1 Introduction

Parents’ role in children’s incomes has been a long-standing question of great importance in economics and public policy. The earlier literature has extensively documented the relationship between parents’ and children’s income levels.1 Yet, little is known about parents’ role in children’s income dynamics. How do fathers’ economic resources (measured by lifetime income and wealth) affect the properties (i.e., mean, variance, skewness, and kurtosis) of workers’ earnings changes? Do the income streams of children and fathers have similar properties? The intergenerational transmission of income dynamics may arise, for instance, because of similarities in risk attitudes, jobs, and occupations between parents and children; workers pursuing different careers depending on available parental insurance; parents’ dynastic precautionary savings motive (as in Boar (2021)); or some combination of these mechanisms.

As part of The Global Repository of Income Dynamics (GRID), which aims to produce harmonized cross-country statistics on earnings dynamics from administrative data sources, we first provide a comprehensive characterization of earnings inequality, volatility, and mobility in Norway. In contrast to earlier literature, we focus on the top earners and the non-Gaussian features of earnings fluctuations. Next, we address the above questions by studying the intergenerational transmission of income dynamics in Norway.

Our dataset is derived from a combination of administrative registers covering the entire Norwegian population from 1967 to 2017. One of the registers is collected to calculate social security pension benefits since 1967. The income variable from this register thus measures the total basis for pension accrual, which is the sum of wages, self-employed income, unemployment benefits, sick leave, and parental leave compensation. Starting in 1993, we can separate labor income from government transfers and have information on household wealth, all of which we use in our analysis. All registers include personal identifiers that allow us to link children to their parents.

We start by describing the salient features of the labor income distribution. While earnings inequality is low relative to other developed economies, Norway has not been immune to the recent increase in top income inequality observed in other countries (e.g., Aaberge et al. (2017), Domeij and Floden (2010)). In particular, the share of income accrued to the top 1% of earners has increased by 25% among men and 28% among women between 1993 and Great Recession. Furthermore, unlike most other developed economies (see Lagakos et al. (2018) for a cross-country comparison), earnings dispersion below the 90th percentile declines sharply over the life cycle but increases significantly for those in the top 10%. Also, the earnings dispersion of recent cohorts is more unequal at age 25, which is mainly a result of the higher dispersion above the median.

Turning to the income dynamics, we find that the earnings growth distribution exhibits negative skewness and excess kurtosis. The extent of these nonnormalities varies with age and earnings level, which are similar to those documented for the U.S. and other countries (Guvenen et al. (2021)). For example, older or upper-middle-income workers face less volatile but more left-skewed and more leptokurtic earnings growth compared with younger workers or those at both ends of the income distribution, respectively. Finally, income mobility declines significantly after age 35 and is higher for women.

We then investigate whether workers differ in their income dynamics also because of differences in their parental backgrounds. For completeness and consistency with earlier work, we start our analysis by documenting the relation between parents’ and children’s lifetime incomes. To this end, we include individuals with at least 20 years of income observations in our sample. Our results confirm the findings of the earlier literature of significant intergenerational persistence in income: a 10% increase in fathers’ lifetime income is associated with a 2.4% (2.3%) increase in sons’ (daughters’) lifetime income. Furthermore, we find that the intergenerational income elasticity is fairly uniform across the fathers’ lifetime income distribution, indicating a roughly linear relationship between the incomes of two generations.

Turning to the features of income growth, we first investigate how average income growth over the life cycle varies by family resources. We find that workers born in more affluent families enjoy significantly stronger annual income growth. For example, the sons of fathers at the 90th percentile of the lifetime income or wealth distribution experience a median (average) income growth that is approximately 1% (2%) higher relative to those with parents at the 10th percentile. This heterogeneity is economically significant, considering that the estimates of the standard deviation of heterogeneous income profiles are around 2% for the U.S. (e.g., Guvenen et al. (2021)).

In addition, we also find a strong correlation between fathers’ and children’s life-cycle income growth. For each individual, we compute the median income growth over the life cycle using at least 20 years of observations. A 5% increase in the father’s median income growth is associated with a roughly 1% (0.8%) increase in the son’s (daughter’s) median income growth. This strong correlation in income growth between fathers and children emphasizes the importance of using lifetime incomes for measuring intergenerational income elasticity (e.g., Haider and Solon (2006)) and developing models of multi-dimensional intergenerational skill transmission (e.g., Lochner and Park (2020)).2

As for the second moment, we show that children’s income volatility follows a U-shaped pattern by fathers’ lifetime income and net worth, with workers from middle- and upper-middle-class families experiencing the most stable incomes. Children of very affluent fathers face particularly more volatile incomes over the life cycle. For example, the difference between the 90th and 10th percentiles (P90-P10) of income growth for workers with fathers at the top 1% of the lifetime income or wealth distribution is around 15 to 18 log points higher compared to those of fathers at the median. This higher income volatility, combined with the steeper income growth, suggests that children of affluent parents can pursue careers with higher growth potential but also higher risk.

We also document significant intergenerational transmission of income volatility in that fathers with more volatile incomes have children with riskier income streams too. In particular, income volatility—measured by the P90-P10 of an individual’s income growth stream over the working life—increases from 35 to 45 (45 to 55) log points for sons (daughters) as fathers’ volatility increases from 10 to 50 log points.3

Next, we show that the skewness of children’s income growth increases as we move from poorer to richer fathers. Up to around the 85th percentile of the fathers’ lifetime income or wealth, the increase in skewness—which is accompanied by a decrease in dispersion— reflects more of a decline in the likelihood of a sharp fall in income (left tail risk). As for children of the top 10% fathers, and in particular, of the top 1%, both tails of the income growth distribution stretch, but the right tail expands more than the left tail, thereby generating an increase in skewness and dispersion. These findings are again consistent with the conjecture that workers with more parental insurance can pursue higher-return, higher-risk careers. Furthermore, we find a strong correlation between fathers’ and children’s skewness of income changes: fathers with higher left tail risk tend to have children with higher downside risk.

The significant correlation between fathers’ and children’s income dynamics can be explained by their having similar risk attitudes; working in occupations, sectors, and jobs with similar risk profiles; or both. We investigate the latter mechanism by investigating the intergenerational persistence in education using 47 categories of degrees. We find a strong correlation between fathers’ and children’s education, especially for those with high levels of education such as dentists, lawyers, and doctors. For example, the sons of dentists are more than 20 times more likely to study dentistry than the population average. At the other extreme, we find some upward socioeconomic mobility for children of relatively low-educated fathers, such as those with a primary education.

Finally, we examine whether fathers’ role in workers’ income dynamics is simply spurious because of omitted variables such as workers’ own permanent income. For this purpose, we run “horse race” regressions with all four factors investigated above—fathers’ income dynamics, lifetime income, and net wealth, as well as workers’ own permanent income—included as explanatory variables in the same model. We find that all four regressors are statistically significant at the 1% level and economically important.

2 Institutional Background and Data

2.1 Institutional and Historical Background

Norway is a typical Scandinavian welfare state with a proactive labor market policy, comprehensive social security benefits, and a redistributive tax policy (see Blundell, Graber and Mogstad (2014)). Welfare provision is financed primarily through high labor and capital income taxes and, to a smaller extent, by returns from a sovereign wealth fund (which, by 2021, has a market capitalization more than three times the GDP). The labor market functions relatively well, with low unemployment and high participation rates for men and women. This is partly because of strong cooperation between unions, employers, and government that allows for wage flexibility to generate competitiveness (see Nilsen (2020)).

Although the unemployment rate is low, the number of working-age Norwegians who receive sickness or disability benefits is among the highest in the OECD (e.g. Hemmings and Prinz (2020)). While the duration of unemployment benefits and average replacement rates are relatively generous (currently two years and 62.4%, respectively), requirements for unemployment benefits are strict (Fevang, Markussen and Roed (2014)). Sickness pay is available for all employees with a 100% replacement rate up to a limit. Bratsberg, Fevang and Roed (2013) have shown that a large fraction of disability claims is triggered by job loss.

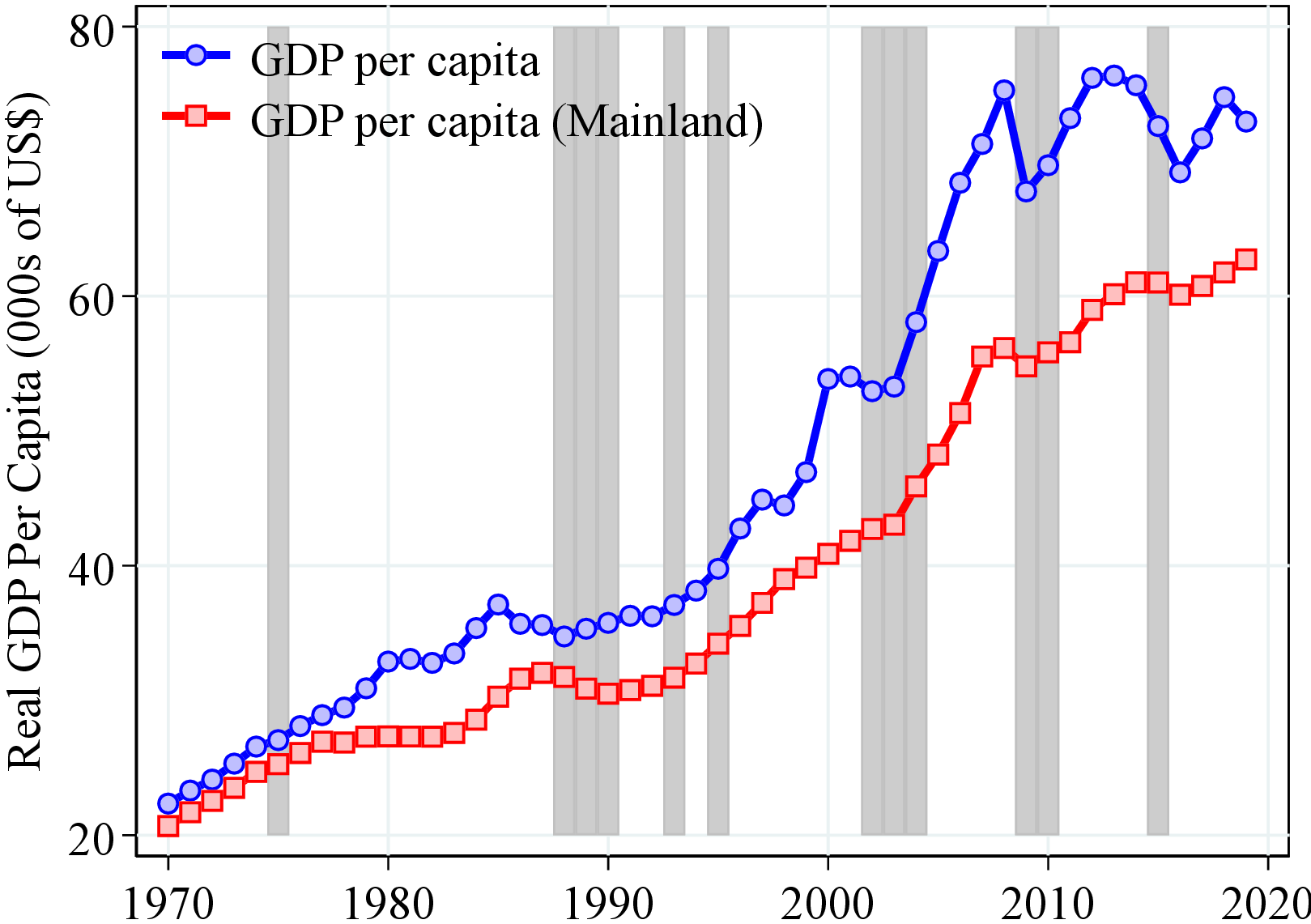

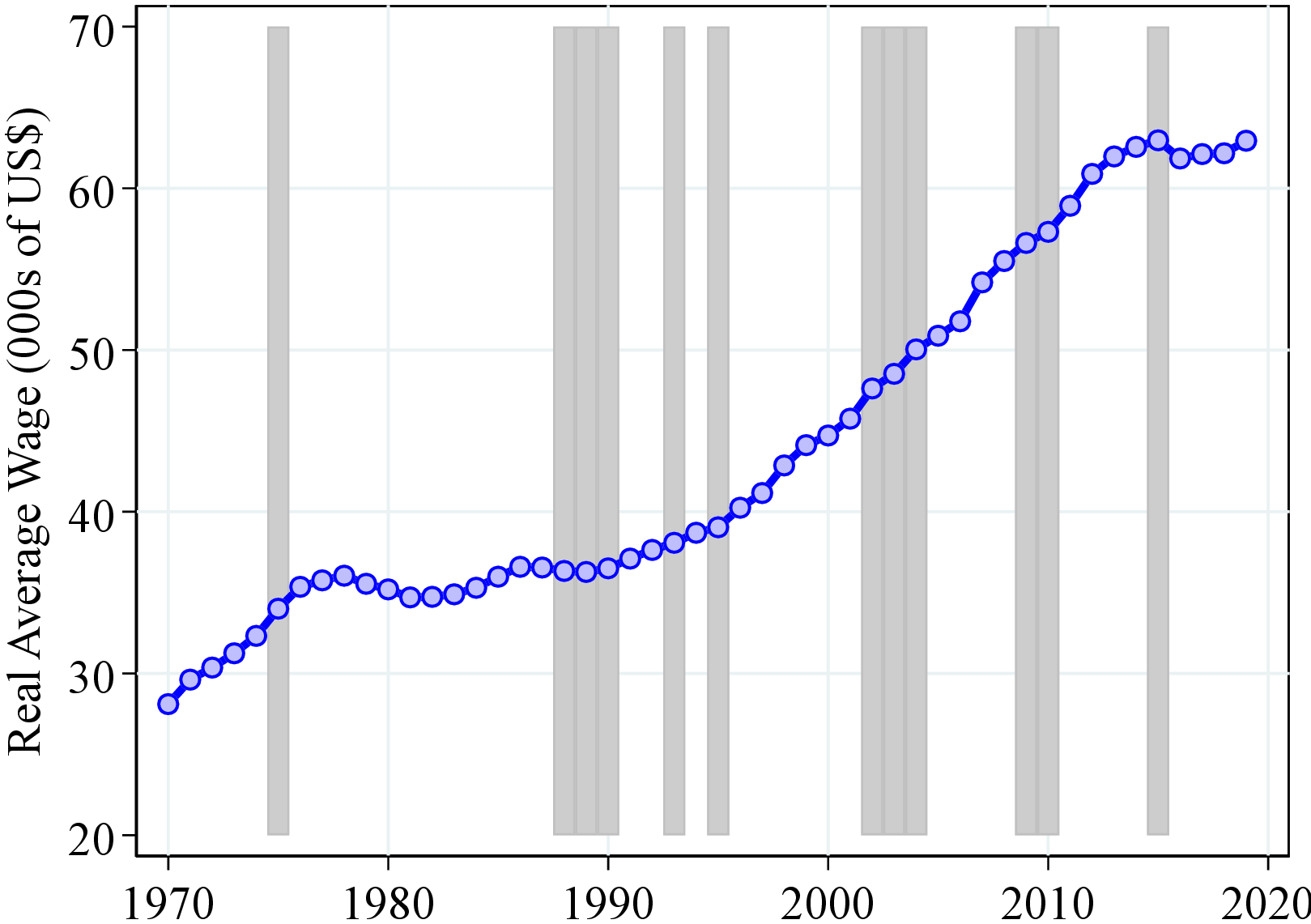

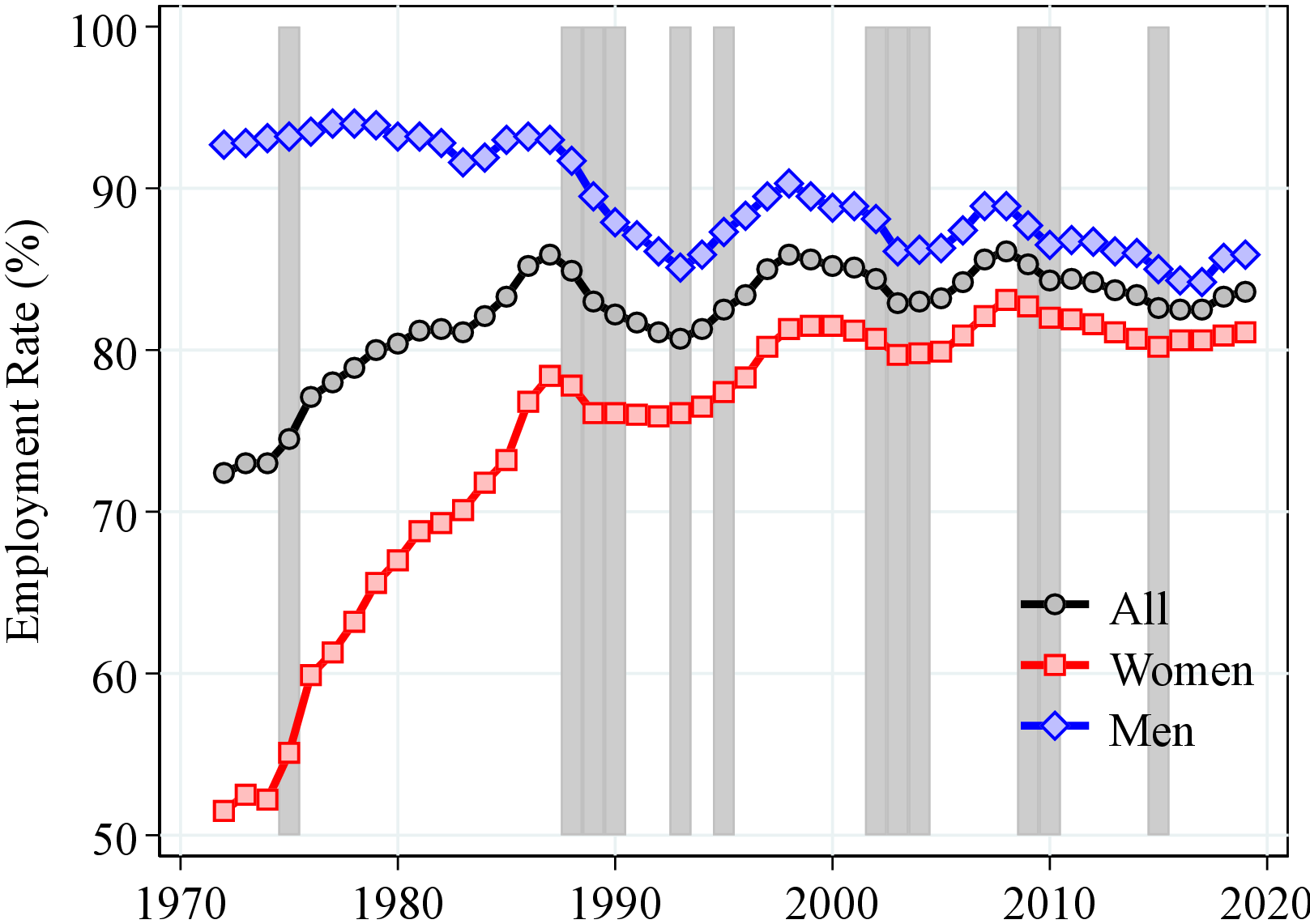

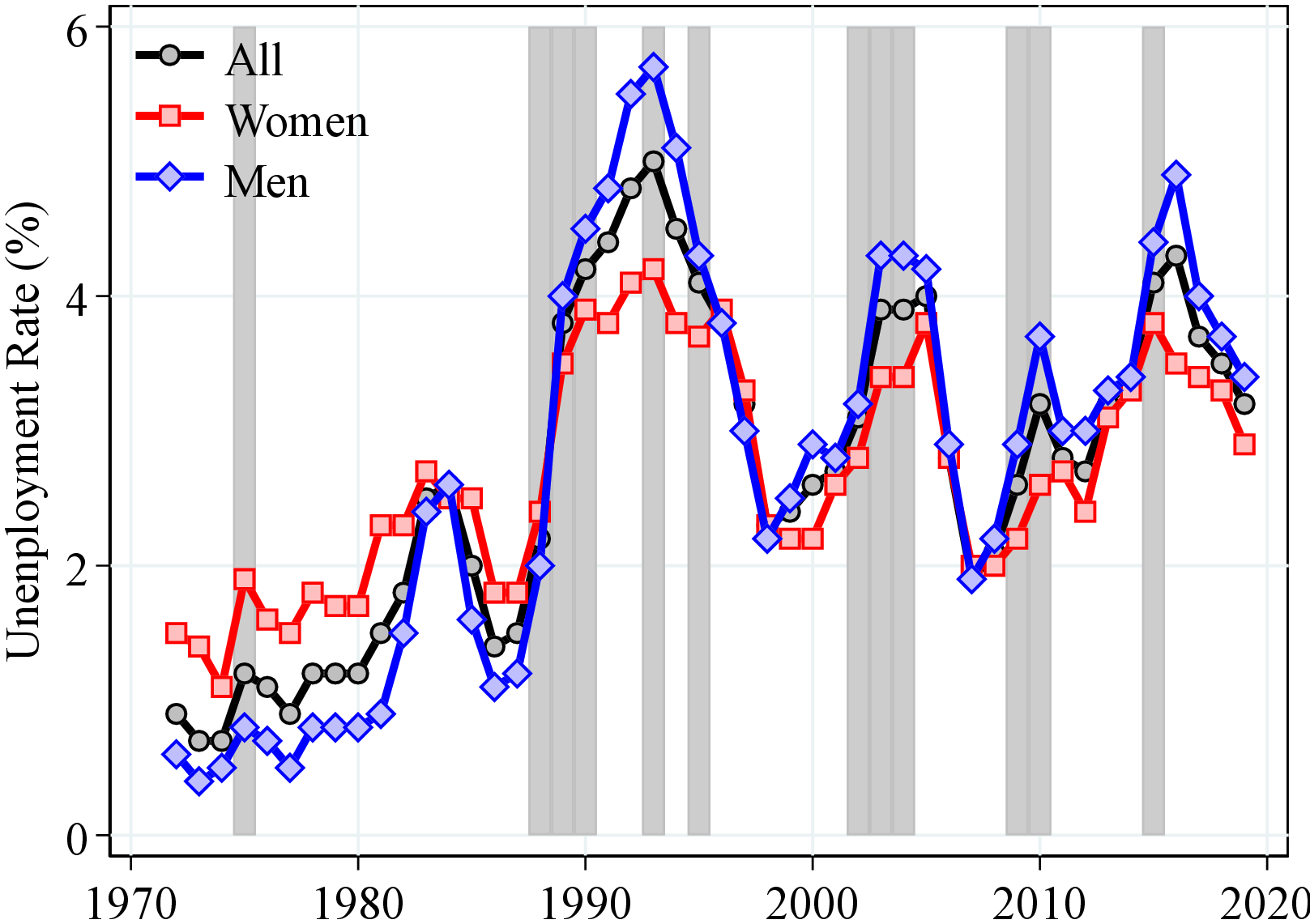

Norway experienced a remarkable increase in GDP per capita since the 1970s, which almost quadrupled from $22,000 to more than $75,000 (Figure 1a). Despite this overall outstanding performance, the economy has been subject to large cyclical variations. Until the banking crisis of the early 1990s, Norway experienced a large increase in labor force participation of women by around 25 percentage points (pp.) reaching to almost an 80% participation rate, one of the highest among developed countries (Figure 1c). The large inflow of workers contributed to the steady growth during this period. As a result, average real wages grew by only around 25% during this period (Figure 1b) compared to the 70% growth in GDP per capita. However, the banking crisis led to a sharp decline in GDP and labor force participation (especially for men, from 94% to 85%) and an increase in unemployment from around 1% to 5% (Figure 1d).

The aftermath of the recession, however, brought a quite significant resurgence of growth, with GDP per capita increasing from $40,000 to $75,000 in a span of 18 years until the Great Recession. During this period, oil prices increased sevenfold, which significantly contributed to the strong economic growth. The share of the oil sector in the economy grew from 5% to 10% in 1990 to 35% in 2007 at the peak of the oil prices (Figure 1a). Average wage growth was also strong during this period from $40,000 to $56,000 (Figure 1b). The Great Recession put a stop to this rapid economic growth, after which the Norwegian economy has been stagnating for 10 years without significant improvement, although, Norway managed to maintain high labor participation rate (above 80%) and low unemployment rate (around 4%) during this stagnation period.

Notes: Figure 1 shows the evolution of main macroeconomic aggregates in Norway since 1970 (employment/unemployment rates from the Norwegian Labor Force Survey that started in 1972). GDP and average wage are expressed in U.S. dollars of 2018. Mainland Norway consists of all domestic production activity except exploration of crude oil and natural gas, transport via pipelines, and ocean transport. The gray bars represent recession years, defined as years with an unemployment growth rate of 0.4 pp. or more and an output gap of -0.5 or less. Source: National Accounts and Labor Force Survey, Statistics Norway.

2.2 Data Description

Our dataset consists of several high-quality registers covering the entire Norwegian population. All of them are collected for administrative purposes; thus, our data are less subjected to the measurement error and sample attrition that usually plague survey data. In our analysis, we use two different measures of income. The first one is labor earnings between 1993 and 2017. The second one covers a longer time span between 1967 and 2017 and includes both earnings and work-related government transfers. Below, we describe each income measure and explain how they are used in our analysis.

Labor earnings. The first income variable is a comprehensive measure of labor income from all jobs (except for self-employment income).4 It is obtained from annual tax records and is third-party reported by employers.5 This measure allows our benchmark results on earnings inequality and volatility in Sections 3.1 and 3.2 to be comparable with other articles in this issue of the journal, which also use labor earnings in their analysis.

After-transfers income. The second income variable is collected to calculate social security pension benefits since 1967 and includes all work-related pensionable income components: labor income (as described above), self-employment earnings, unemployment, sick leave, parental leave, vocational rehabilitation, and time-limited disability benefits. The long panel dimension (51 years) of this variable is key for our analysis of the intergenerational transmission of income dynamics.

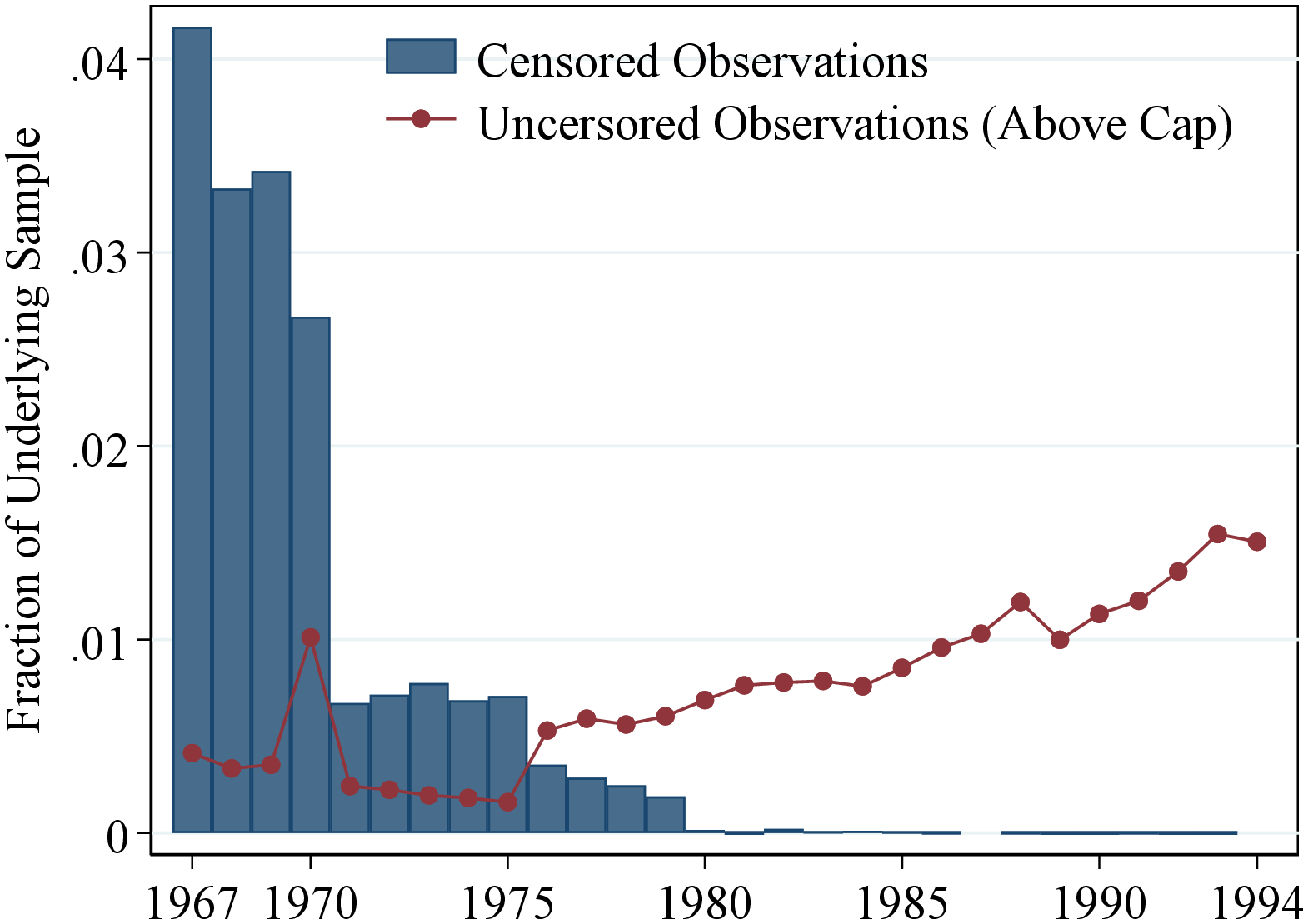

Certain measurement issues warrant specific attention for this income variable. First, some observations are top-coded as a result of an earnings limit for pension accrual. Top coding was most prevalent between 1967 and 1979. From 1986 on, there is none whatsoever (see Figure A.1 in Appendix A). Second, there are changes to how benefits are included in the data throughout the sample period: (i) Paid sick leave and parental leave were included after 1978 (paid sick leave was included even before 1978 if it was more than 90% of annual income); (ii) unemployment benefits were included after 1980; and (iii) various work activity benefits were included after 2002, 2004, and 2010. Finally, a tax reform in 1992 changed the way earnings from self-employment were reported.

Since the definition of this income measure changes over time, one should be careful in interpreting the trends in inequality and volatility derived from this income measure. Therefore, in Section 3 we focus on our consistent measure of labor earnings starting in 1993. However, these measurement issues are less of a concern for our intergenerational analysis, which pertains to the comparison of earnings risk within cohorts (e.g., fathers with more volatile incomes among their peers, or sons with steeper life-cycle income growth within their cohort) and not its variation across cohorts or over time.

We complement our data on income and wages with information on families to link children to their parents (derived from the Norwegian Population Register), educational attainment (from the National Education Register), and household wealth (from tax returns since 1993), which we will explain in more detail in Section 4. All nominal incomes are deflated to their 2018 real values using the Consumer Price Index in Norway. Furthermore, to make our results comparable across countries, we convert Norwegian kroner (NOK) values to U.S. dollars using the average exchange rate in 2018.

2.3 Sample Selection and Descriptive Statistics

Our baseline sample includes all residents in Norway between ages 25 and 55 who have a personal identification number. The number of individual-year observations between 1993 and 2017 is about 51.3 million in total. As a standard practice in the literature, we trim observations below a certain time-varying annual minimum earnings threshold (\(Y_{t}^{min}\)), both to focus on workers with a meaningful labor force attachment and to avoid few observations of very low earnings affecting our results. Norway does not have a national minimum wage defined by law. Thus, we define \(Y_{t}^{min}\) as the annual earnings of an individual who works 40 hours a week for a full quarter at half the US minimum wage, which roughly equals NOK 12,000 in 2017 (see Guvenen, Ozkan and Song (2014)). 16% of the earnings observations between 1993 and 2017 are below this threshold. However, most of these individuals are out of the labor force and receive zero labor earnings during a given year, whereas only 2% of individuals with positive labor earnings are below \(Y_{t}^{min}\). Using the after-transfer income measure, only 11% of observations are trimmed, of which 1.2% have positive after-transfer income below \(Y_{t}^{min}\).

| Panel A: Sample Statistics | ||||||||||||

| Obs. (1000s) | Mean Earnings | Age % | Public % | Education % | ||||||||

| Year | Men | Women | Men | Women | \([25,35]\) | \([36,45]\) | \([46,55]\) | Men | Women | \(\lt HS\) | \(HS\) | \(CD+\) |

| 1995 | 1,046 | 954 | 44,467 | 27,805 | 42.1 | 31.8 | 26.1 | 27.1 | 52.0 | 41.9 | 27.4 | 30.8 |

| 2015 | 1.017 | 943 | 65,509 | 46,094 | 36.4 | 32.3 | 31.3 | 25.3 | 52.0 | 23.8 | 32.7 | 43.5 |

Notes: Table I shows summary statistics for the baseline sample. All nominal values are deflated to 2018 prices using the CPI of Norway and converted to US dollars using the average exchange rate in 2018. In the right columns of Panel A, we separate workers into three groups. \(<HS\) are workers with less than a high school diploma, \(HS\) are workers with a high school degree, and \(CD+\) are workers with a college degree or more advanced degrees.

Table I shows selected statistics for earnings from our baseline sample. First, our sample is almost evenly split between men (52%) and women (48%). Second, similar to other developed economies, the Norwegian working population has become older and more educated. Third, between 1995 and 2015, the earnings of men and women across all income levels have grown (Panel B). Finally, despite high employment rates for women, the gender earnings gap is relatively high, which stems from women working shorter hours and working more in part-time jobs (see Statistics Norway (2005)).

