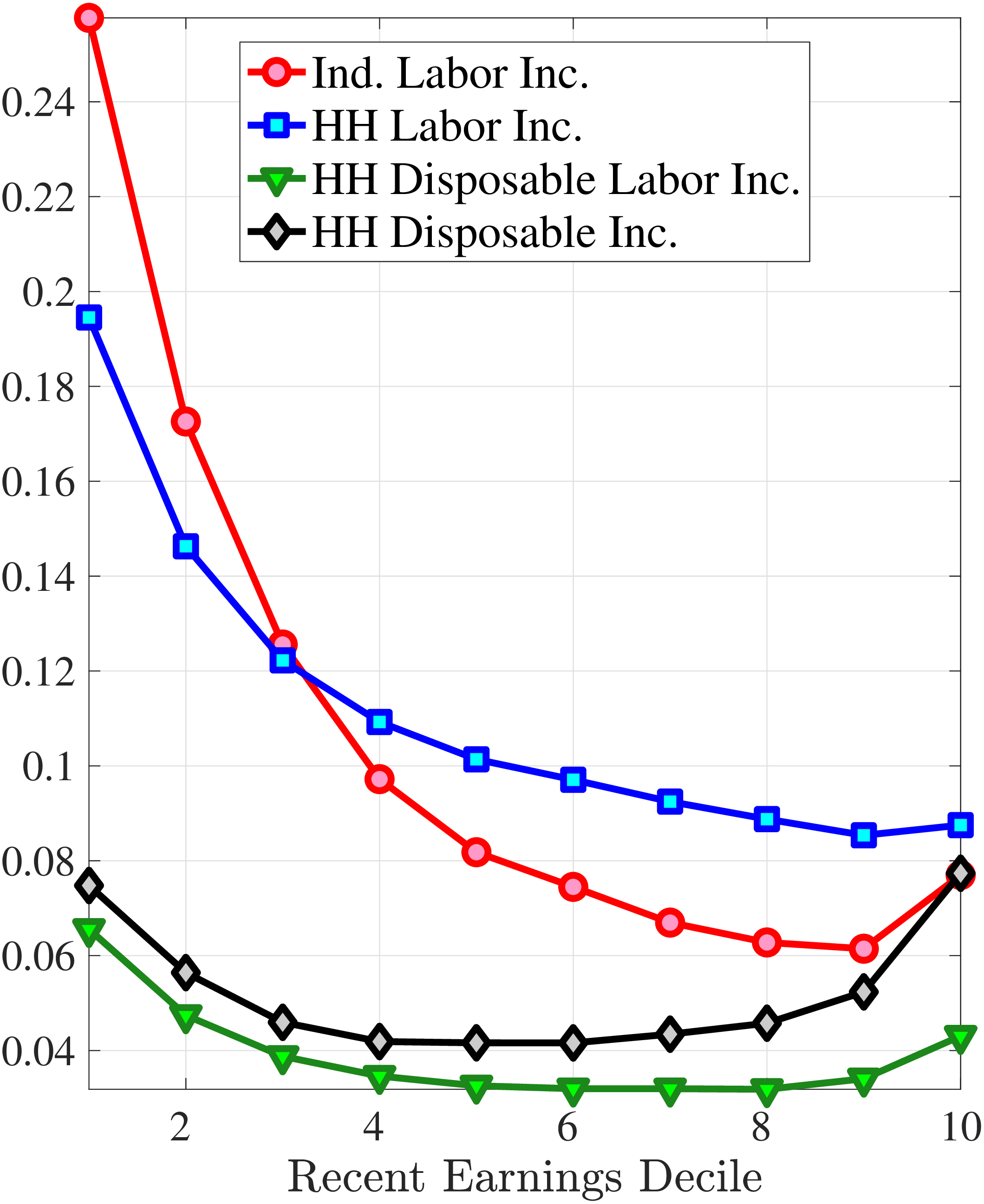

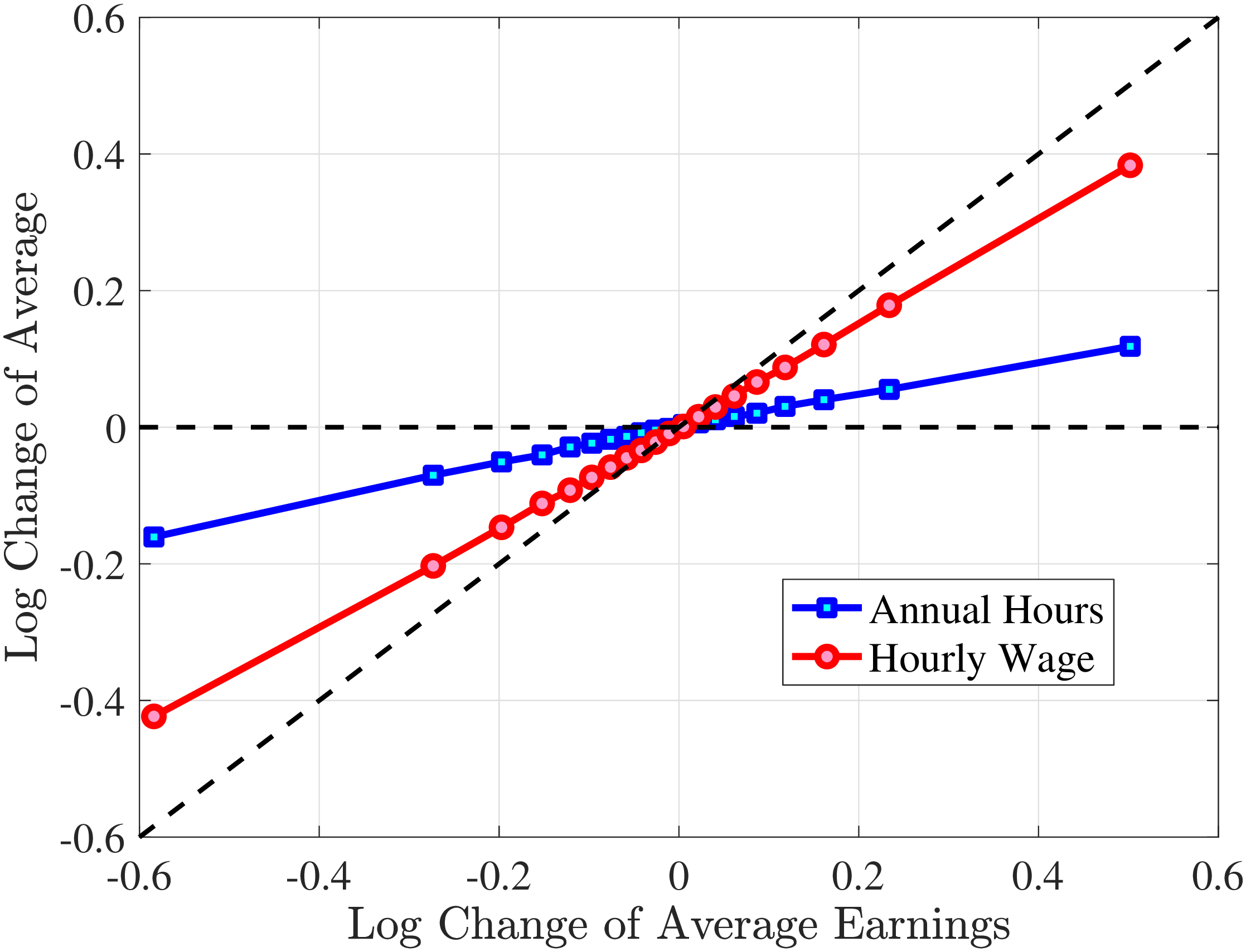

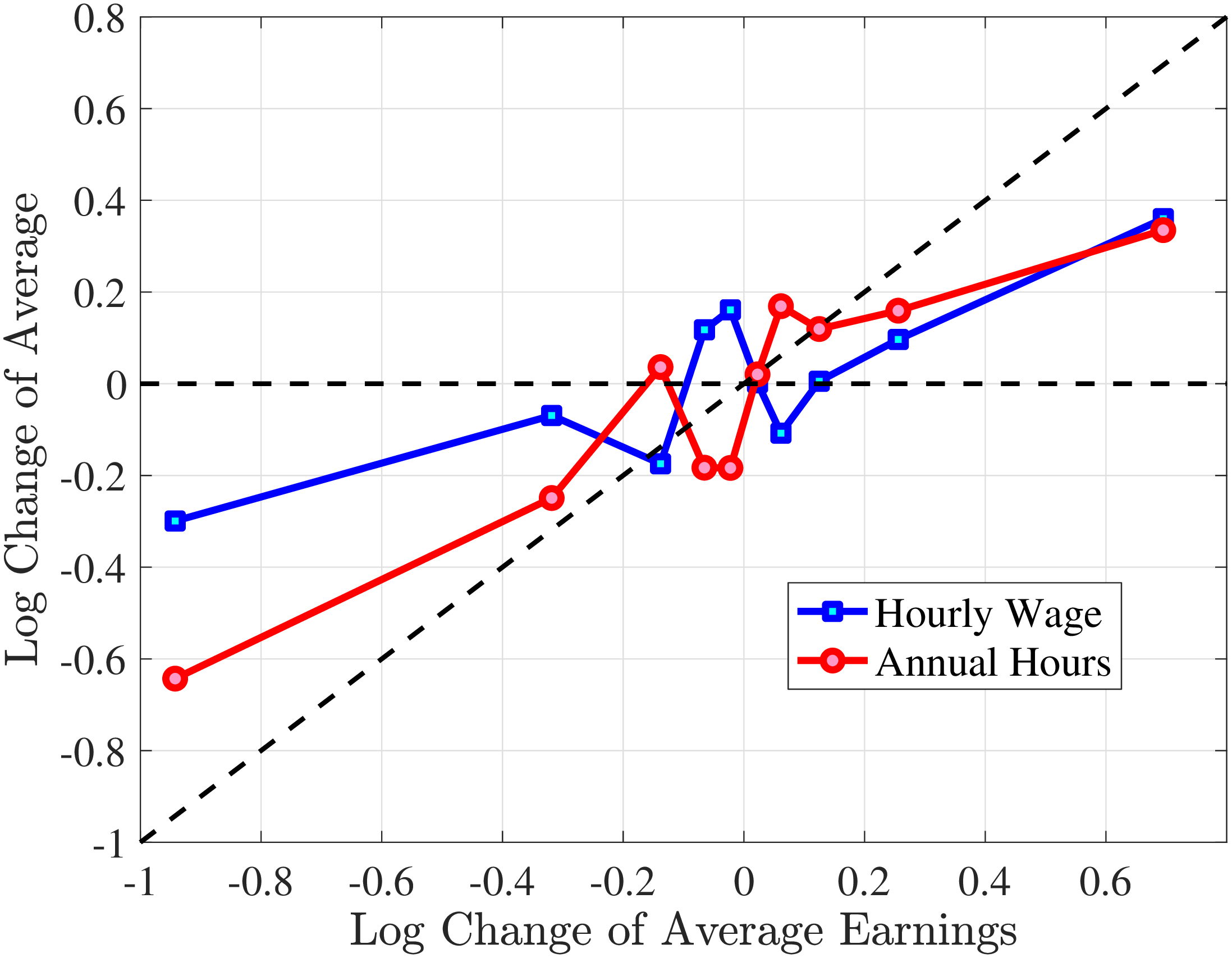

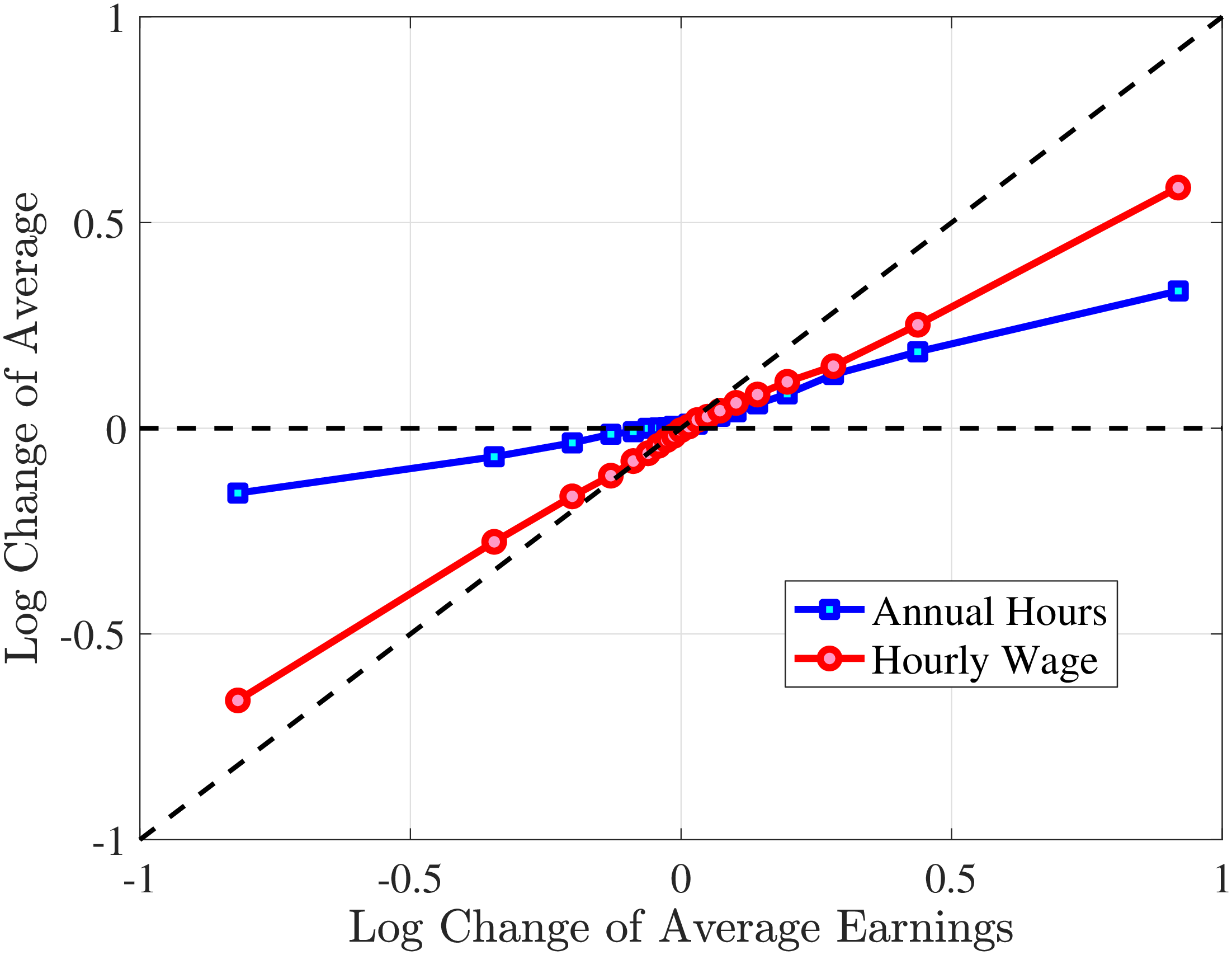

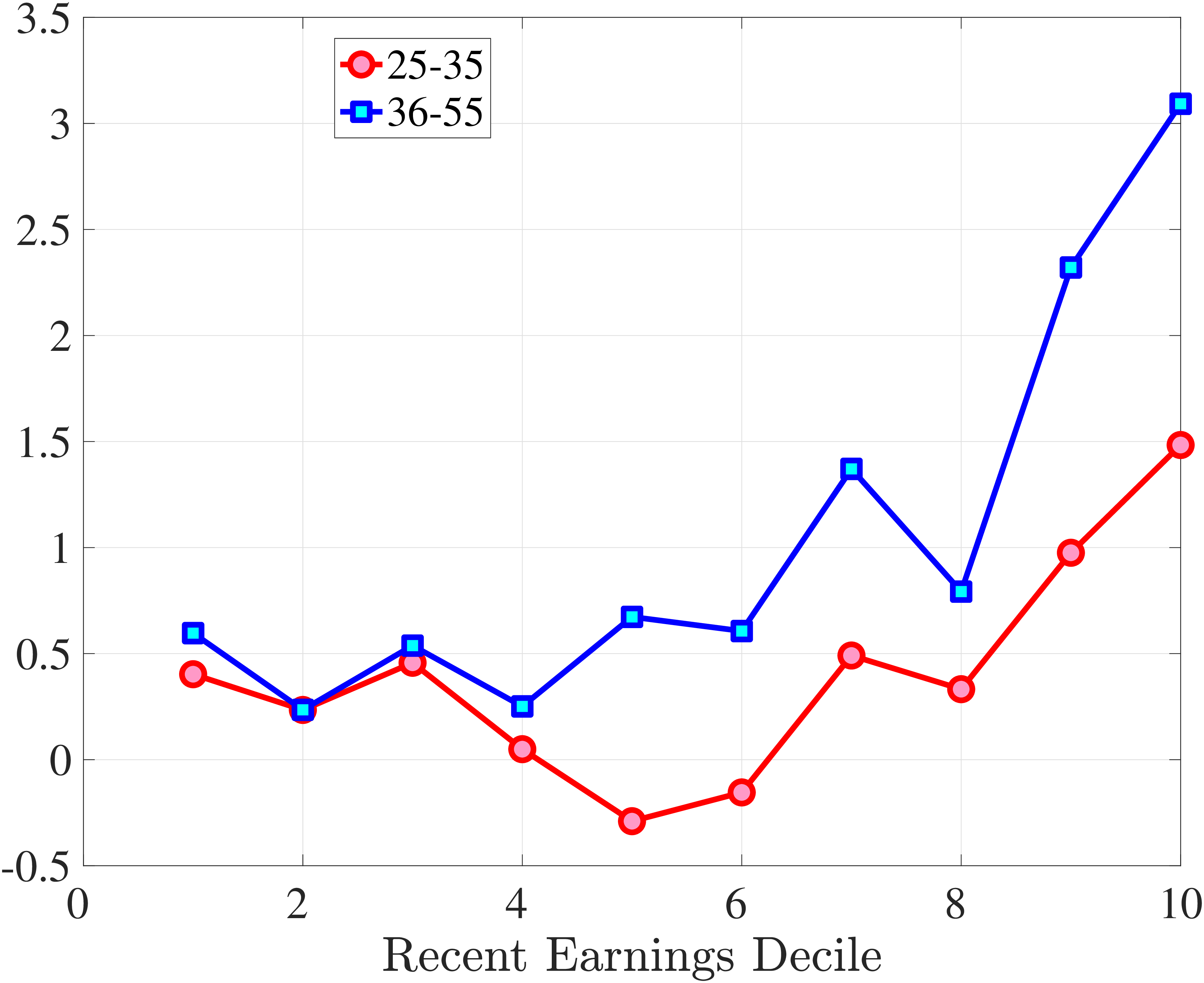

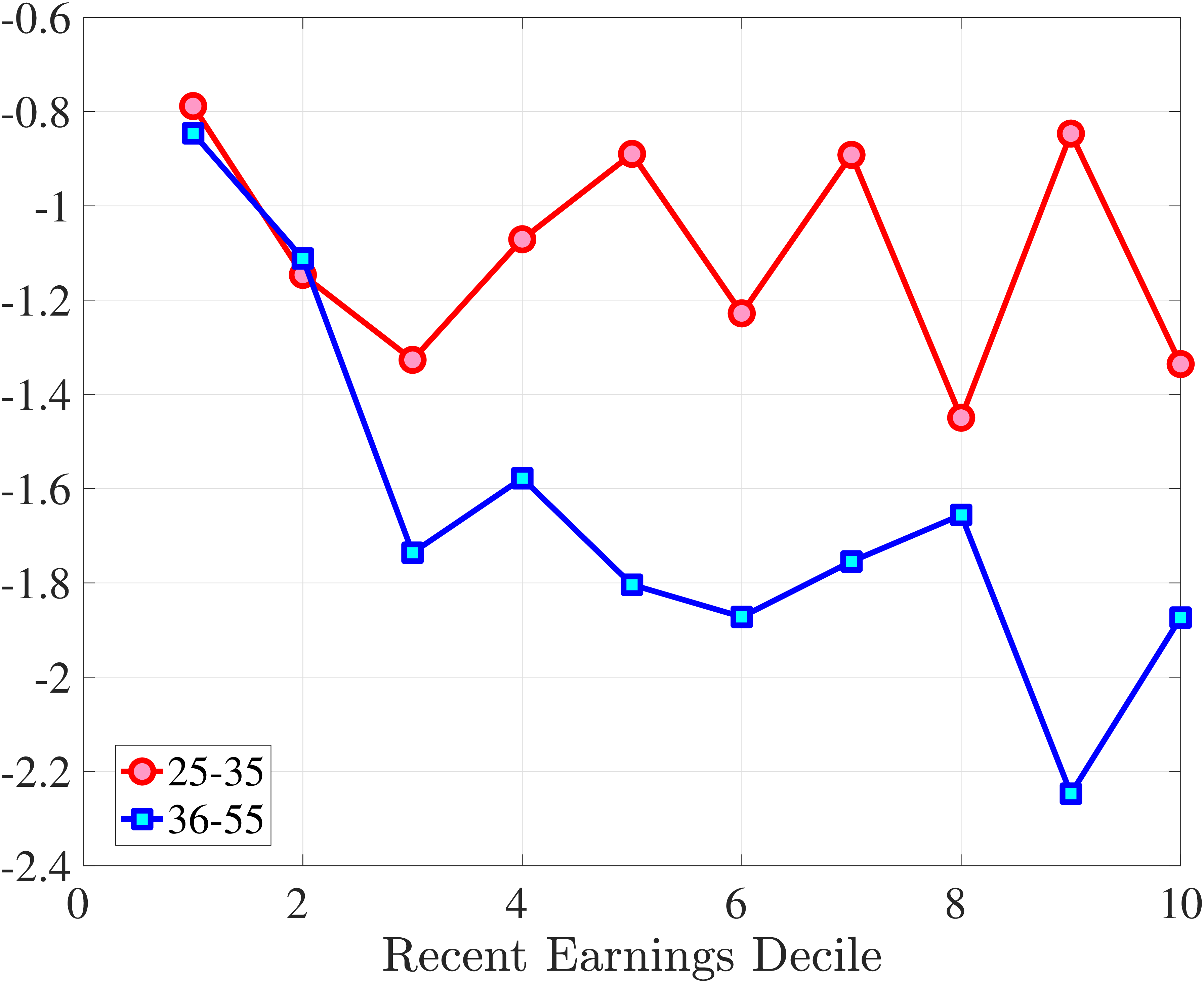

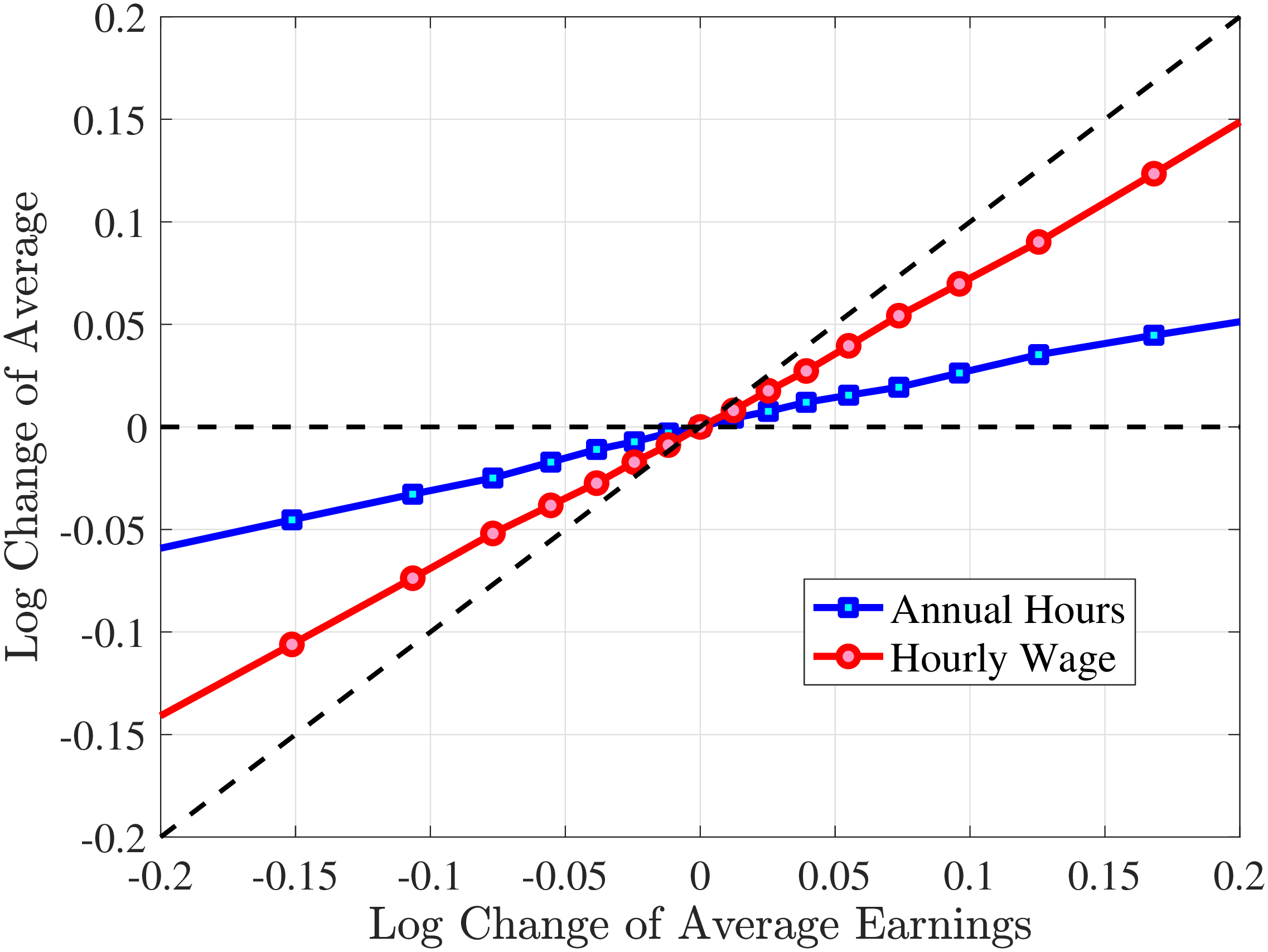

We next consider the role of hours and wage changes for the extreme ends of the recent earnings groups. Figure 3 plots the changes in hours worked and wage rates against changes in earnings for the bottom decile (left panel) and top decile (right panel) of recent earnings (see Appendix B.2 for the 2nd, 3rd, 8th, and 9th RE deciles). For the bottom decile of recent earnings, changes in hours worked are more important than changes in wage rates in accounting for earnings changes, especially for large earnings declines. This result is flipped for the top earners: high earners experience only minor changes in hours worked, and most of their earnings changes can be attributed to changes in hourly wage rates. These findings suggest that different economic mechanisms are behind the earnings dynamics of high and low earners. These results are consistent with previous research showing that unemployment risk is an important component of idiosyncratic risk for low-income workers, whereas wage fluctuations are the main drivers of income risk of workers at the higher end of the income distribution who have more stable jobs (Karahan et al. (2019)).

1st RE Decile

10th RE Decile

Figure 3

–

Contribution of Hours and Wage Rates to Earnings Shocks

Note: The figure displays the one-year representative agent change (log change of averages) for imputed hours and imputed wage rates for 20 different groups of prime-age males (ages 36 to 55) in the 1st RE decile (left panel) and 10th RE decile (right panel), plotted against their contemporaneous one-year log change in average annual earnings.