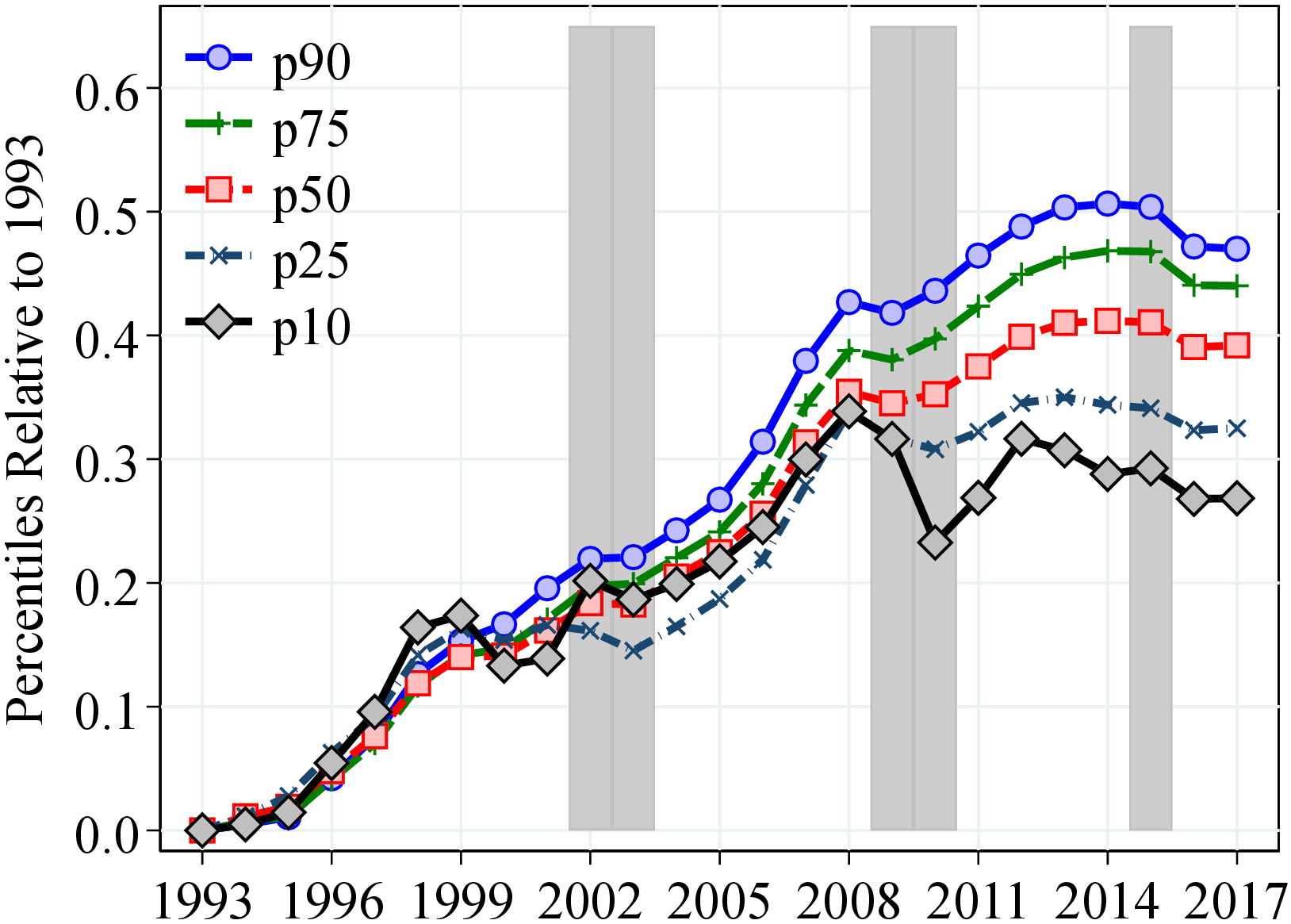

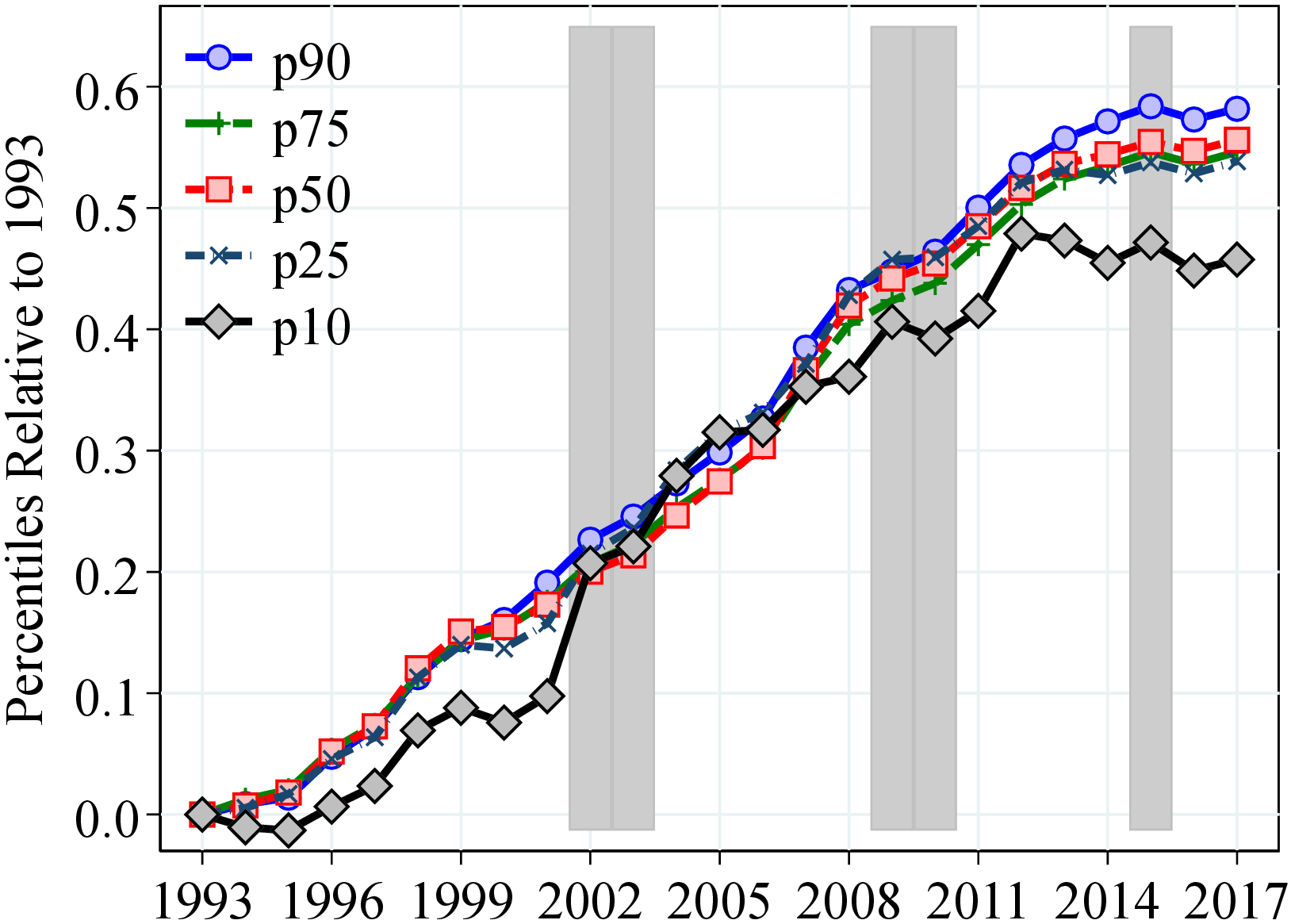

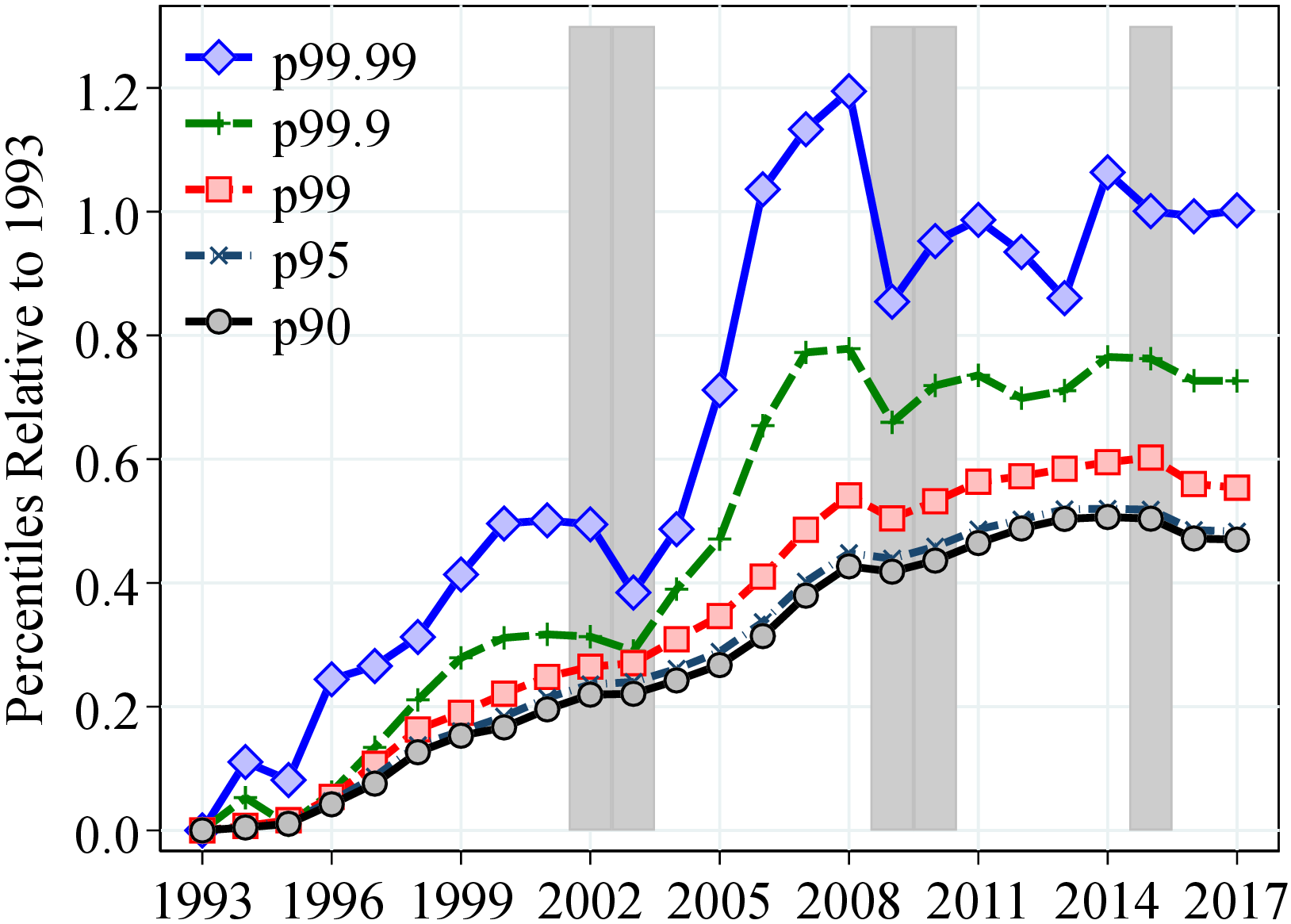

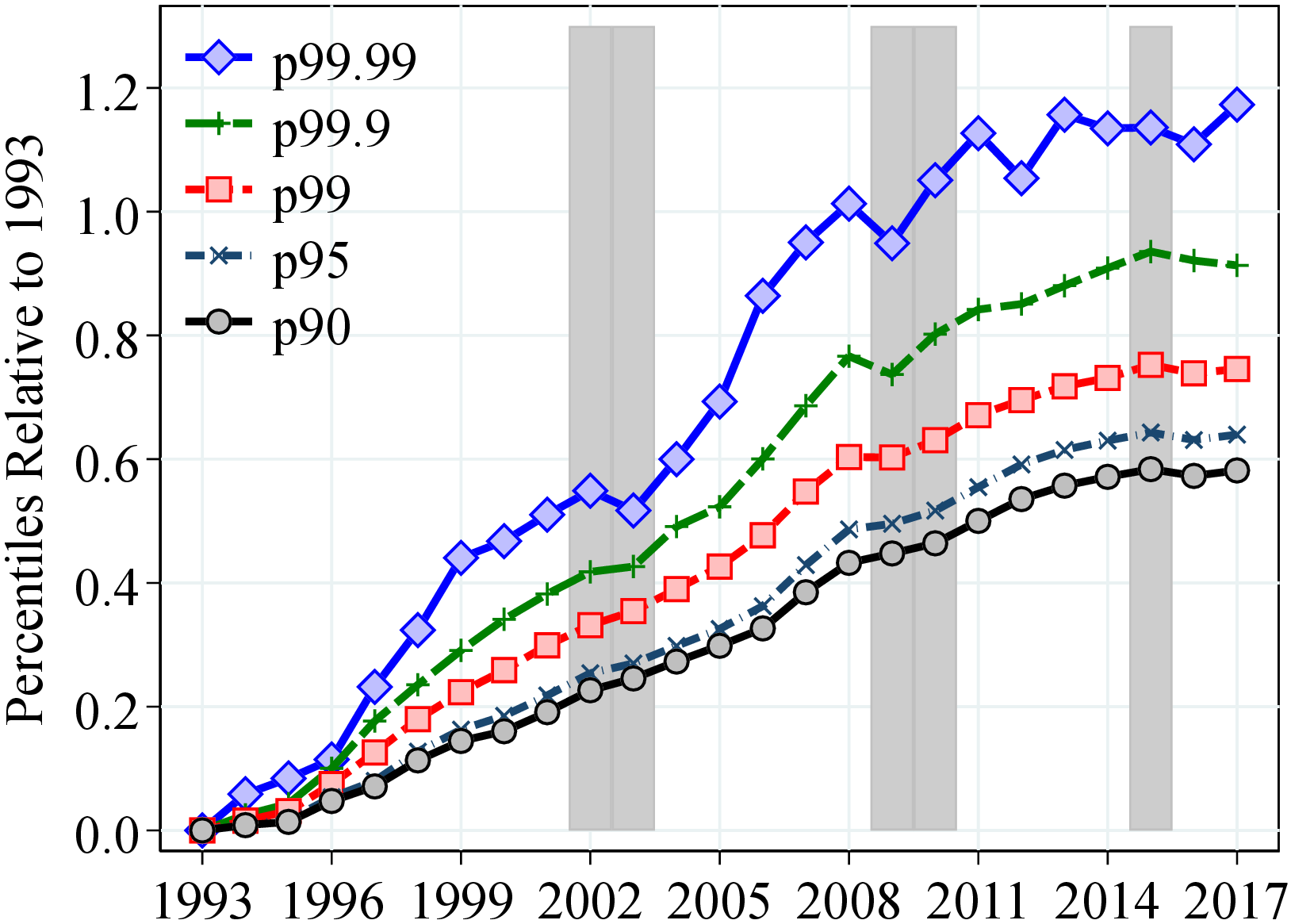

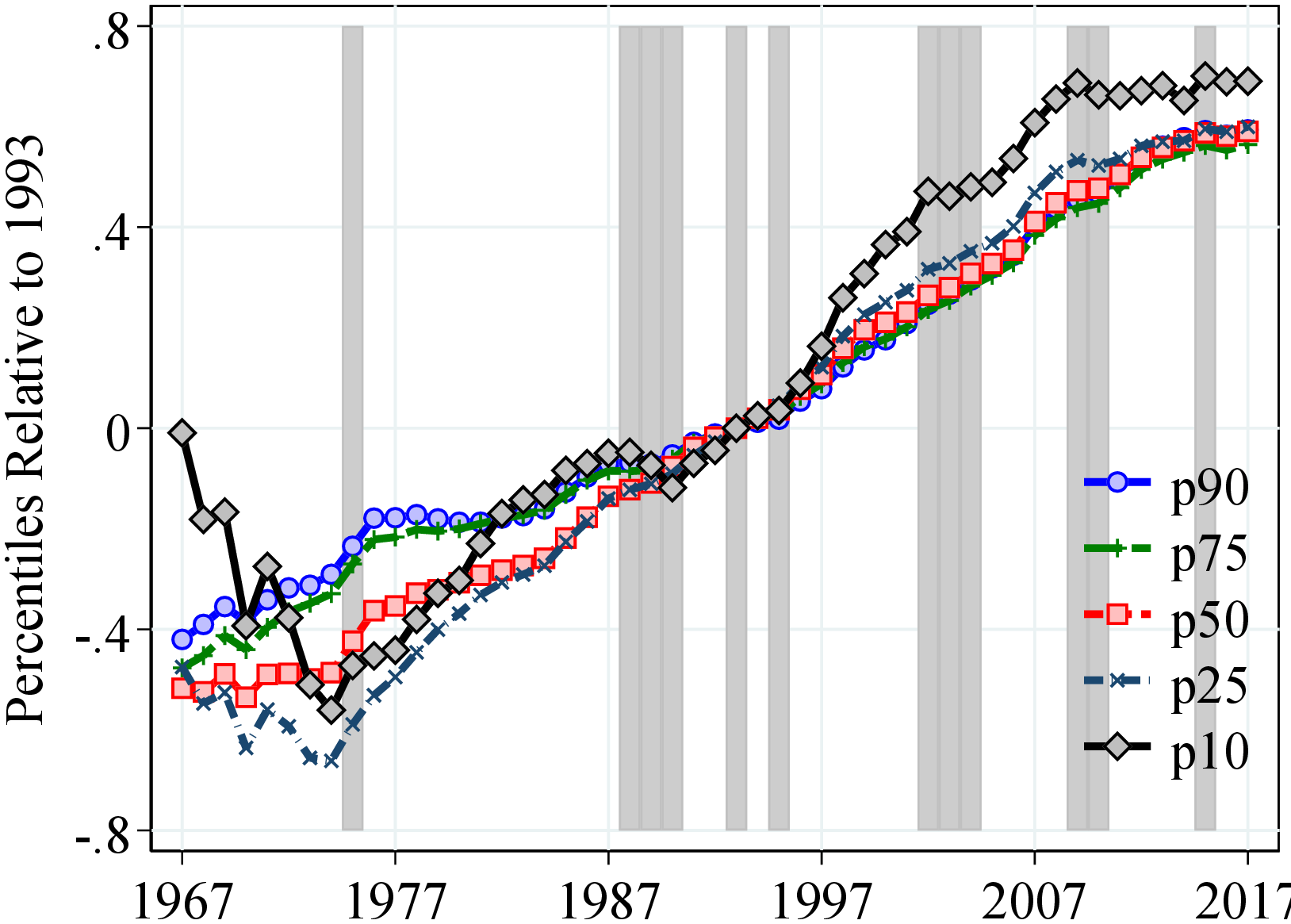

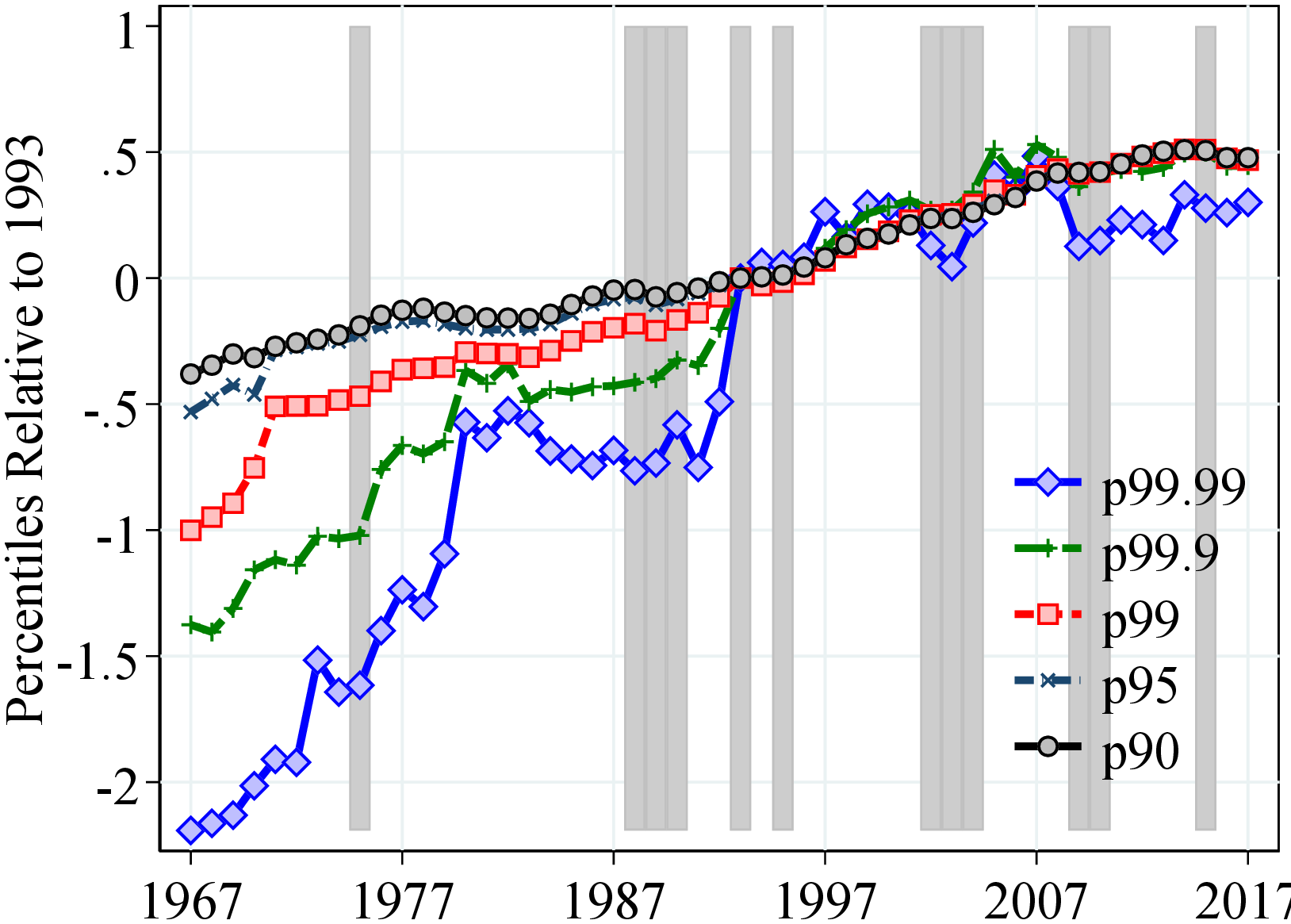

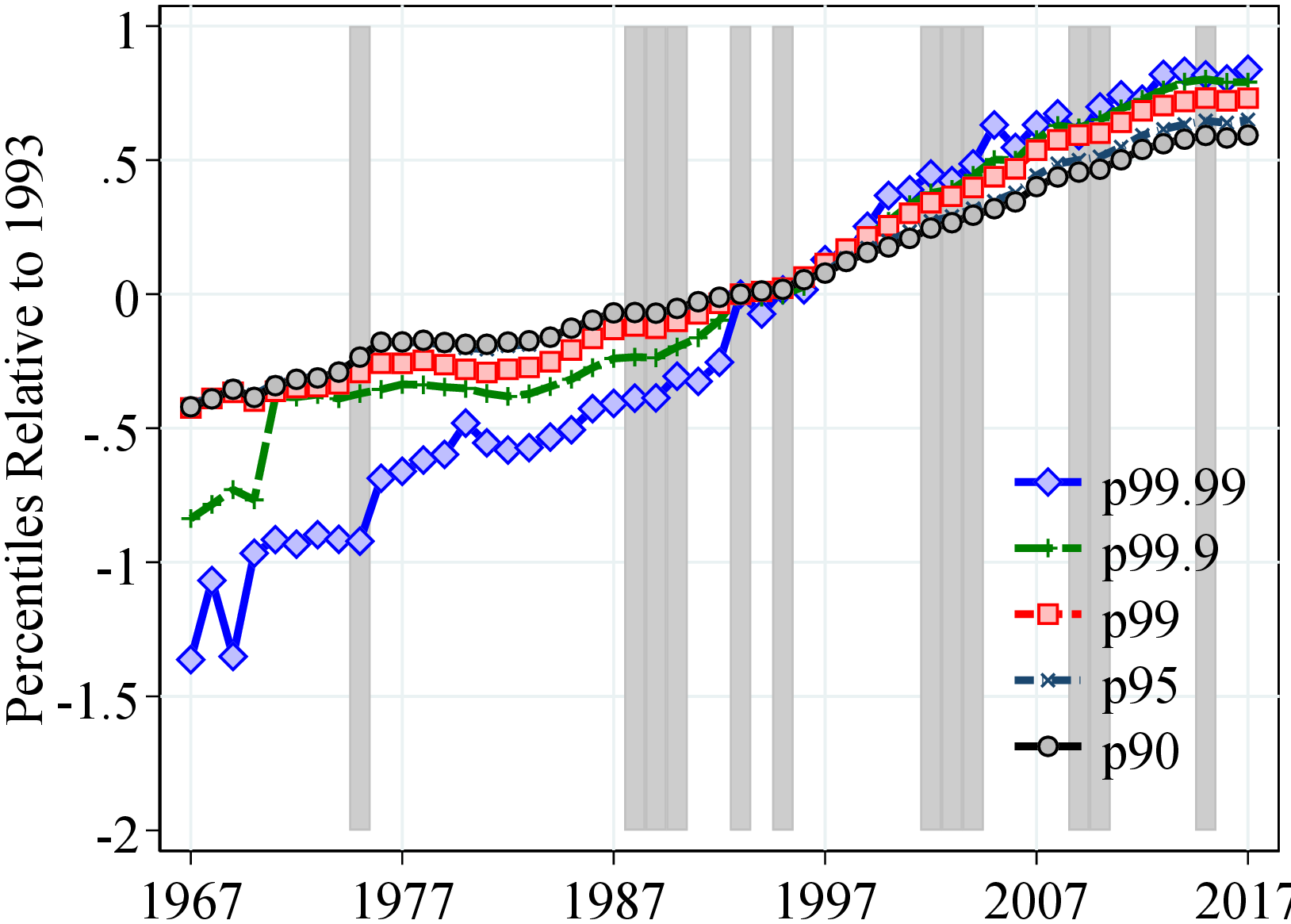

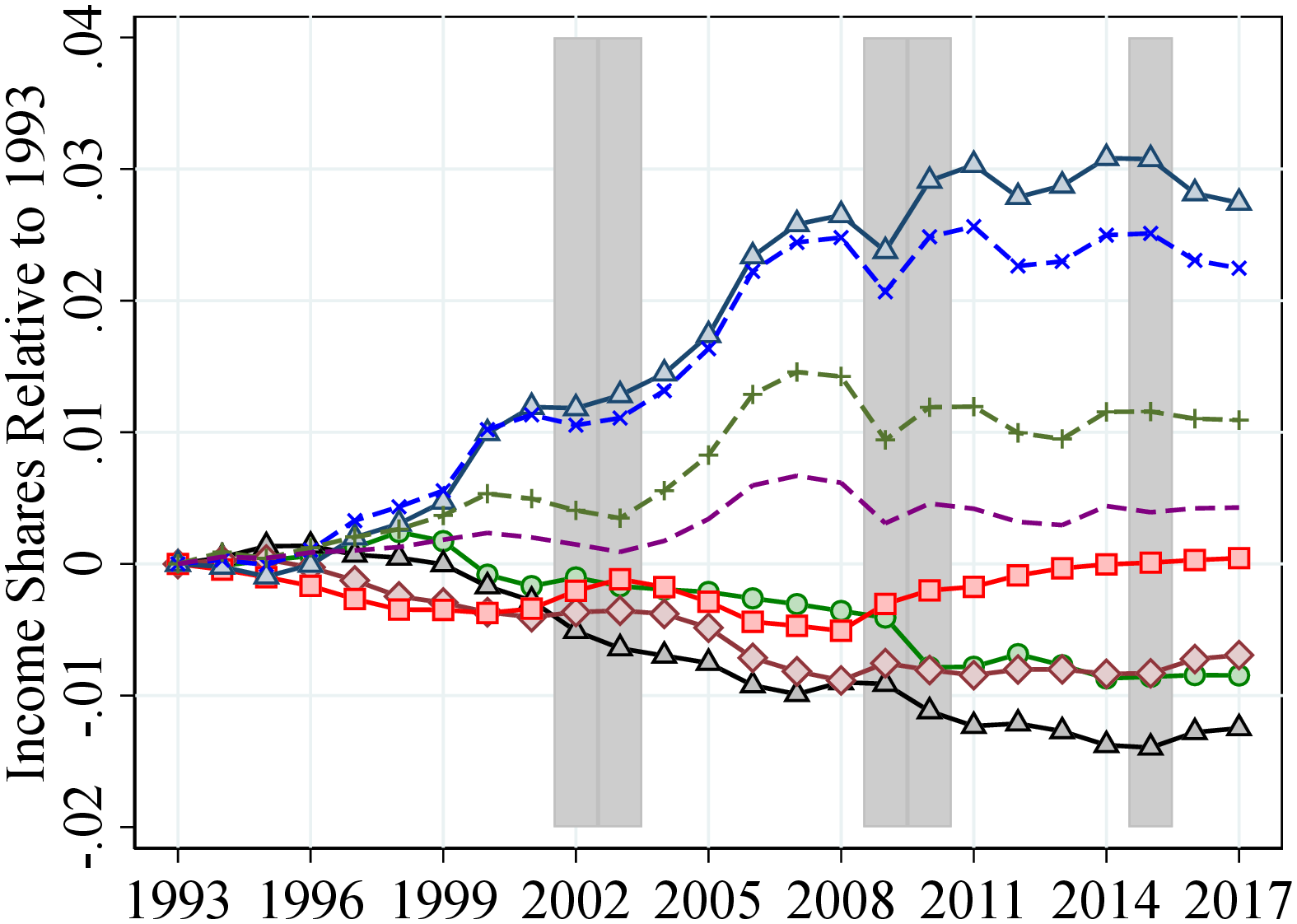

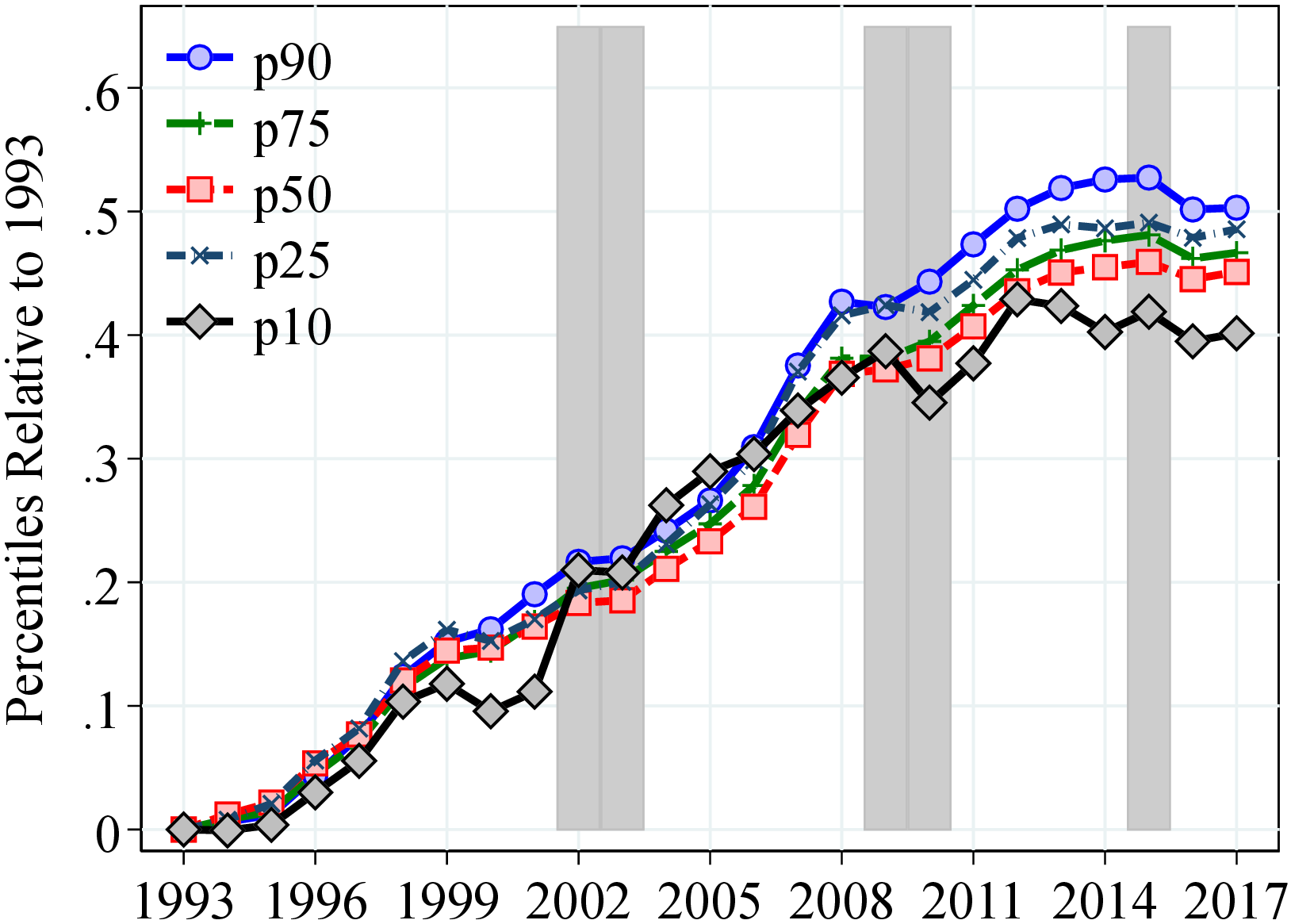

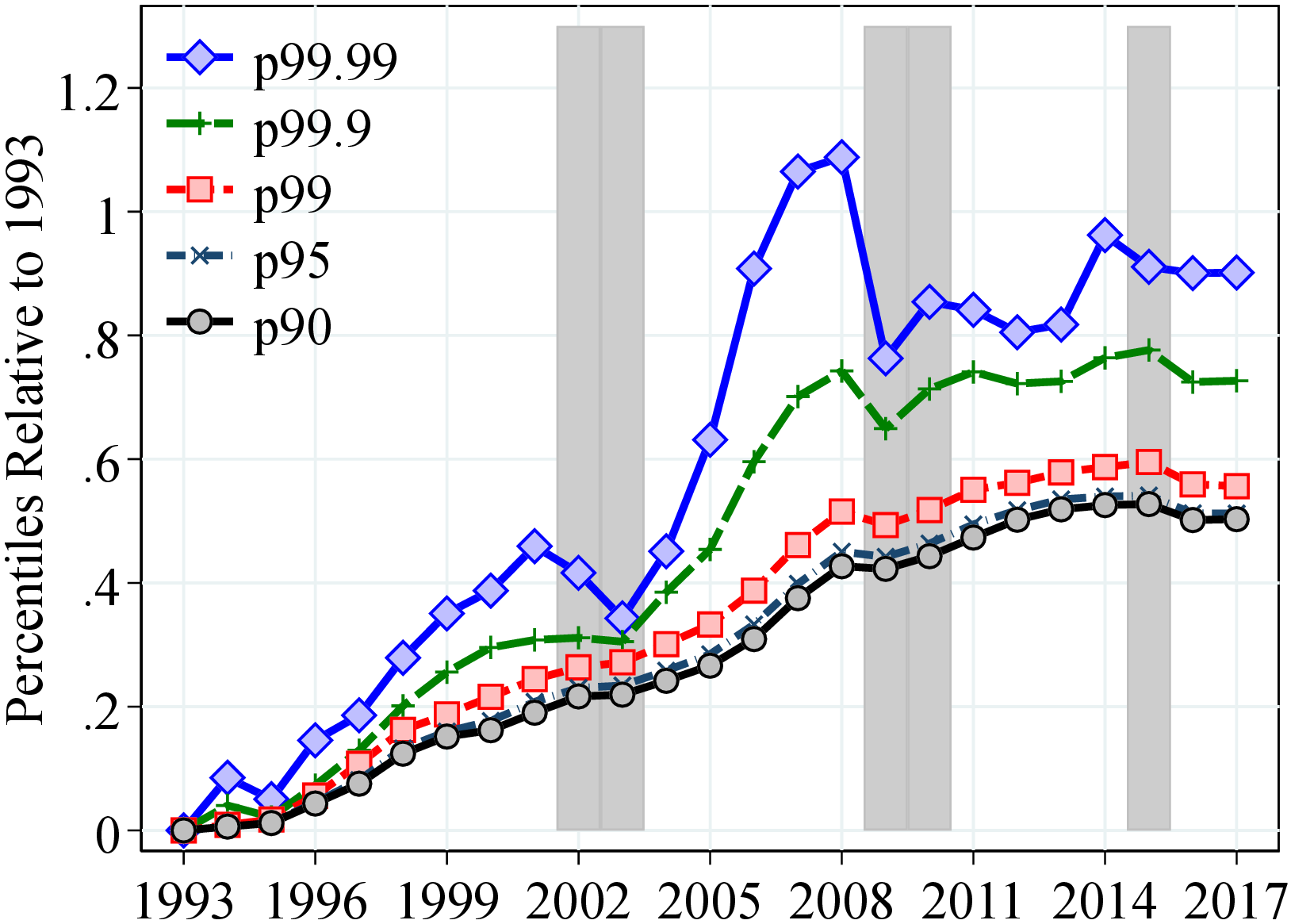

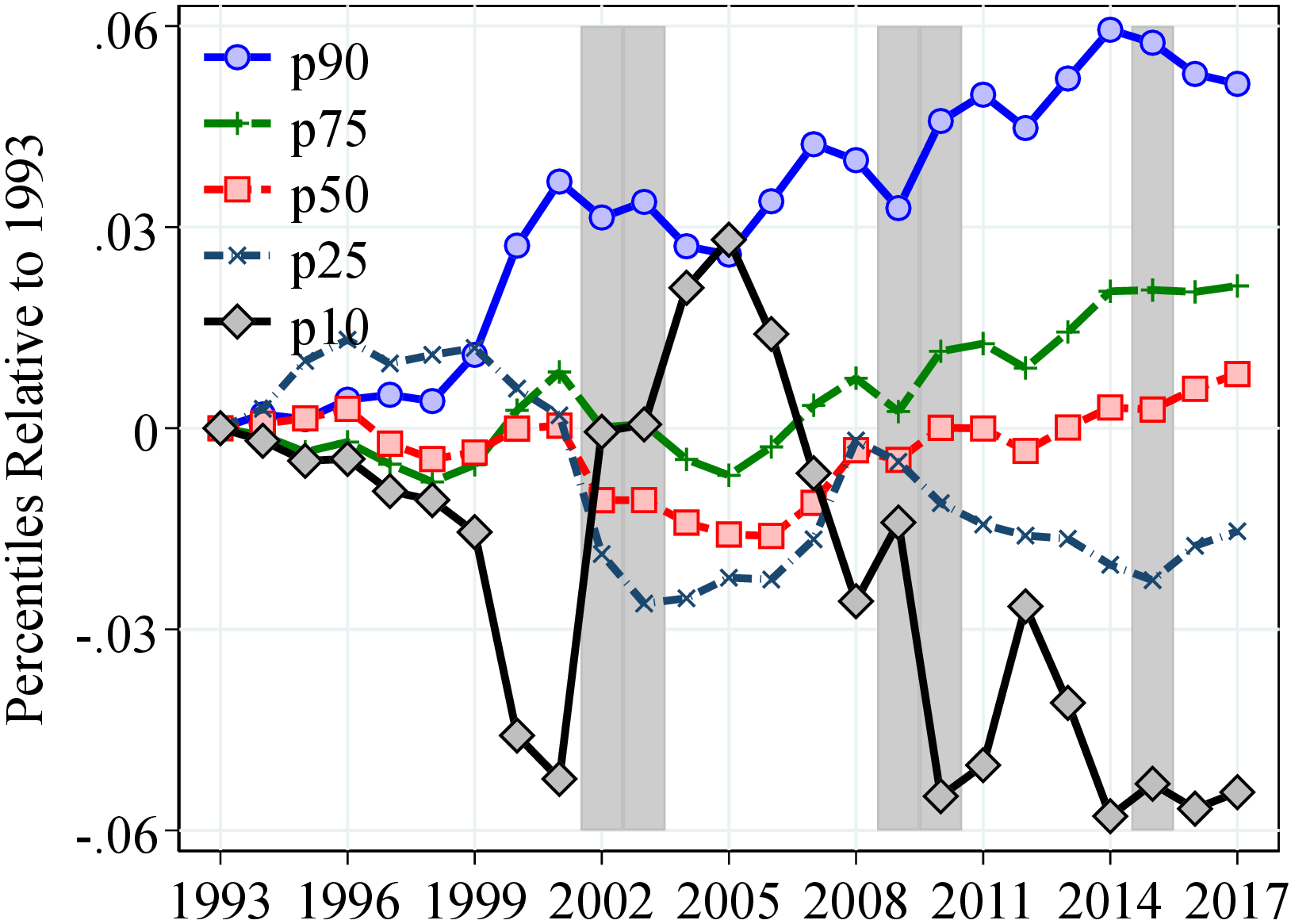

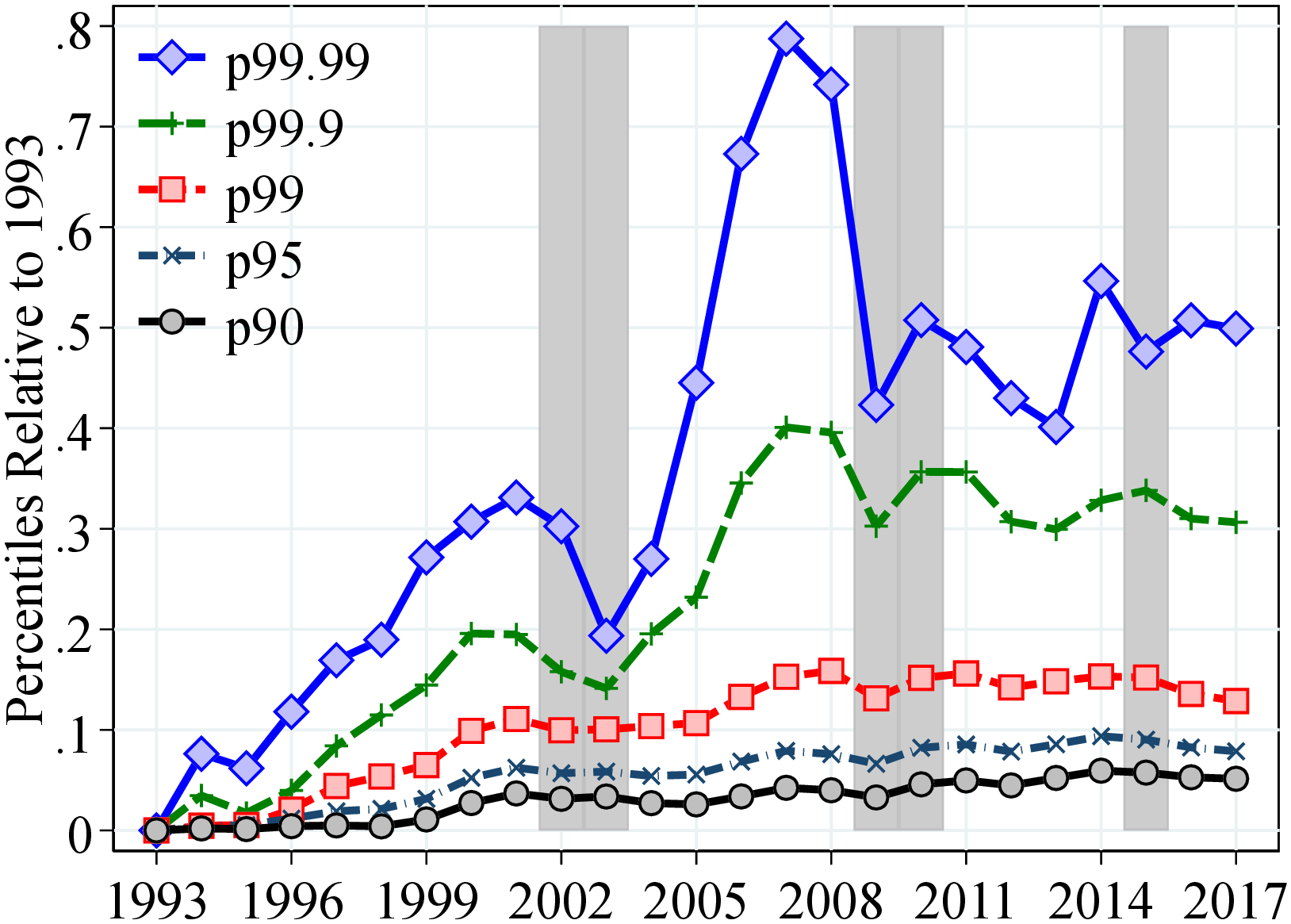

Notes: Figure 2 shows the evolution of the following percentiles of log earnings for men and women: Panels (a) and (b): P10, P25, P50, P75, P90; Panels (c) and (d): P90, P95, P99, P99.9, P99.99. All percentiles are normalized to 0 in 1993. Shaded areas represent recession years which are defined as years with an unemployment growth rate of more than 4 pp. and an output gap of more than 5%. See Section 2 for sample selection and definitions.

Stata Programs for the GRID Database. To ensure the harmonization of the statistics in the GRID database, Ozkan and Salgado (2022) provide a set of Stata programs that can be easily implemented using any panel data on earnings with only minor adaptations. The common set of results presented in this issue of the journal is generated by these programs.

3 Earnings Dynamics in Norway

3.1 Earnings Inequality

We begin our analysis with the evolution of the earnings distribution (above \(Y_{t}^{min}\)) between 1993 and 2017. We also comment on longer-run trends from our 1967-2017 sample by referring to the corresponding figures in Appendix A. Throughout the paper, we present results for men and women separately (see Appendix B.2 for the results from the combined sample). The results in this section are for raw earnings without controlling for changes in educational attainment or the age composition of the population. We find qualitatively similar patterns if we control for these observable characteristics of workers (see Appendix B.3), which suggests that compositional changes are not likely to be the main driver of the evolution of earnings distribution over our sample period.

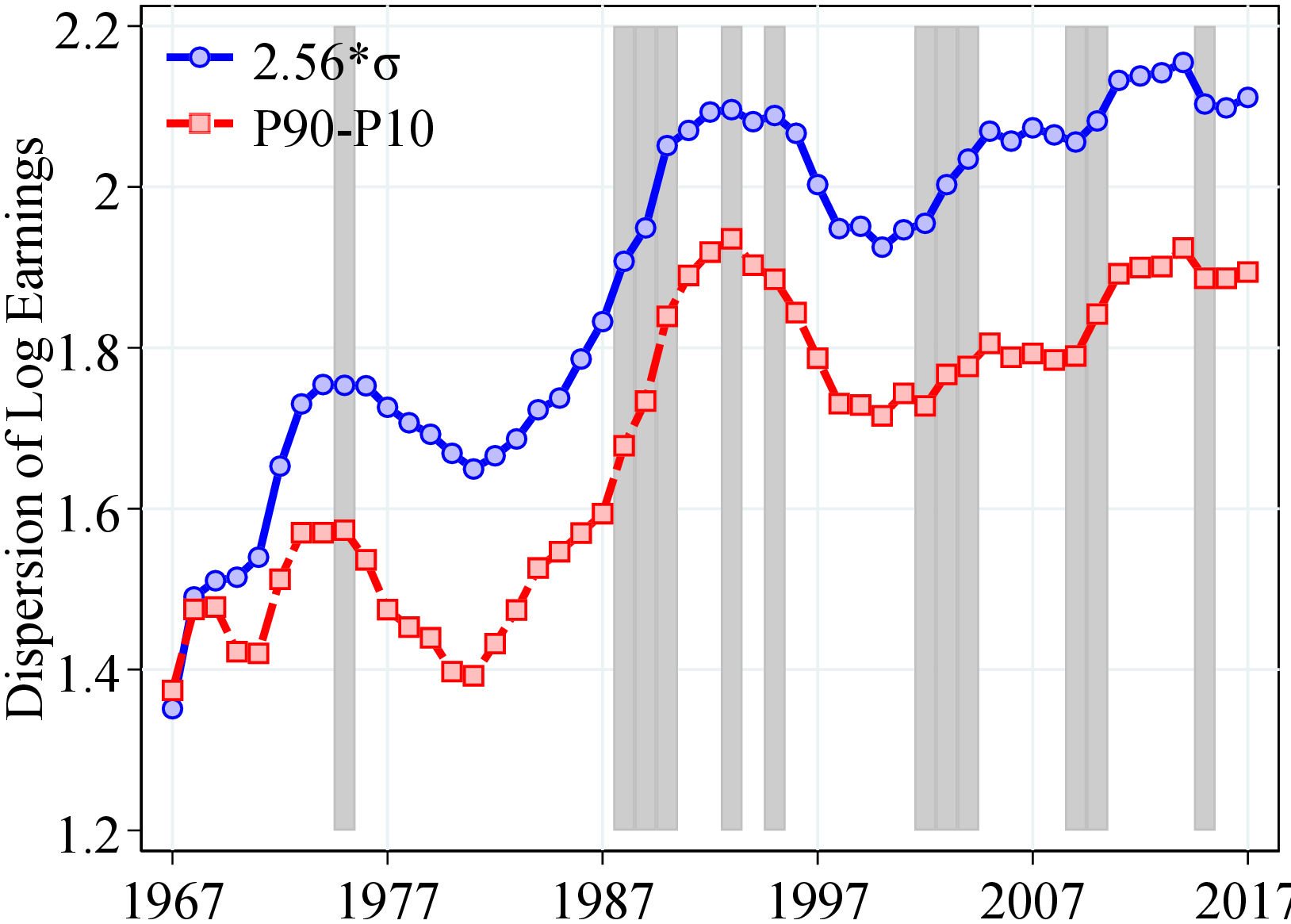

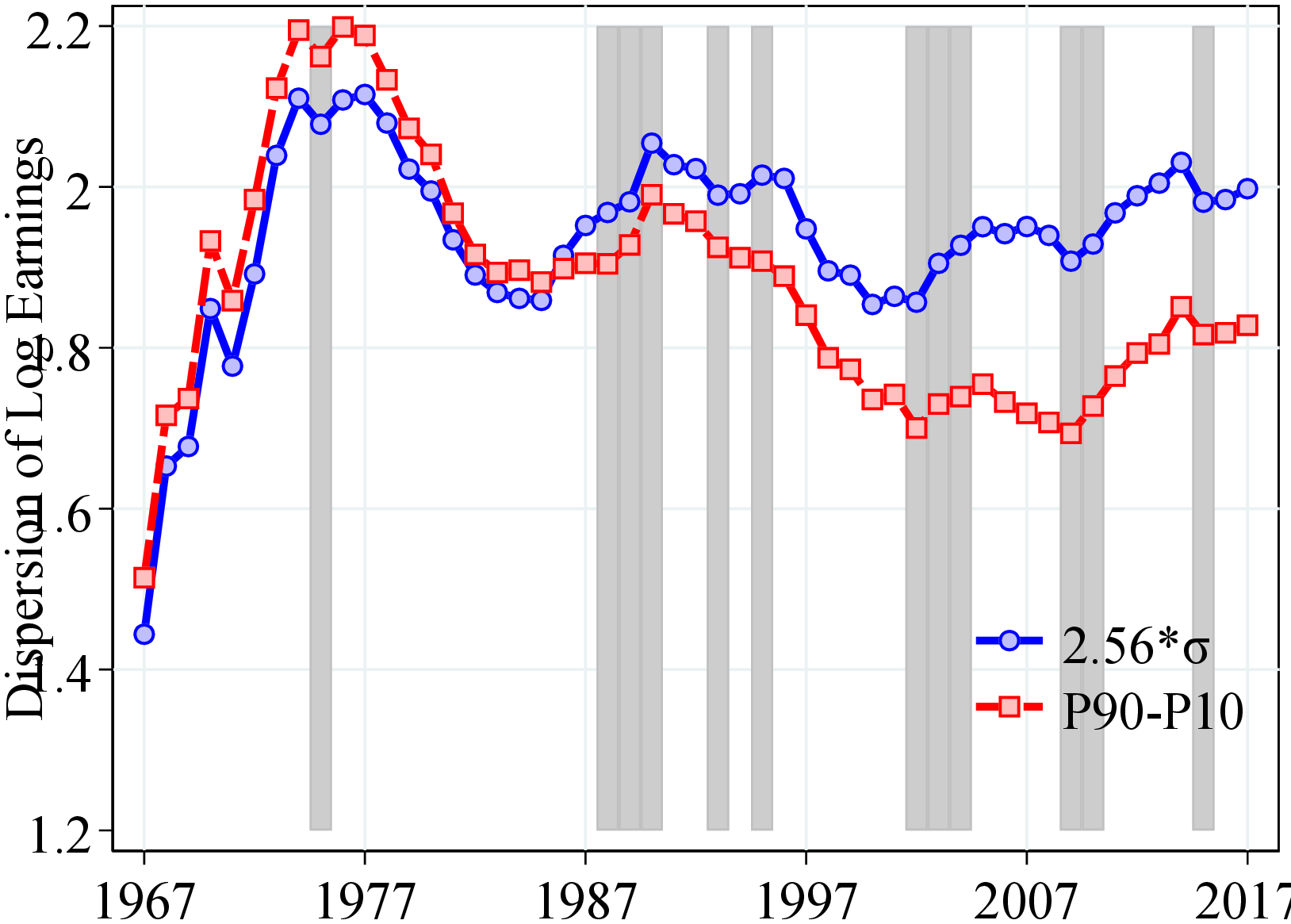

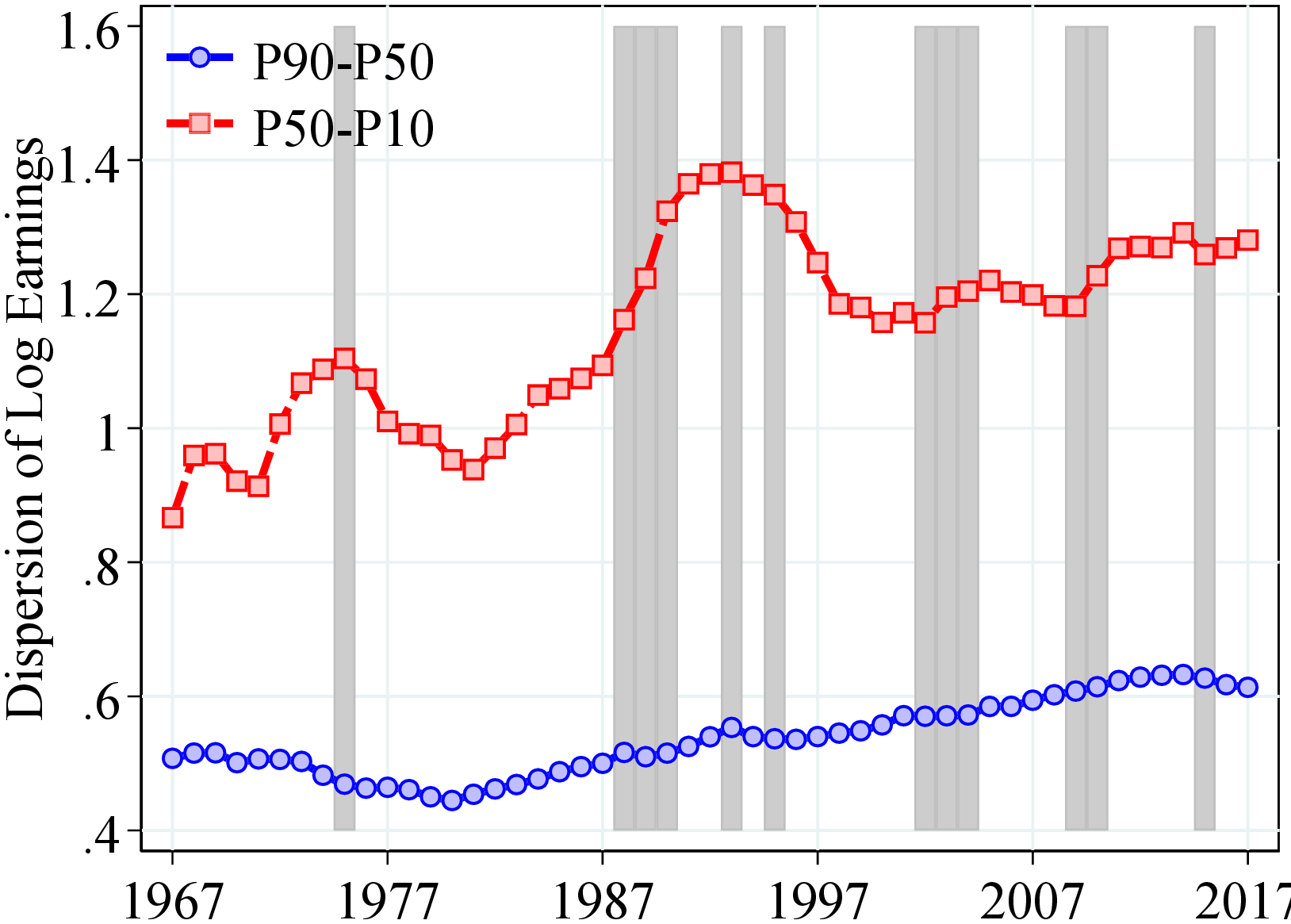

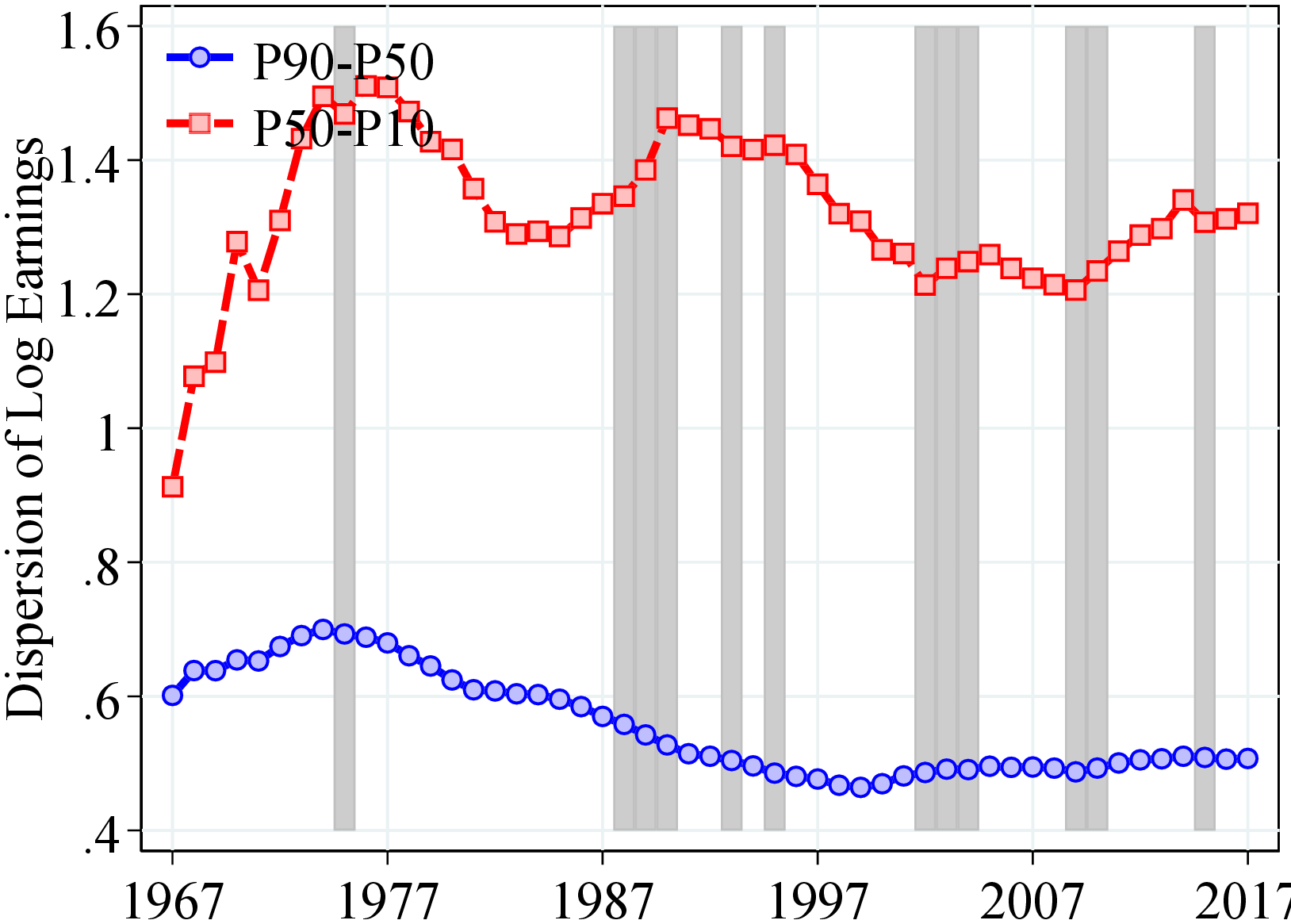

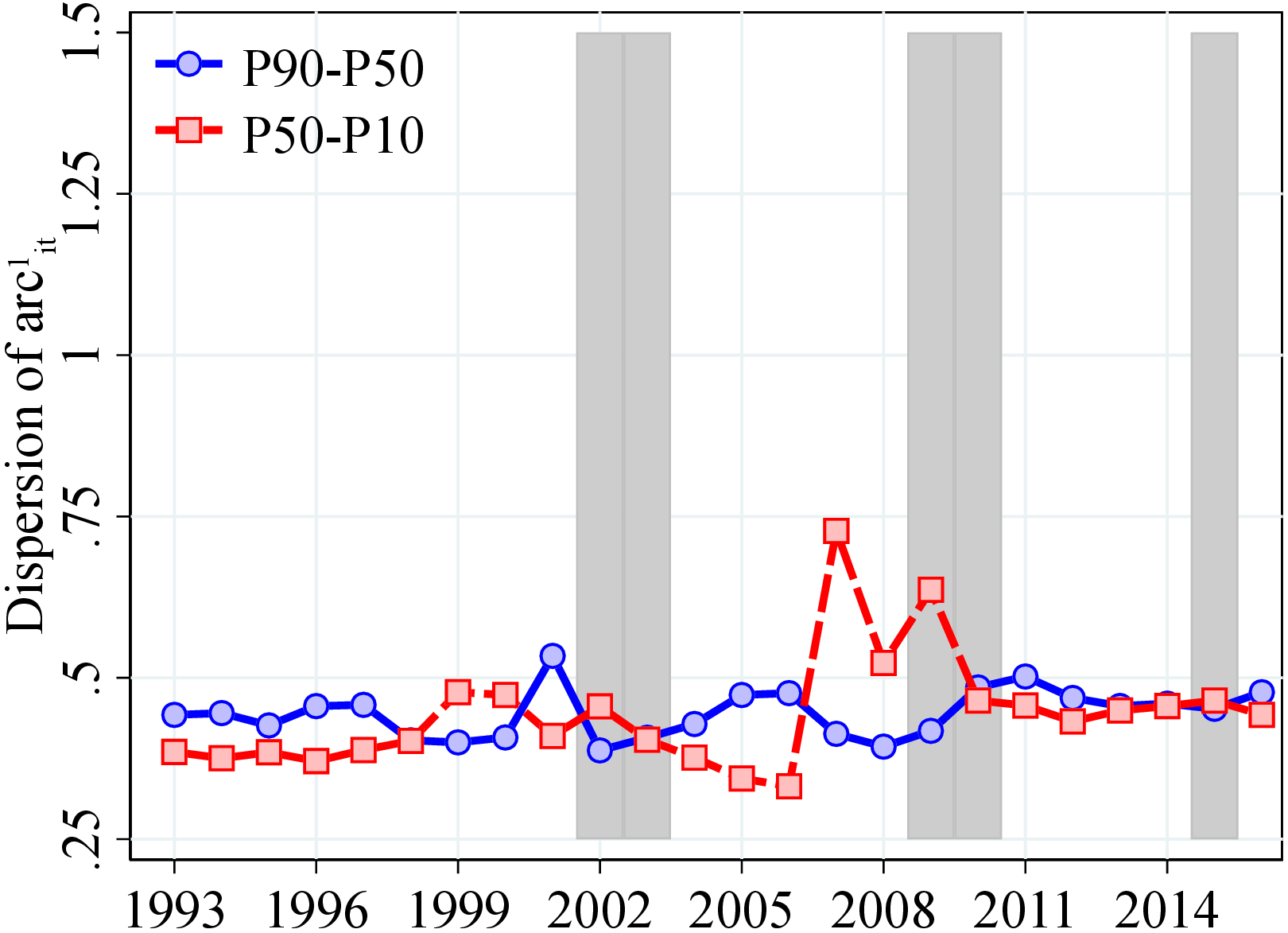

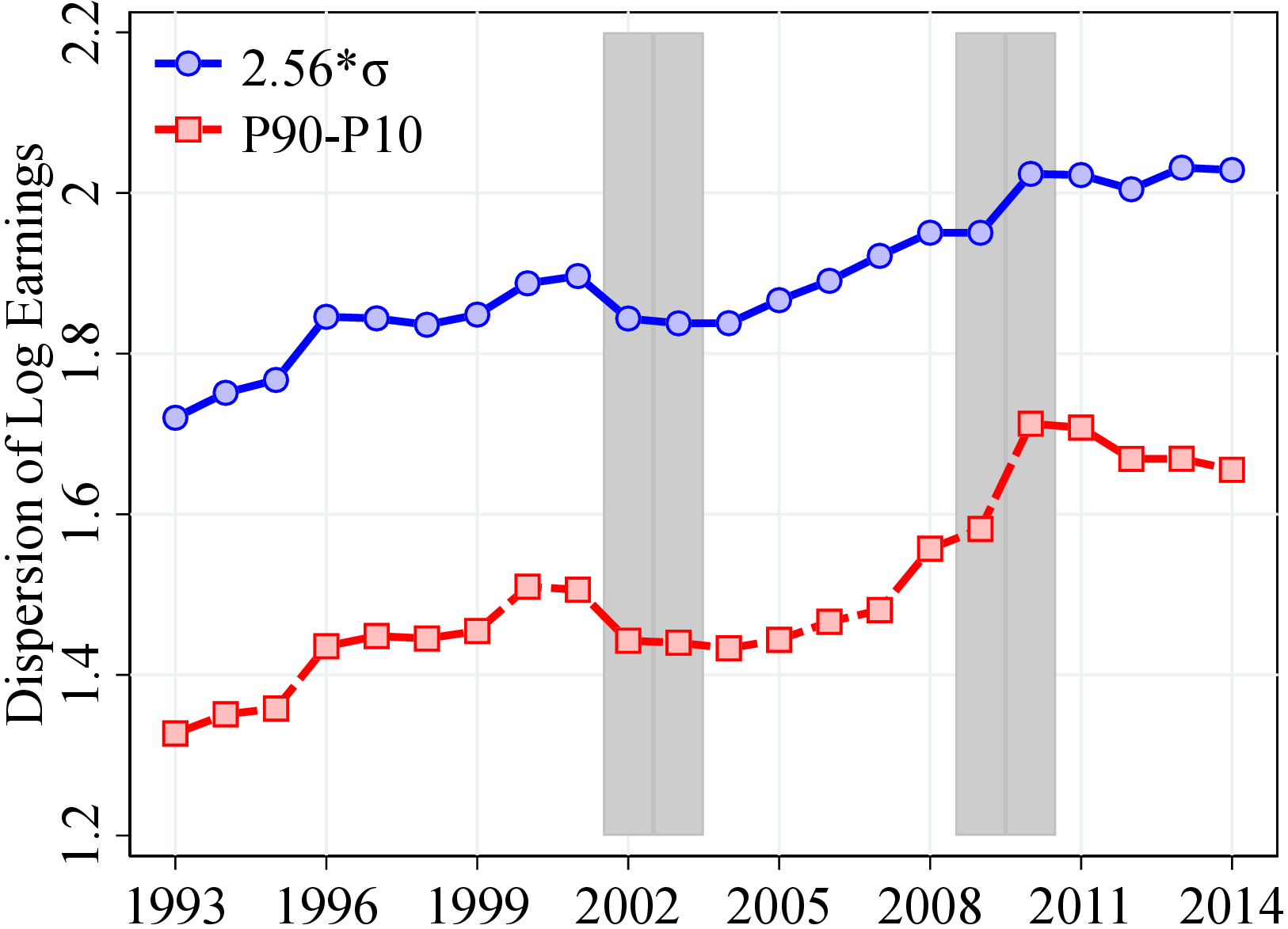

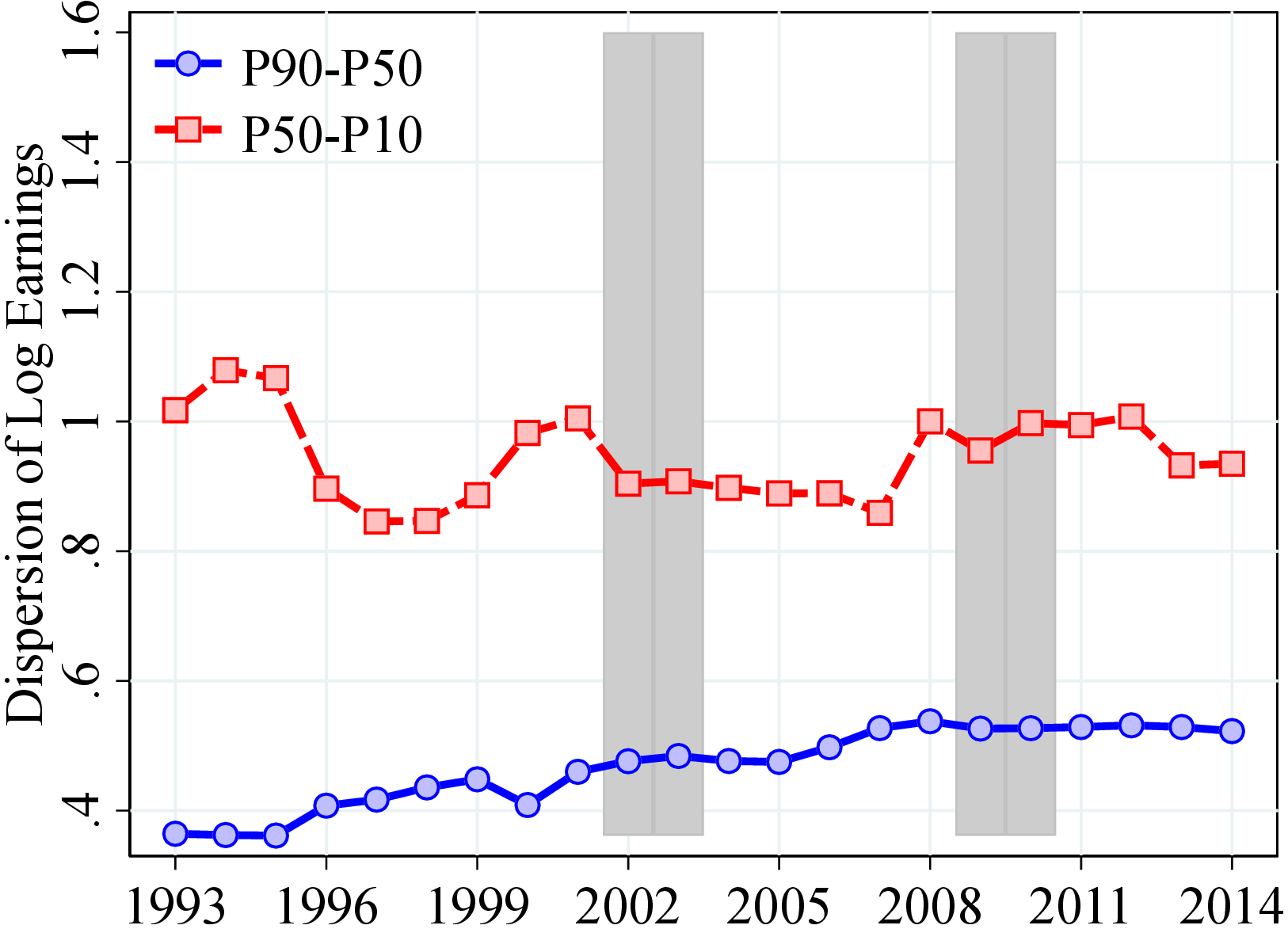

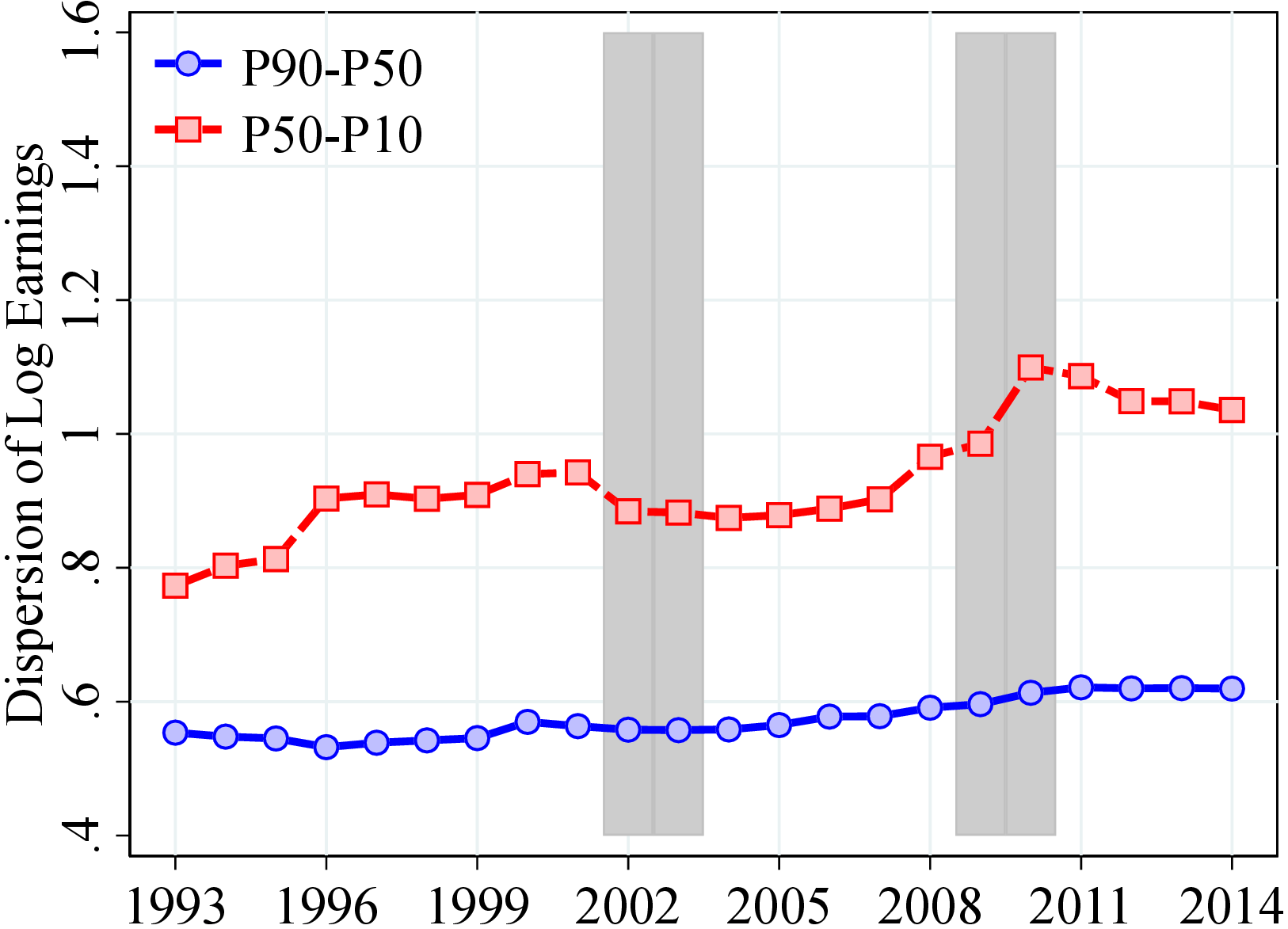

Similar to other Scandinavian countries, Norway has a relatively compressed earnings distribution compared to other developed economies. For example, the spread between the 90th and 50th percentiles (hereafter, P90-P50) and between the 50th and 10th percentiles (P50-P10) of log labor earnings for men is on average 55 and 115 log points over our sample period (Figure B.1), respectively, compared to 100 and 150 log points for a similar sample from the U.S. in 2010 (see Guvenen, Ozkan and Song (2014)). Employing a similar sample selection and methodology, Friedrich et al. (2021) and Leth-Petersen and Saverud (2021) find roughly similar levels of inequality for Sweden and Denmark, respectively. The earnings distribution for women is relatively more dispersed than for men, mainly because of the higher inequality below the median (e.g., the P50-P10 for women is around 140 log points versus 115 log points for men).

In 1993, Norway was emerging from a severe banking crisis (see Gerdrup et al. (2004)) and entering a period of relatively strong growth, partly because of high oil prices (see Bjornland and Thorsrud (2016)). Until the Great Recession, the earnings of men grew steadily at a similar pace except for those above the 90th percentile, who enjoyed relatively steeper growth (Figures 2a and 2c). This steady growth is roughly a continuation of a longer-run trend since the 1970s except for low earners, who saw large losses during the 1991 recession (Figure A.2).6

During and in the aftermath of the Great Recession, however, this stable earnings growth either halted or significantly slowed down for most workers, and earnings inequality grew noticeably (Figure B.1). For example, between 2008 and 2017, incomes between the 90th and 50th percentiles grew by a mere 5 log points, whereas the 10th percentile declined during this 10-year period (Figure 2). These concerning developments are partly because of a sharp drop in oil prices from 2014 to 2015, which hit the oil-rich Norwegian economy and caused another recession in 2015.

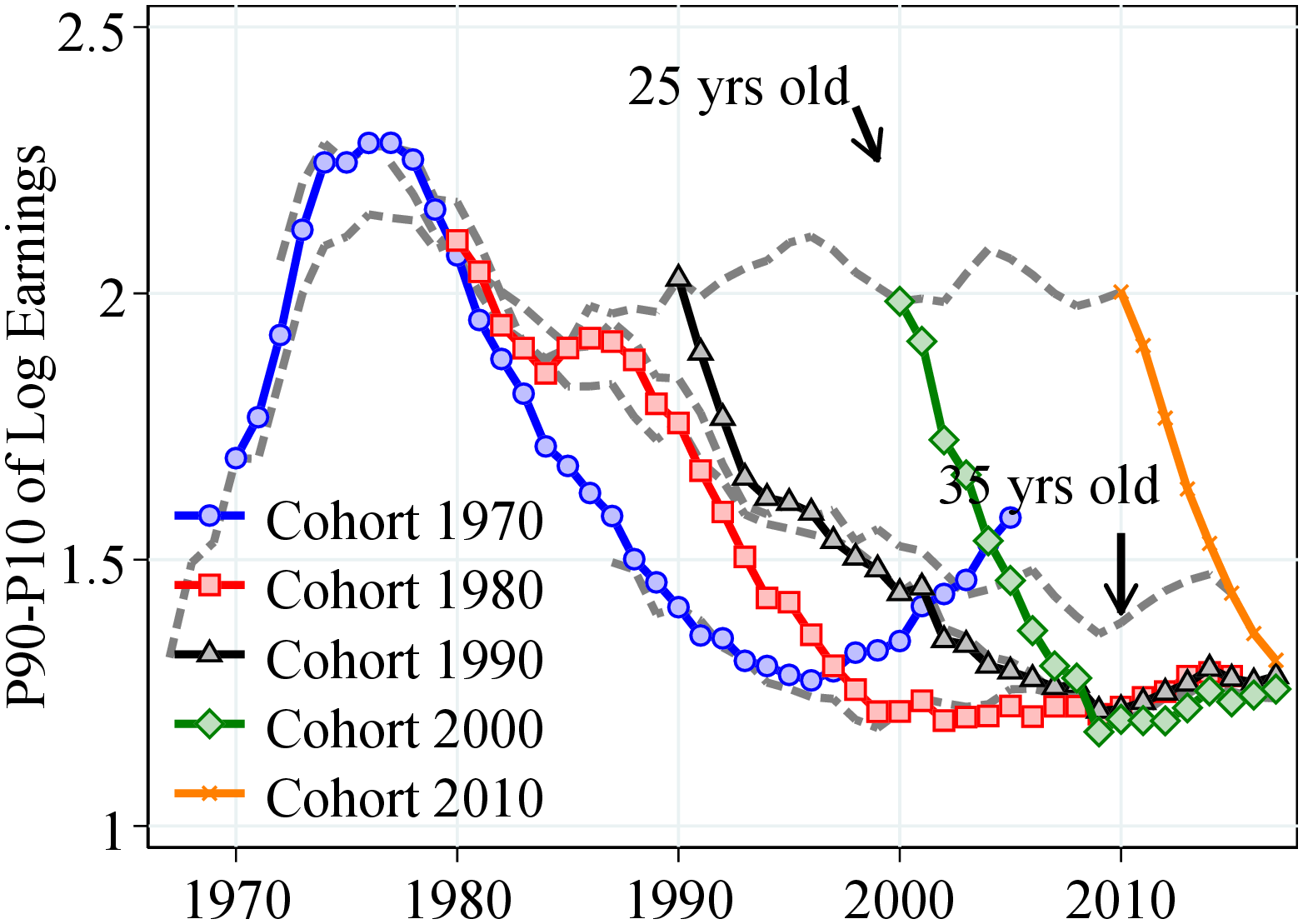

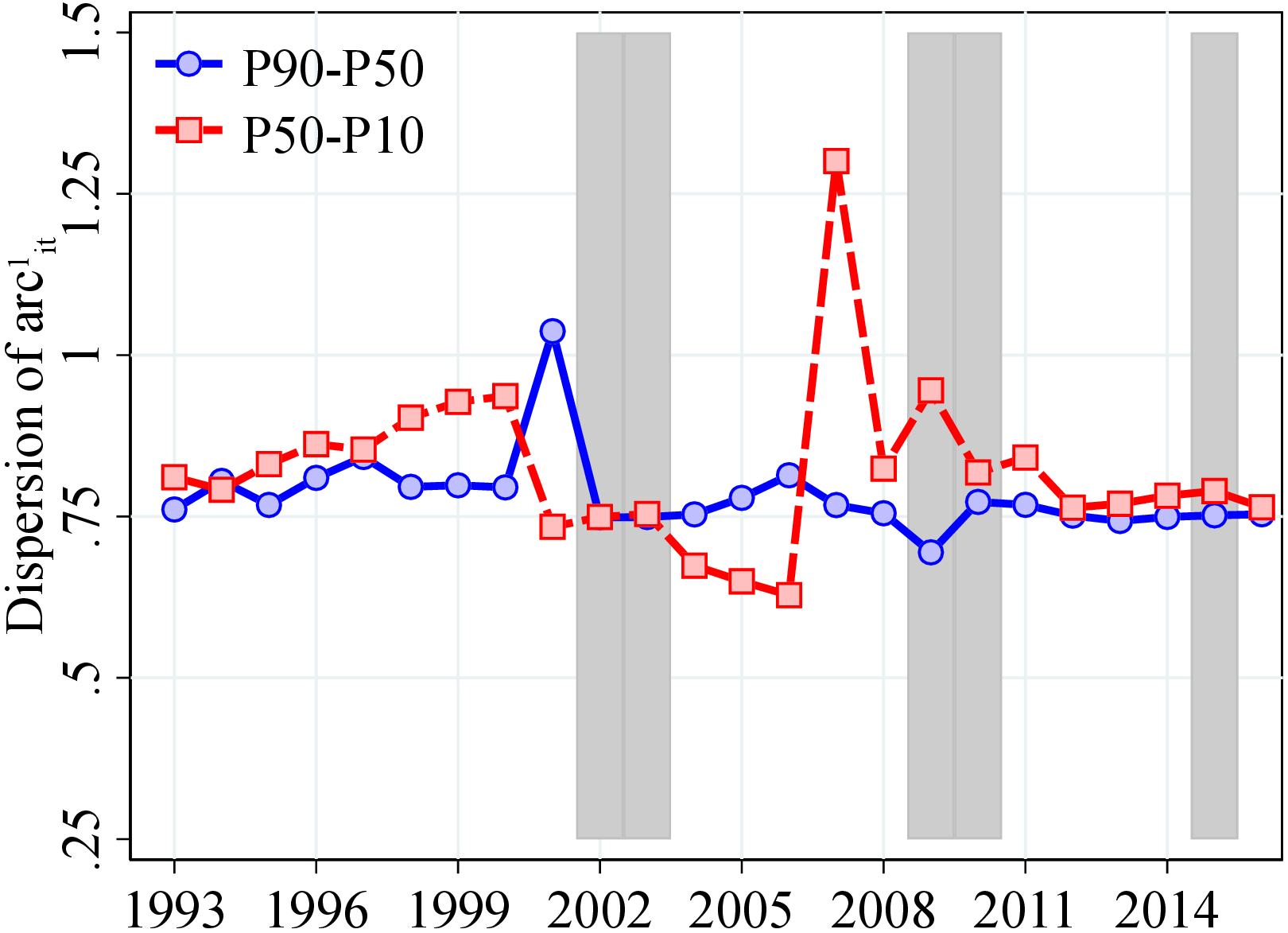

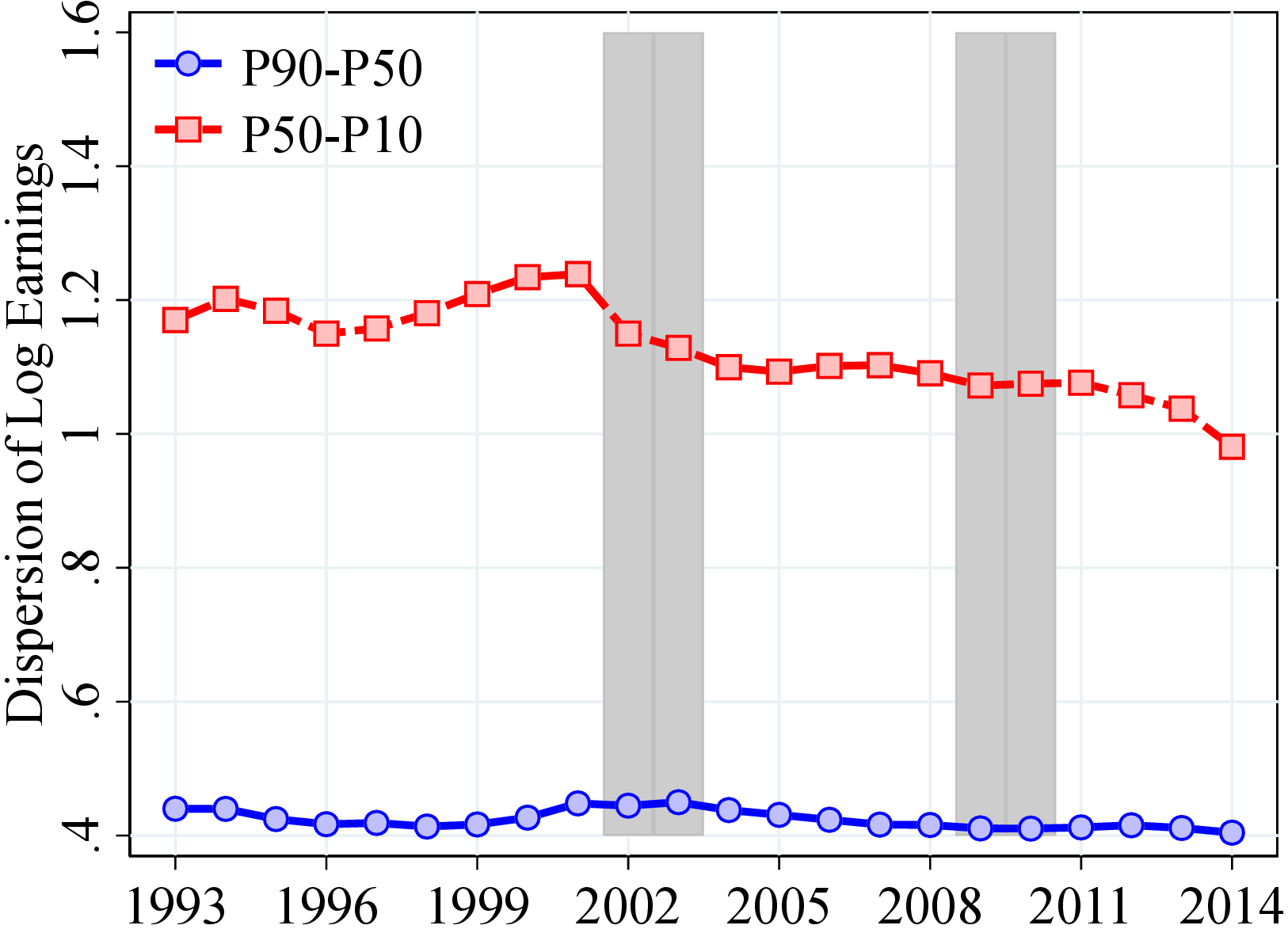

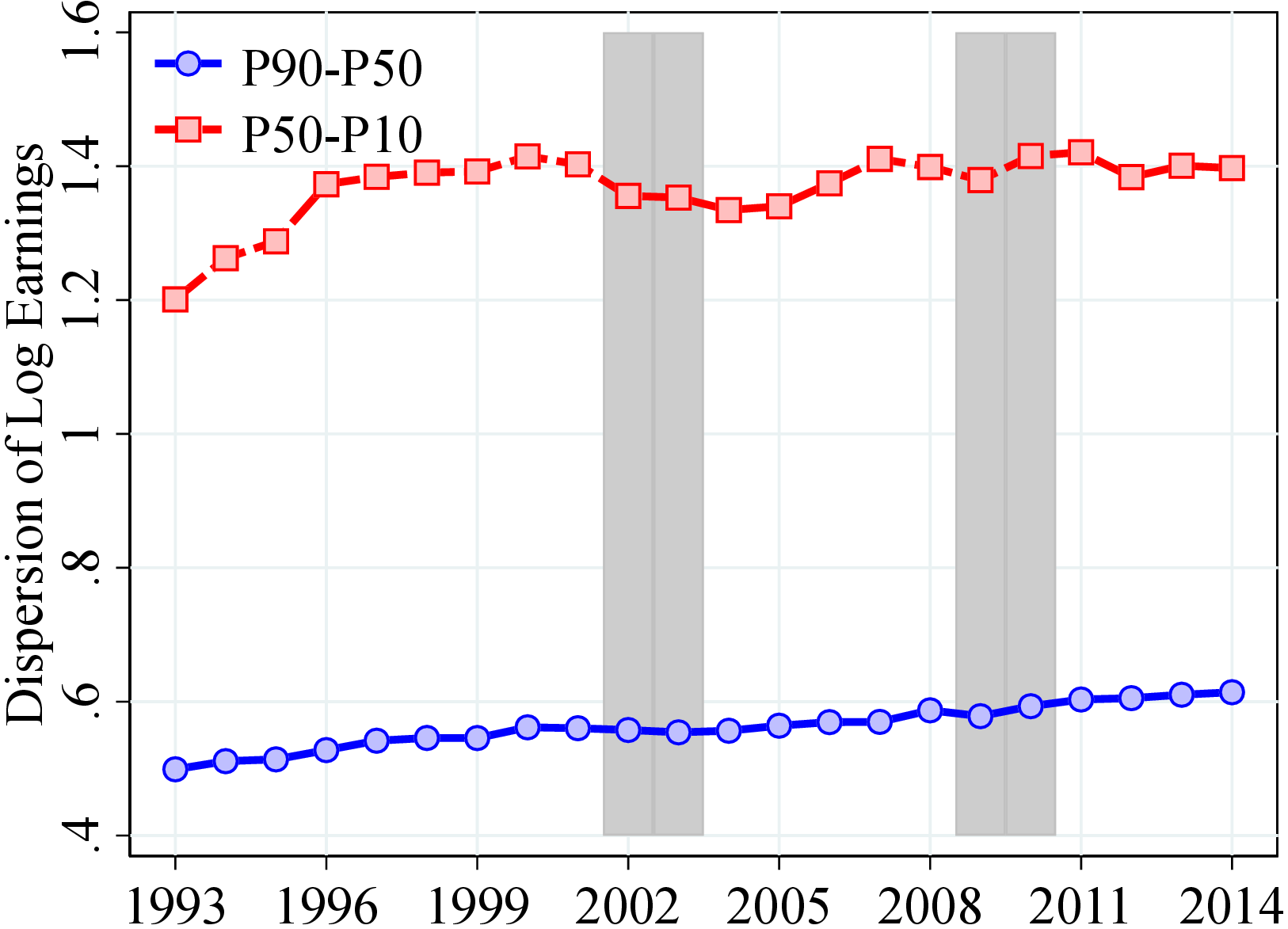

Similar to men, women in the bottom 90th percentile experienced steady earnings growth of around 40 to 50 log points between 1993 and 2008 (Figure 2b). After 2008, income growth slowed down for everyone but more so at the bottom of the distribution, thereby increasing P50-P10, albeit to a smaller extent than for men (Figure B.1). These trends are broadly in line with those from the after-transfer income, with the key exception that after-transfer income in the bottom 10% has grown faster after the banking crises of the early 1990s (Figures A.2b and A.3b), which then led to a significant reduction in inequality until the early 2000s. Furthermore, the P90-P10 of log after-transfer income reveals a slow long-run trend of decline, starting in the mid-1970s when the labor force participation of women started increasing steeply (Figure 1c).7

Interestingly, earnings in the top 10% evolved differently from the rest of the distribution until 2008 as they grew faster and more unequal, albeit to a lesser extent than seen for the U.S. or the U.K. (Figures 2c and 2d). For example, male workers at the 90th percentile in 2008 earn 53% (43 log points) more relative to 1993, whereas the earnings of those at the 99th, 99.9th, and 99.99th percentiles grew by around 75%, 120%, and 230%, respectively (Figure 2c).8 However, after 2008, high-earnings men experienced stagnant or shrinking incomes, which also led to a slight decline in top income inequality. For women, however, top income growth has not slowed as much after 2008, and inequality has continued to increase, albeit at a slower pace.9

Inequality within Public and Private Sectors. Income inequality in the private and public sectors has evolved quite differently over the last 20 years (see Online Appendix A). For instance, the P90-P10 for workers employed in the private sector increased by 30 log points between 1993 and 2014. Among men, most of the increase in inequality is accounted for by an expansion of the left tail of the distribution. For women, the increase in inequality is due to the stretching of both of the tails. In contrast, inequality in the public sector has remained the same among men and declined quite significantly among women, especially after 2001. These results highlight the prominent role that the public sector plays in reducing income inequality in Norway.

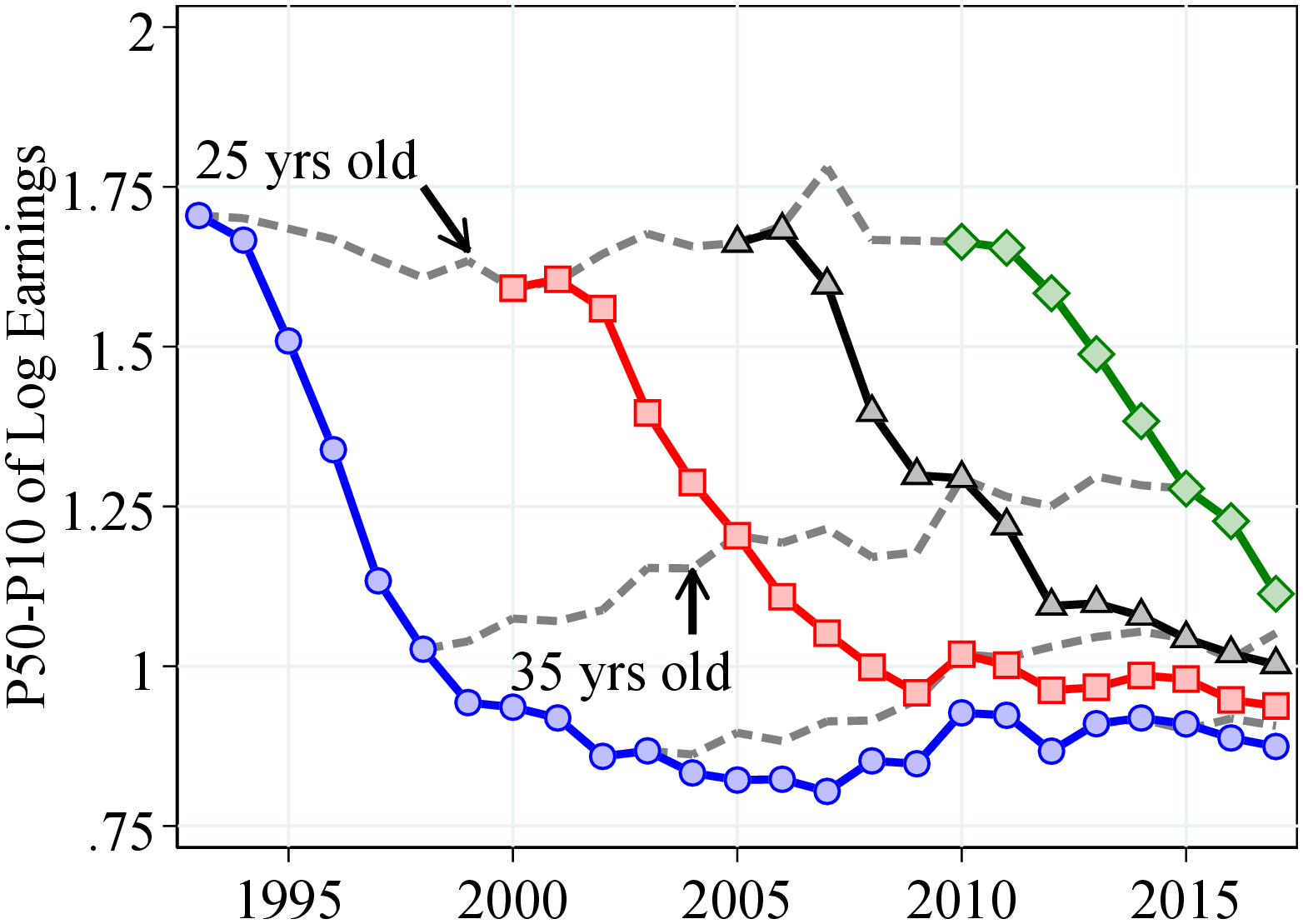

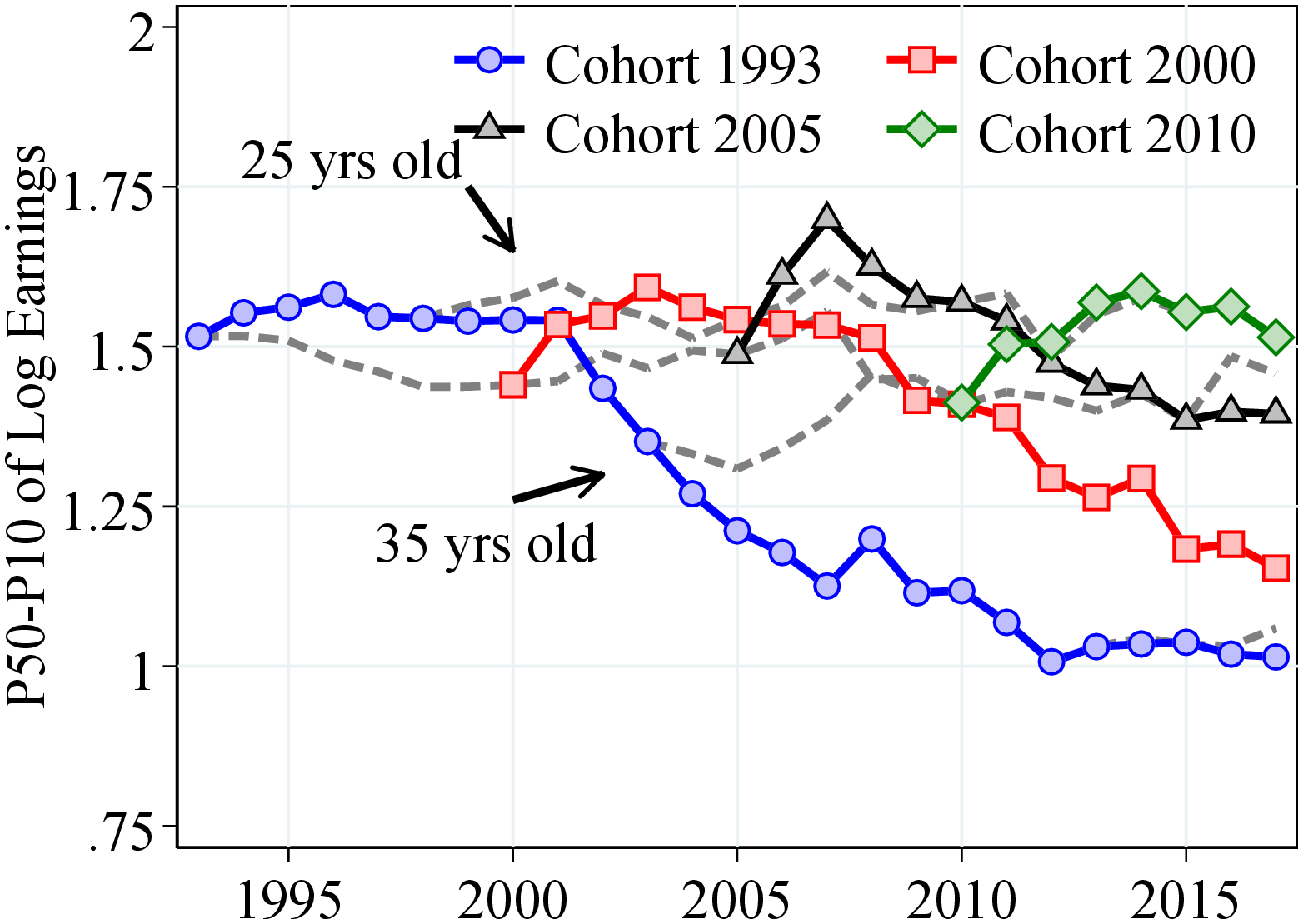

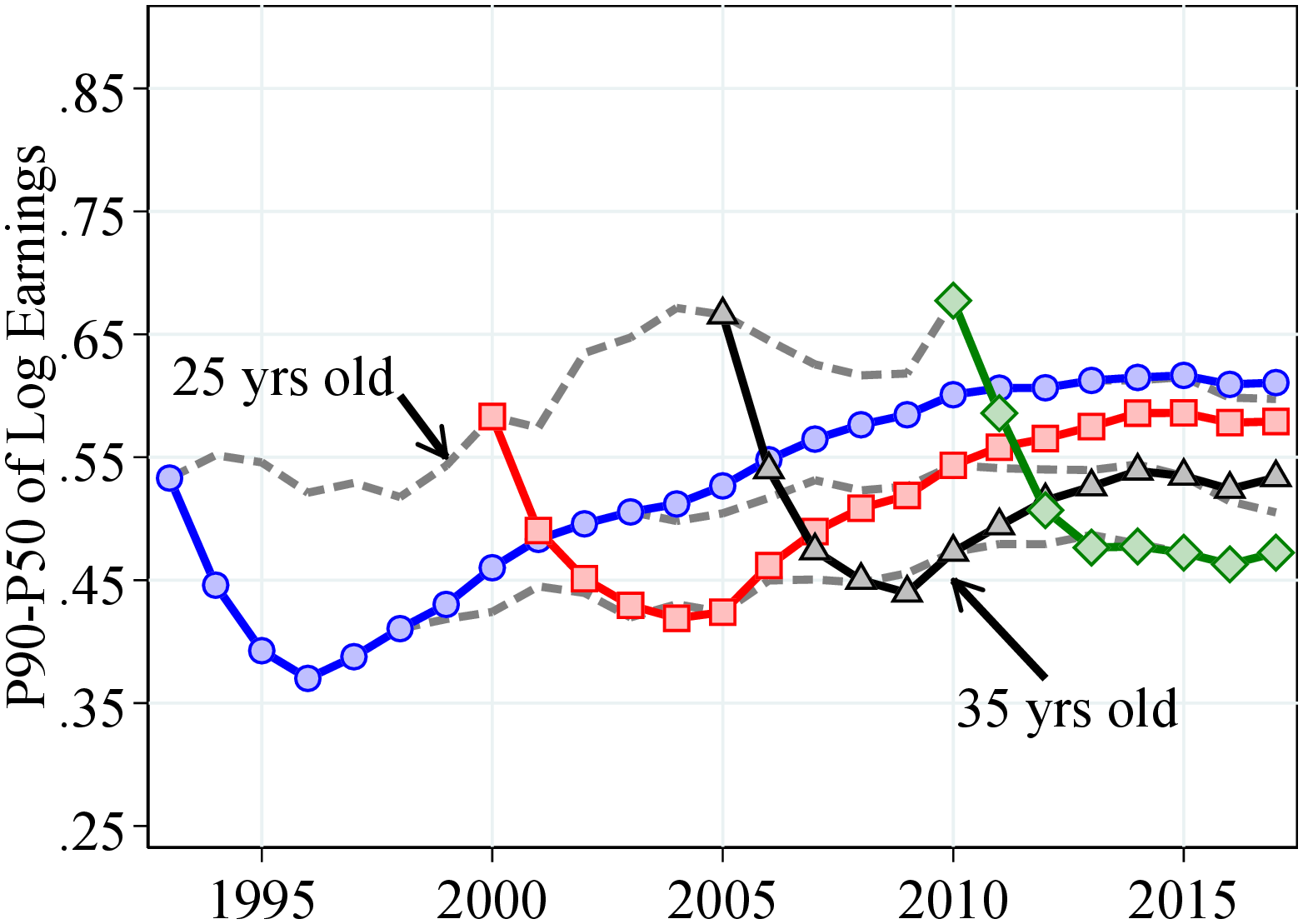

3.1.1 Life-Cycle Earnings Inequality

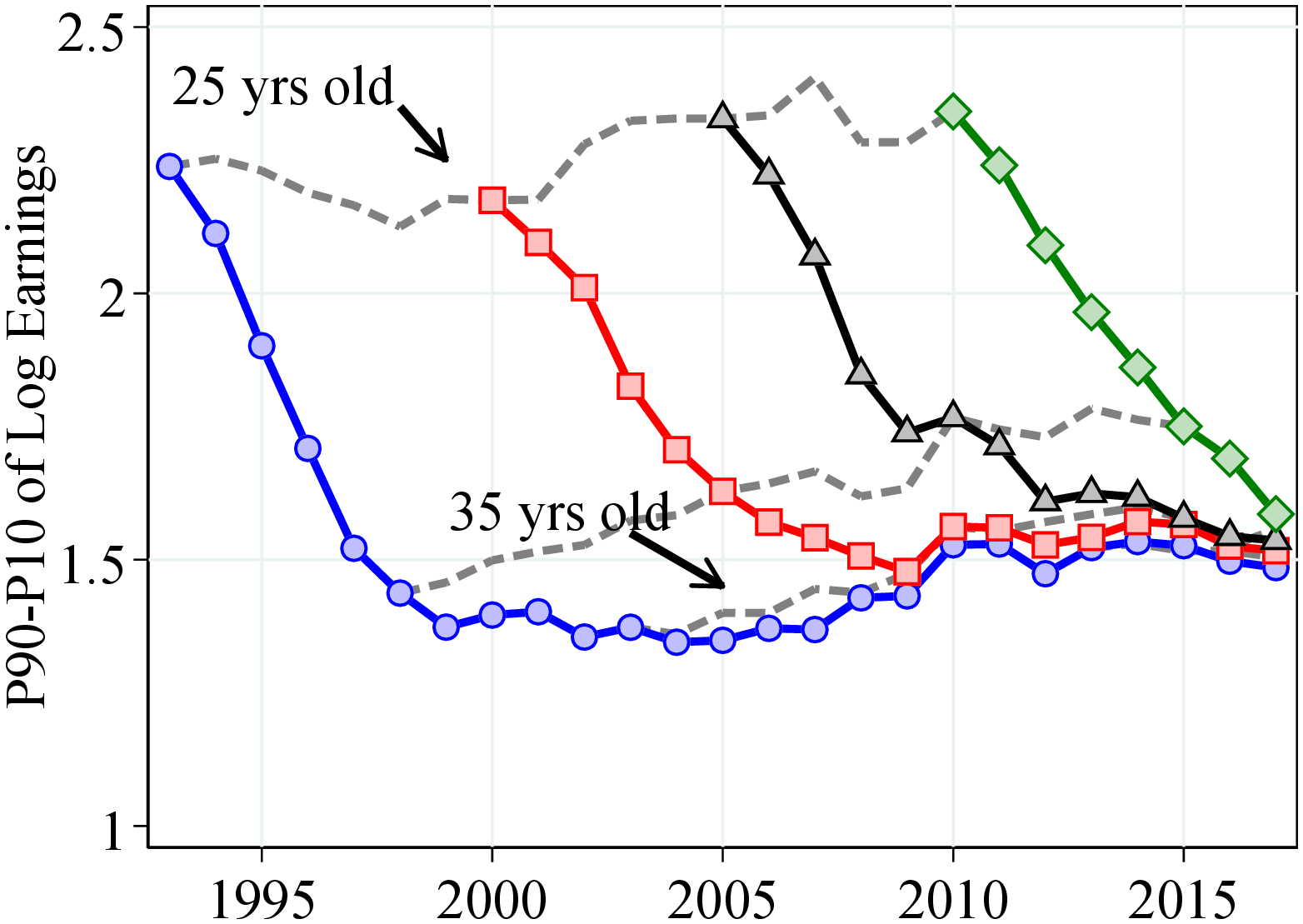

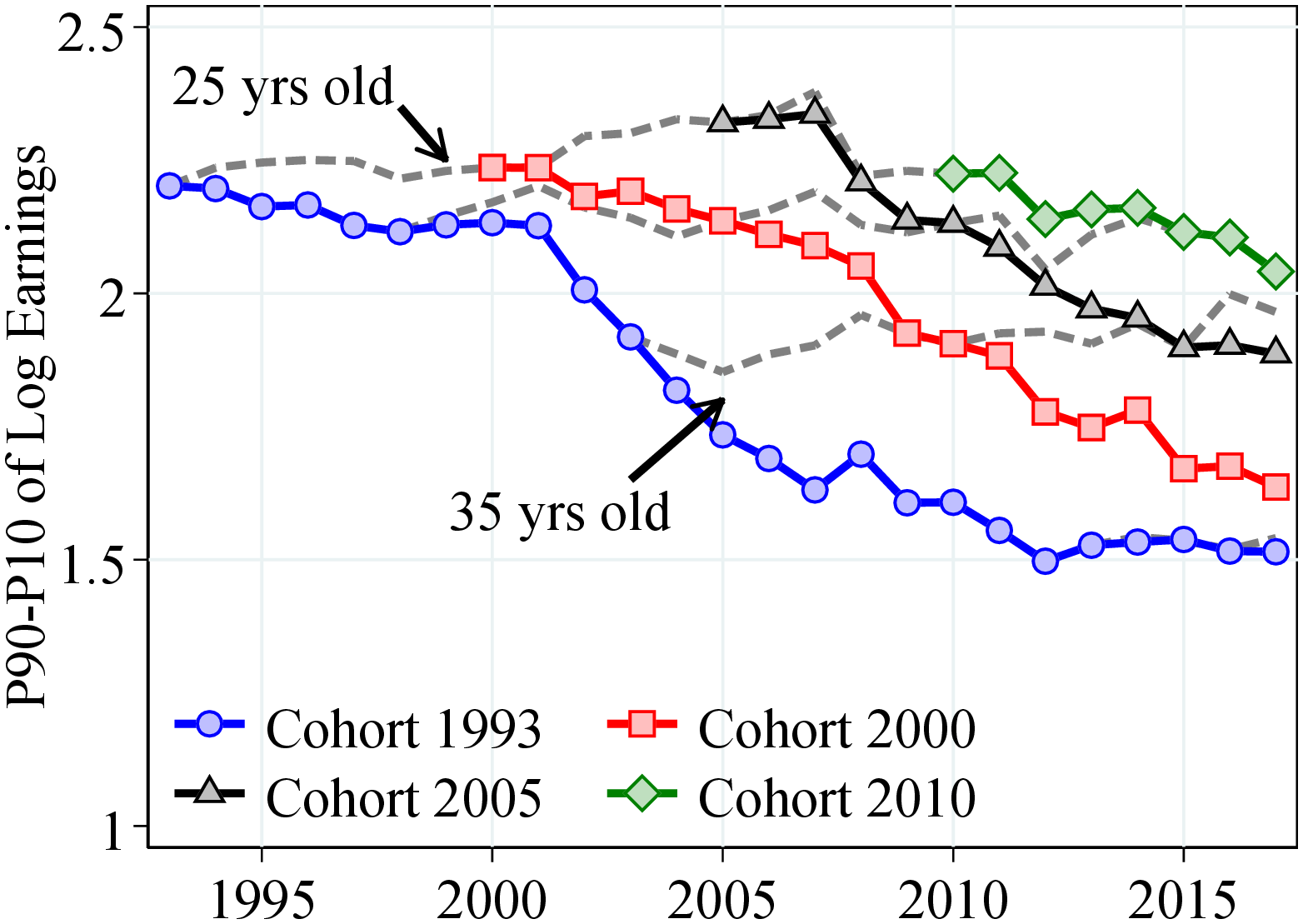

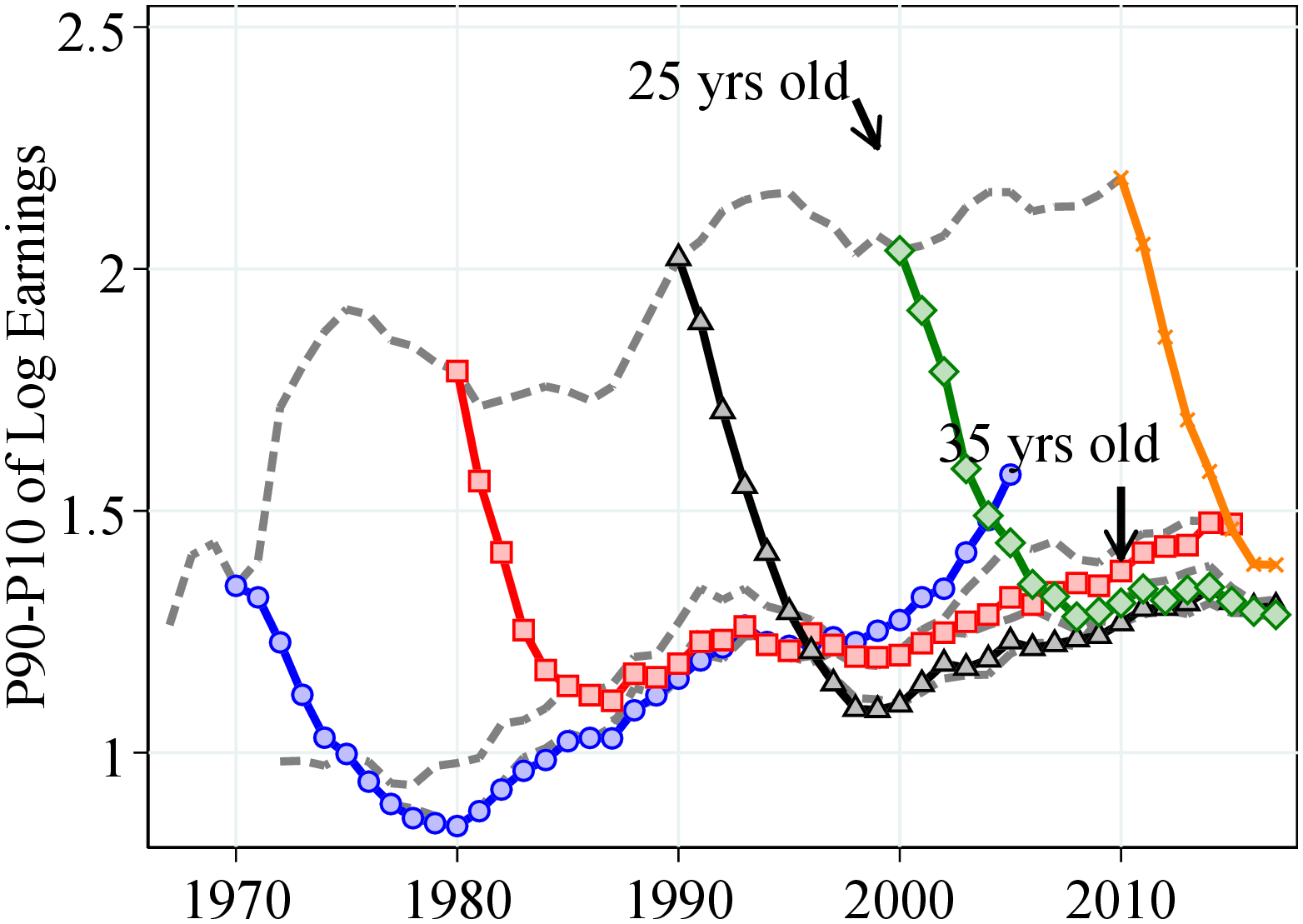

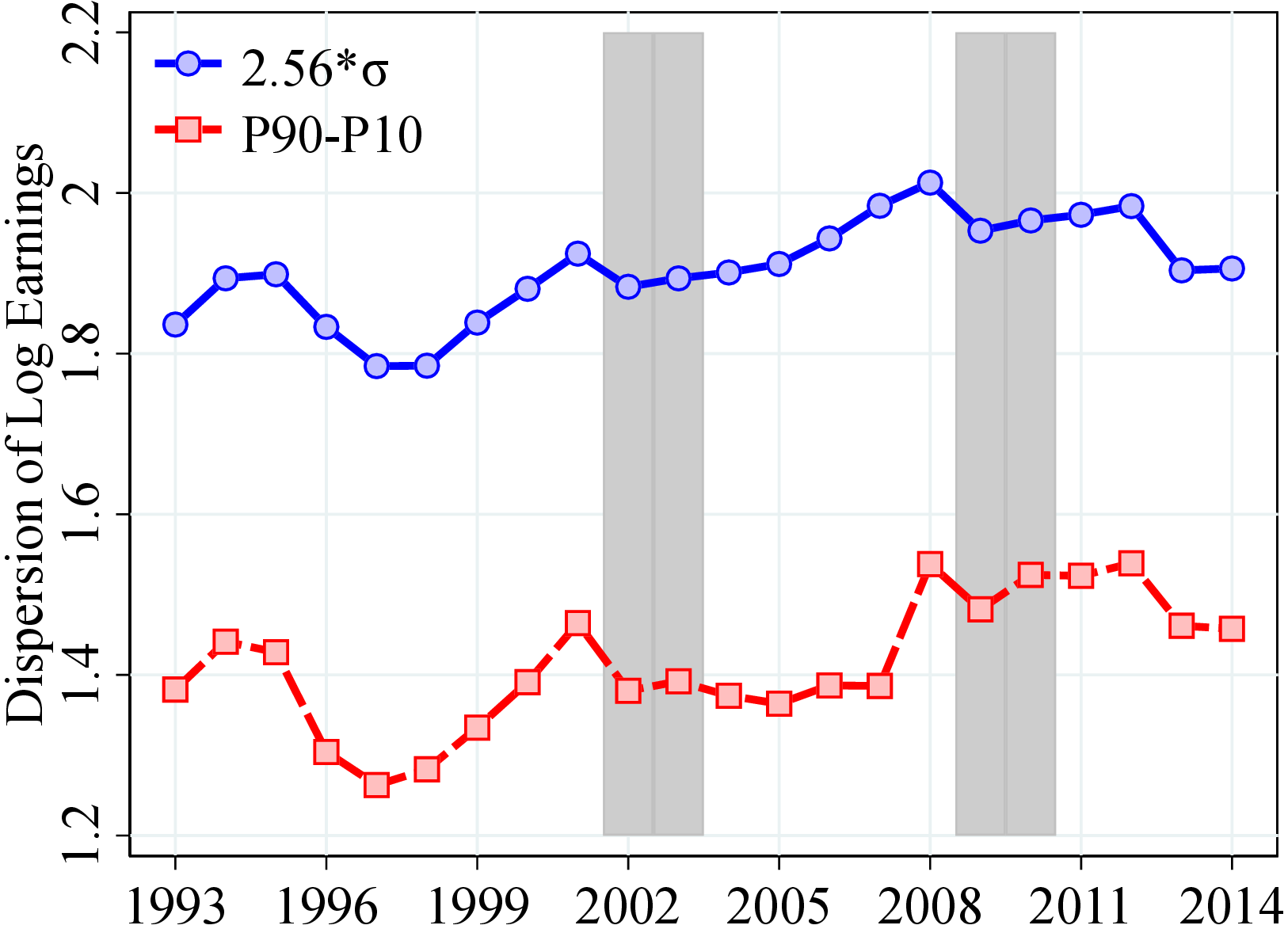

The relatively compressed earnings distribution and the changes in inequality could, in principle, be separated into two components: inequality at young ages and the life-cycle evolution of earnings dispersion. To investigate each component, we document how within-cohort inequality evolves over the life cycle and across different cohorts. Specifically, Figure 3 plots the P90-P10 of log earnings in each age for 18 cohorts of workers entering the labor market at age 25 from 1993 to 2010. The colored markers connect different ages of the same cohort, thus showing how within-cohort inequality evolves over the life cycle. Dashed lines connect the same ages of different cohorts and show how the inequality in a particular age evolves over time.

Notes: Figure 3 shows the P90-P10 log earnings differential over the life cycle for selected cohorts for men and women. A cohort is defined by the year in which the cohort turns 25. Dashed lines connect individuals of the same age. The plots consider cohorts born between 1969 and 1986.

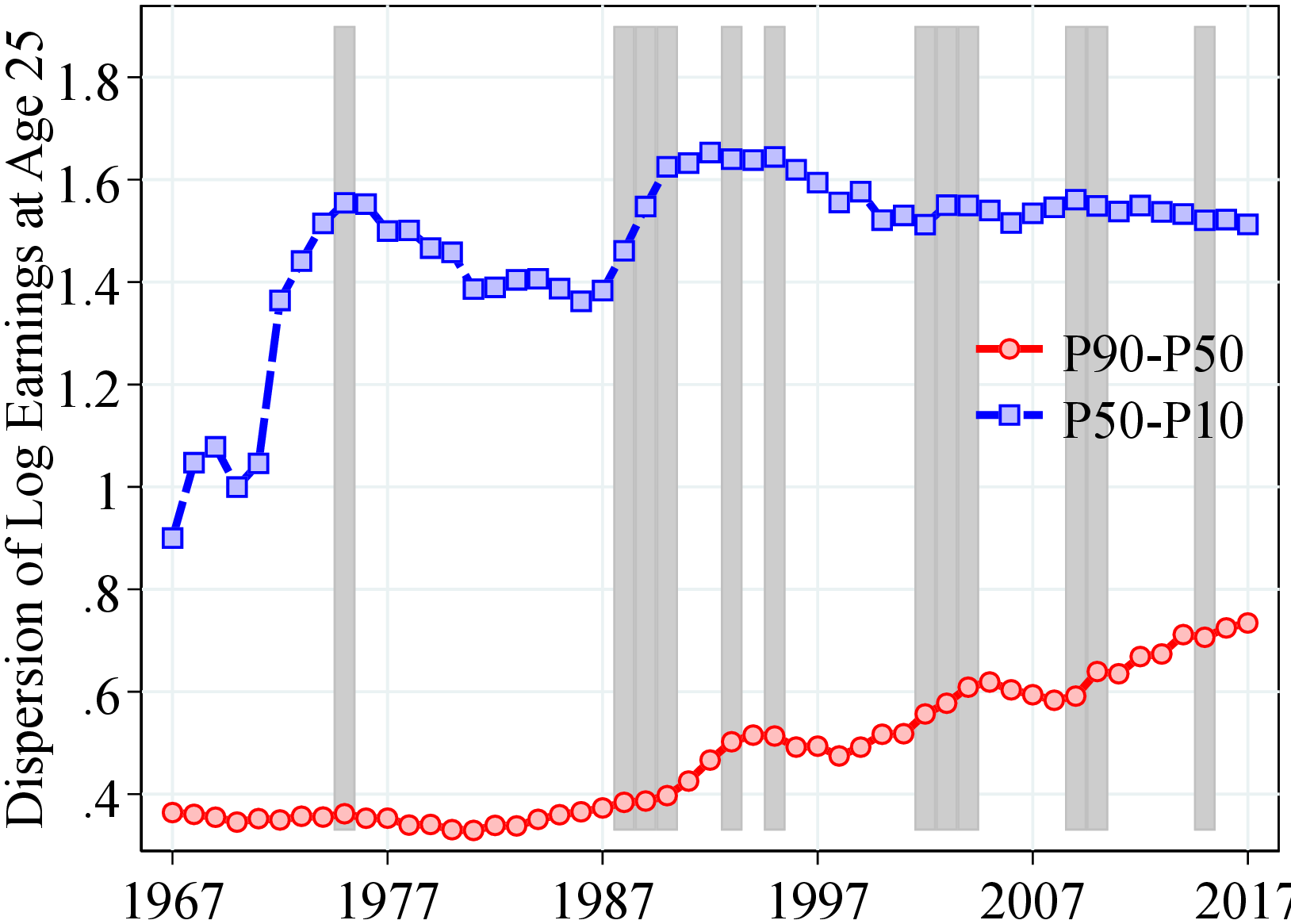

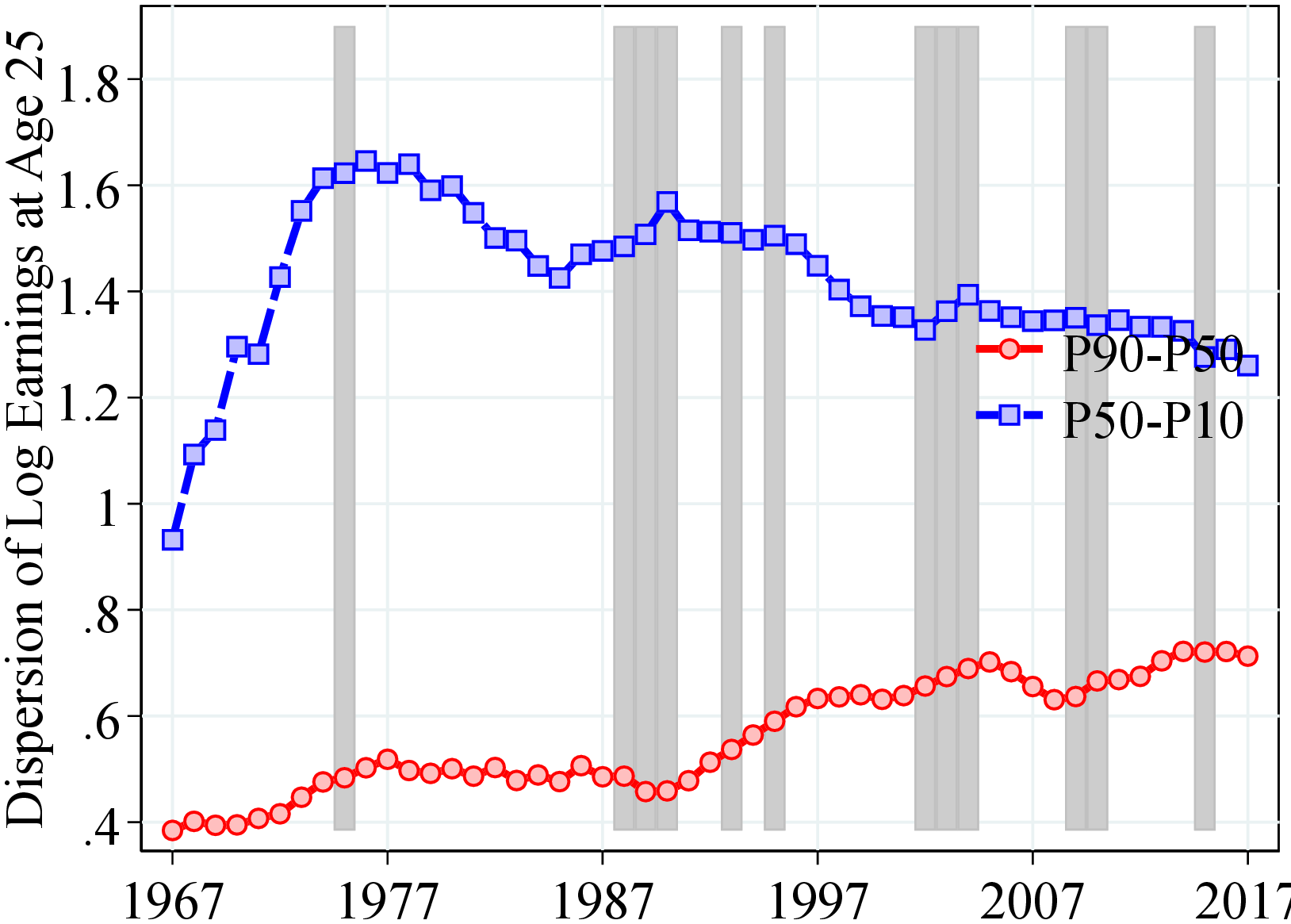

Despite the lower overall earnings inequality in Norway compared to the U.S., initial dispersion at age 25 is relatively high. For example, P90-P10 of log earnings for 25-year-old men is 230 log points in 2010 versus 220 log points for the U.S. (Guvenen et al. (2018)). In fact, initial dispersion in Norway is significantly higher compared to several other countries, for example, Sweden (Friedrich et al. (2021)), Denmark (Leth-Petersen and Saverud (2021)), and Canada (Bowlus et al. (2021)).

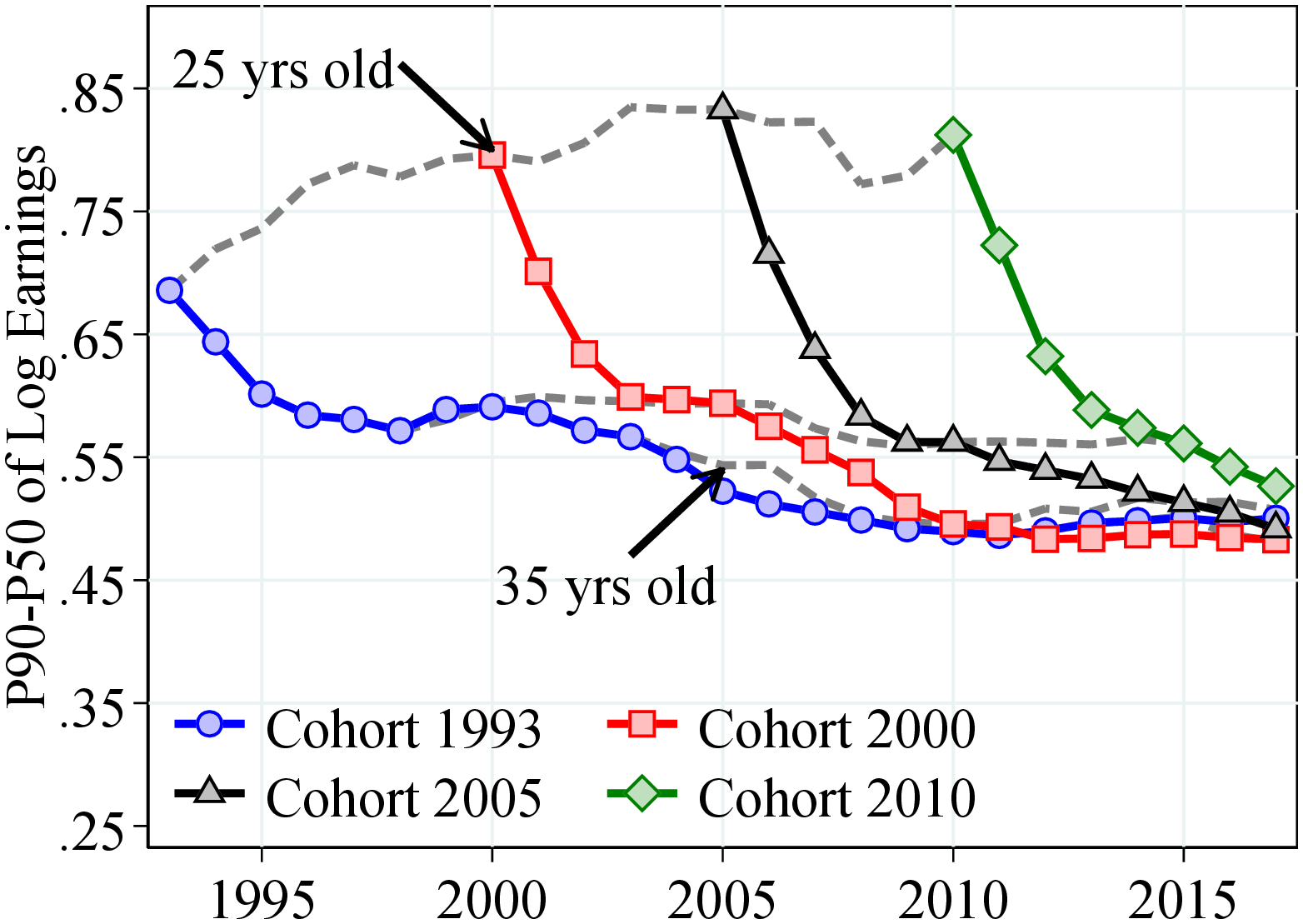

Furthermore, newer cohorts enter the labor market more unequal, especially above the median, compared to older cohorts, and more so for men (Figure B.4). In particular, the P90-P50 of log earnings for 25-year-old men (women) is 55 (70) log points in 1993 versus 75 (80) log points in 2017. We find similar patterns for the after-transfer income measure starting in the mid-1970s (Figure A.3). The higher initial inequality for newer cohorts mirrors the change in overall earnings inequality. Guvenen et al. (2018) and Engbom et al. (2021) also document that initial inequality and overall inequality track each other very closely in the U.S. and Brazil, respectively.10

The life-cycle profile of earnings inequality is roughly similar for all cohorts: For men between 25 and 35 years old, within-cohort inequality declines by around 70 log points and remains relatively stable afterward. Women experience a slower but roughly steady decline in inequality throughout the life cycle. Using the after-transfer income measure between 1967 and 2017, we find that men and women experience a steep decline in inequality until they are 35 years old, but then income dispersion increases slightly for men and stays relatively constant for women (Figure A.4). These findings are in sharp contrast to the increasing age profile of earnings inequality seen in several developed economies (Lagakos et al. (2018)). For example, Guvenen et al. (2021) document that the variance of log earnings increases by 55 log points between ages 25 and 55 in the U.S. The decline in earnings inequality over the life cycle also explains why Norway has a relatively compressed earnings distribution.

For men, the decline in P90-P10 over the life cycle is mainly a result of the closing of the gap between the bottom and median workers. P50-P10 declines by around 70 log points between ages 25 and 35 and remains roughly constant afterward (Figure B.4a).11 In comparison, the P90-P50 decreases only until age 28 and then increases steadily (Figure B.4c). These patterns are remarkably different for women, with life-cycle inequality declining at both ends of the distribution (Figures B.4b and B.4d).

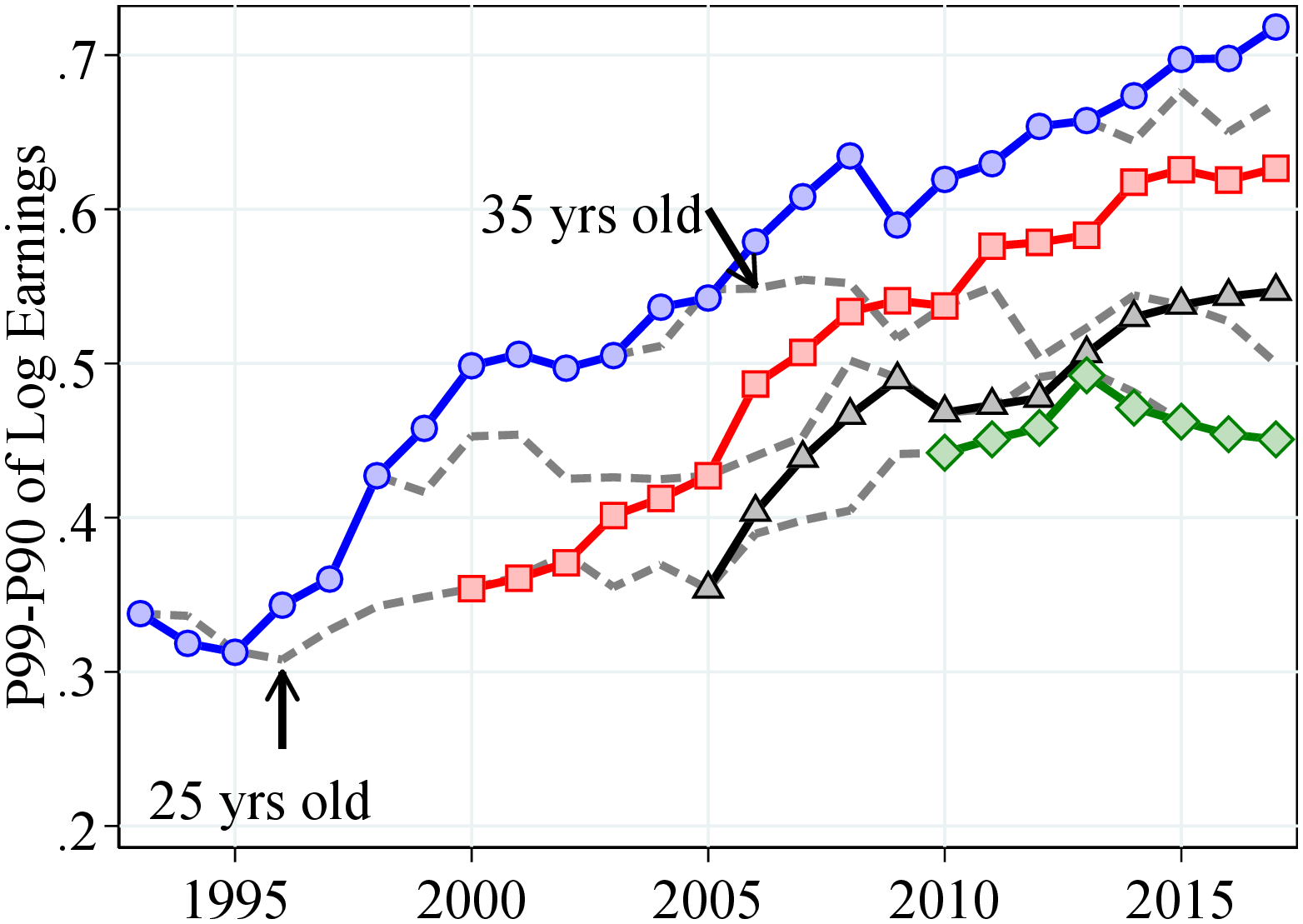

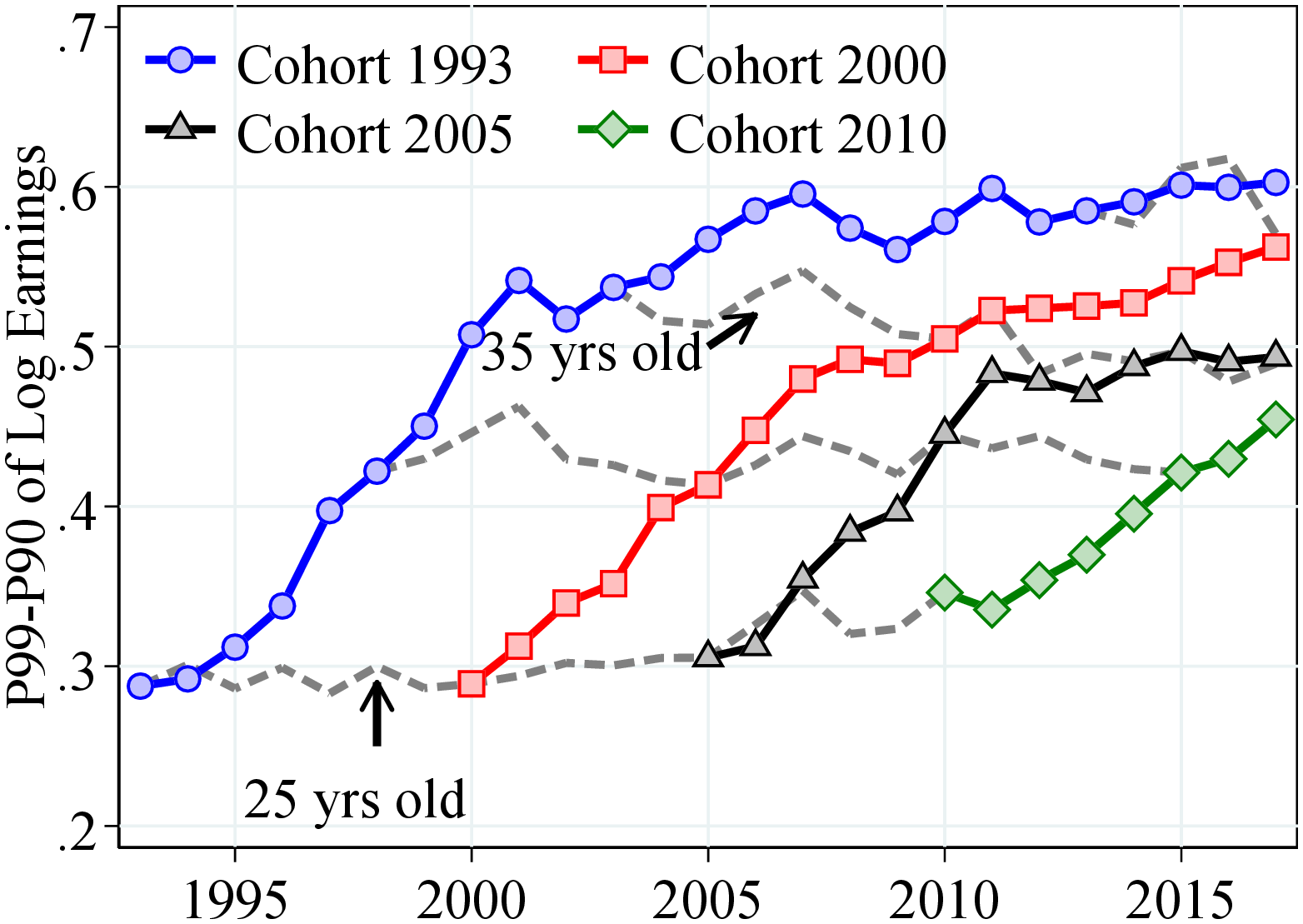

In contrast to the marked decline in earnings inequality below the 90th percentile, top income inequality increases significantly over the life cycle. The difference between the 99th and 90th percentiles of log earnings (P99-P90) increases over the life cycle by around 40 log points for men and 30 log points for women (Figures B.4e and B.4f, respectively). Furthermore, P99-P90 is higher for newer cohorts at all ages compared to older cohorts. These patterns track the rise in overall top income inequality over our sample period.

Our findings suggest that different economic mechanisms may be at play in determining the inequality at different parts of the earnings distribution, which is consistent to what other studies have found. For instance, Karahan, Ozkan and Song (2022) show that in the U.S., earnings differences between the bottom and median earners are mainly a result of the differences in unemployment risk, whereas the right-skewed distribution of returns to experience explains the inequality between the top and median earners.

3.2 Distribution of Earnings Growth

In this section, we characterize income volatility by documenting the properties of the distribution of individual earnings changes in Norway. We measure income change as the log growth rate of residual earnings between years \(t\) to \(t+k\), \(g_{it}^{k}=\tilde{\varepsilon}_{it+k}-\tilde{\varepsilon}_{it}\) for \(k=\left \{1,5\right \}\). We obtain residual earnings, \(\tilde{\varepsilon}_{it}\), by regressing log earnings in each year on a set of age dummies for men and women separately.12

3.2.1 Higher-Order Moments of Individual Earnings Growth

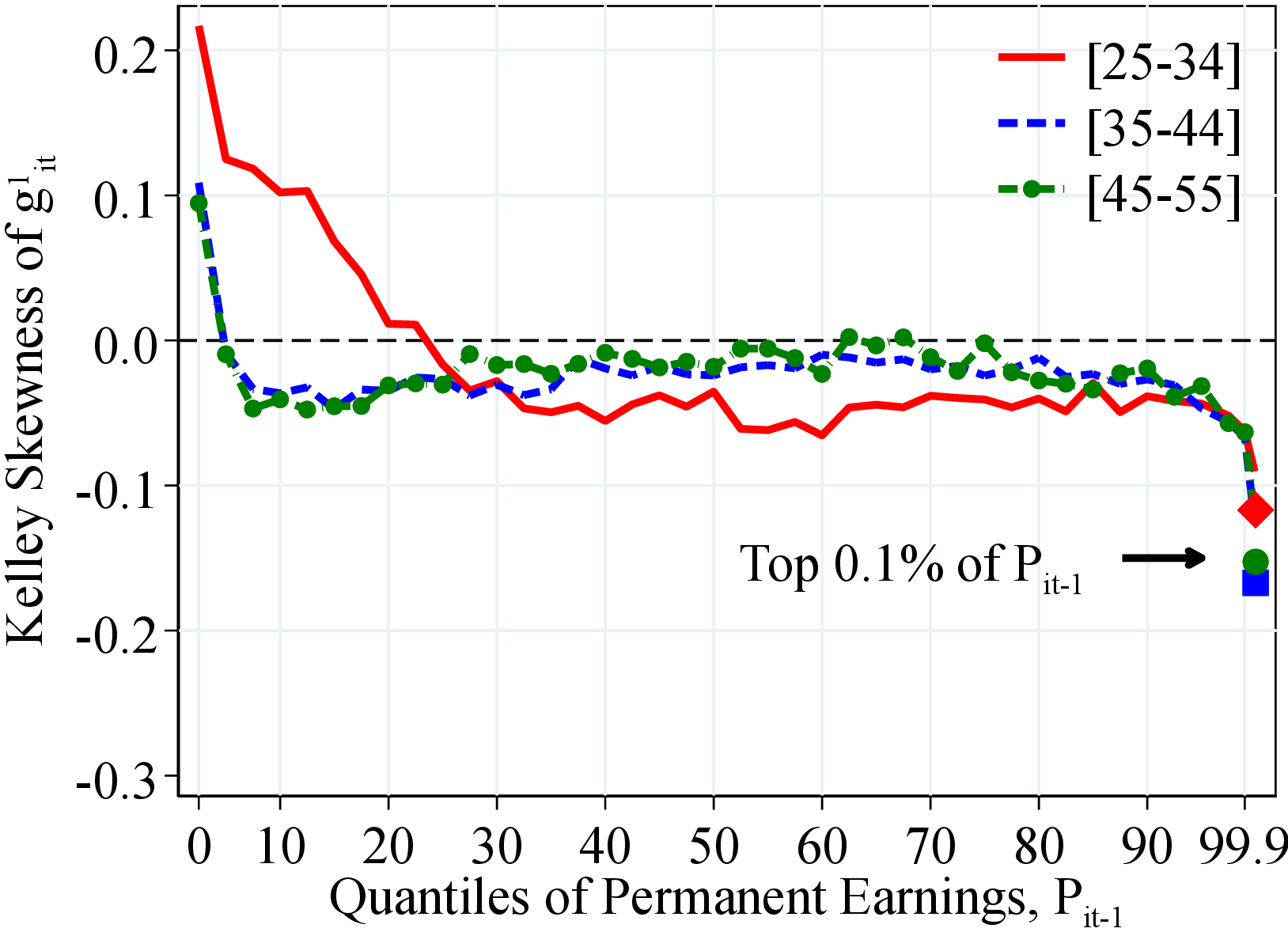

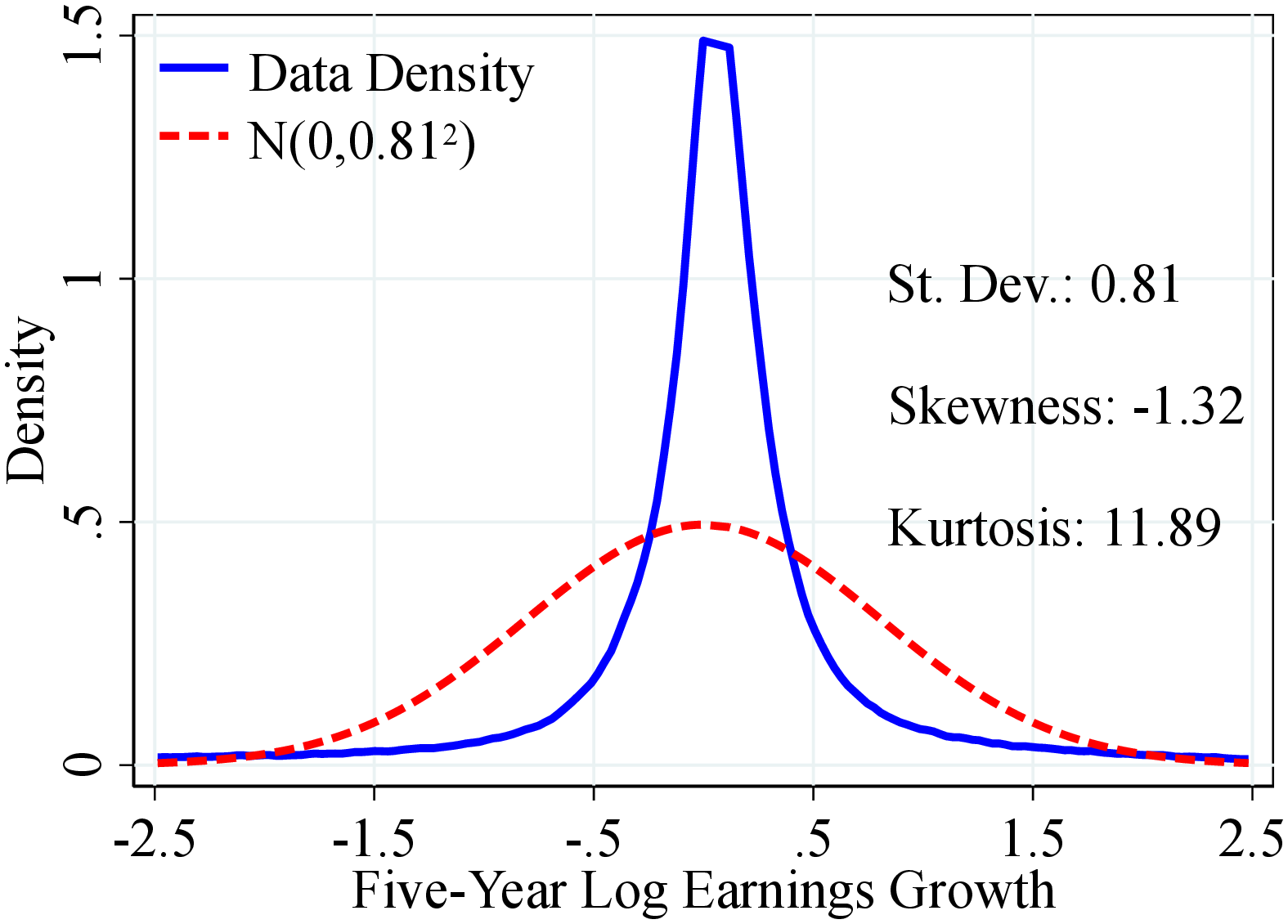

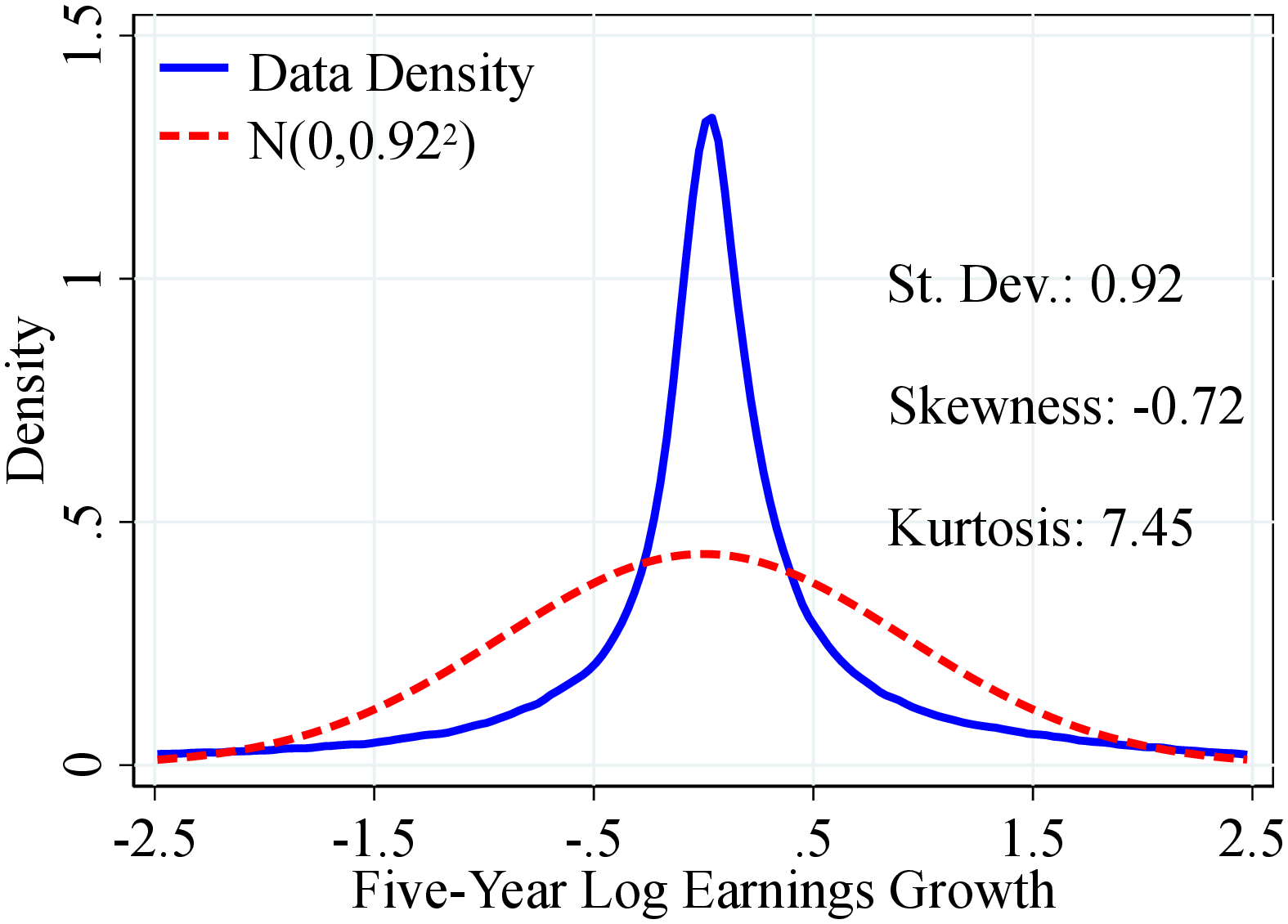

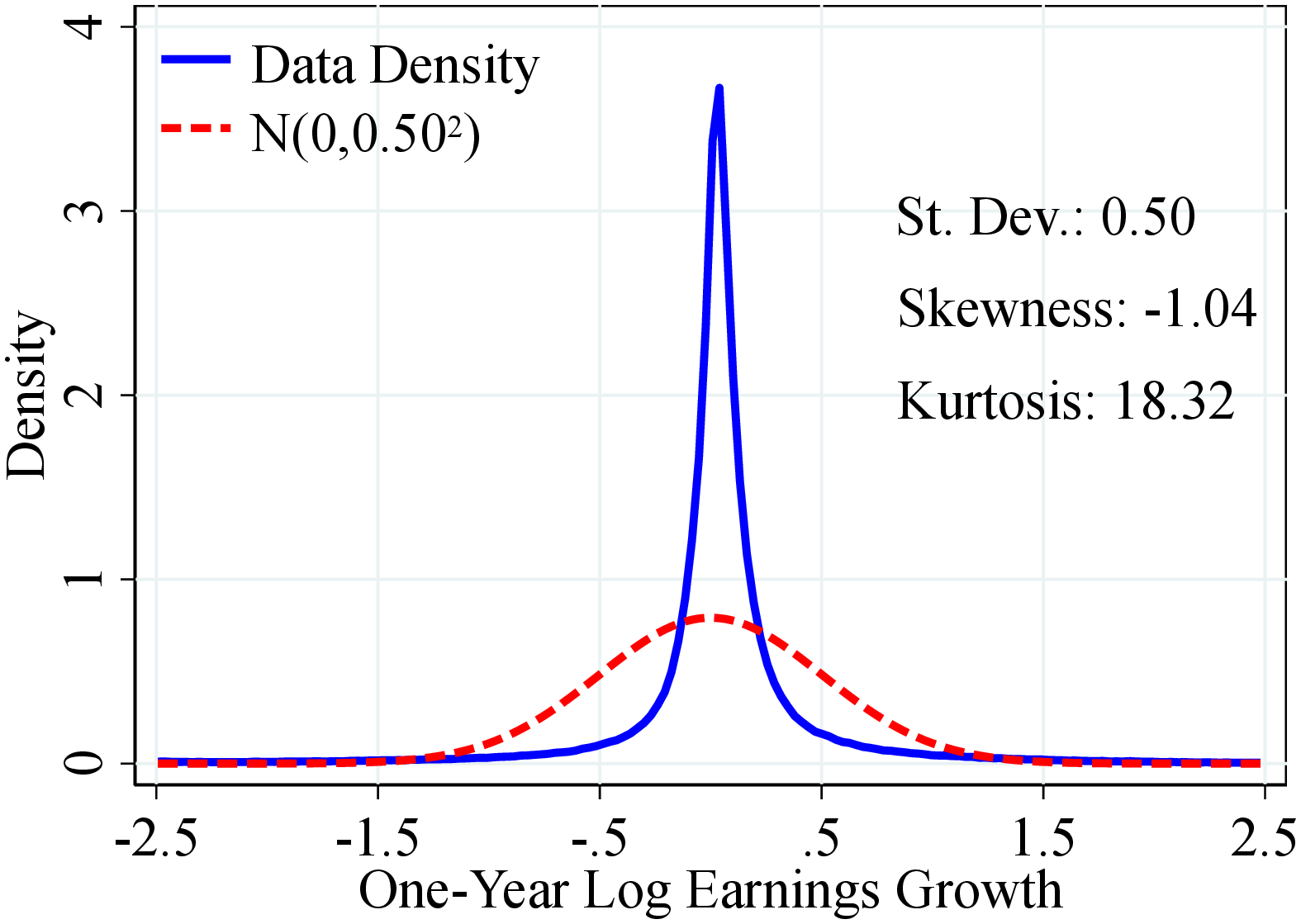

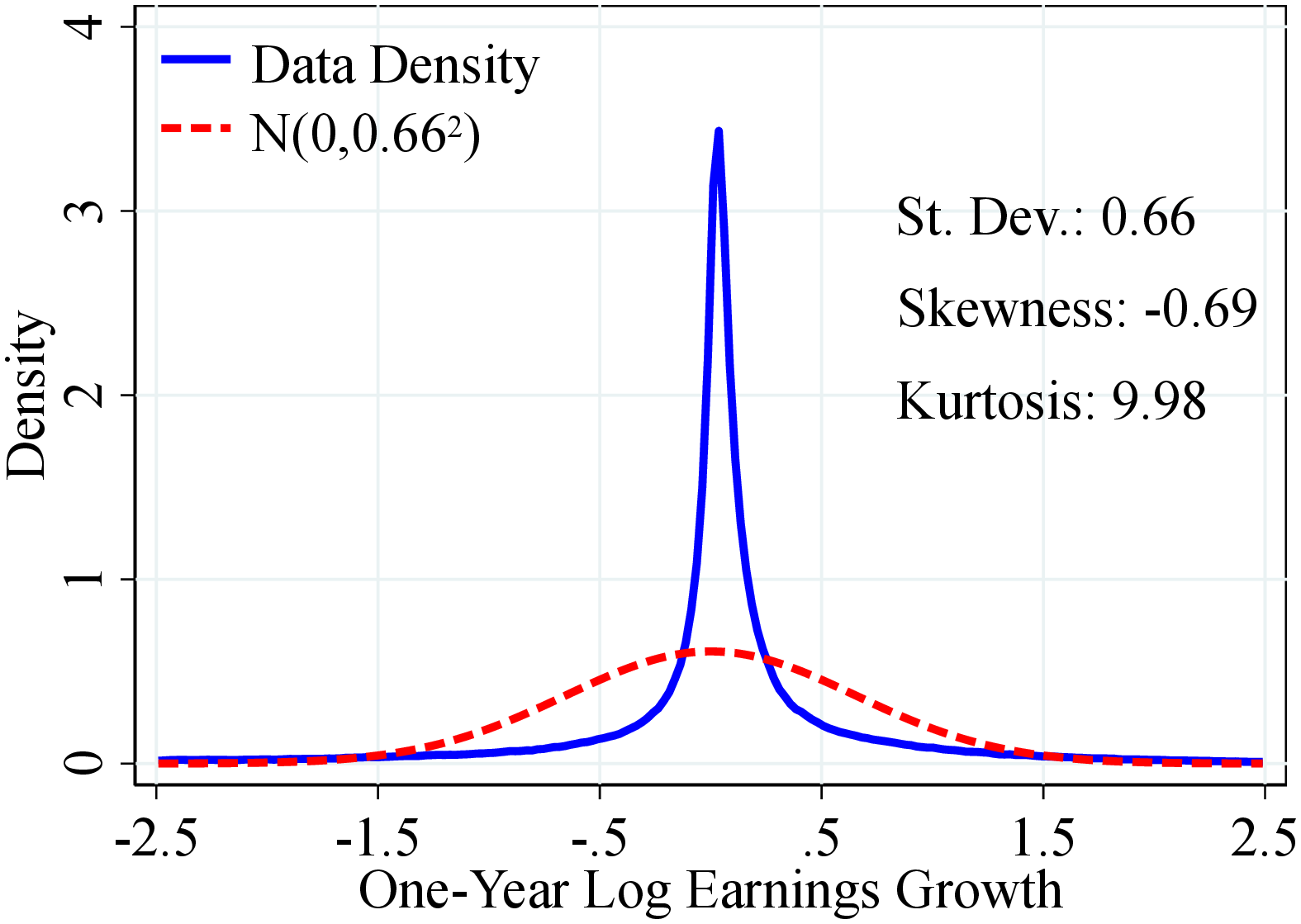

Recent literature has shown that idiosyncratic earnings changes display strong non-Gaussian features—such as left skewness and excess kurtosis—and that the extent of these non-normalities varies significantly with age and earnings level (e.g., Arellano, Blundell and Bonhomme (2017); Guvenen et al. (2021)). Furthermore, these features have important implications for the consumption and savings behavior of households (e.g., Kaplan, Moll and Violante (2018); De Nardi, Fella and Paz-Pardo (2020)). Exploiting our dataset’s sheer size and high quality, we also focus on these moments, in addition to first and second moments.

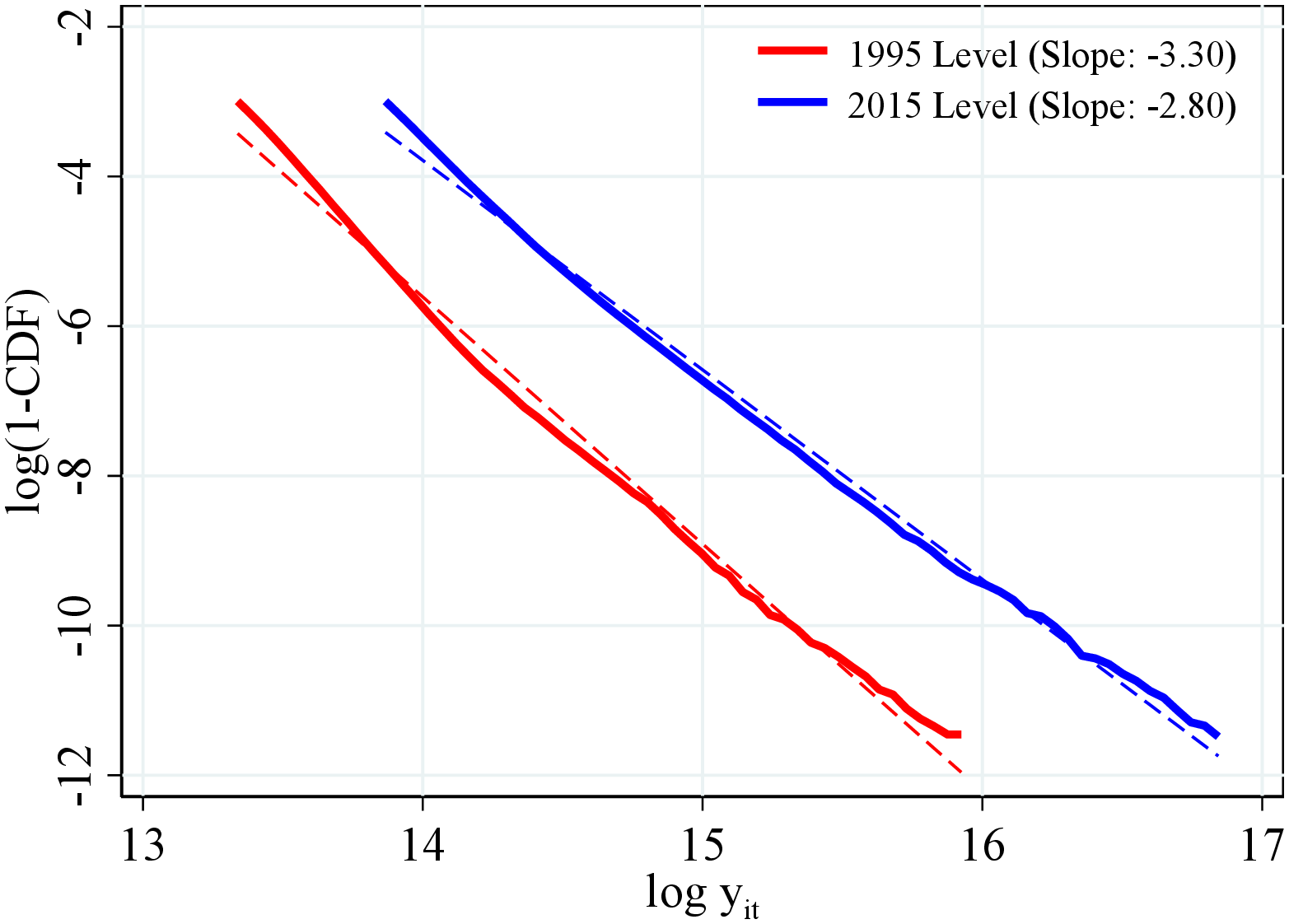

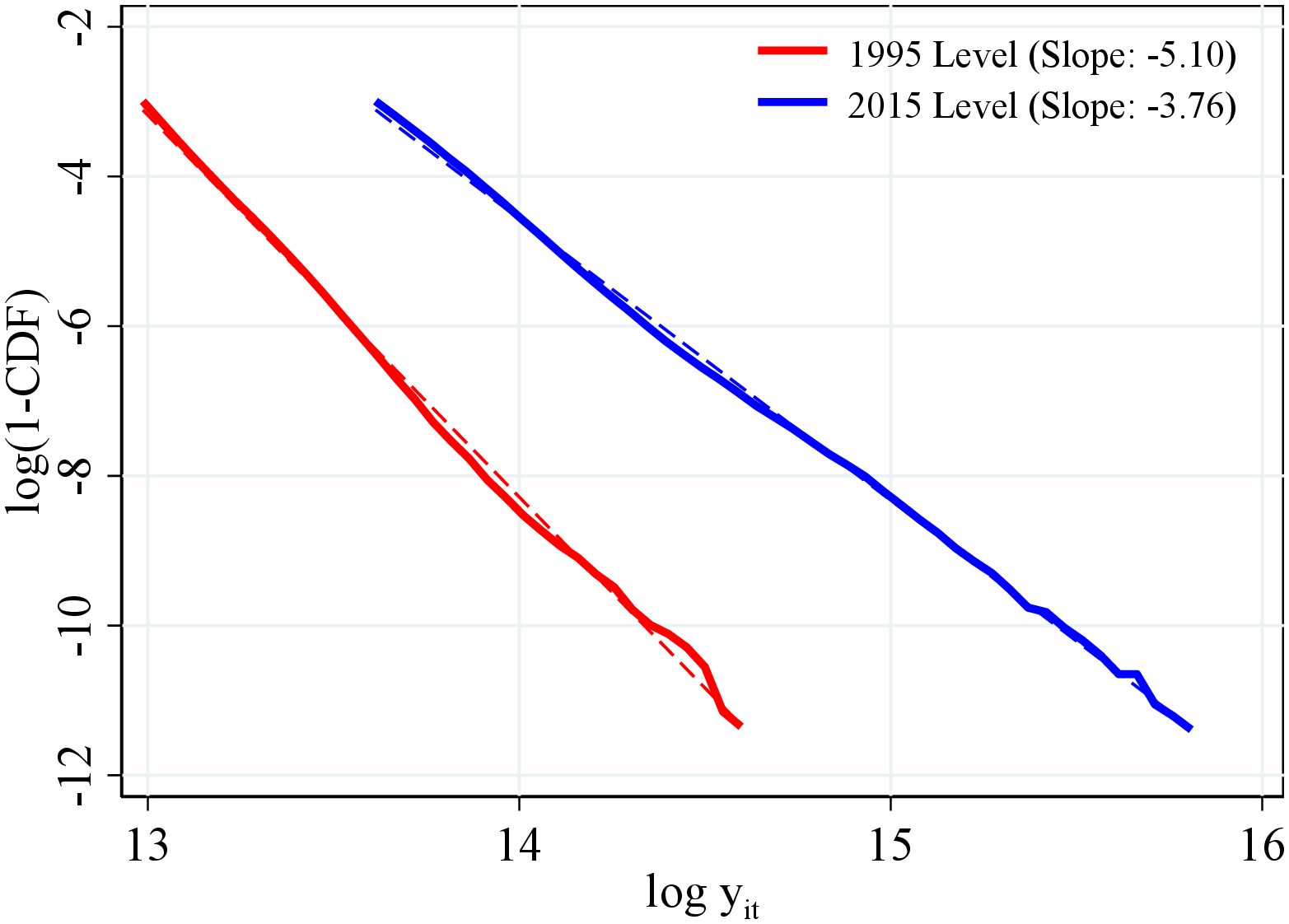

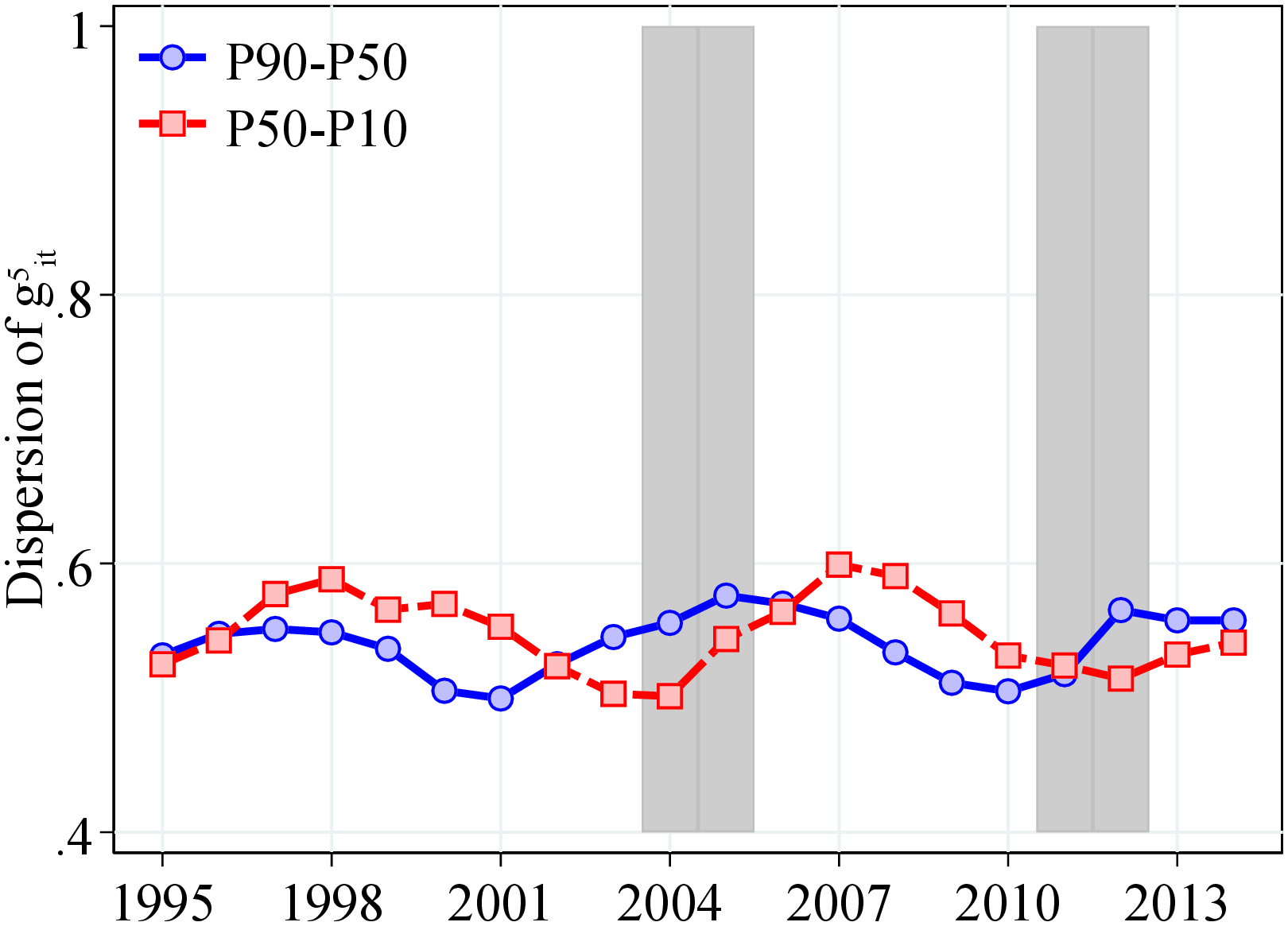

Similar to other countries (e.g., De Nardi et al. (2021)), one-year and five-year earnings growth distributions in Norway display left (negative) skewness and excess kurtosis relative to a normal density (Figures C.4 and C.3). For example, almost twice as many workers experience a decline of more than three standard deviations (“disaster shocks”) as those experiencing increases of the same size (Table C.1). At the same time, the fraction of workers who experience an earnings change of less than 5% is 31.8% in the data versus 6.8% from a normal density with the same standard deviation. Similarly, in the data, 3.3% of workers see their incomes change by more than three standard deviations or more versus 0.2% from a normal density.