Figure: Figure 3 – Contribution of Hours and Wage Rates to Earnings Shocks

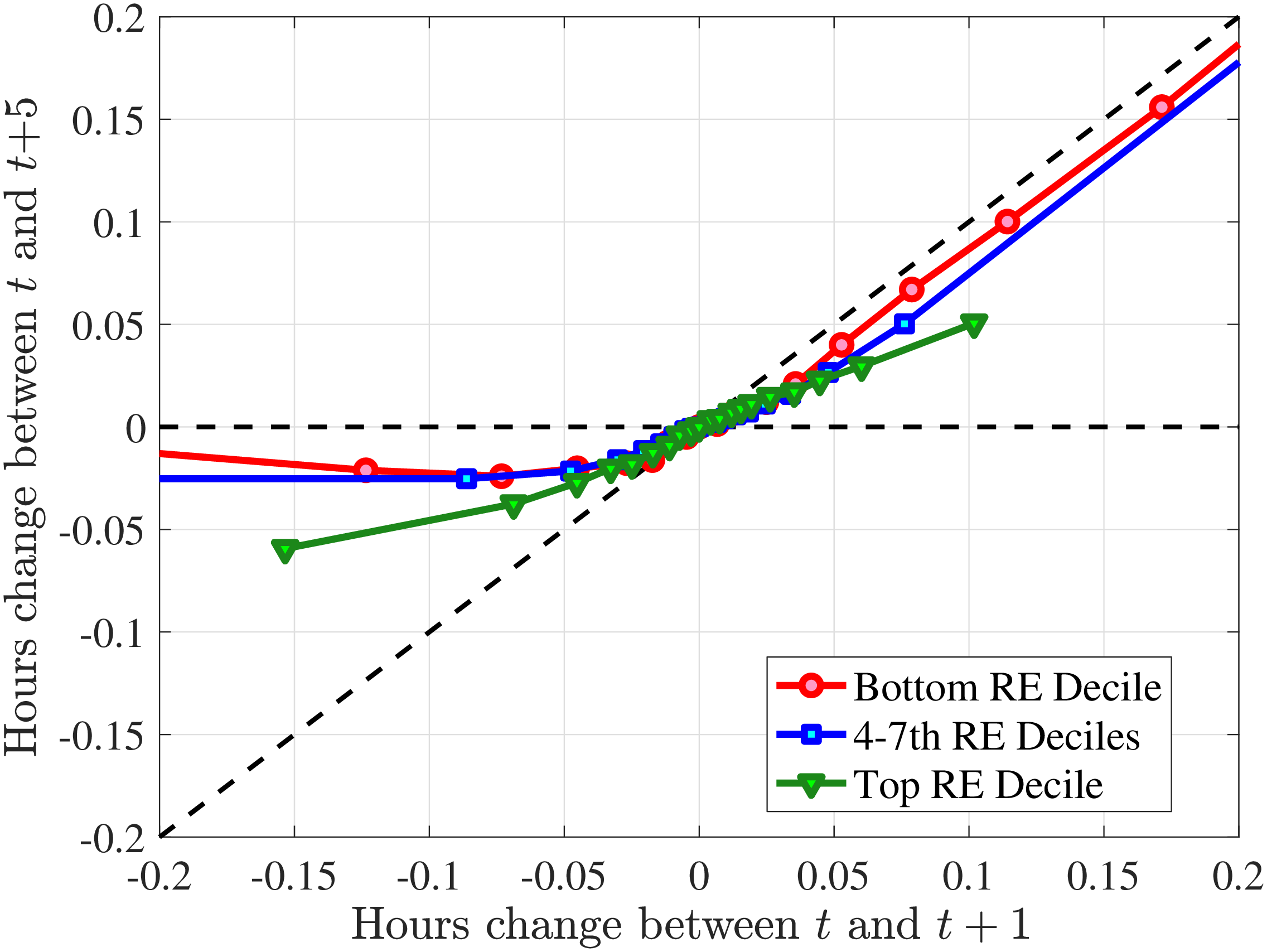

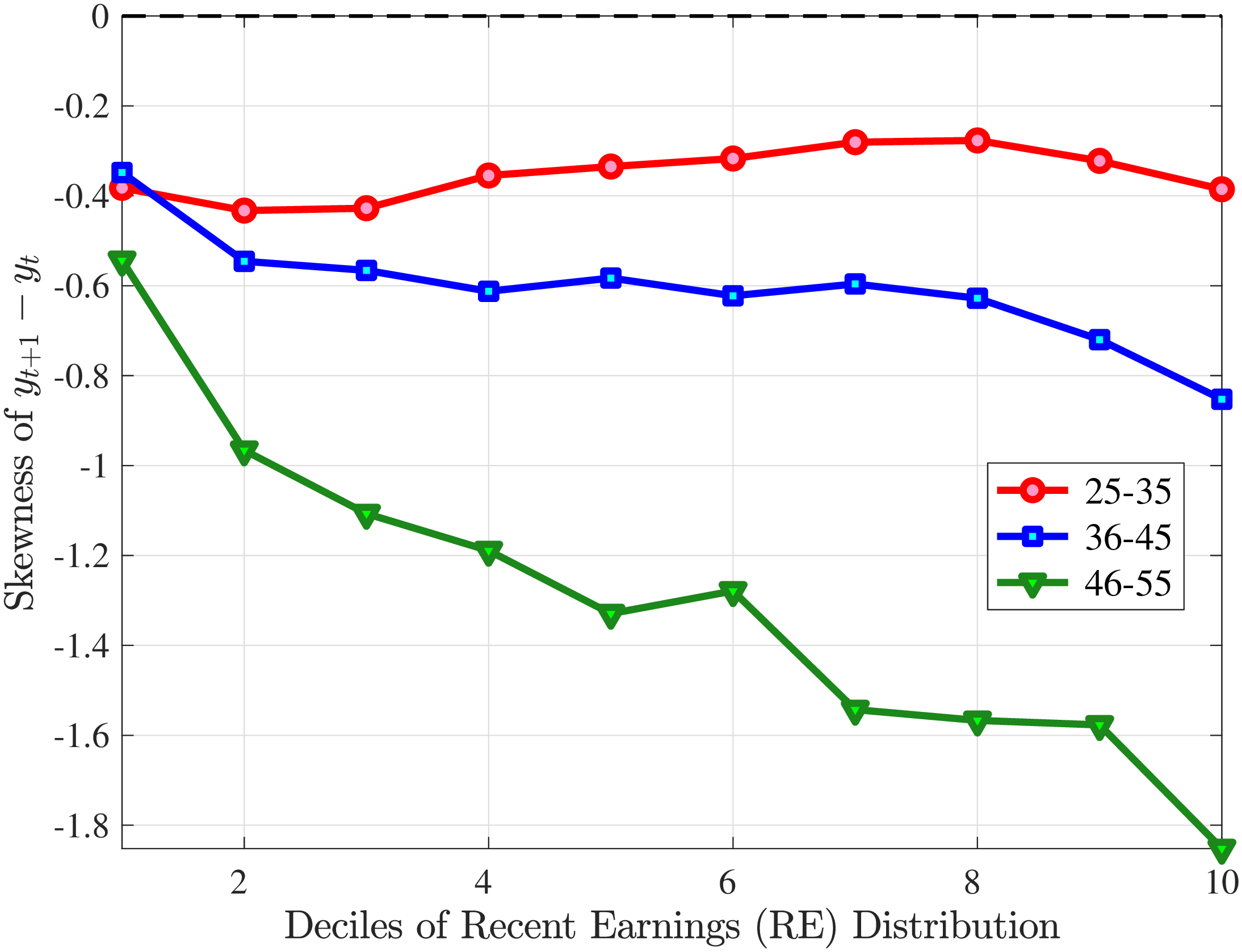

4.2 Asymmetric Mean Reversion

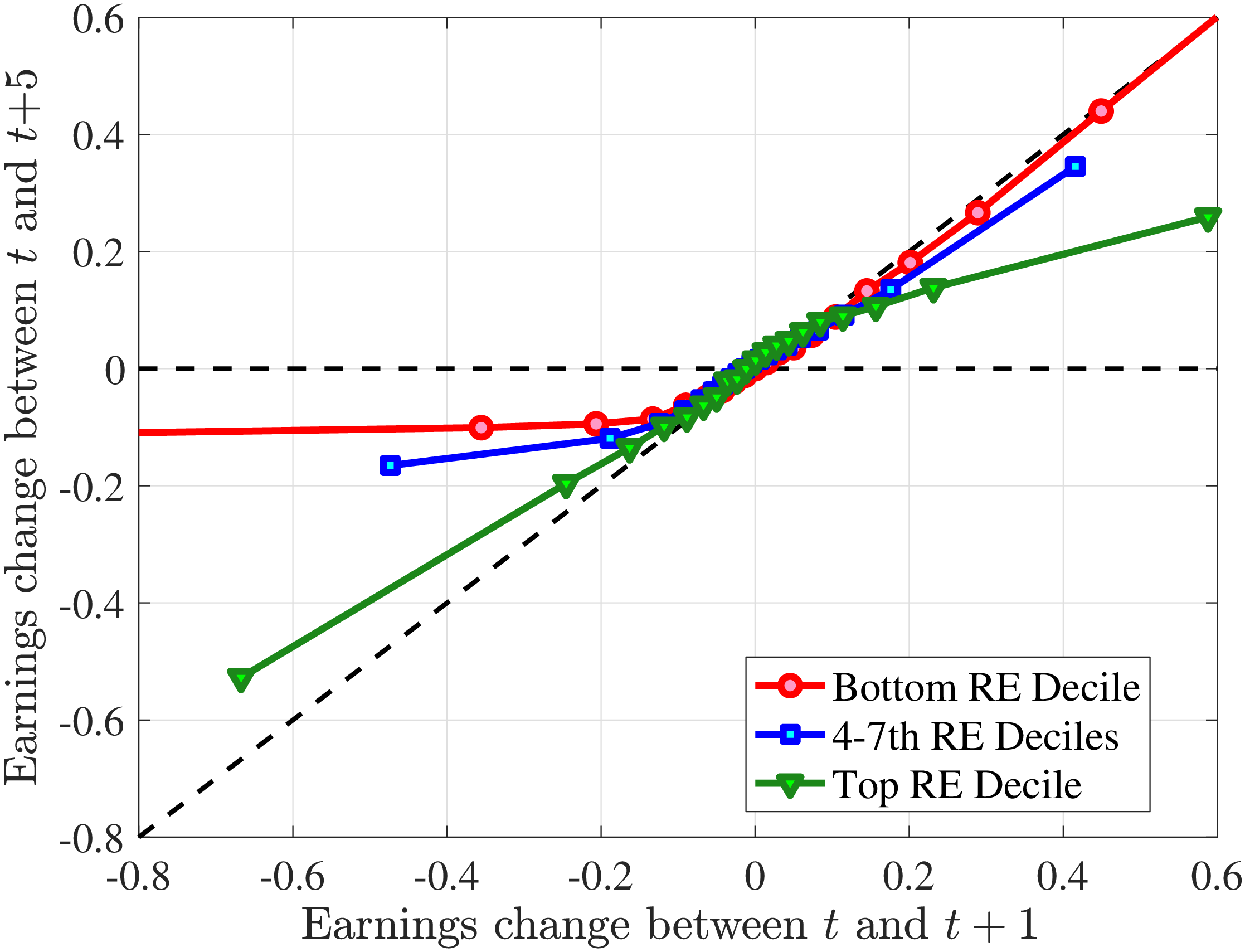

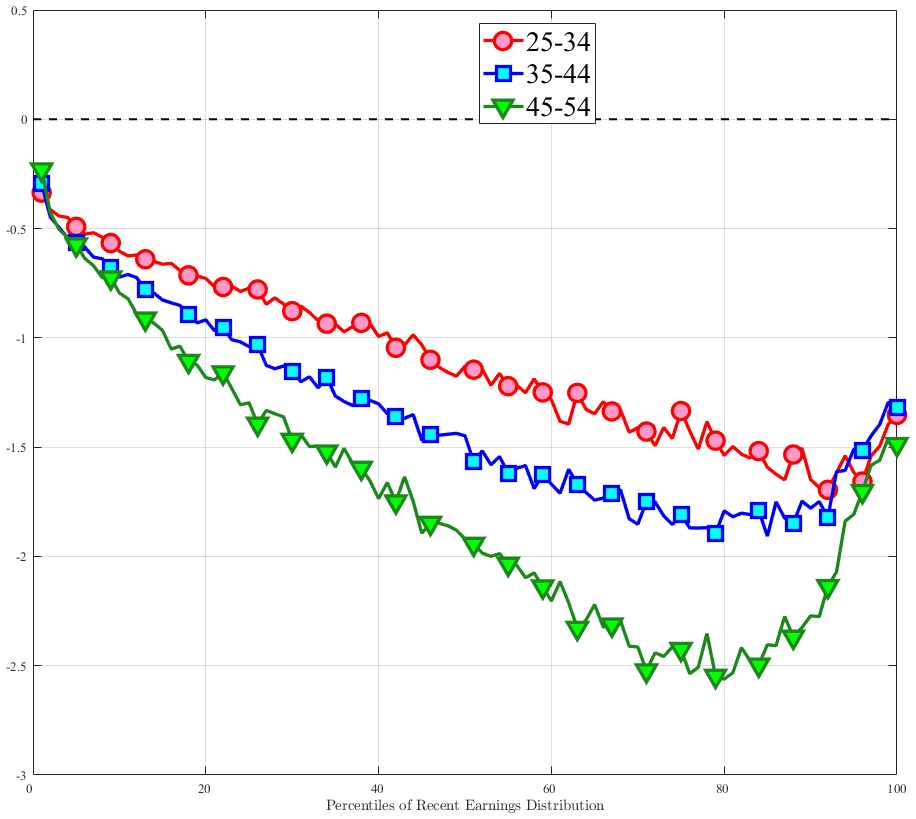

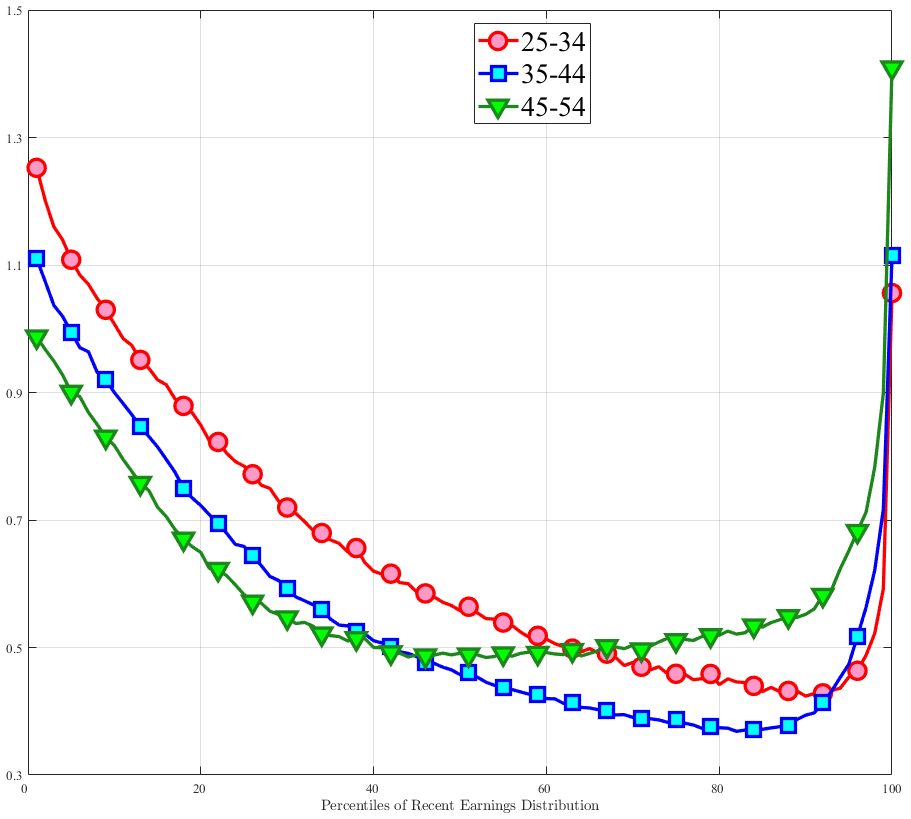

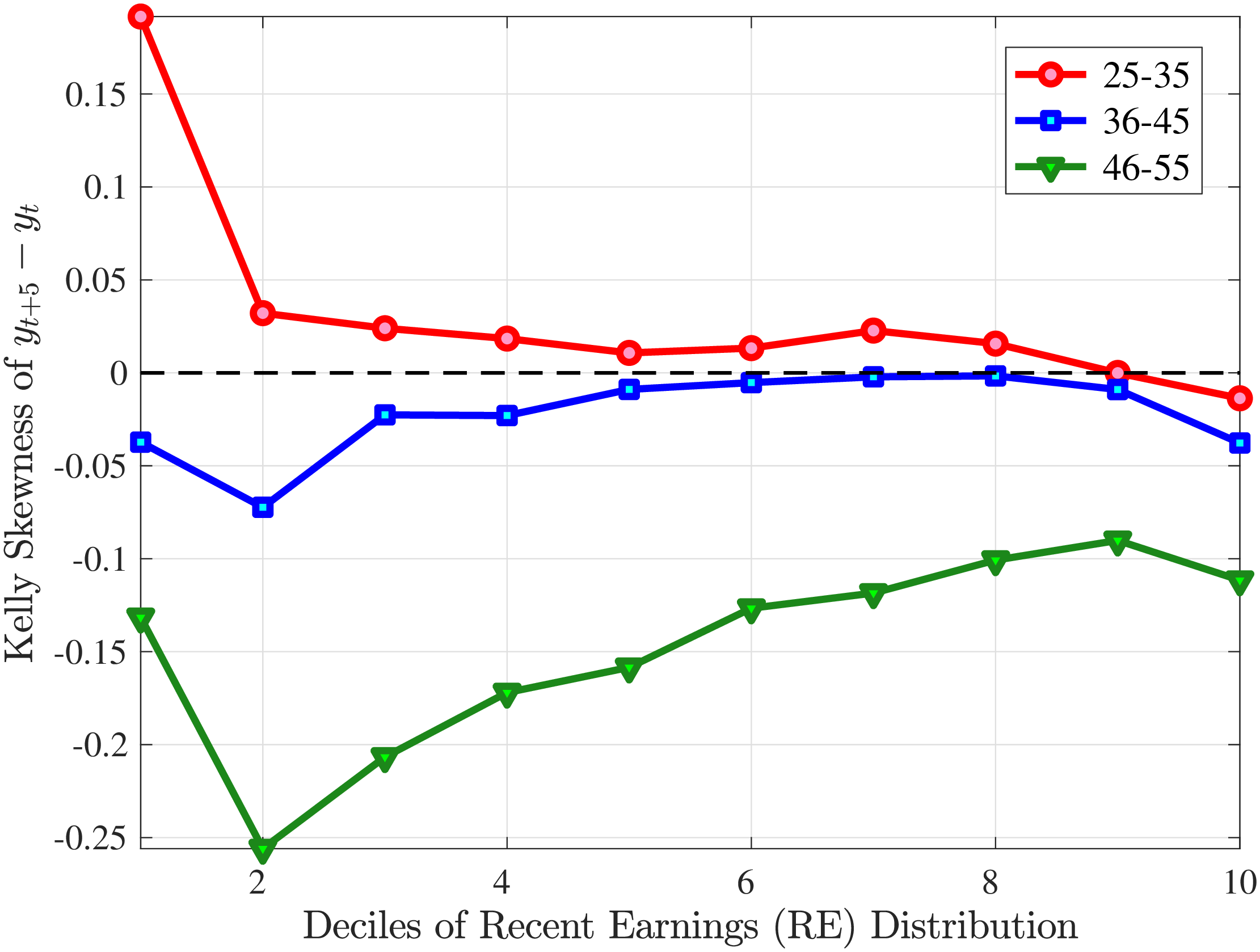

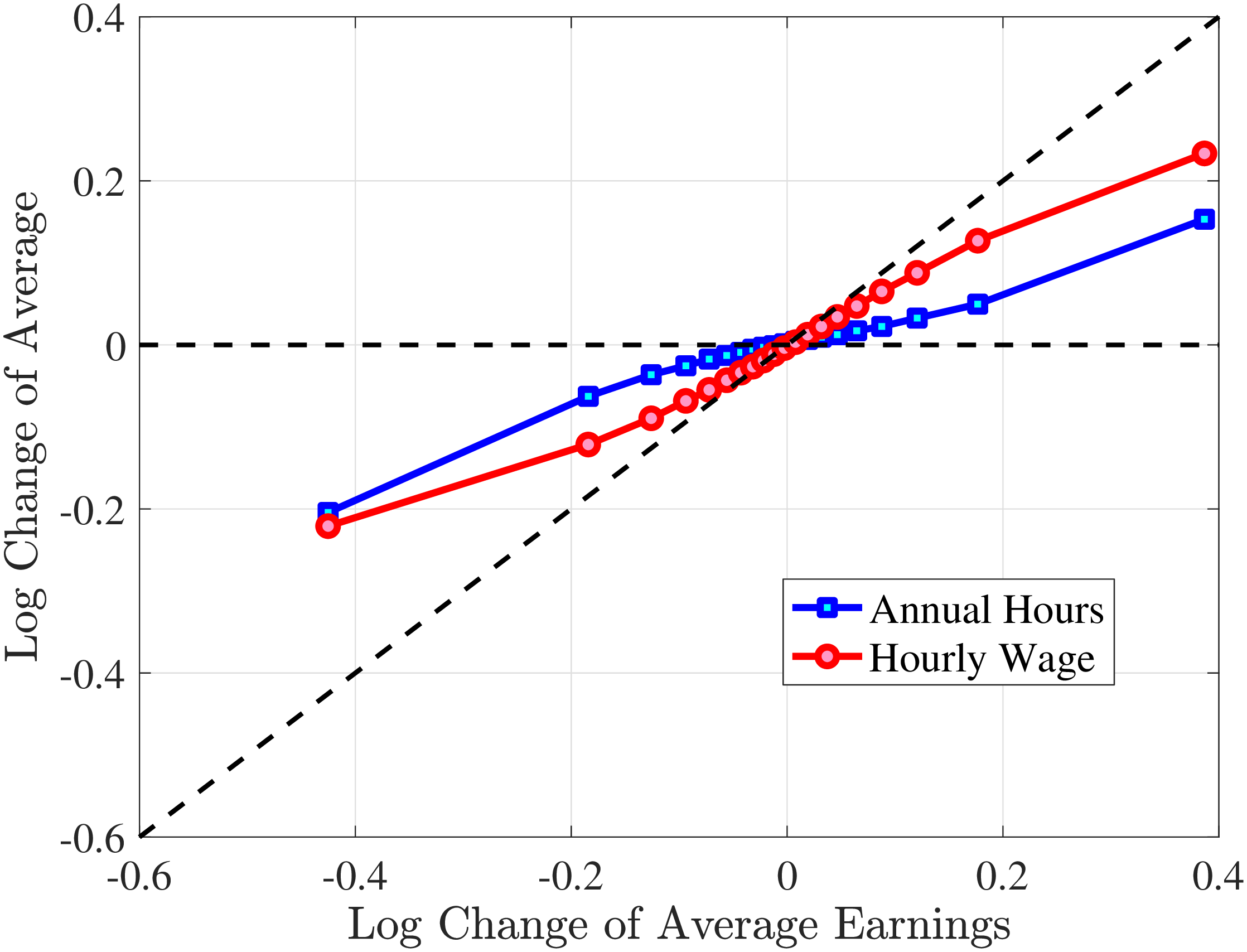

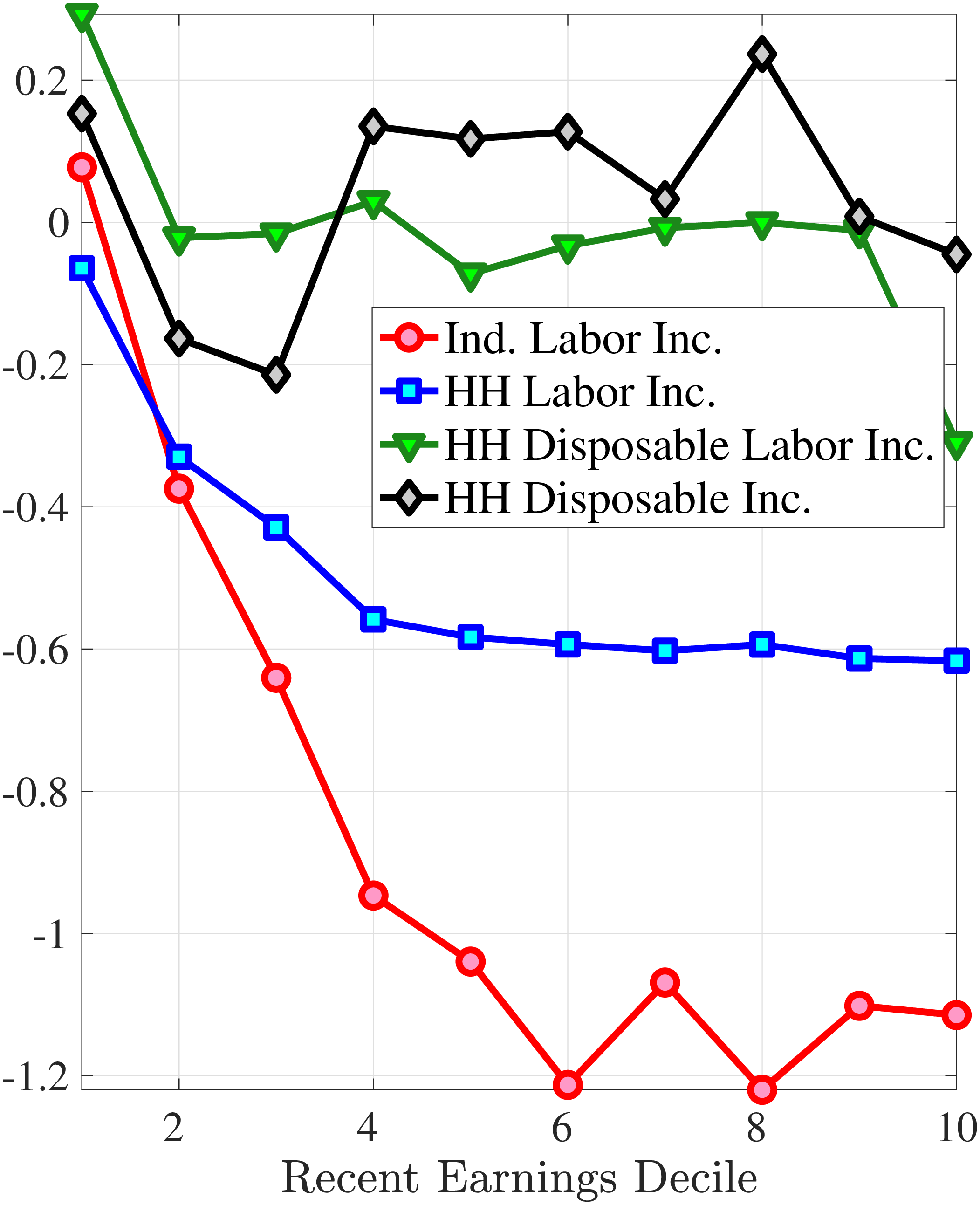

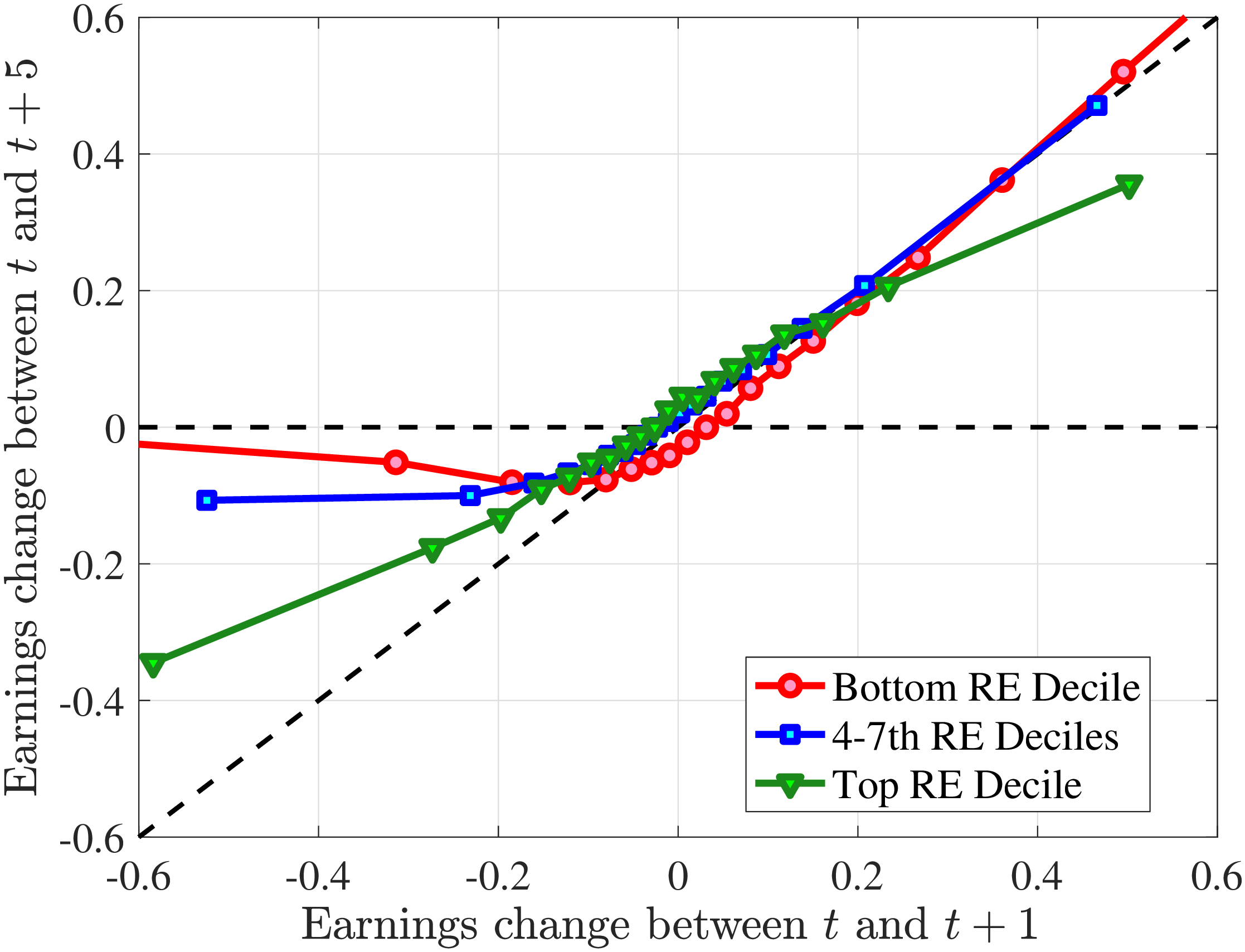

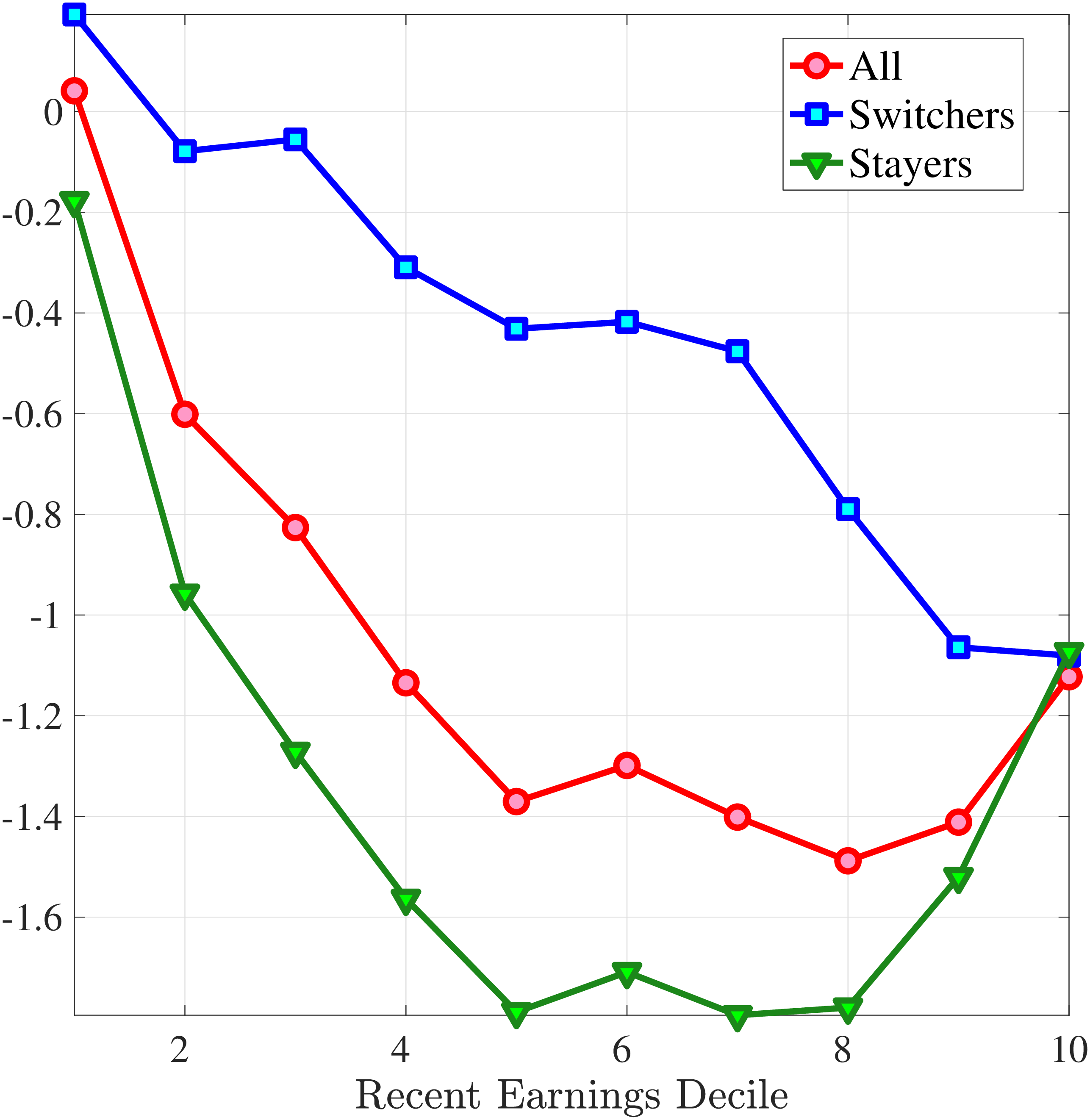

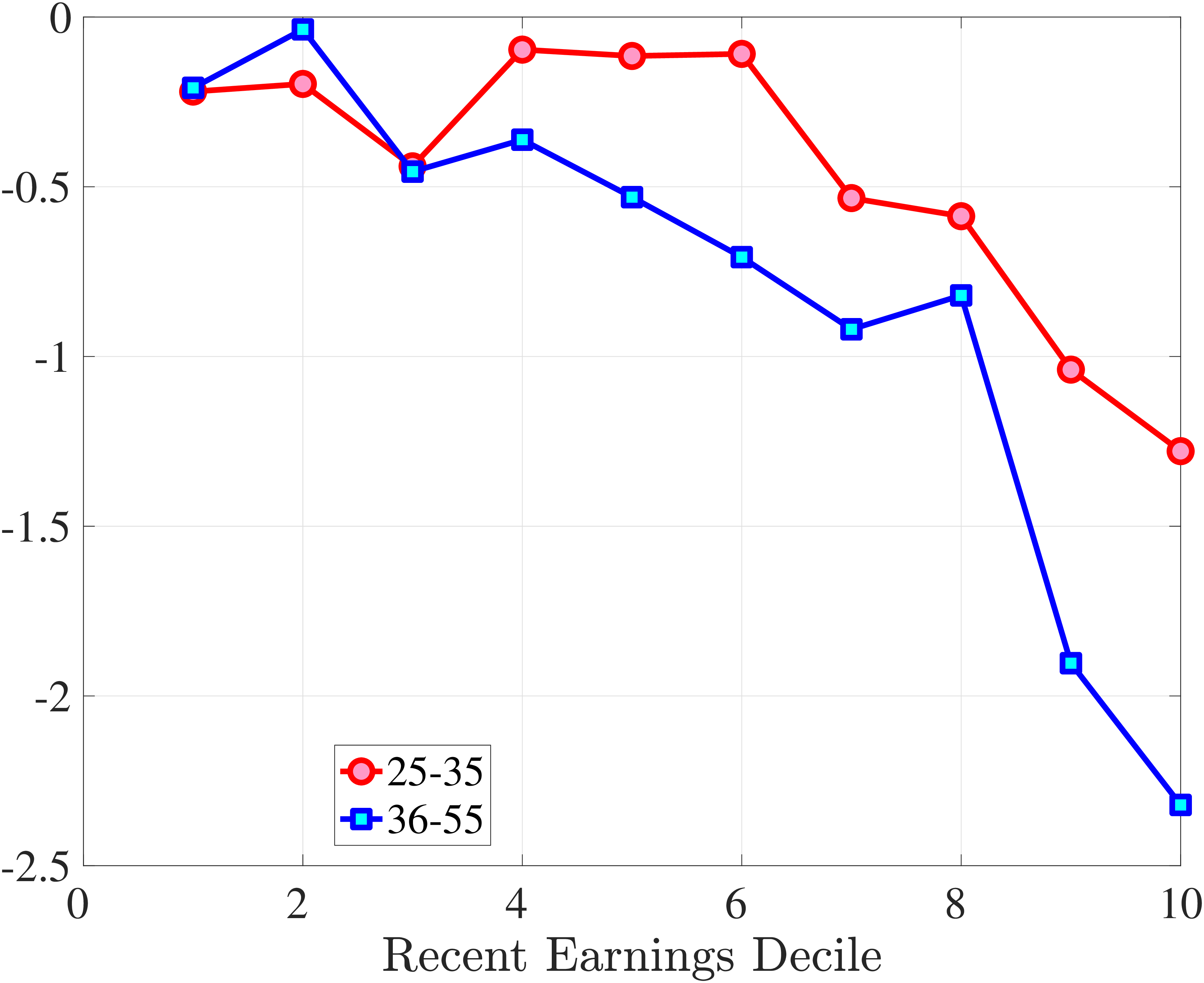

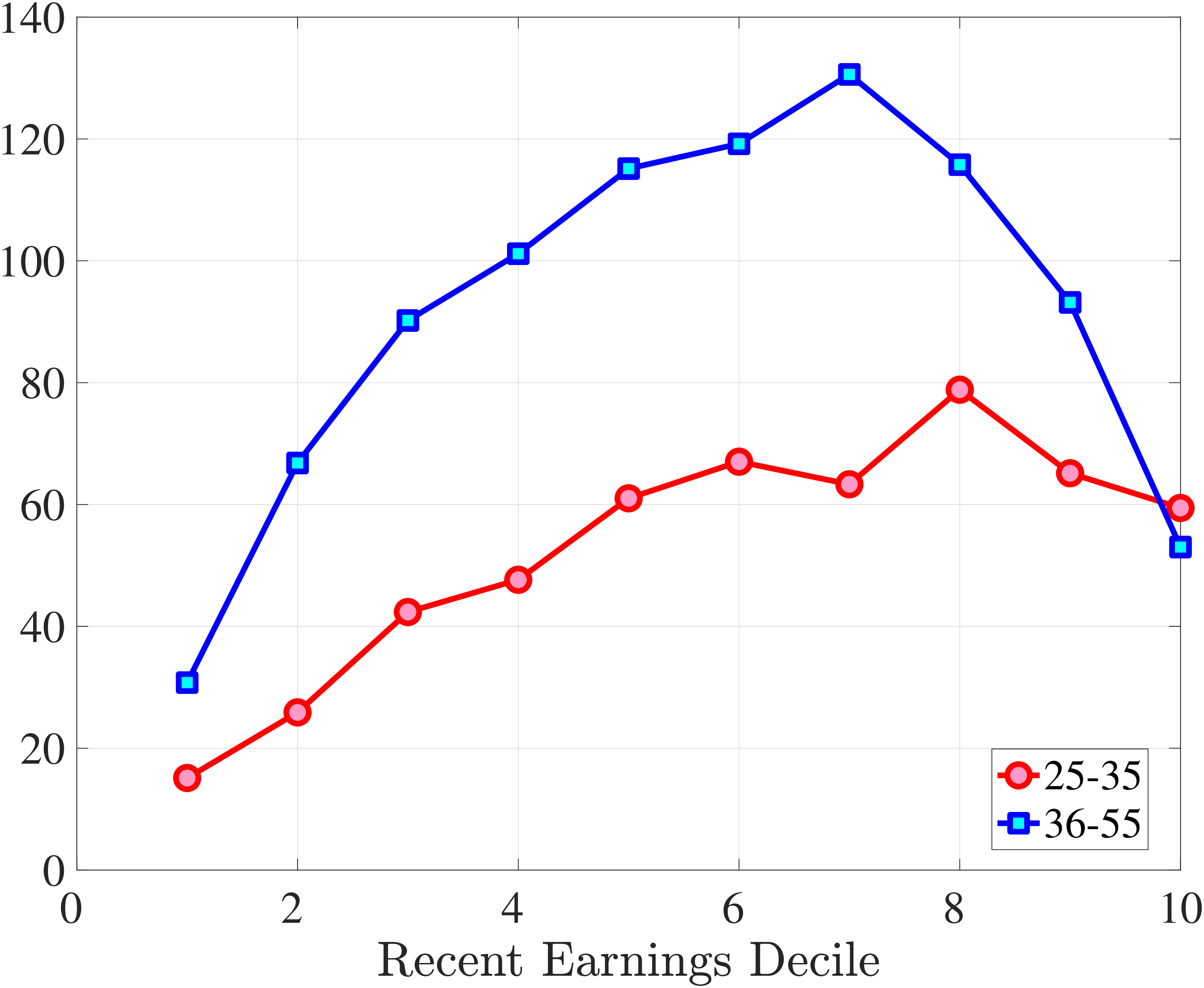

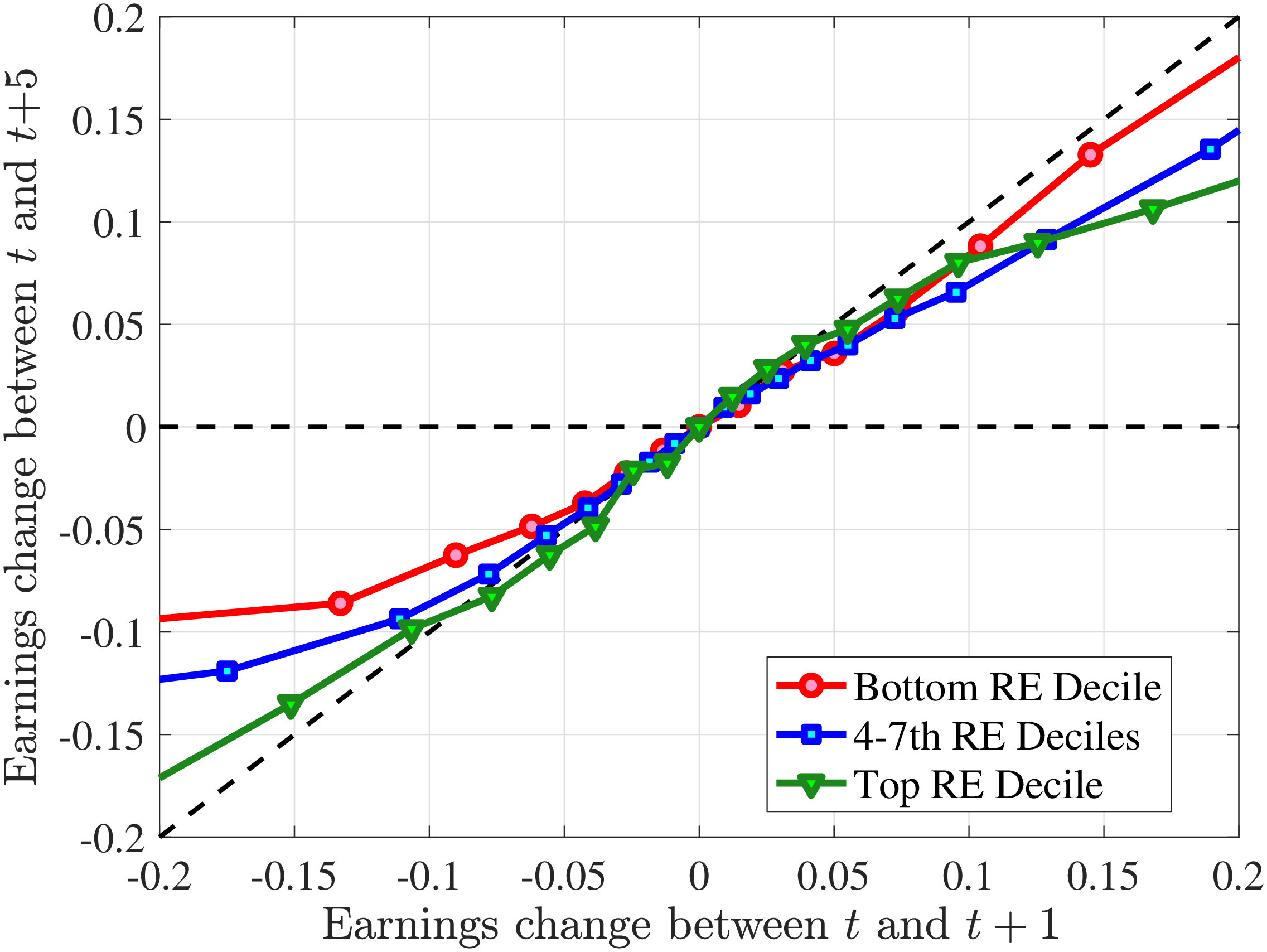

We now investigate how the persistence of earnings changes can be attributed to the dynamics of hours versus wage rates. We start by documenting how the persistence of earnings change varies by the magnitude of the change and recent earnings in Norway (e.g., Guvenen et al. (2019) and Arellano et al. (2017)). To this end, we plot the change in average earnings after five years against the initial change for prime-age males. The x-axis has the initial (average) change \(y_{t+1}^{i}-y_{t}^{i}\) for each quantile of workers, sorted by the size of their earnings shock. The y-axis plots the representative agent change in earnings, that is, the change in the log of average earnings for each such quantile from \(t\) to \(t+5,\log \mathbb{E}\left [Y_{t+5}^{i}\right]-\log \mathbb{E}\left [Y_{t}^{i}\right]\), where \(Y_{t}^{i}\) is the income level net of age and time effects of individual \(i\). If the initial change were permanent, then \(\mathbb{E}\left [Y_{t+5}^{i}\right]=\mathbb{E}\left [Y_{t+1}^{i}\right]\) because individual changes after \(t+1\) wash out across people in the quantile. In this case, the observations would line up along the 45-degree line. Conversely, if the change between \(t\) and \(t+1\) were transient, then \(\mathbb{E}\left [Y_{t+5}^{i}\right]=\mathbb{E}\left [Y_{t}^{i}\right]\), and the observations would line up on the x-axis. Recall that this approach incorporates changes in the extensive margin of labor supply after the initial change. While, by construction, all people in the sample satisfy the sample restrictions in periods \(t\) and \(t+1\), we do not impose any restriction for period \(t+5\). Therefore, all individuals in the quantile, even those with zero earnings and hours, are included in \(t+5\).

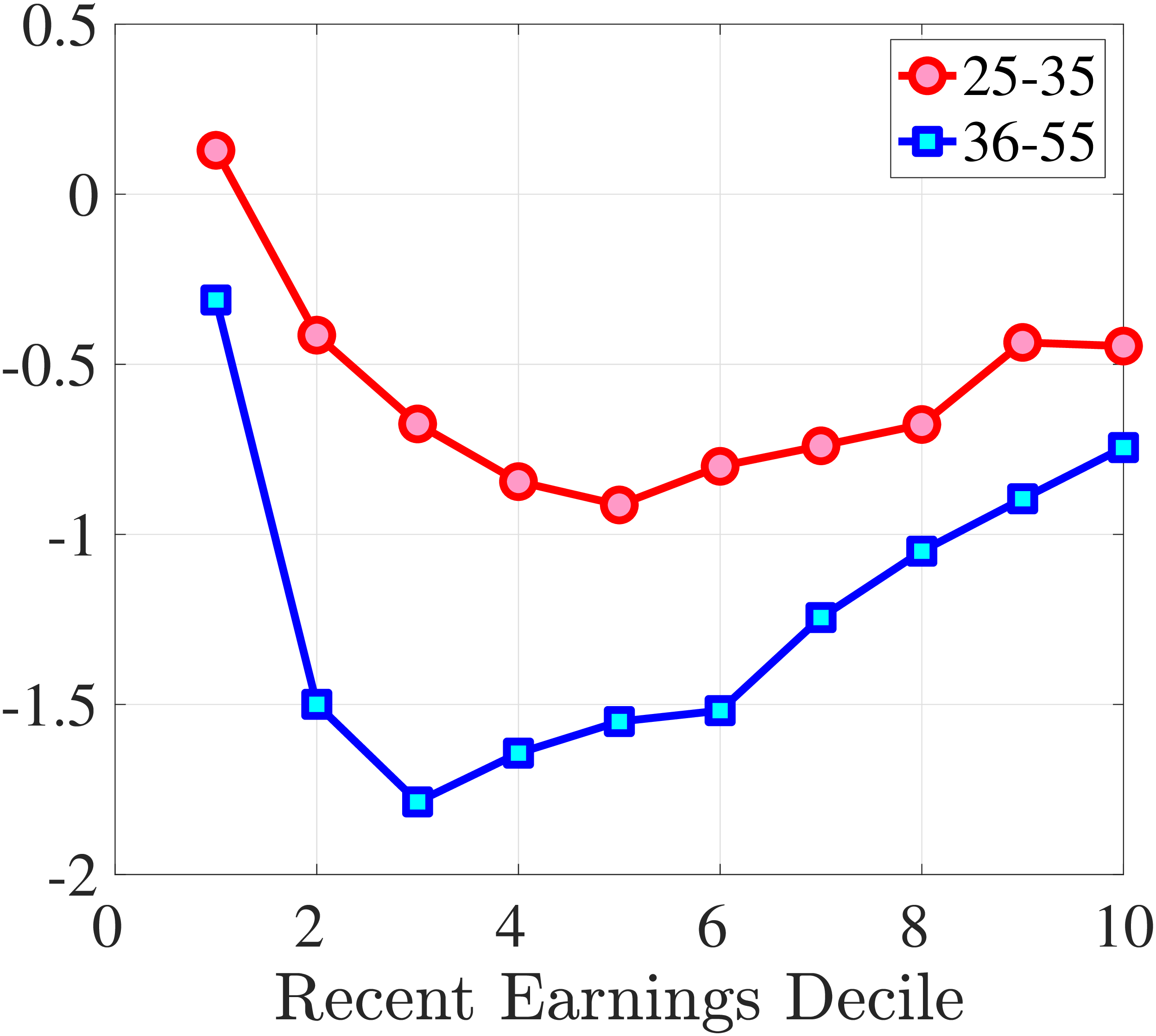

Consider first the workers around the median of recent earnings (4th to 7th deciles). Figure 4 reveals a striking pattern: both small changes and large positive changes are close to permanent. However, for the 10% of workers who experience the largest negative changes (i.e., reductions in earnings of more than 15%), the earnings changes are more transitory. For example, workers who experience an initial 35% decline (45 log points) in earnings relative to time \(t\) have an average reduction in earnings of just 15% five years later (relative to year \(t\)).

For the bottom decile of RE workers, these patterns are even more pronounced: earnings losses are transitory, whereas earnings gains are, for all practical purposes, permanent. For example, workers in this group who experienced around a 55% decline (80 log points) in their earnings between \(t\) and \(t+1\) will on average experience earnings five years later that are only 10% less than their \(t\) values. However, there is no mean reversion for either small changes or large positive changes.

Consider now the top decile of RE workers. For this group, small changes are also permanent. However, different from low-earnings workers, large positive changes are quite transient whereas large negative changes are highly persistent. For example, for the workers with initial earnings increases of 75% (55 log points), only half of the initial change remains after five years. Conversely, the workers who experience an initial 50% decline (70 log points) see a sustained 40% decline (50 log points) five years later.

Figure 4

–

Persistence of Earnings Changes, Prime Age Males

Note: The figure displays the five-year representative agent change (log change of averages) in earnings for 20 different groups of prime-age males (ages 36 to 55) in the 1st RE decile, 4th-7th RE deciles, and 10th RE decile, plotted against their respective one-year log change in average annual earnings.

Figure: Figure 4 – Persistence of Earnings Changes, Prime Age Males

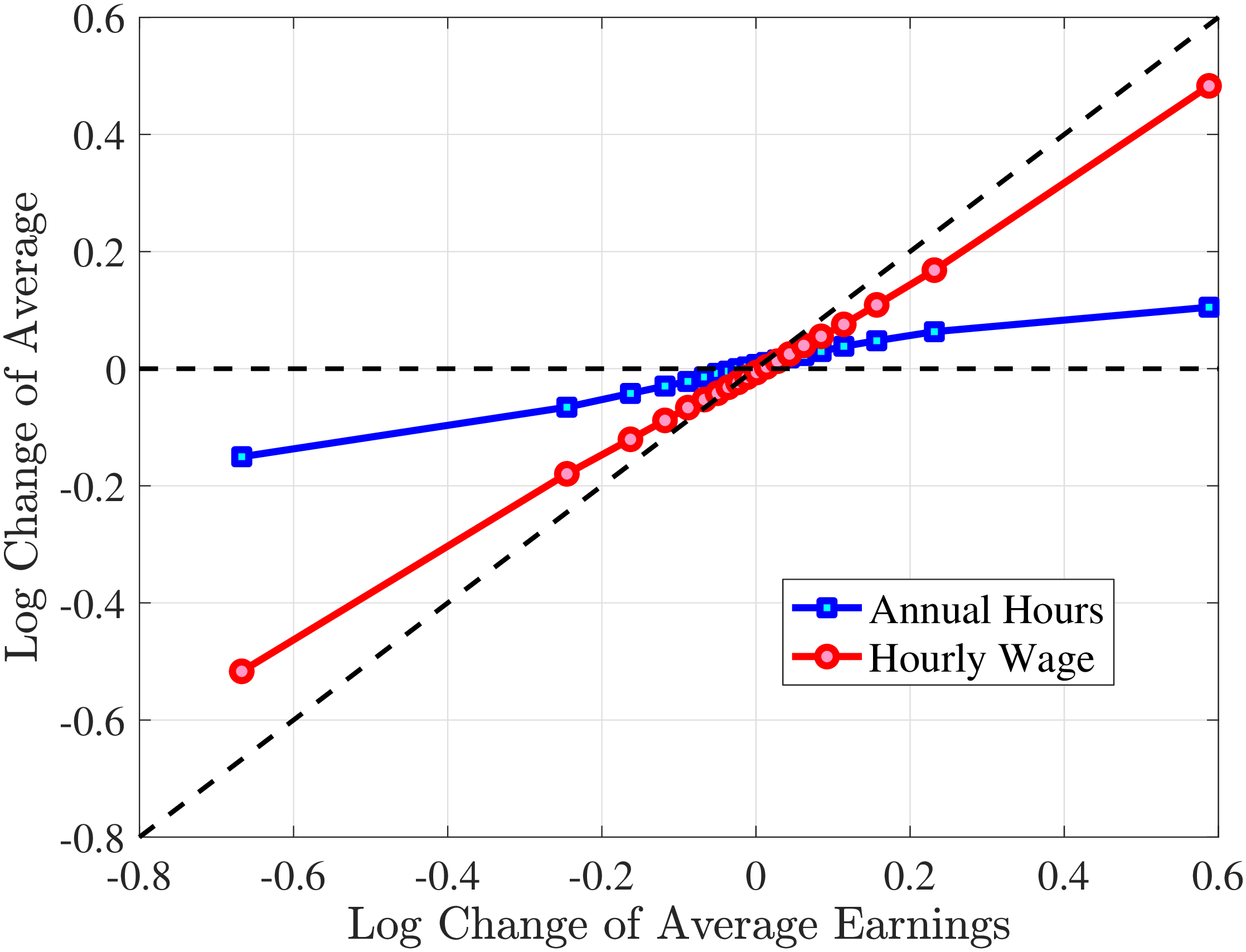

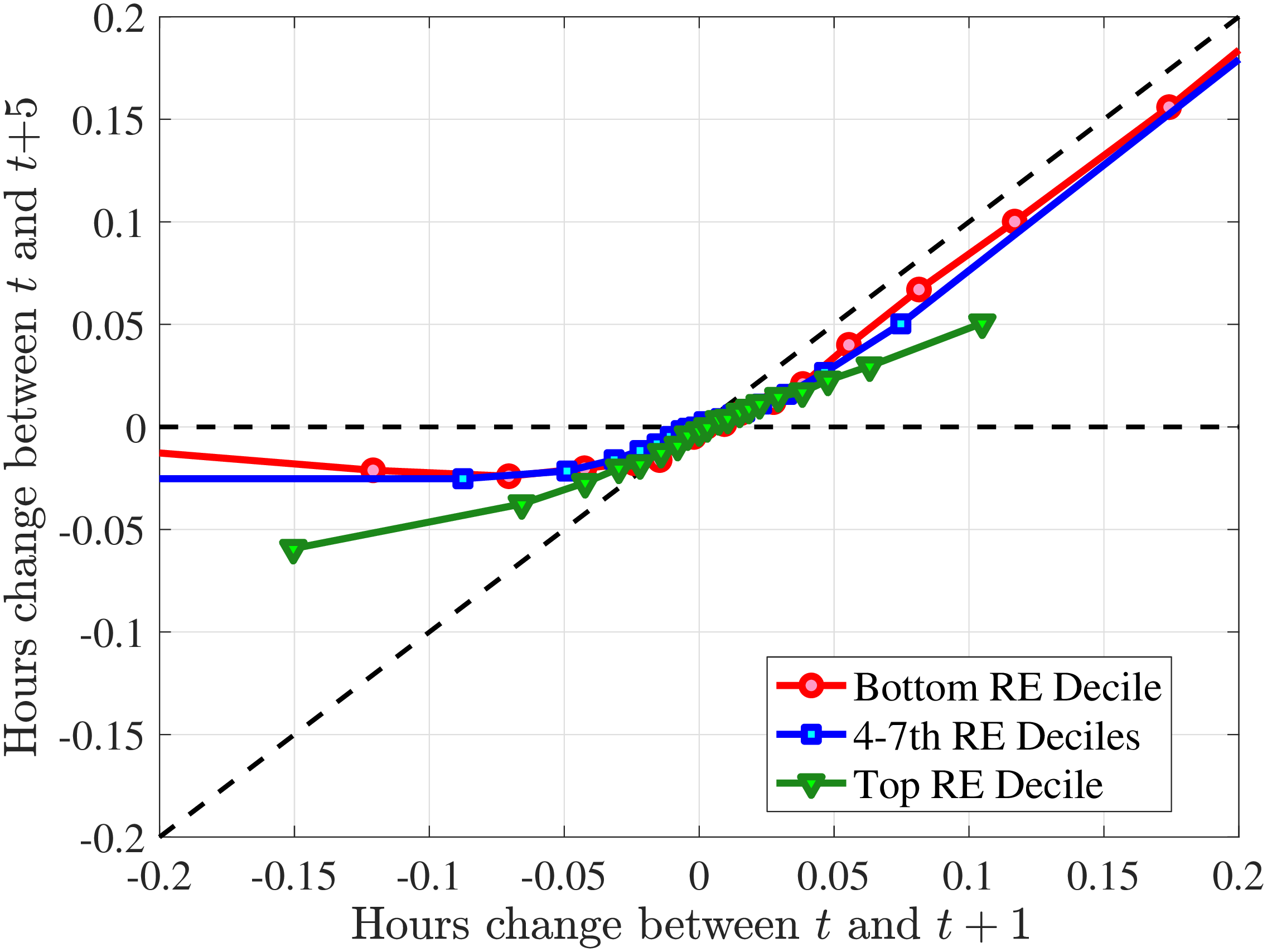

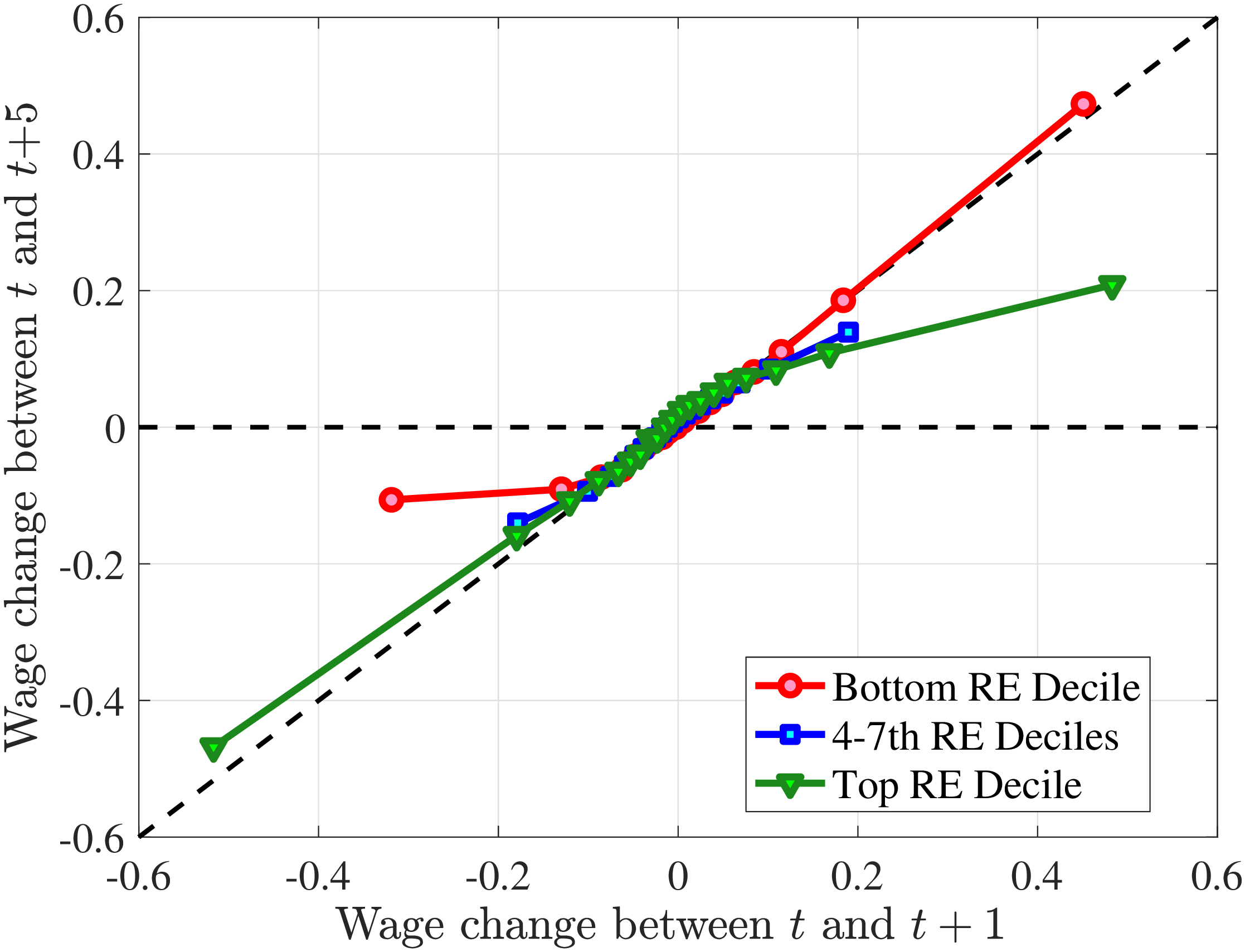

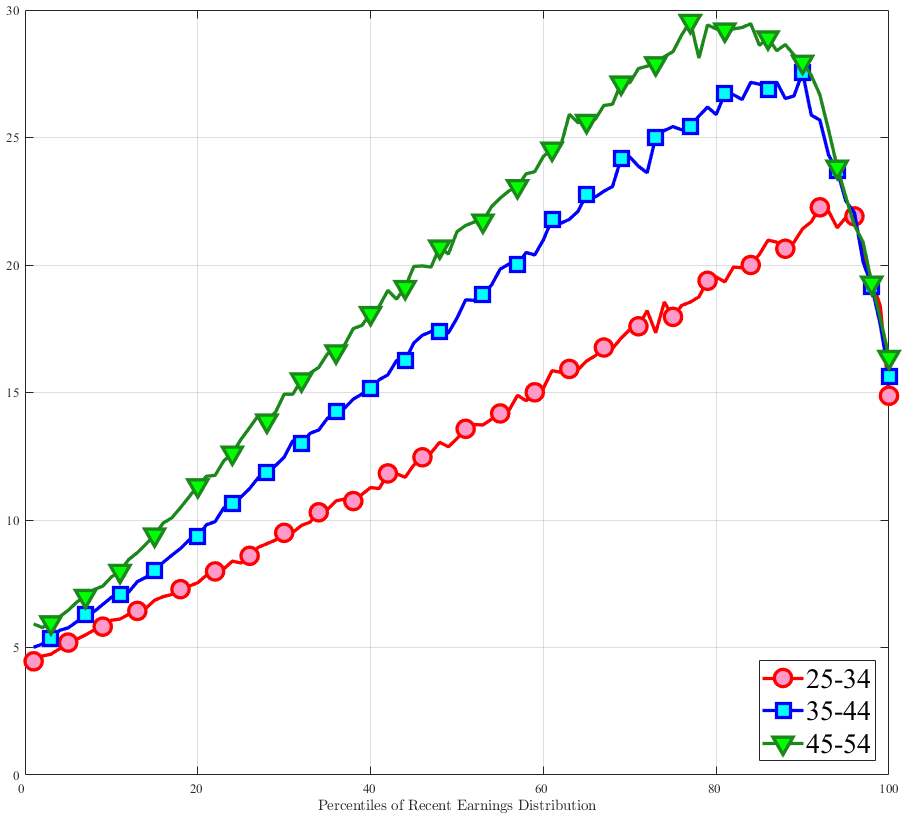

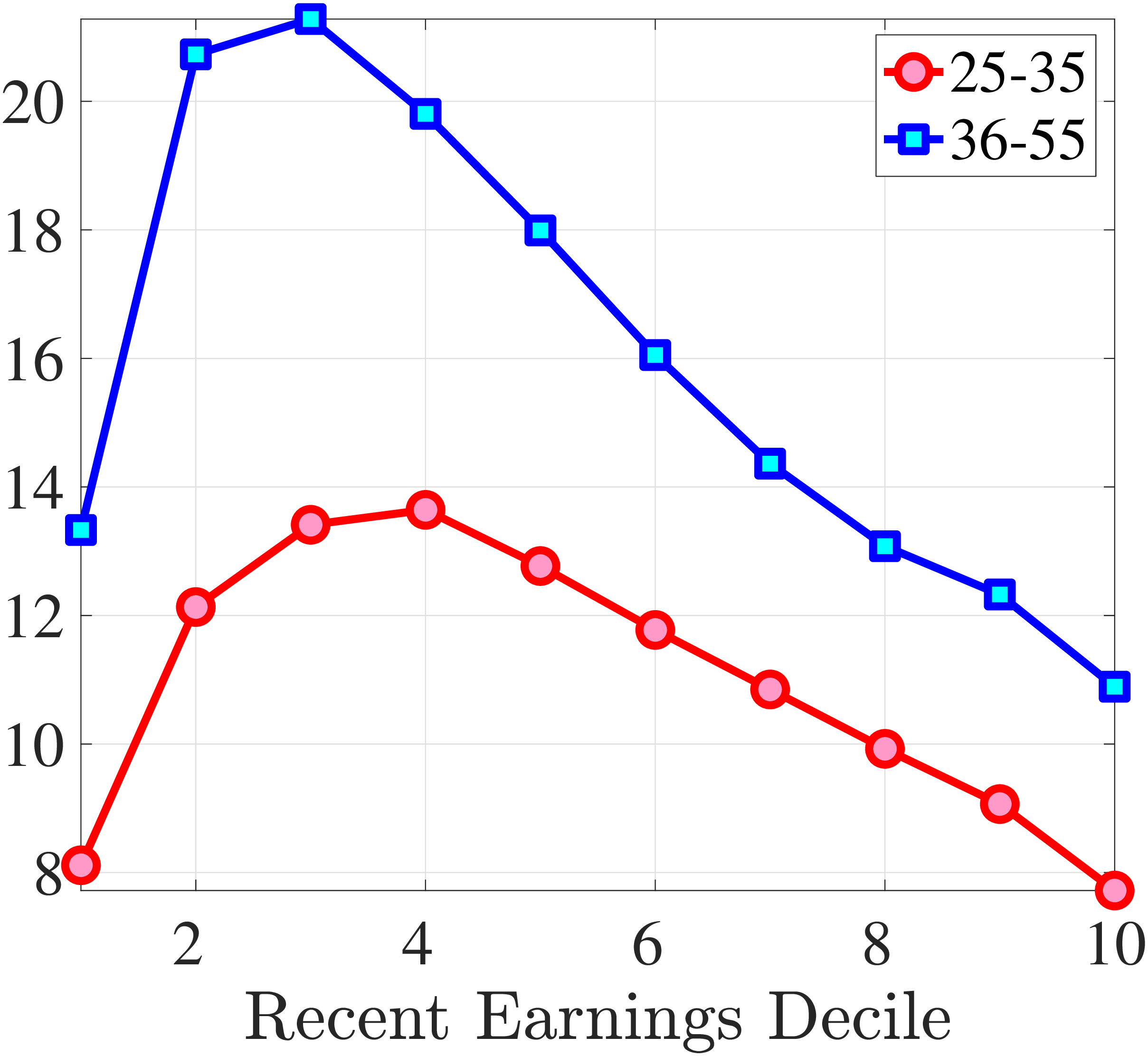

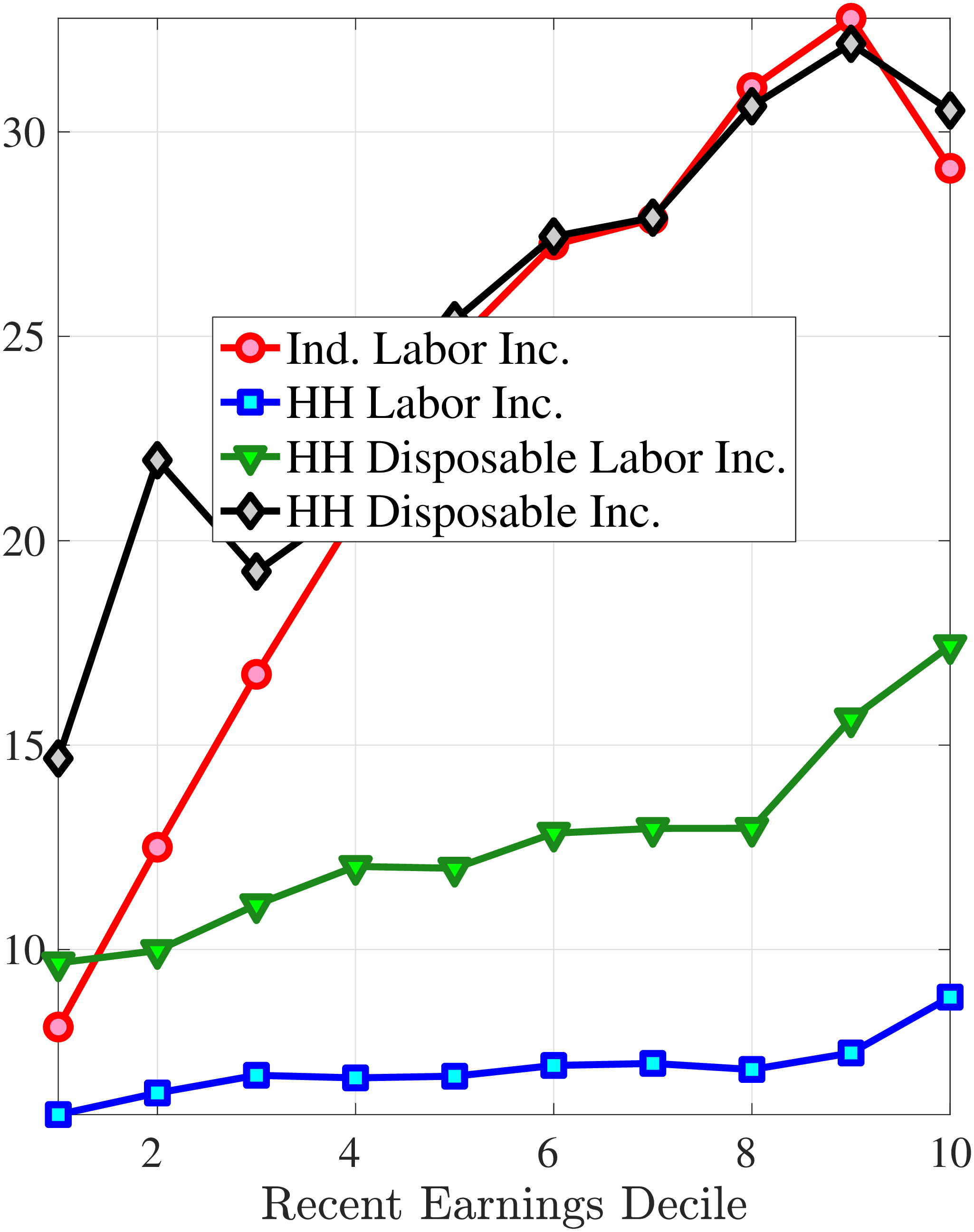

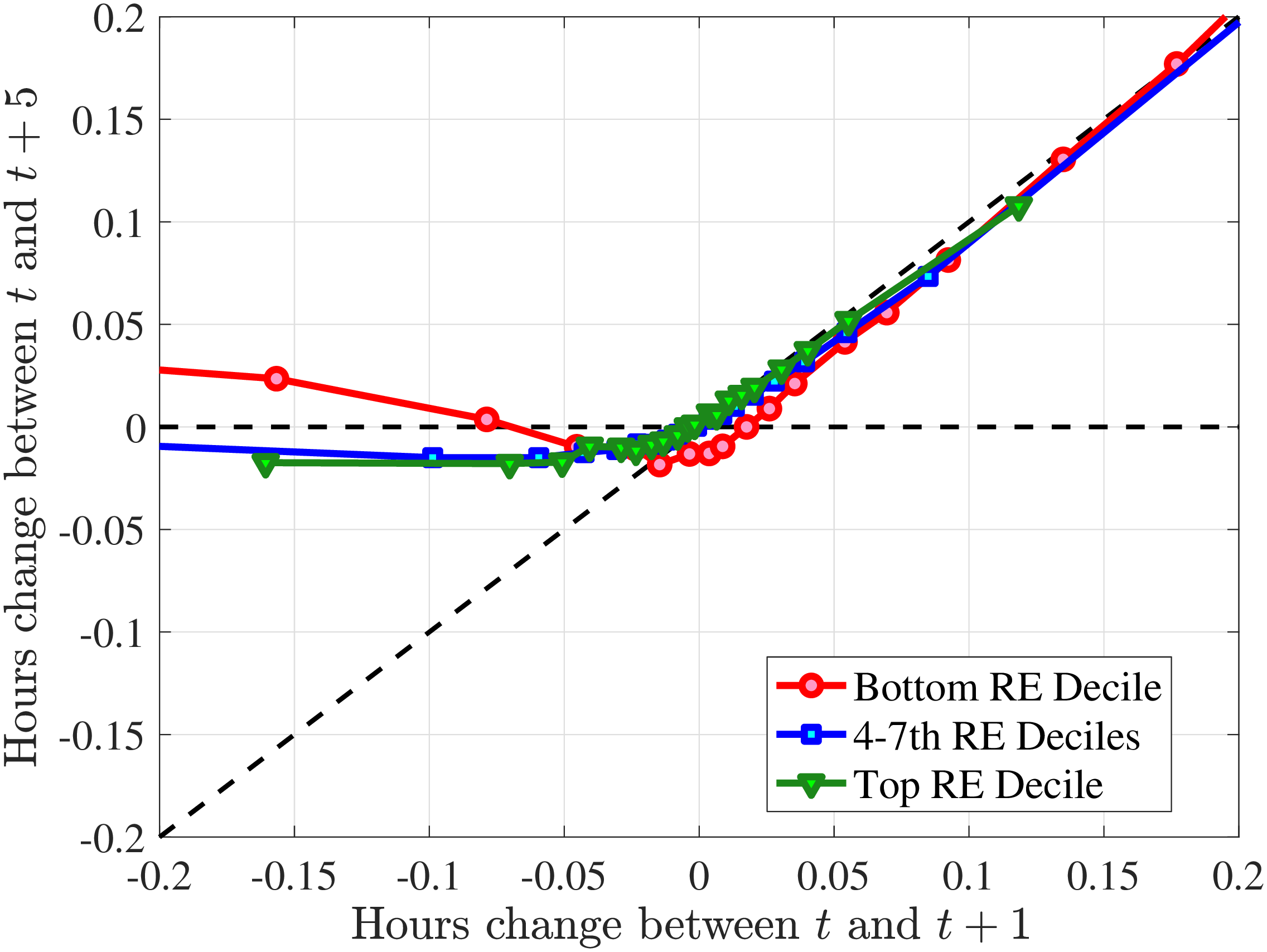

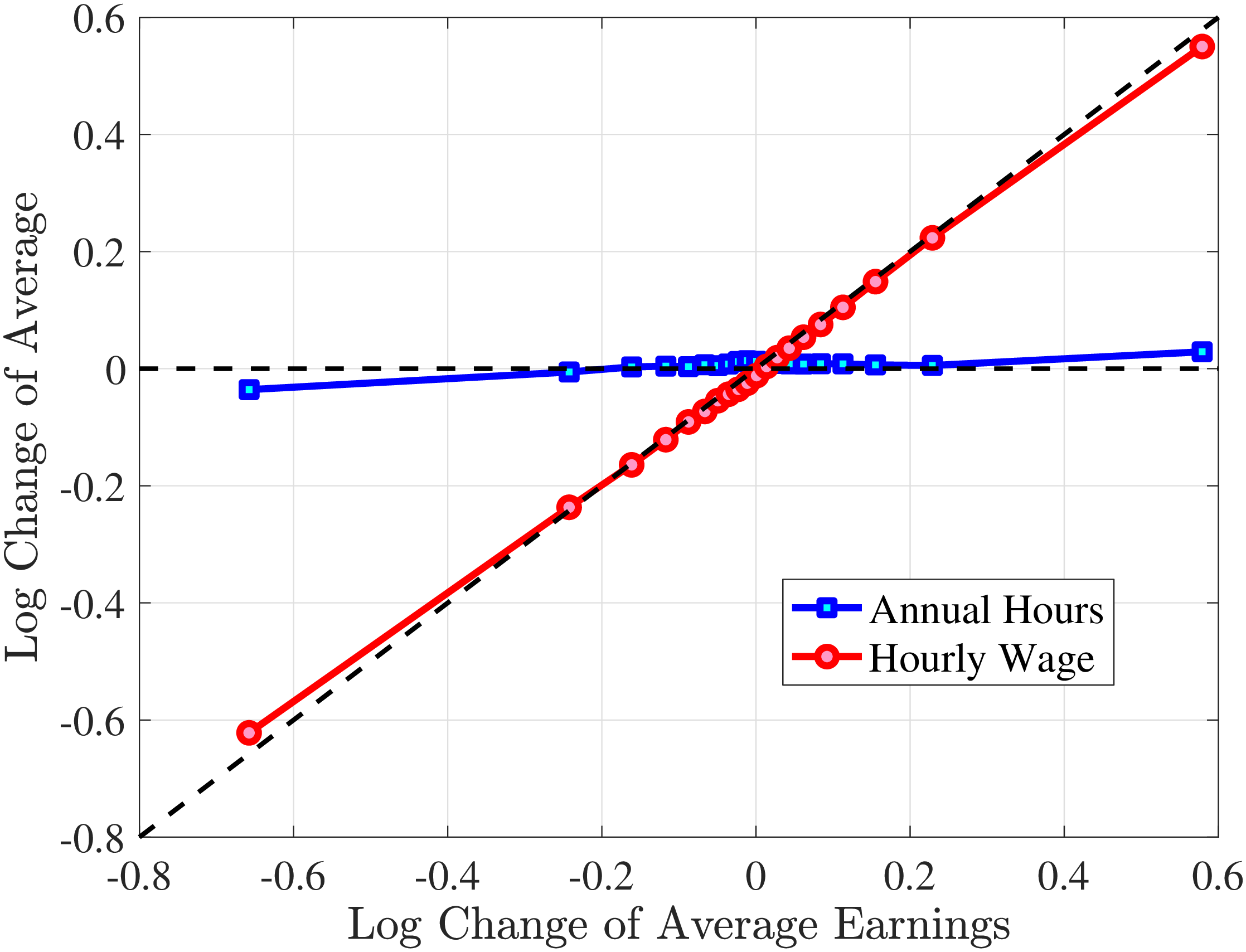

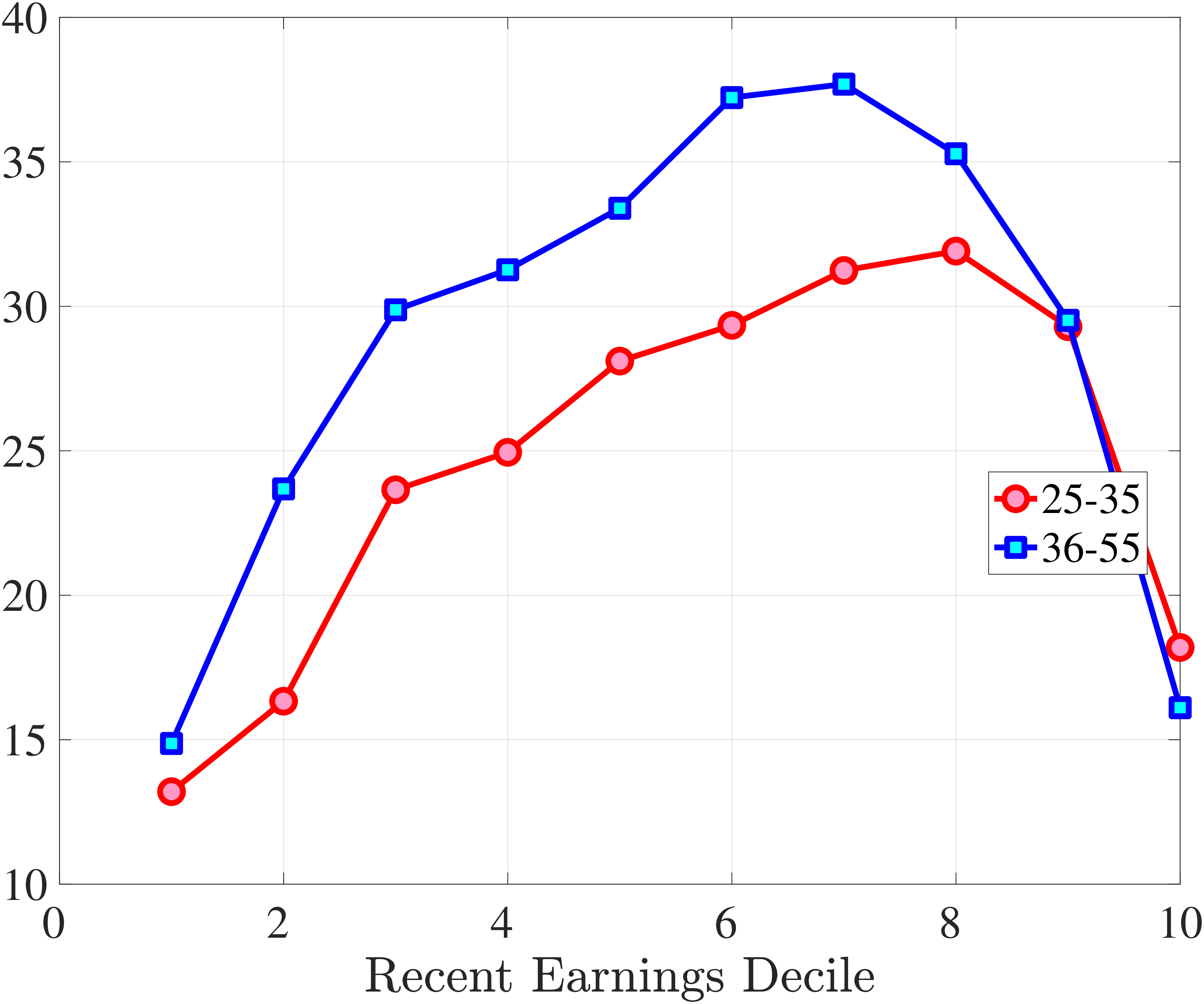

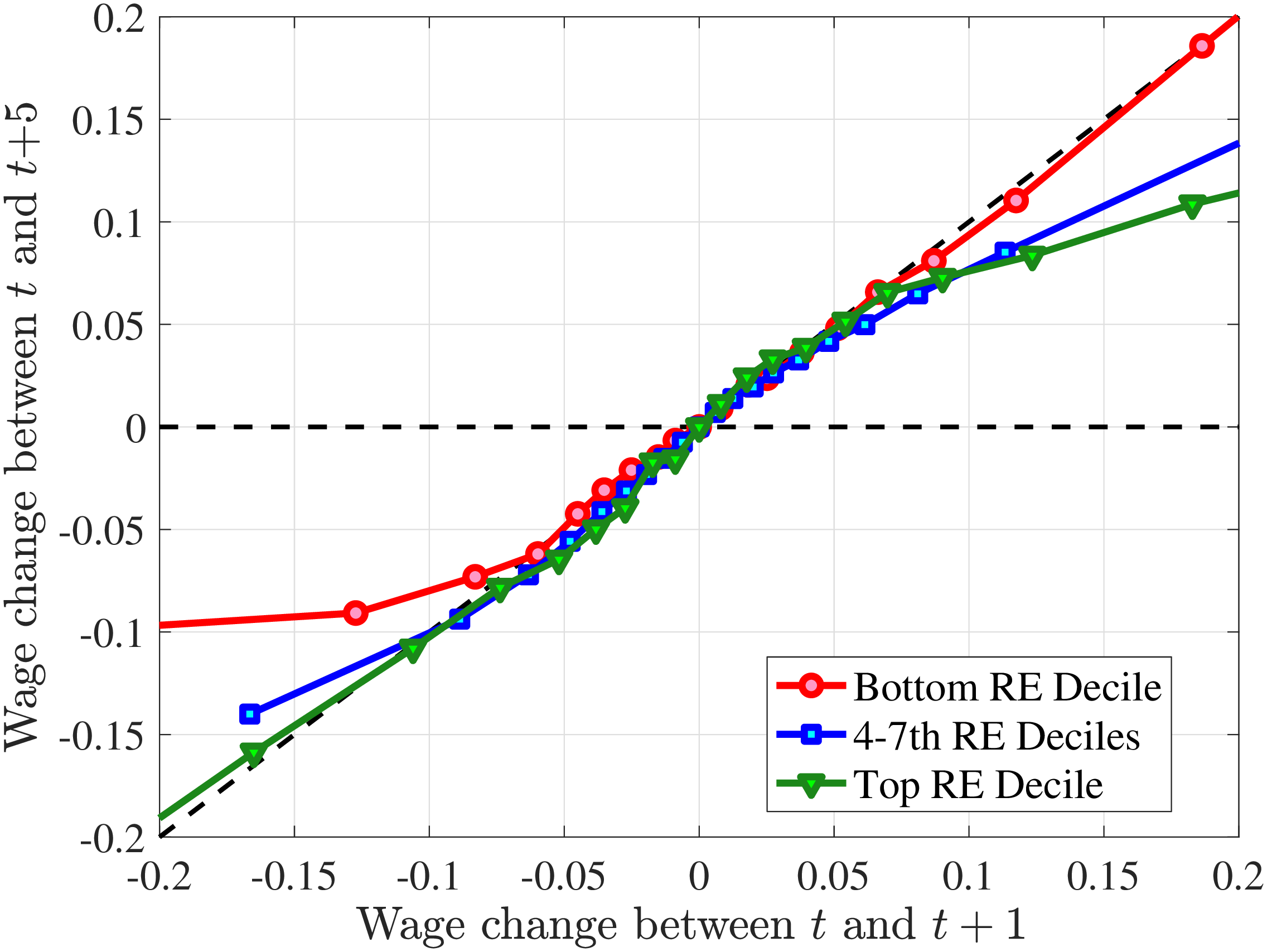

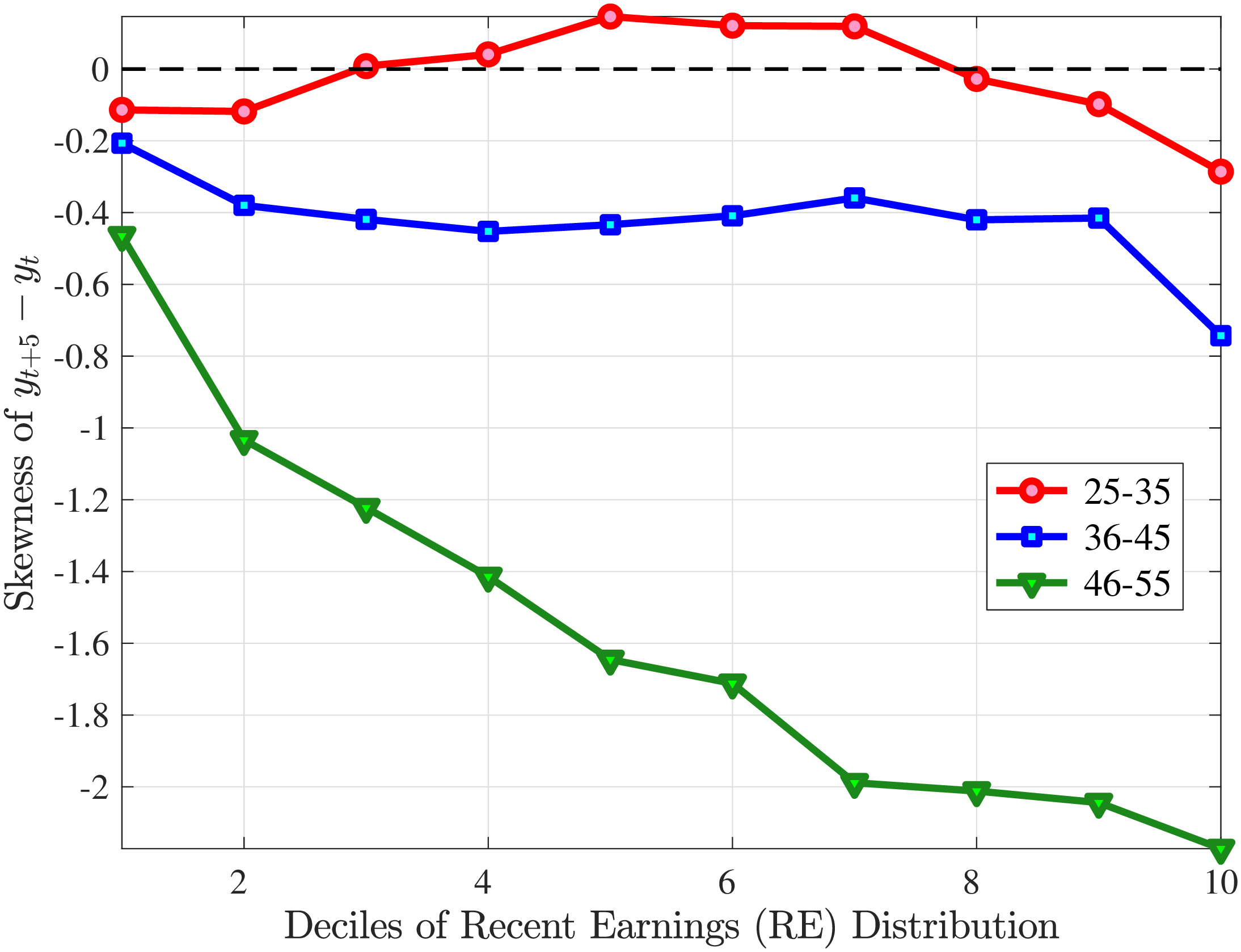

4.2.1 Mean Reversion of Hours and Wage Changes

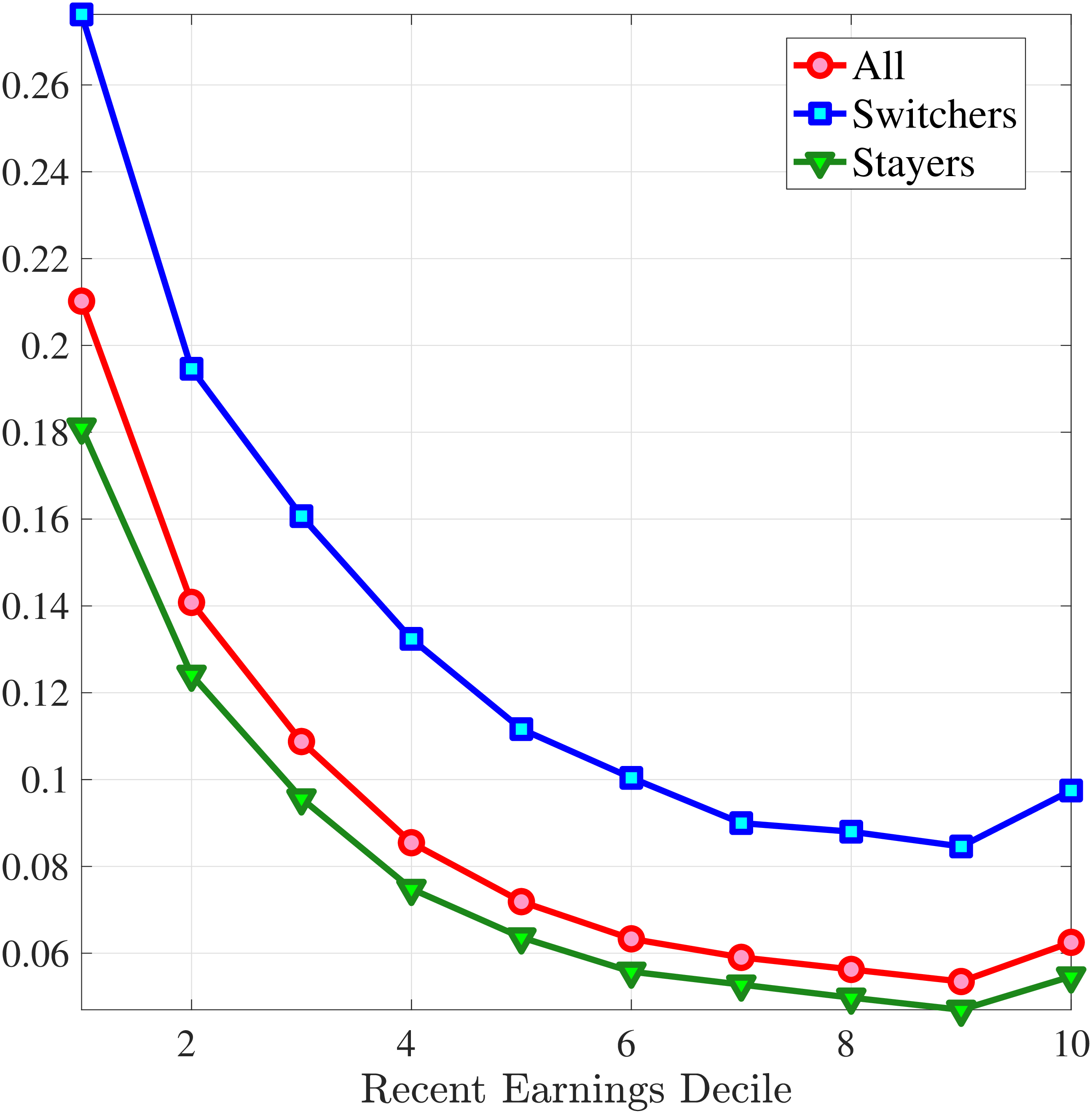

What explains this asymmetric mean reversion for earnings? To answer this question, we investigate the persistence of hours and wage rate changes separately. In line with the strategy above, we group workers with respect to age and recent earnings as well as their hours or wage rate growth between \(t\) and \(t+1\). For each quantile of change in hours or wage rate, we plot the log of the five-year growth of averages within the quantile (\(t\) to \(t+5\)) on the y-axis against the log of the one-year growth (\(t\) to \(t+1\)) on the x-axis.

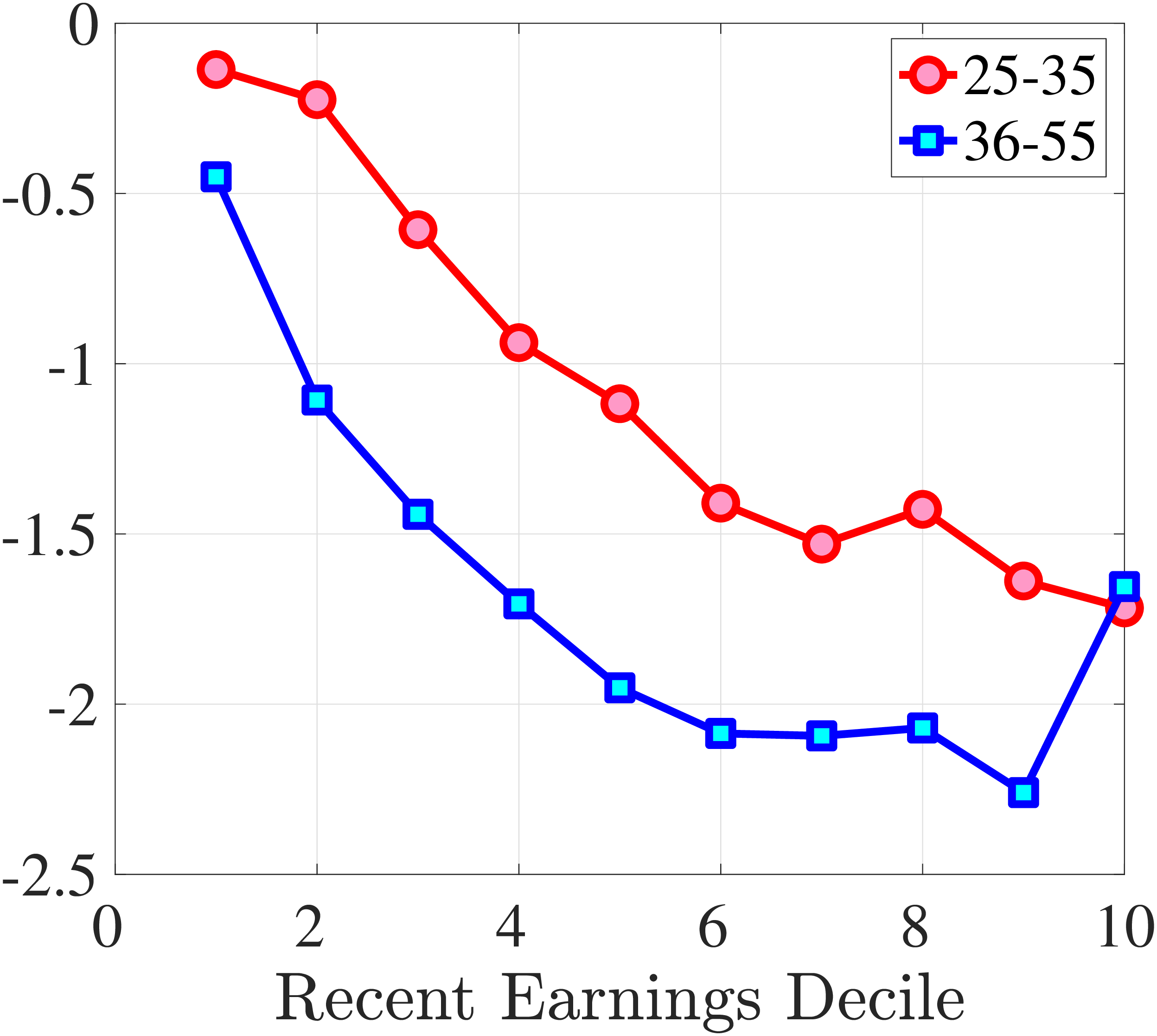

Starting with the persistence of hours change, the left panel of Figure 5 shows the five-year log change in average hours for different sizes of impulses for workers around the median of recent earnings (4th to 7th deciles), as well as those in the bottom and top deciles (similar to Figure 4). We show this graph only for the prime-age group, as young workers display a very similar pattern (see Figure D.3 in the Online Appendix). The main insights from the figure are that hours declines are very transitory, whereas hours increases are close to permanent. This finding is in line with the evidence in Krusell et al. (2011) that the duration of employment spells is much longer than the duration of unemployment spells. It is also in line with Jarosch (2021), who finds that the scarring effects of unemployment on future employment mostly dissipate after five years.24

These patterns of persistence of hours—declines being mostly transitory and increases being mostly permanent—are broadly shared across income groups. The one exception is for workers in the top decile of recent earnings, for whom increases in hours become slightly less persistent and declines become somewhat more persistent. These differences might be due to different events leading to hours changes for different income groups. For example, for the bulk of workers, the main drivers of hours changes are likely to involve transitions between non-employment and employment or from part-time to full-time work, whereas for the richest workers, changes in hours might to a larger extent reflect more flexible work conditions such as the possibility of working overtime or having multiple employments. We revisit this issue in Section 4.3 when we associate earnings changes with real-life events.