We next investigate how the earnings growth distribution evolves over time, over the business cycle, and between different groups of workers. Below we present results for one-year earnings changes to better capture the high-frequency business-cycle variation. The corresponding figures for five-year changes—which capture more persistent innovations—are reported in Appendix C.1 and show similar qualitative patterns. Also, in the main text, we report percentile-based moments (e.g., Kelley skewness and Crow-Siddiqui kurtosis), which are robust to outliers but overlook valuable information in the tails of the distribution. Therefore, we also document standardized moments in Appendices C.1 and C.2 and discuss any substantial differences in our findings from these measures.

3.2.2 Trends and Business-Cycle Variation

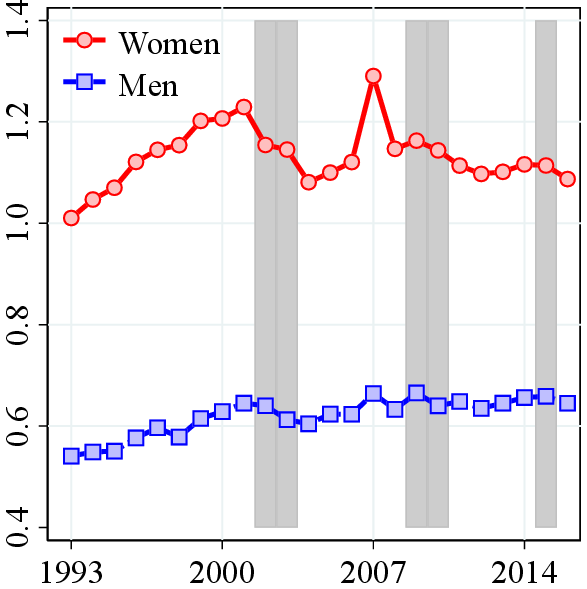

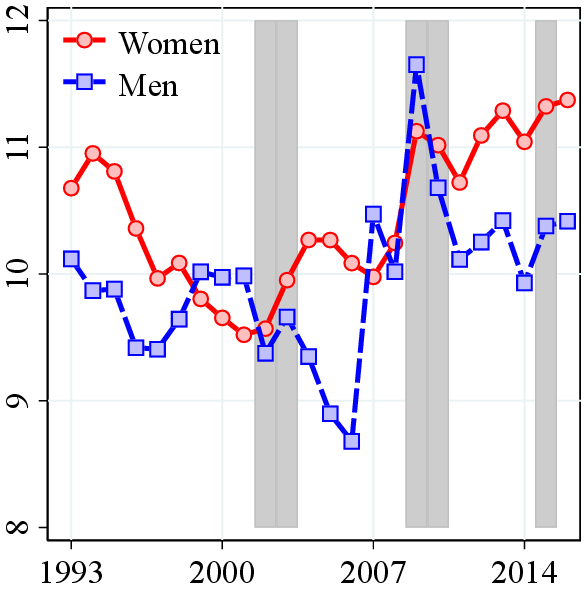

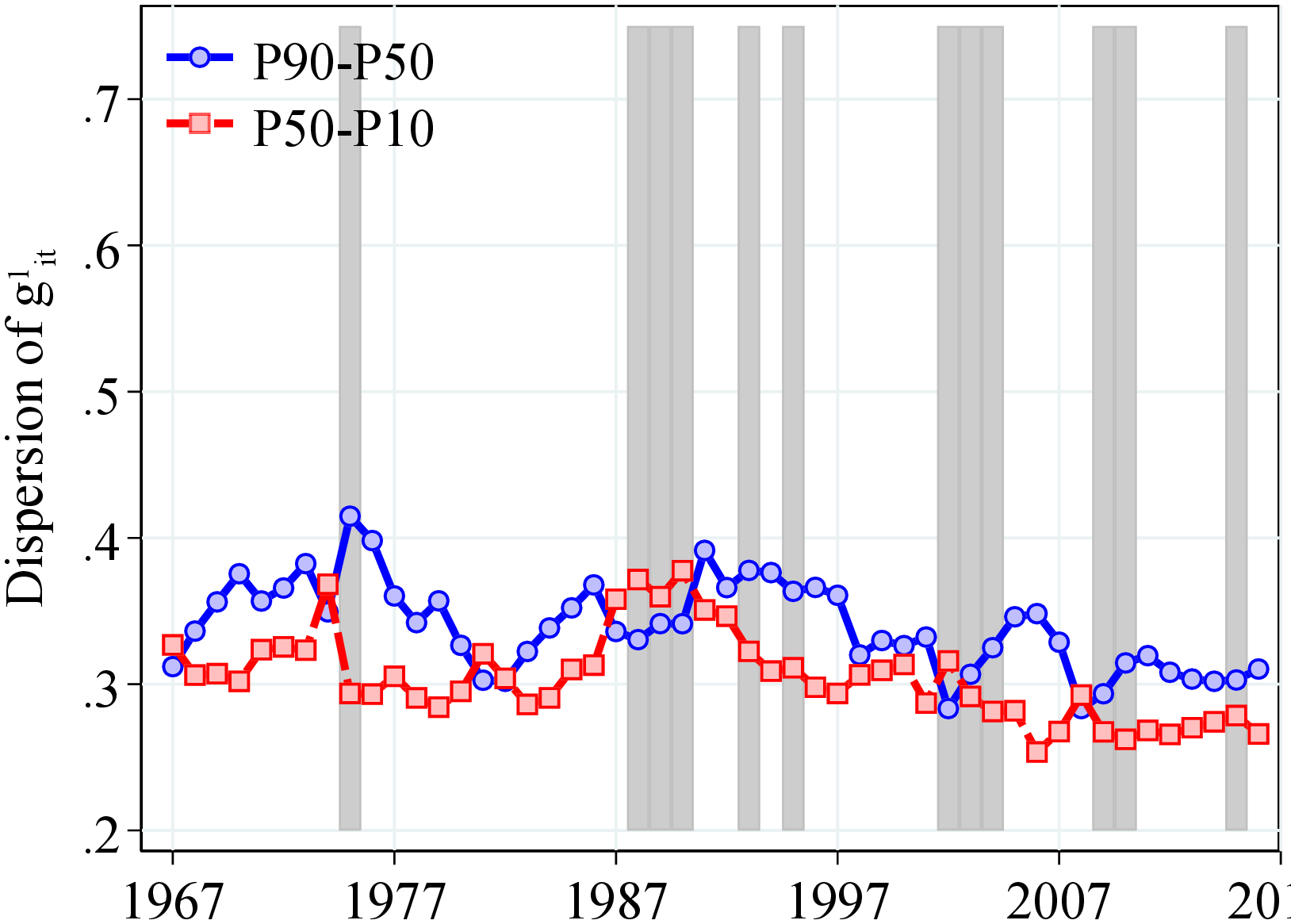

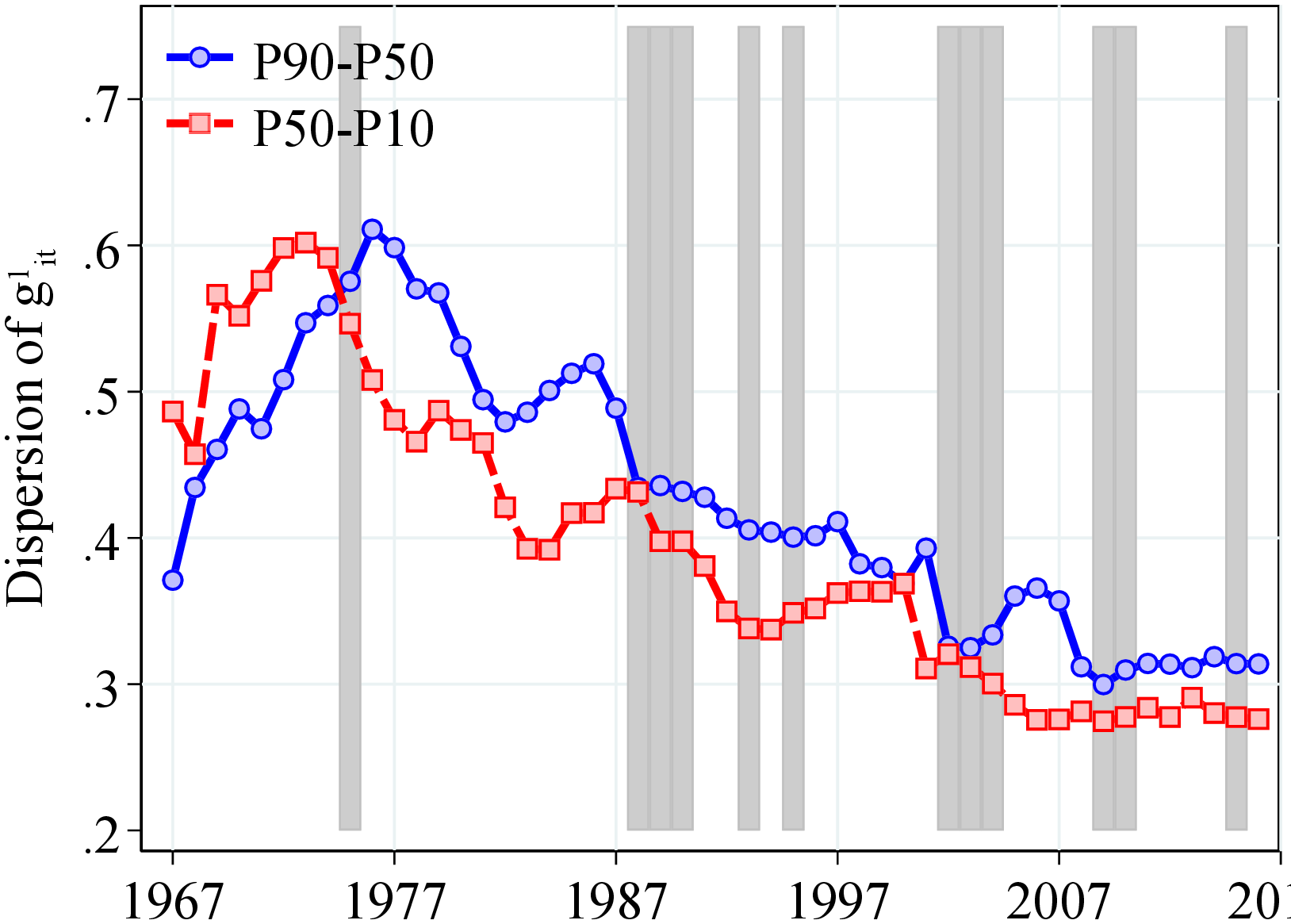

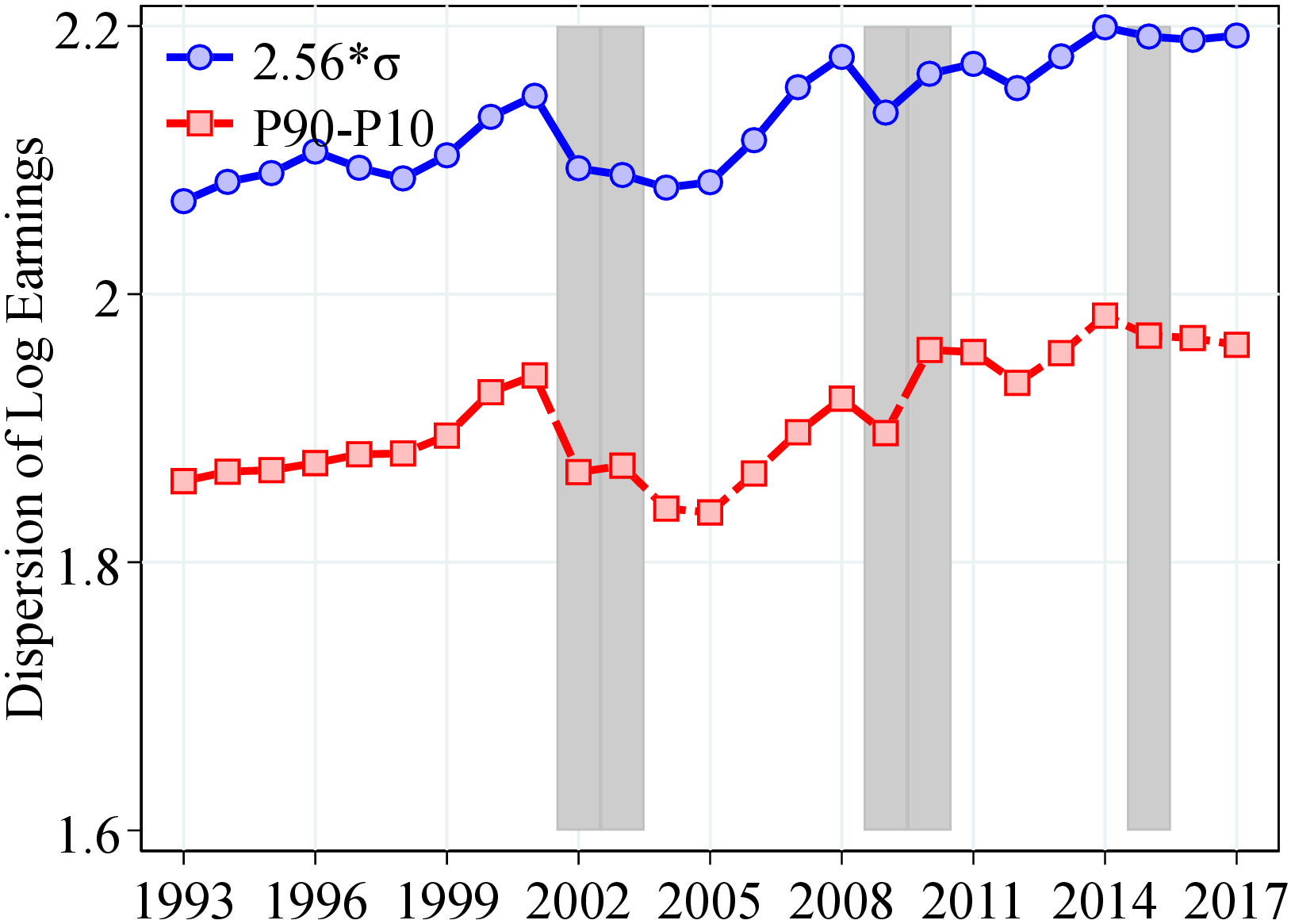

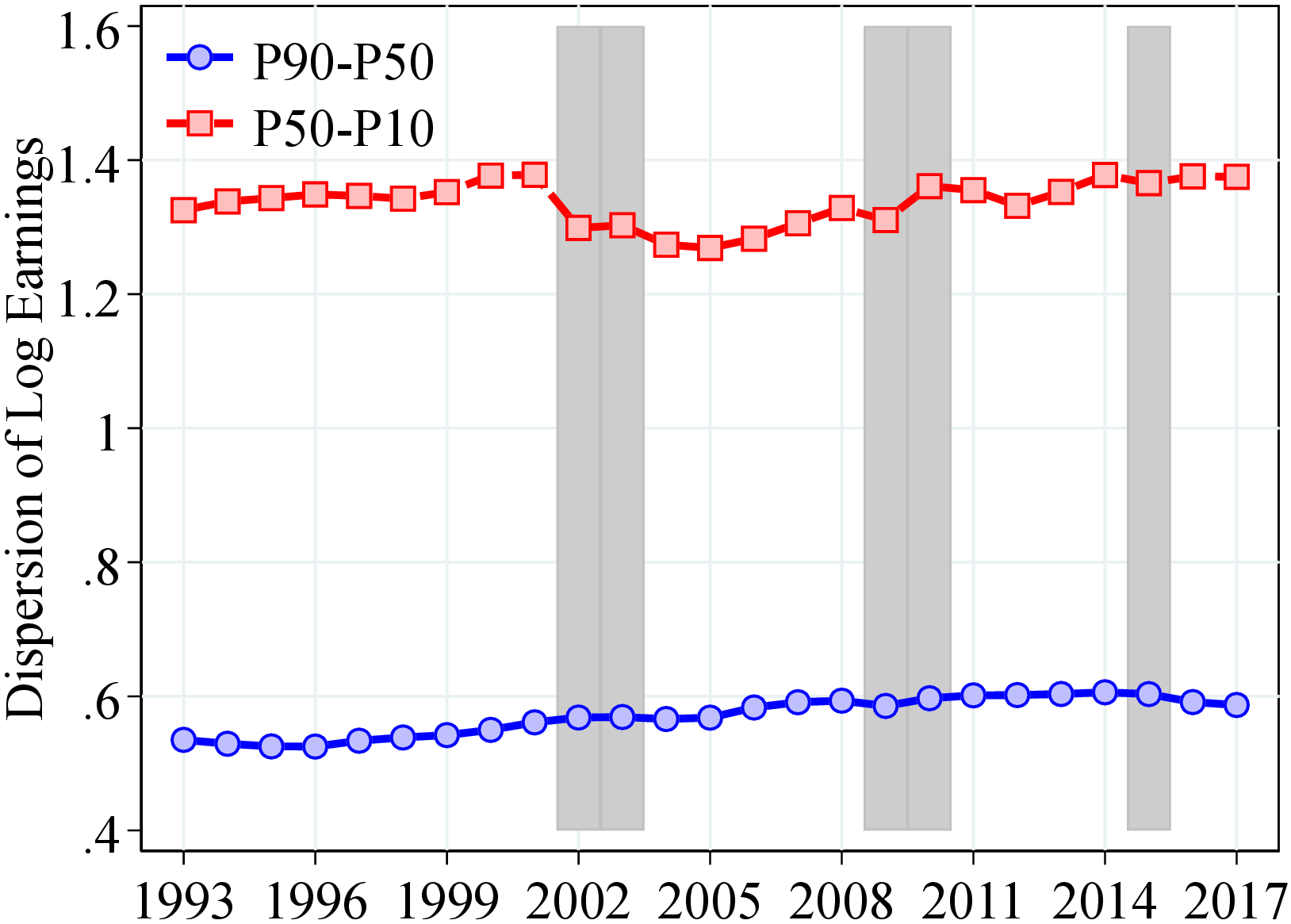

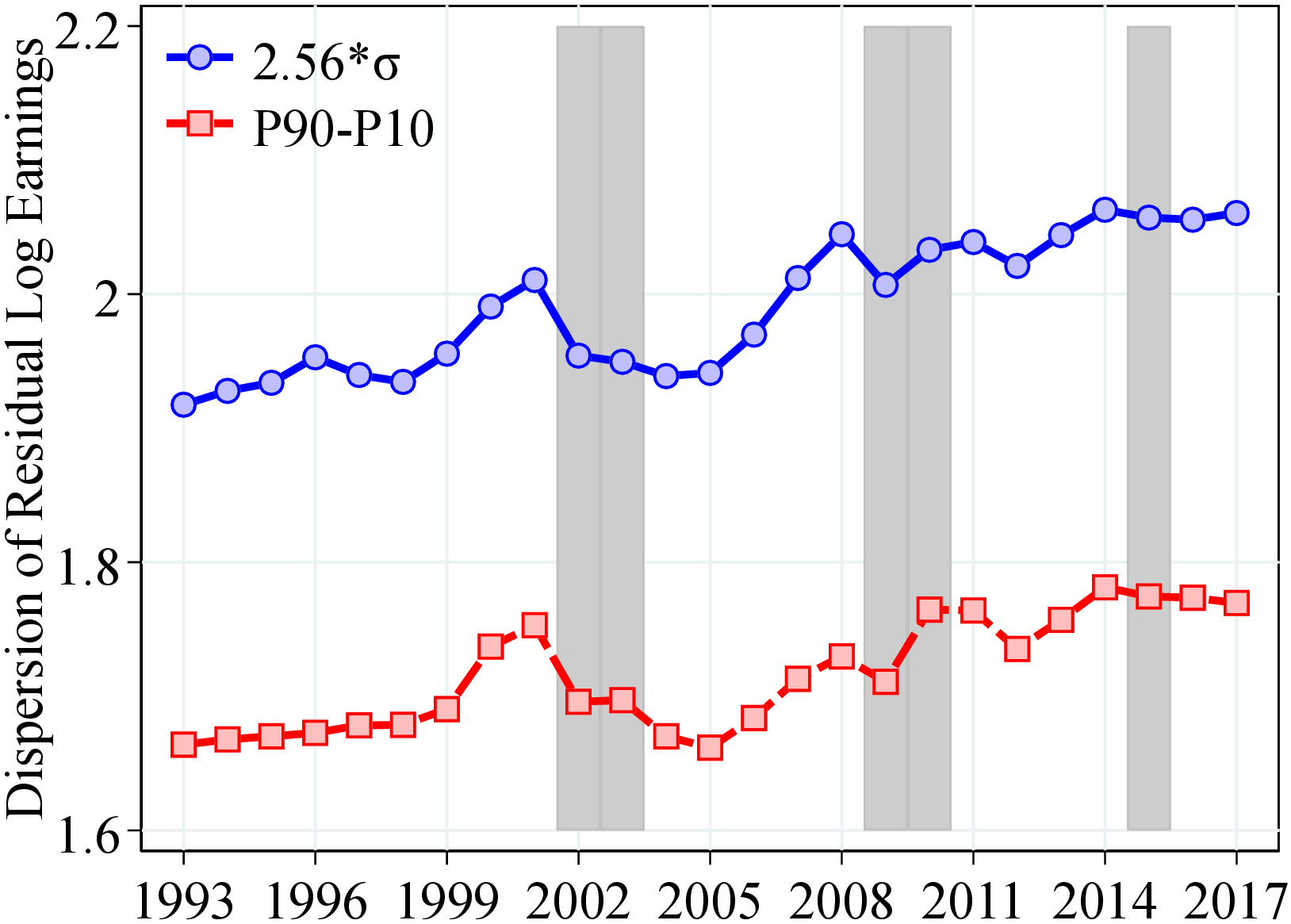

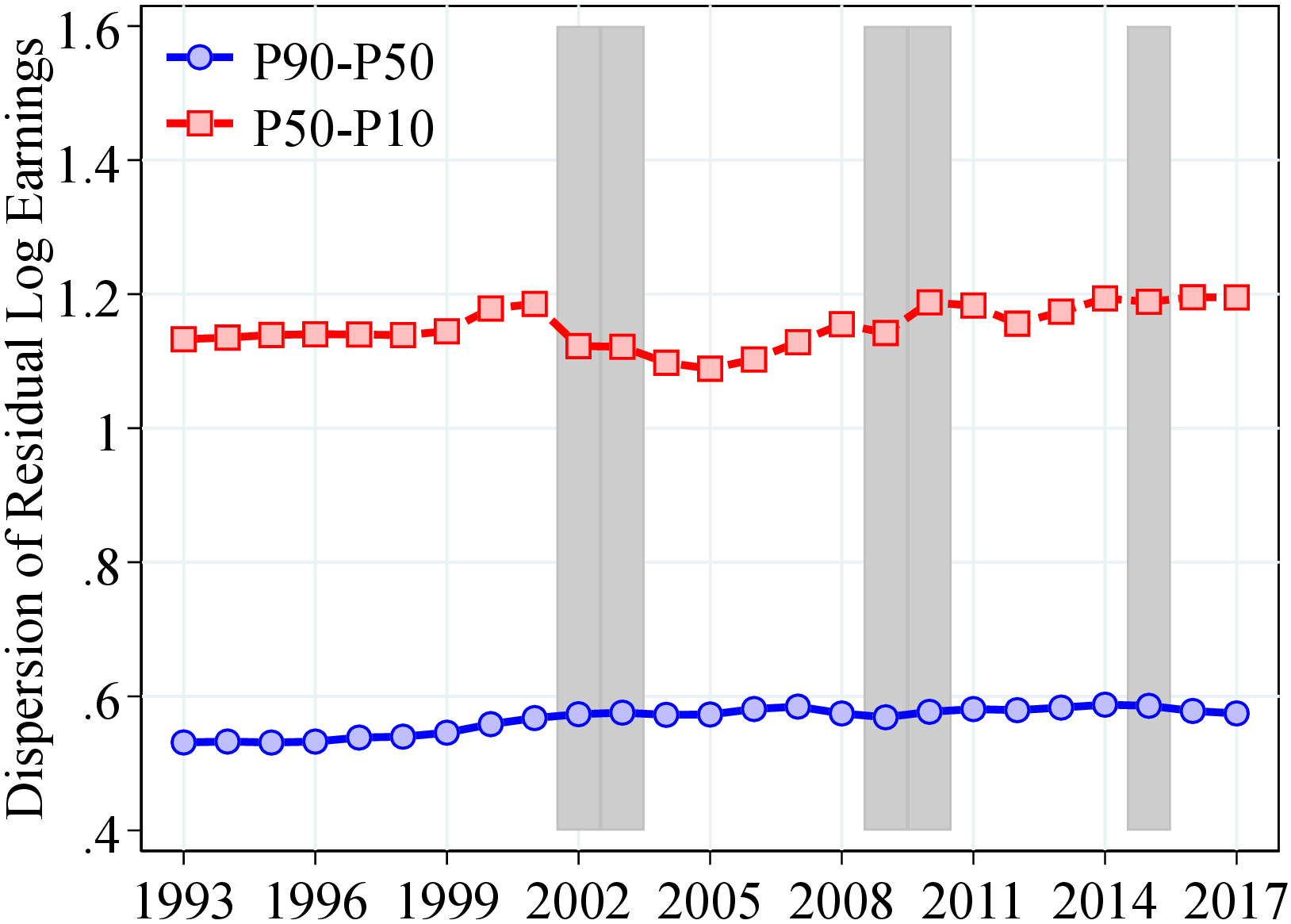

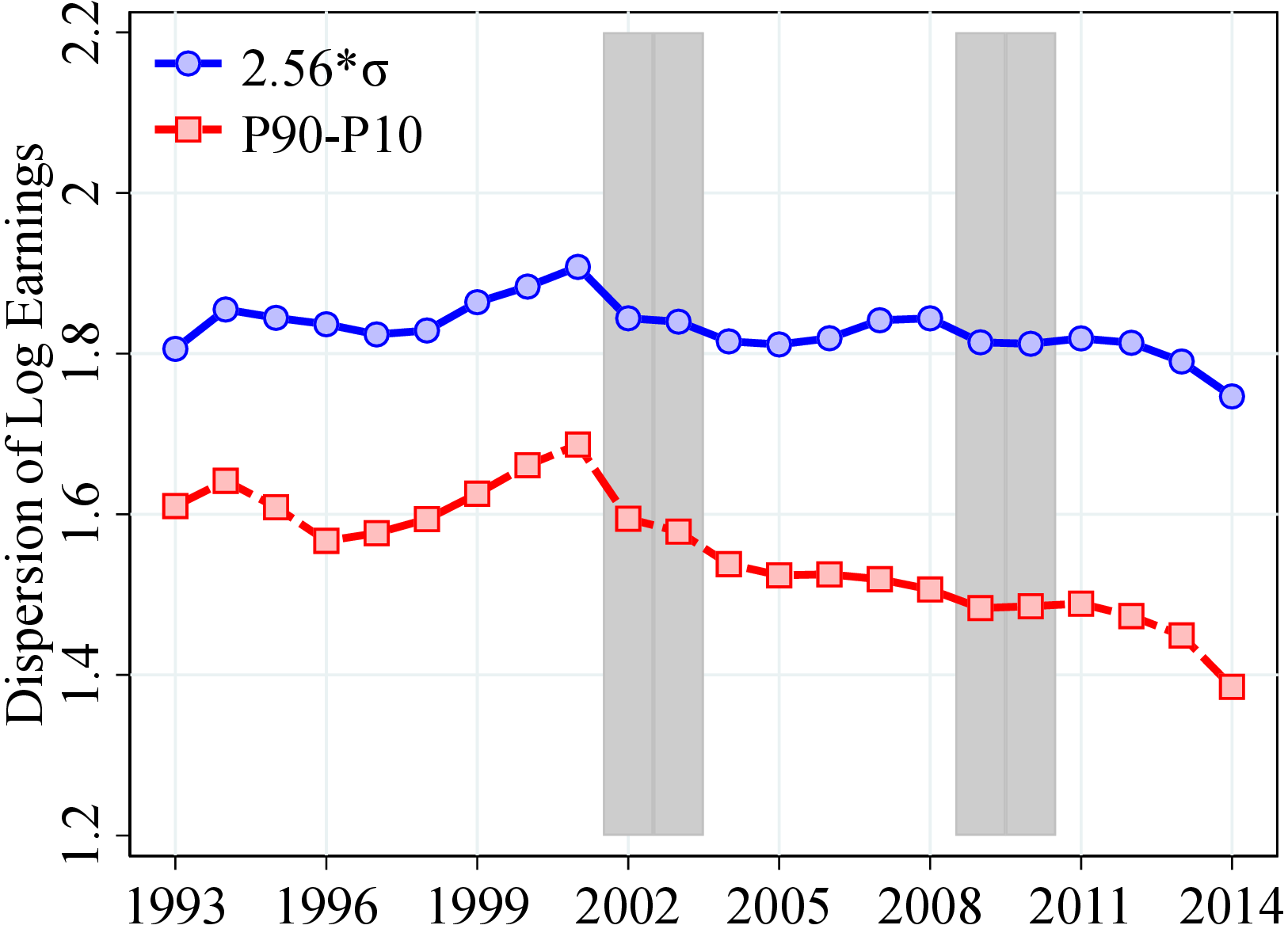

Volatility. Overall earnings volatility for women—as measured by the P90-P10 of log income changes—is almost twice as large as the earnings volatility for men, hovering around 115 log points for women versus 60 log points for men (Figure 4a). This is likely a result of the generous maternity leave benefits provided by the Norwegian government (up to nine months of full pay), the fact that women are more likely to work in part-time jobs with more flexible hours, and an overall weaker labor market attachment (OECD, 2019). In addition, the income volatility of men has risen significantly over our sample period, with P90-P10 increasing from 54 log points in 1993 to 65 log points in 2016, whereas for women, income volatility has remained relatively stable over time (see Figure C.5 for upper- and lower-tail volatility). These findings are in contrast with the evidence from the U.S.—also based on administrative data—that volatility is roughly similar for men and women and has been trending down since the 1980s for both (Bloom et al. (2017)). Our results, however, are similar to those documented for Italy (Hoffmann, Malacrino and Pistaferri (2021)), the U.K. (Bell, Bloom and Blundell (2021)), and Sweden (Friedrich et al. (2021)).

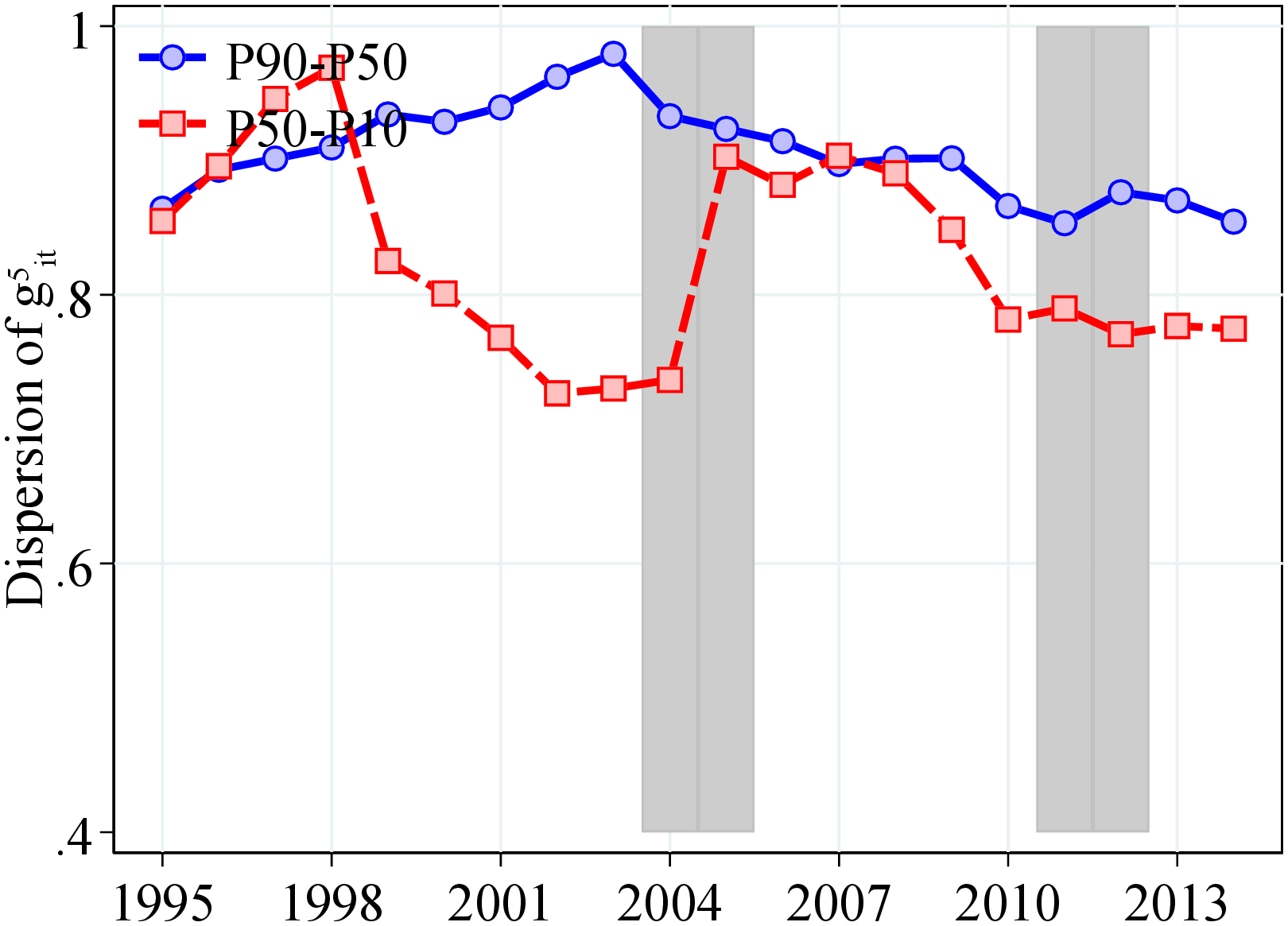

After-transfer income volatility displays different trends relative to earnings volatility (Figure A.5). After-transfer income volatility declines steeply since the mid-1970s especially for women, when sickness benefits and unemployment insurance were added to our after-transfer income measure. In fact, in 2017 men and women face similar volatility according to the after-transfer income measure.

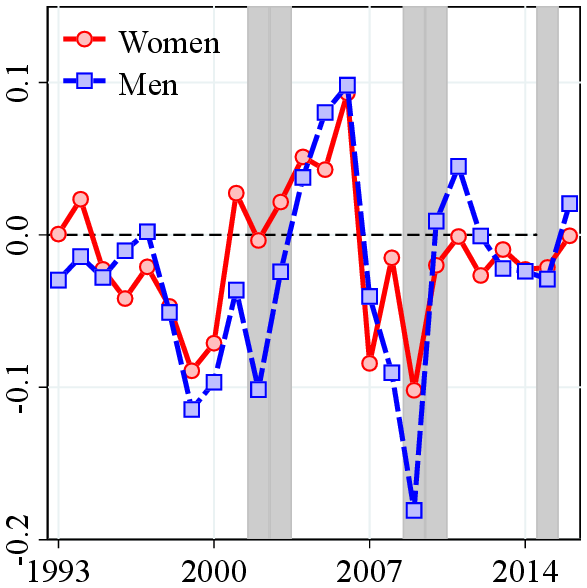

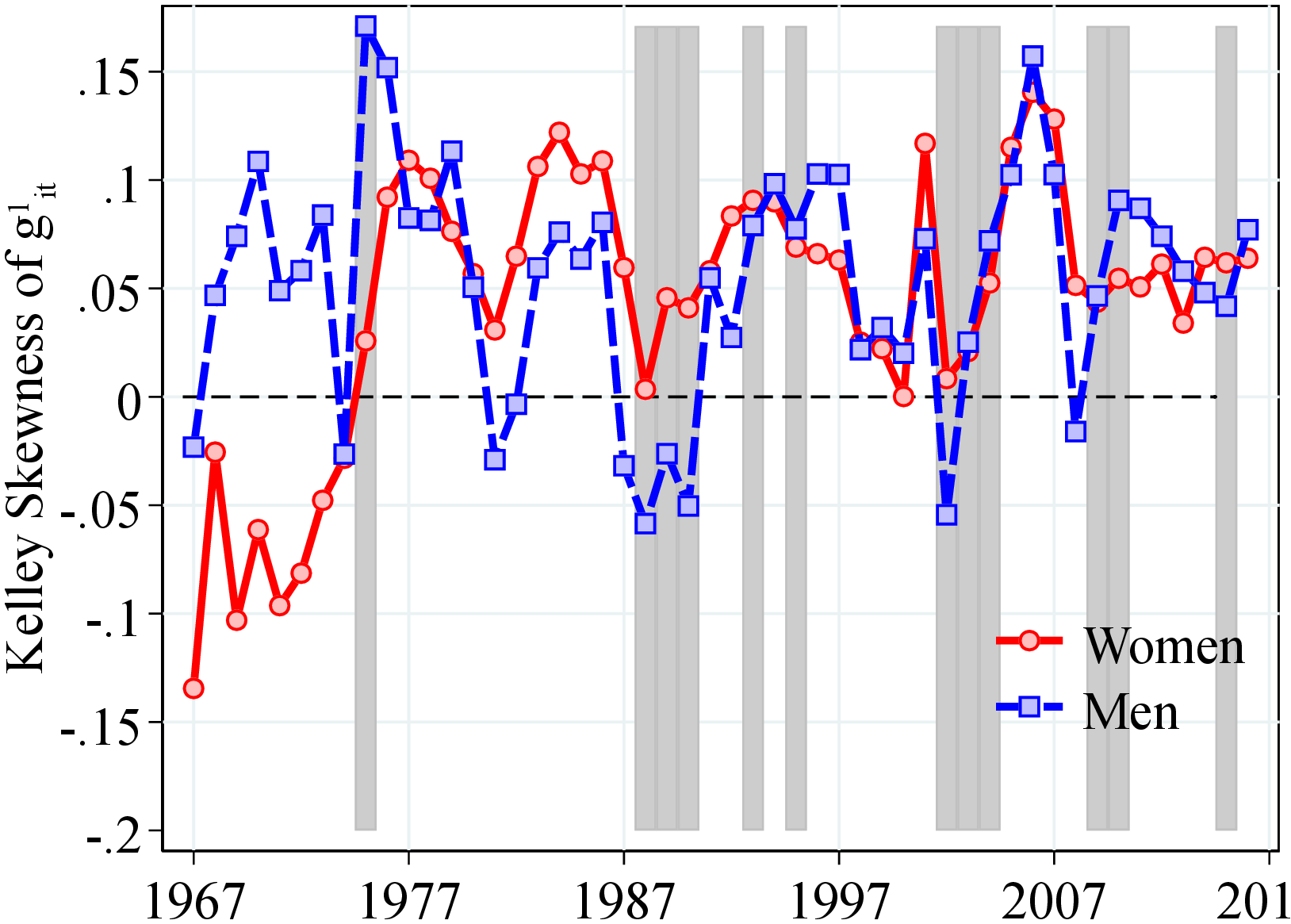

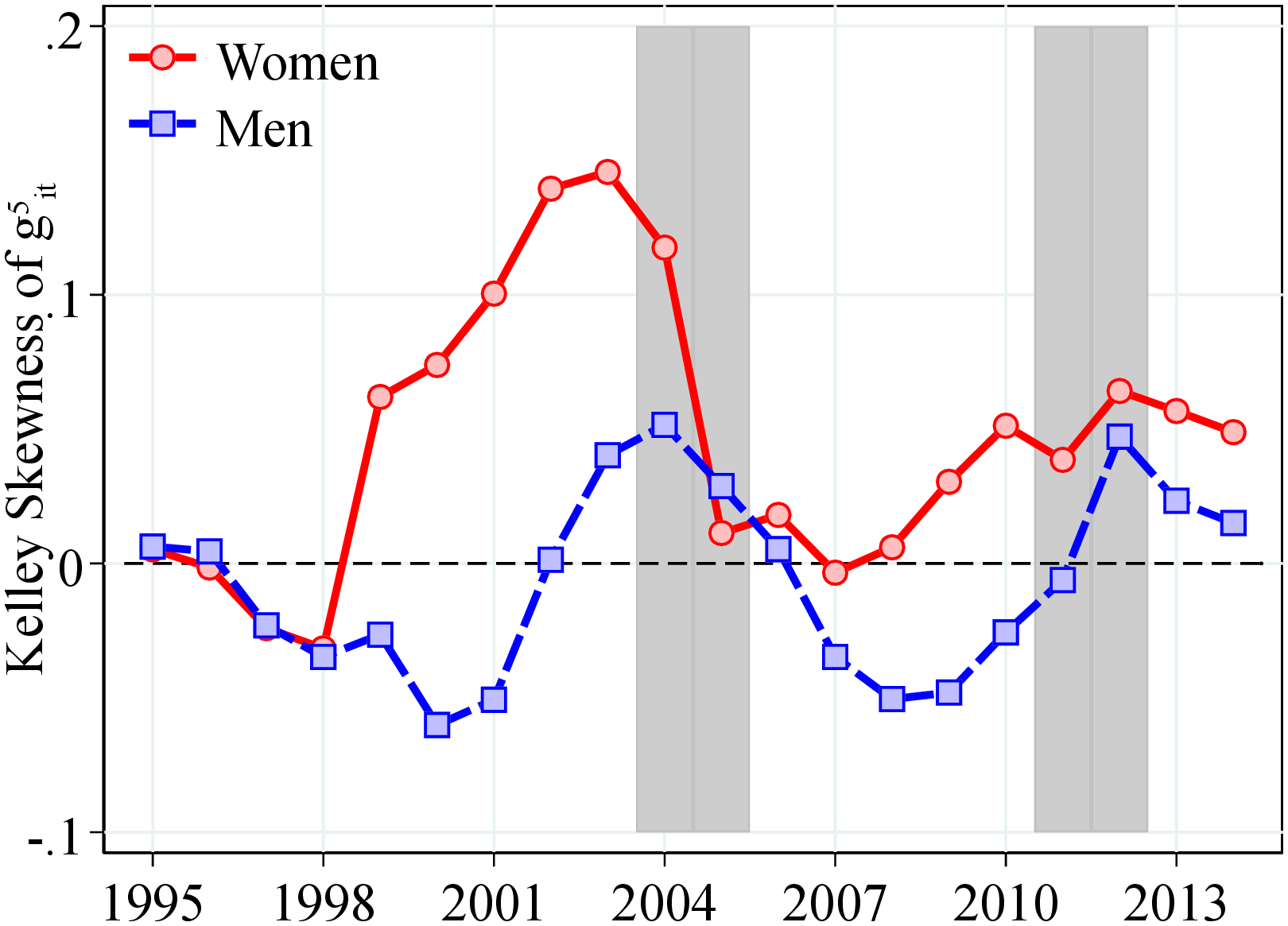

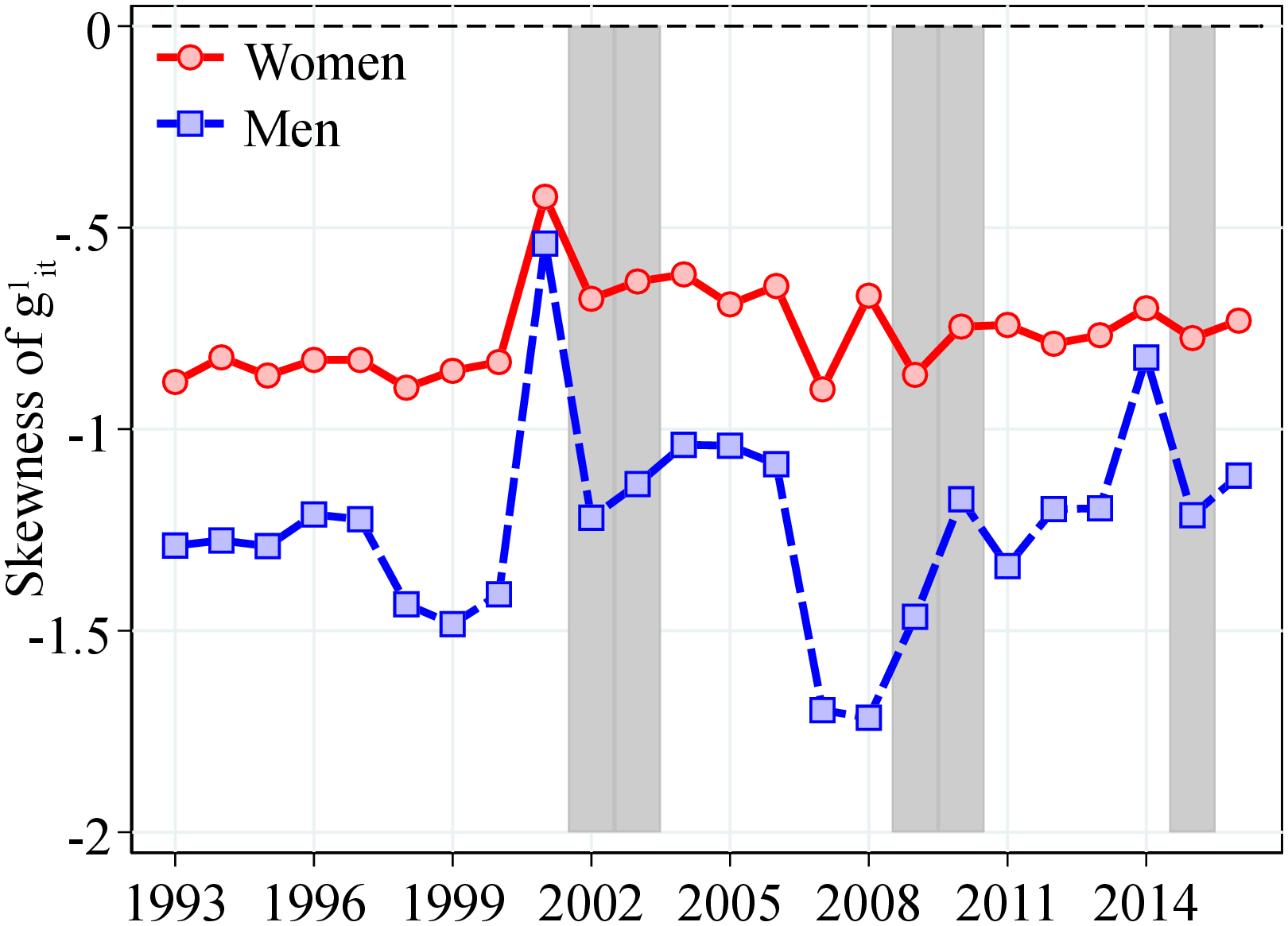

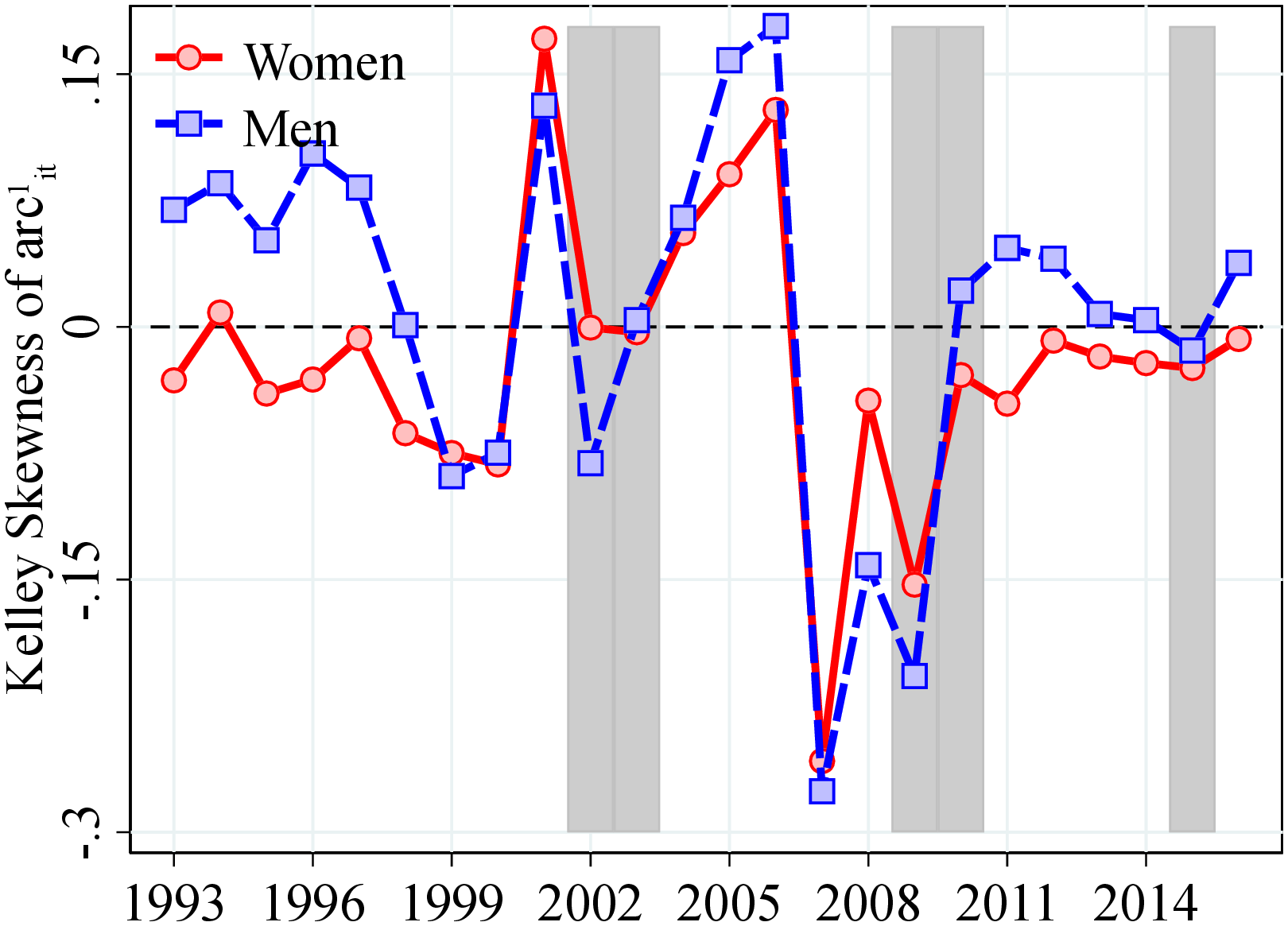

Skewness. Figure 4b shows the asymmetry in the distribution of earnings growth as measured by the Kelley skewness (Kelley, 1947), \(\mathcal{S_{K}}=\frac{\text{(P90-P50)}-\text{(P50-P10)}}{\text{P90-P10}}\). In Norway, Kelley skewness of log earnings growth averages -0.025 for men and -0.014 for women during our sample period. However, when measured with the third standardized moment, earnings growth displays strong negative skewness in all years (Figure C.5c), indicating a stronger asymmetry in the extreme tails of the distribution. As expected, this negative skewness is ameliorated after including public transfers in the income measure. In fact, after-transfer income changes are positively skewed (Figure A.6).

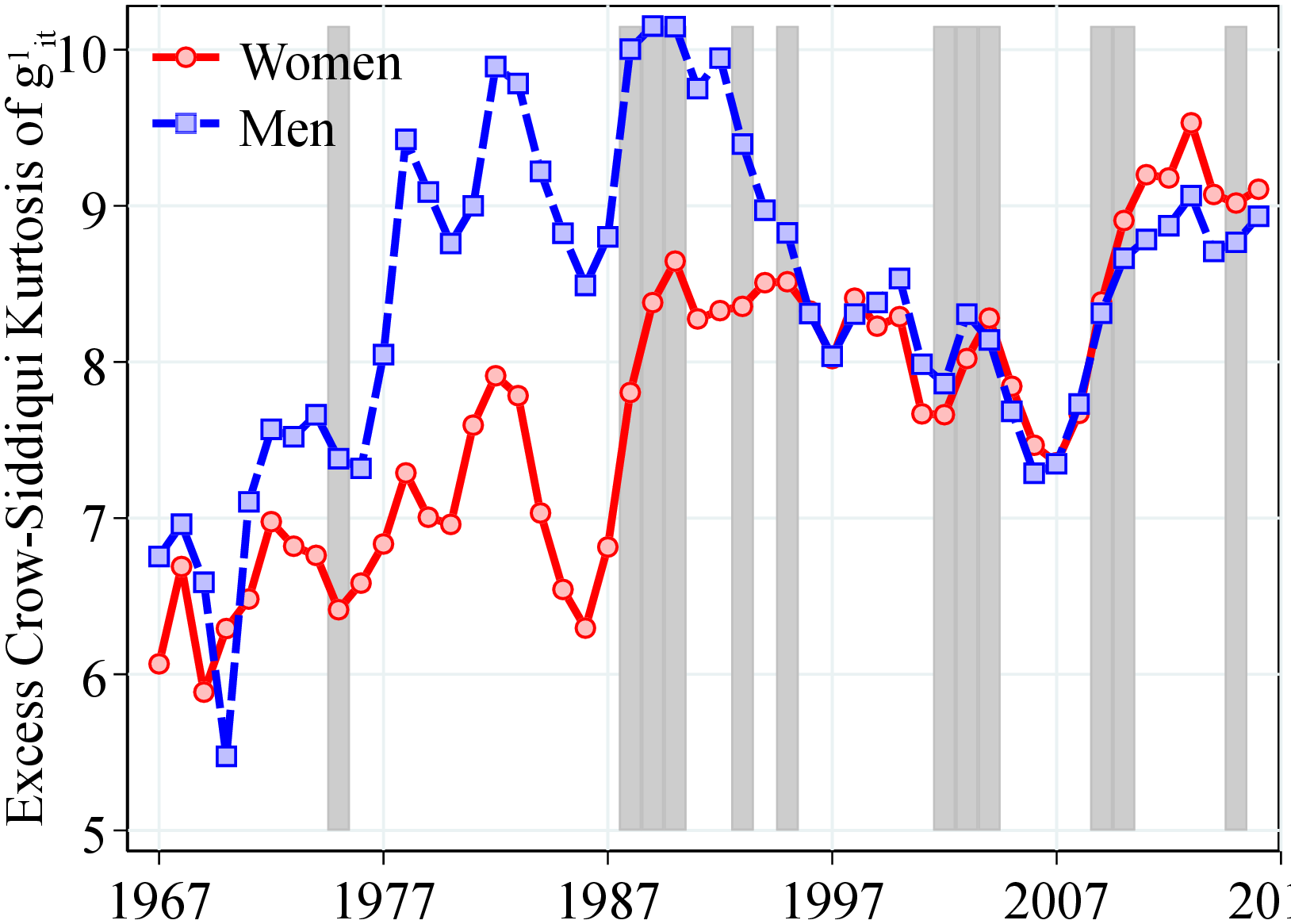

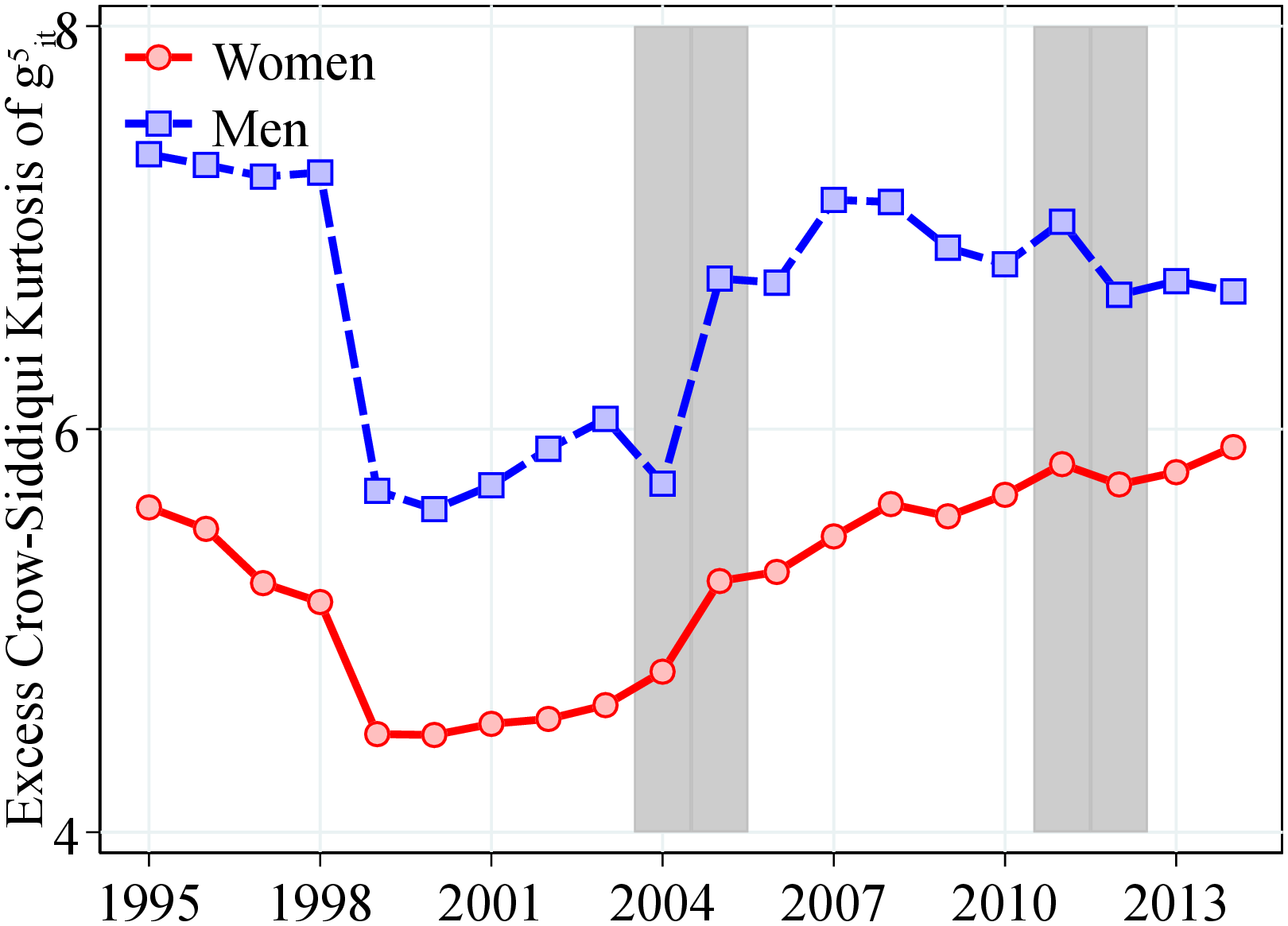

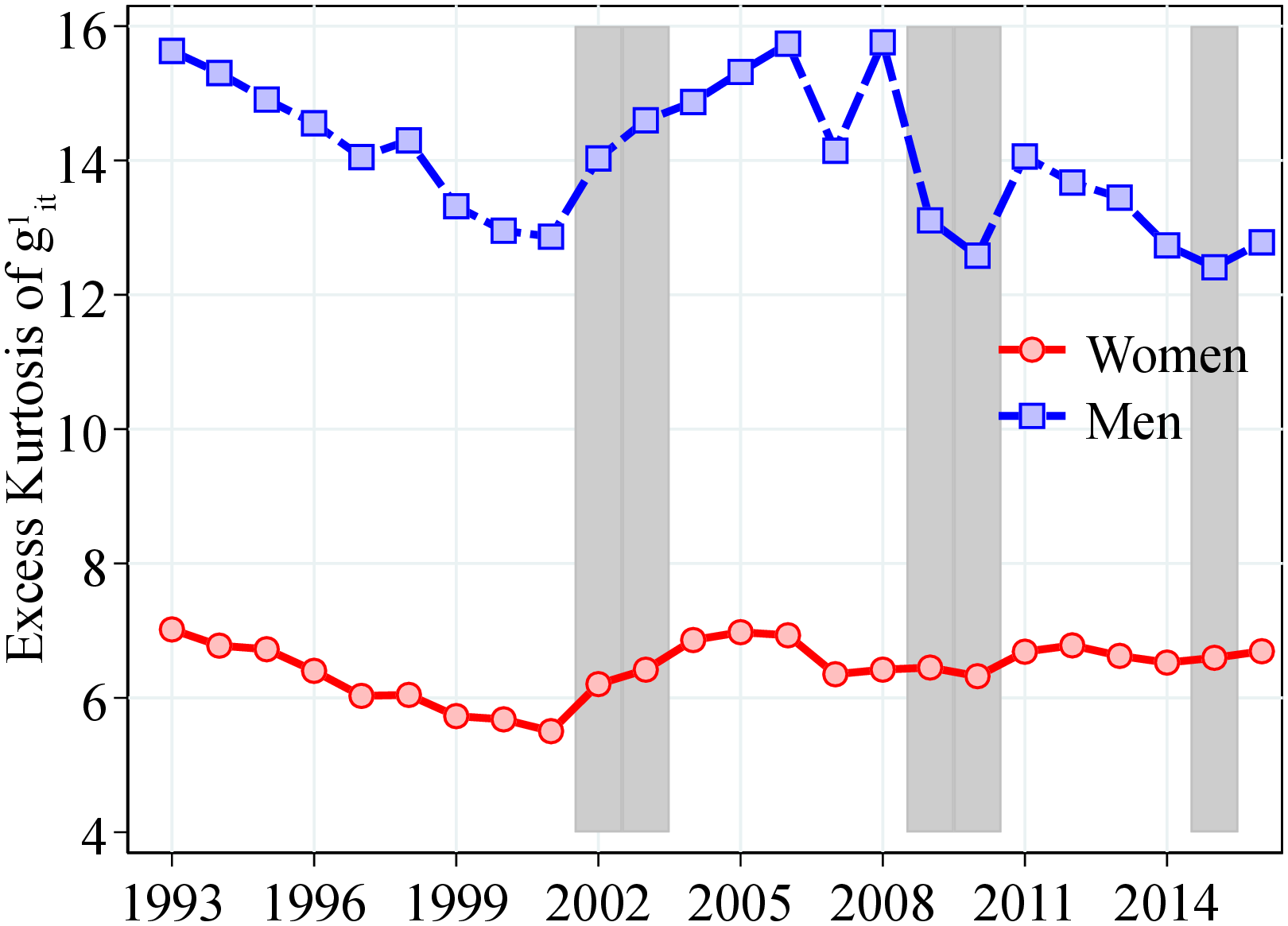

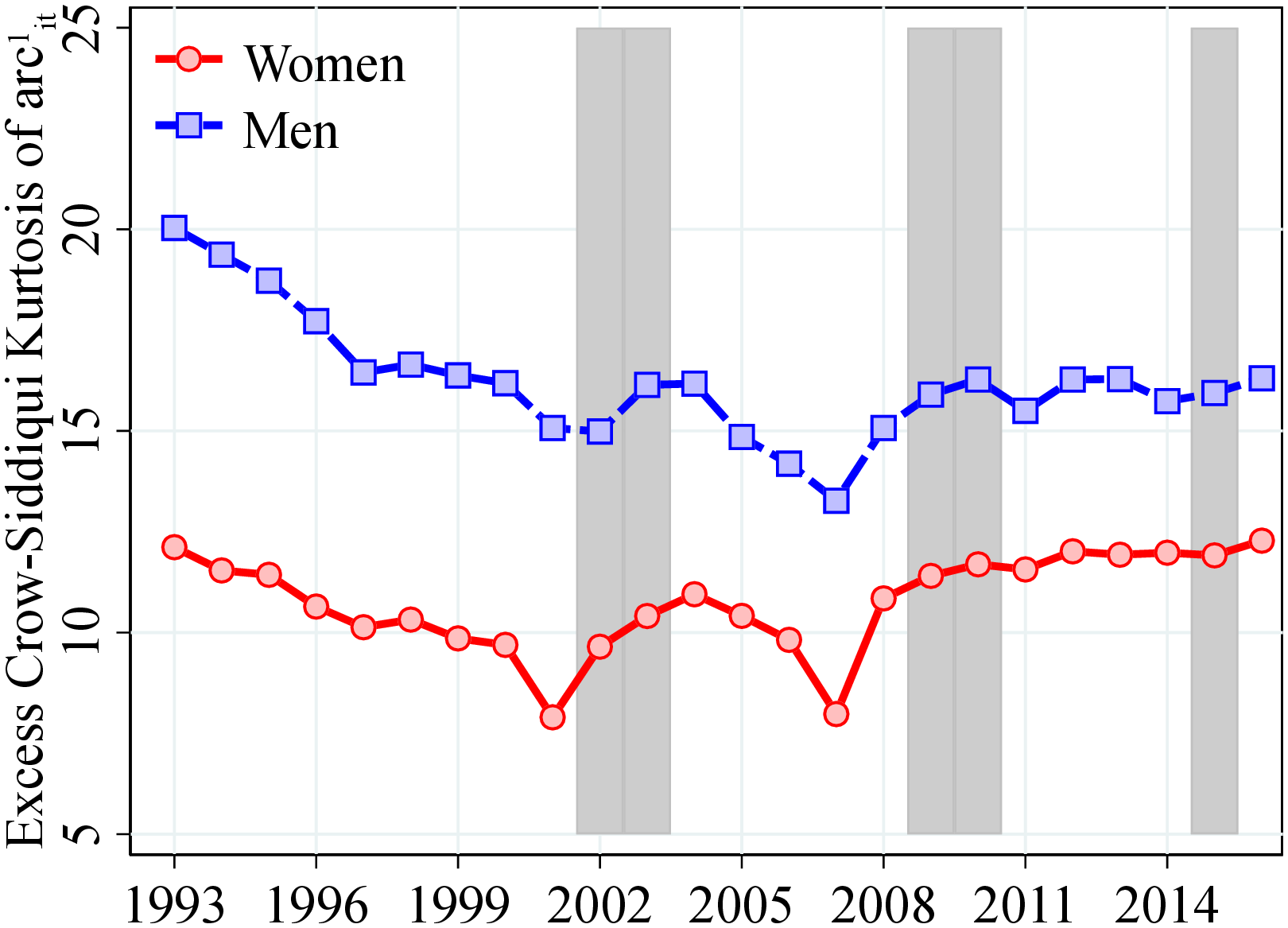

Kurtosis. Figure 4c shows the excess kurtosis of one-year earnings changes for men and women as measured by Crow and Siddiqui (1967) kurtosis, \(\mathcal{C_{K}}=\frac{\text{(P97.5-P2.5)}}{\text{P75-P25}}-2.91\), where 2.91 corresponds to \(\frac{\text{(P97.5-P2.5)}}{\text{P75-P25}}\) of a normal distribution. The kurtosis of earnings growth has remained relatively stable around at 10 over our sample period, showing only a slight increase after the Great Recession for women.13 Again, including public transfers makes income changes less leptokurtic, albeit only very little (Figure A.6).