The right panel of Figure 5 shows the persistence of wage rate changes. Unlike hours changes, wage rate changes are highly persistent regardless of whether they are positive or negative. We see few deviations from this pattern across recent earnings groups, although we note that large wage rate increases for top earners and large wage rate losses for bottom earners tend to be somewhat less persistent. One factor contributing to the low persistence of earnings gains for the top earners could be the fact that high earners receive some of their income in the form of bonuses and stock options, and this income is highly cyclical (c.f.?).

We conclude that the nonlinear persistence of earnings changes documented in Figure 4 is largely a result of nonlinear persistence in hours worked. In particular, hours changes exhibit nonlinear persistence patterns that are very similar to those of earnings. In contrast, wage rate dynamics are close to linear, except for workers in the tails of the income distribution. These wage rate dynamics are very different from the wage rate dynamics that one would obtain in a theoretical wage ladder model where workers climb a wage ladder within each job spell. Finally, earnings declines are very persistent for high earners because hours do not move much for these workers—the fall in their earnings is due to a decline in wage rates.

(a) Annual Hours

(a) Annual Hours (b) Hourly Wage

(b) Hourly Wage

Figure 5

–

Persistence of Hours and Wage Changes by RE Decile

Note: The left panel displays the five-year representative agent change (log change of averages) in imputed annual hours for 20 different groups of prime-age males (ages 36 to 55) in the 1st RE decile (red line), 4th-7th RE deciles (blue line), and 10th RE decile (green line), plotted against their respective one-year log change in imputed annual average hours. The right panel displays the corresponding figure for imputed hourly wage rates.

Figure: Figure 5 – Persistence of Hours and Wage Changes by RE Decile

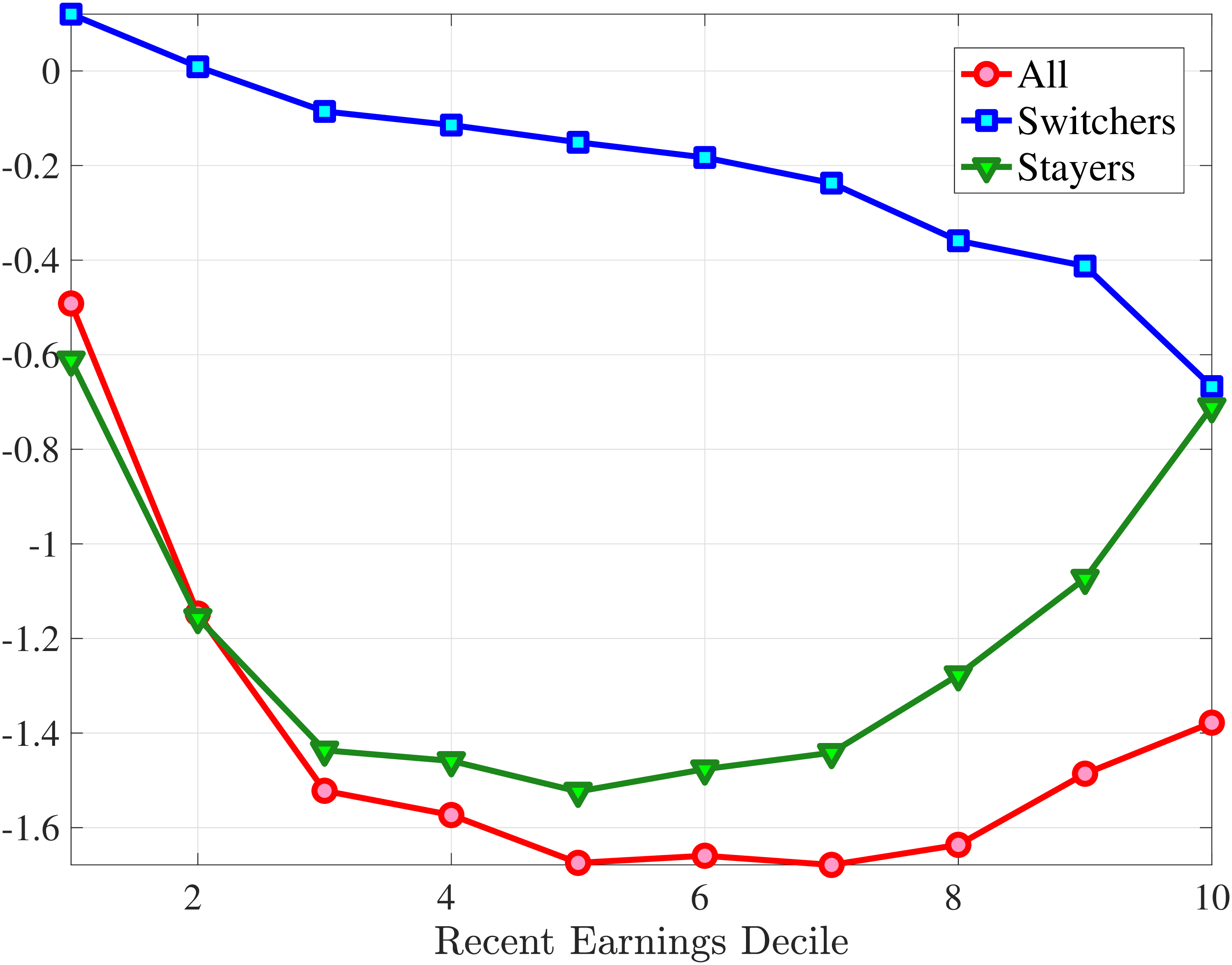

4.3 Life Events Associated with Large Earnings Shocks

A natural question when dissecting idiosyncratic earnings changes is, what are the major events in an individual’s life that lead to small versus large earnings changes (e.g., see?)? Our data set allows us to link individuals’ earnings to information available in other administrative data sets. In particular, we focus on five important events workers experience that are known to have significant effects on their earnings: transitioning into and out of (i) unemployment, (ii) long-term sickness, (iii) part-time work, (iv) parental leave, and (v) job change to a different firm.

We obtain data on days on unemployment benefits, sick days, and days on parental leave from the Social Security Administration Register. Transition into unemployment is defined as having zero days on unemployment benefits in year \(t\) and a positive number of days on unemployment in year \(t+1\). The same definition applies to days on parental benefits and number of sick days reimbursed by social security (number of days exceeding 16 days of a sickness spell). Conversely, transitioning out of unemployment, parental leave, and sickness is defined as having a positive number of days in year \(t\) and zero days in year \(t+1\). We obtain information on contracted work hours and main employer from the Employment Register. Transition into part-time represents changes from full-time in year \(t\) into part-time in year \(t+1\), where part-time is defined as 36 hours per week or less. Finally, we use the firm identifier of the main employer to construct firm change from year \(t\) to \(t+1\). Note that life cycle events are not mutually exclusive. A person can both become unemployed and change main employer in the same year.

We investigate the likelihood of these events in six groups of workers, sorted by the size of their earnings change between \(t\) and \(t+1\).25 Rows (1)-(5) of Table II show the fraction of workers within each group who experience the listed five life-cycle events. In rows (6)-(9), we report the average changes in log hours and log wage rates for each group of workers on impact (between \(t\) and \(t+1\)) and five years later (between \(t\) and \(t+5\)). The upper panel shows the entire sample of males, and the second and third panels show the results for the bottom and top recent earnings deciles, respectively.

The events corresponding to the largest earnings changes (bigger than 50 log points, columns (1) and (6)) and the intermediate changes (between 25 to 50 log points, columns (2) and (5)) are quite similar. The only exception is that parental leave is more likely in columns (2) and (5) than it is in columns (1) and (6). As for the minor changes—the ones smaller than 25 log points—they are less likely to be associated with these events.

The most frequent cause of large losses (>50 log points) is long-term sickness, 23%, followed by change of employer, 19%, and going from full-time to part-time, 15%. Only 8% of those suffering large losses have experienced unemployment. However, an unemployment spell is on average longer than a sickness spell. The average number of weeks with sickness benefits (for males in our base sample) is around 8 weeks, whereas an average unemployment spell is 20 weeks. For those experiencing the largest earnings losses, the average decline in log hours is slightly smaller than the average log hourly wage loss: -0.40 versus -0.44. However, as discussed above, wage rate declines are substantially more persistent than hours declines. After five years, wage rates are down by 19 log points, whereas hours is only 3 log points lower.

The events behind the large positive earnings changes are relatively symmetric to the events associated with large earnings losses. The events most frequently associated with large positive changes are change of employer, 23%; going from part-time to full-time, also 23%; and returning from long-term sickness, 25%. The average change in log hours for workers with the largest positive earnings shocks is 0.40, which is somewhat smaller than the average change in the log hourly wage rate, 0.45. Increases in both hours and wages are quite persistent as well.

Overall, these patterns are similar for most income groups except for the top earners, for whom large earnings losses are to a smaller extent caused by unemployment or sickness. For the top group, large earnings losses are more closely associated with firm change than anything else. Conversely, for low-income earners, large earnings gains are chiefly associated with changes of employer and changes from part-time to full-time. The results in rows (6)-(9) of Table II confirm the findings from Figure 5 that negative shocks are transitory and positive shocks are permanent for the average worker, including the bottom decile, whereas for top earners, large negative changes in hourly wage rates are more persistent than negative changes in hours.

5 Higher-Order Earnings Risk

We now turn to the higher-order moments of individual earnings, hours and hourly wage changes. In order to investigate “transitory” and “persistent” innovations separately, it is useful to distinguish between growth over short (one-year between \(t\) and \(t+1\)) and long (five-year from \(t\) to \(t+5\)) horizons. The persistent component of changes becomes more salient the longer the horizon (Guvenen et al. (2019)).26 In the main text, we focus on five-year changes since persistent changes are economically more important for consumption and savings behavior. The results for one-year changes are qualitatively similar (see Appendix B). In constructing the figures, we calculate the average of the moment of interest for each age/RE group over the years between 2003 and 2009.

| Annual Earnings Change, \(\Delta y\in\) | |||||||

| All | One-Year Earnings Loss | One-Year Earnings Gain | |||||

| Life-cycle event | \(\lt -0.5\) | \([-0.5,-0.25)\) | \([-0.25,0.0)\) | \([0.0,0.25)\) | \([0.25,0.5)\) | \(\geq 0.5\) | |

| into/out of | (1) | (2) | (3) | (4) | (5) | (6) | |

| (1) | Unemployment | 0.08 | 0.06 | 0.02 | 0.02 | 0.08 | 0.10 |

| (2) | Long-term sickness | 0.23 | 0.23 | 0.09 | 0.10 | 0.22 | 0.25 |

| (3) | Part-time | 0.15 | 0.11 | 0.05 | 0.07 | 0.16 | 0.23 |

| (4) | Parental leave | 0.06 | 0.08 | 0.04 | 0.05 | 0.08 | 0.05 |

| (5) | Firm change | 0.19 | 0.22 | 0.12 | 0.13 | 0.21 | 0.23 |

| (6) | \(\mathbb{E}\left [\Delta _{\log}^{1}h_{t}^{i}\right]\) | -0.40 | -0.16 | -0.03 | 0.03 | 0.17 | 0.40 |

| (7) | \(\mathbb{E}\left [\Delta _{\log}^{5}h_{t}^{i}\right]\) | -0.03 | -0.03 | -0.03 | 0.00 | 0.13 | 0.37 |

| (8) | \(\mathbb{E}\left [\Delta _{\log}^{1}w_{t}^{i}\right]\) | -0.44 | -0.18 | -0.04 | 0.05 | 0.17 | 0.45 |

| (9) | \(\mathbb{E}\left [\Delta _{\log}^{5}w_{t}^{i}\right]\) | -0.19 | -0.15 | -0.04 | 0.04 | 0.13 | 0.40 |

| (10) | # of Obs. | 104,727 | 298,777 | 2,219,654 | 1,973,893 | 320,891 | 111,353 |

| Lowest decile (RE=1) | (1) | (2) | (3) | (4) | (5) | (6) | |

| (1) | Unemployment | 0.10 | 0.09 | 0.04 | 0.05 | 0.10 | 0.10 |

| (2) | Long-term sickness | 0.20 | 0.19 | 0.10 | 0.10 | 0.14 | 0.13 |

| (3) | Part-time | 0.16 | 0.12 | 0.06 | 0.13 | 0.25 | 0.32 |

| (4) | Parental leave | 0.03 | 0.04 | 0.03 | 0.02 | 0.03 | 0.02 |

| (5) | Firm change | 0.19 | 0.22 | 0.14 | 0.17 | 0.24 | 0.28 |

| (6) | \(\mathbb{E}\left [\Delta _{\log}^{1}h_{t}^{i}\right]\) | -0.38 | -0.16 | -0.03 | 0.05 | 0.17 | 0.37 |

| (7) | \(\mathbb{E}\left [\Delta _{\log}^{5}h_{t}^{i}\right]\) | -0.00 | -0.01 | -0.02 | 0.03 | 0.13 | 0.37 |

| (8) | \(\mathbb{E}\left [\Delta _{\log}^{1}w_{t}^{i}\right]\) | -0.50 | -0.19 | -0.05 | 0.05 | 0.17 | 0.51 |

| (9) | \(\mathbb{E}\left [\Delta _{\log}^{5}w_{t}^{i}\right]\) | -0.05 | -0.06 | -0.01 | 0.06 | 0.13 | 0.58 |

| (10) | # of Obs. | 17,813 | 22,993 | 124,680 | 145,885 | 39,418 | 37,547 |

| Top decile (RE=10) | (1) | (2) | (3) | (4) | (5) | (6) | |

| (1) | Unemployment | 0.05 | 0.02 | 0.00 | 0.00 | 0.02 | 0.10 |

| (2) | Long-term sickness | 0.08 | 0.09 | 0.05 | 0.05 | 0.08 | 0.25 |

| (3) | Part-time | 0.15 | 0.11 | 0.06 | 0.06 | 0.11 | 0.23 |

| (4) | Parental leave | 0.05 | 0.08 | 0.05 | 0.06 | 0.08 | 0.05 |

| (5) | Firm change | 0.31 | 0.24 | 0.13 | 0.12 | 0.21 | 0.23 |

| (6) | \(\mathbb{E}\left [\Delta _{\log}^{1}h_{t}^{i}\right]\) | -0.18 | -0.09 | -0.02 | 0.03 | 0.08 | 0.16 |

| (7) | \(\mathbb{E}\left [\Delta _{\log}^{5}h_{t}^{i}\right]\) | -0.03 | -0.03 | -0.02 | 0.00 | 0.04 | 0.10 |

| (8) | \(\mathbb{E}\left [\Delta _{\log}^{1}w_{t}^{i}\right]\) | -0.67 | -0.25 | -0.06 | 0.05 | 0.26 | 0.64 |

| (9) | \(\mathbb{E}\left [\Delta _{\log}^{5}w_{t}^{i}\right]\) | -0.50 | -0.23 | -0.05 | 0.04 | 0.14 | 0.30 |

| (10) | # of Obs. | 15,274 | 34,208 | 310,628 | 298,130 | 32,251 | 11,015 |

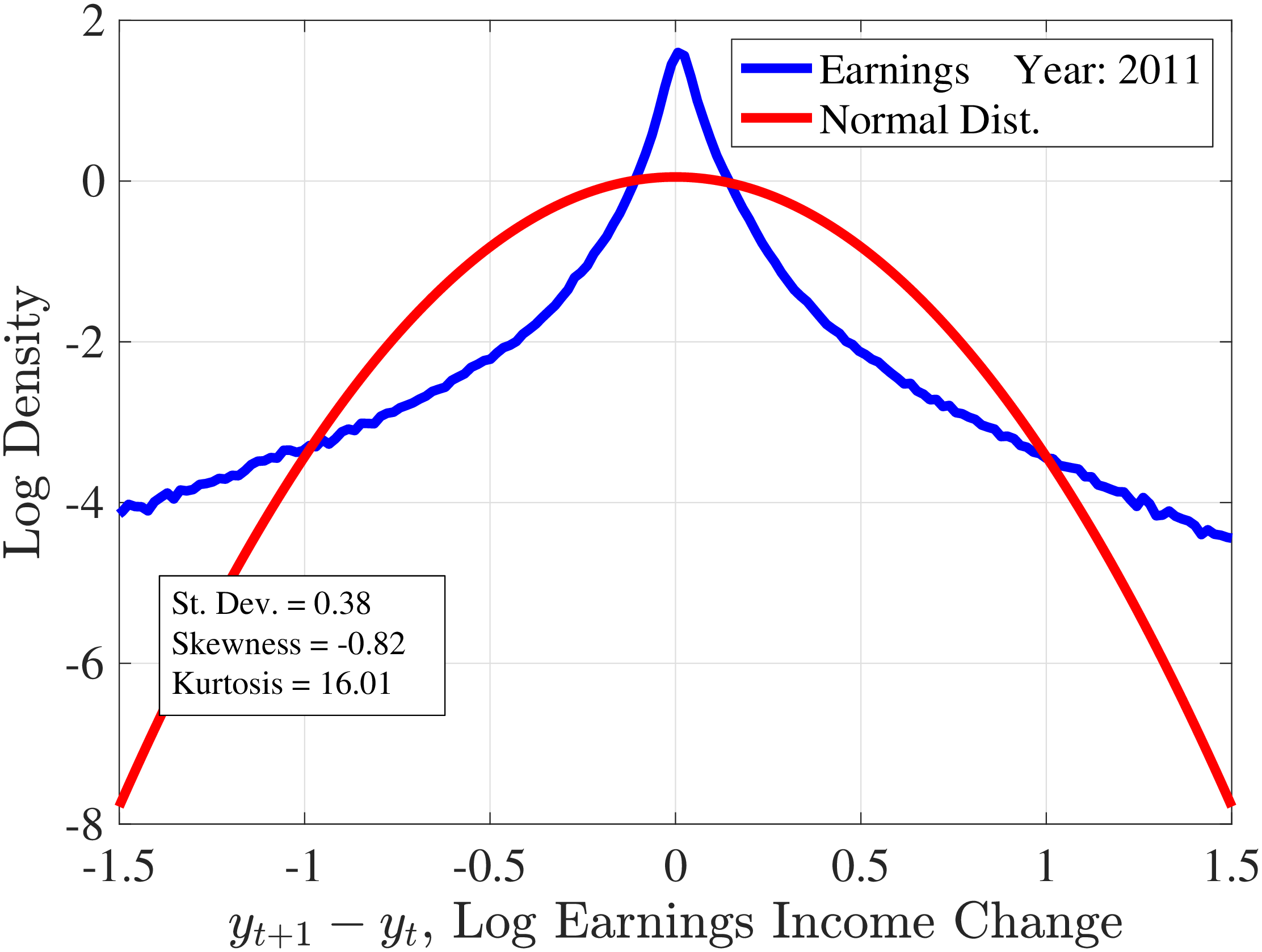

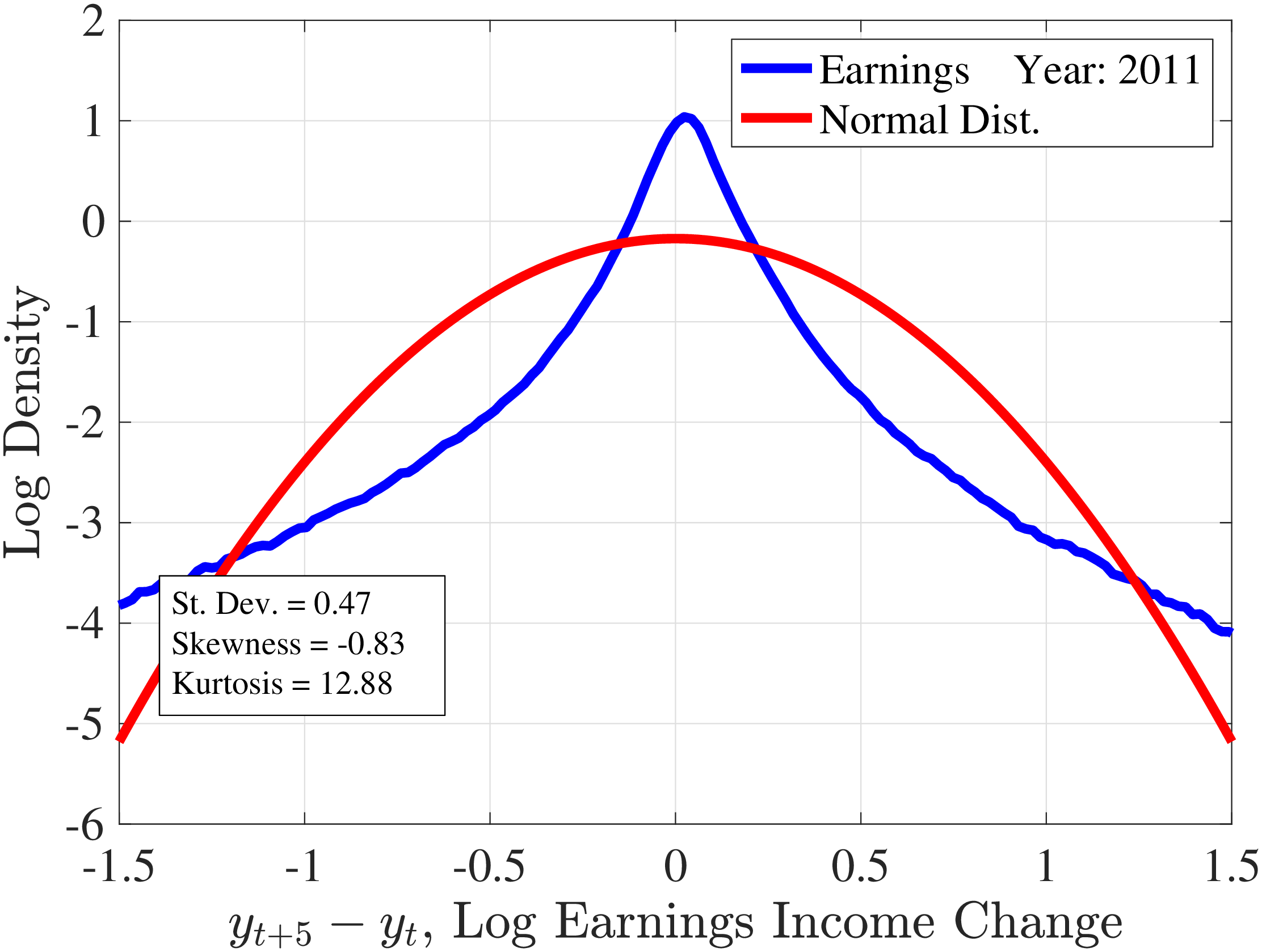

Figure 6 displays the distribution of one-year (left panel) and five-year (right panel) individual earnings growth for male workers in the base sample defined in Section 3.3, along with Gaussian densities with the same standard deviation as in the data. The earnings growth distribution displays left (negative) skewness and excess kurtosis relative to a Gaussian density. In other words, workers face an earnings change distribution with a slightly longer left tail relative to the right tail, and there are far more people with very small and very large changes and fewer people with intermediate changes. Note that the deviations from normality are larger for one-year changes than for five-year changes. These qualitative properties are in line with findings for many other countries.

Figure 6

–

Histograms of One- and Five-Year Log Earnings Changes

Note: The figure plots the empirical densities of one- and five-year earnings changes superimposed on Gaussian densities with the same variance. The data are for male workers in the base sample defined in Section 3 and \(t=2011\).

Figure: Figure 6 – Histograms of One- and Five-Year Log Earnings Changes

5.1 Higher-Order Moments for Male Earnings Growth

We now document the higher-order moments of earnings growth in Norway. Appendix B.1 contains analogous results for the U.S. as well as results for one-year earnings growth in Norway.27 For comparability with earlier work, we focus on men. The results for women are reported in Appendix E. Our measure of skewness is the third standardized moment (i.e., \(\operatorname{Skew}[X]=\sum _{i}^{N}\left (X_{i}-\bar{X}\right)^{3}/[(N-1)*\sigma ^{3}]\)), and our measure of kurtosis is the fourth standardized moment (i.e., Pearson’s kurtosis, \(\operatorname{Kurt}[X]=\sum _{i}^{N}\left (X_{i}-\bar{X}\right)^{4}/[(N-1)*\sigma ^{4}]\)).

(a) Variance

(a) Variance  (b) Skewness

(b) Skewness  (c) Kurtosis

(c) Kurtosis

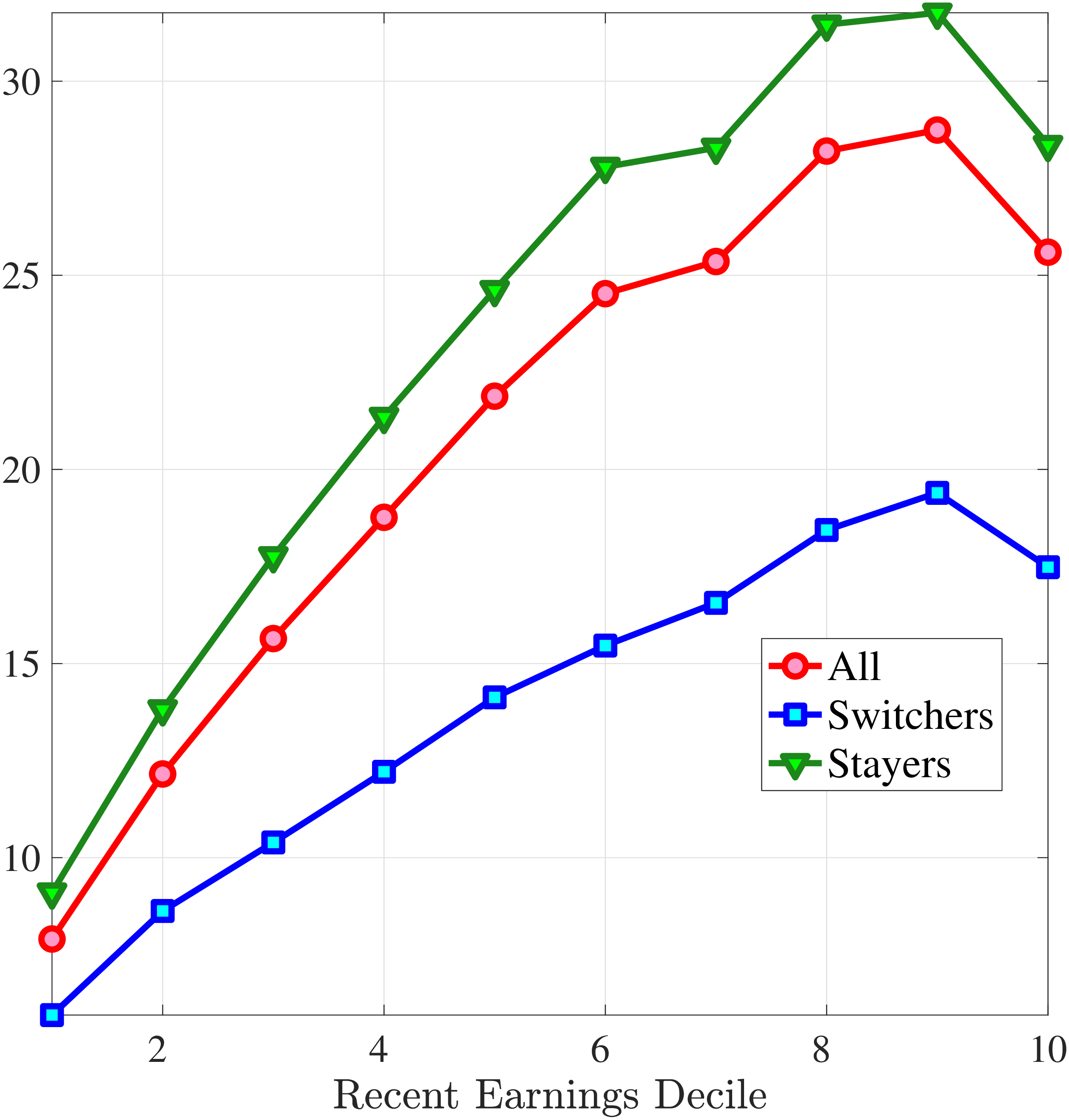

Figure 7

–

Cross-Sectional Moments for Five-Year Earnings Growth in Norway

Note: The figure displays the higher-order moments of five-year log earnings changes (\(y_{t+5}-y_{t}\)) for young males (red line) and prime-age males (blue line) for each decile of RE.

Figure: Figure 7 – Cross-Sectional Moments for Five-Year Earnings Growth in Norway

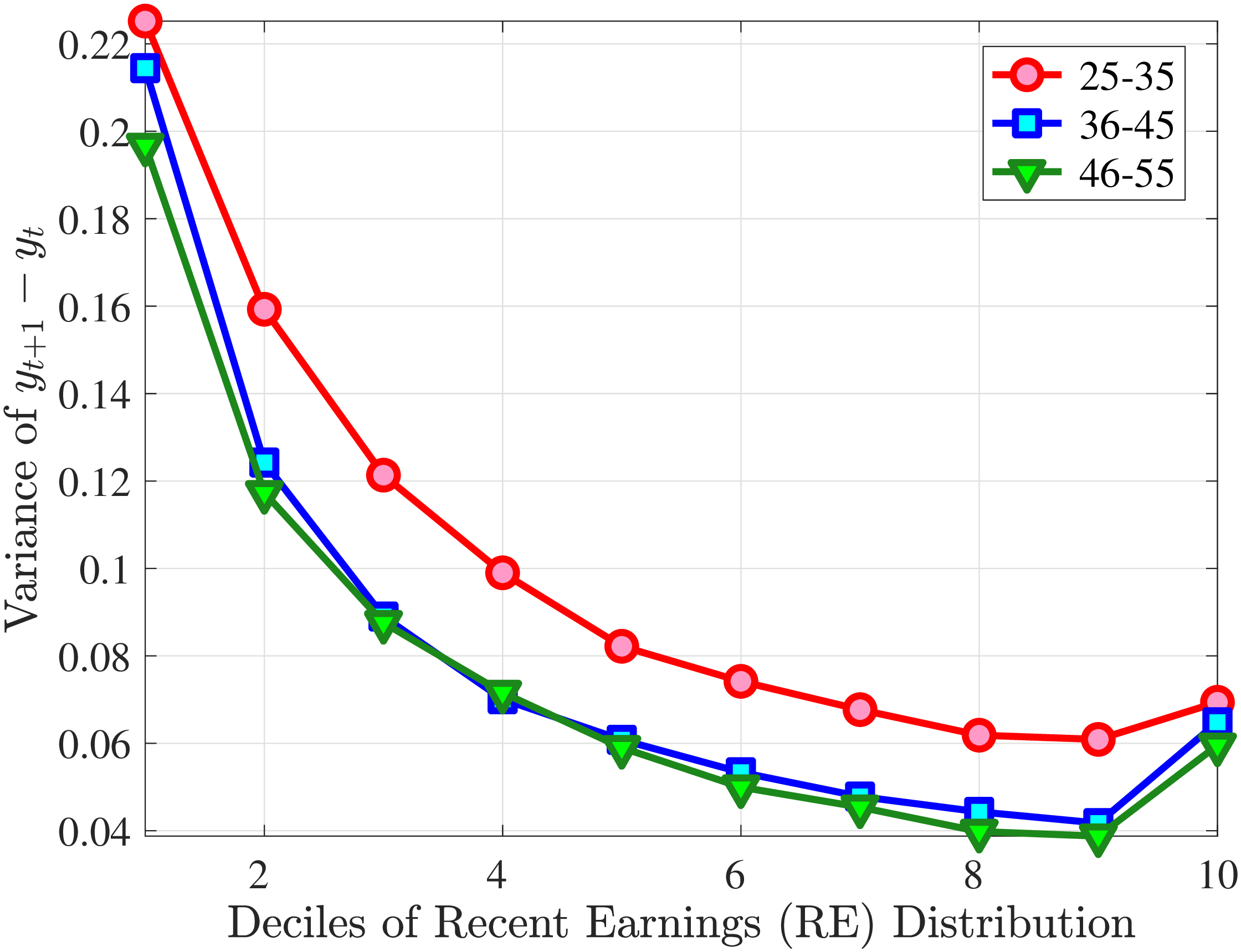

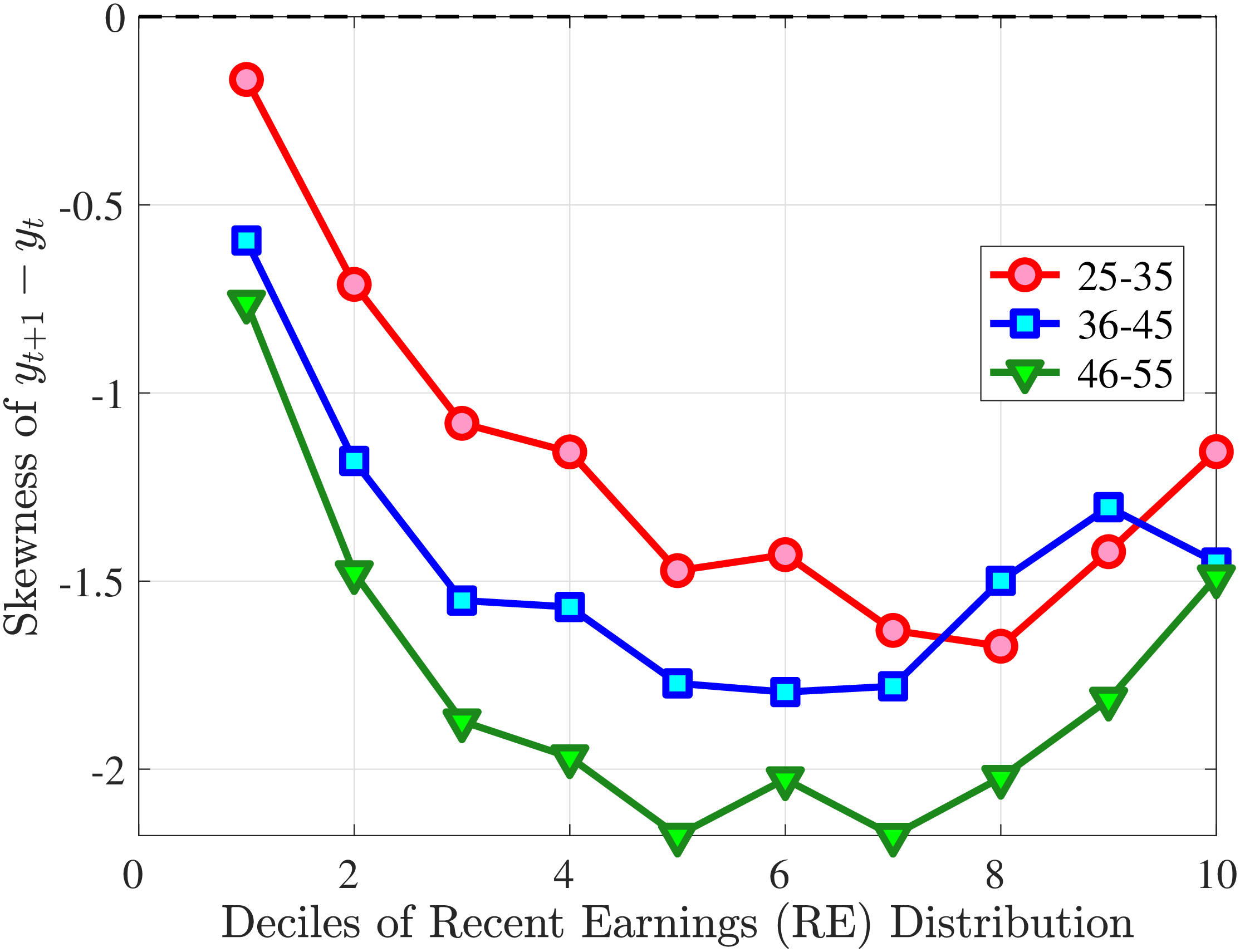

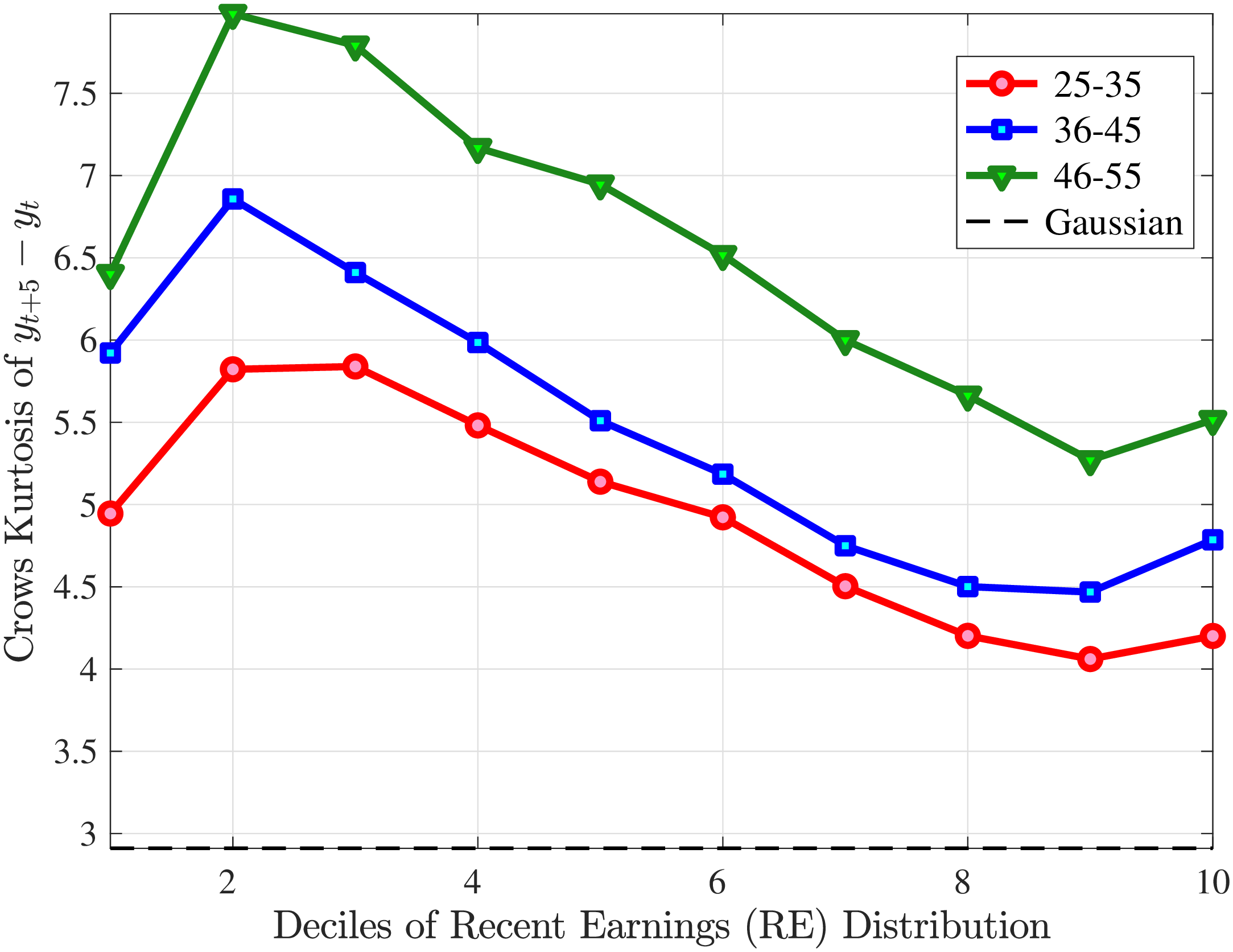

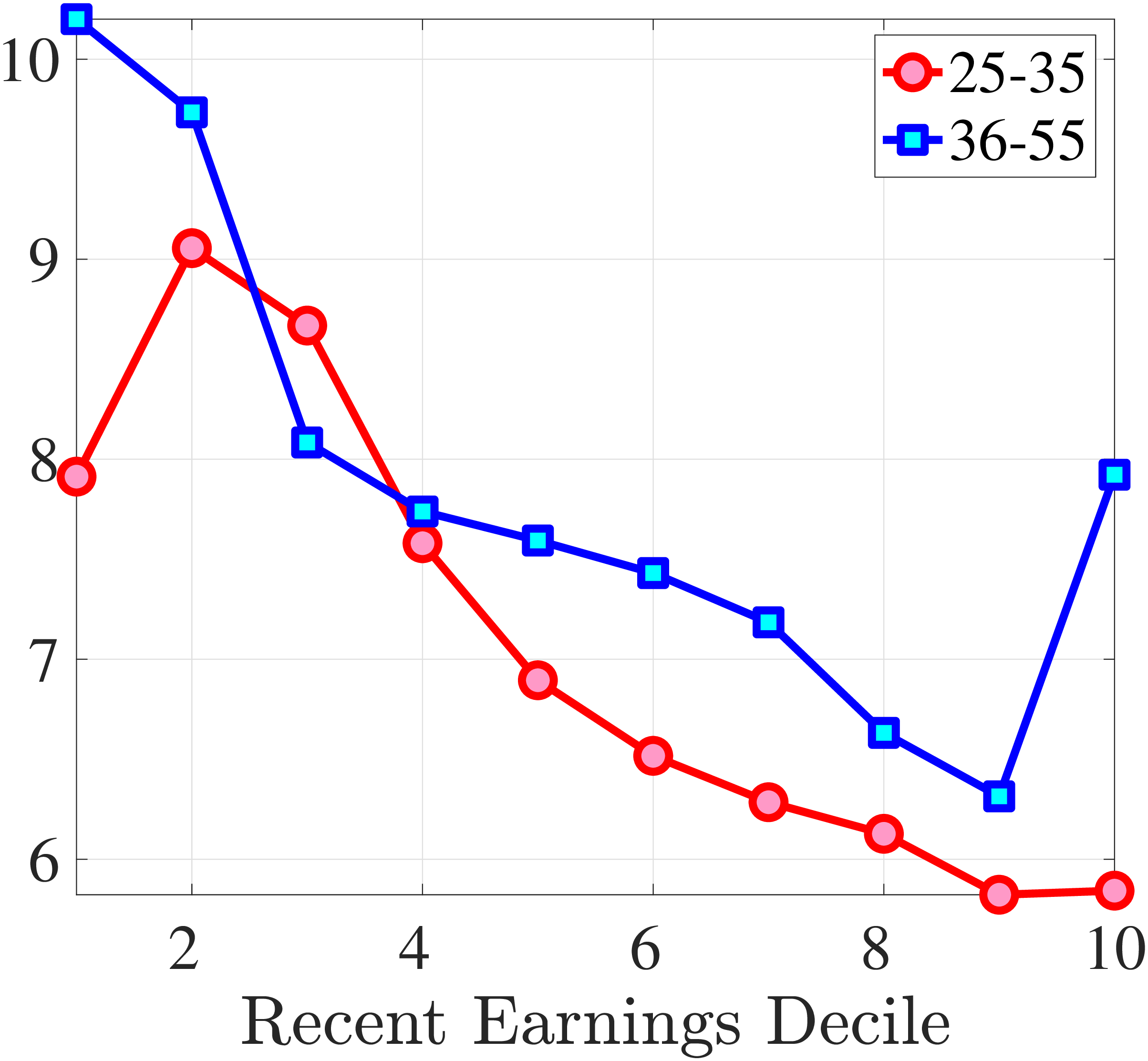

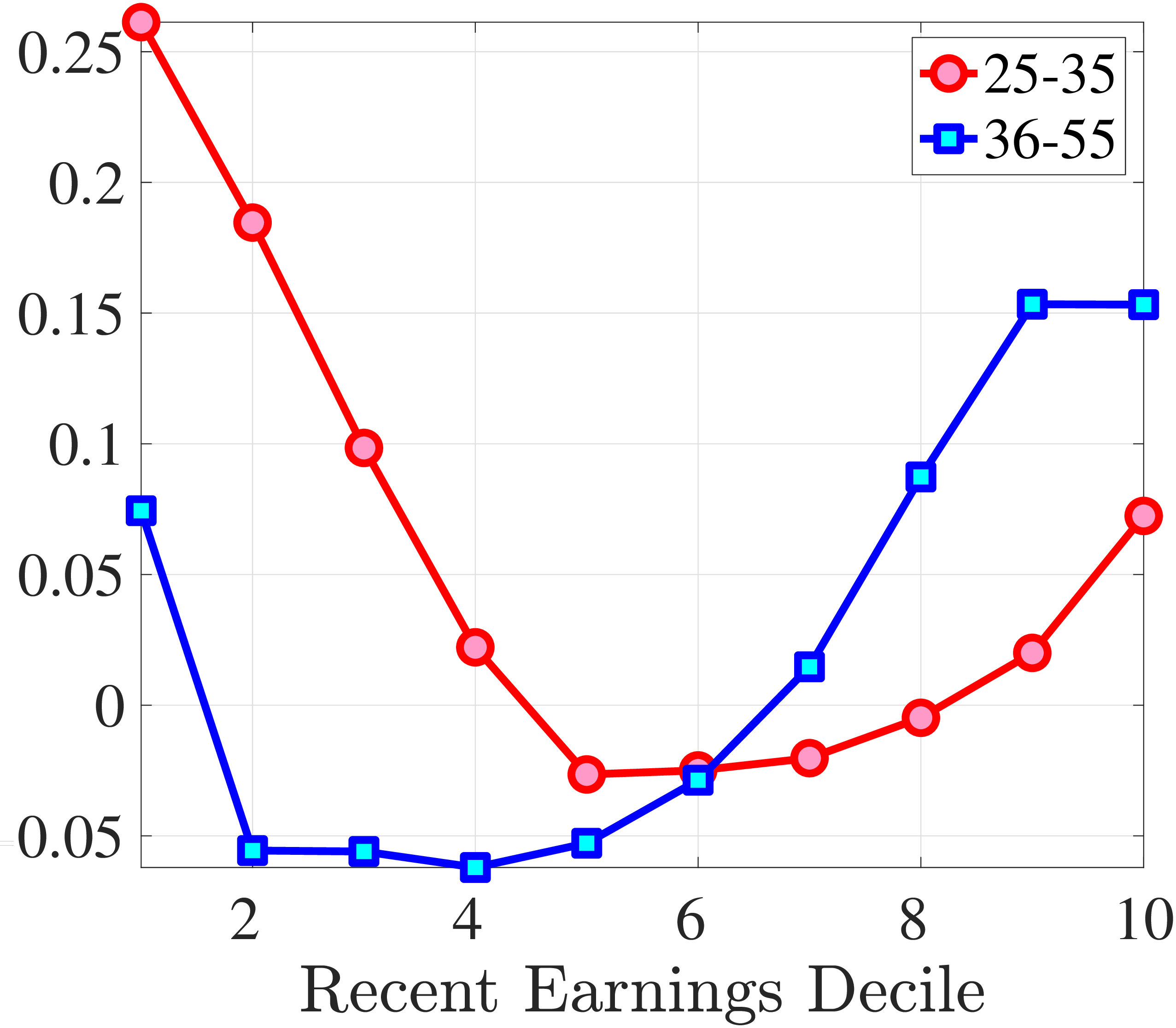

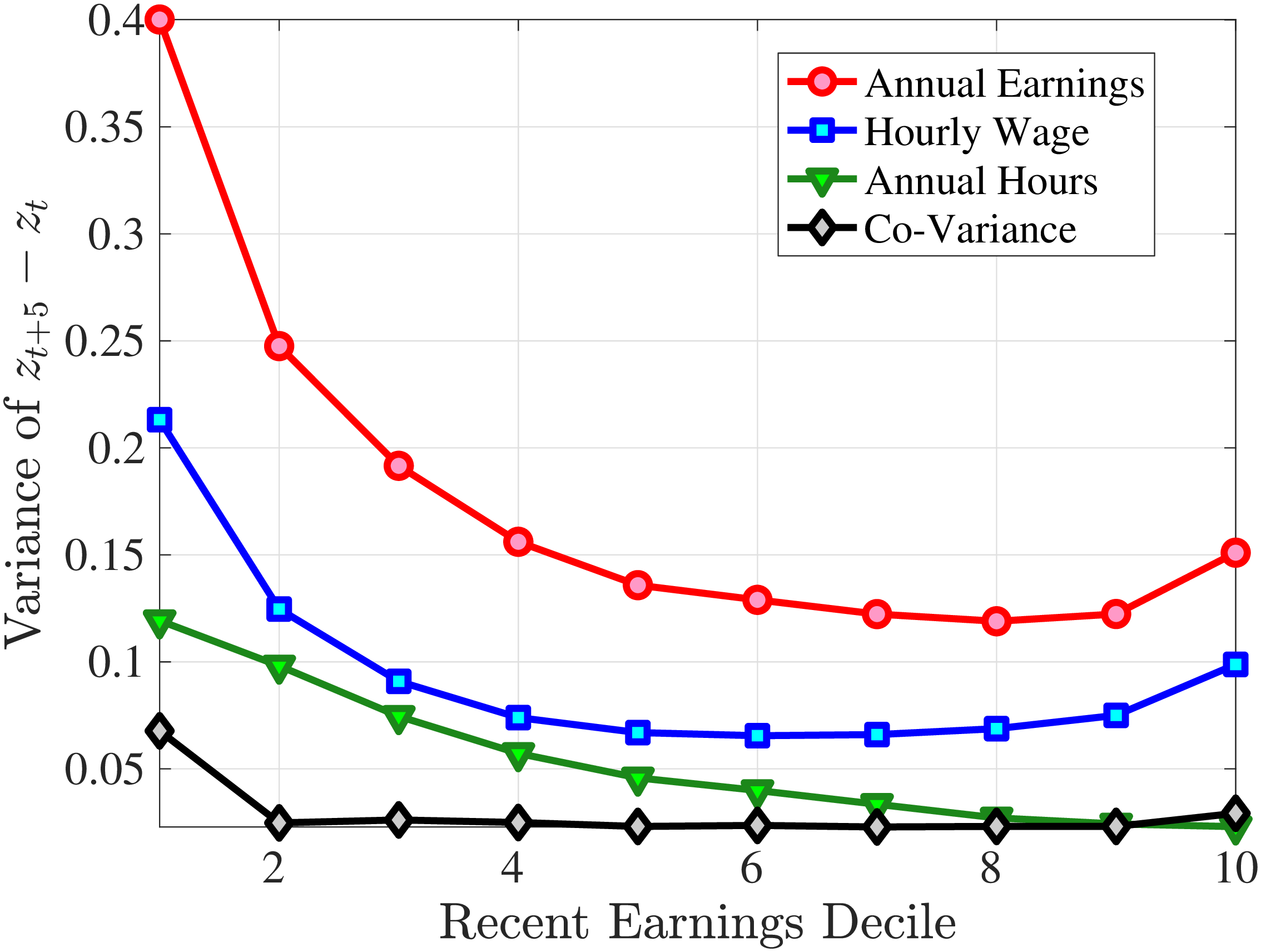

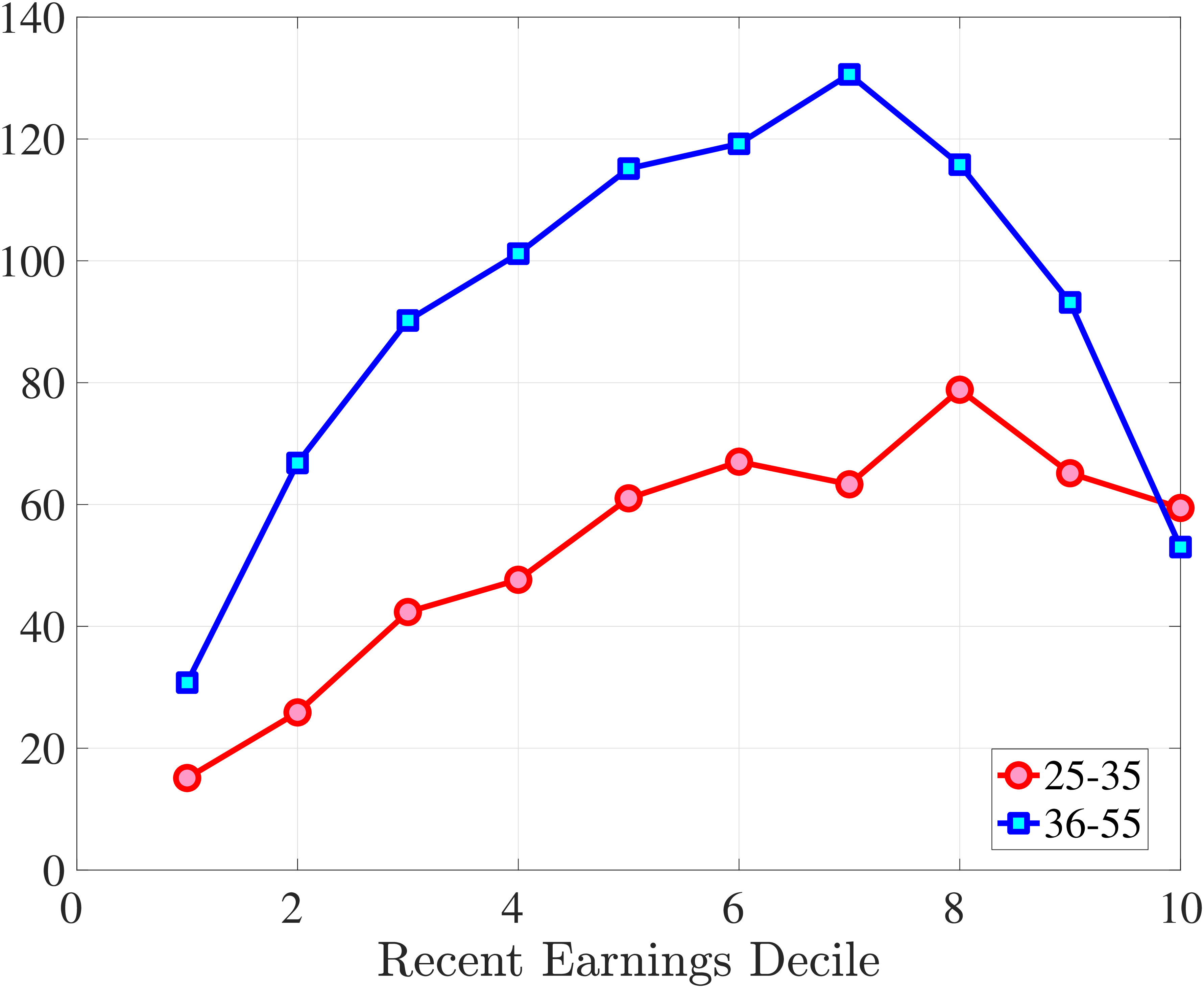

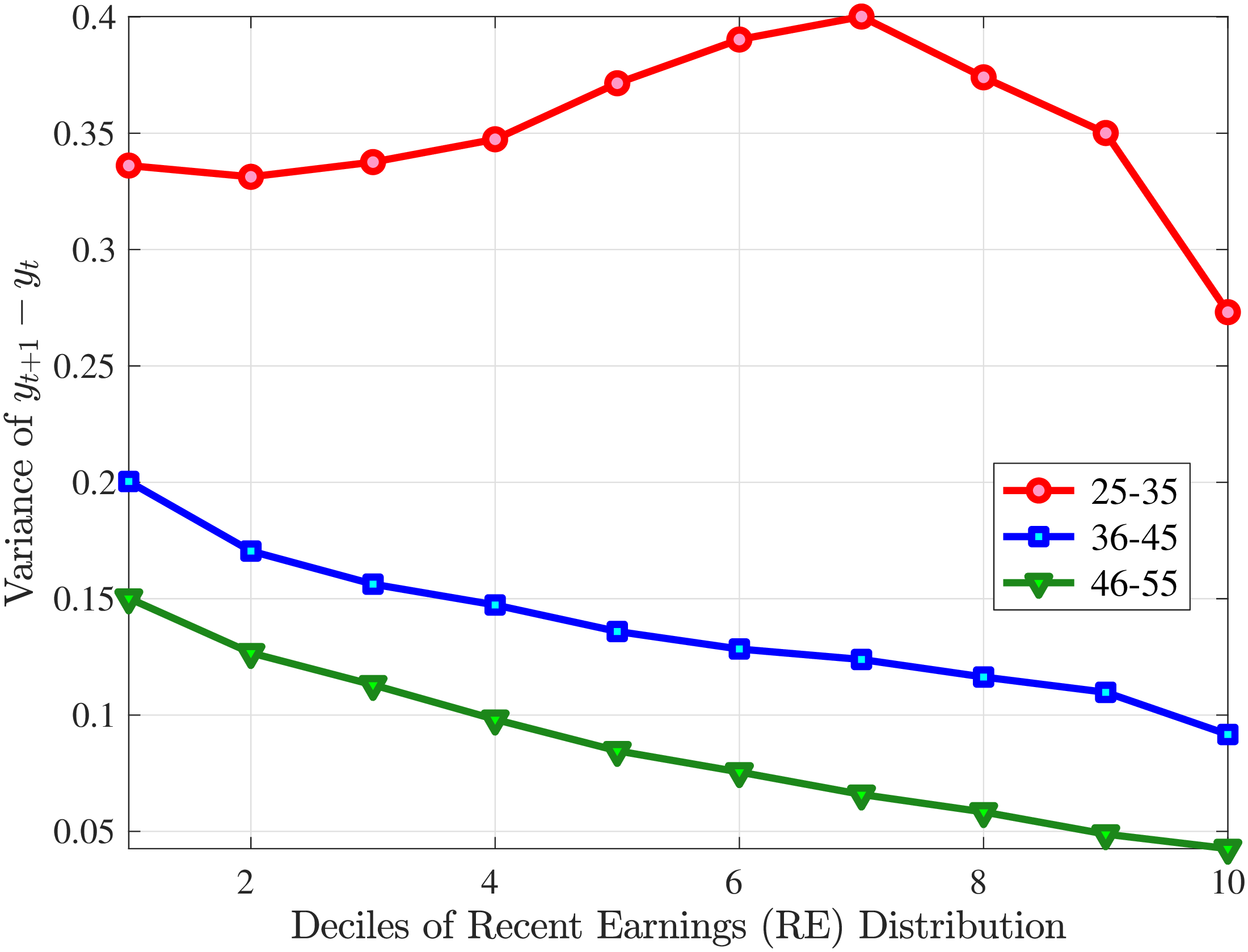

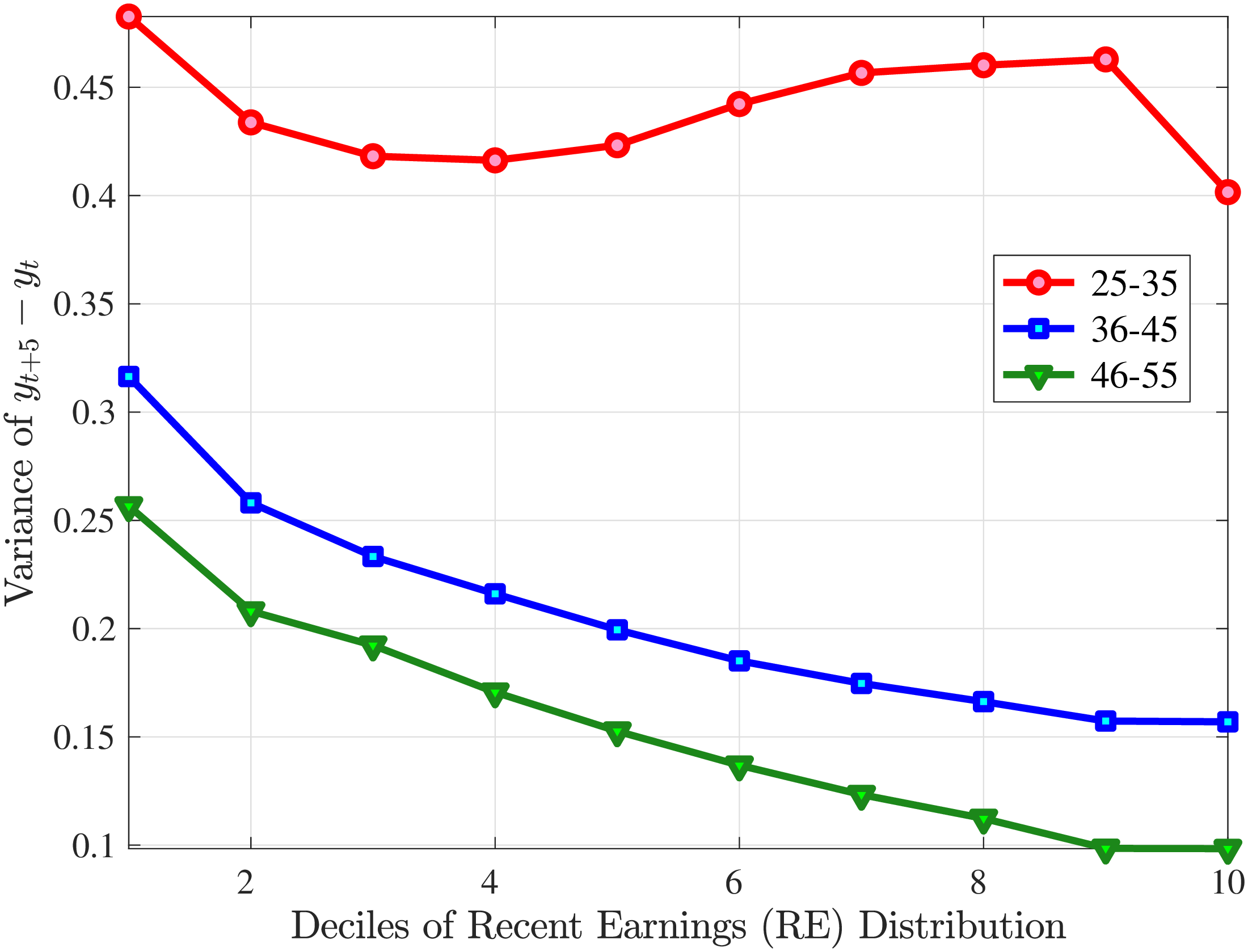

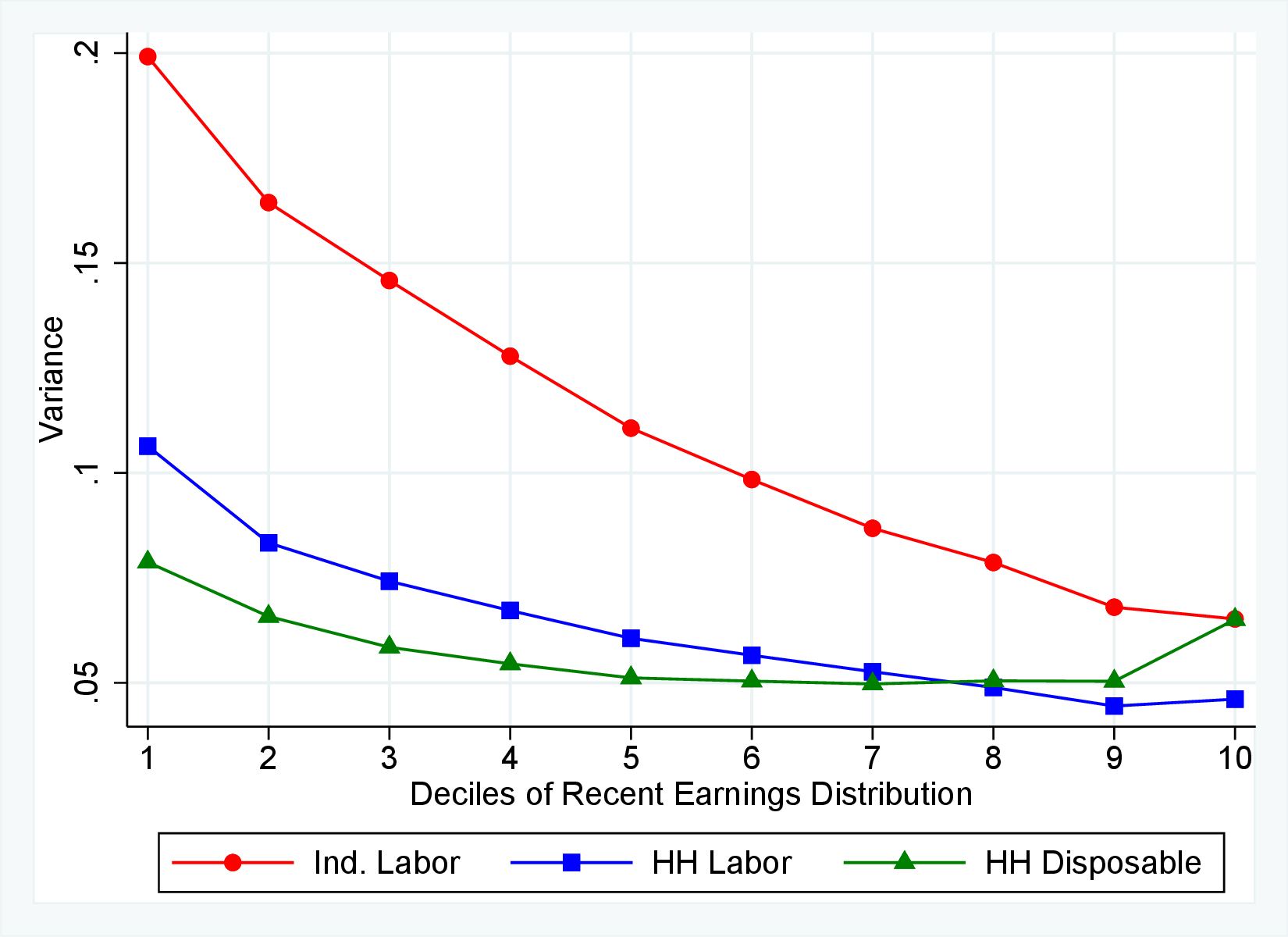

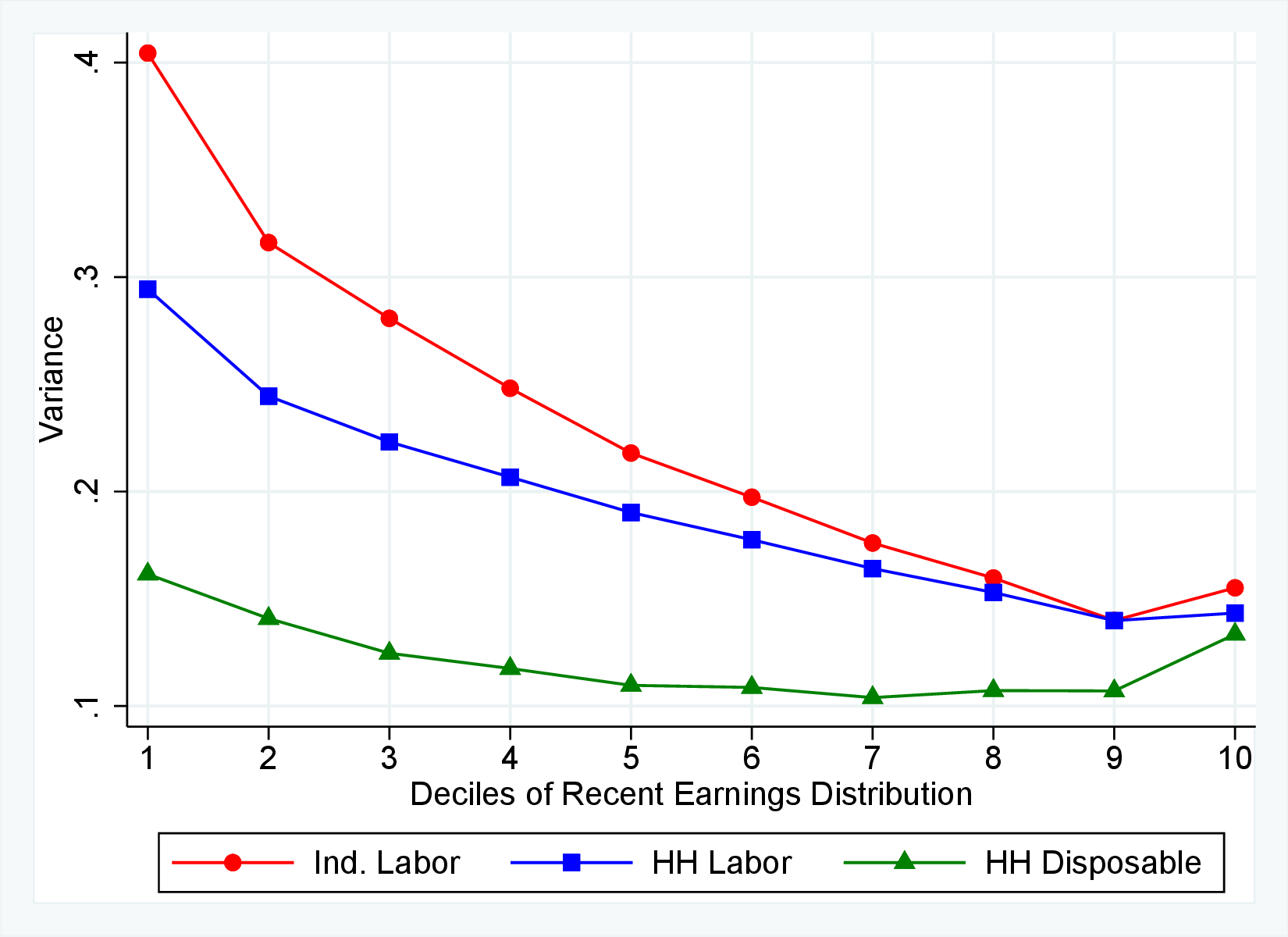

Starting with the second moment, Figure 7 shows the variance of five-year earnings growth between \(t\) and \(t+5\) conditional on workers’ age and RE in \(t-1\). Workers differ significantly in the dispersion of earnings growth they face with respect to their RE. In particular, for prime-age workers, the variance declines monotonically from around 0.30 for the bottom decile of RE to roughly 0.09 for the 90th percentile, after which it increases to 0.14. The life-cycle variation is smaller than the differences across RE groups, with the variance of shocks being largest for the young workers (ages 25-35). These patterns are qualitatively similar to those found for the U.S., although the variance of earnings growth is substantially smaller in Norway (Figures B.1 and B.2).

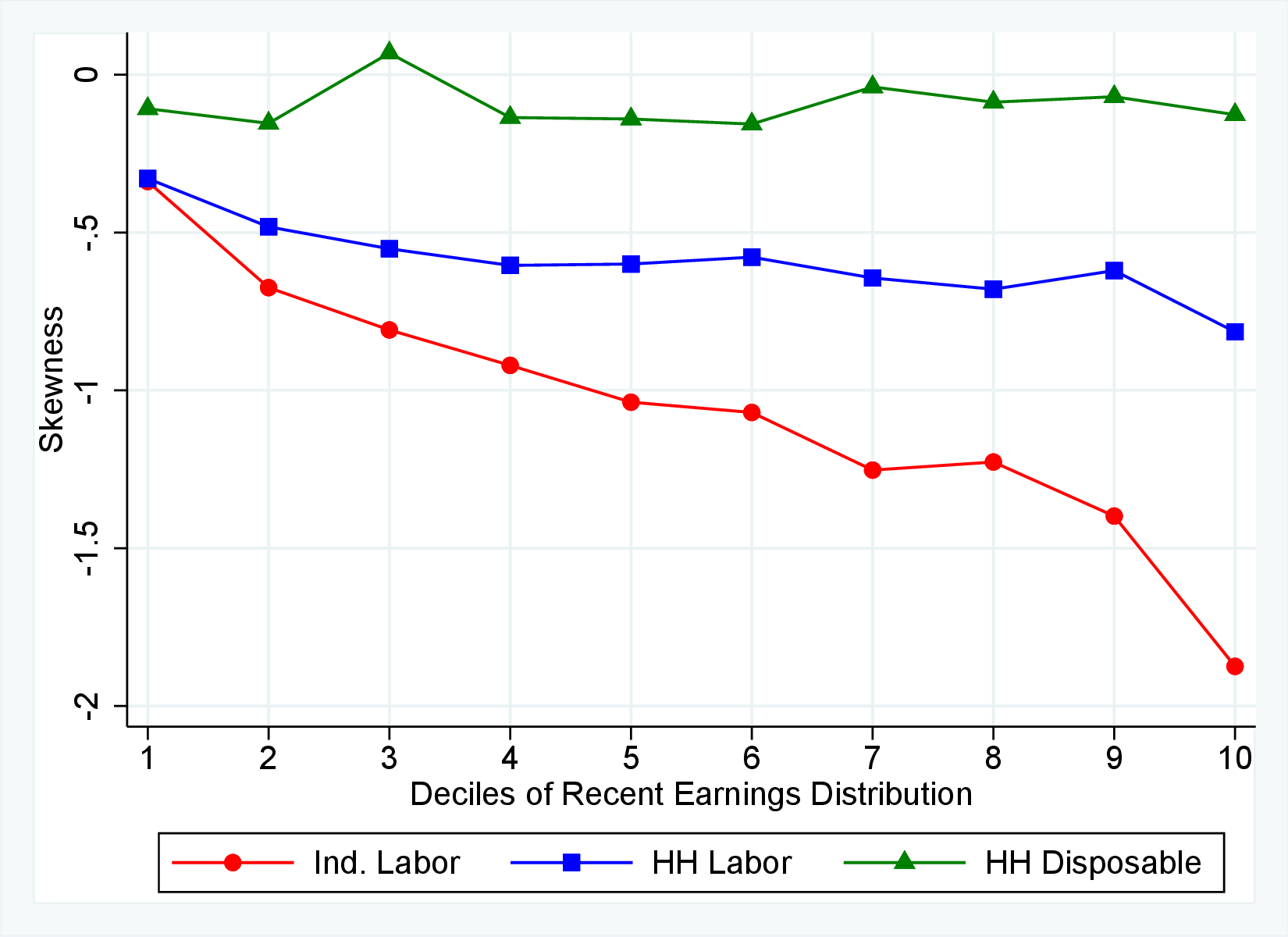

Next, Figure 7 shows that almost all male workers face a left-skewed distribution of five-year log earnings growth regardless of their RE and age, meaning that experiencing very large declines in earnings is more likely than seeing very large increases.28 However, skewness is more negative for prime-age workers.29 Thus, the older an individual gets or the higher his current earnings, the more gradual will be the upward movements and the more drastic will be the fall in earnings. These skewness patterns for earnings changes are similar to those documented for the U.S.

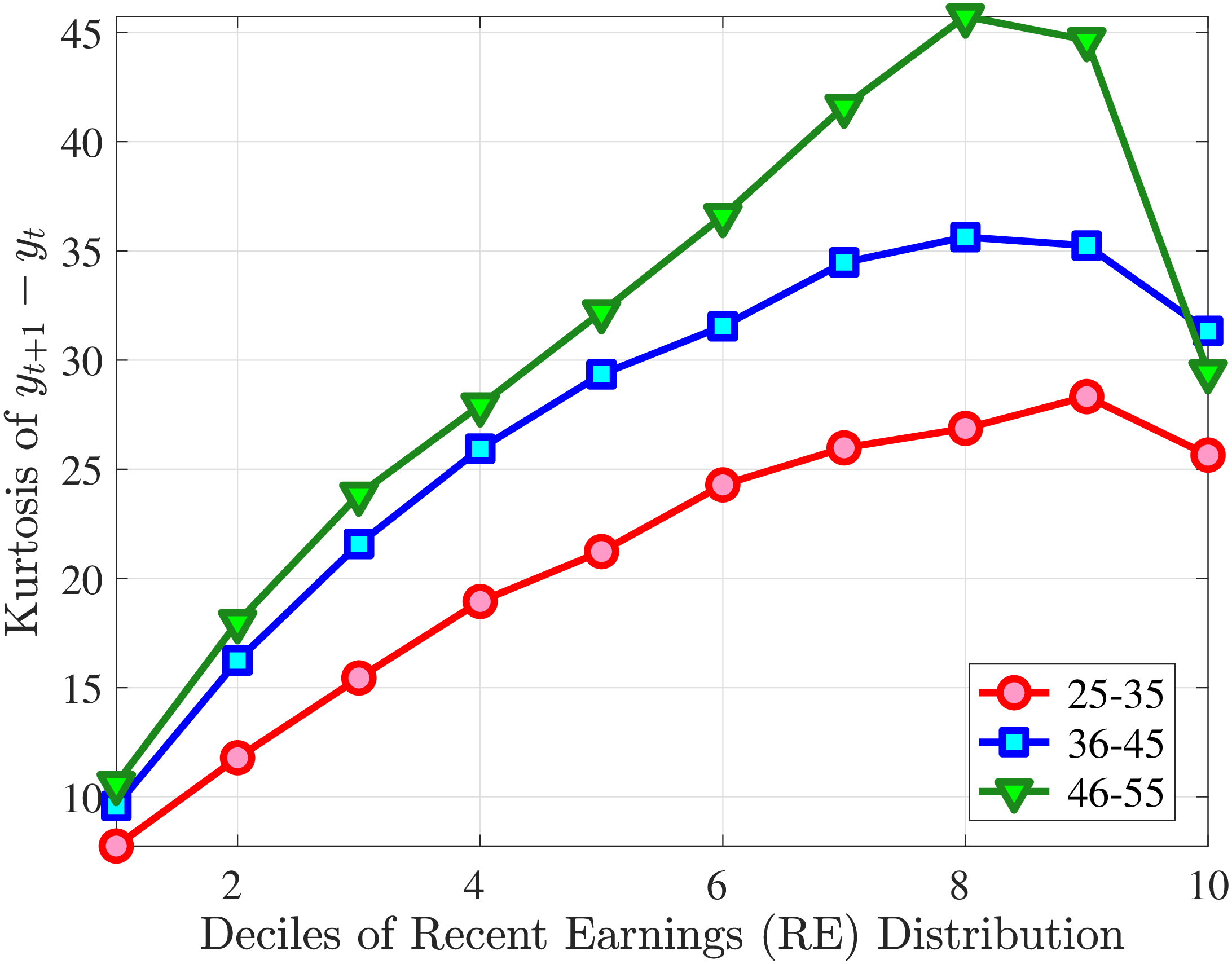

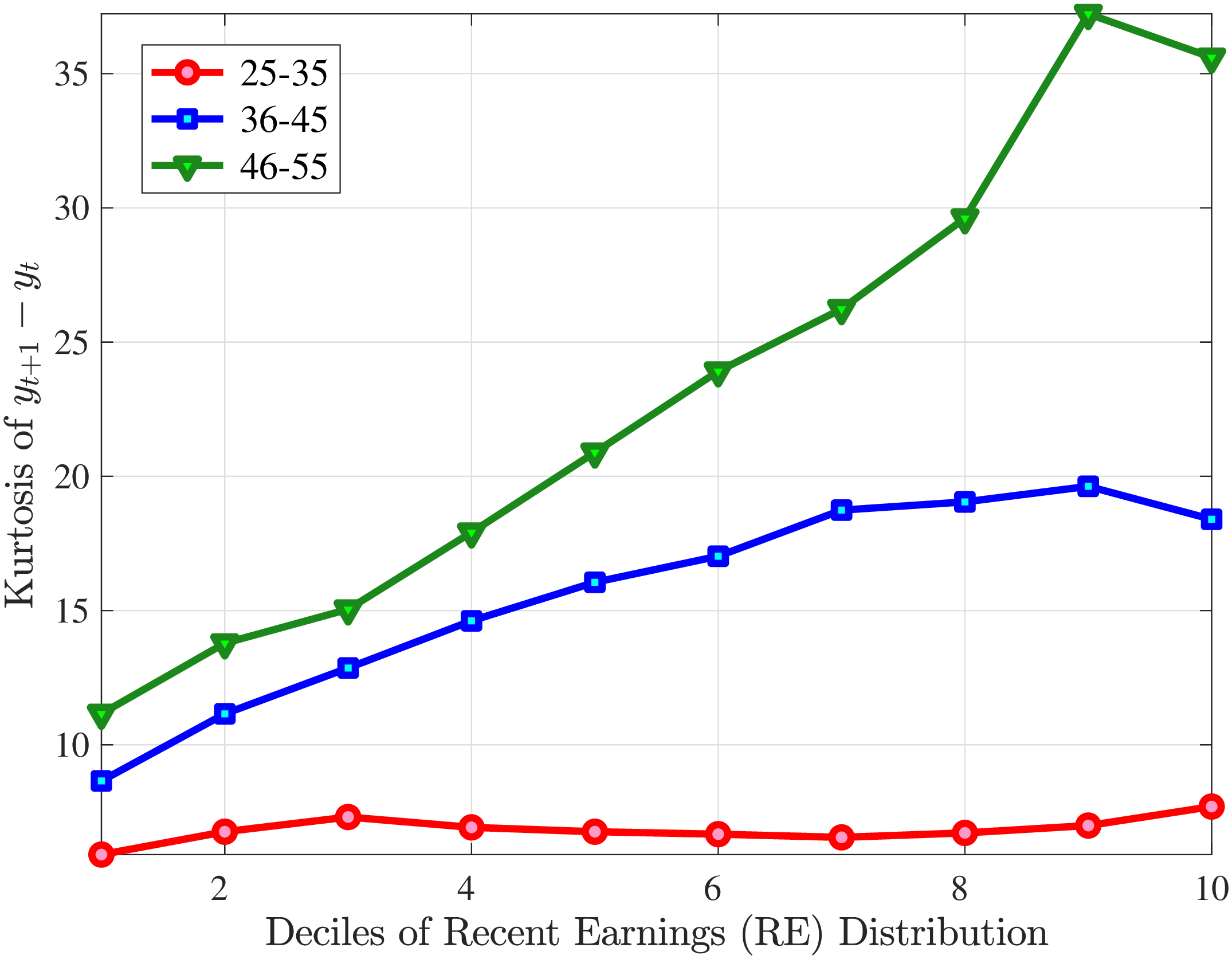

Figure 7 plots the fourth standardized moment of five-year earnings growth by age and RE. This kurtosis measure increases from around 8 for the bottom earners to more than 20 for workers with recent earnings above the median. The high kurtosis suggests that most workers experience negligible shocks, whereas a few workers experience large ones. Moreover, this asymmetry increases with age and tends to increase with recent earnings. Finally, the RE and age variations in the kurtosis of annual earnings growth in Norwegian data are similar to those documented for the U.S.