Notes: Figure 4 shows the P90-P10, Kelley skewness, and excess Crow-Siddiqui kurtosis of earnings growth for men and women. The shaded areas represent recession years, with unemployment growth in the rate of more than 4 pp. and an output gap of more than 5%. See Section 2 for sample selection and definitions.

Cyclical Nature of Individual Earnings Growth. To measure the business-cycle variation in income risk, we estimate time-series regressions of earnings growth moments on the unemployment rate and GDP growth (both standardized). Only some aspects of income risk seem to be cyclical (see Table C.2).14 Even when it is statistically significant, the cyclical variation in income risk is not economically significant except during the Great Recession.15 This result can be partly explained by a coordinated bargaining system between employers, unions, and the government that allows for some wage flexibility to prevent large increases in unemployment (and large declines in earnings) during recessions (Nilsen (2020)).16

3.2.3 Heterogeneity in Idiosyncratic Earnings Changes

We now investigate how the properties of earnings growth vary by age and permanent earnings (PE). Our measure of PE for worker \(i\) in period \(t-1\), \(P_{t-1}^{i}\), is defined as the average earnings between \(t-1\) and \(t-3\) net of age and year effects.17 In each year \(t\) (starting 1996), we first divide workers into three age groups: 25–34, 35–44, and 45–55. Then, within each gender-age group, we rank individuals into 40 quantiles with respect to their level of \(P_{t-1}^{i}\). To capture the earnings risk of top earners, we place the top 0.1% workers in a separate group. Finally, within each quantile, we compute moments of residual earnings growth, \(g_{it}^{k}\), between periods \(t\) and \(t+k\). The conditional distribution of earnings growth can be thought of as the income uncertainty that workers of the same gender, age, and PE face looking ahead. In our figures, we plot the average of these moments over the 17 years between 1996 and 2012, which is the last year we can compute five-year earnings growth.

(a) Men

(a) Men  (b) Women

(b) Women

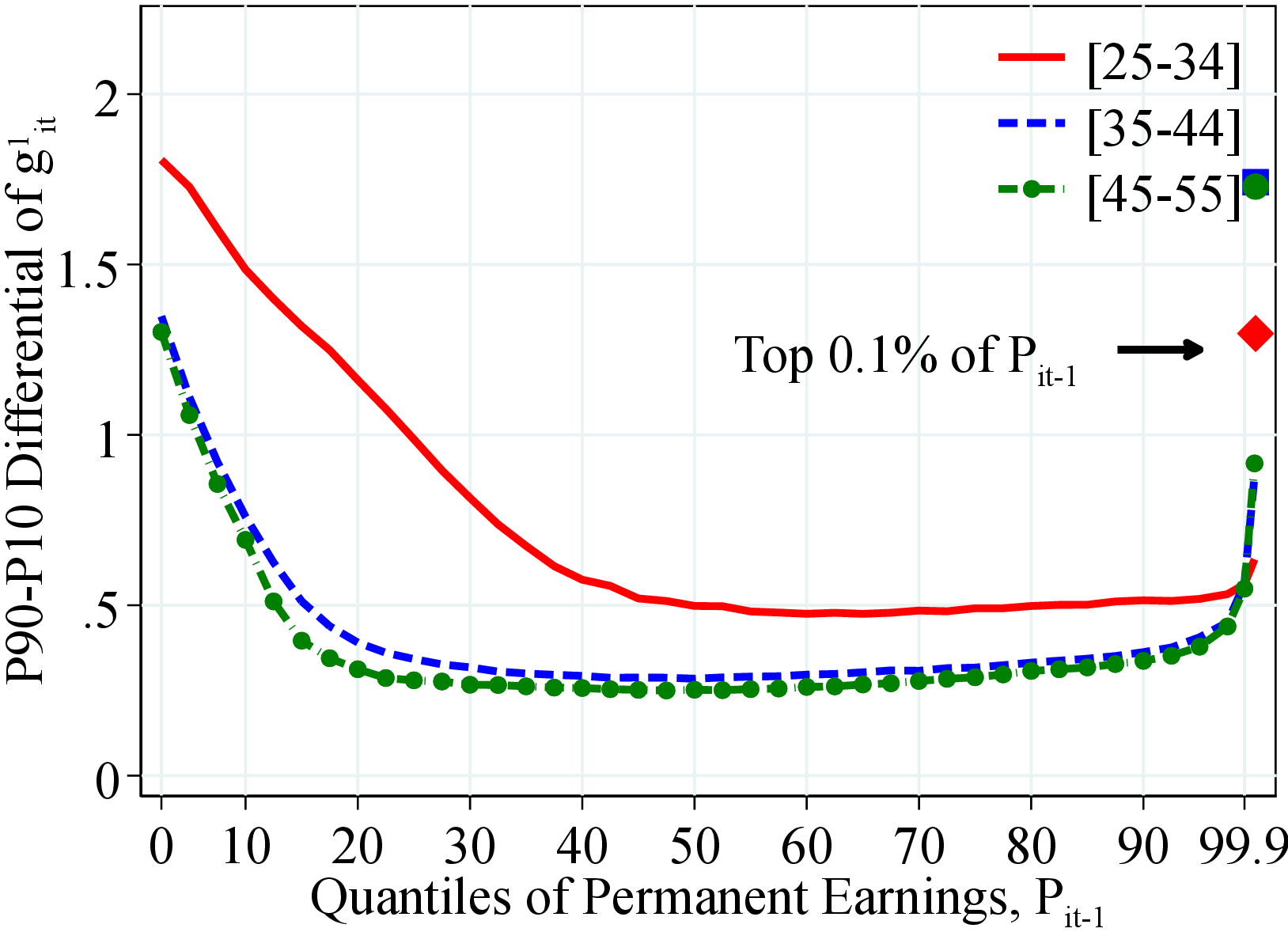

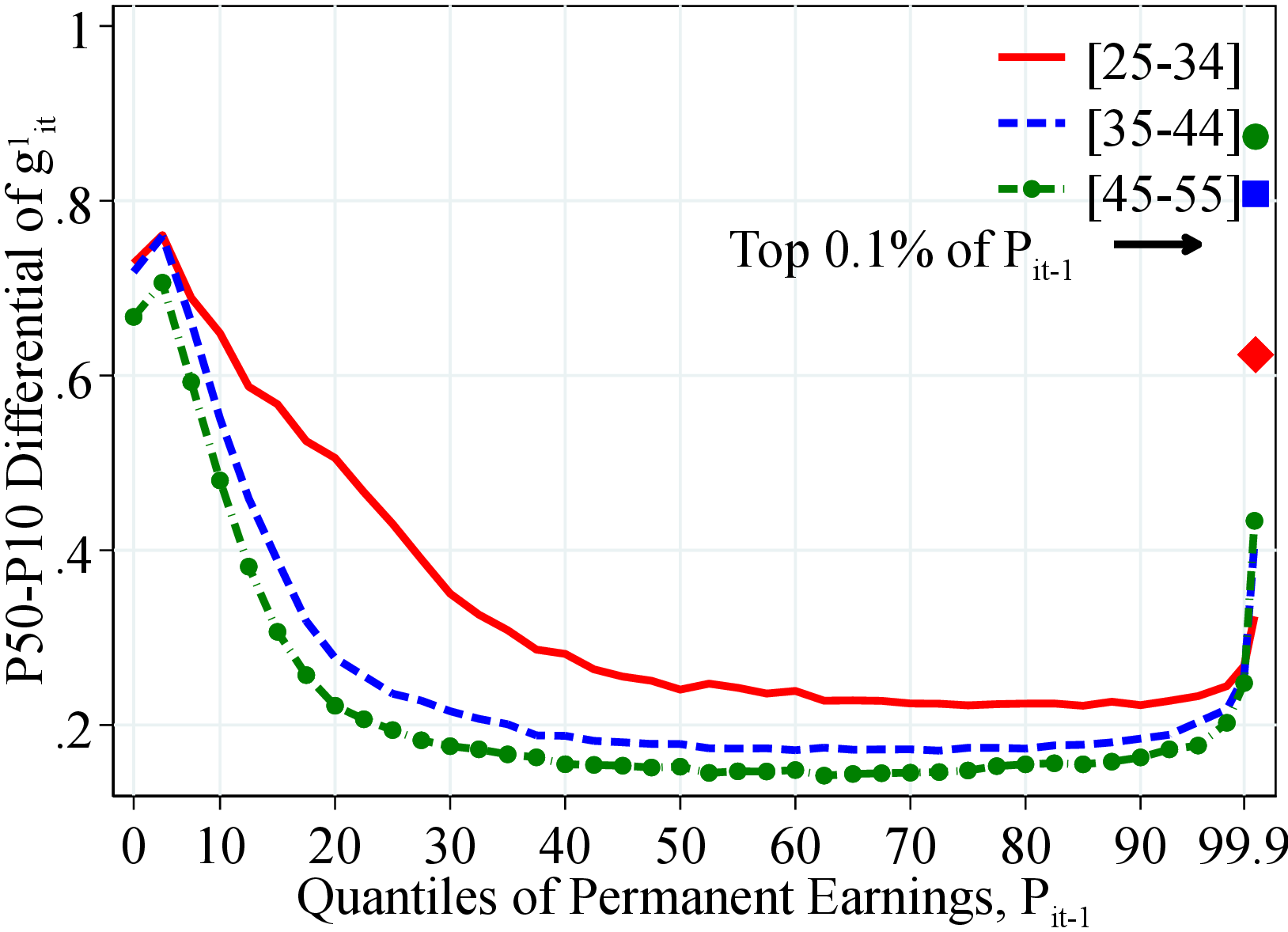

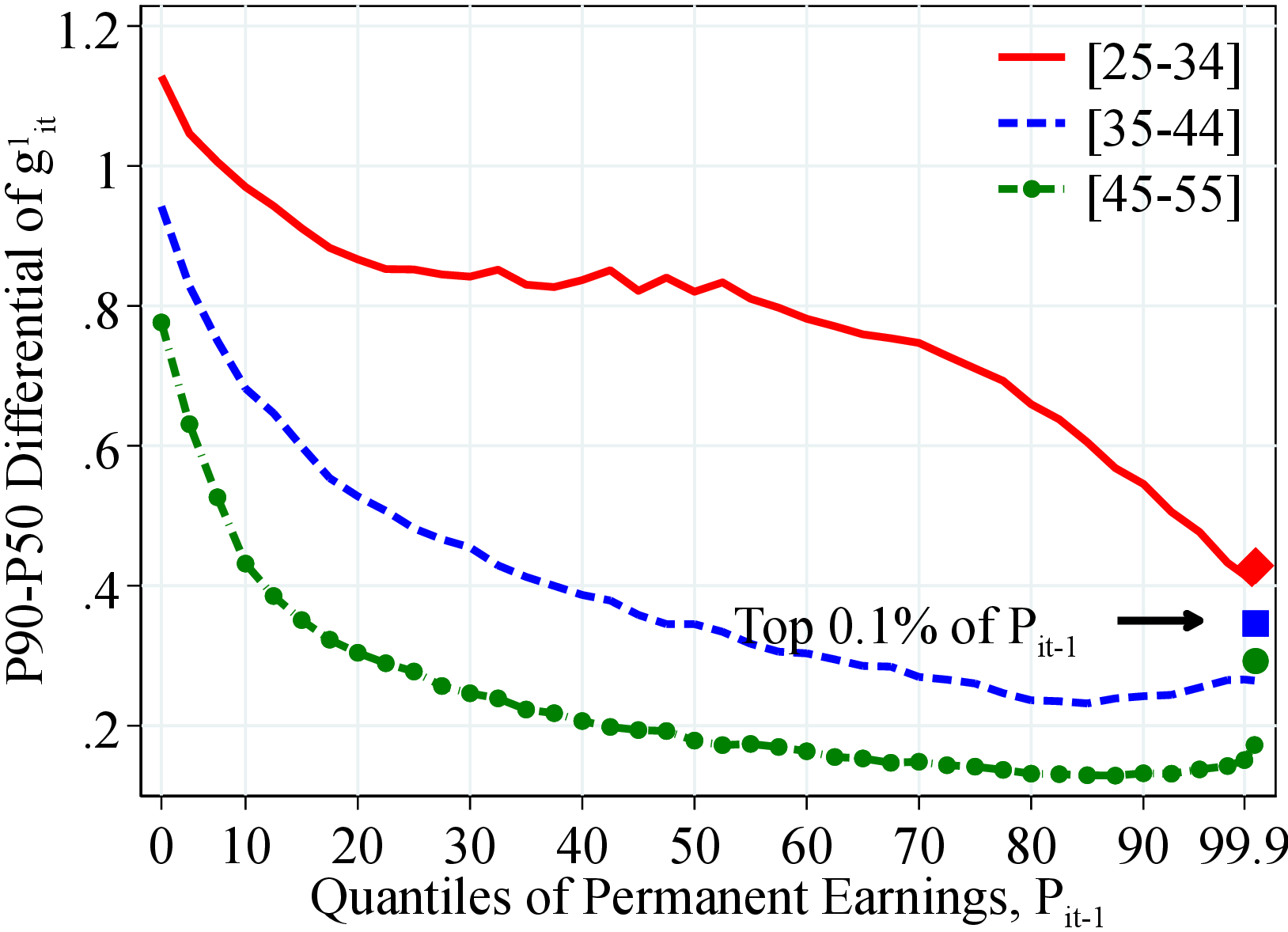

Figure: Figure 5 – Dispersion of Earnings Growth by Permanent Earnings and Age

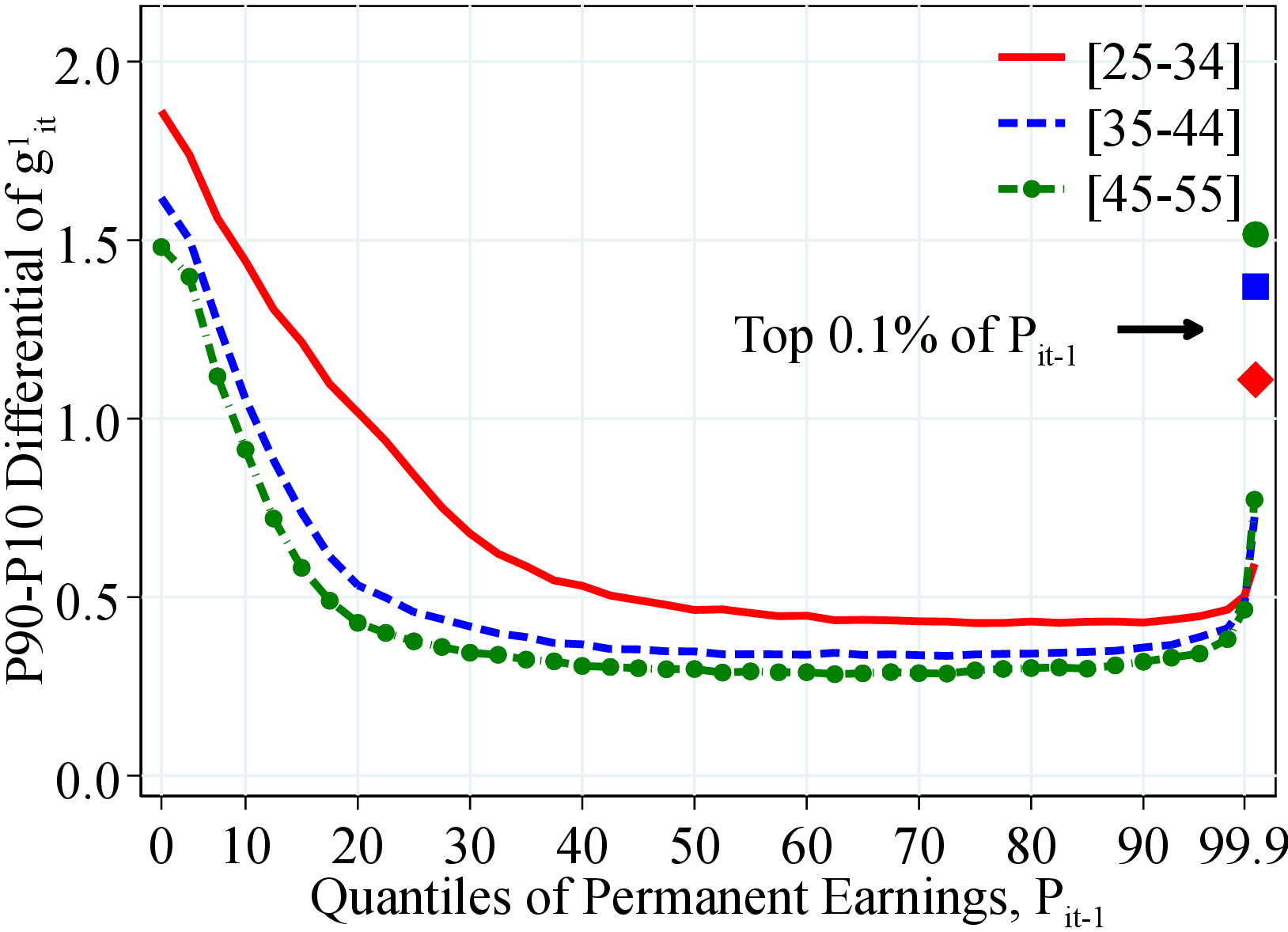

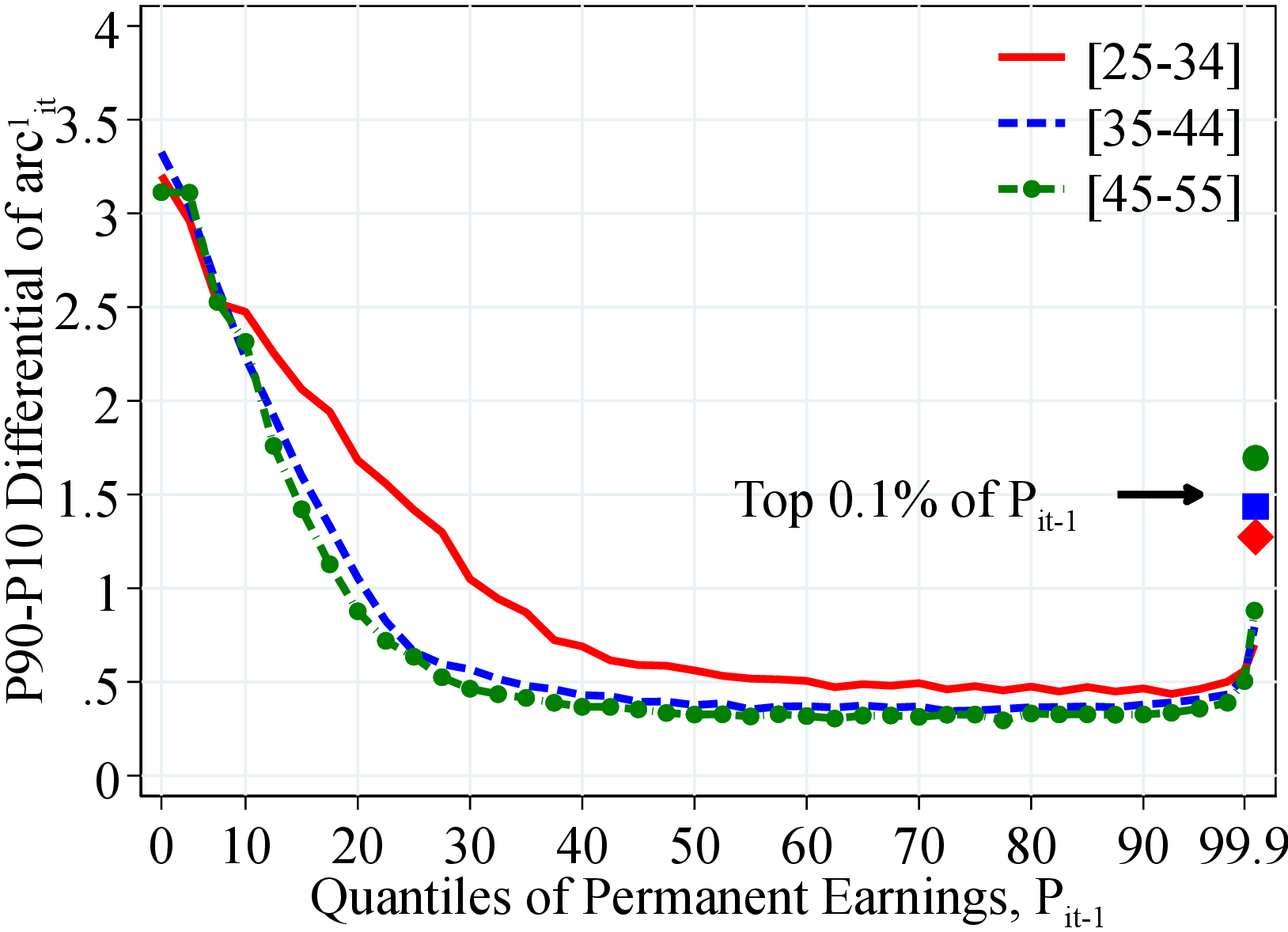

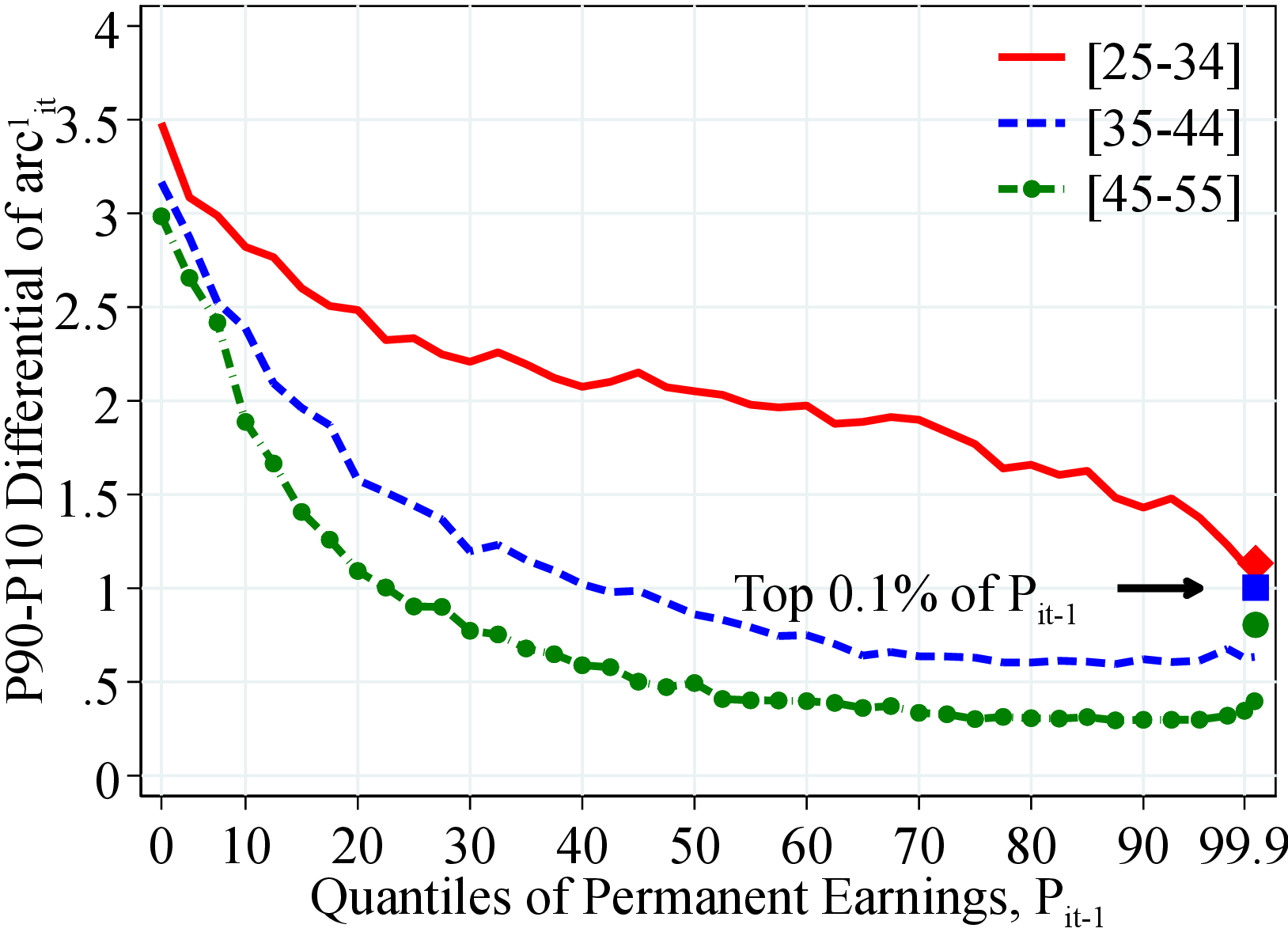

Notes: Figure 5 shows the P90-P10 of the log growth rate of residual earnings for men and women within quantiles of the PE distribution, \(P_{it-1}\). The solid markers represent P90-P10 for those workers at the top 0.1% of the PE distribution for different age groups (diamond for 25 to 34 years old, square for 35 to 44 years old, and circle for 45 to 55 years old).

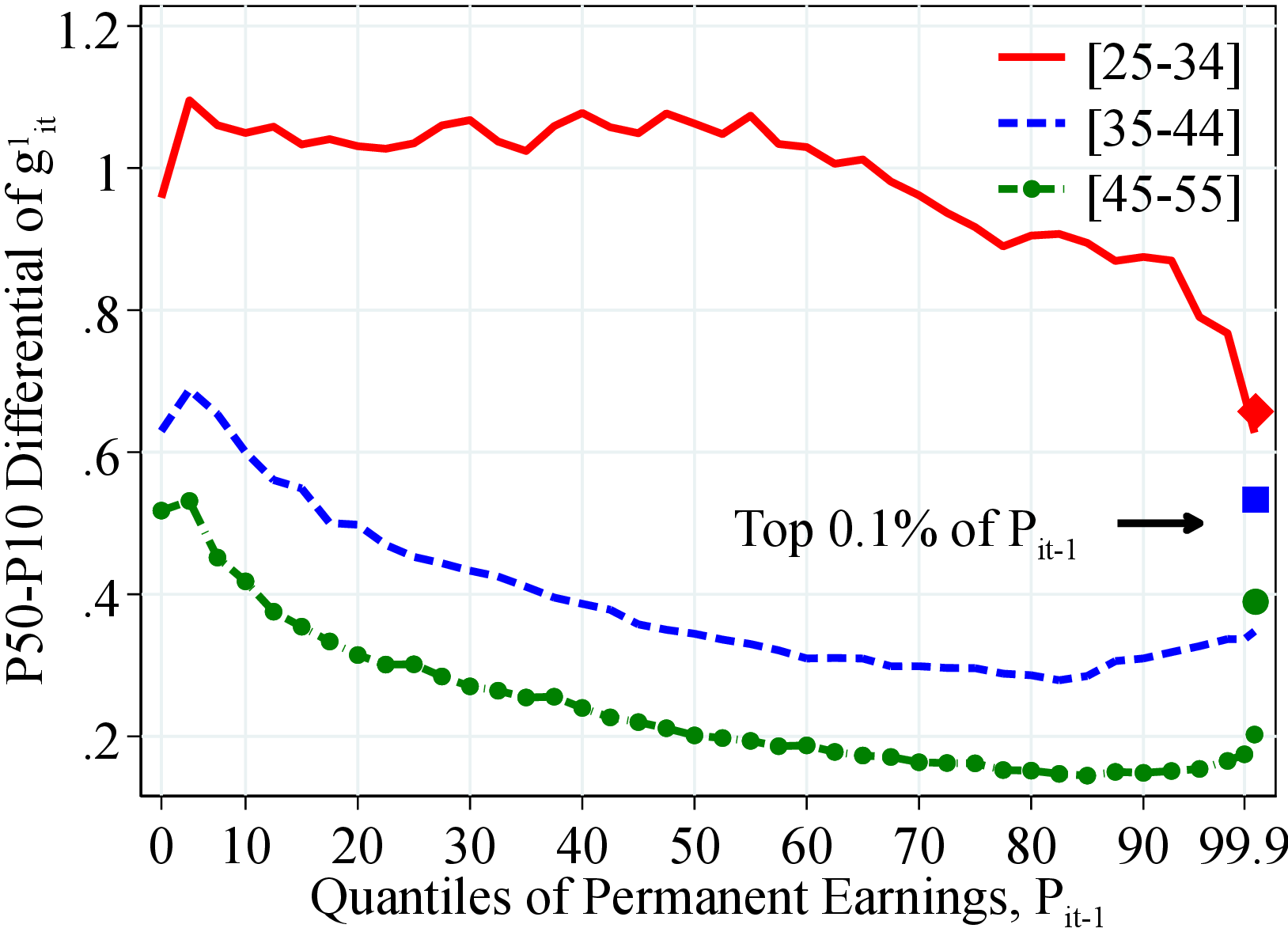

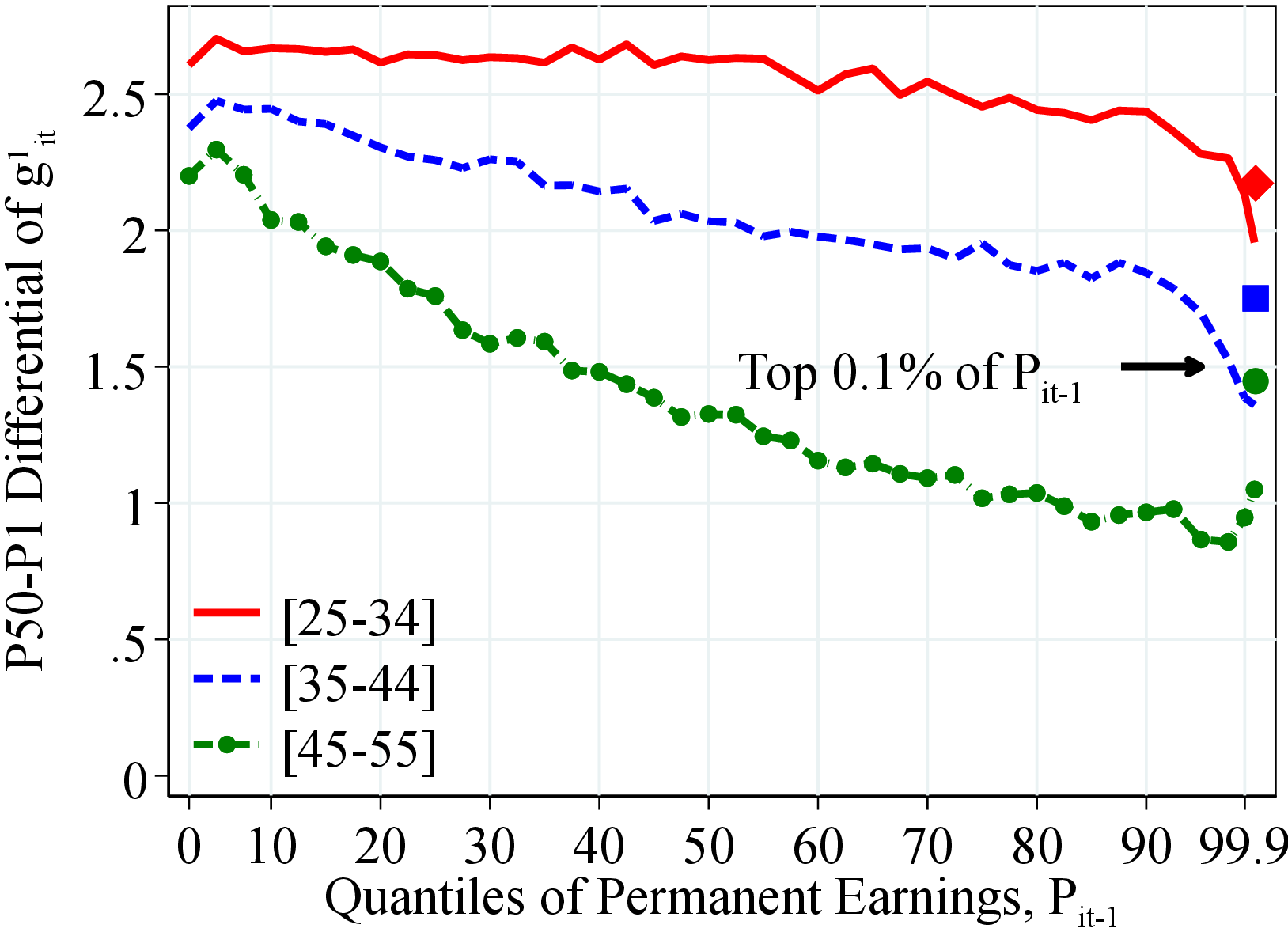

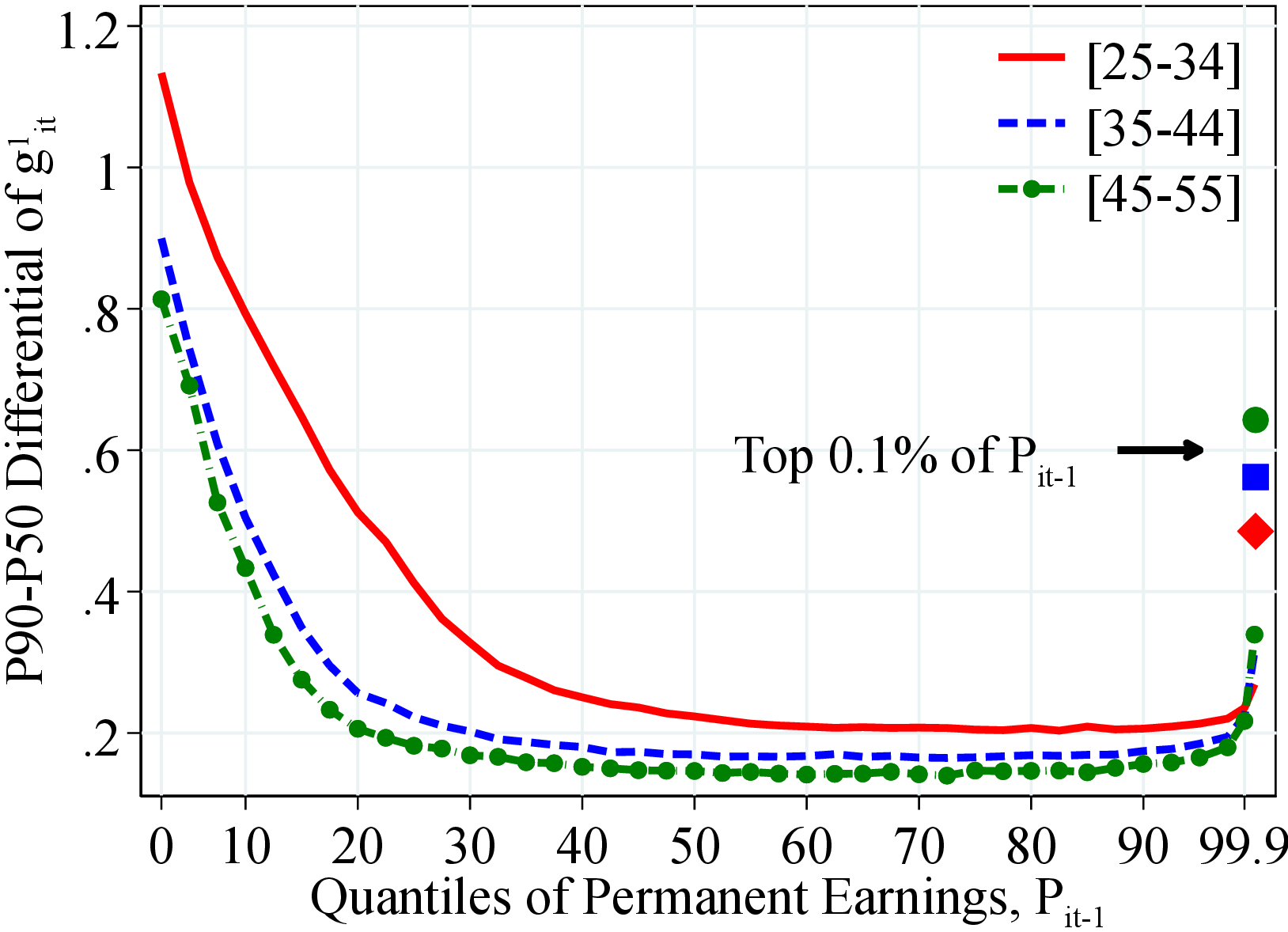

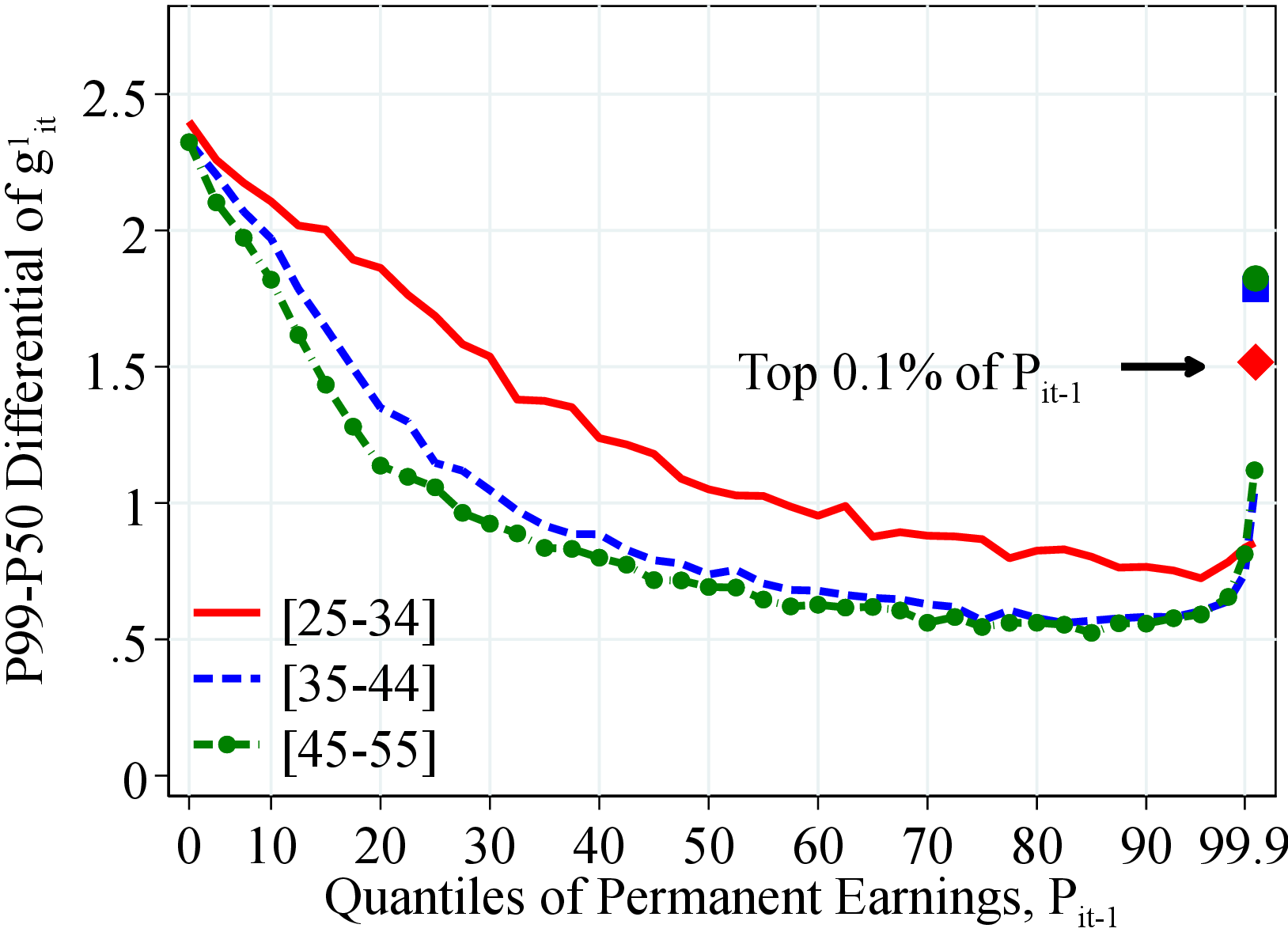

Heterogeneity in Volatility. For men and women, the dispersion of earnings changes steeply declines from low-income workers to those around and above the median of the PE distribution (Figure 5). Earnings growth dispersion is relatively flat between the 40th and 97th percentiles and only increases at the top of the PE distribution. This finding is consistent with top earners being more likely to have performance-based compensation (e.g., Parker and Vissing-Jorgensen (2010)). Notice also the significant age variation in volatility among women, as young women face the most volatile earnings (similar patterns are found for U.S. males (Karahan and Ozkan (2013))).

(a) Men

(a) Men  (b) Women

(b) Women

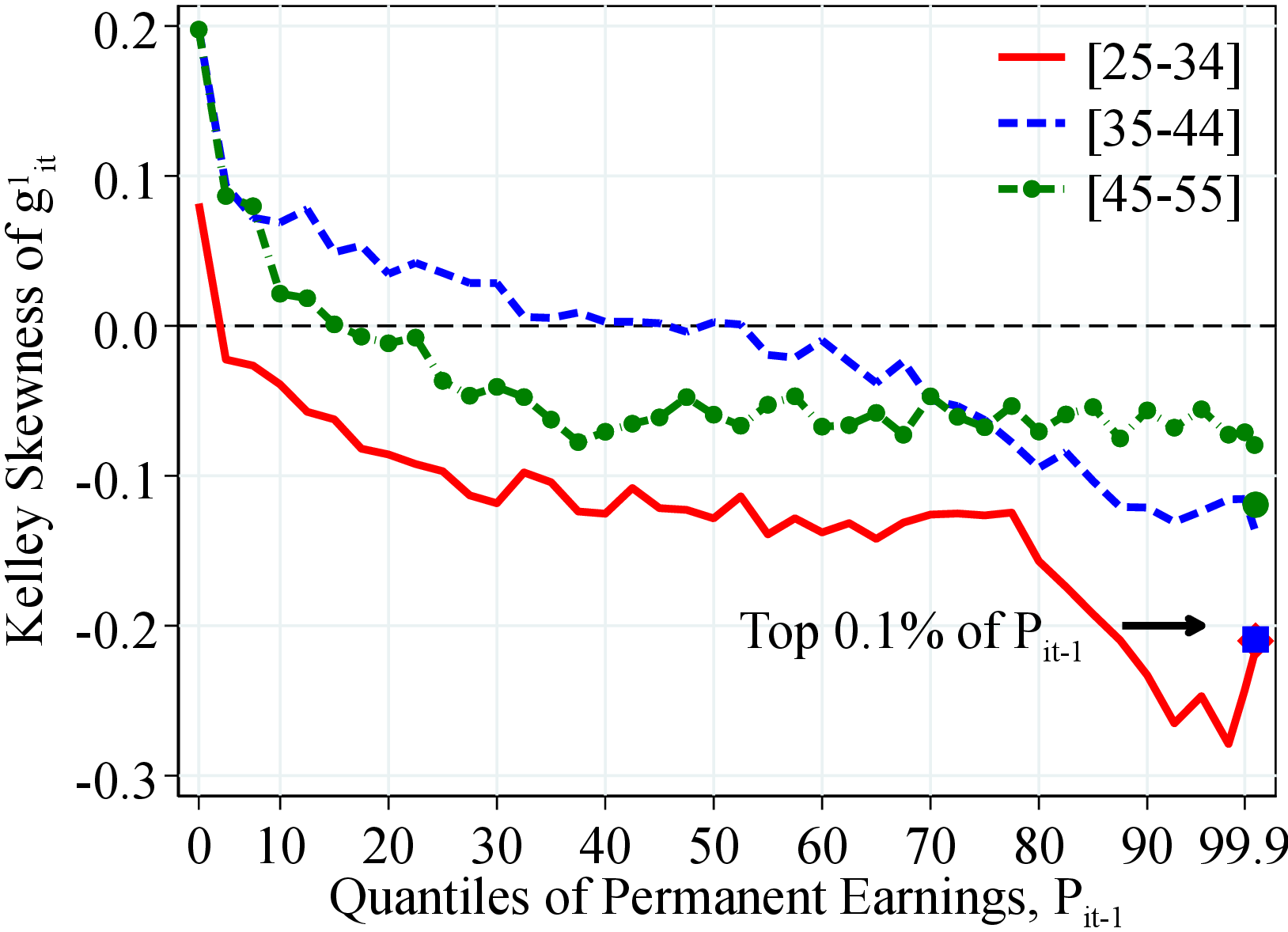

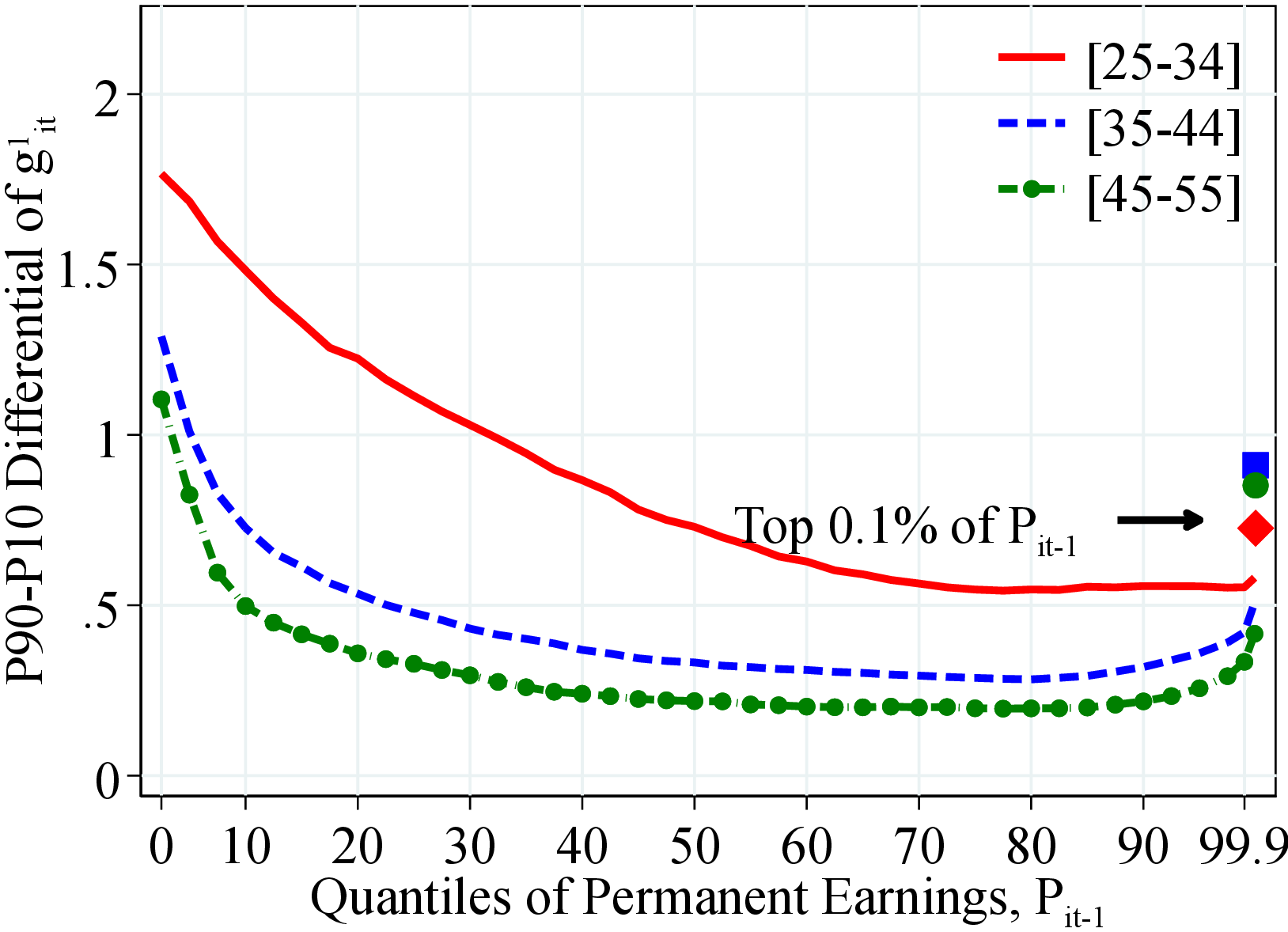

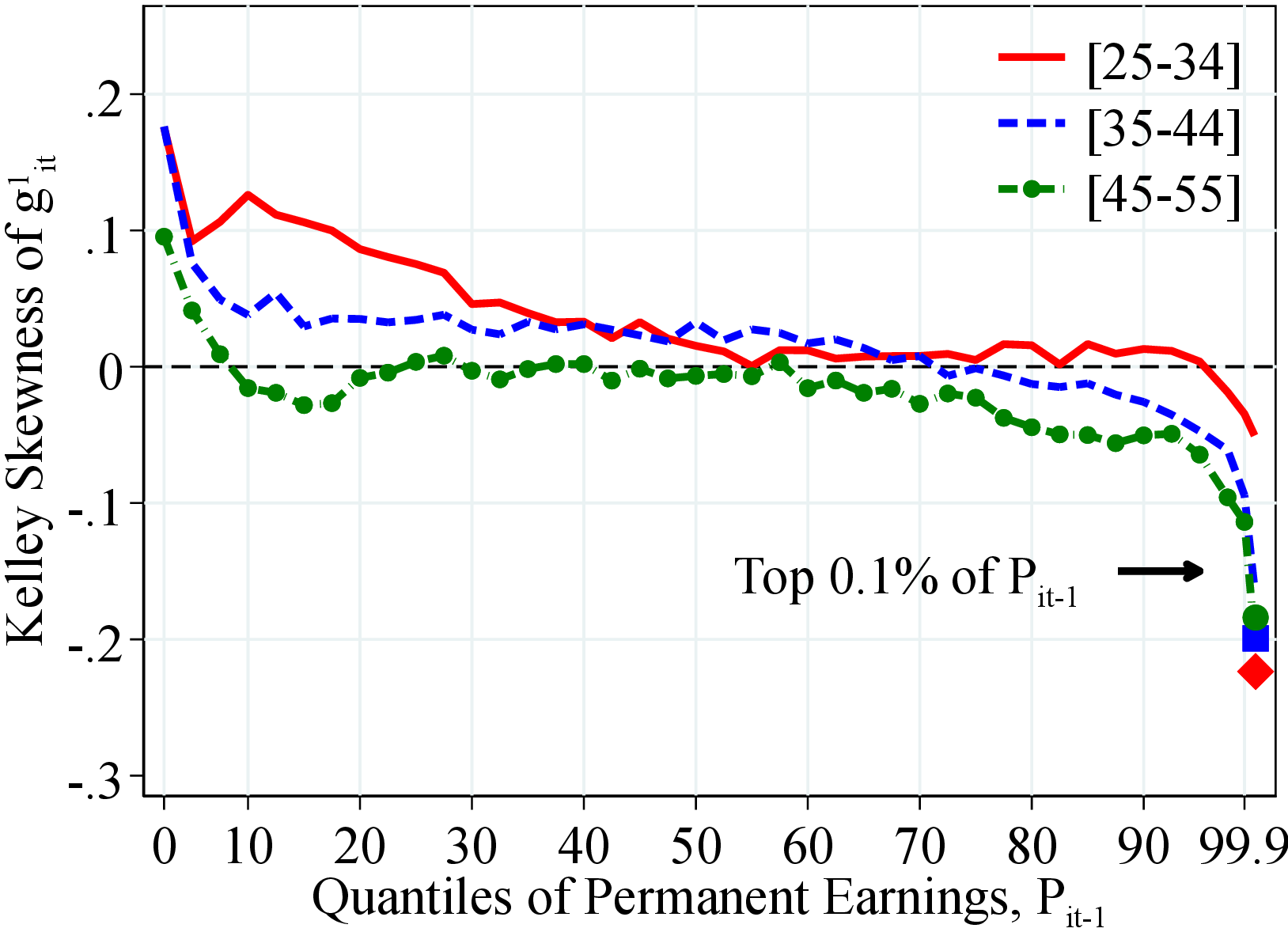

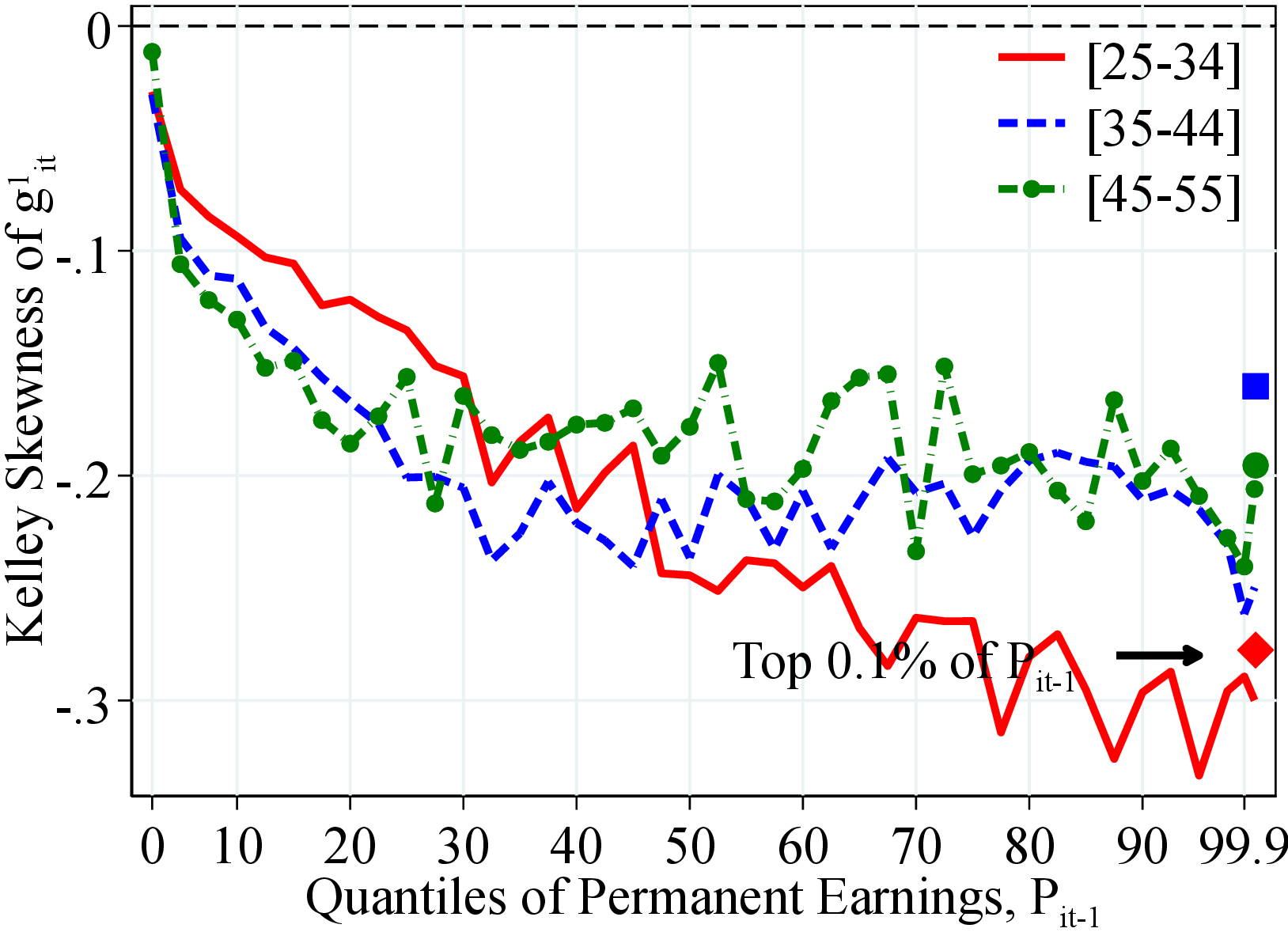

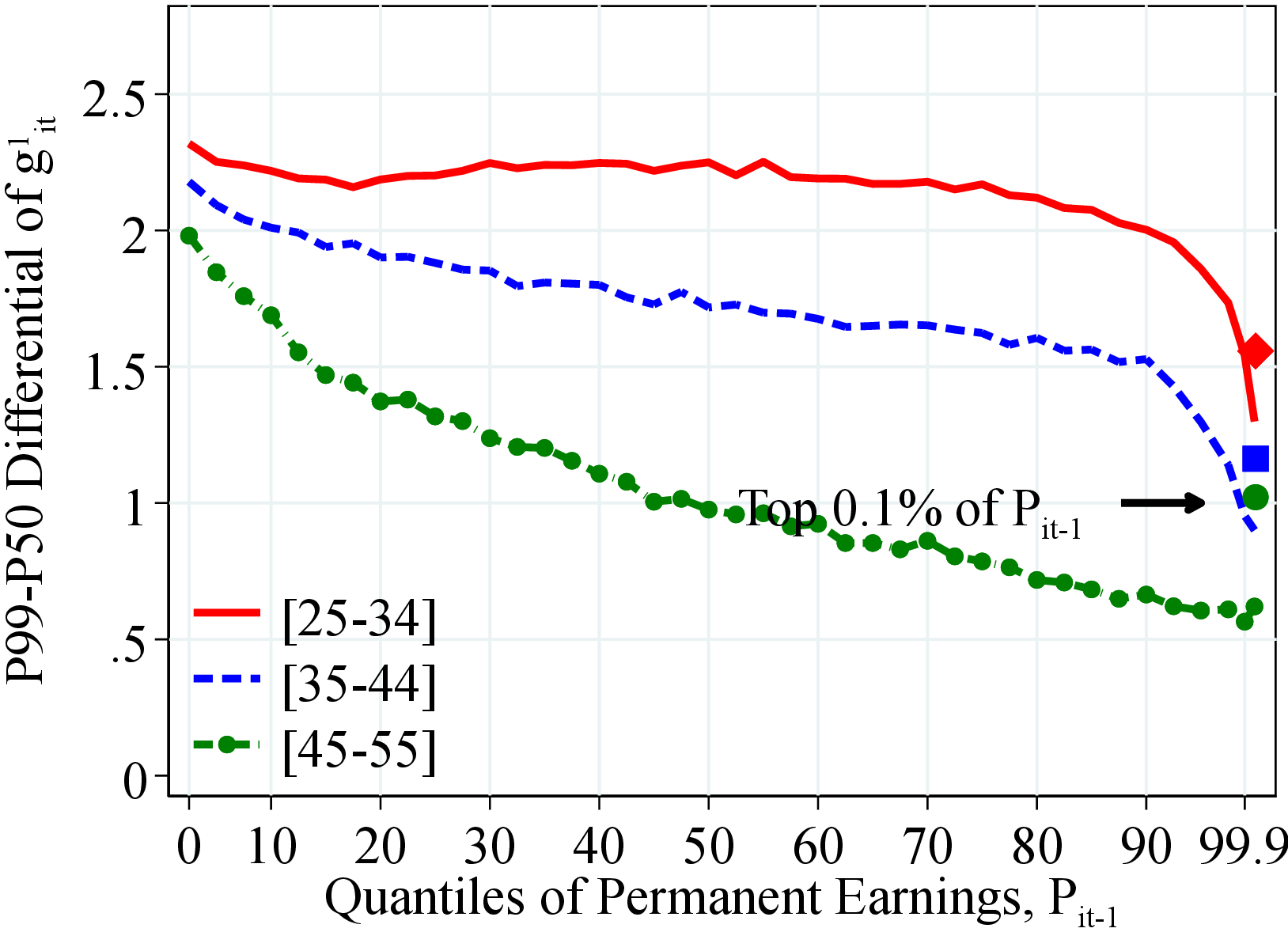

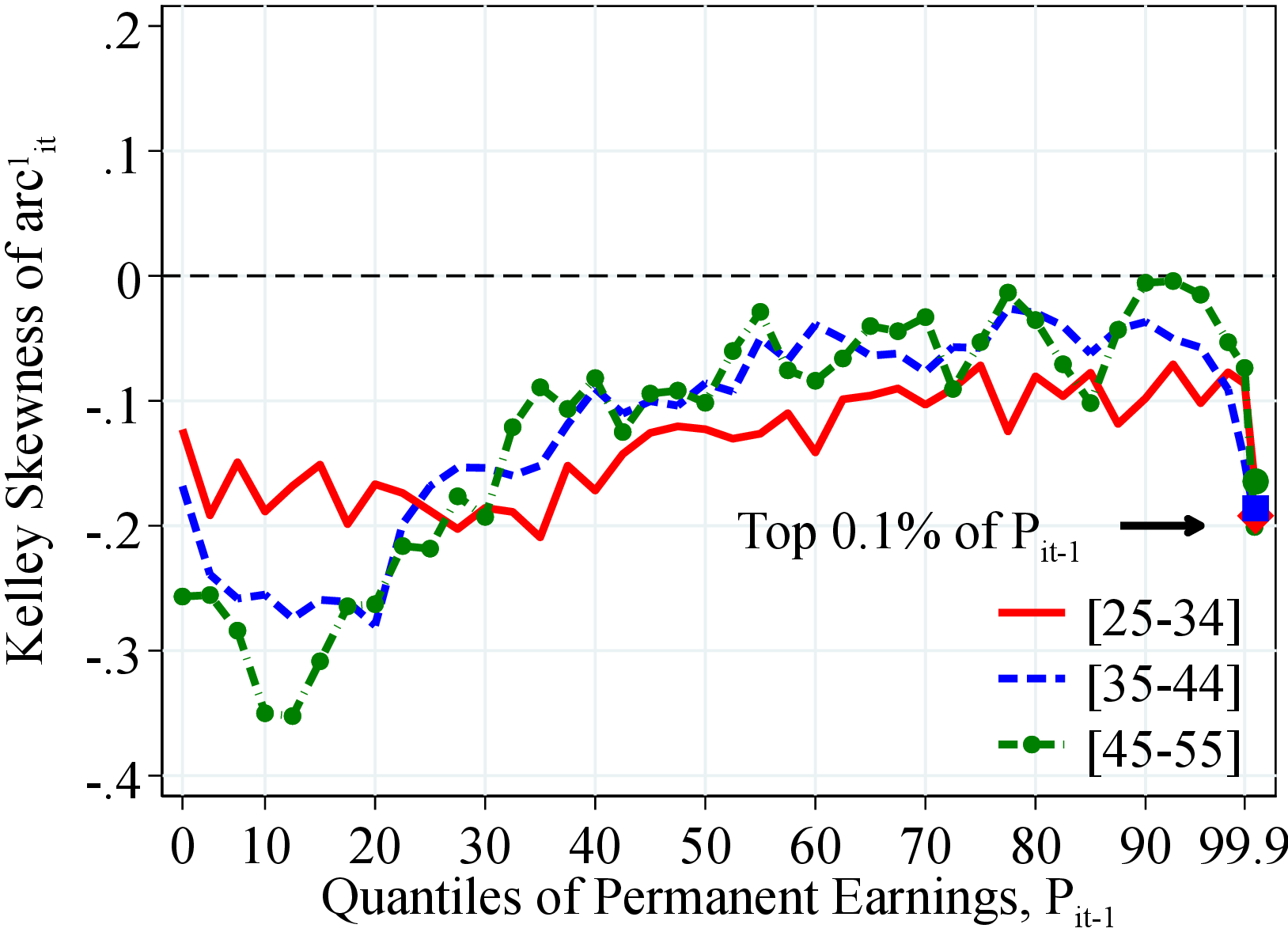

Figure: Figure 6 – Kelley Skewness of Earnings Growth by Permanent Earnings and Age

Notes: Figure 6 shows the Kelley skewness of the log growth rate of residual earnings for men and women within quantiles of the PE distribution, \(P_{it-1}\). The solid markers represent P90-P10 for those workers at the top 0.1% of the PE distribution for different age groups (diamond for 25 to 34 years old, square for 35 to 44 years old, and circle for 45 to 55 years old).

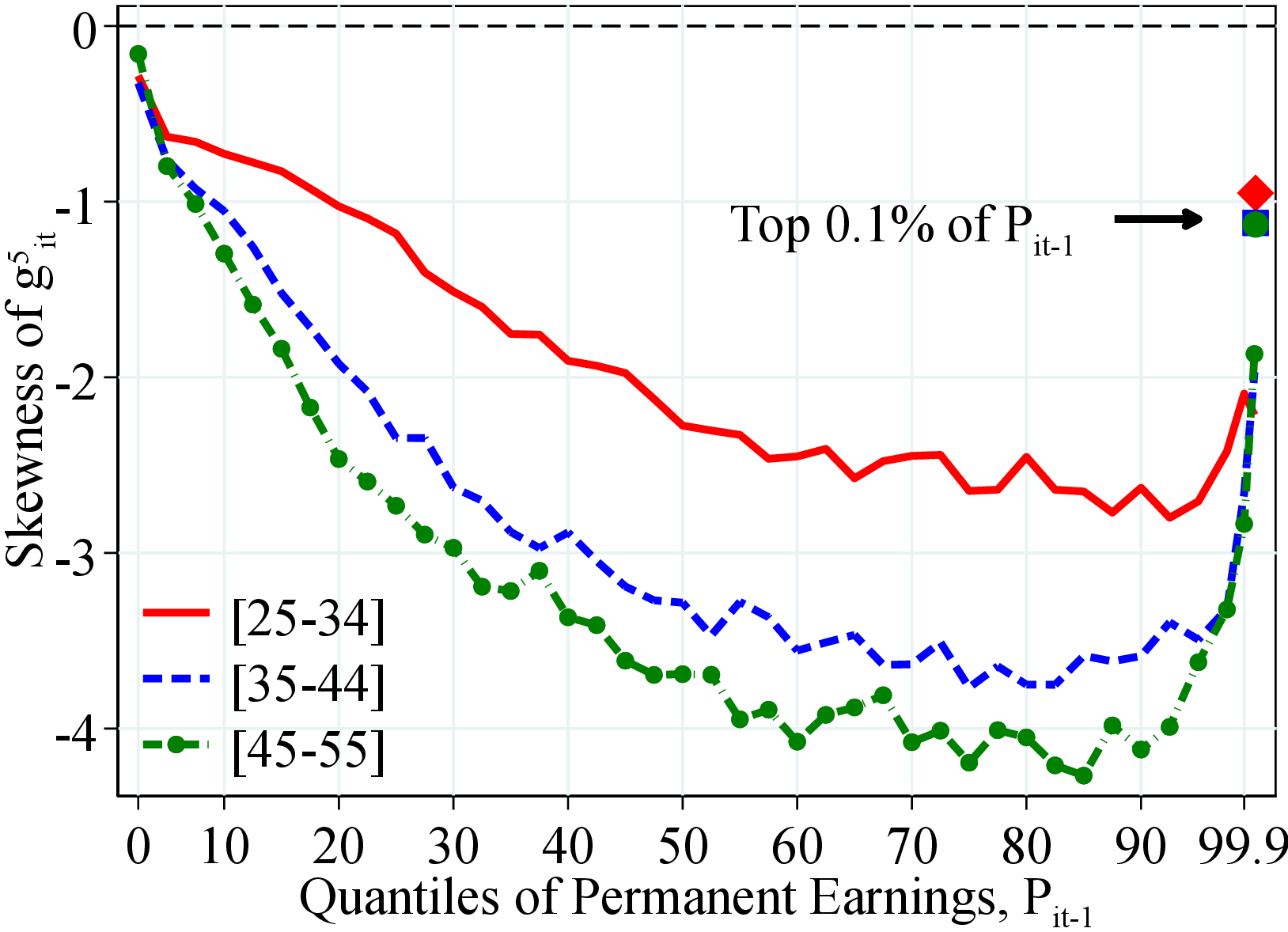

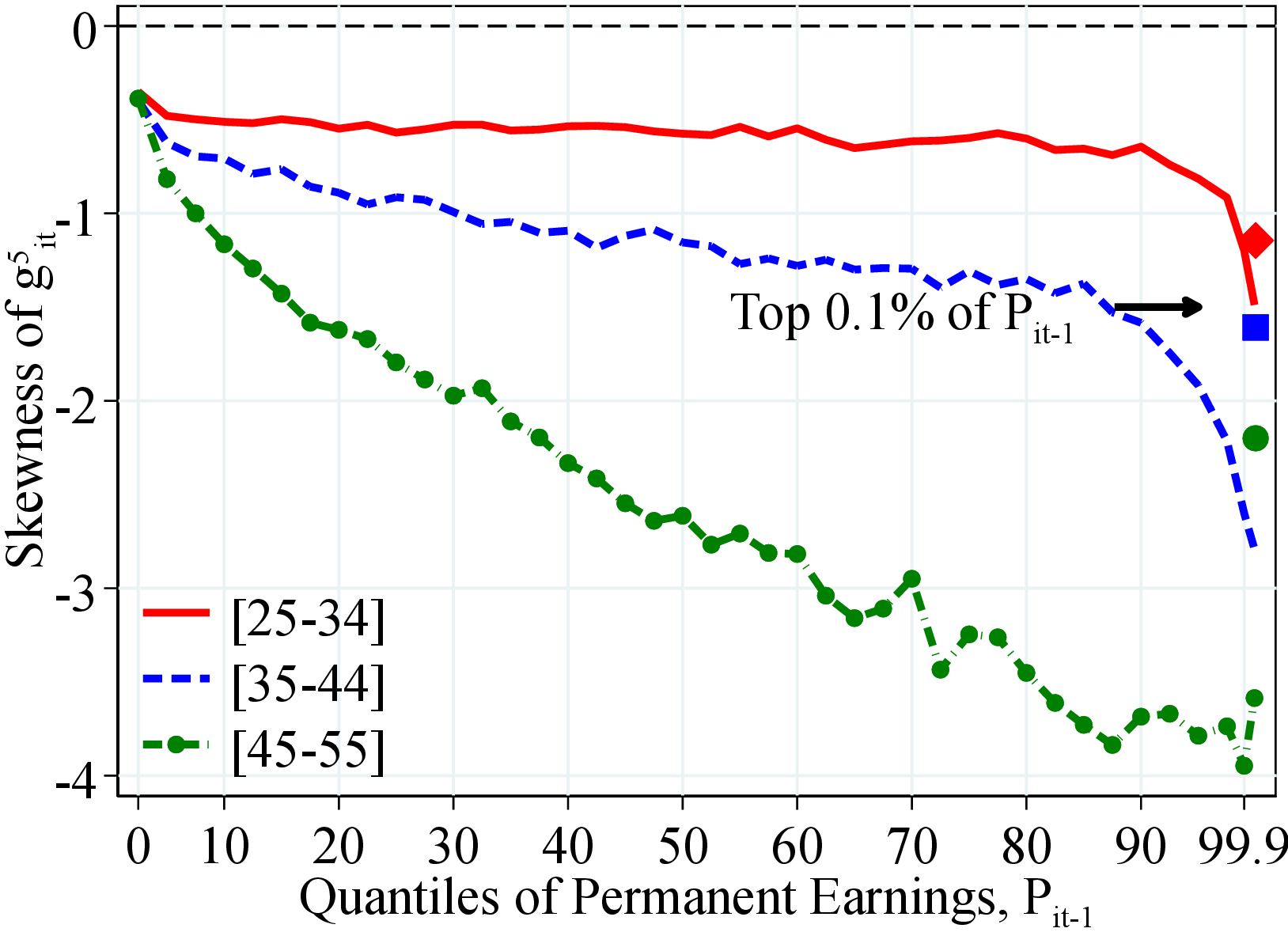

Heterogeneity in Skewness. Skewness declines as we move from low to high PE workers (Figure 6). This decline is more marked for women than for men. In fact, for men between the 30th and 80th percentiles, skewness is mostly flat and close to zero and only drops significantly at the very top of the PE distribution. Furthermore, earnings growth becomes more left skewed over the life cycle, with the largest differences being between the youngest and the oldest age groups. Overall, the variation in skewness by PE and age is similar to the variation found for the U.S. (see Guvenen et al. (2021)).

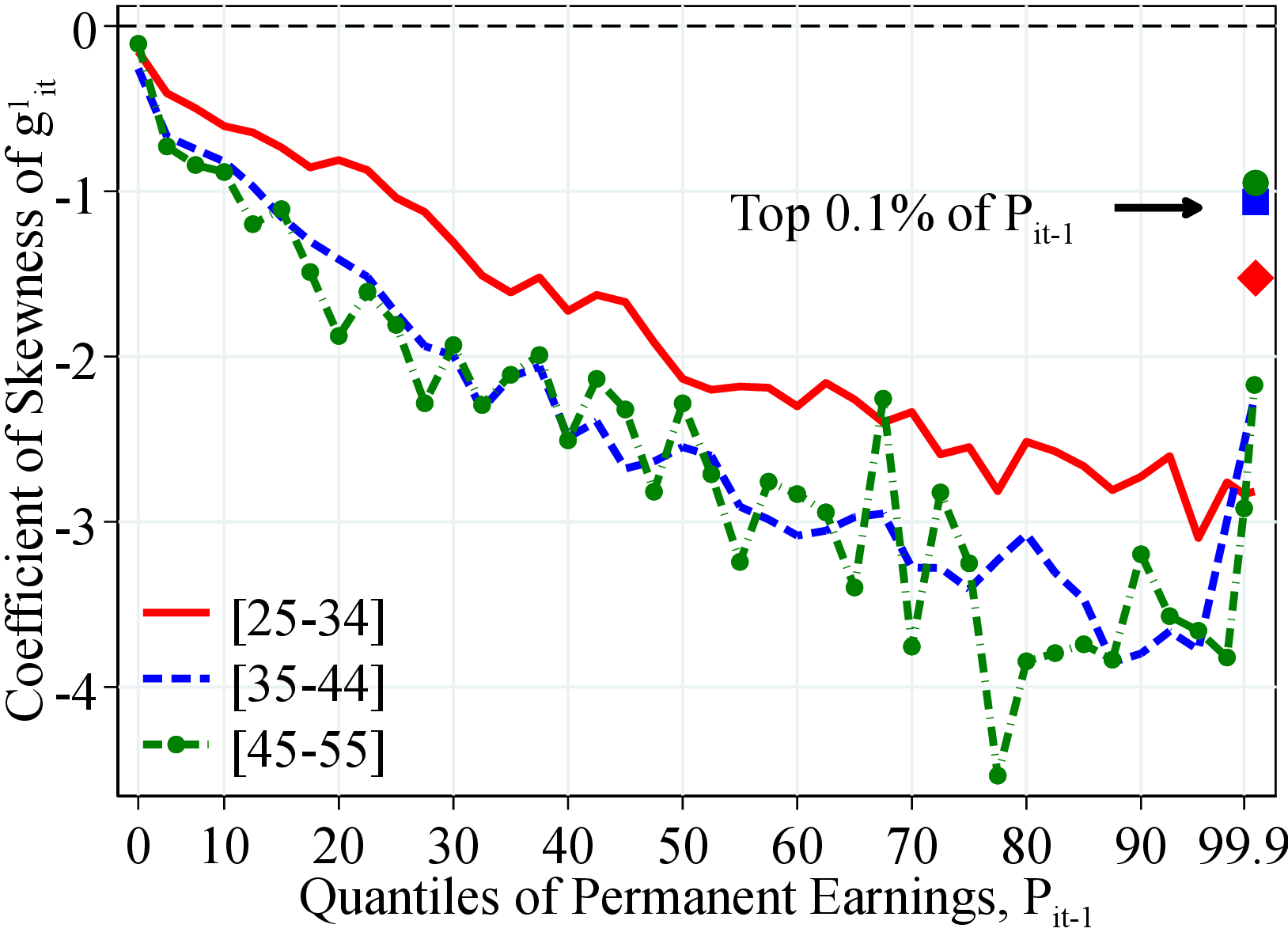

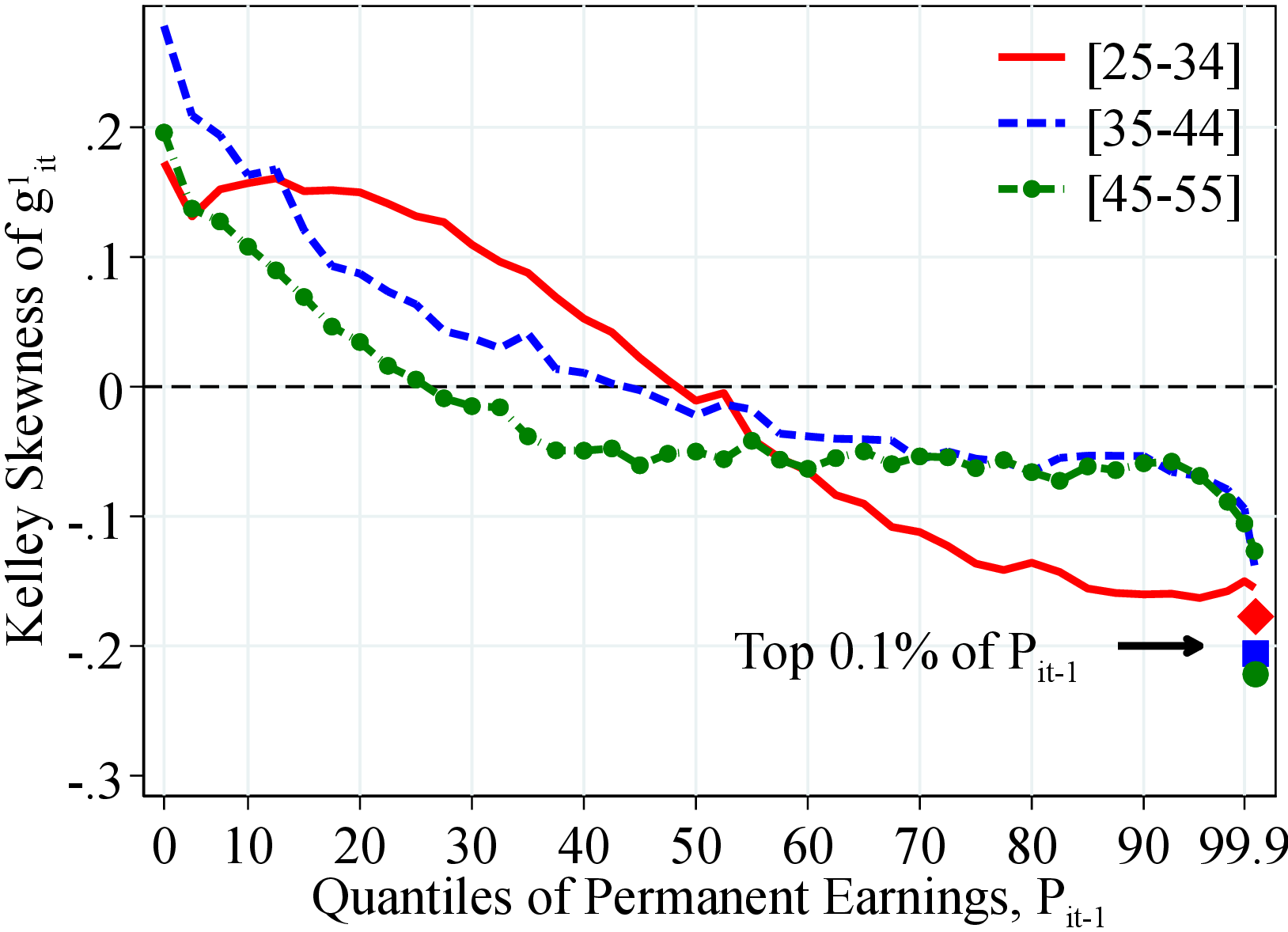

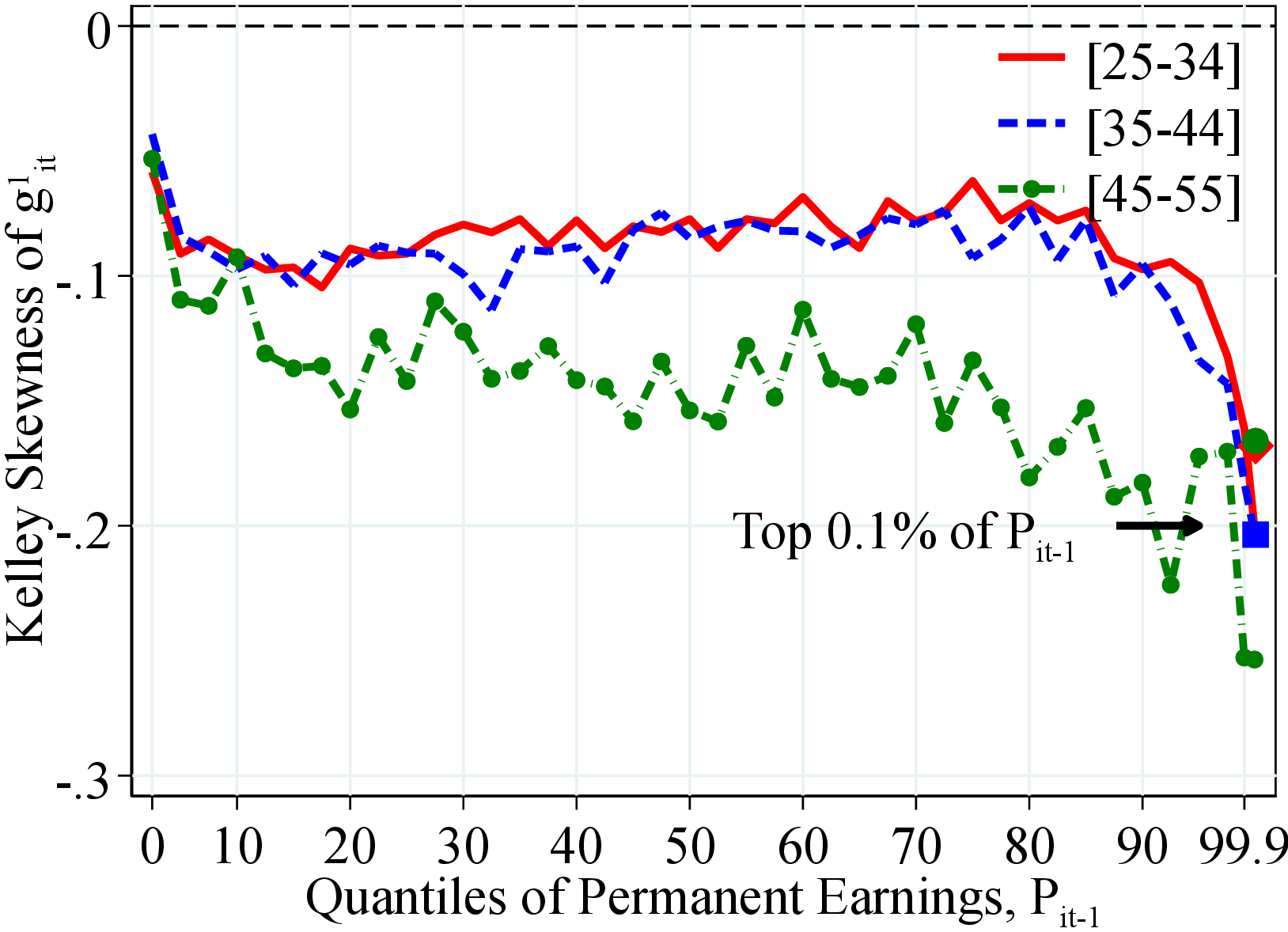

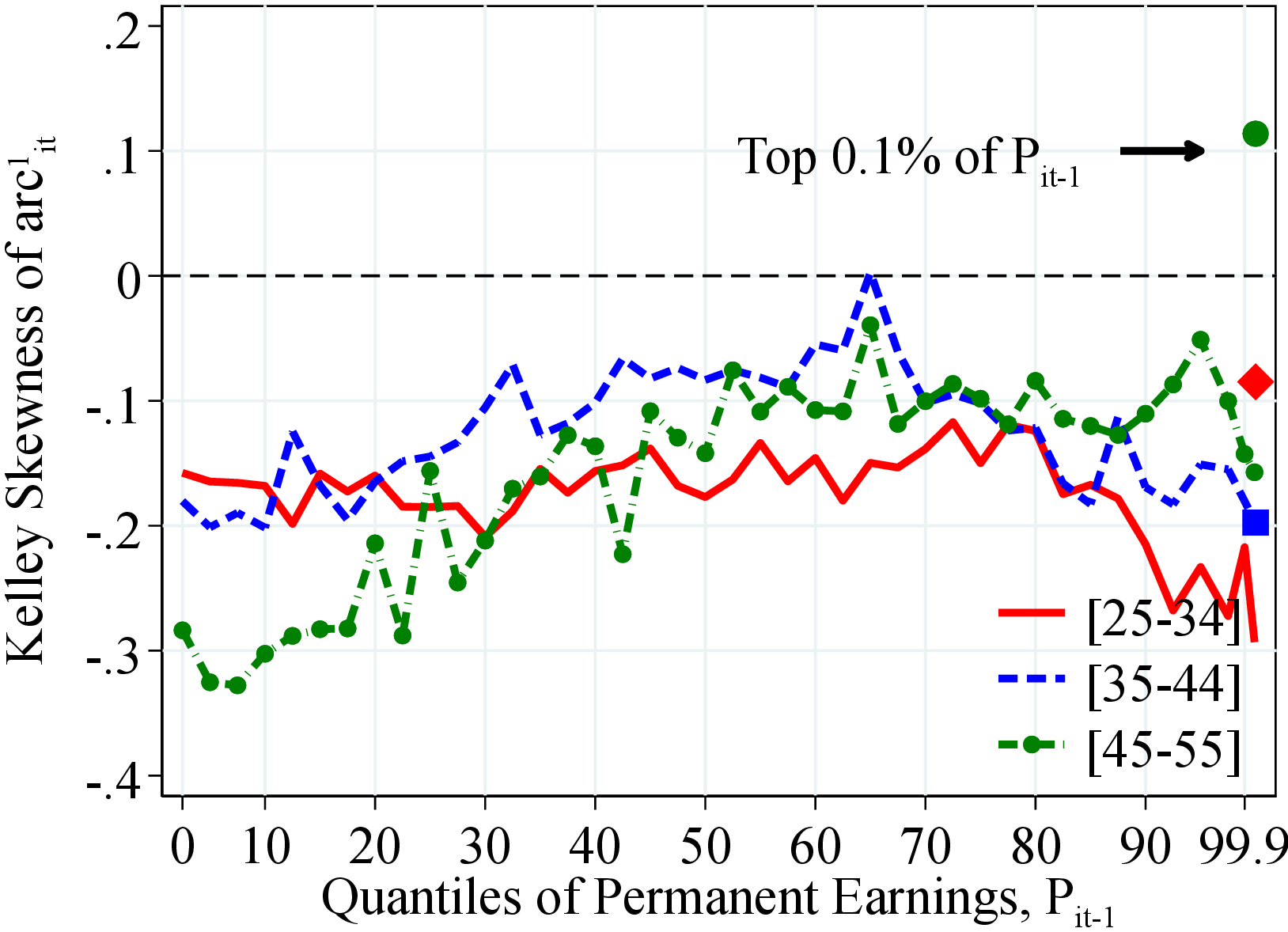

Again, the standardized third moment depicts different patterns compared with the Kelley measure: it is significantly negative and declines substantially from the bottom to the top of the PE distribution (Figure 7). Furthermore, for the top 0.1% workers (except for the youngest women), earnings growth is less left skewed relative to other high-income peers, suggesting that a significant fraction of them experience large positive earnings changes. The marked differences between these two measures highlight the importance of considering the entire distribution when analyzing higher-order moments.18

(a) Men

(a) Men  (b) Women

(b) Women

Figure: Figure 7 – Skewness of Earnings Growth by Permanent Earnings and Age

Notes: Figure 7 shows the coefficient of skewness (third standardized moment) of the log growth rate of residual earnings for men and women within quantiles of the PE distribution, \(P_{it-1}\). The solid markers represent the top 0.1% of the PE.

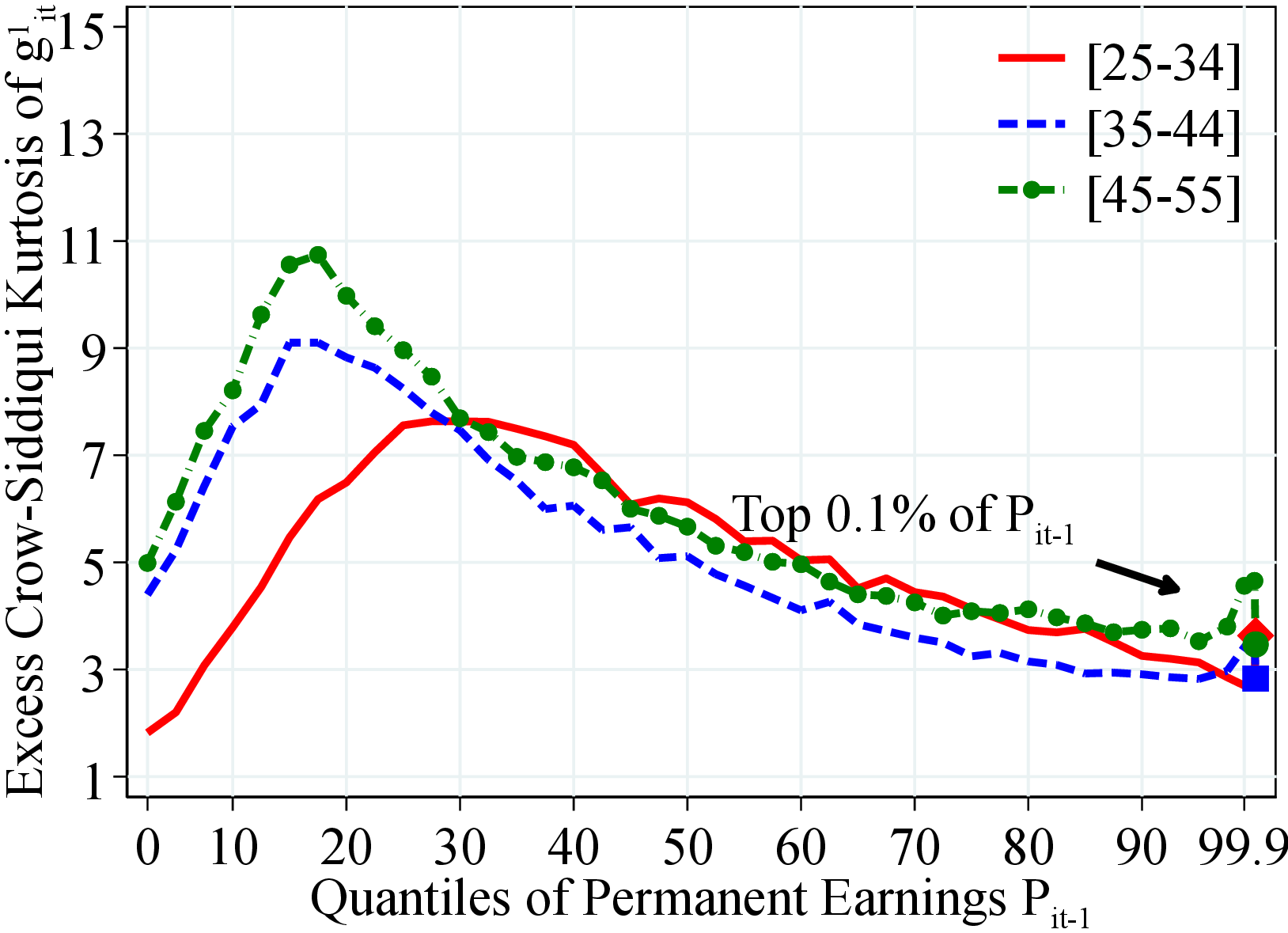

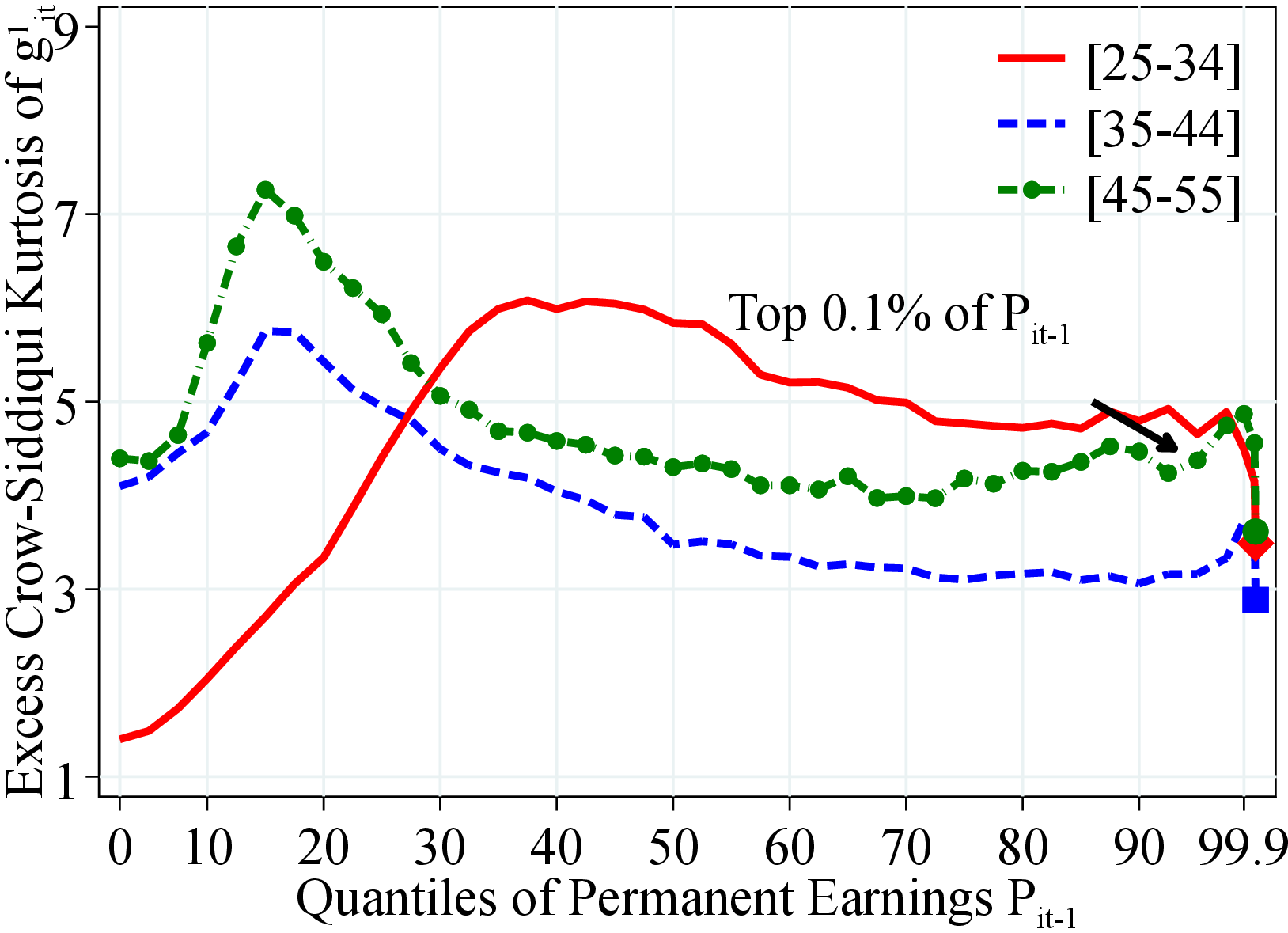

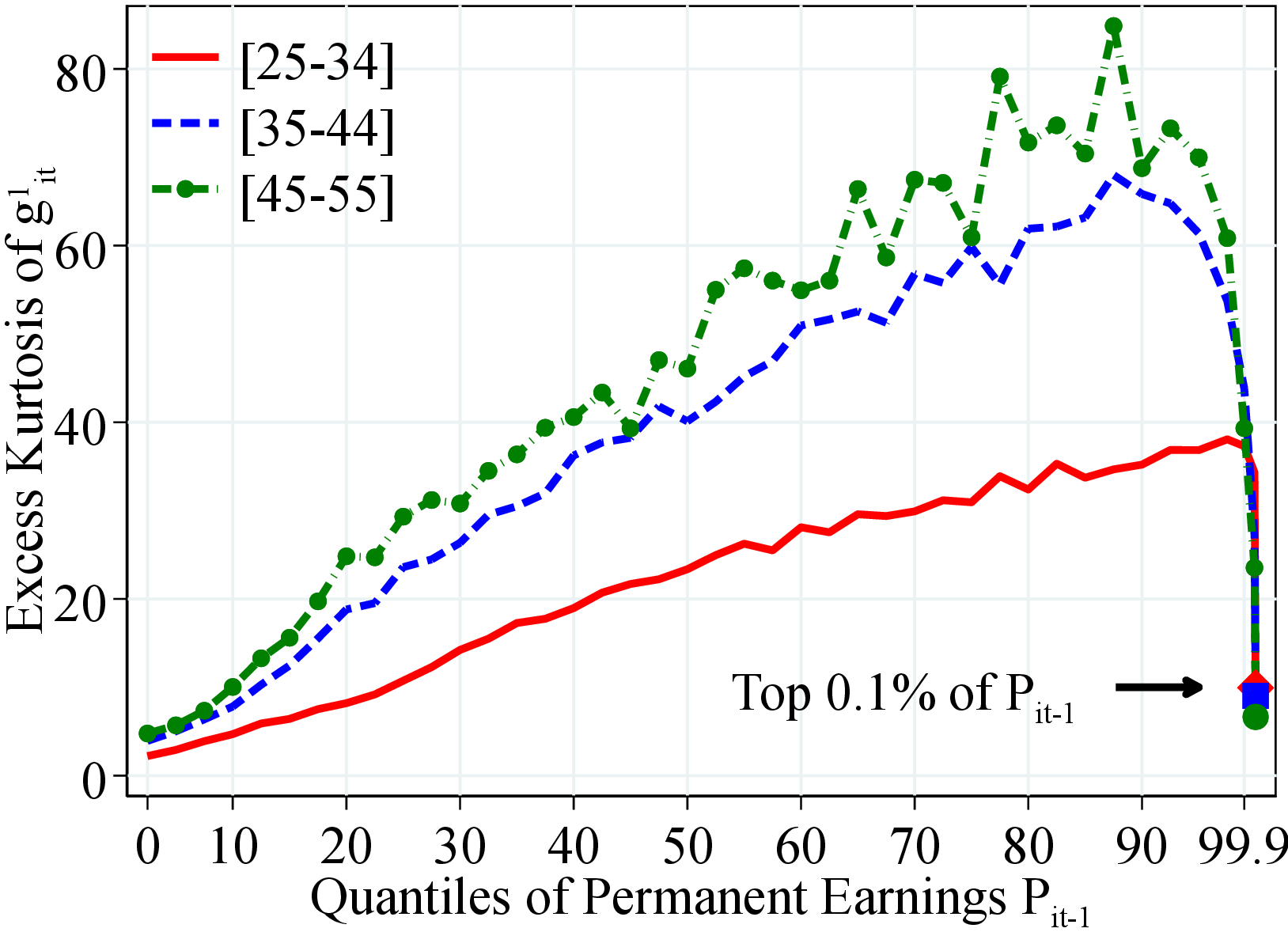

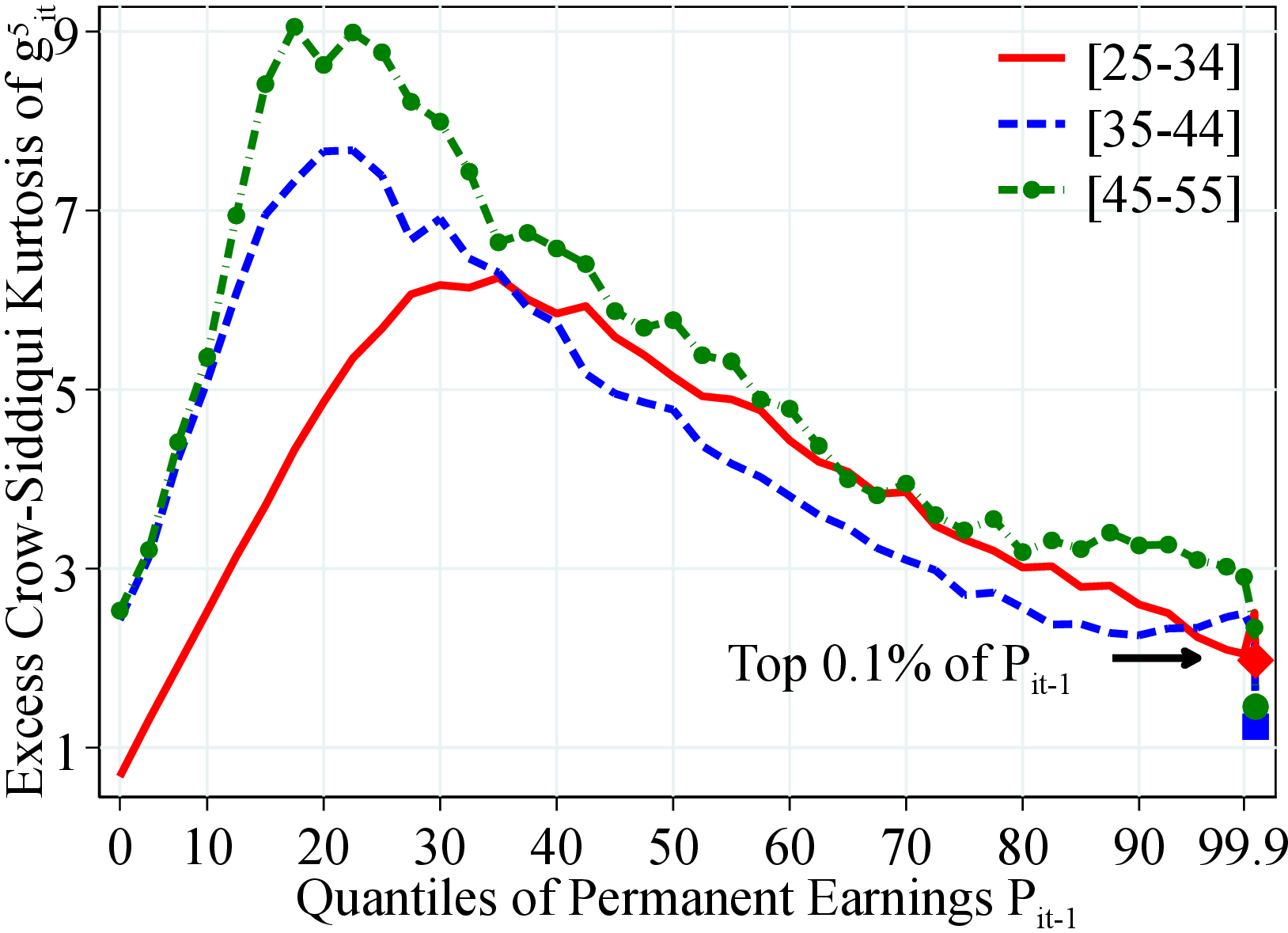

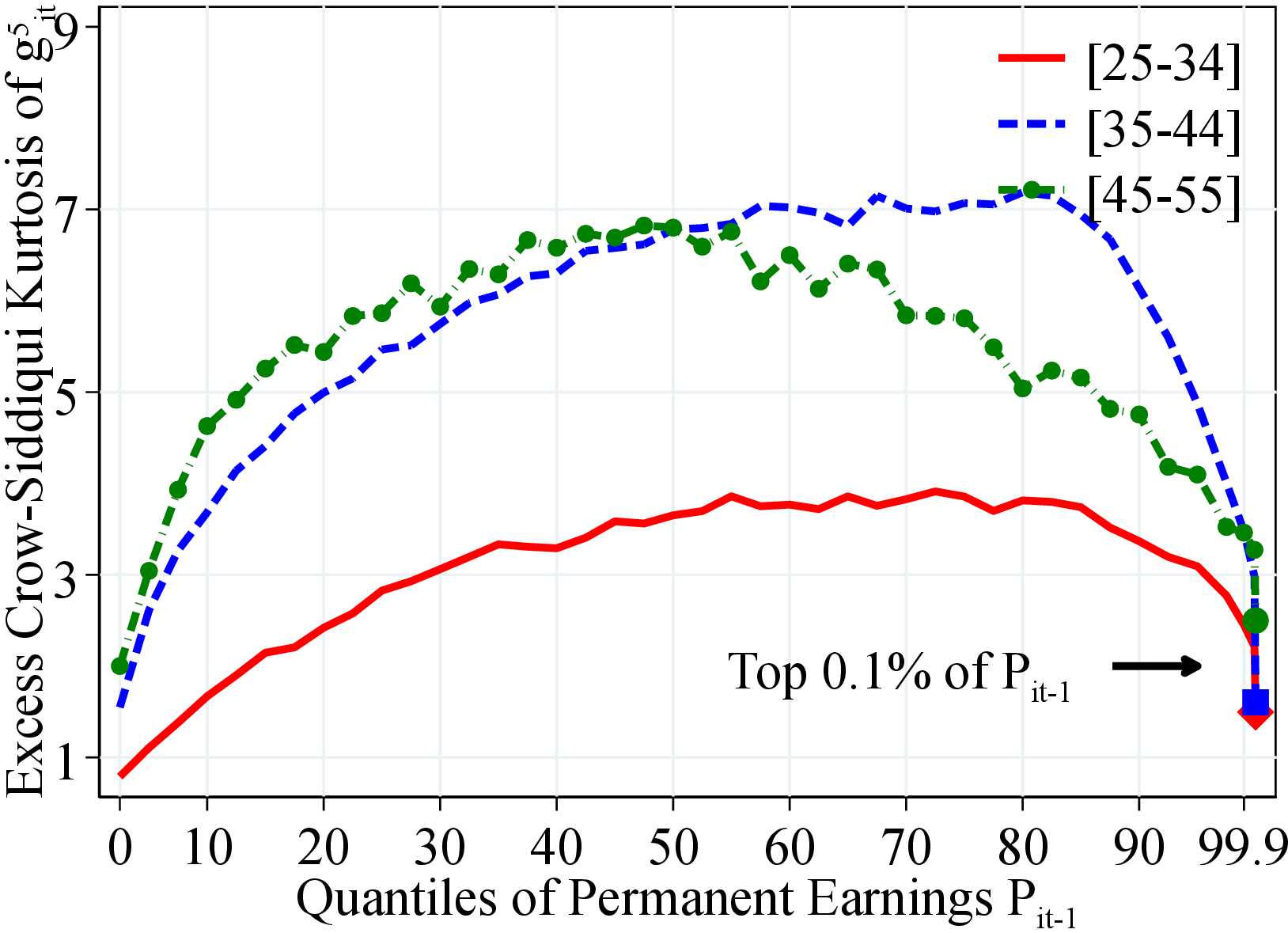

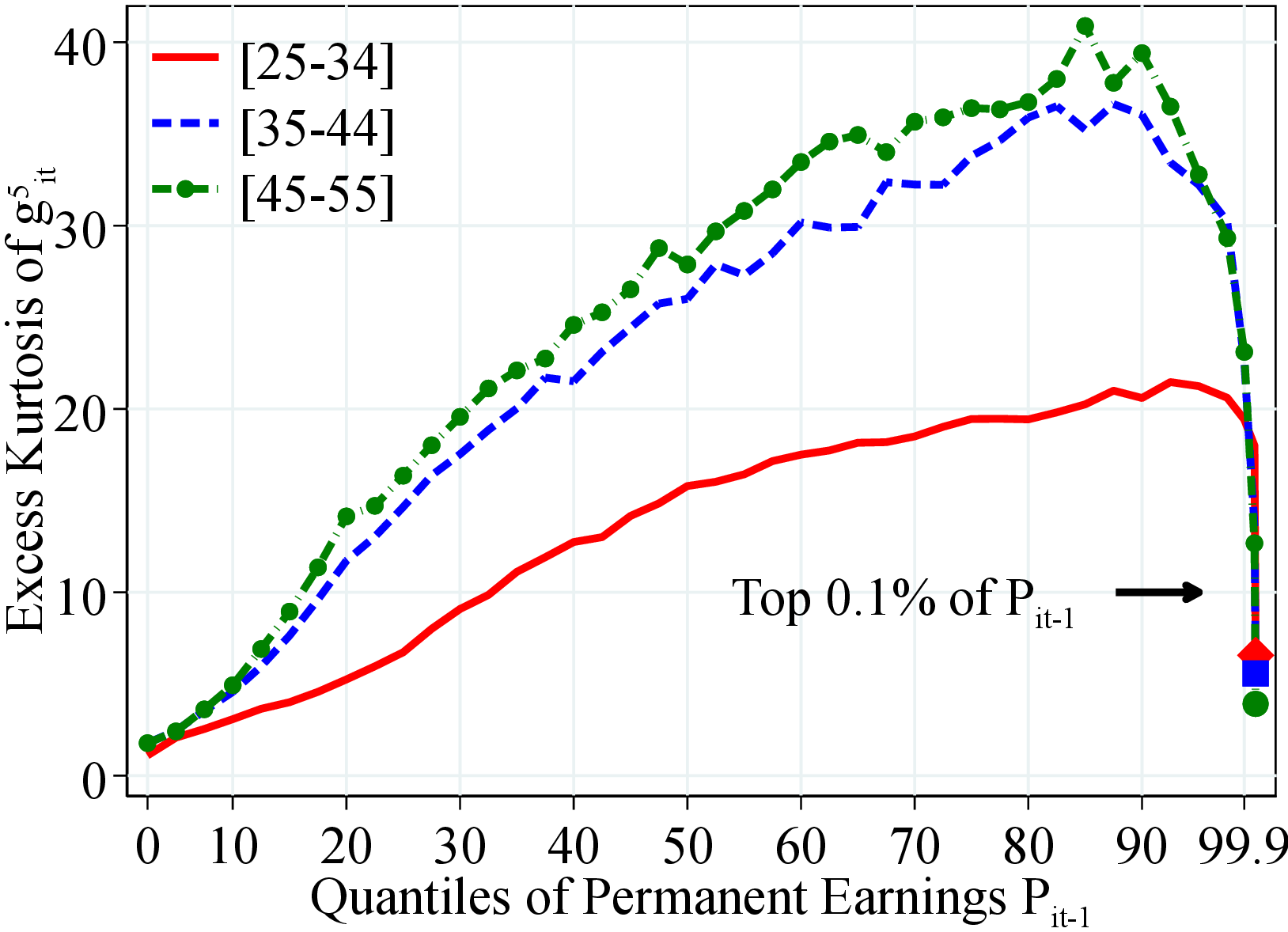

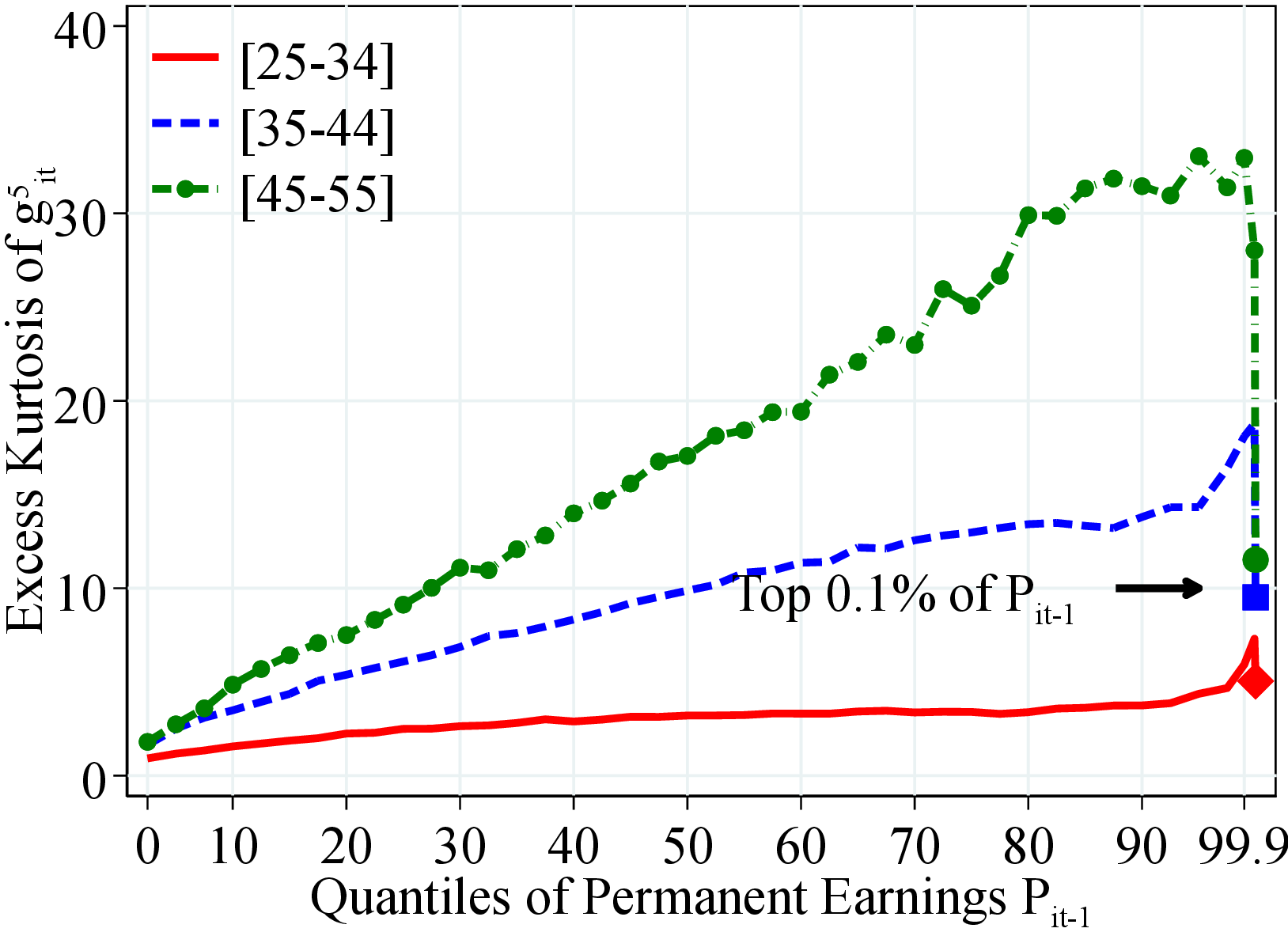

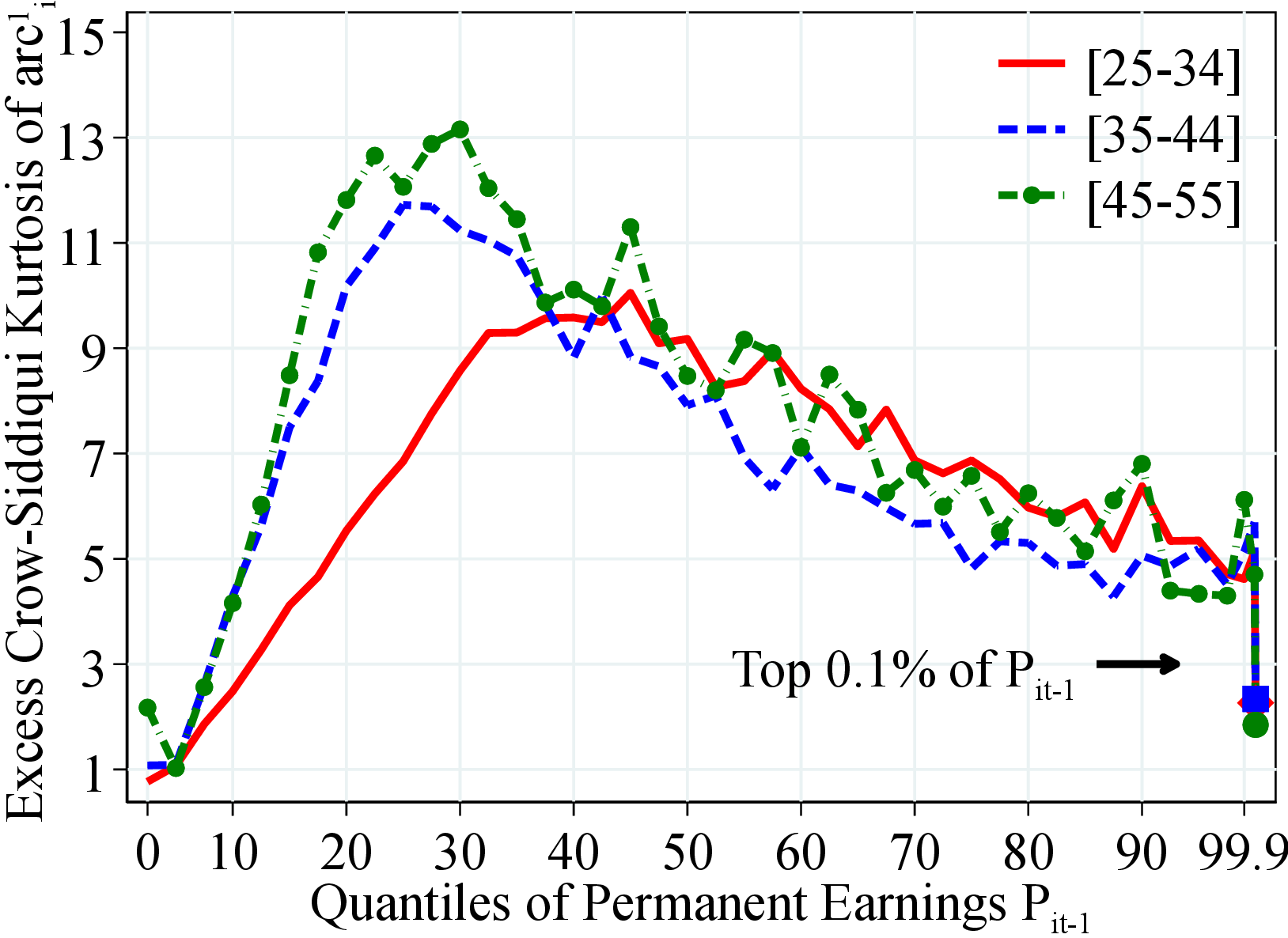

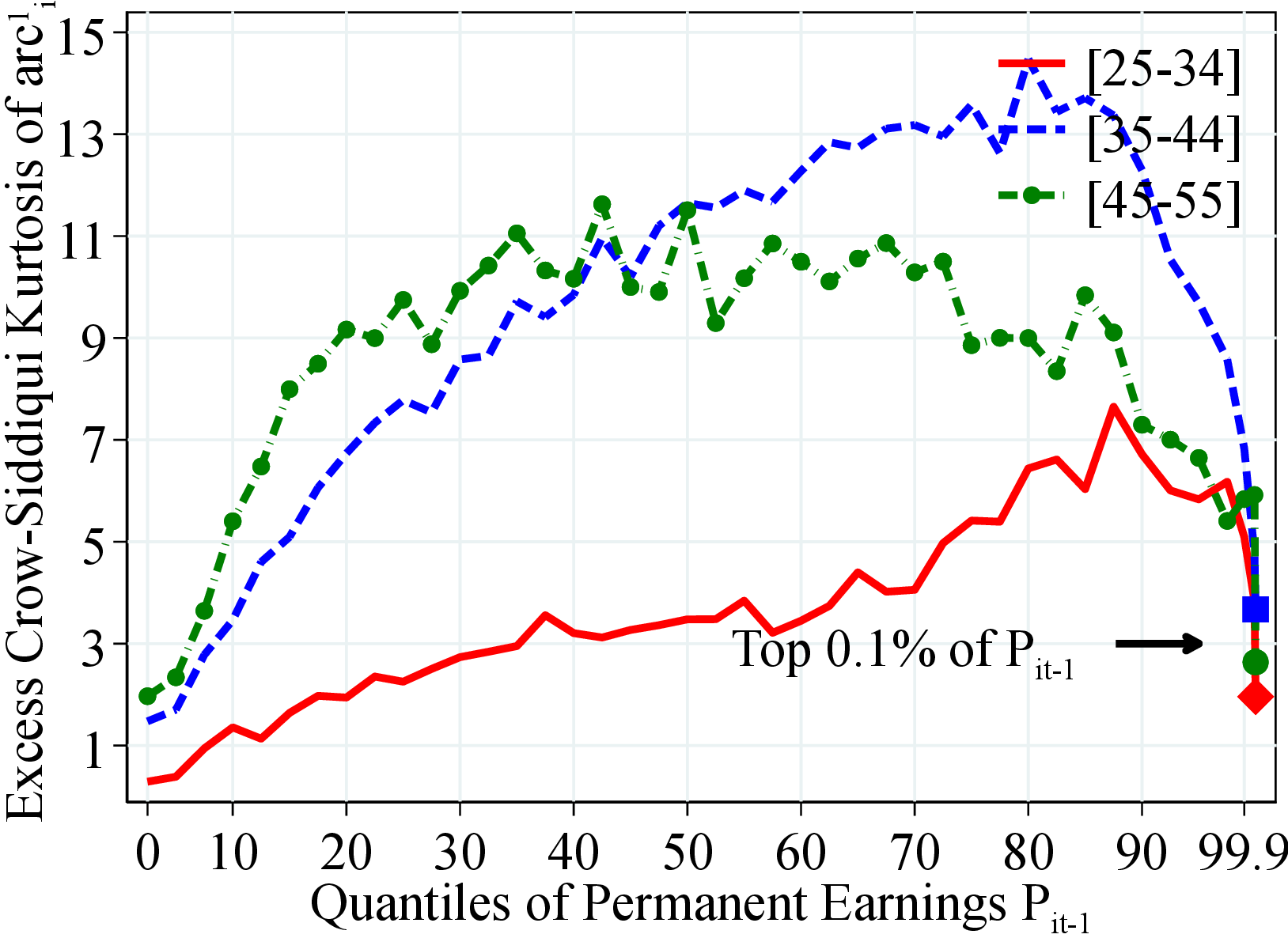

Heterogeneity in Kurtosis. Kurtosis exhibits a hump-shaped profile over the PE distribution and is usually higher for older workers with a higher peak for women (14 versus 11 for men) and the peak being at a higher PE for women (Figure 8). Similar to skewness, the fourth standardized moment depicts relatively different patterns compared to the Crow-Siddiqui measure (again because of the role played by extreme earnings changes). The fourth standardized moment increases almost monotonically as we move from low- to high-PE workers, peaking at around the 97th percentile (Figure C.11).

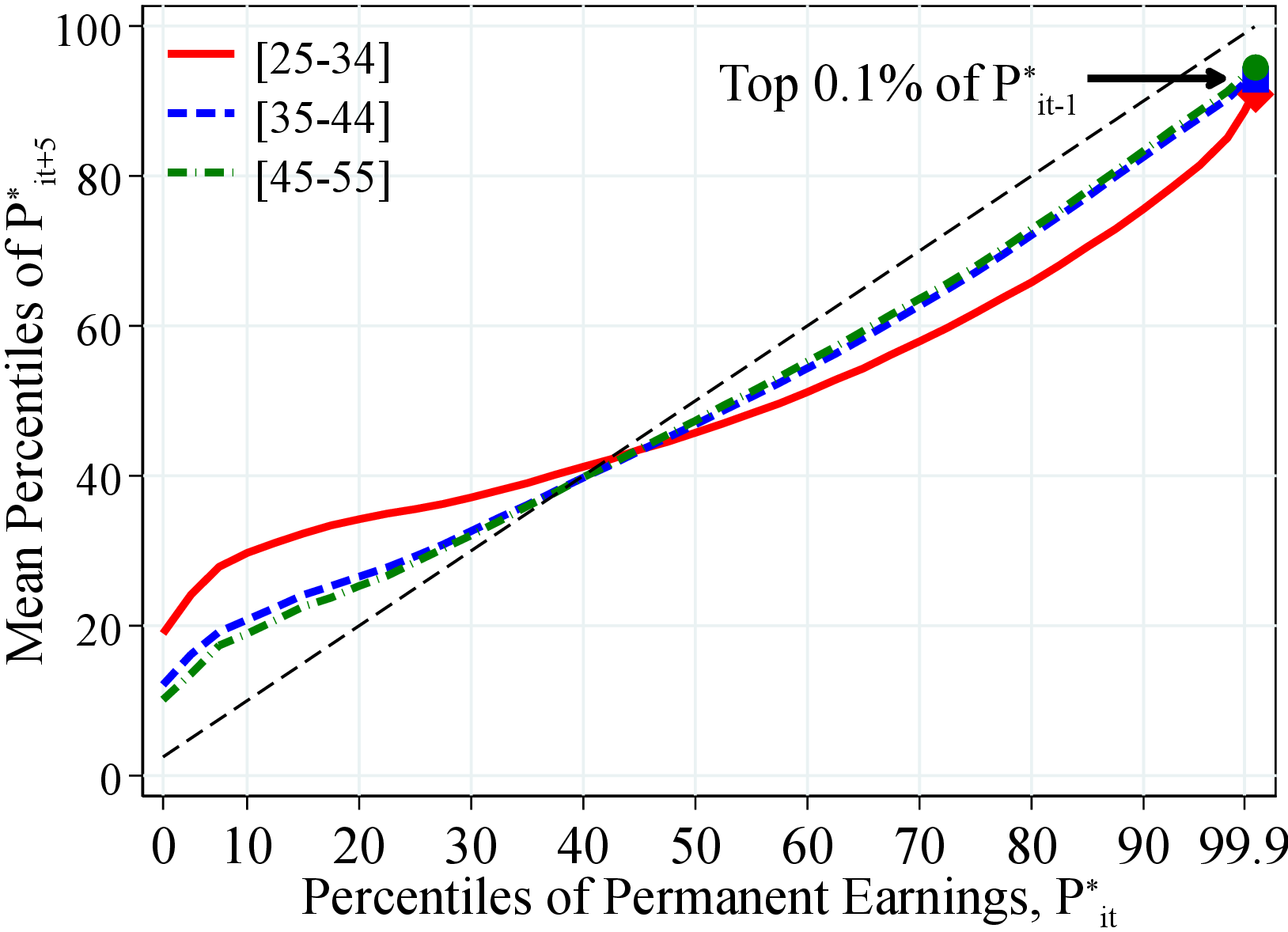

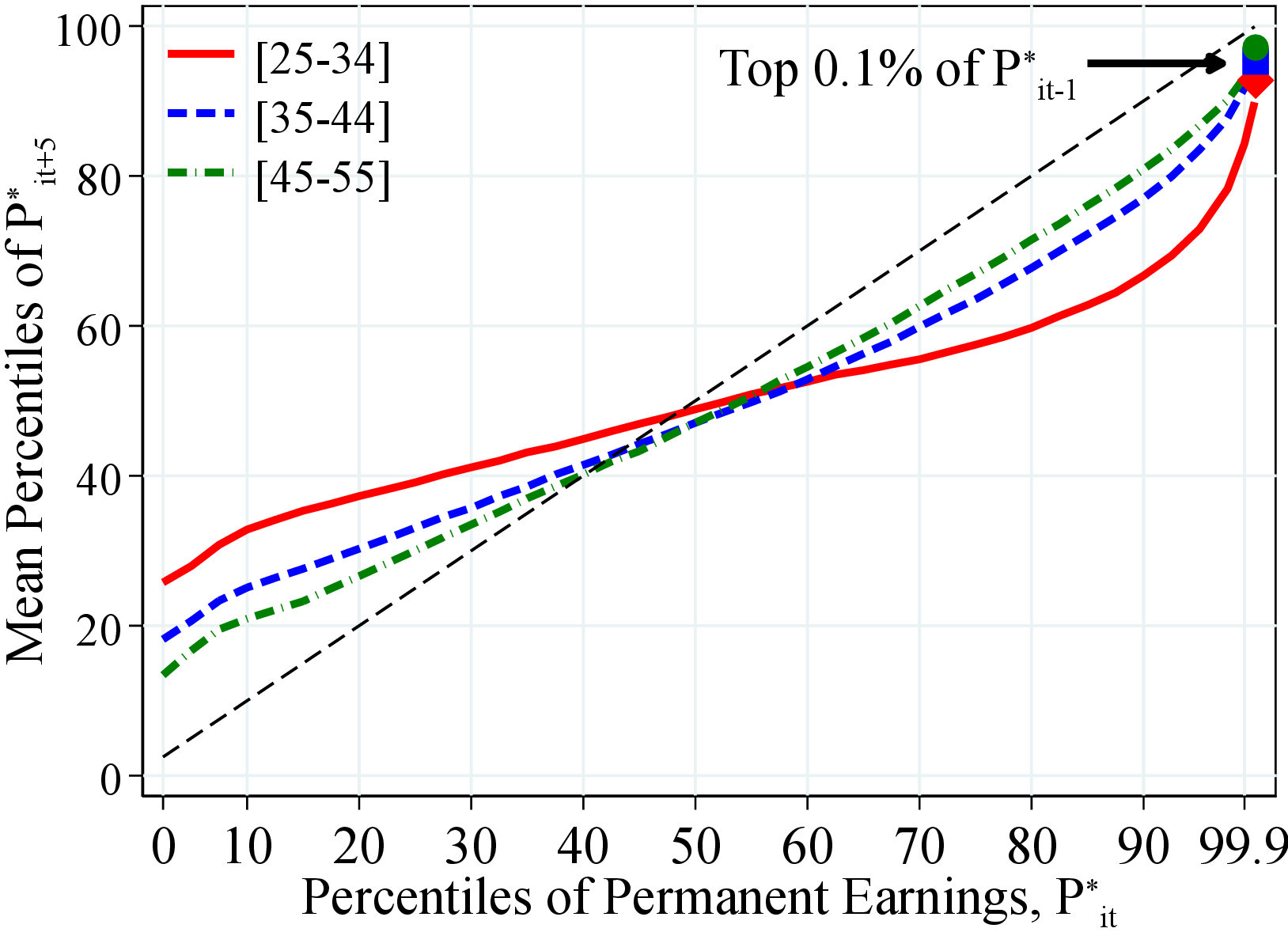

3.3 Earnings Mobility

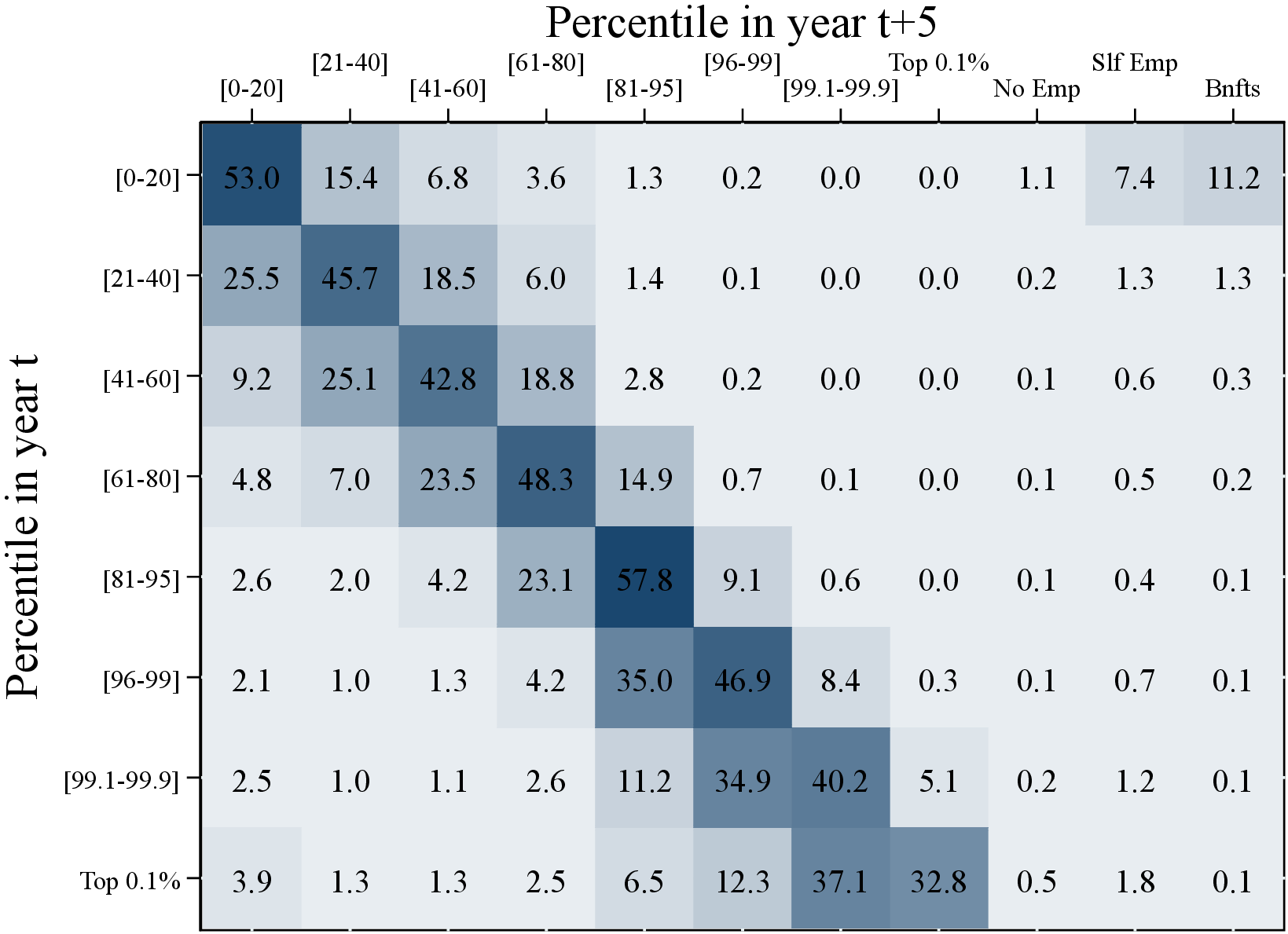

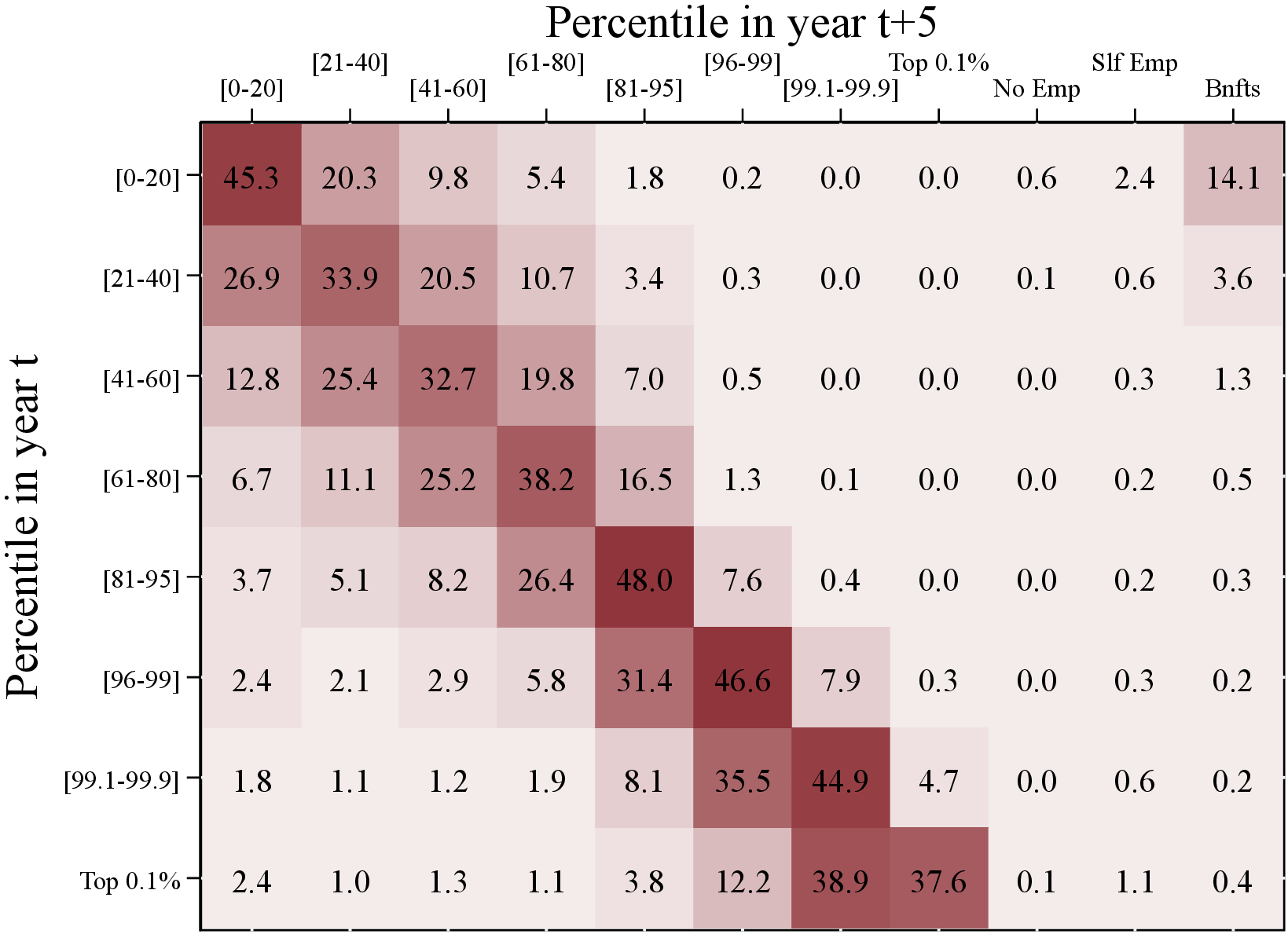

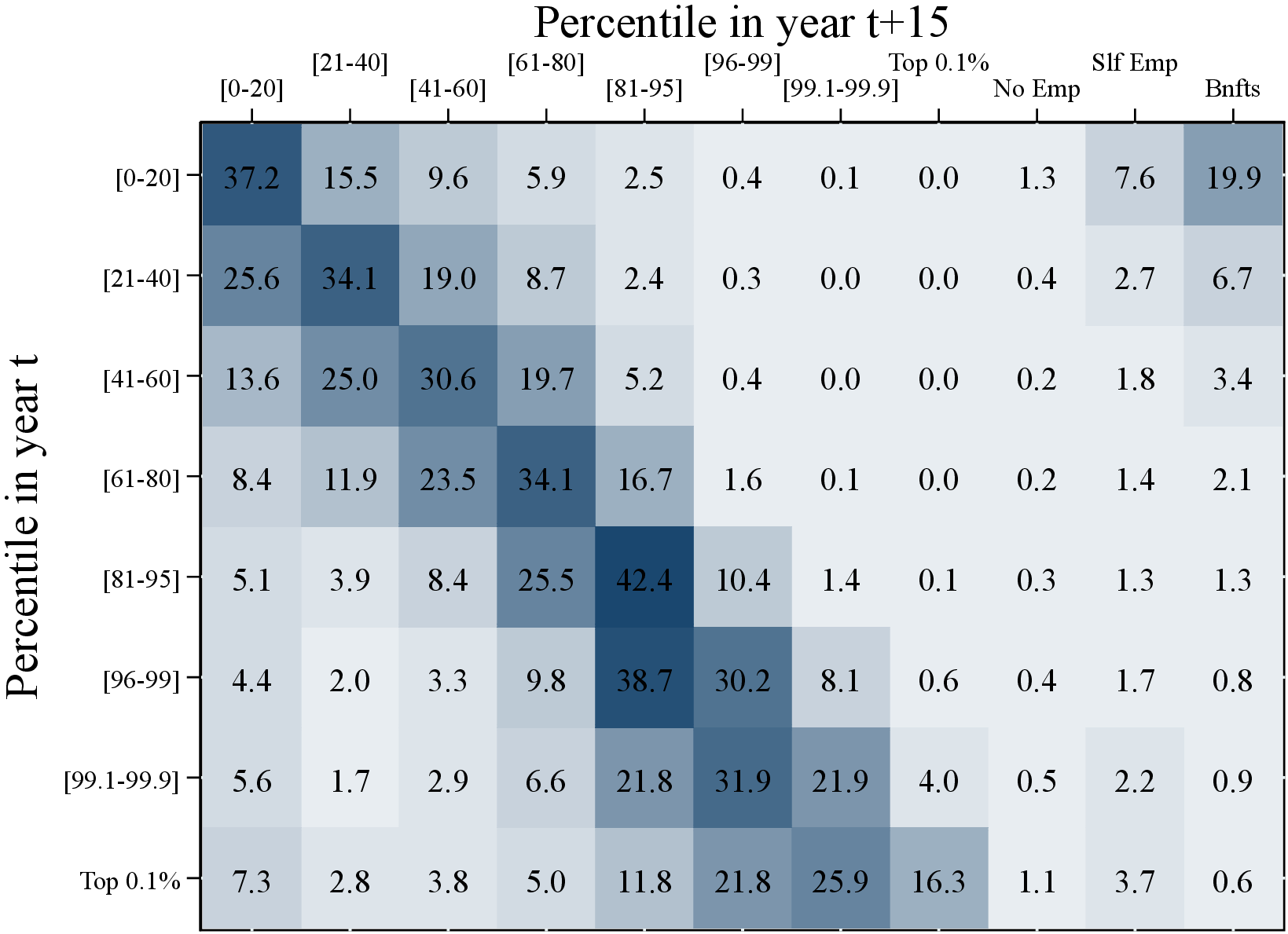

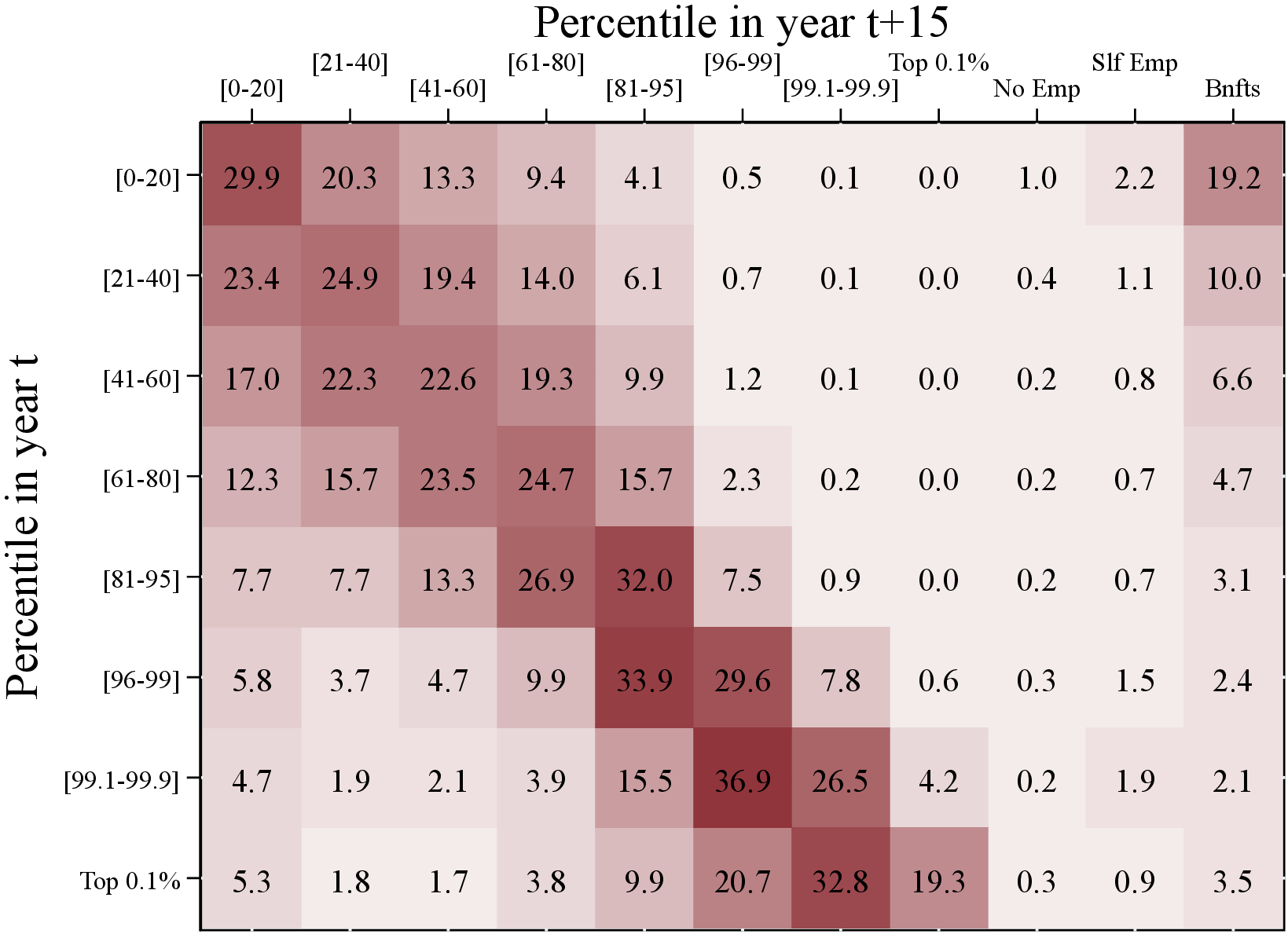

Having studied the properties of the distribution of earnings levels and growth, we now take a longitudinal perspective and turn to earnings persistence. Following our graphical approach, we plot the average rank-rank mobility that measures the expected position of an individual in the income distribution in year \(t+k\) conditional on the individual’s position in year \(t\). To isolate the persistent component of earnings, we use a slightly different version of permanent income, \(P_{it}^{*}\), defined as the average of labor earnings between periods \(t\) and \(t-2\) including earnings below the minimum earnings threshold.19 In this section, we present the average rank-rank mobility measure between \(t\) and \(t+10\). Further details and the results for 5-year average rank-rank mobility figures are presented in Appendix B, where we also report the 5-, 10-, and 15-year Markov transition matrices for \(P_{it}^{*}\) for a more complete picture of workers’ earnings dynamics.