5.2 Distributions of Wage and Hours Growth

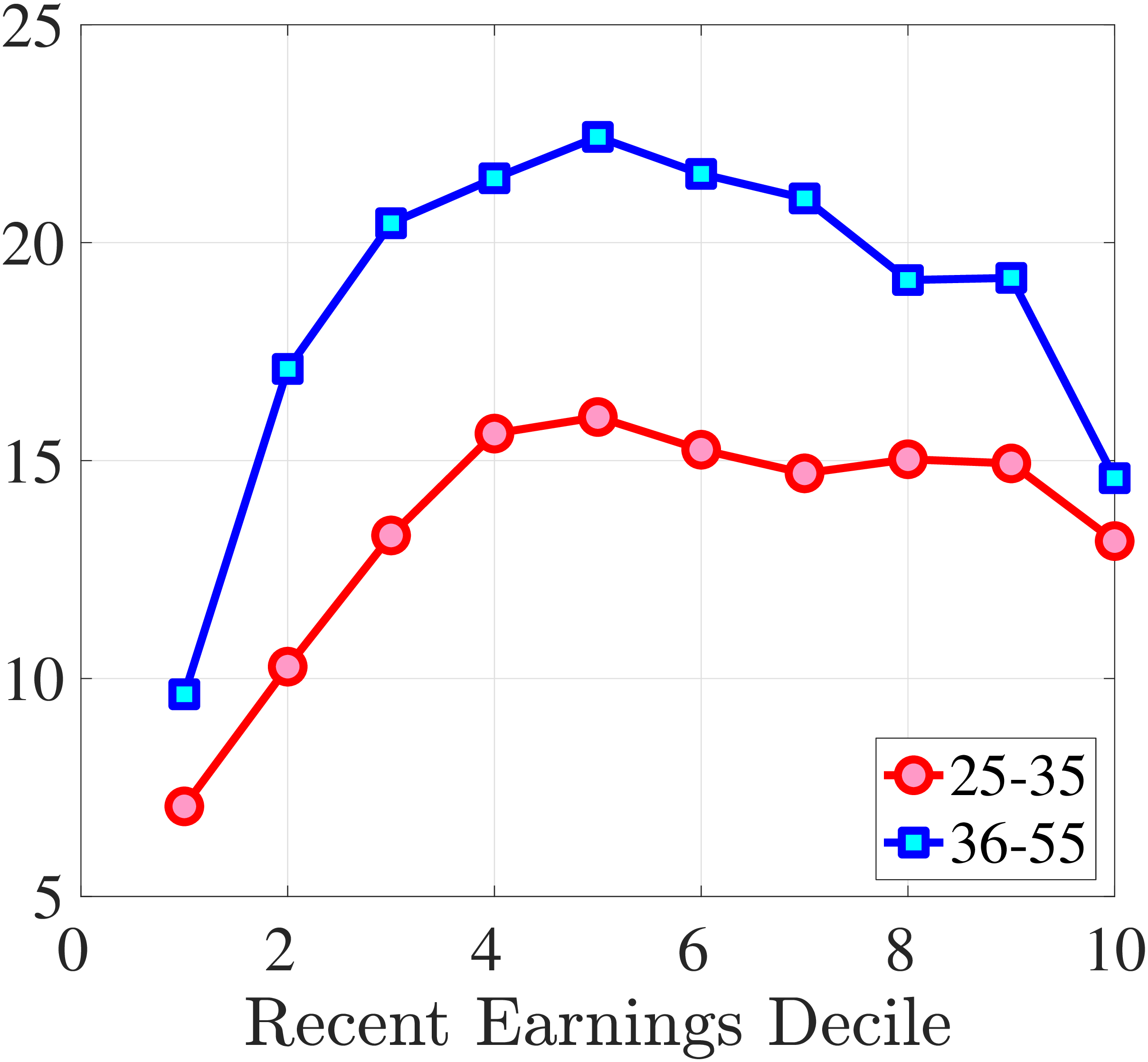

In this section, we study the extent to which the distributions of hours and wage growth display non-Gaussian features and investigate their roles in the higher-order moments of earnings. We follow a similar graphical methodology as in Section 5.1 and present the cross-sectional moments of hours and wage growth conditional on 3 age groups and 10 deciles of recent earnings.

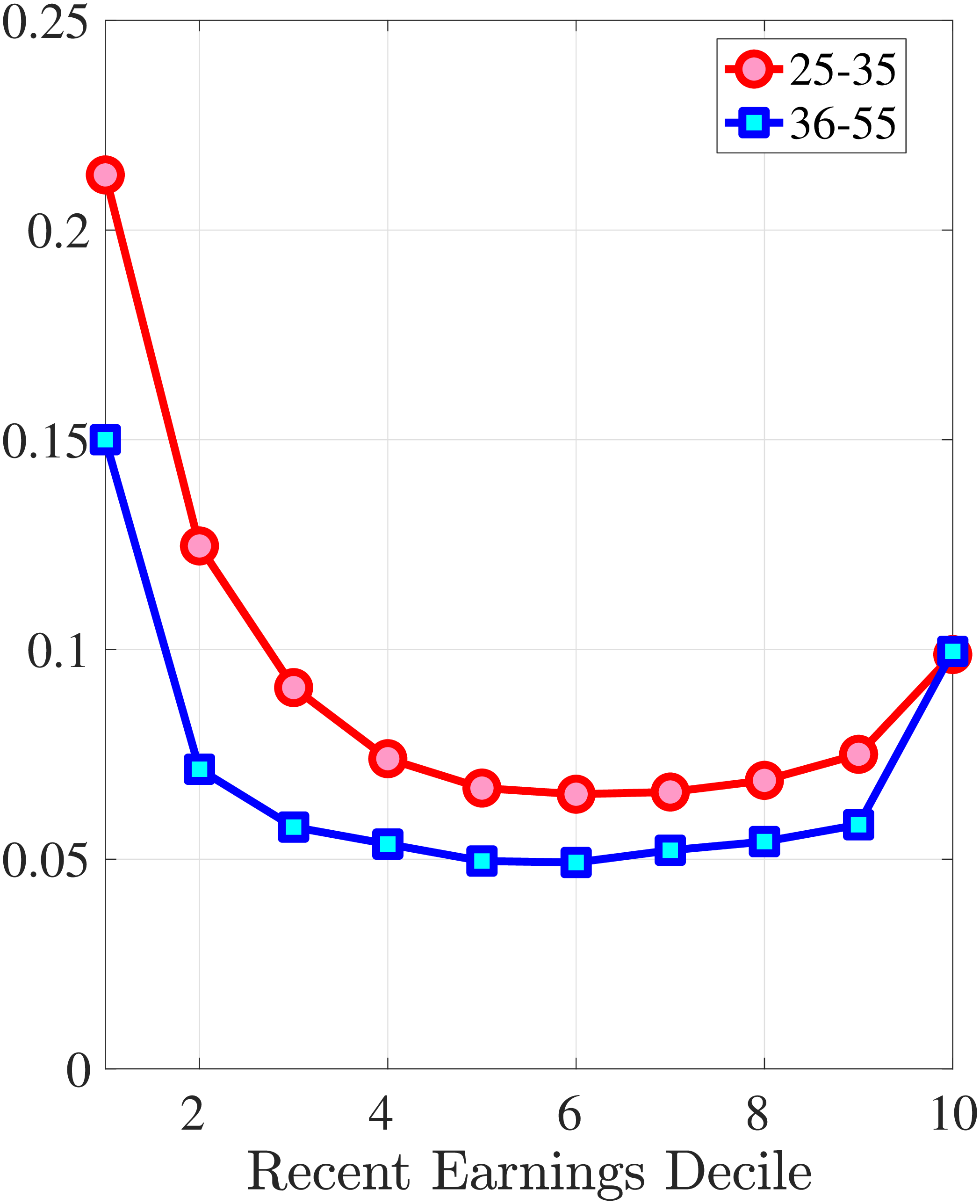

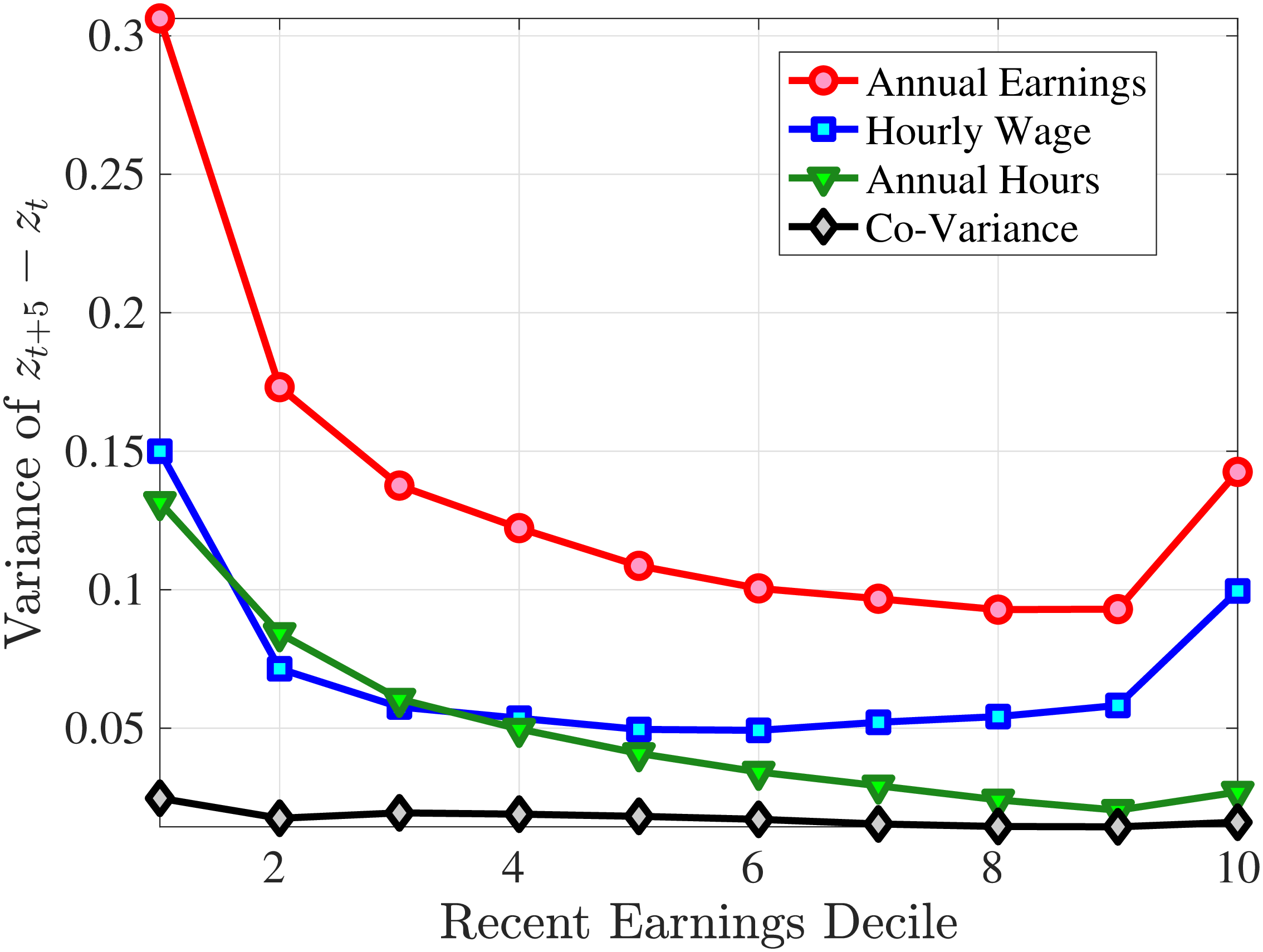

Second Moment: Variance

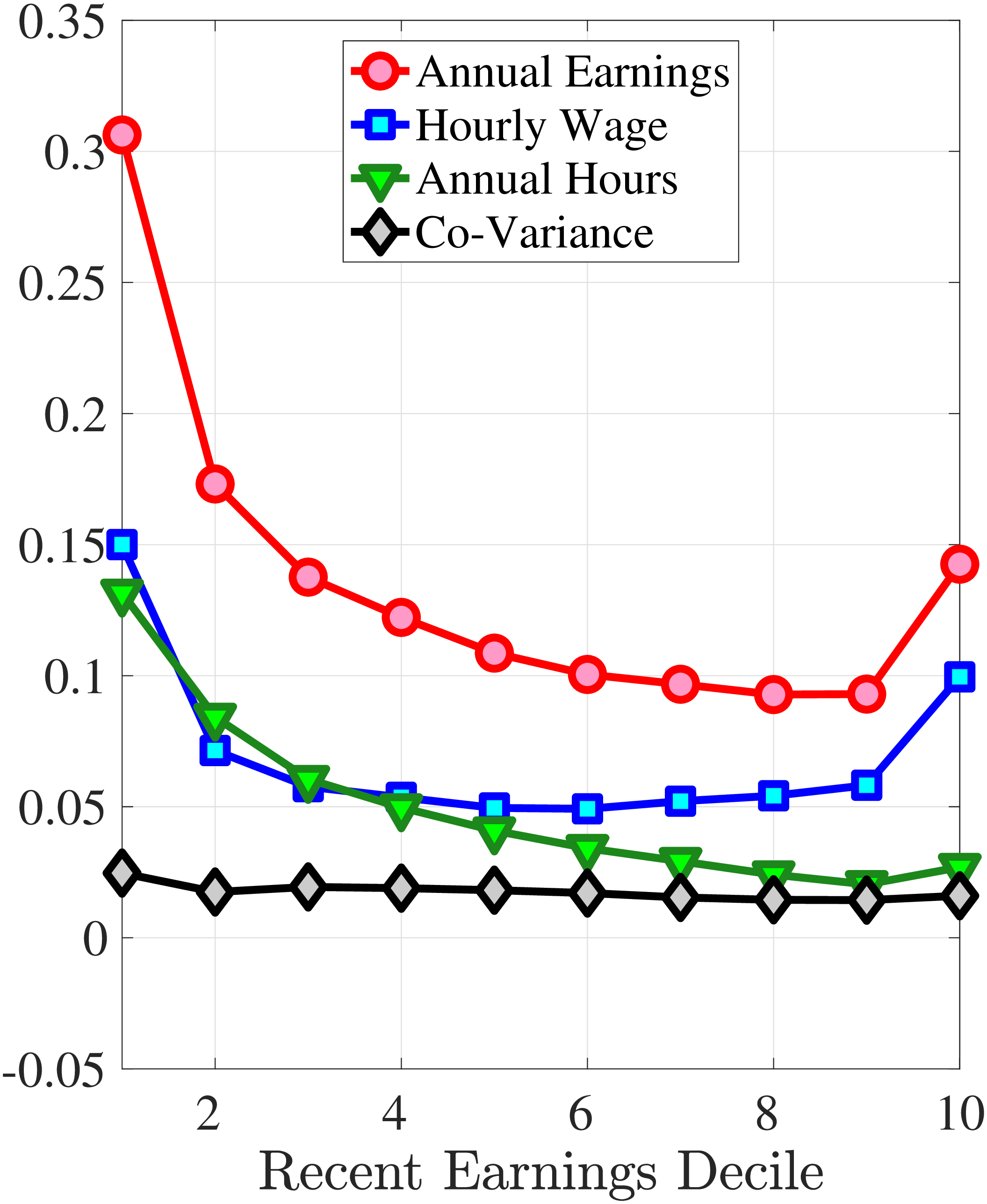

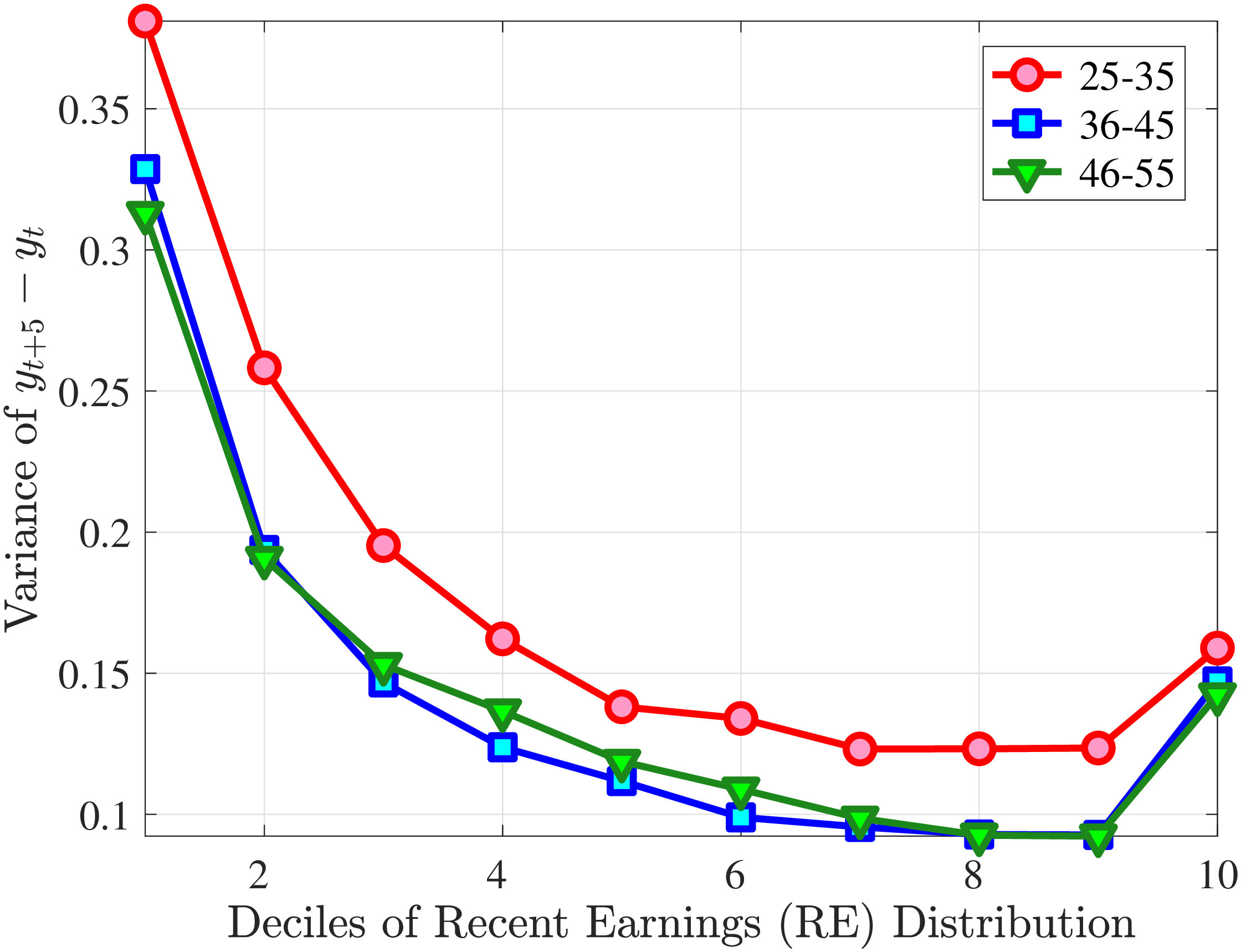

Figure 8 shows the variance of changes in hourly wage rates (panel A) and hours (panel B) over the life cycle and across the recent earnings distribution. Panel C documents the decomposition of the variance of earnings changes into hours changes and hourly wage changes along with their covariance. The way the variance of both the wage rate and hours changes vary with age and recent earnings are qualitatively similar to those of annual earnings growth (panel C in Figure 8) in that the volatility of both hours and wage rate changes is falling with age. Moreover, lower-income workers tend to face a more dispersed distribution of wage rate and hours growth relative to higher-income workers. However, for recent income above the median, the patterns differ for hours versus hourly wages: the variance of changes in hours worked is monotonically falling in recent income, whereas the variance of wage rate growth is U-shaped in recent earnings, weakly increasing for groups with RE above the median. This suggests that the increasing part of the U-shaped profile of the variance of earnings growth across RE groups in Figure 7 is a result of wage rate growth becoming more volatile for the top earners. This is consistent with the view of, for example, Parker and Vissing-Jo rgensen (2010), who argue that the earnings volatility of high earners is affected by a performance-based compensation structure such as bonuses and stock options.

For workers below the median recent earnings, changes in hours and changes in wage rates are approximately equally volatile, whereas for workers at or above the median recent earnings, wage rates are more volatile than hours. The relatively volatile hours worked for poor workers might reflect that unemployment shocks are more relevant for this group. That wage rates are, broadly speaking, more volatile than hours is consistent with Heathcote et al. (2014), who document that changes in wage rates are slightly larger than changes in hours worked in the PSID. It is also consistent with the evidence from Section 4.1 that earnings changes for high earners tend to be driven by changes in wage rates rather than hours.

(a) Variance \(\Delta _{\log}^{5}w_{t}^{i}\)

(a) Variance \(\Delta _{\log}^{5}w_{t}^{i}\)  (b) Variance \(\Delta _{\log}^{5}h_{t}^{i}\)

(b) Variance \(\Delta _{\log}^{5}h_{t}^{i}\)  (c) Decomposing \(Var(\Delta _{\log}^{5}y_{t}^{i})\)

(c) Decomposing \(Var(\Delta _{\log}^{5}y_{t}^{i})\)

Figure 8

–

Variance of Five-Year Log Hourly Wage and Hours Growth

Note: The figure plots the variances of five-year wage rate changes (pane A) and hours changes (panel B) by RE decile for young men (red line) and prime-age men (blue line). Panel C shows a decomposition of the variance of earnings changes into changes in hours, hourly wages, and their covariance for prime-age men (36-55 years old).

Figure: Figure 8 – Variance of Five-Year Log Hourly Wage and Hours Growth

Panel C in Figure 8 illustrates that the variance of five-year earnings growth for prime-age workers is higher than the variance of both hours growth and wage growth (see Appendix B.4 for a similar decomposition for young workers). Note that the covariance between hours growth and wage rate growth is small but positive. This positive co-movement is in line with our findings in Section 4.1. This is an important result for two reasons. First, a positive correlation between changes in hours and hourly wage rates tends to mitigate the welfare costs of (an exogenous) volatility of hourly wages. The reason is that if the correlation between changes in wage rates and changes in hours is positive, hourly wage rate changes tend to increase average productivity and average wages (see Heathcote et al. (2009) for an analysis of the aggregate welfare effects of wage rate volatility when labor supply is endogenous). In contrast, Heathcote et al. (2014) document that for U.S. workers (based on data from from PSID), hours changes and wage rate changes are negatively correlated. Second, wage-hours correlation is informative about the presence of m.e. in our imputed hours. Recall that we measure hourly wages as earnings divided by imputed hours. Classical m.e. in imputed hours will therefore give rise to a division bias lowering the measured covariance between hourly wages and hours.30 The fact that we find a positive correlation between imputed hours changes and wage rate changes suggests that m.e. in our imputation of hours worked must be of minor magnitude.

Higher-order moment decomposition. The skewness and kurtosis of earnings growth can be decomposed into hours and wage components as shown in the following lemma.

Lemma 1. If x and y are two random variables, then

\[ \begin{aligned} \text{skew}\left (x+y\right) &= \left (\frac{std\left (x\right)}{std\left (x+y\right)}\right)^{3}\cdot \text{skew}\left (x\right)+\left (\frac{std\left (y\right)}{std\left (x+y\right)}\right)^{3}\cdot \text{skew}\left (y\right)\\ &\quad + \underbrace{\frac{3}{\left (std\left (x+y\right)\right)^{3}}\left (cov\left (x^{2},y\right)+cov\left (x,y^{2}\right)-2\left (E\{y\}+E\{x\}\right)\cdot cov\left (x,y\right)\right)}_{\text{co-skewness terms}} \end{aligned} \]

\[ \begin{aligned} \text{kurt}\left (x+y\right) &= \left (\frac{var\left (x\right)}{var\left (x+y\right)}\right)^{2}\text{kurt}\left (x\right)+\left (\frac{var\left (y\right)}{var\left (x+y\right)}\right)^{2}\text{kurt}\left (y\right)\\ & \underbrace{\begin{array}{cc} + & \frac{4}{\left (var\left (x+y\right)\right)^{2}}\left [E\left \{\left [x-E\left (x\right)\right]^{3}\left [y-E\left (y\right)\right]\right \} +E\left \{\left [x-E\left (x\right)\right]\left [y-E\left (y\right)\right]^{3}\right \} \right]\\ + & \frac{6}{\left (var\left (x+y\right)\right)^{2}}E\left \{\left [x-E\left (x\right)\right]^{2}\left [y-E\left (y\right)\right]^{2}\right \} \end{array}}_{\text{co-kurtosis terms}} \end{aligned} \]

See Appendix A for the derivation.

This lemma shows that the skewness (kurtosis) of the sum of two random variables is equal to the weighted sum of skewness (kurtosis) of individual variables plus some co-skewness (co-kurtosis) terms. The weights are determined by the ratio of the variance of individual variables to the variance of the sum. Thus, the more volatile variable will account for a larger share of the moments for the sum of the variables. A negative (positive) co-skewness indicates that both variables tend to undergo extreme negative (positive) deviations at the same time. Similarly, if two random variables exhibit a high level of co-kurtosis, they tend to undergo extreme deviations concurrently.

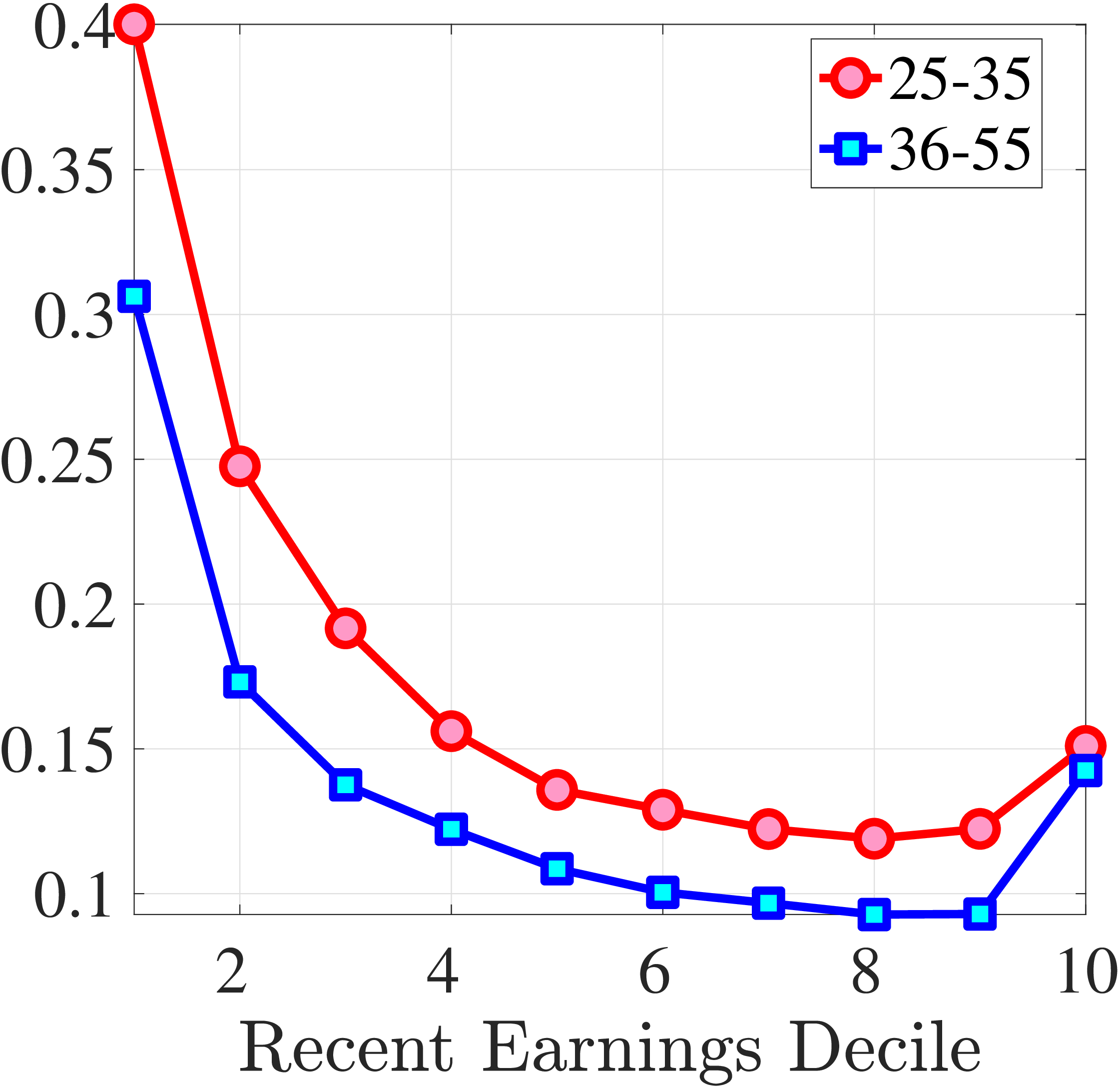

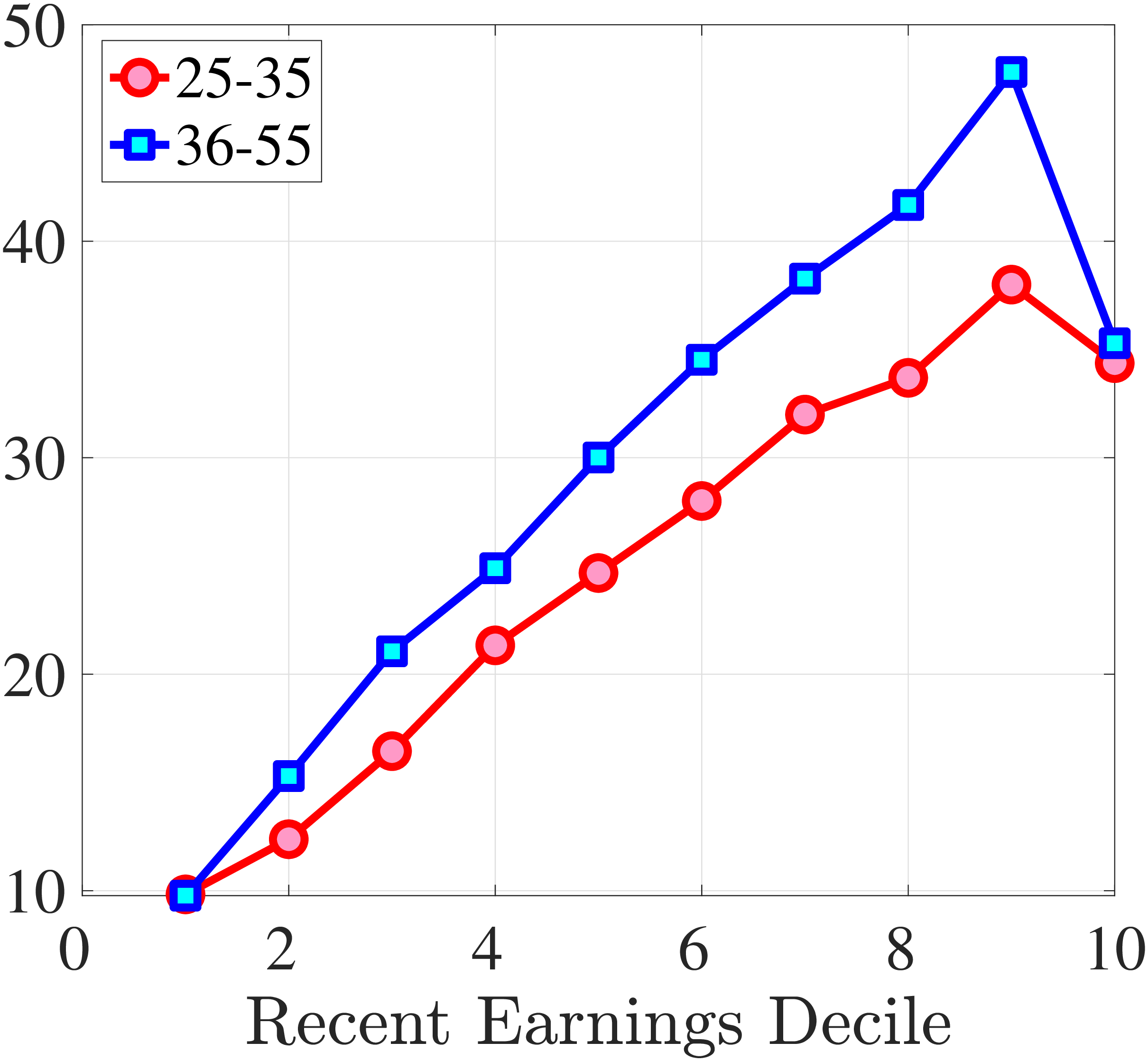

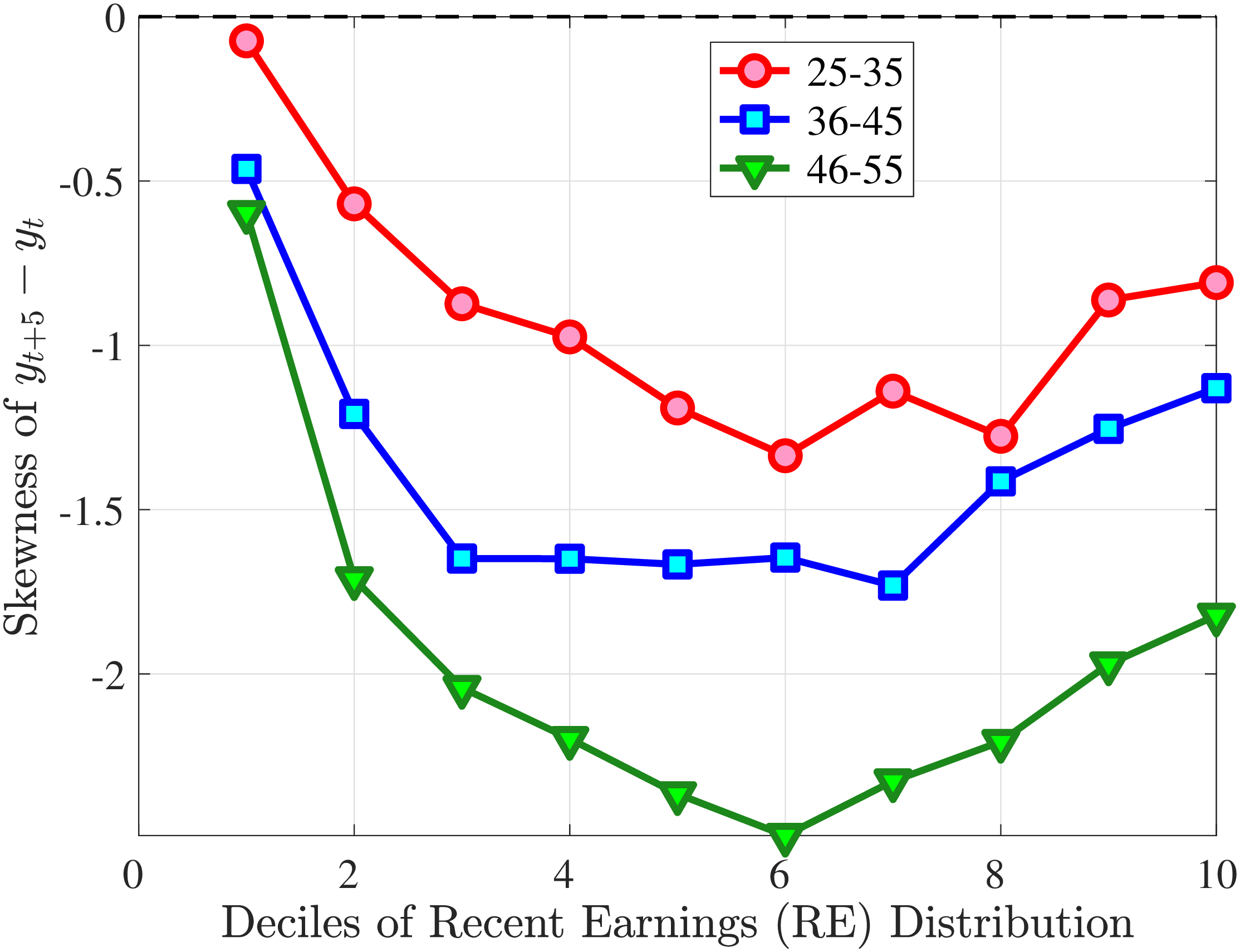

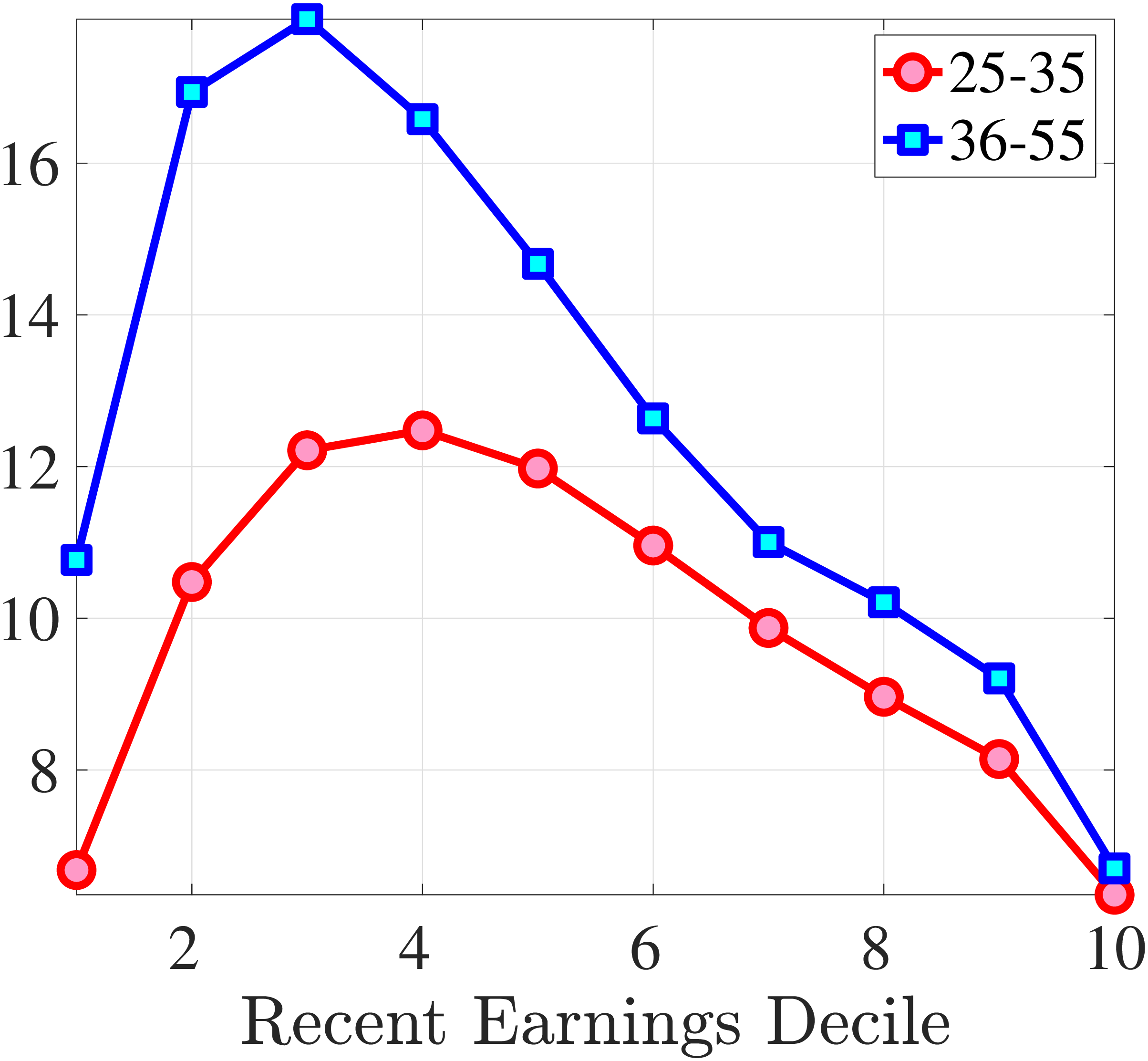

Third Moment: Skewness

Figure 9 documents the third moment of hours and wage rate growth. Again, the age and income variations in their skewness of five-year changes are qualitatively similar to those of annual earnings growth in Figure 7. First, the skewness of hours and wage rates follow a U-shaped pattern over the RE distribution, with middle RE workers facing a more left-skewed distribution of five-year wage and hours changes. Second, the distributions of five-year growth in both wage rates and hours are more left (negatively) skewed for prime-age workers relative to younger workers. Note that hours changes are more negatively skewed than wage rate changes.

(a) Skewness of Hourly Wage Changes, \(\Delta _{\log}^{5}w_{t}^{i}\)

(a) Skewness of Hourly Wage Changes, \(\Delta _{\log}^{5}w_{t}^{i}\)  (b) Skewness of Hours Changes, \(\Delta _{\log}^{5}h_{t}^{i}\)

(b) Skewness of Hours Changes, \(\Delta _{\log}^{5}h_{t}^{i}\)

Figure 9

–

Skewness of Five-Year Log Hourly Wage and Hours Growth

Note: The figure plots the skewness of five-year wage rate changes (left panel) and hours changes (right panel) by RE decile for young men (red line) and prime-age men (blue line).