Figure 9 shows the average rank-rank mobility for two age groups, 25-34 and 35-44, separately. Several remarks are in order. First, earnings mobility declines significantly after the first decade of working life. This finding is consistent with the previous results in the literature (see Karahan and Ozkan (2013); Guvenen et al. (2021)) in that income becomes more persistent as individuals advance in their career until around the ages of 45 to 55. Second, relative to men, earnings mobility is higher for women, and even more so for younger women in the upper half of the distribution (Panel B of Figure 9). Third, income mobility is the highest around the 10th and 90th percentiles of the income distribution, especially for younger workers. Furthermore, upward mobility in the bottom half of the income distribution is higher relative to the downward mobility in the upper half of the distribution. In fact, higher upward mobility in the bottom half leads the rank-rank measure to cross the 45-degree line below the 50th percentile.

4 Intergenerational Transmission of Income Dynamics

The results in the previous section show that there is striking heterogeneity in earnings dynamics across workers by their permanent income and age (see also, e.g., Alvarez, Browning and Ejrnaes (2010)). We now investigate whether there is further heterogeneity in idiosyncratic income dynamics that stems from differences in parental backgrounds. The relationship between parents’ and children’s incomes has been an important question in economics and public policy (see Piketty (2000), Corak (2013), and Jantti and Jenkins (2015) for recent reviews of the literature). Following the seminal work of Solon (1992), several papers have documented intergenerational persistence in income in different countries, such as the U.S., the U.K. (Long and Ferrie (2013)), and Norway (e.g., Bratberg, Anti Nilsen and Vaage (2005), Pekkarinen, Salvanes and Sarvimaki (2017), and Markussen and Roed (2019)).

(a) Men

(a) Men  (b) Women

(b) Women

Figure: Figure 8 – Kurtosis of Earnings Growth by Permanent Earnings and Age

Notes: Figure 8 shows the excess Crow-Siddiqui kurtosis of the log growth rate of residual earnings for men and women with quantiles of the PE, \(P_{it-1}\). Excess Crow-Siddiqui kurtosis is defined as \(\mathcal{C_{K}}=\left (\text{P97.5-P2.5}\right)/\left (\text{P75-P25}\right)-2.91\) where \(2.91\) is the value of the Crow-Siddiqui measure for a normal distribution. In each plot, the solid markers represent the corresponding measure of kurtosis for those workers at the top 0.1% of the earnings distribution for different age groups.

Unlike most of the literature, which has focused on the relationship between parents’ and children’s income levels, we study the intergenerational transmission of income dynamics.20 In particular, we investigate whether children of fathers with steeper life-cycle income growth, more volatile incomes, or higher downside risk also have income streams with similar properties. Such correlations can arise, for example, if fathers and children share similar risk attitudes or work in similar jobs and sectors. We also investigate how the income dynamics of workers vary with parents’ financial resources. Our results from this study shed light, for instance, on the roles of (i) the dynastic precautionary savings motive of parents in wealth accumulation (as in Boar (2021)), (ii) the importance of family resources for children’s human capital accumulation (as in Holter (2015)), and (iii) the importance of parental insurance for the career choices of young adults (i.e., whether children of families with more resources can pursue high-risk, high-return careers, as in Fawcett (2020))).

(a) Men

(a) Men  (b) Women

(b) Women

Figure: Figure 9 – Income Mobility: Rank-Rank Measures by Age

Notes: Figure 9 shows the average rank of individuals in period \(t+10\) according to their permanent earnings, \(P_{it+10}^{*}\), within different percentiles of permanent earnings in period \(t\). To construct this figure, we calculate the average rank in \(t+10\) for each year in our sample between 1993 and 2007 (the last years in which a 10-year change can be calculated) for each age group. We then average across all years in our sample. The 45-degree (dashed black) line represents the perfect immobility case (on average, individuals remain in the same percentile after \(t+10\) years).

We start our analysis in Section 4.1 with the intergenerational lifetime income mobility for both completeness and consistency with the earlier work. Next, in Section 4.2, we investigate how workers’ income risk varies by their fathers’ financial resources. For this purpose, we show the variation in moments of children’s idiosyncratic income changes by their fathers’ lifetime income and wealth. Finally, in Section 4.3, we study the intergenerational transmission of income dynamics by documenting the relation between (the first three) moments of parents’ and children’s income changes over the life cycle.

Intergenerational Data. Our administrative registers include family identifiers that allow us to link children to their parents. The information on family links is collected from the Norwegian Population Register, which was established in the early 1960s using information from the 1960 census. All individuals born after 1950 can be linked to their parents. For earlier cohorts, we were able to identify most parents. We focus on father-children pairs to prevent our results from being affected by the increase in female labor force participation over our sample period (Figure 1c).

The analysis in this section is based on the after-transfer income measure, which dates back to 1967 and ends in 2017. The very long panel dimension of the data—specifically, 51 years long—is crucial for our purposes for at least two reasons. First, it allows us to precisely measure each individual’s income risk over the life cycle. For example, we have 48 cohorts born between 1928 and 1975, for which we have at least 20 observations of annual incomes to compute individual-specific income risk measures (e.g., percentile-based dispersion and skewness measures of income growth). Second, it is crucial to use a dataset with a long panel for our purposes because a short-panel dataset can end up having only a few observations for one of the individuals in a father-child pair.

Wealth Data. Our wealth measure includes financial and non-financial assets derived from Norwegian administrative records and available from 1993 on. This high-quality dataset is mostly third-party reported to the tax authorities, and very little is self-reported. Employers, banks, brokers, insurance companies, and other financial institutions are obliged to send information on the value of the asset owned and on the income earned from these assets for all taxpayers in Norway. In our analysis, we use household net wealth that accounts for all financial wealth (e.g., stocks and bonds) and real wealth (e.g., imputed value of houses) net of short- and long-term liabilities (e.g., credit card debt and mortgages).21

Sample selection. We consider a sample of workers between 23 (typical college graduation age) and 60 years old (instead of the 25-55 age range used in previous sections) to maximize the number of observations for each individual. We include all individuals who have at least 20 years of non-missing income observations, half of which are above the minimum threshold, \(Y_{t}^{min}\). This sample allows us to compute a permanent income measure that is less sensitive to transitory changes in fathers’ and children’s incomes. Furthermore, it also ensures that we can reliably measure income risk at the individual level. Finally, we require fathers to have at least two years of wealth observations to be included in the sample. The final sample includes 965,743 father-child pairs, of which 471,229 are father-daughter pairs.

4.1 Intergenerational Income Mobility

We start by documenting the relation between fathers’ and children’s lifetime income levels. Since our sample includes individuals who have at least 20 years of income observations, our estimates are robust to the well-known attenuation bias in measures of intergenerational elasticity of income that arises when few observations are used to calculate permanent income (see Solon (1992); Black and Devereux (2011)). Notice that our sample consists of cohorts who were born between 1928 and 1975. Furthermore, we observe some cohorts for a shorter period of time than others, either when they are young or when they are old. Thus, to make the lifetime incomes comparable across cohorts, we normalize incomes in each year and age by their corresponding year-age cell average. Then, we define the residual lifetime income of an individual \(i\) born in cohort \(c\) (birth year) as

\[ LI_{i,c}=\frac{\left [\sum _{t=\max \left \{25+c,1967\right \}}^{\min \left \{60+c,2017\right \}}\frac{I_{it}}{d_{t,h(i,t)}}\right]}{\min \left \{60+c,2017\right \} -\max \left \{25+c,1967\right \} +1}, \]

where \(I_{it}\), \(h(i,t)\), and \(d_{t,h(i,t)}\) denote the real after-transfer income, age of \(i\) in year \(t\), and the average income at age \(h(i,t)\) and in \(t\), respectively.

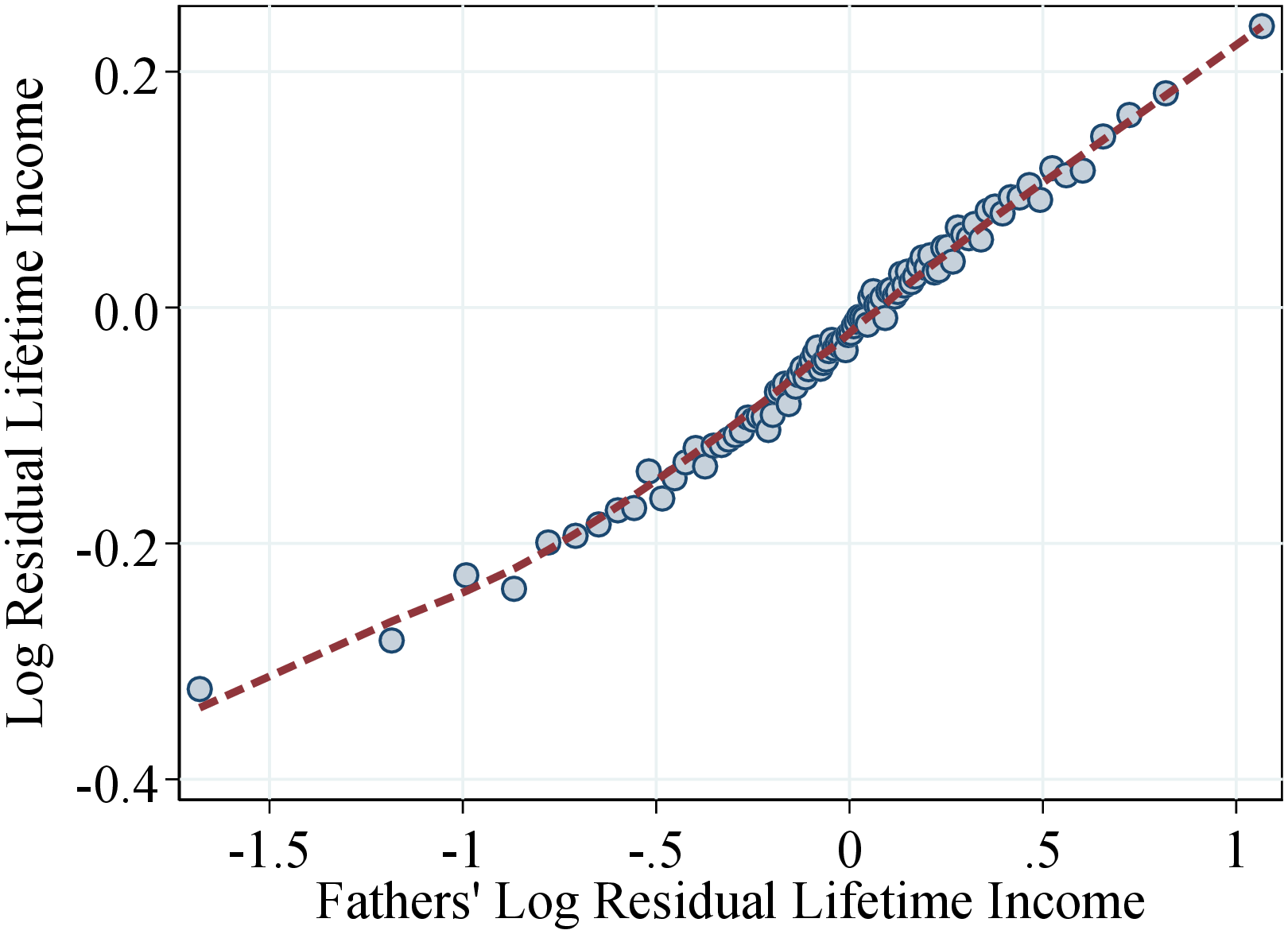

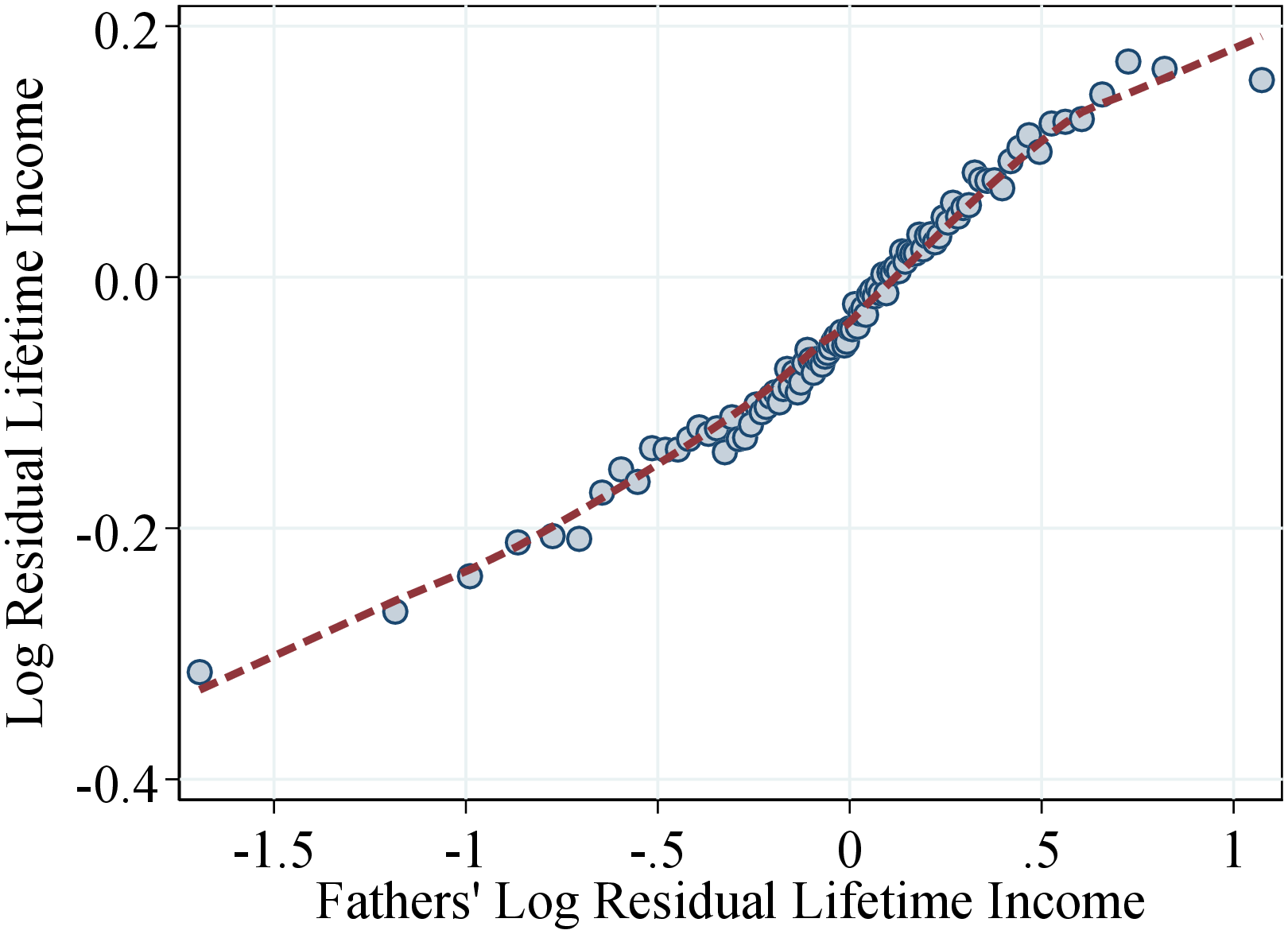

Figure 10 shows a binned scatter plot of the log lifetime incomes of father-son pairs (left panel) and father-daughter pairs (right panel). In particular, on the \(x\)-axis we rank fathers into 100 bins with respect to their (log) lifetime incomes and plot the average log lifetime incomes of children in each bin on the \(y\)-axis. Our results confirm the findings of the earlier literature of a strong intergenerational persistence in income. We find that the relation between fathers’ and children’s lifetime income is fairly linear, with an elasticity of intergenerational income of 0.24. For example, an increase in fathers’ log lifetime income from -0.5 to 0.5—where the bulk of the sample is—is associated with an average increase in sons’ earnings of 25 log points (Figure 10a). The results are quite similar for the father-daughter pairs, with a slightly weaker elasticity of 0.23 (Figure 10b).22

(a)

(a)  (b)

(b)

Figure: Figure 10 – Fathers and Children Income Correlation

Notes: Figure 10 shows a binned scatter plot of fathers’ and children’s residual lifetime income using 100 bins. All nominal values are deflated to their 2018 real values using the Consumer Price Index in Norway. The plot is based on a sample of fathers and children with 20 years of data or more between 1967 and 2017.

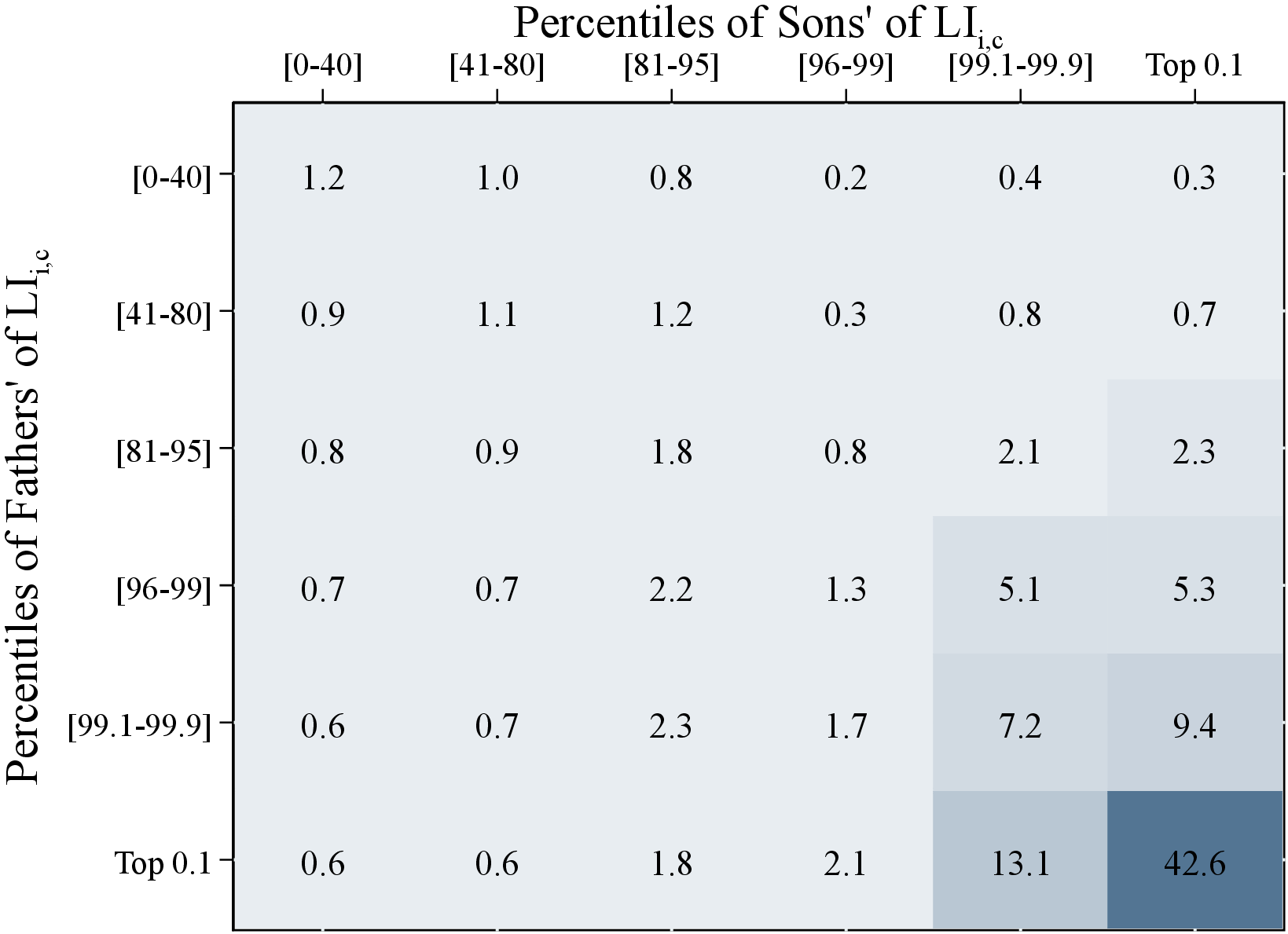

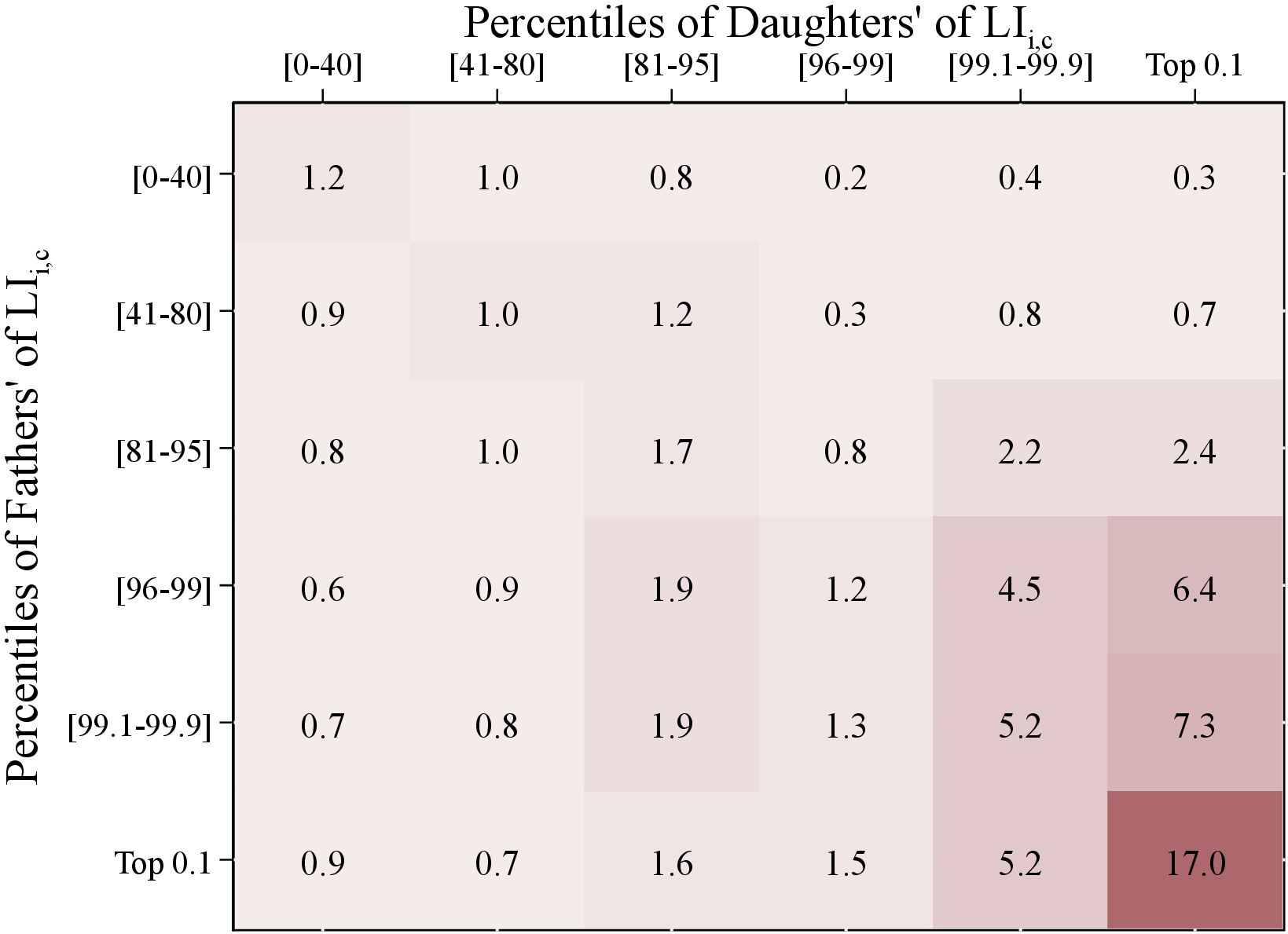

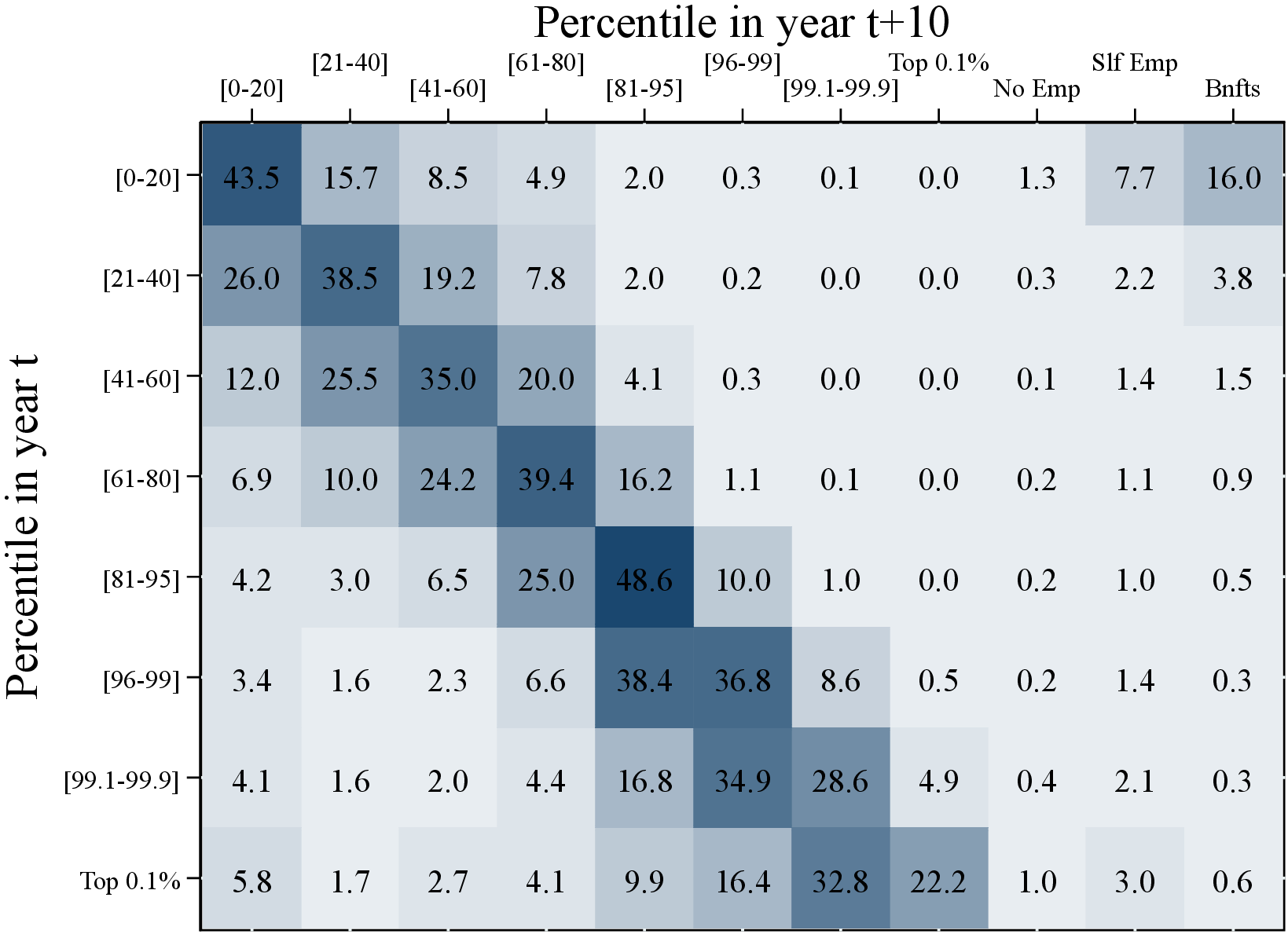

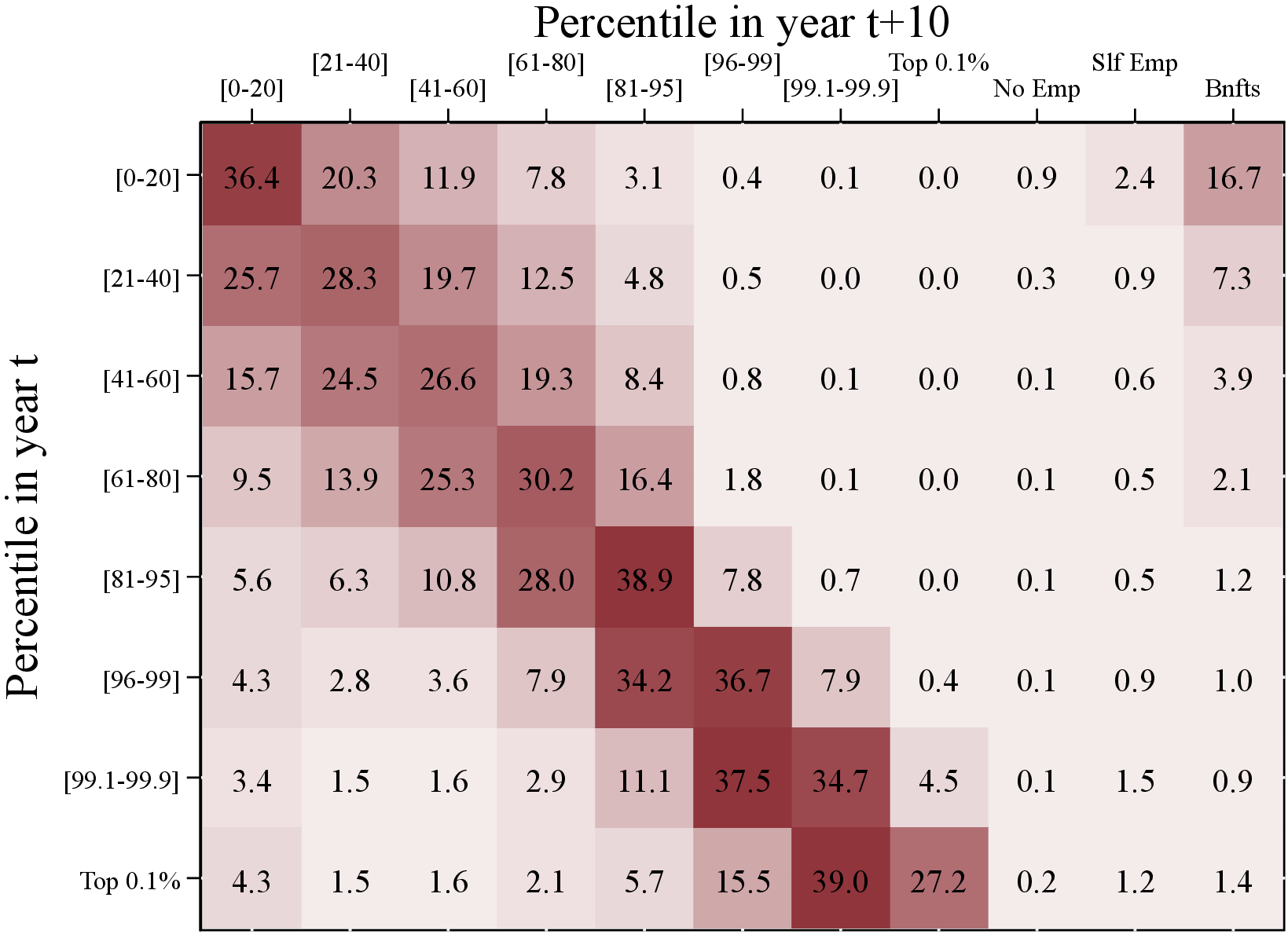

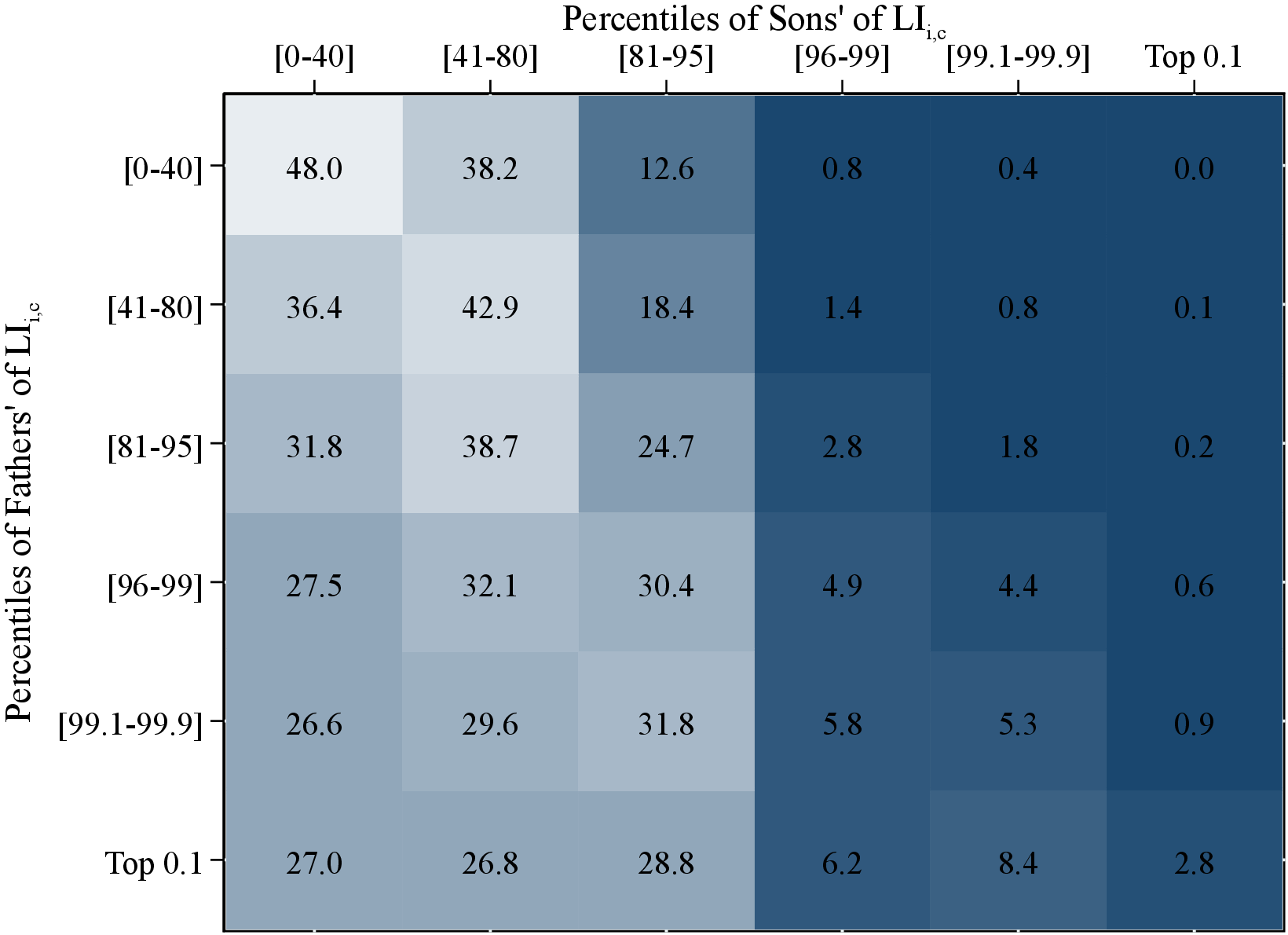

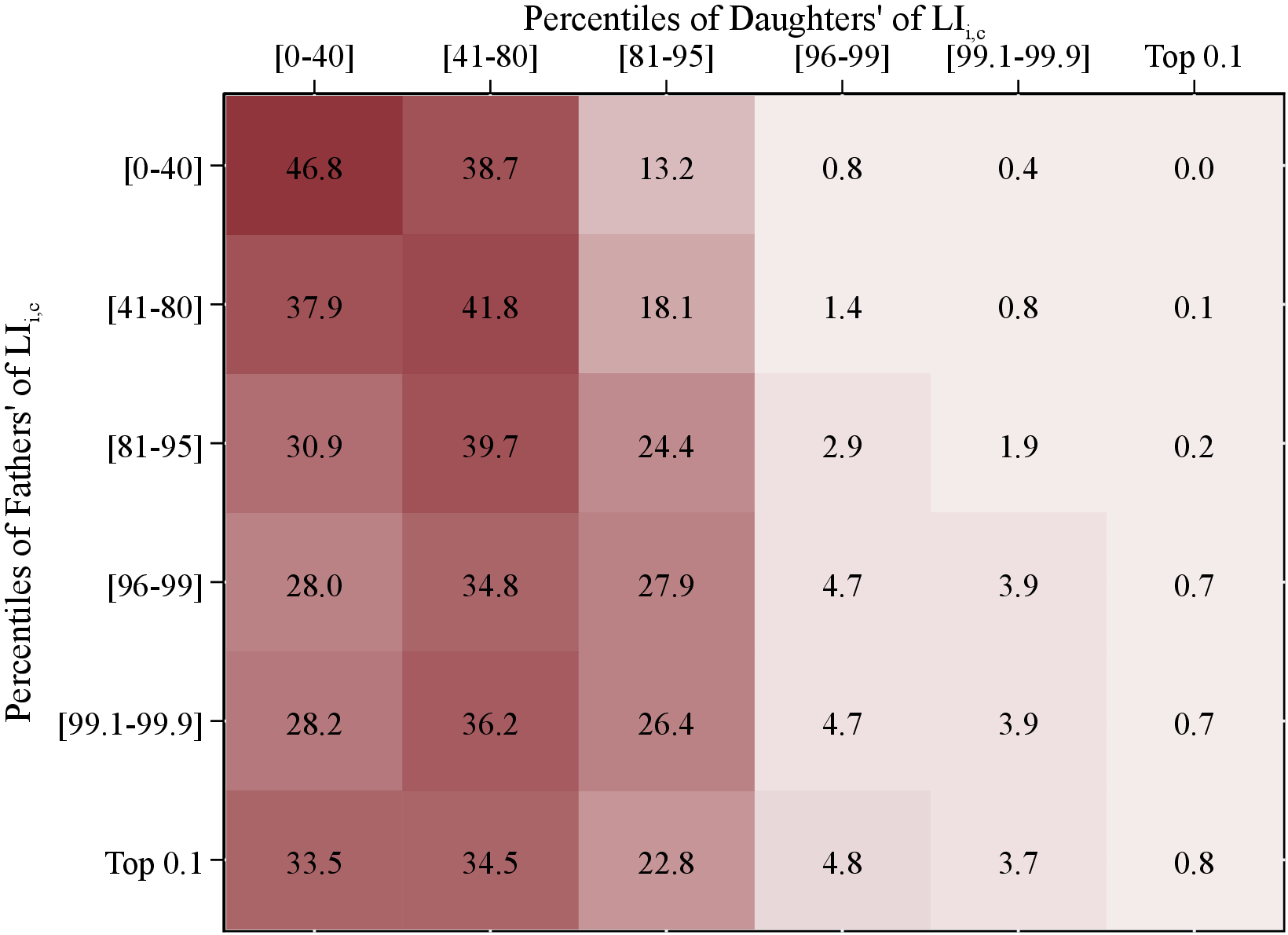

To obtain a more granular view of the relation between fathers’ and children’s lifetime income, we construct intergenerational transition matrices (see Figure 11; for matrices with more income groups, see Appendix C.1). We rank fathers, sons, and daughters separately with respect to their lifetime incomes within age groups. These matrices then show the probability that a father in the \(ith\) income group (in the rows of the matrix) has a child in the \(jth\) income group (in the columns of the matrix) normalized by the size of the child’s quantile (i.e., population probability). For example, we find that 48% of the bottom 40% of fathers have a child in the bottom 40%. Therefore, the top left number in Figure 11 is \(1.2=\frac{48\%}{40\%}\)—the likelihood of a father in the bottom 40% having a son also in the bottom 40% relative to the population average.

The larger the numbers on the diagonal of the matrix are, the stronger the intergenerational persistence is. A diagonal of ones means that incomes of children and fathers are entirely uncorrelated as children have the same probability of being in their fathers’ income quantile as the population average. In contrast, for cells away from the diagonal the lower the numbers are, the lower the intergenerational income mobility is. For example, the likelihood of a father in the bottom 40% having a child in the top 0.1% quantile relative to the population average is only 30% (the top right number in Figure 11).

We find that all the values on the diagonal (and in most neighboring cells) are larger than 1, pointing to some degree of intergenerational persistence for all income groups. More interestingly, intergenerational persistence is highest in the top income groups: Sons of fathers in the 0.1% of the income distribution are 42.6 times and 13.1 times as likely to be in the 0.1% and next 0.9% relative to the population average, respectively. The intergenerational persistence for daughters at the top of the income distribution is lower compared to the sons.

How much upward and downward income mobility is there? The likelihood that the children (both sons and daughters) of the bottom 40% of fathers will reach the top 5% is only around 24% of the population average (i.e., 1.2% probability versus 5% probability in the population). Similarly, the probability that the sons (daughters) of the top 0.1% of fathers drop to the bottom 40% income group is 60% (90%) of the population average. These results show that even in Norway (which is known for its redistributive policies as well as free public schools and universities), upward and downward income mobility is still fairly low.

(a) Sons

(a) Sons  (b) Daughters

(b) Daughters

Figure: Figure 11 – Intergenerational Lifetime Income Mobility

Notes: Figure 11 uses fathers’ and children’s income data for a pooled sample of individuals between 1967 and 2017. The matrix shows the transition probabilities between quantiles of fathers’ lifetime incomes (rows) and children’s lifetime income groups (columns) normalized by the measure of the children’s quantile, therefore, indicating the likelihood relative to the population average. To construct this figure, we rank fathers, sons, and daughters separately among their peers with respect to their lifetime incomes, \(LI_{i,c}\).

4.2 Fathers’ Resources and Children’s Income Dynamics

Arguably, parents’ financial resources have a significant effect on children’s income dynamics. For example, high-income or high-wealth parents tend to spend more on their children’s education, which allows them to accumulate more human capital and enjoy high incomes from more stable jobs. Alternatively, children from rich families might be able to pursue high-risk, high-return careers or could afford to live off their inheritances without maintaining stable employment. Furthermore, parents may accumulate wealth to insure their children against income risk (e.g., Boar (2021)).

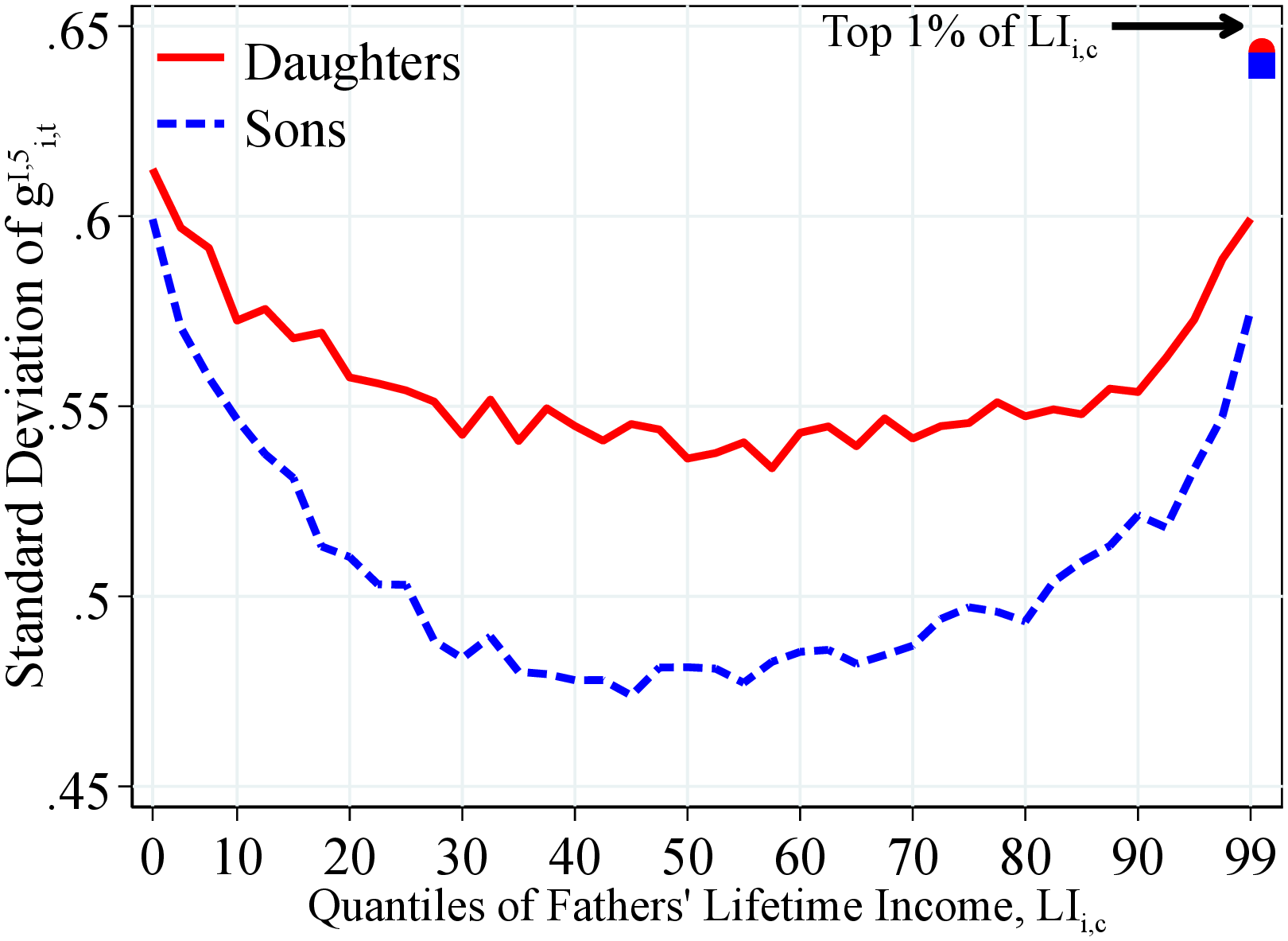

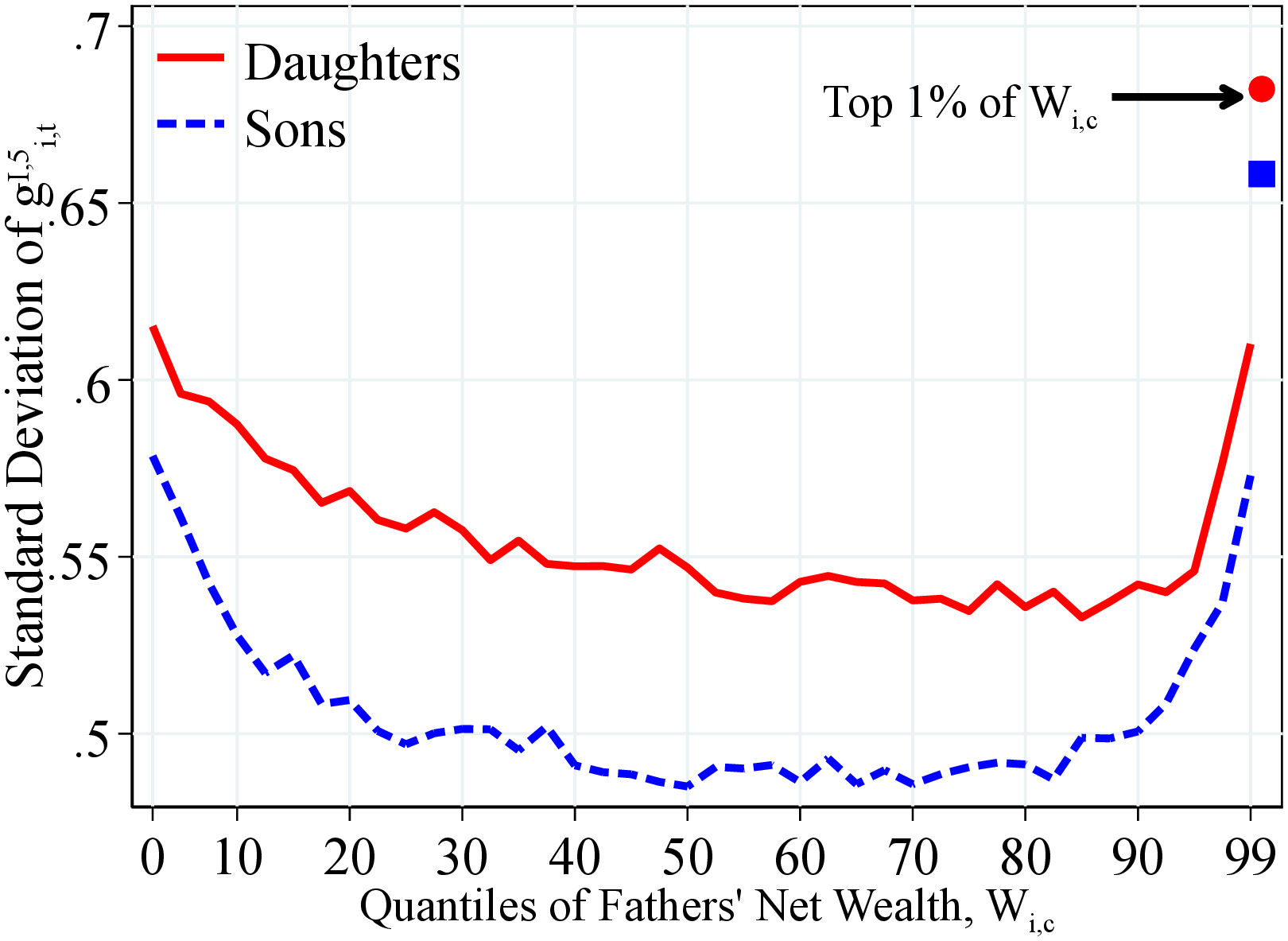

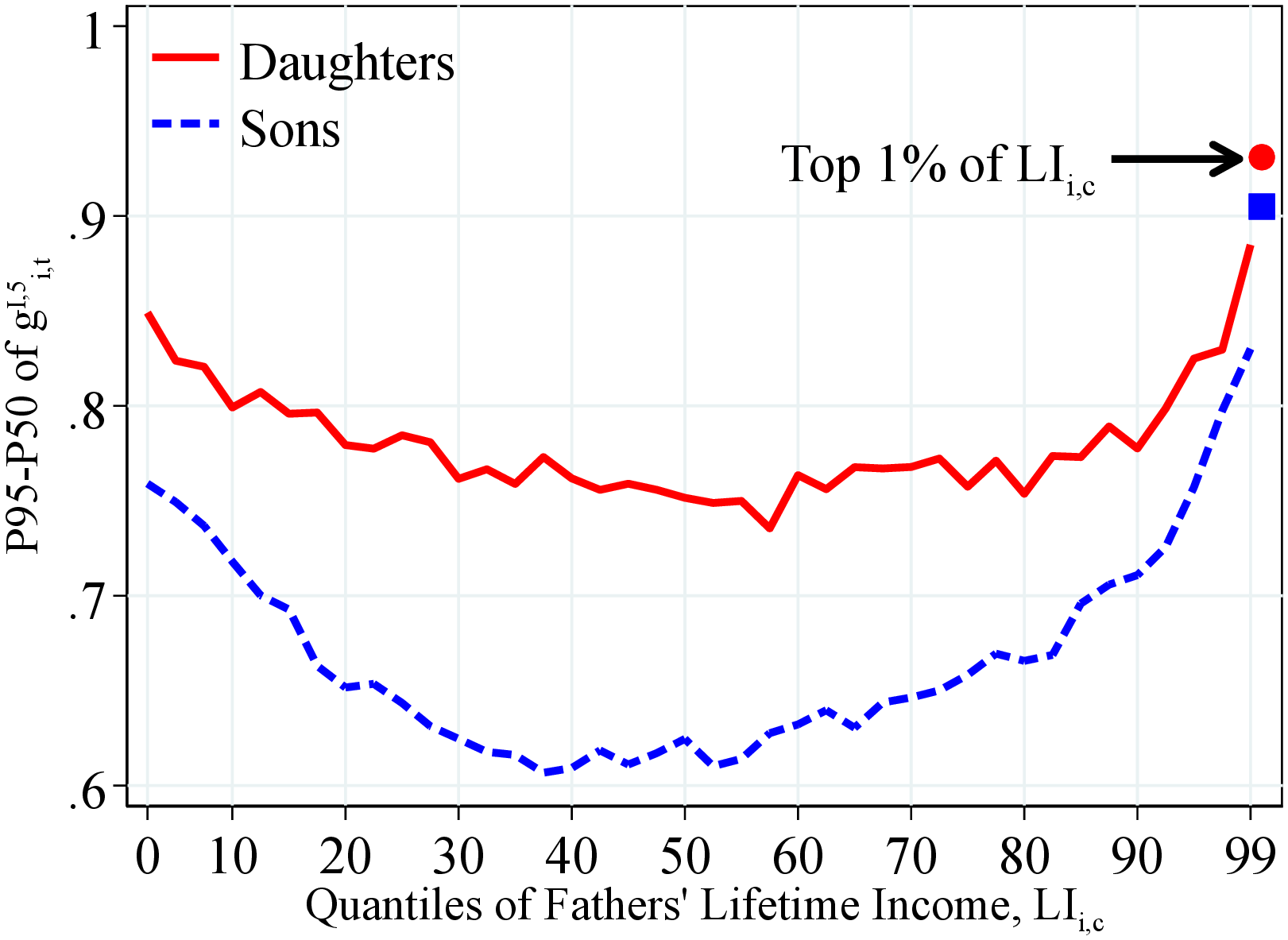

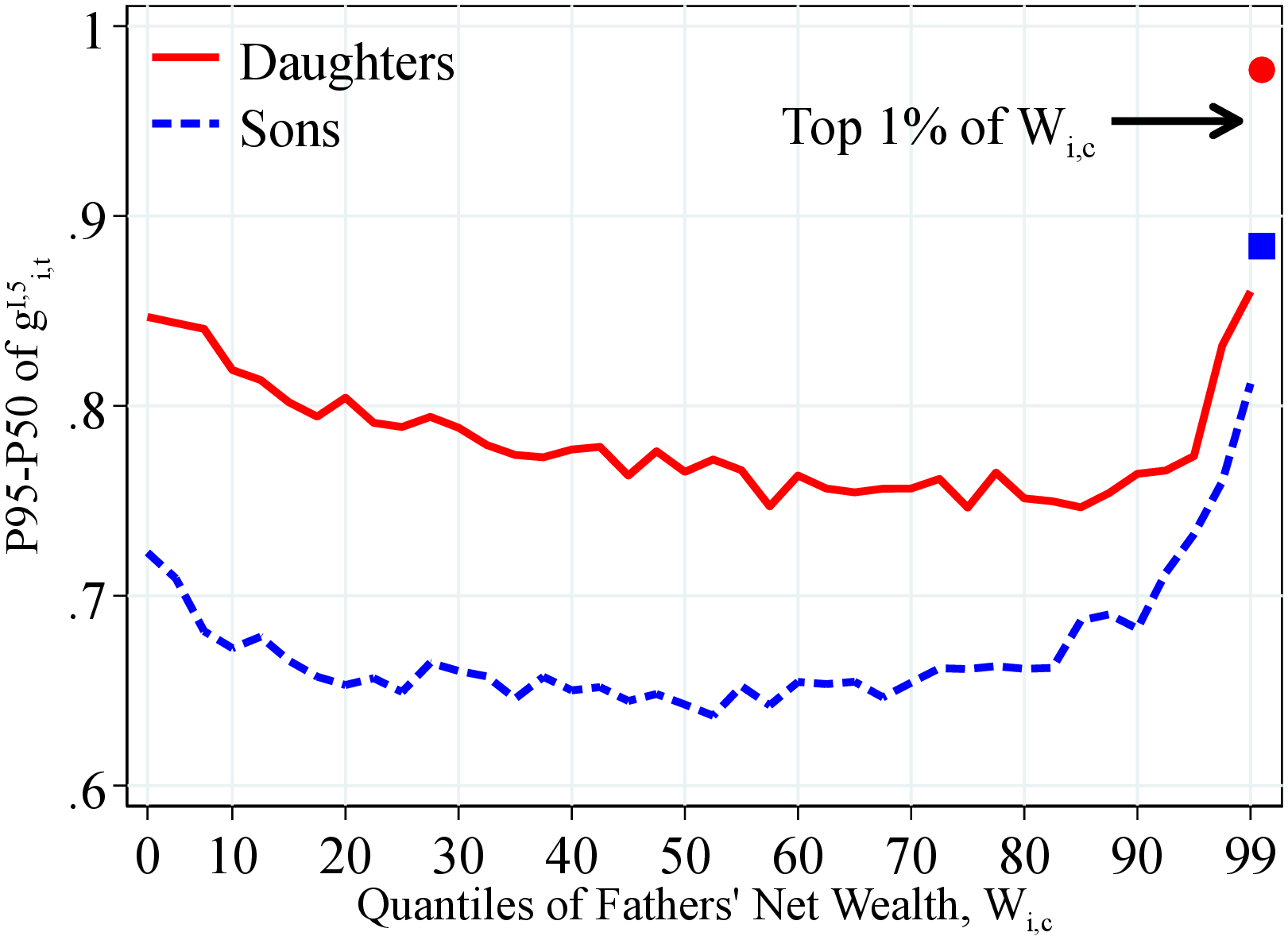

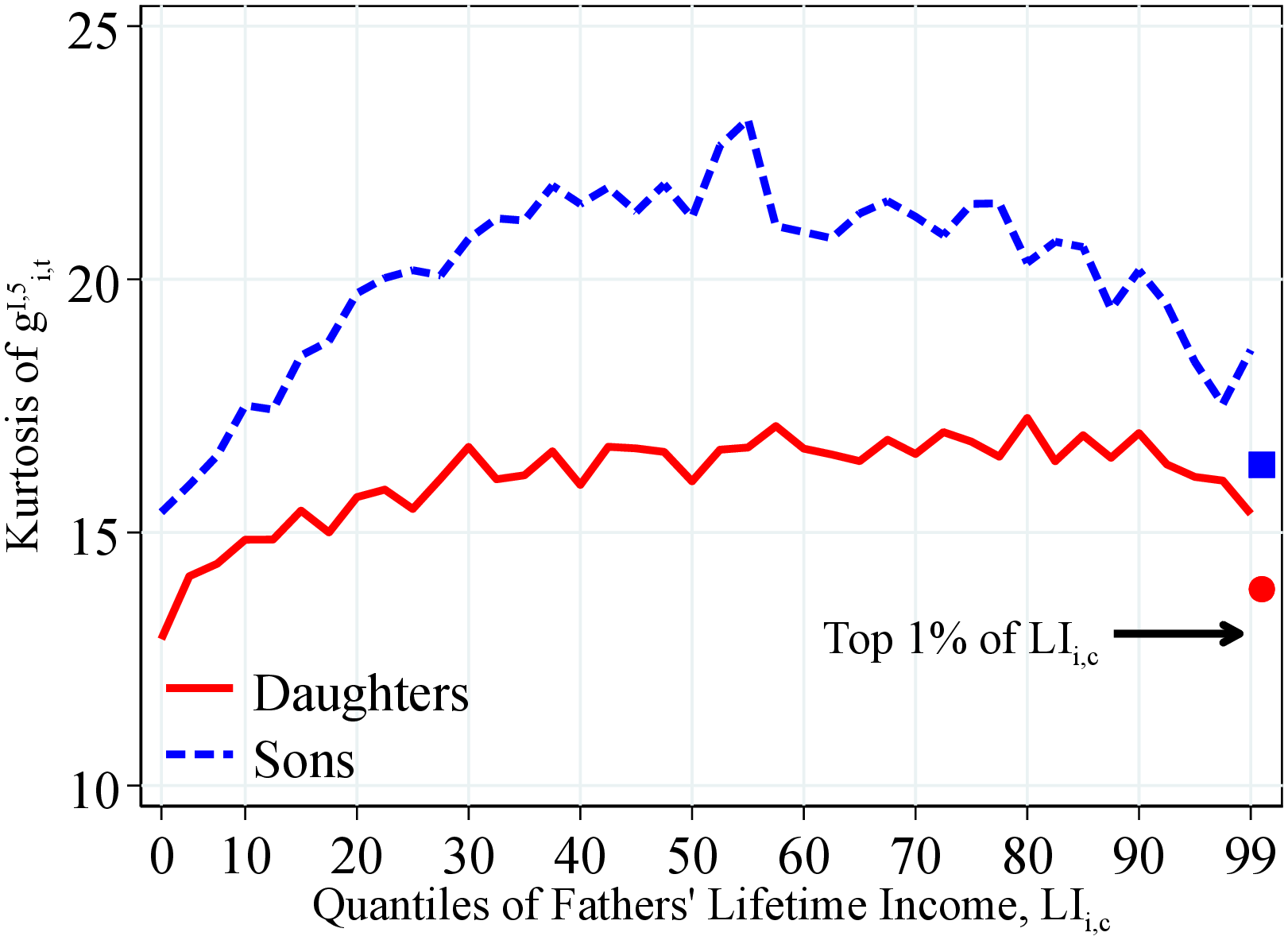

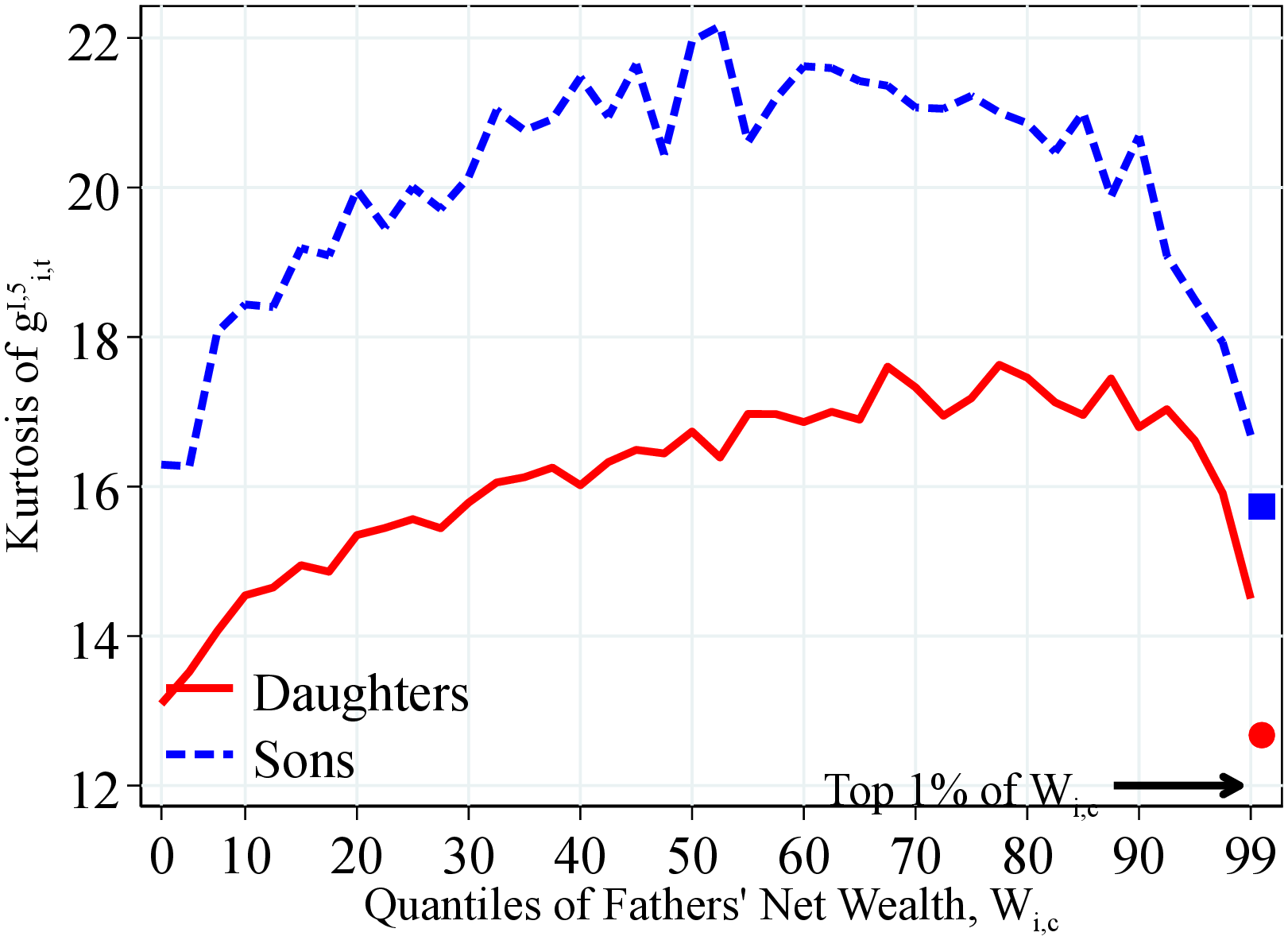

Motivated by these ideas, we investigate the relation between family resources—fathers’ lifetime income and net wealth—and children’s income dynamics. We follow the same methodology of Section 3.2.3 and analyze how the first four moments—mean, dispersion, skewness, and kurtosis—of the distribution of one-year log income changes of children vary across the distribution of fathers’ lifetime income and wealth. In particular, we rank fathers into 40 quantiles with respect to either their lifetime income, \(LI_{i,c}\), or their wealth, denoted by \(W_{i,c}\). We further group children of fathers at the top 1% of the income or wealth distribution in a separate bin. We then calculate the first four moments of residual income growth, \(g_{it}^{I,k}\), of children within each quantile.23 Similar to the previous section, we focus on percentile-based moments for one-year income changes. We also present results from standardized moments (because higher-order moments are sensitive to the extreme observations) as well as those for the five-year changes (which capture more persistent changes in after-transfer income) in Appendices C.2 and C.3, respectively. They show qualitatively similar patterns.