Figure: Figure 9 – Skewness of Five-Year Log Hourly Wage and Hours Growth

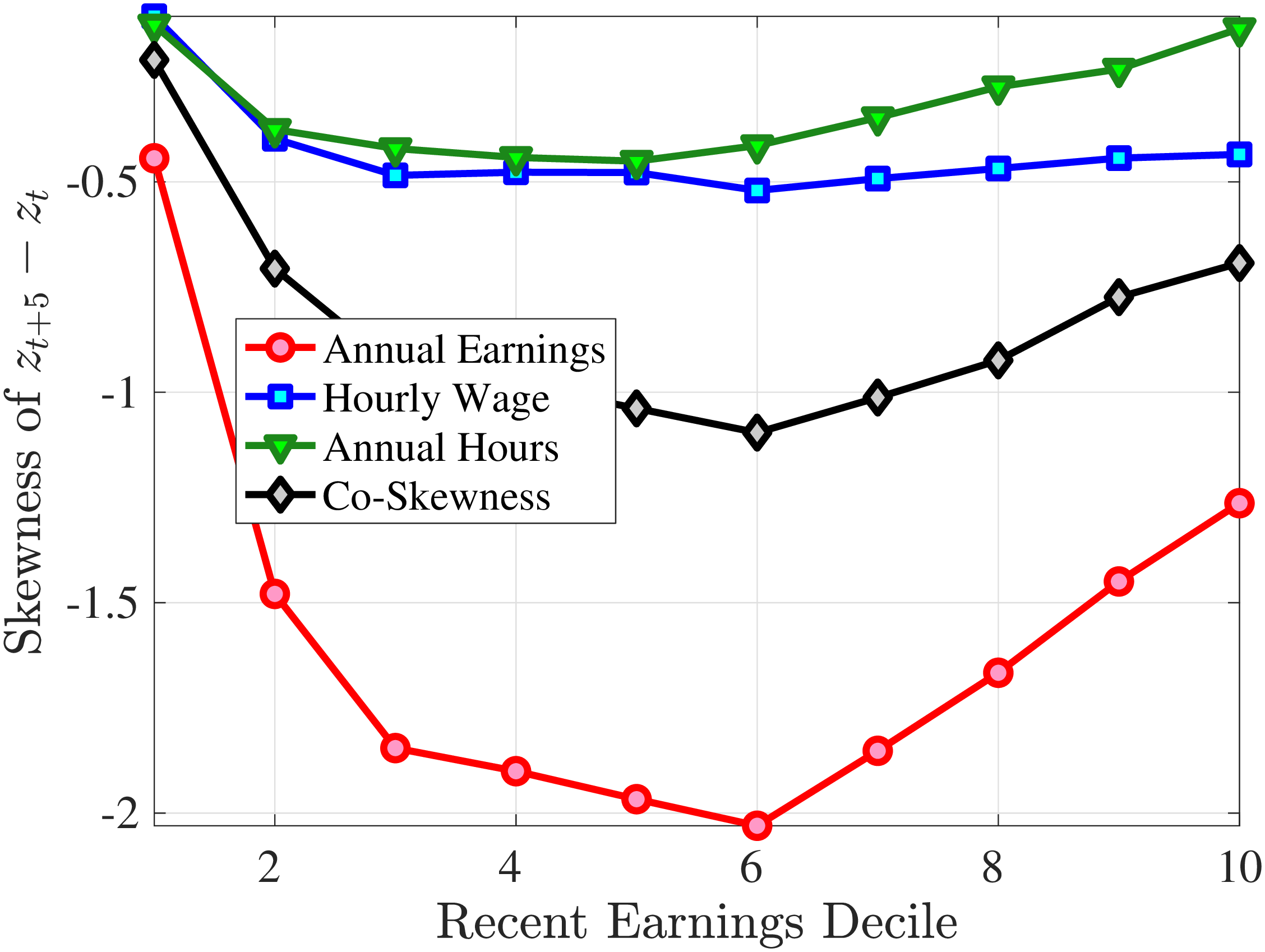

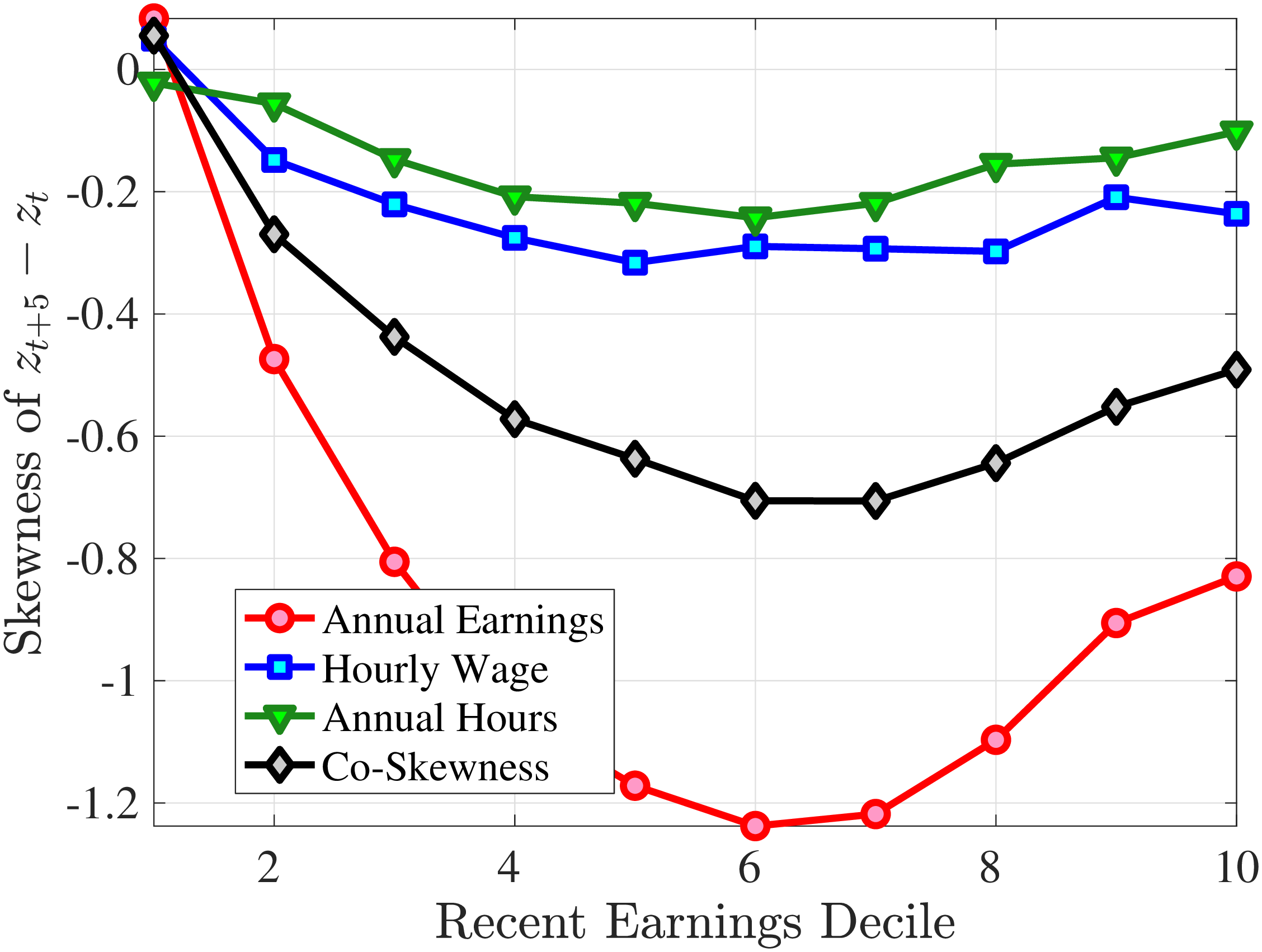

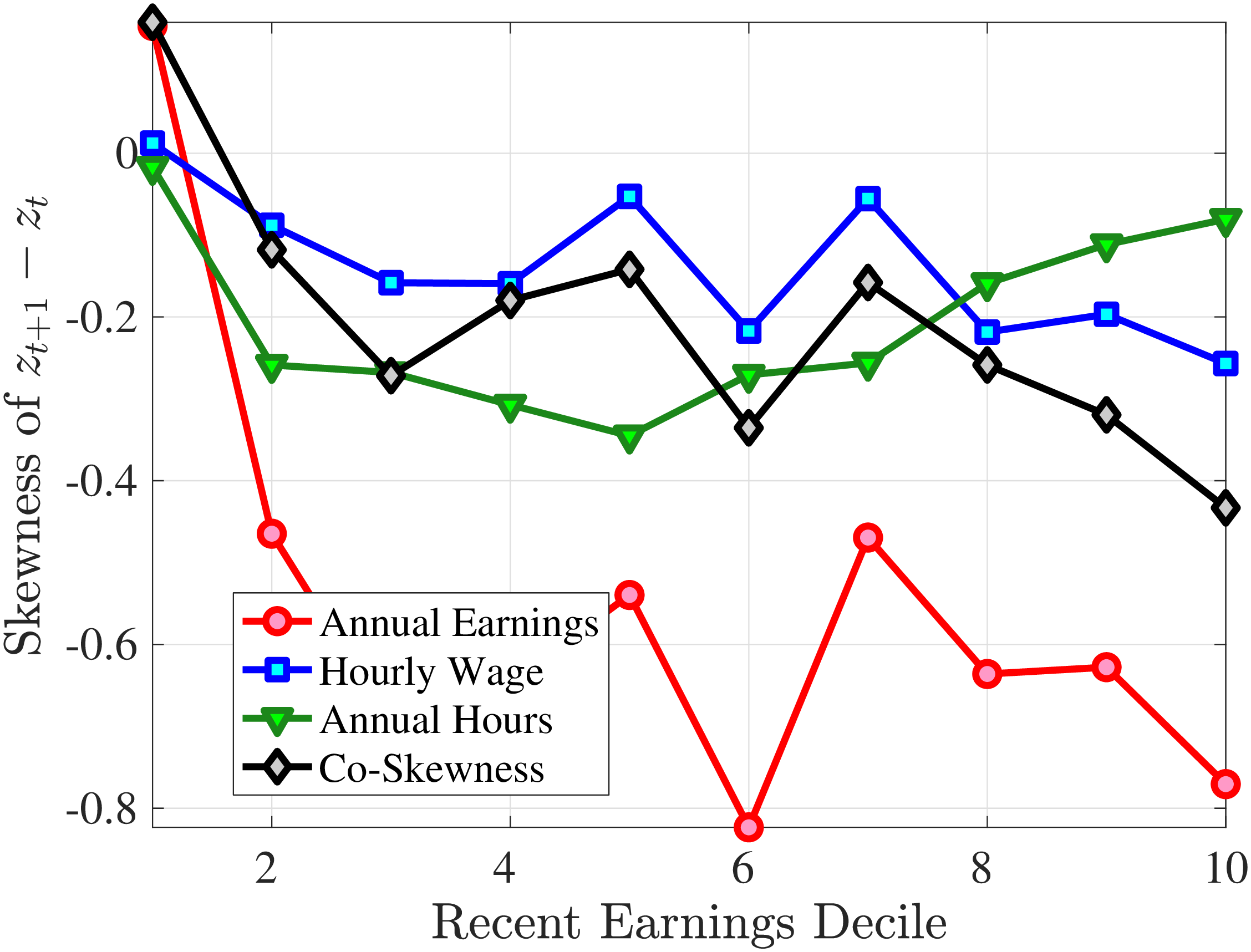

We next decompose the skewness of the earnings growth distribution into hours and wage growth components as well as the co-skewness term as defined in Lemma 1 (the left panel of Figure 10). Recall that hours and wage growth contribute to the skewness of earnings growth according to the ratio of their variance to the variance of earnings growth. Thus, even though hours growth is more left skewed than wage rate growth, the fact that wage rate growth is more volatile implies that it accounts for a larger share of the left skewness of earnings growth, especially for groups with RE above the median. More importantly, the main driver of the left skewness of the earnings changes are the co-skewness terms. This component captures the fact that hours and wages tend to undergo large negative changes simultaneously, in line with the evidence in Figures 2 and 3. Thus, when workers experience large hours cuts, they also see their wages decline sharply. This finding is consistent with the literature studying the labor market dynamics associated with unemployment, where large initial declines in hours are associated with large and persistent declines in earnings (e.g., Jacobson et al. (1993); Von Wachter et al. (2009), and Huttunen et al. (2011) for Norway). However, our results from Section 4.2.1 suggest that the scarring effect of unemployment takes the form of an initial fall in hours and wage rates, followed by almost full recovery in hours but little recovery in wage rates.

(a) Skewness

(a) Skewness (b) Kurtosis

(b) Kurtosis

Figure 10

–

Decomposition of Skewness and Kurtosis of Five-Year Log Earnings Growth

Note: The figure plots a decomposition of skewness (left panel) and kurtosis (right panel) of five-year log earnings changes (red line) for prime-age men into the skewness/kurtosis of log wage changes (blue line), the skewness/kurtosis of log hours changes (green line), and the co-skewness/co-kurtosis between log wage and log hours changes (black line). Each dot represents a decile of RE. The decomposition is based on Lemma 1.

Figure: Figure 10 – Decomposition of Skewness and Kurtosis of Five-Year Log Earnings Growth

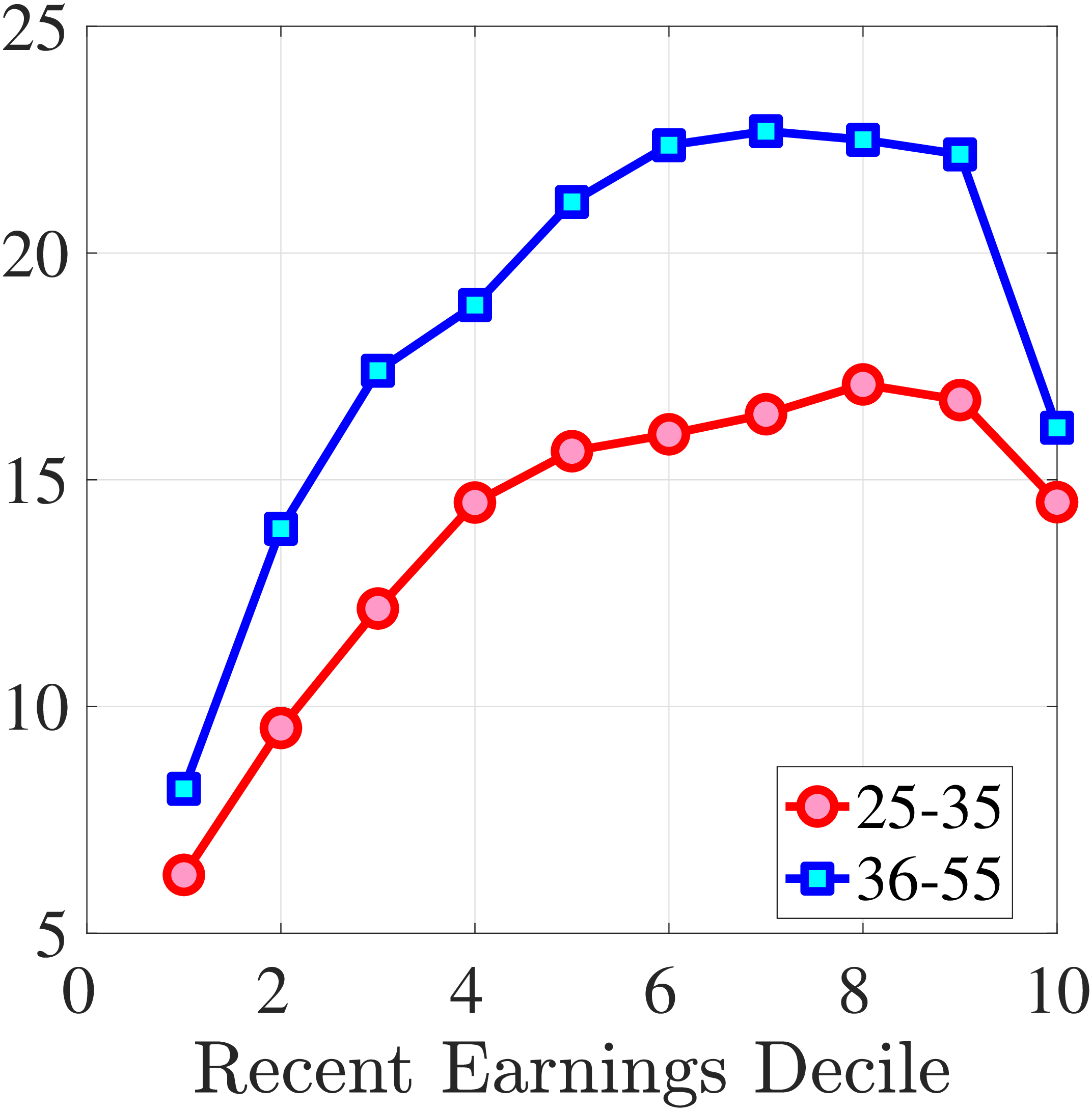

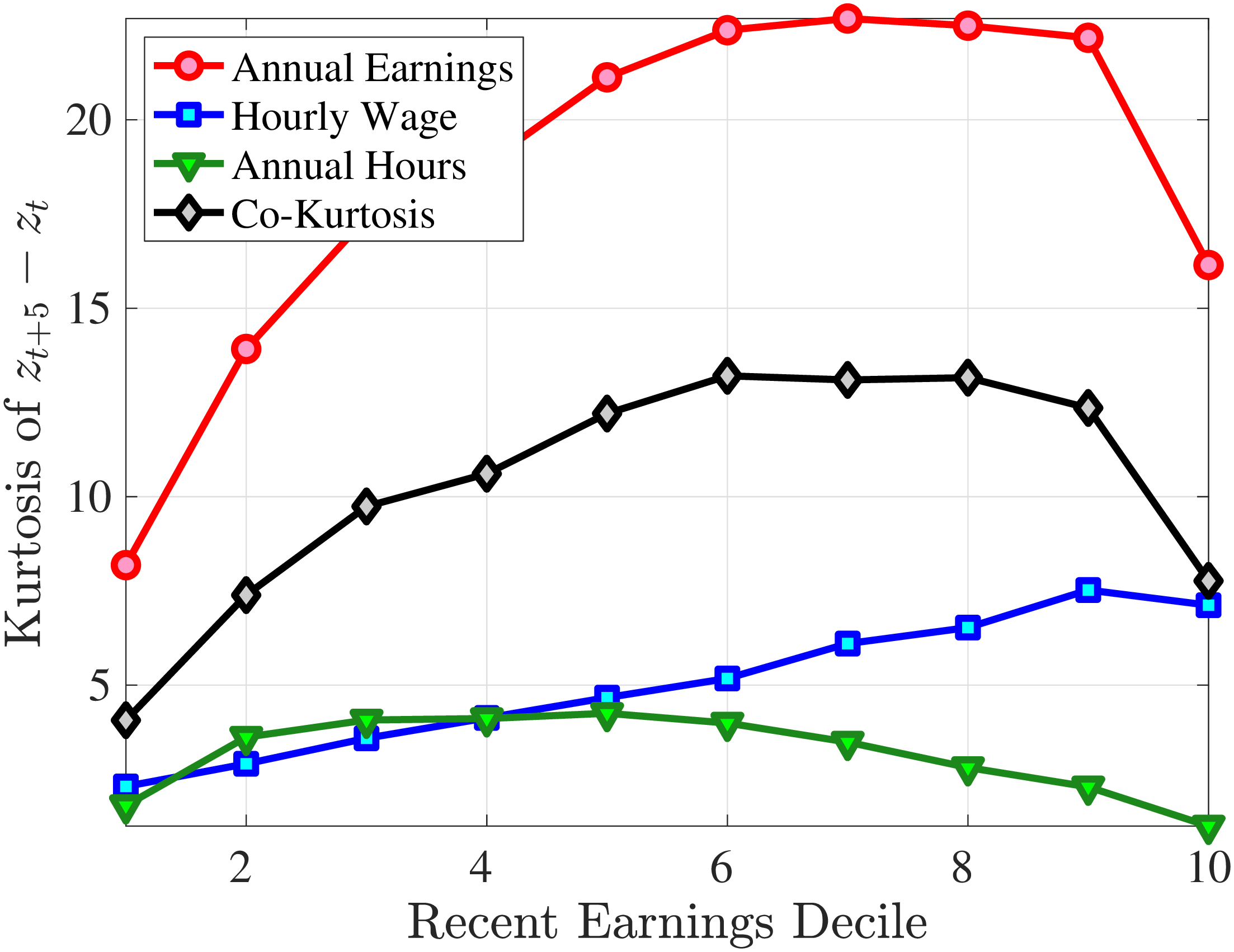

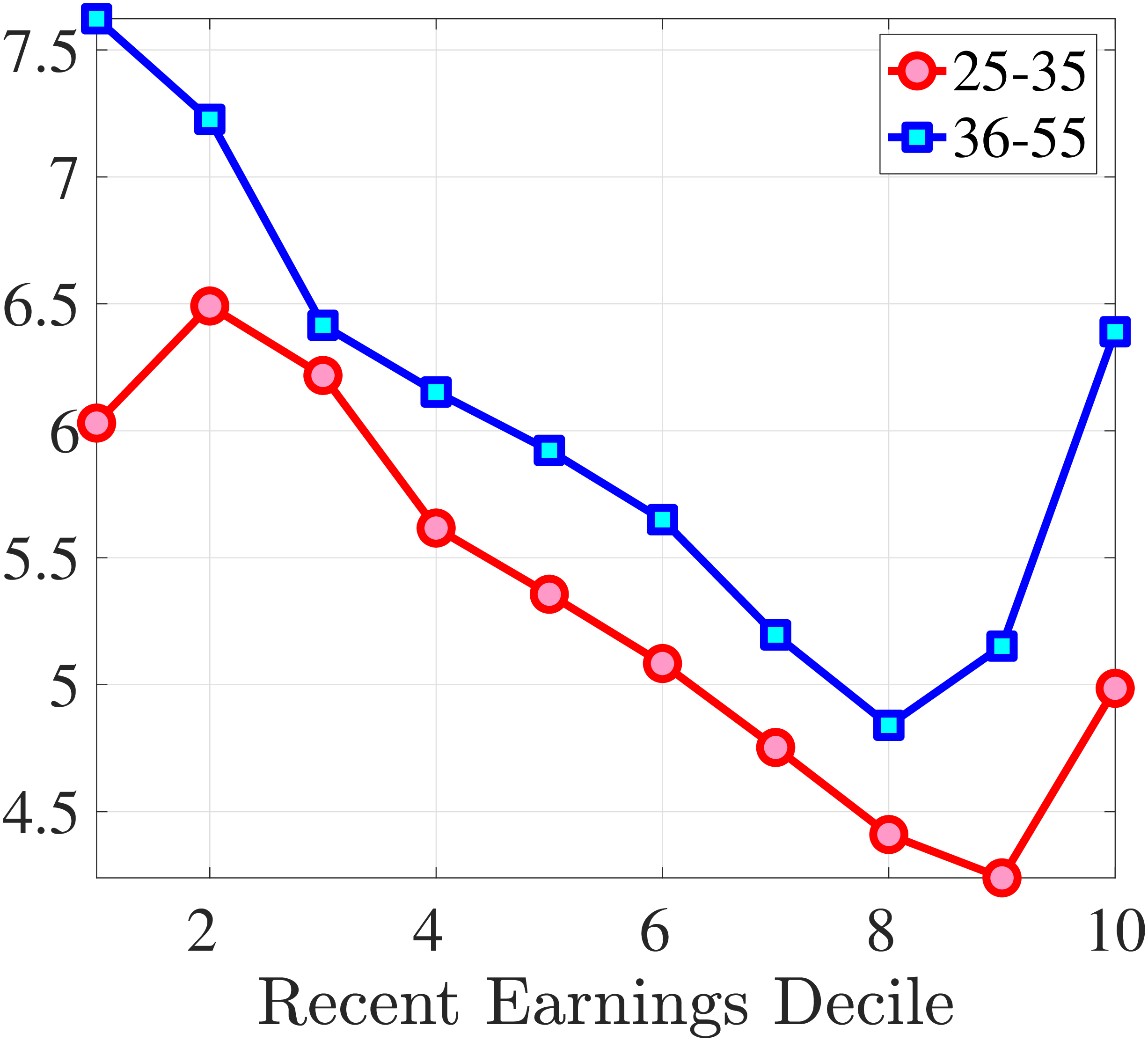

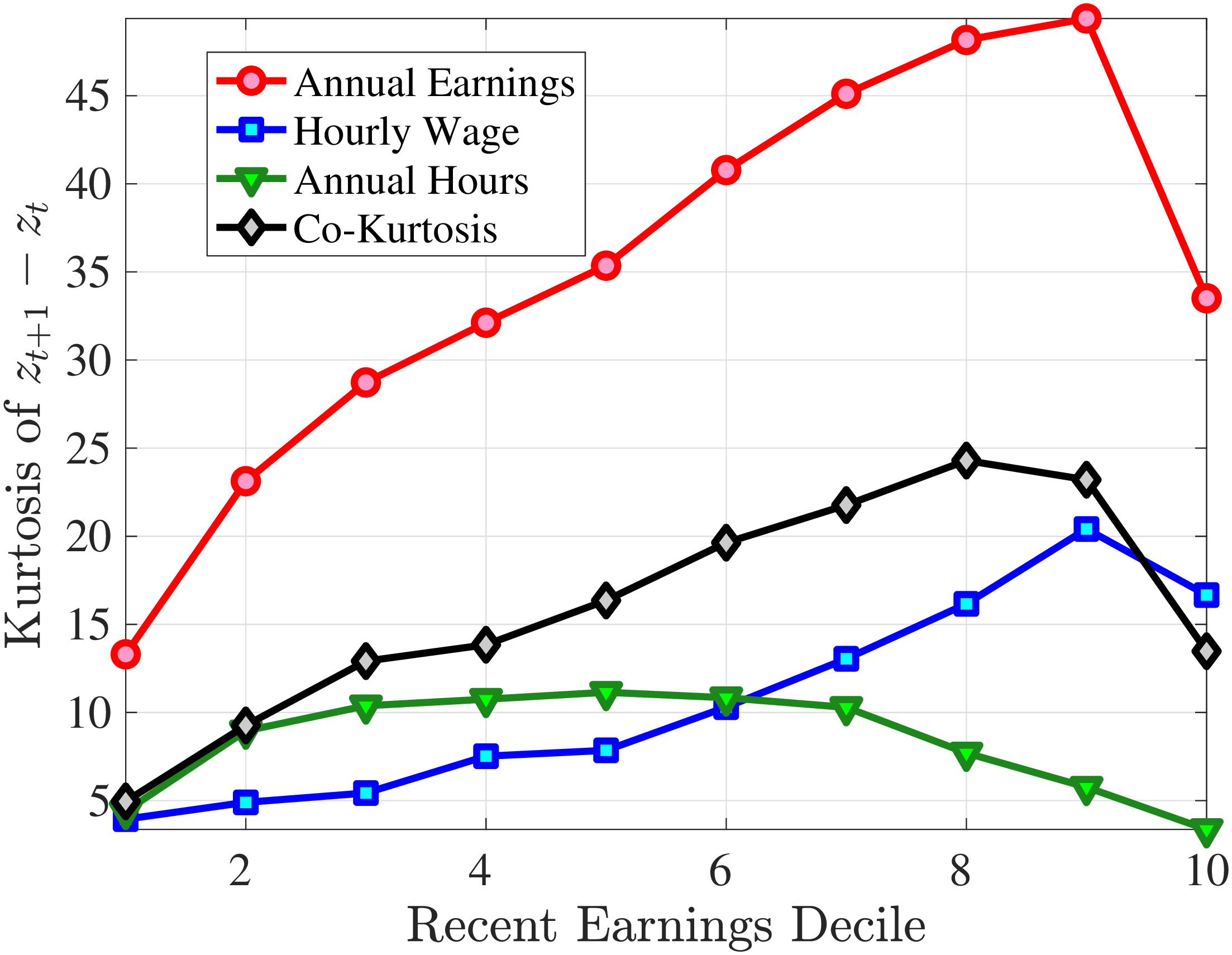

Fourth Moment: Kurtosis

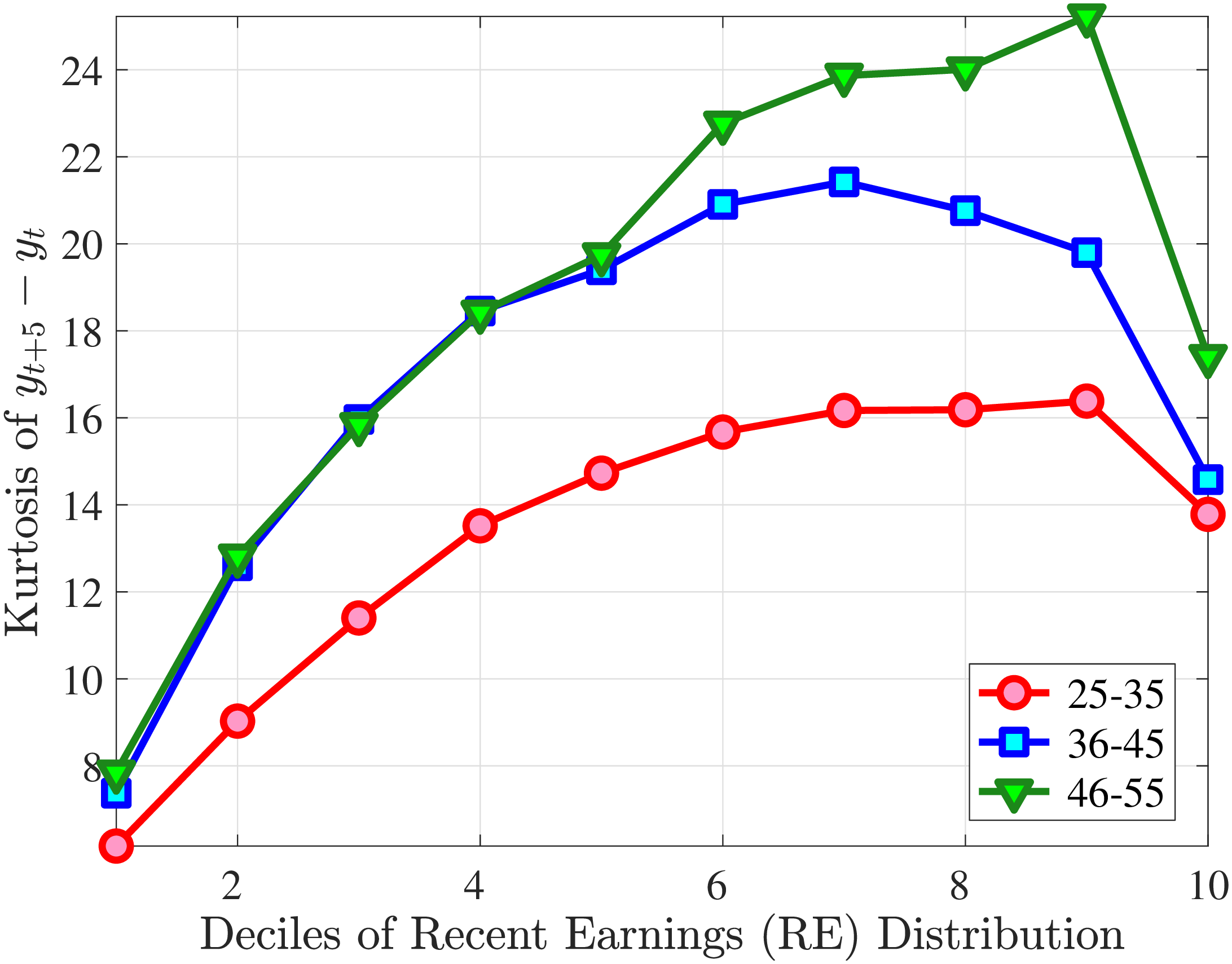

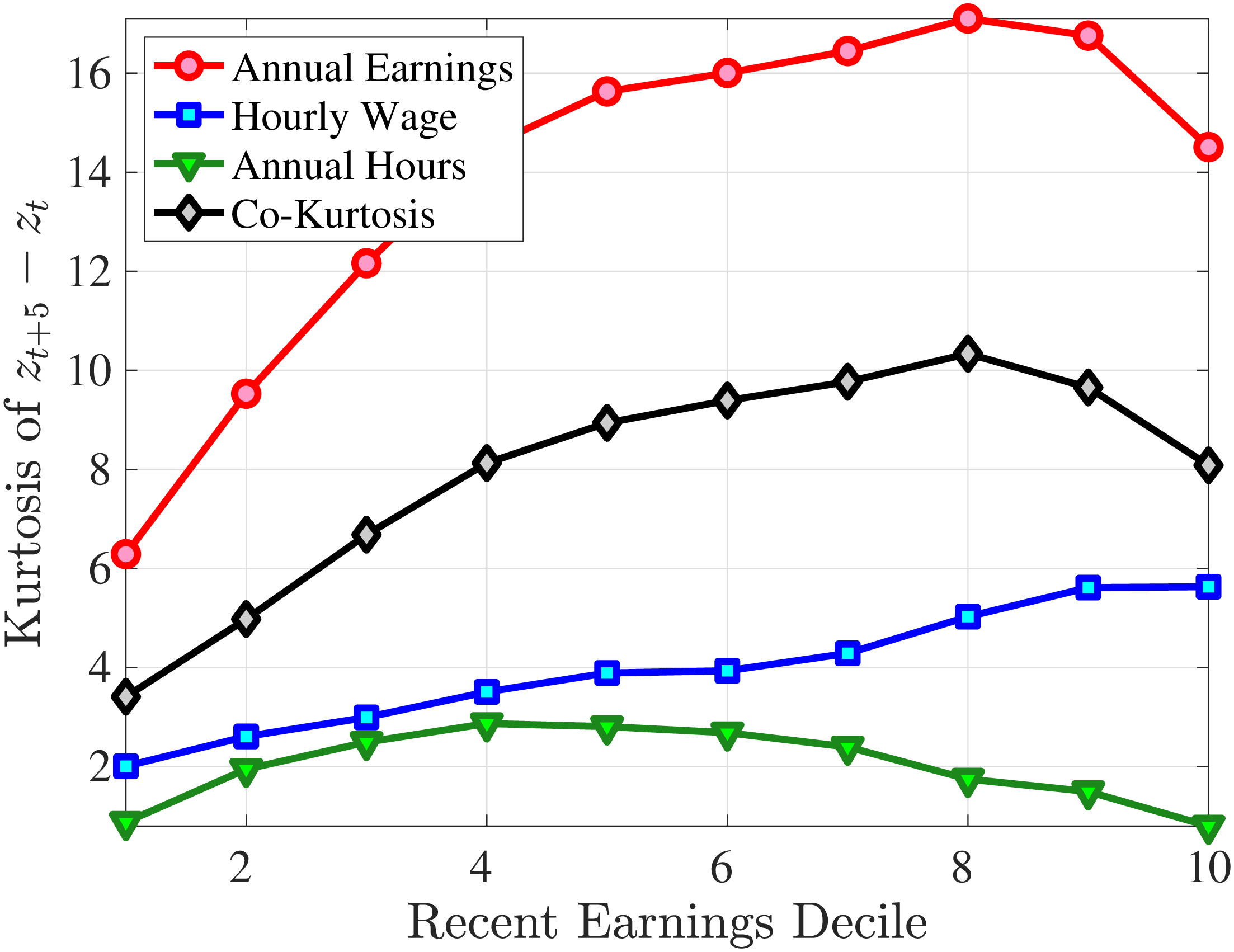

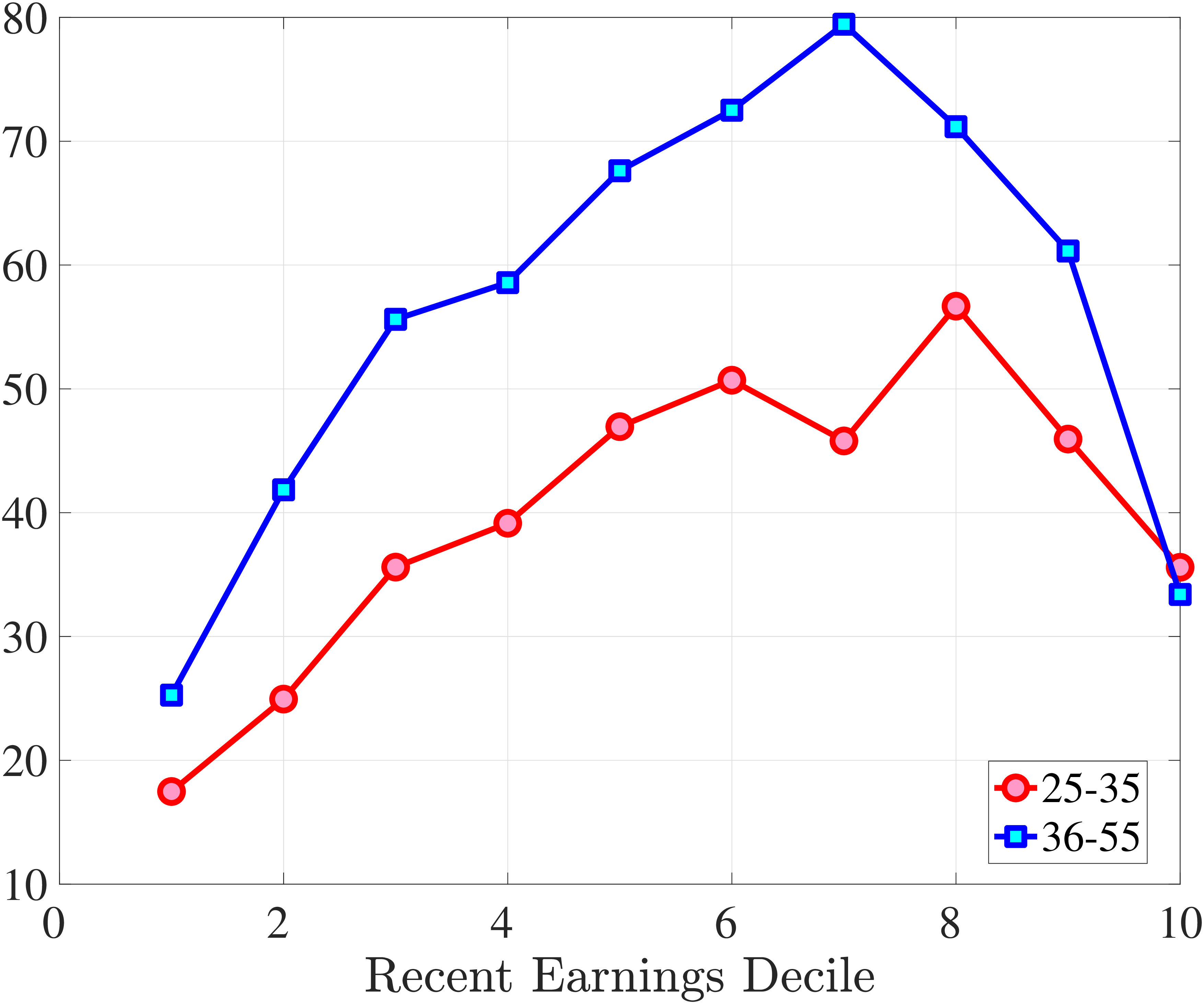

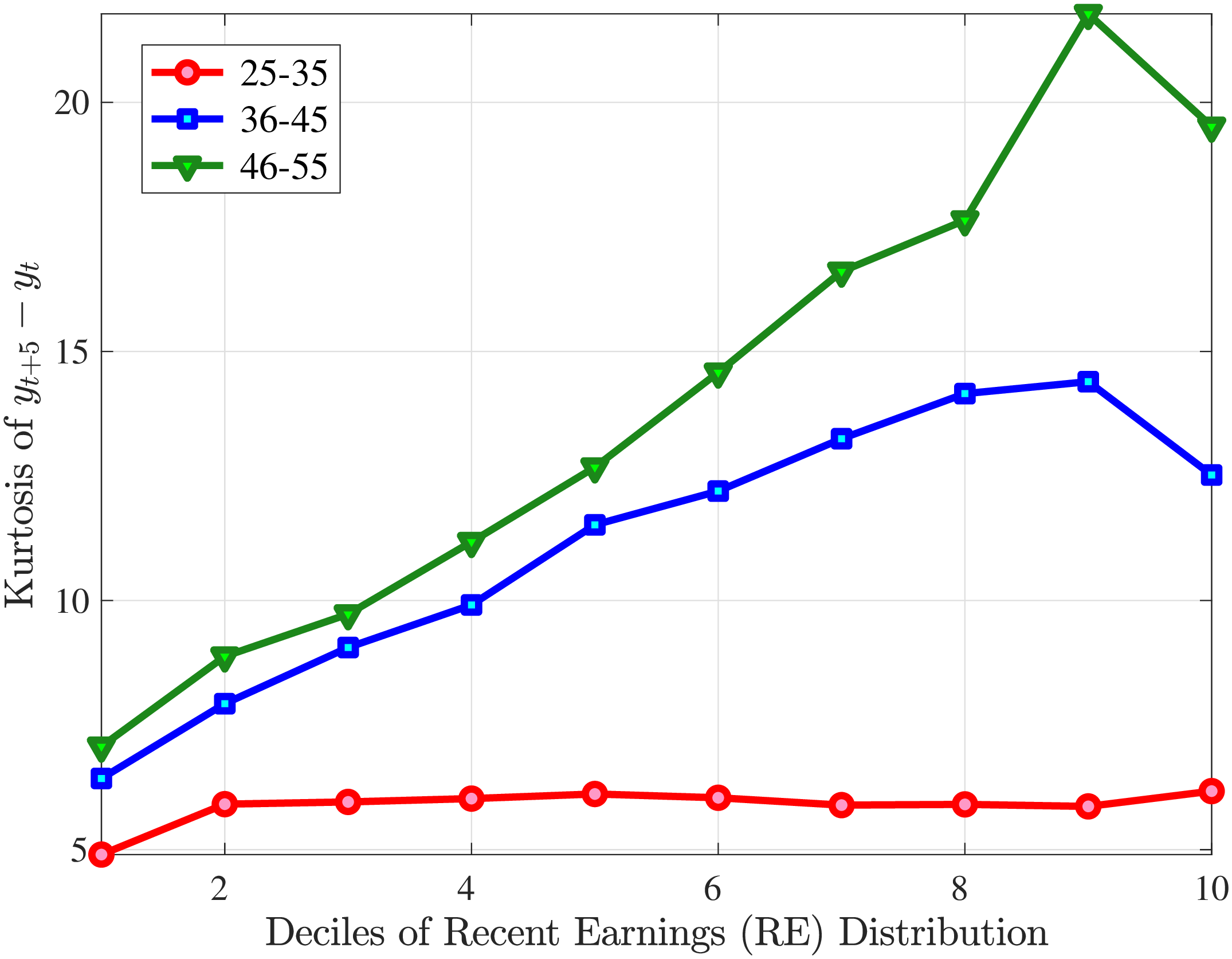

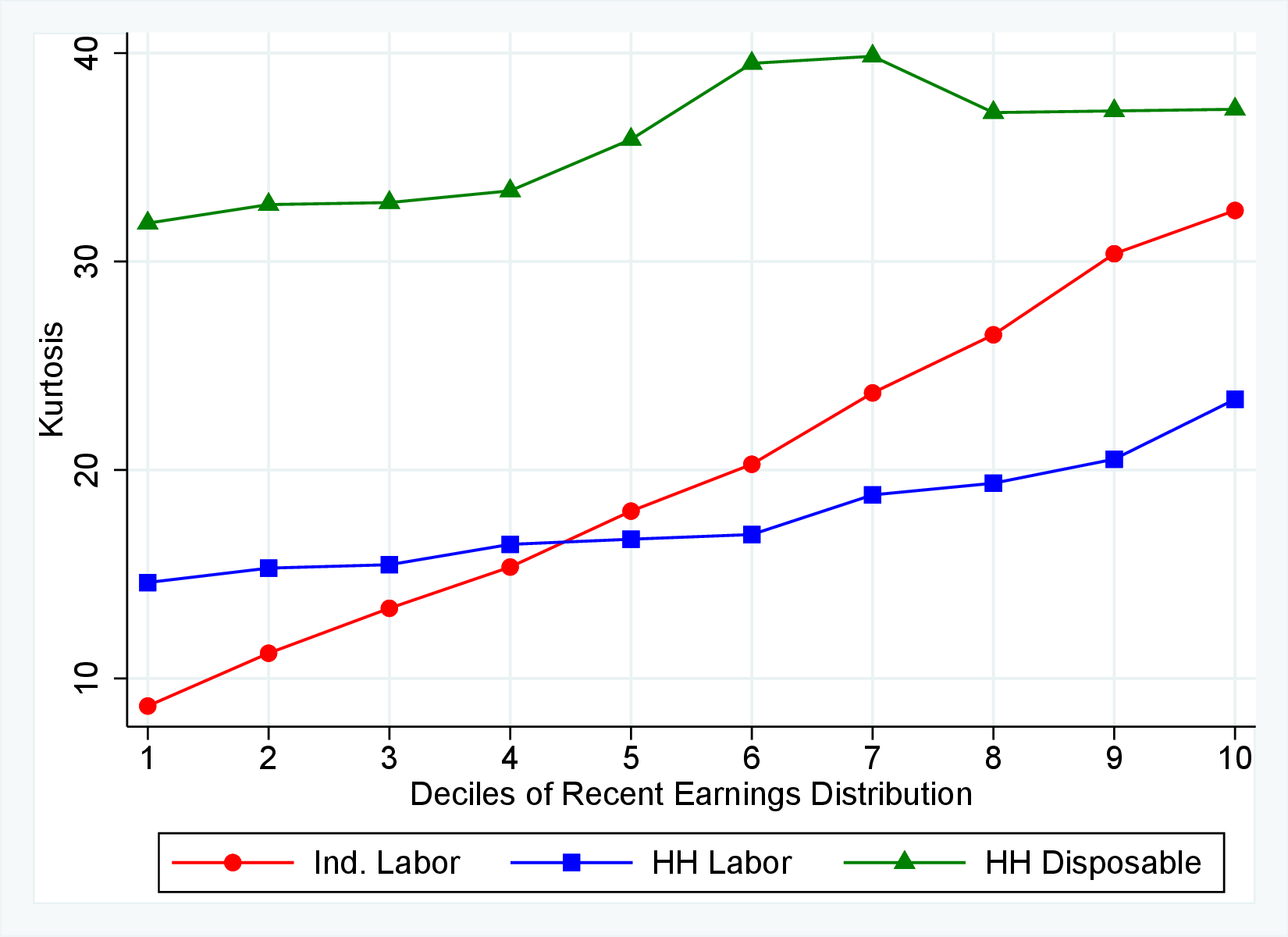

Finally, Figure 11 shows the income and age profiles of the fourth standardized moment of five-year wage (left panel) and hours growth (right panel). Both variables display very large excess kurtosis. The kurtosis of wage rate changes and how it varies with age and recent earnings groups are very similar to those of earnings growth (Figure 7). The kurtosis of hours growth is significantly higher than the kurtosis of wage and earnings growth. Thus, hours changes are less frequent but more extreme, so when they change, the changes are large. Furthermore, the kurtosis of hours changes also displays an increasing profile over the RE distribution, compared to a hump-shaped profile for the kurtosis of wage changes. As for the age variation, older workers are facing more leptokurtic hours, and their wage growth distributions are similar to the distribution of earnings changes. These features of hours changes are broadly consistent with transitions into or out of unemployment or part-time work for prime-age male workers. Such flows feature infrequent but large changes in hours, especially, for those at the higher end of the RE distribution.

(a) Kurtosis of Hourly Wage Changes, \(\Delta _{\log}^{5}w_{t}^{i}\)

(a) Kurtosis of Hourly Wage Changes, \(\Delta _{\log}^{5}w_{t}^{i}\)  (b) Kurtosis of Hours Changes, \(\Delta _{\log}^{5}h_{t}^{i}\)

(b) Kurtosis of Hours Changes, \(\Delta _{\log}^{5}h_{t}^{i}\)

Figure 11

–

Kurtosis of Five-Year Log Hourly Wage and Hours Growth

Note: The figure plots the kurtosis of five-year wage rate changes (left panel) and hours changes (right panel) by RE decile for young men (red line) and prime-age men (blue line).

Figure: Figure 11 – Kurtosis of Five-Year Log Hourly Wage and Hours Growth

The right panel of Figure 10 decomposes the kurtosis of five-year earnings growth into the contributions from changes in work hours, changes in hourly wages, and the co-kurtosis term using Lemma 1. Up to the median RE, both the wage rate and the hours changes contribute equally to the kurtosis of earnings growth. For higher RE deciles, wage rate growth becomes more important in accounting for the kurtosis of earnings changes, partly because wage changes are larger for these workers. However, the dominant driver of earnings kurtosis tends to be the co-kurtosis terms (except for the top RE groups). Recall that these terms are large if hours and wages tend to undergo large changes concurrently.

Taking Stock. In this section, we have shown that both hours and wage changes are negatively skewed and highly leptokurtic. Both hours and wage rates contribute to the higher-order moments of log earnings growth. However, the main culprit for the large negative skewness and large kurtosis of earnings growth turns out to be the co-skewness and co-kurtosis terms, respectively. Thus, earnings growth is negatively skewed and leptokurtic mainly because of the interaction between hours and wage rate changes. Note that this conclusion may depend on the severity of m.e.. In Appendix A.2, we show that the presence of classical m.e. would bias the estimates of the skewness and kurtosis towrad zero relative to the true skewness and kurtosis of an empirical variable. In this context it is of significant importance that the m.e. in imputed hours is quantitatively small, as argued above.

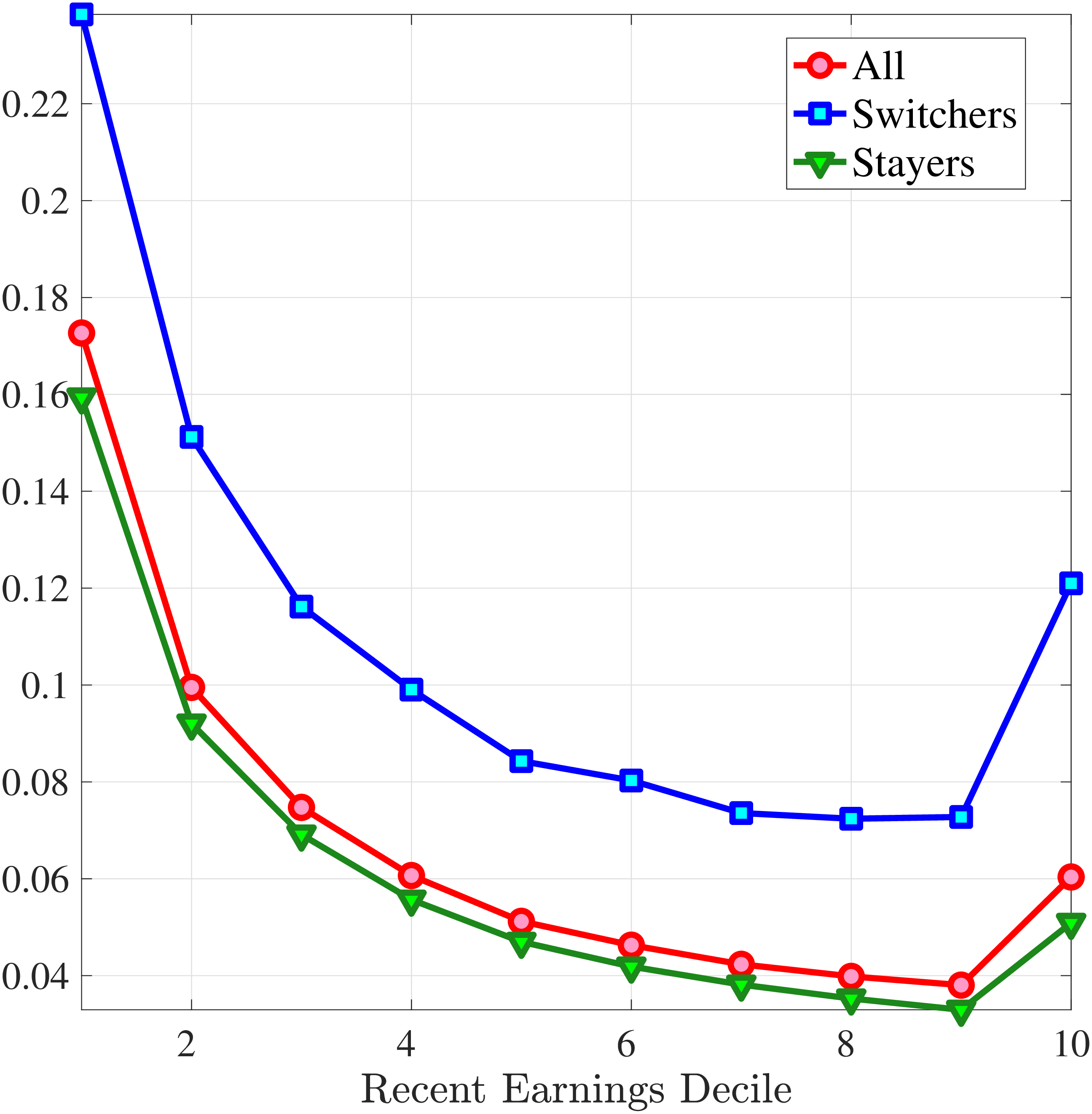

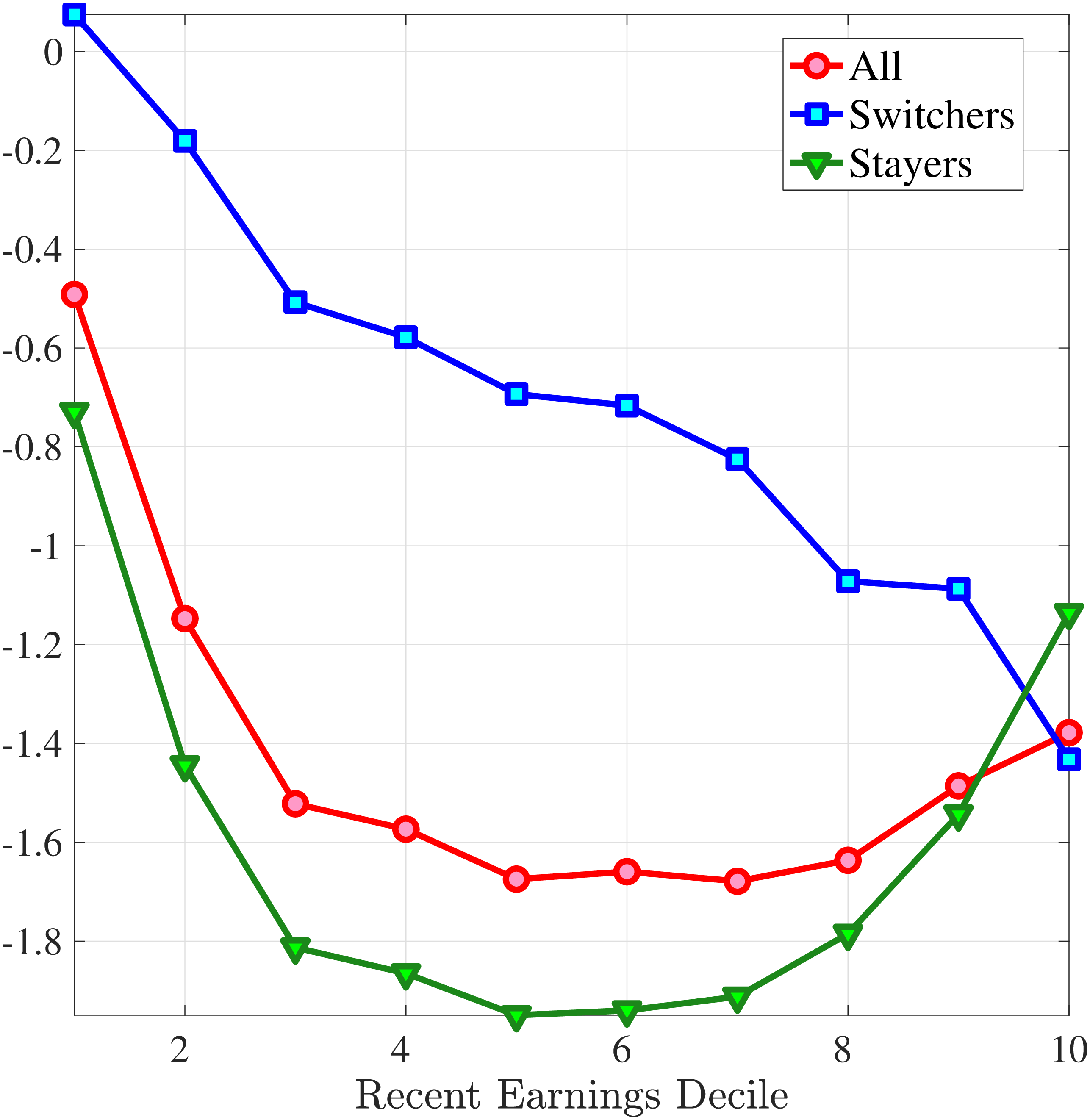

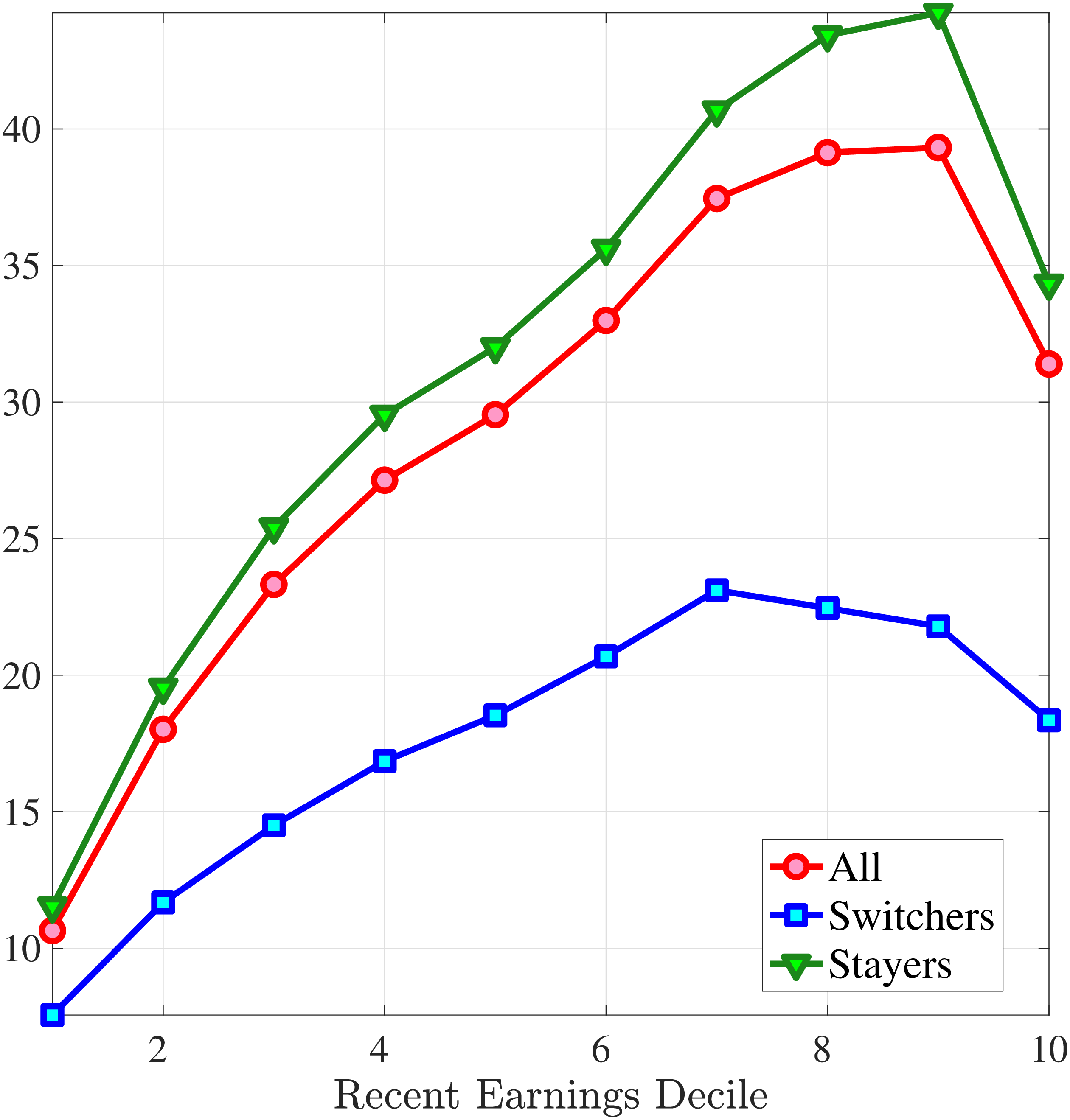

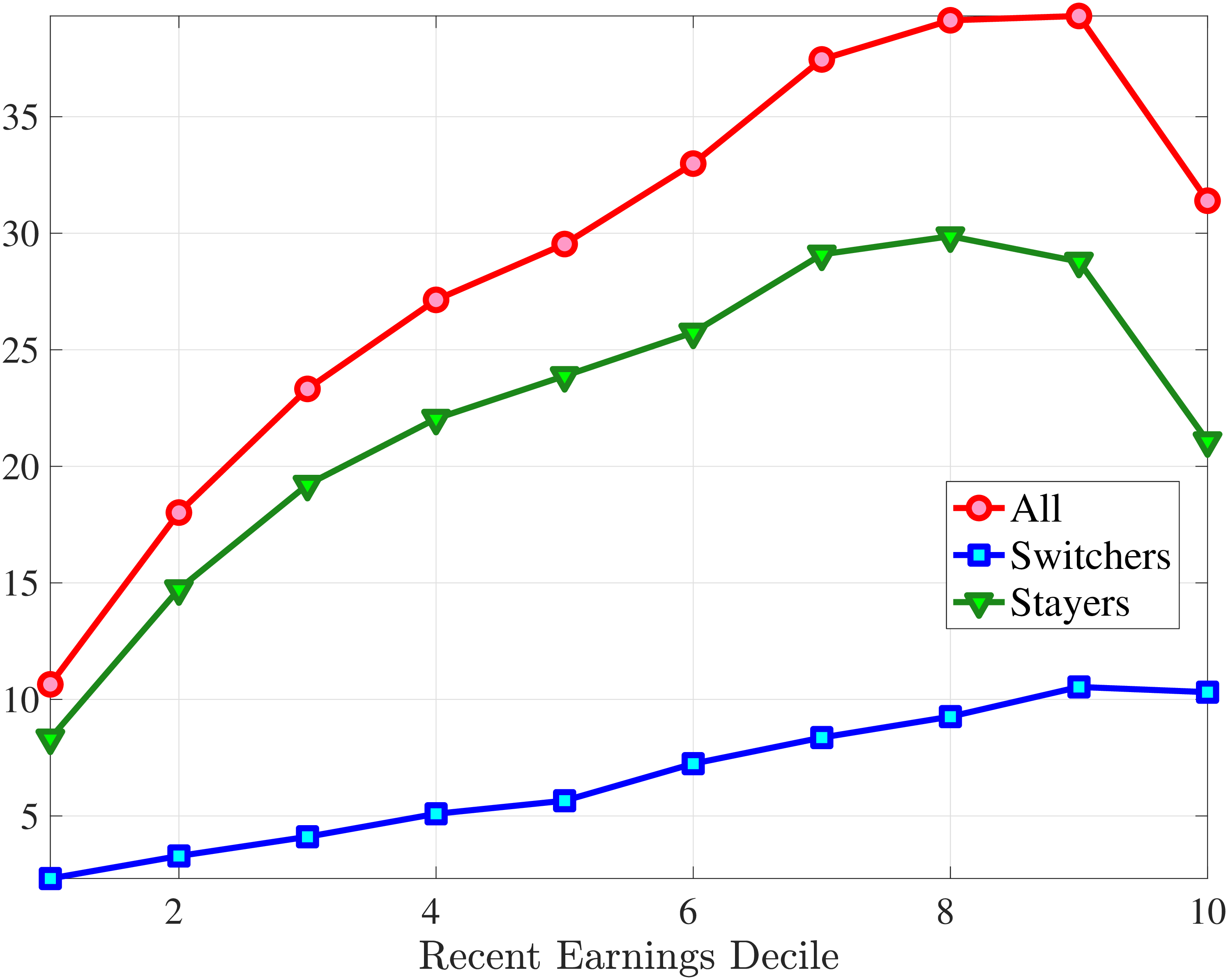

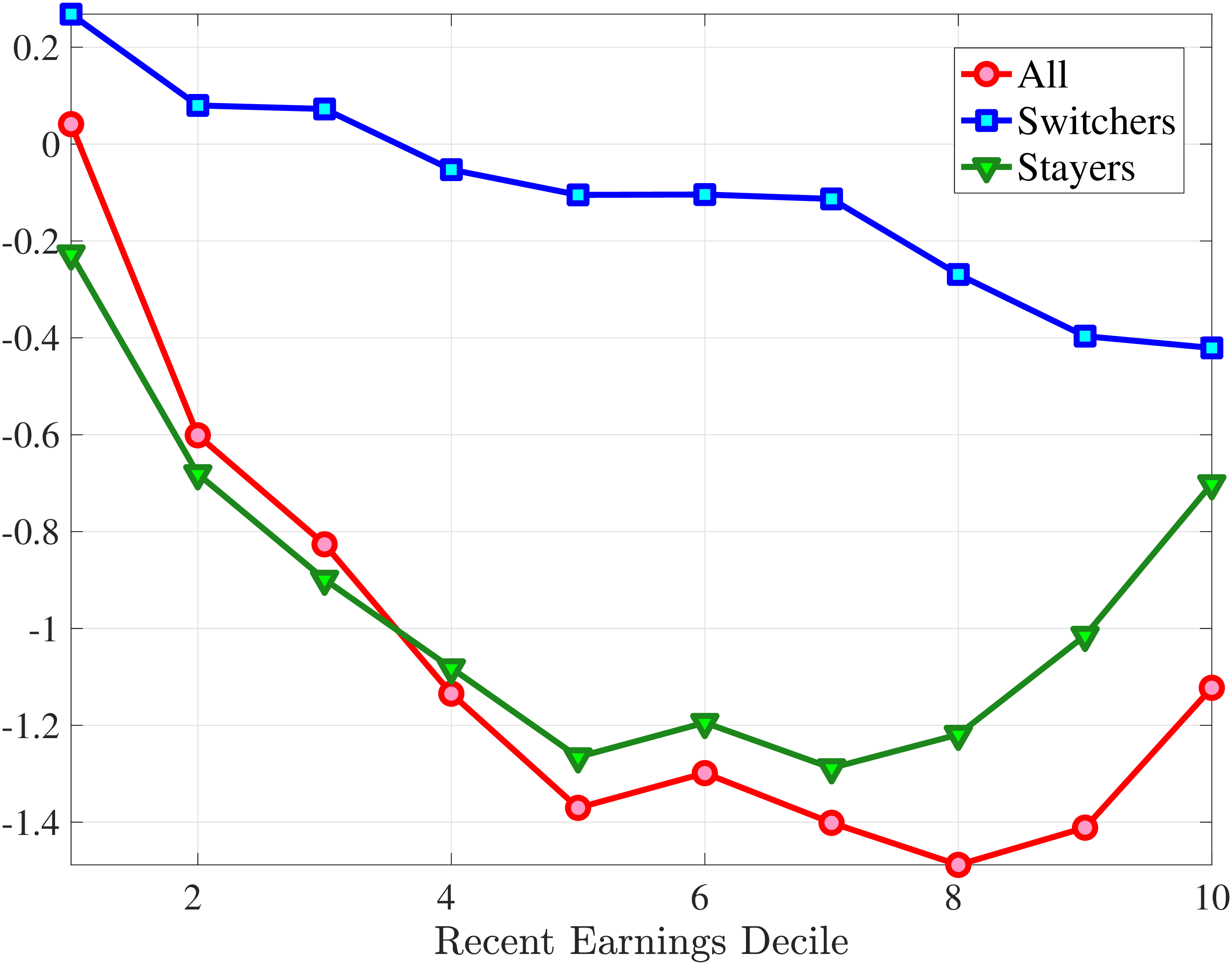

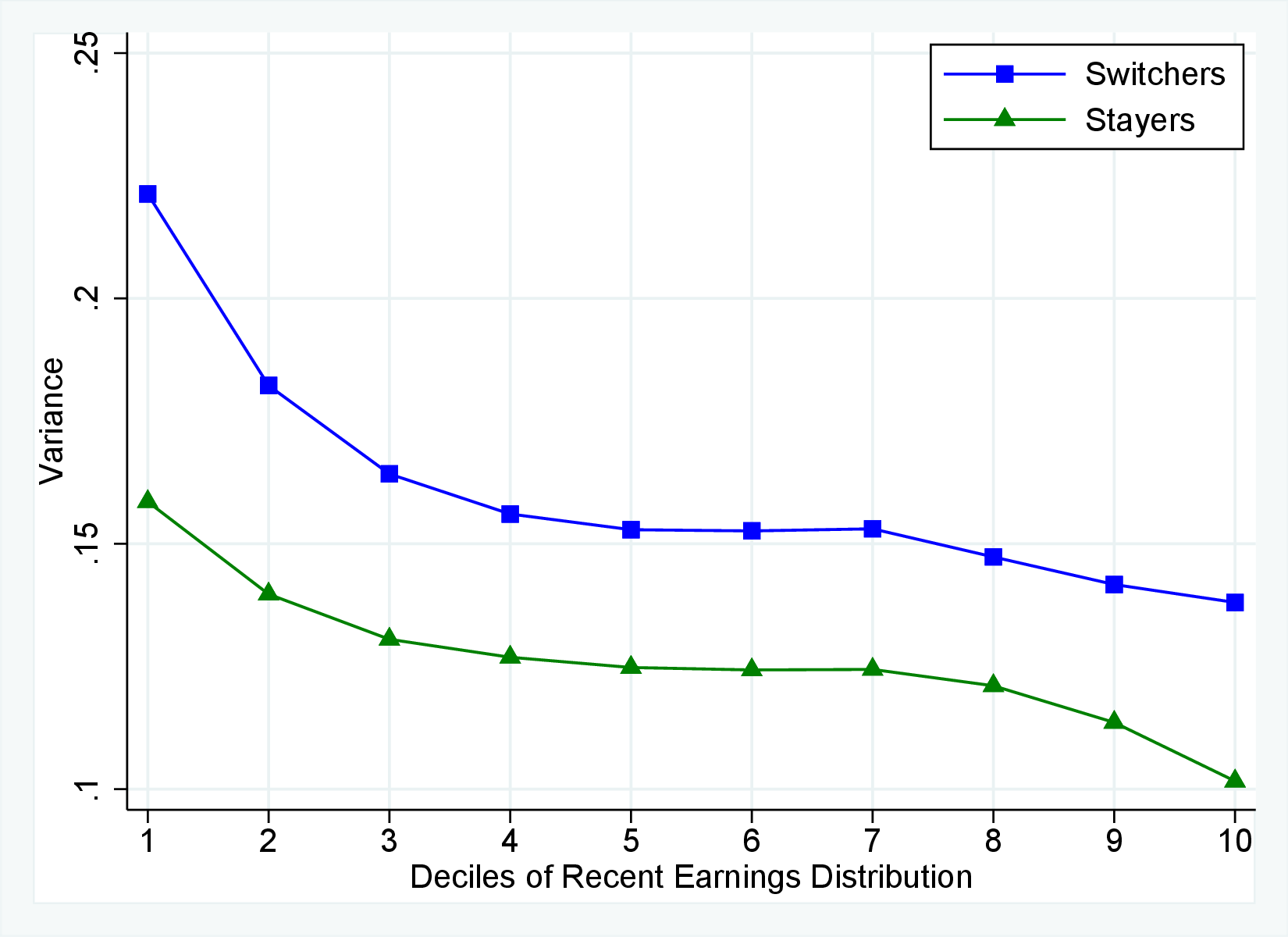

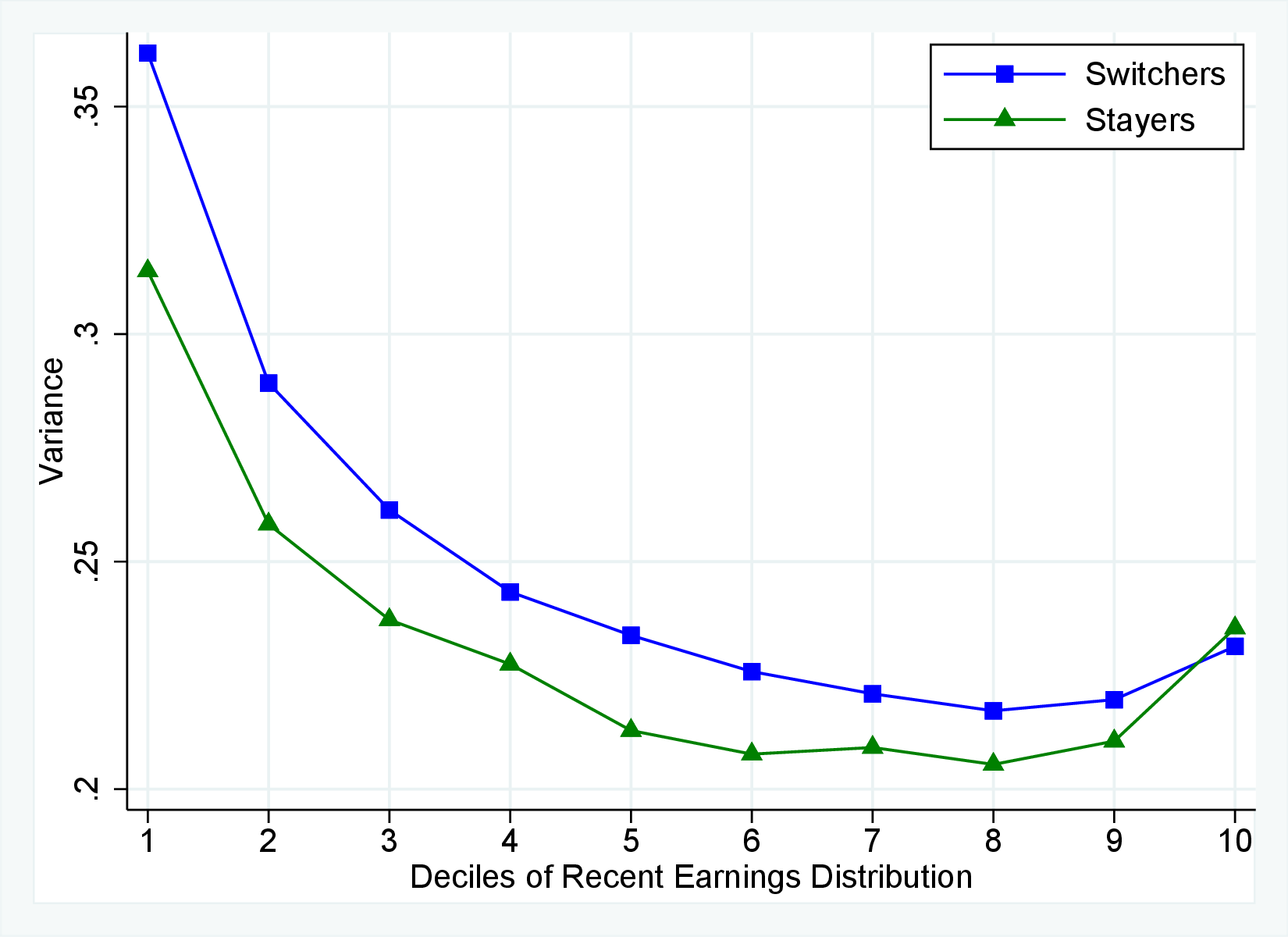

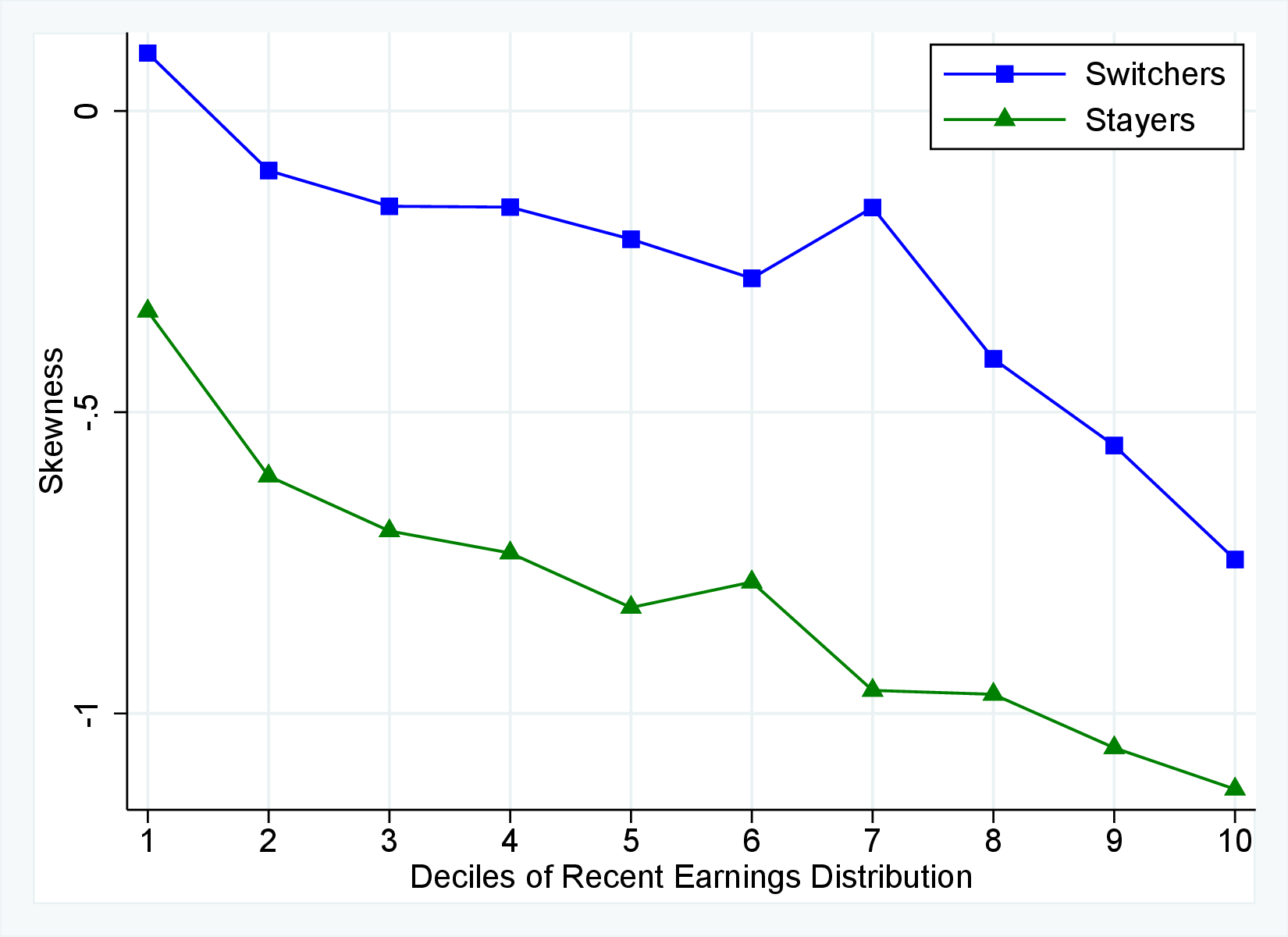

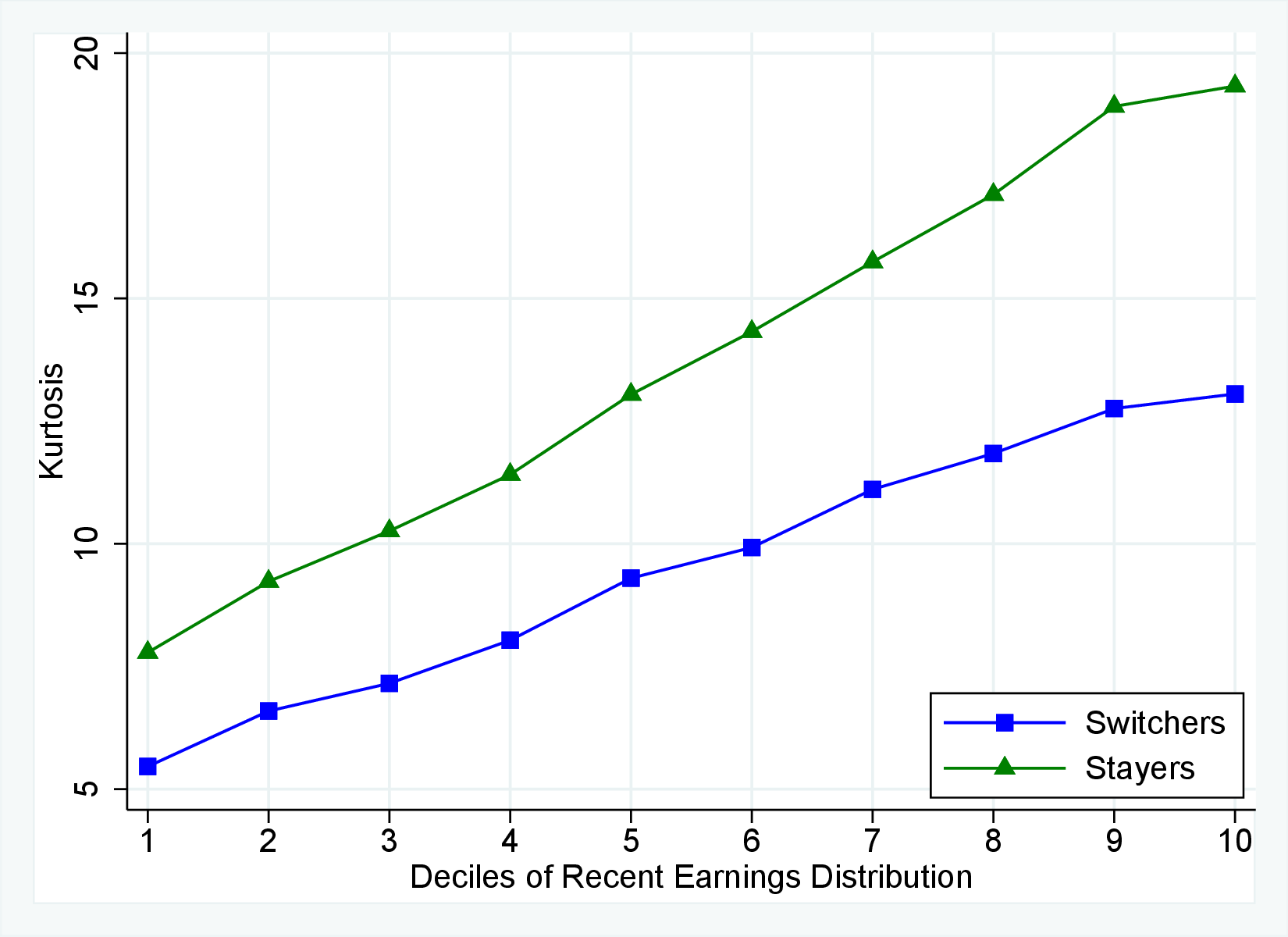

5.3 Job Stayers and Switchers

Section 4.3 documented that a change of employer is a key event causing large earnings changes. A change of employer can happen either via an unemployment spell or through a direct job-to-job movement. In this section, we study the earnings growth distributions of job stayers and job switchers separately and quantify their role in driving the higher-order moments of earnings growth. To this end, we first identify job stayers and job switchers. We define a job switcher as an individual whose main employer is different between years \(t\) and \(t+1\), where the main employment is the job that accounts for the largest share of annual earnings. The rest of the population is composed of job stayers.31 In other words, a job stayer is a worker whose main employer has remained unchanged for two years in a row, and the job spell is contiguous. This classification of stayer workers is similar to the previous literature (Card et al. (2013)).32

(a) Variance of \(\Delta _{\log}^{1}y_{t}^{i}\)

(a) Variance of \(\Delta _{\log}^{1}y_{t}^{i}\) (b) Skewness of \(\Delta _{\log}^{1}y_{t}^{i}\)

(b) Skewness of \(\Delta _{\log}^{1}y_{t}^{i}\) (c) Kurtosis of \(\Delta _{\log}^{1}y_{t}^{i}\)

(c) Kurtosis of \(\Delta _{\log}^{1}y_{t}^{i}\)

Figure 12

–

Moments of One-Year Log Earnings Growth: Stayers versus Switchers

Note: The figure displays the higher-order cross-sectional moments of one-year log earnings growth (\(y_{t+1}-y_{t}\)) for job switchers (blue line), job stayers (green line), and all prime-age males (red line) for each RE decile.

Figure: Figure 12 – Moments of One-Year Log Earnings Growth: Stayers versus Switchers

Figure 12 shows the cross-sectional moments of one-year earnings growth for stayers and switchers separately. Annual earnings changes for switchers tend to be substantially more dispersed, more symmetric (less left skewed), and significantly less leptokurtic than those for stayers. Figure E.5 in the Appendix confirms that a similar pattern holds for women. The differences between stayers and switchers are qualitatively different from the findings in Guvenen et al. (2019) for the U.S. in that they find that annual earnings growth for males is more symmetric for stayers than it is for switchers. One important contributor to strong negative skewness for stayers in Norway is sickness leave, as workers who receive some sickness benefits have more negative skewness than the stayers who do not experience sickness (details are available upon request). Note that by regulation these workers remain employed by the same firm during their sickness leave.

Role of Stayers and Switchers in Distribution of Earnings Growth

How important are the switchers in driving the nonnormal features of annual earnings growth relative to the stayers? It turns out that the contributions of two mutually exclusive groups, such as job stayers and job switchers, to the cross-sectional skewness and kurtosis of earnings changes can be decomposed using two simple formulas that we state in the following lemma.

Lemma 2. Let the sample \(S\) be split into two mutually exclusive groups, \(S=S_{1}\cup S_{2}\) and \(S_{1}\cap S_{2}=\emptyset\). Skewness can then be decomposed into \(S_{1}\) and \(S_{2}\) components,

\[ \begin{aligned} \text{skew}\left (y\right) &= \underset{\text{skewness due to }S_{1}}{\underbrace{\frac{1}{\left (std\left (y\right)\right)^{3}}\int _{\left \{i\in S_{1}\right \}}\left (y_{i}-E\left (y\right)\right)^{3}dF\left (y\right)}}+\underset{\text{skewness due to }S_{2}}{\underbrace{\frac{1}{\left (std\left (y\right)\right)^{3}}\int _{\left \{i\in S_{2}\right \}}\left (y_{i}-E\left (y\right)\right)^{3}dF\left (y\right)}}. \end{aligned} \]

Kurtosis can be decomposed into components stemming from \(S_{1}\) and \(S_{2}\),