To make the measures of wealth comparable across cohorts, we normalize each individual’s net wealth by a year-age cell average—similar to how we construct the lifetime income measure. The data on wealth only span from 1993 to 2014; therefore, we cannot observe the wealth of most fathers when they were young. However, this is a minor issue since wealth is a stock variable—unlike income (a flow variable)—which makes it much more persistent than income. Therefore, in our analysis we consider the average residual net worth of a household calculated between ages 45 and 54. Some cohorts either are not in our sample or have only a few observations in this age interval. For them, we use observations in years closest to these ages.

(a) By Lifetime Income

(a) By Lifetime Income (b) By Net Wealth

(b) By Net Wealth

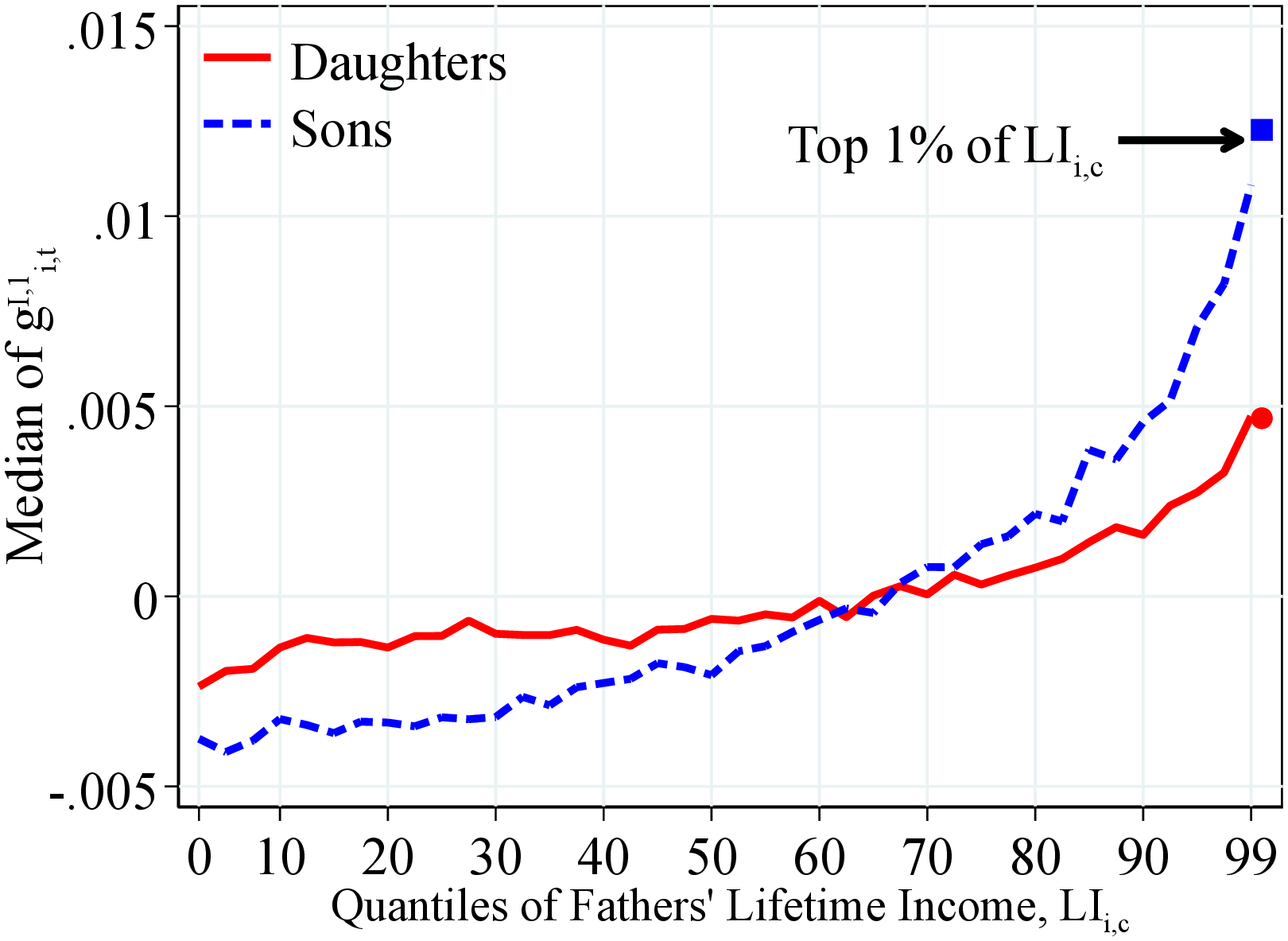

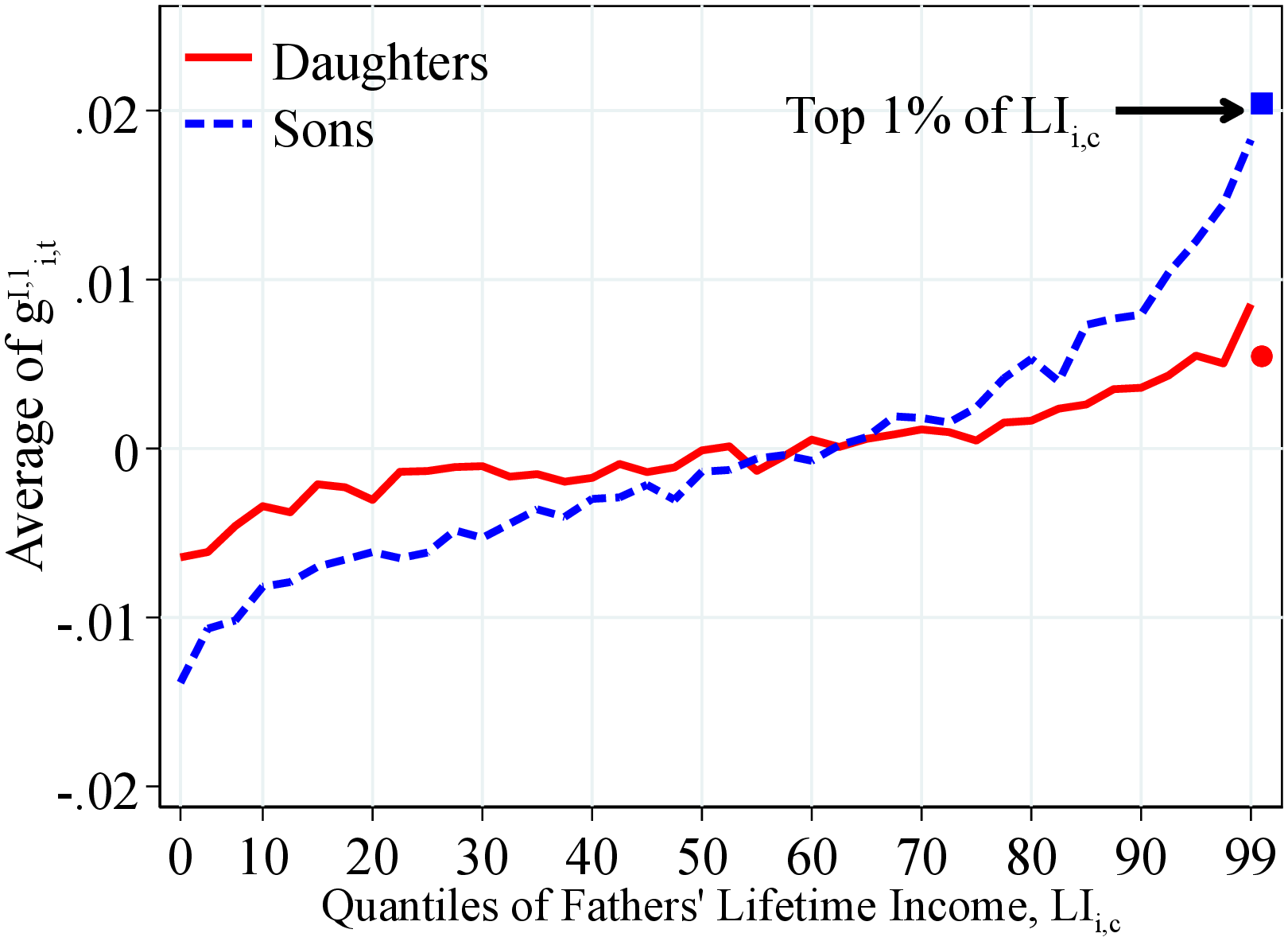

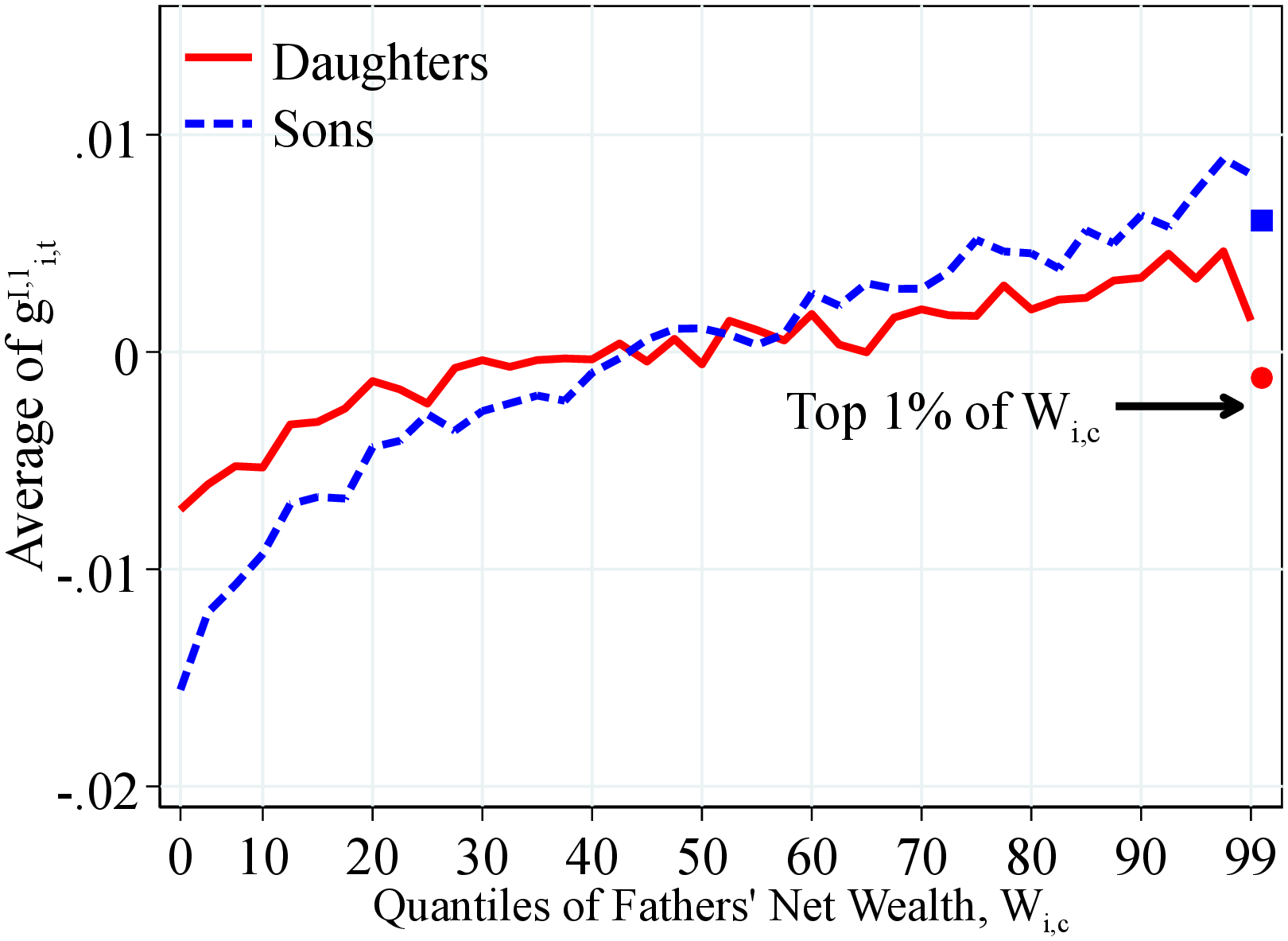

Figure: Figure 12 – Median Log Income Growth by Fathers’ Resources

Notes: Figure 12 shows the median of one-year residual earnings growth for men and women within quantiles of fathers’ lifetime income distribution (Panel A) and fathers’ household net wealth distribution (Panel B) in 40 quantiles. Each line has been normalized to have a mean of 0. The top 2.5% of the distribution is further separated into two groups (97.5th to 99th and 99th percentile and above) for a total of 41 quantiles. The markers identify the children of fathers at the top 1% of the lifetime income and wealth distributions. We show the average across annual moments between 1990 and 2012 as we require that individuals have non-missing one- and five-year changes.

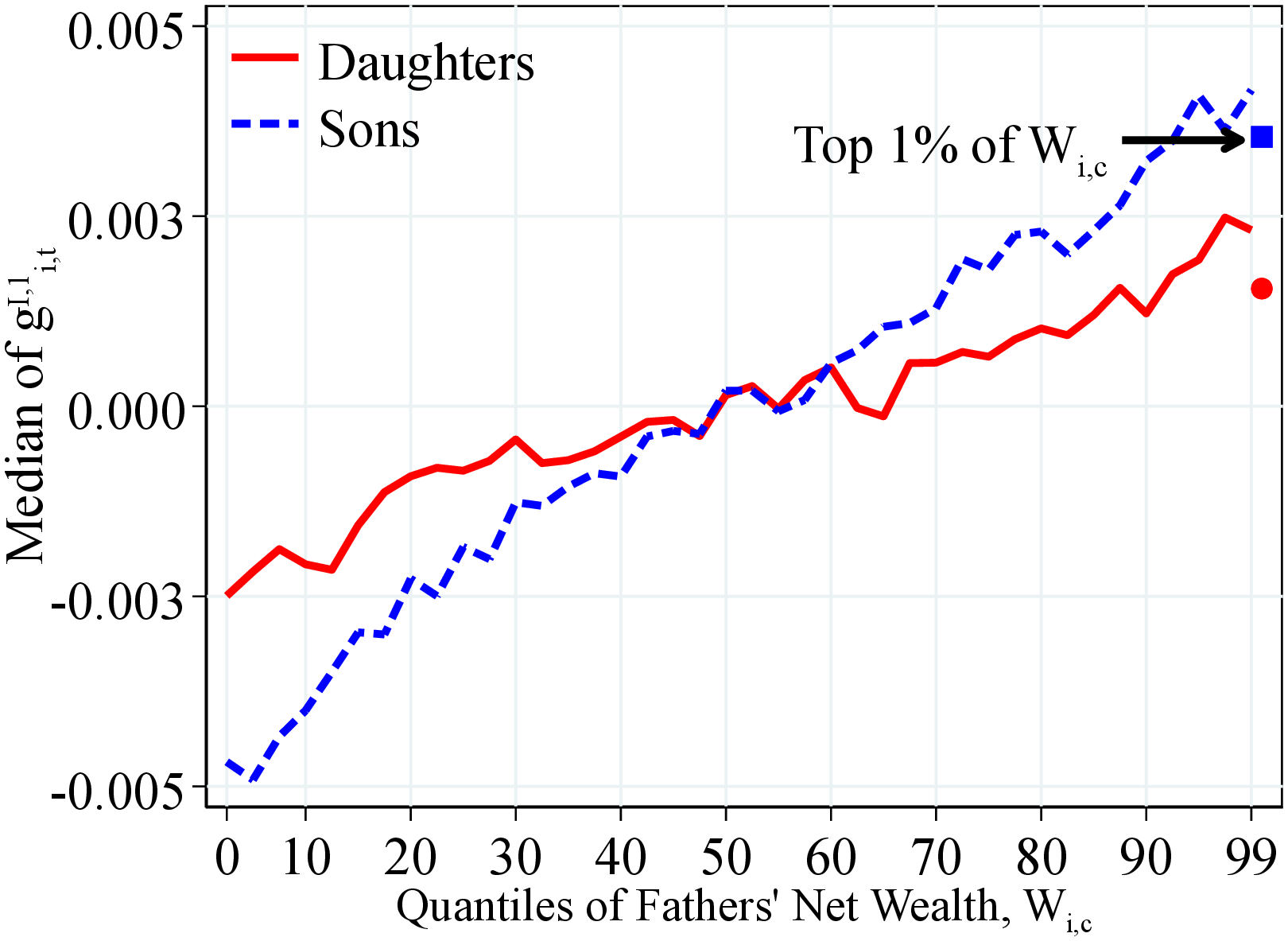

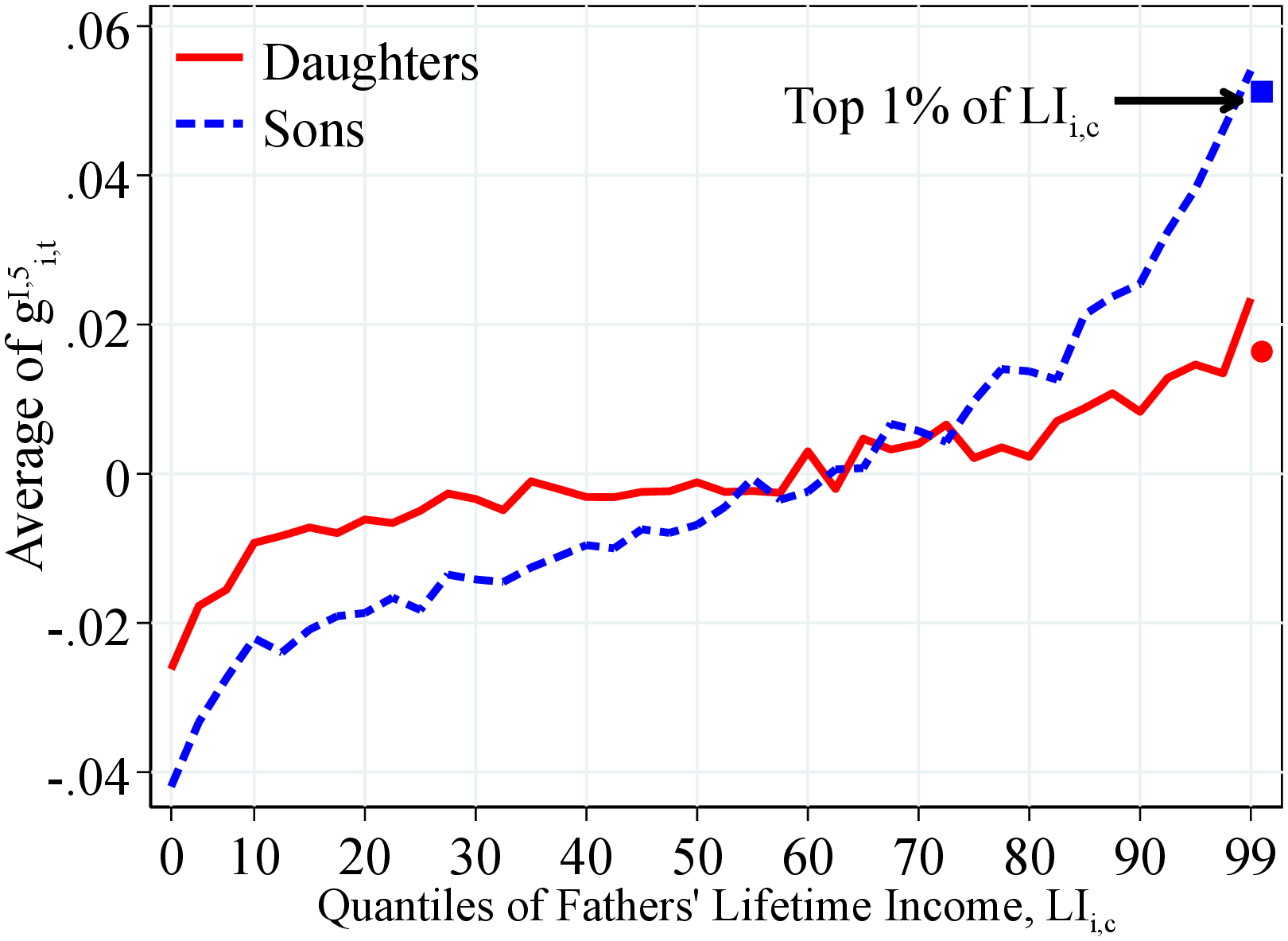

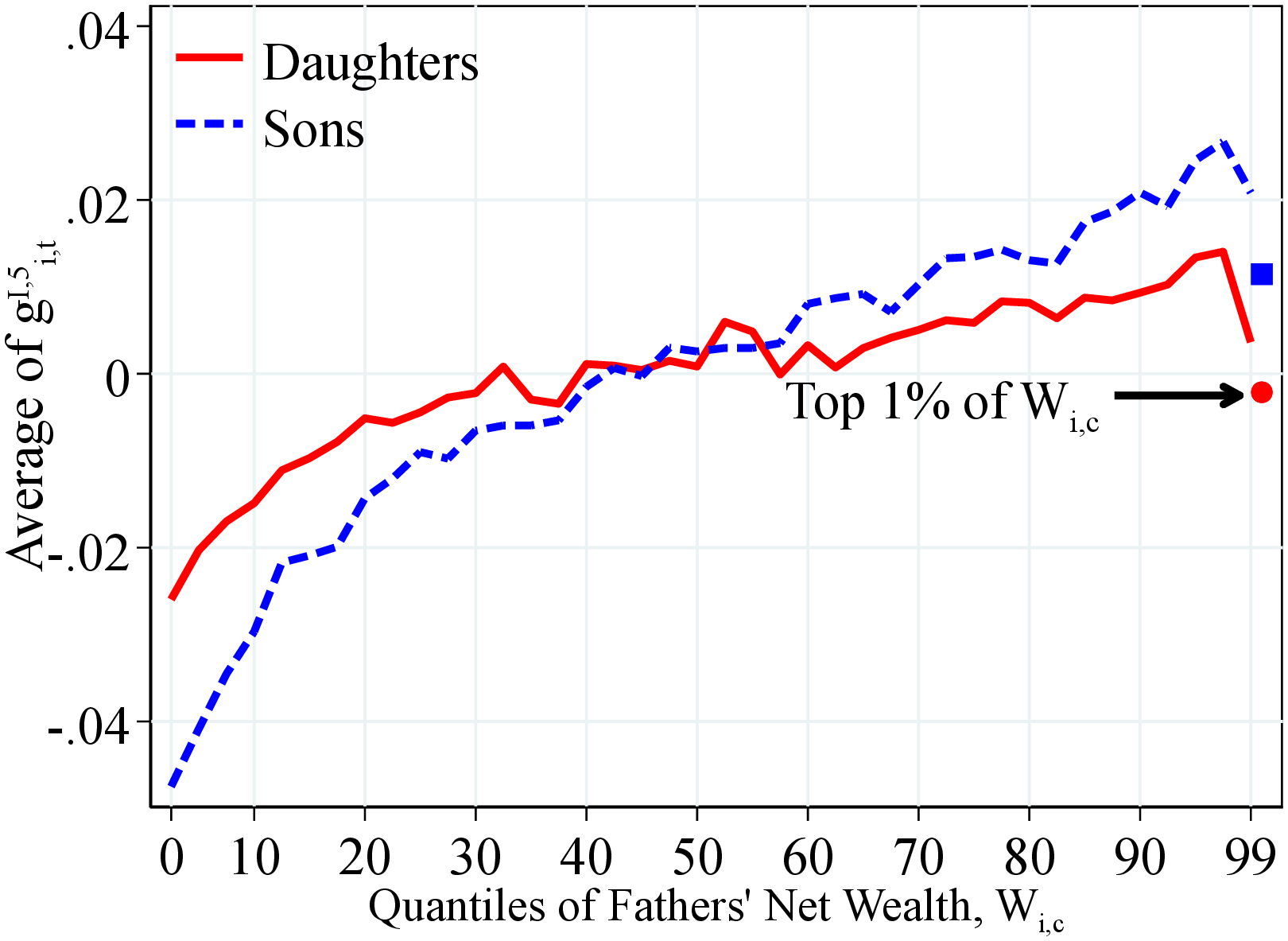

Median Income Growth. Figure 12 shows how children’s median annual income growth varies by family resources measured by fathers’ lifetime income or wealth. We find that lifetime income growth is significantly higher for workers born into richer families. For example, median annual income growth for sons of fathers at the 90th percentile of the lifetime income distribution is almost 1% higher relative to those with parents at the 10th percentile. The corresponding difference among daughters is lower at around 0.5%. This heterogeneity is economically significant, considering that the typical estimates of the standard deviation of heterogeneous income profiles are around 2% for the U.S. (see Guvenen et al. (2021)). The variation over the father’s wealth distribution is qualitatively and quantitatively similar and slightly more pronounced.

The heterogeneity in average income growth arising from parental financial resources is even larger, with around a 2% difference between the children of parents at the 90th percentile and those from the 10th percentile (Figure OA.III.4). Furthermore, children of top earners enjoy an exceptionally steeper average income growth over the life cycle—specifically, 2% higher compared to those from the median-income families. These results indicate an increasingly right-skewed distribution of earnings growth by fathers’ income. We confirm this conjecture when we investigate the skewness of income growth.

(a) By Lifetime Income

(a) By Lifetime Income (b) By Net Wealth

(b) By Net Wealth

Figure: Figure 13 – Dispersion of Log Earnings Growth by Fathers’ Resources

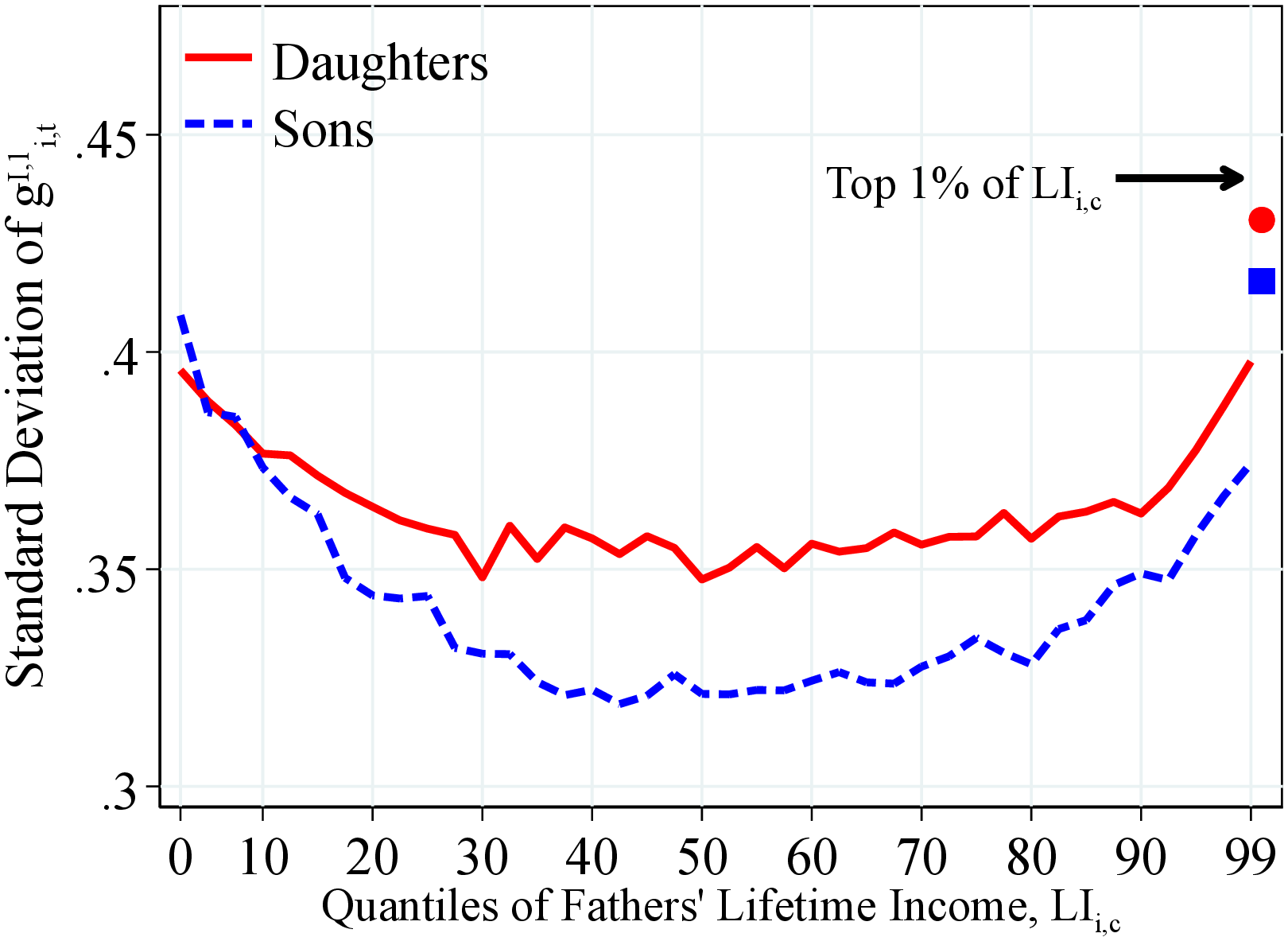

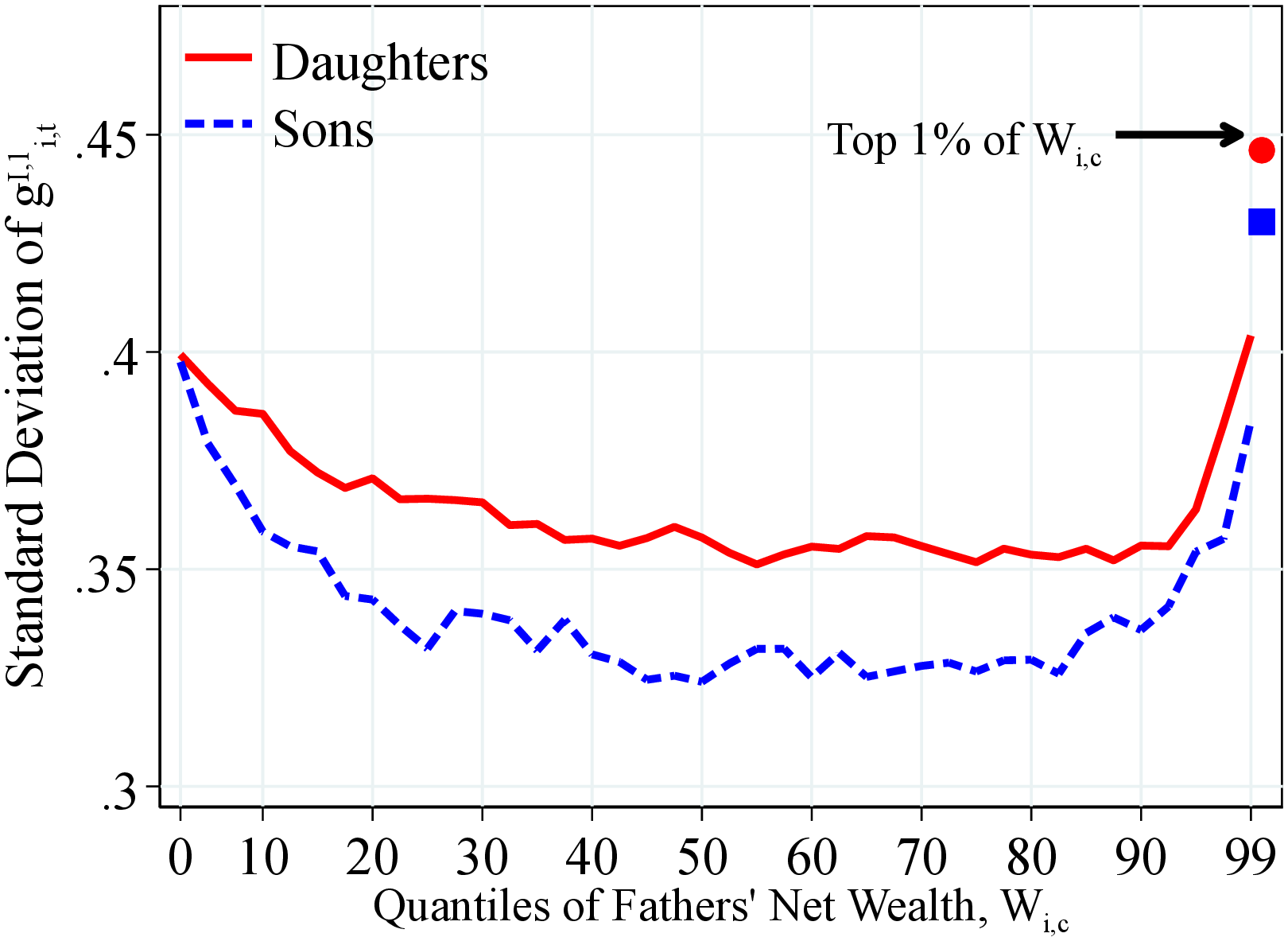

Notes: Figure 13 shows the standard deviation of one-year residual earnings growth for men and women within quantiles of fathers’ lifetime income distribution (Panel A) and fathers’ household net wealth distribution (Panel B) in 40 quantiles. The top 2.5% of the distribution is further separated into two groups (97.5th to 99th and 99th percentile and above) for a total of 41 quantiles. The markers identify the children of fathers at the top 1% of the lifetime income and wealth distributions. We show the average across annual moments between 1990 and 2012 as we require that individuals have non-missing one- and five-year changes.

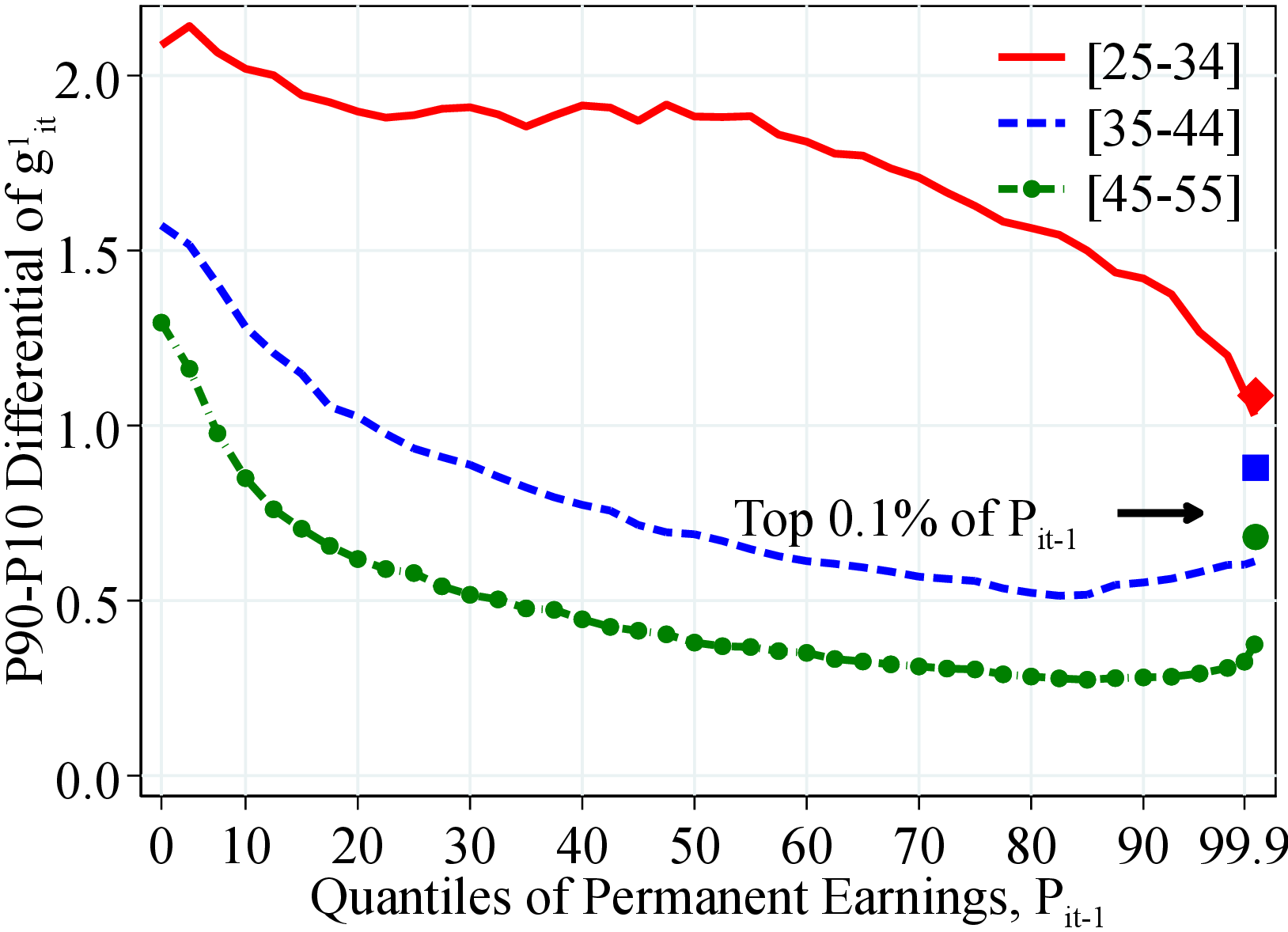

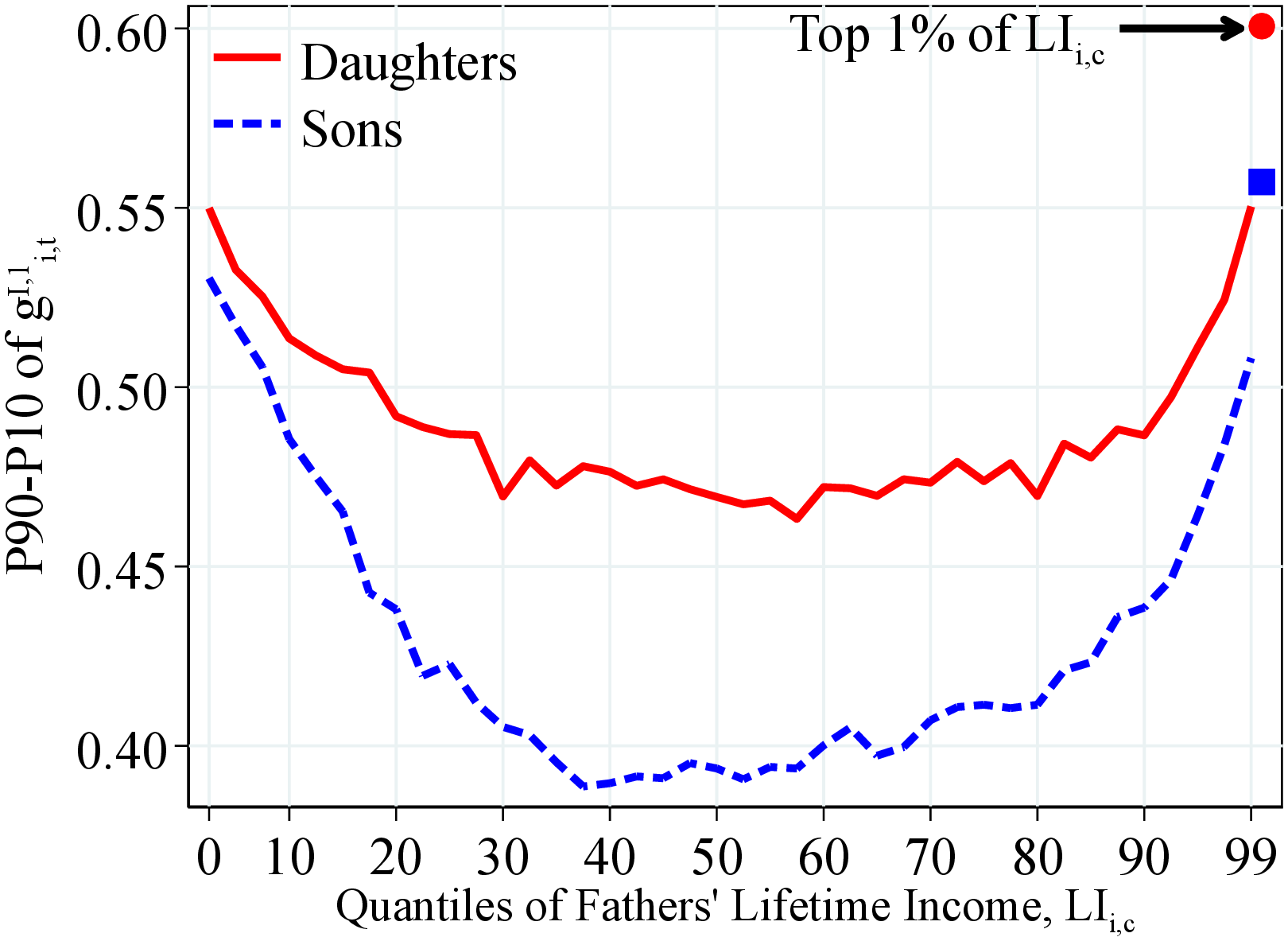

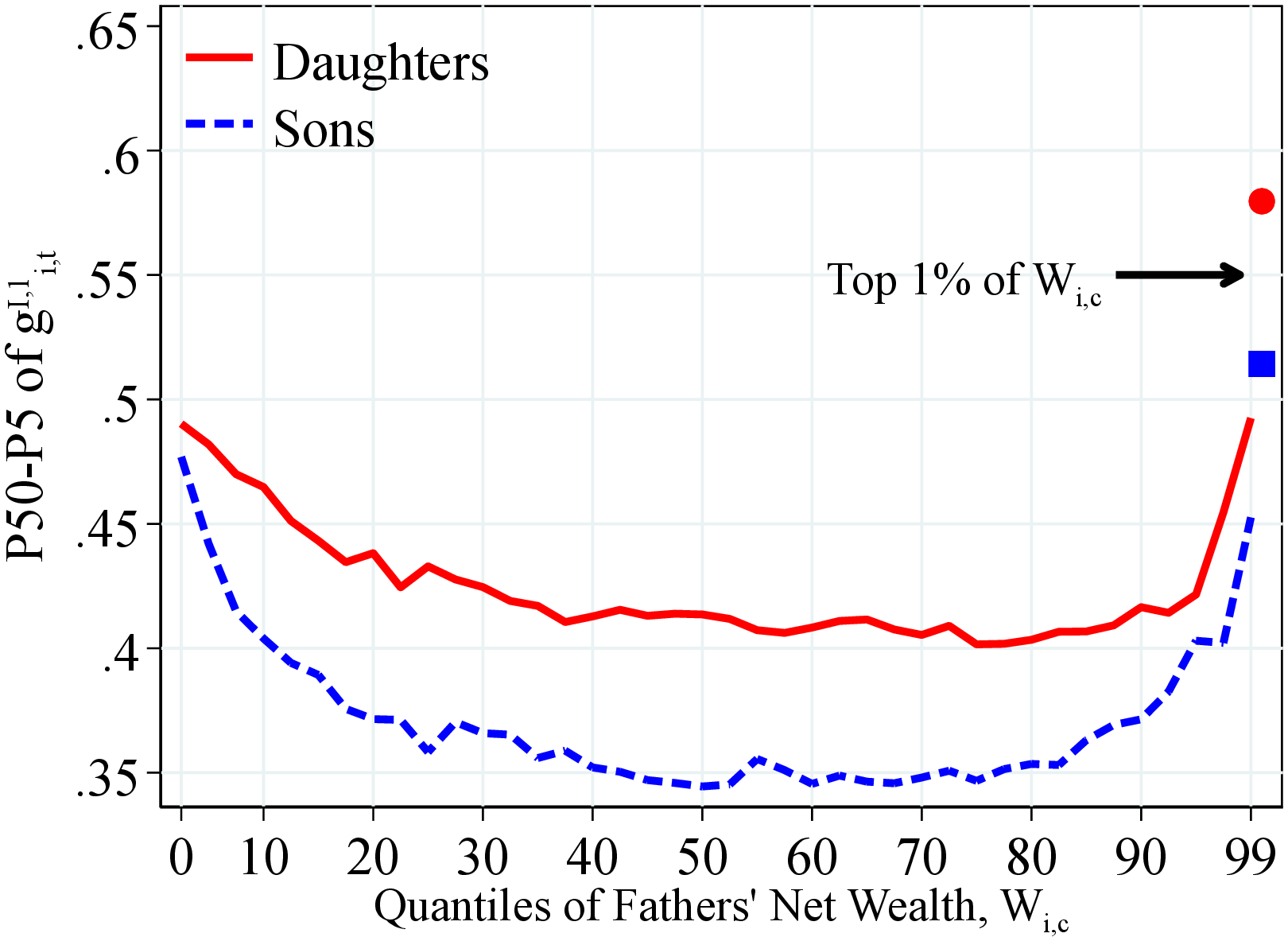

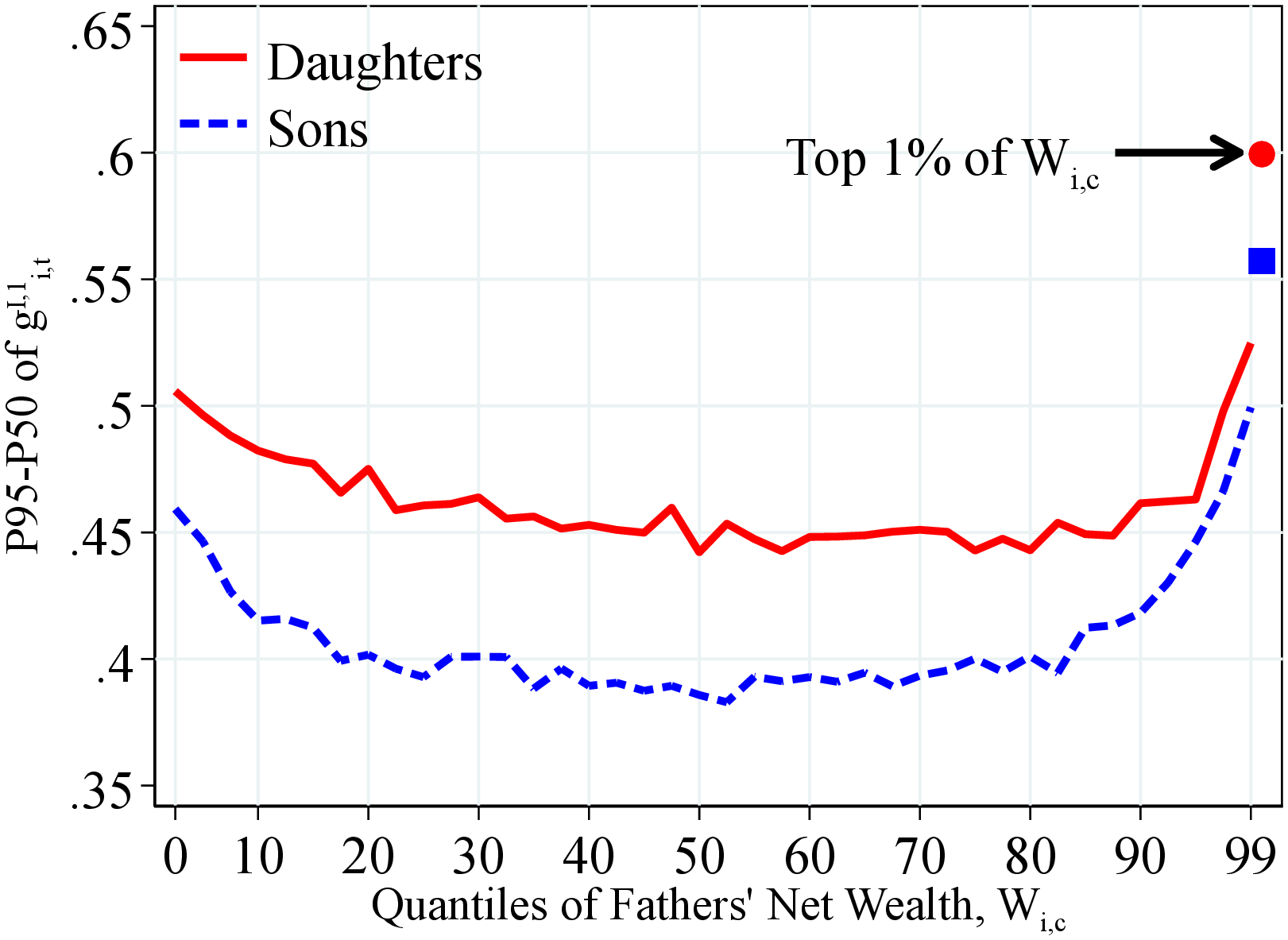

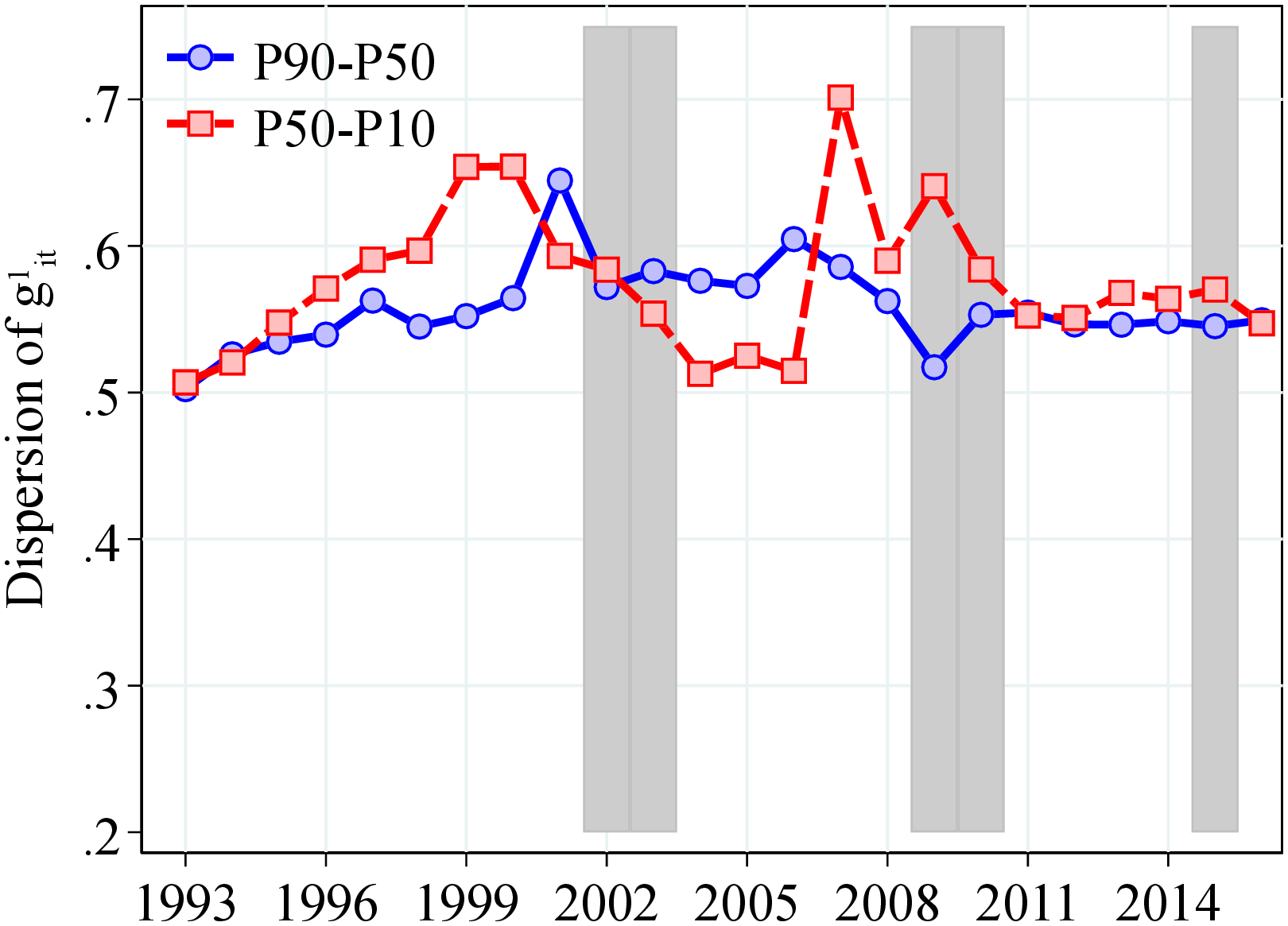

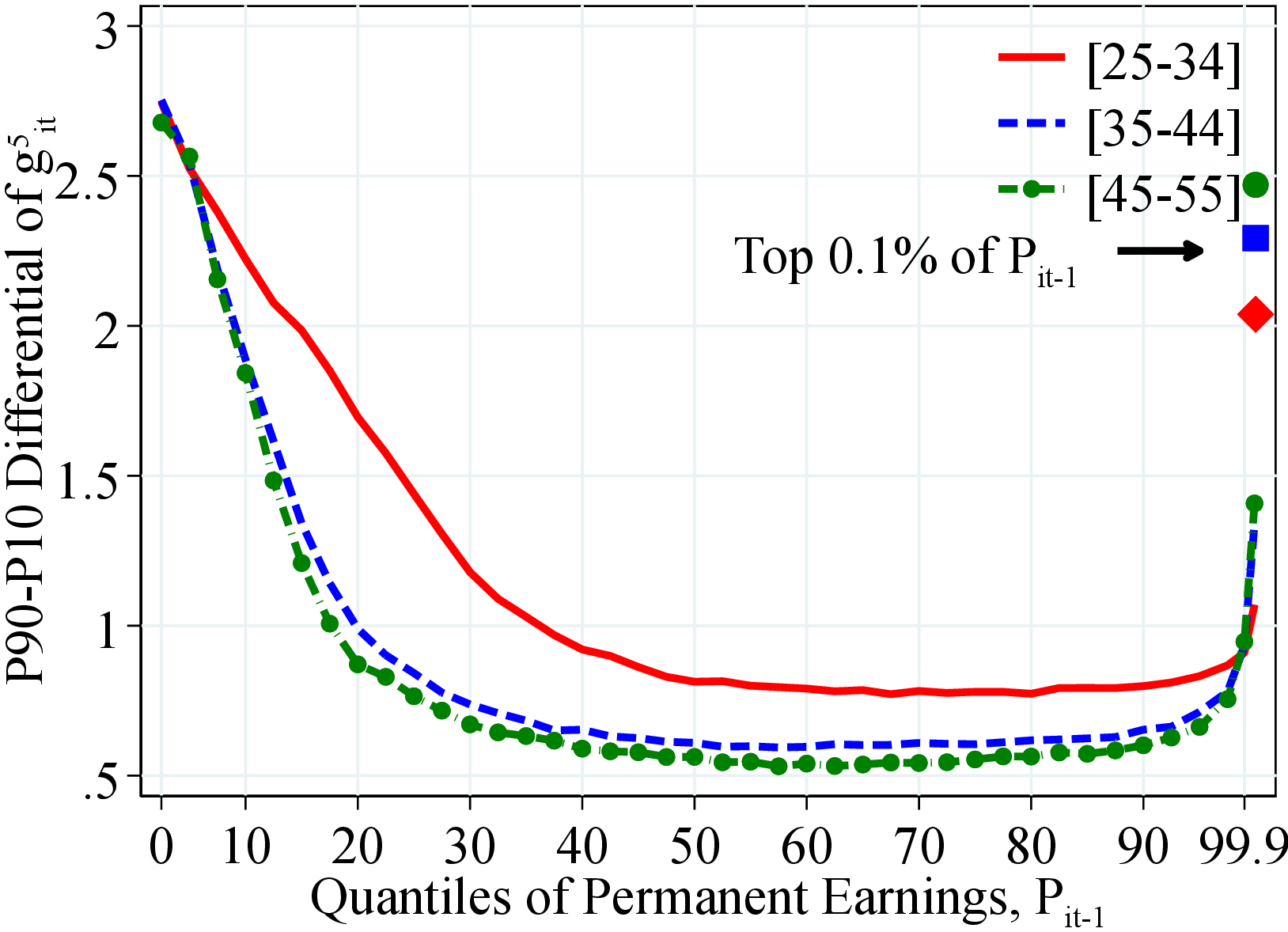

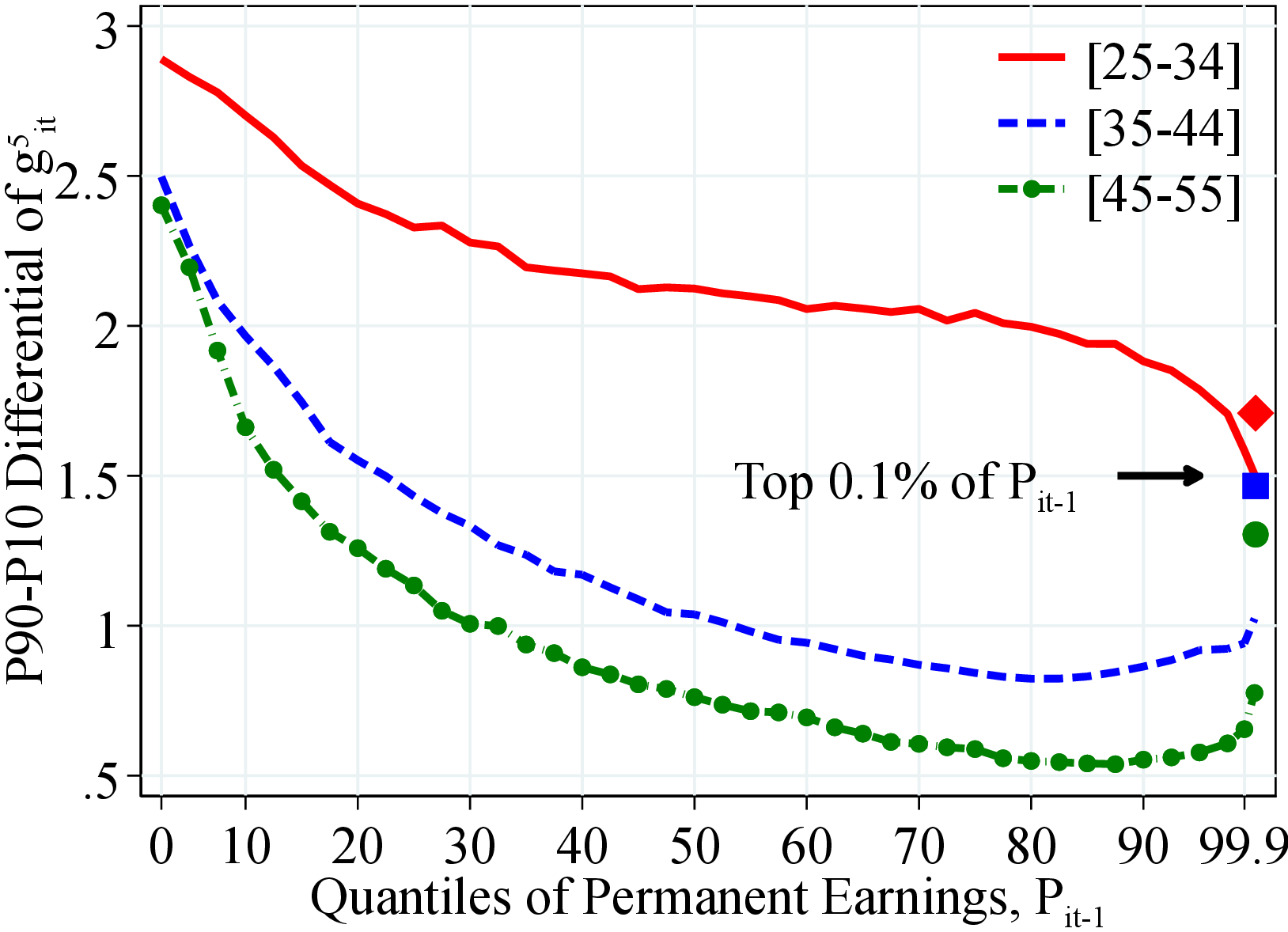

Volatility of Income Growth. Figure 13 shows that the volatility of children’s income growth—as measured by the P90-P10 differential—follows a U-shaped pattern by the fathers’ lifetime income (left panel) and wealth (right panel). This pattern is more pronounced for sons than for daughters. For example, the P90-P10 of income changes for sons (daughters) with fathers at the 1st and 99th percentiles of the lifetime income distribution is around 12 (9) log points larger than those with median-income fathers.

Children of more affluent fathers face significantly more volatile incomes. For example, the P90-P10 of income growth for workers of fathers from the top 1% of the lifetime income or wealth distributions is roughly 12 to 18 log points higher compared to those of fathers at the median. This higher income volatility for children with rich fathers, combined with their exceptionally higher median and (especially) average income growth (shown in Figures 12 and OA.III.4), suggests that they can pursue high-risk, high-return careers that children from modest backgrounds cannot.

Recall that we also find a U-shaped pattern in the dispersion of earnings growth over workers’ permanent earnings in Section 3.2.3 (Figure 5). However, the U-shaped pattern here is tilted toward the right over the fathers’ lifetime income and wealth distribution compared to the variation by workers’ own permanent earnings. That is, children of high-income, high-wealth fathers experience the most volatile incomes, whereas the volatility of earnings shocks is the highest for workers with the lowest permanent earnings. These results suggest that the relation between workers’ income volatility and their fathers’ financial resources is not due to the omitted variable of workers’ permanent earnings, which is correlated with fathers’ resources. We investigate this conjecture further in Section 4.4 when we control for a full set of children and father characteristics.

(a) By Lifetime Income

(a) By Lifetime Income (b) By Net Wealth

(b) By Net Wealth

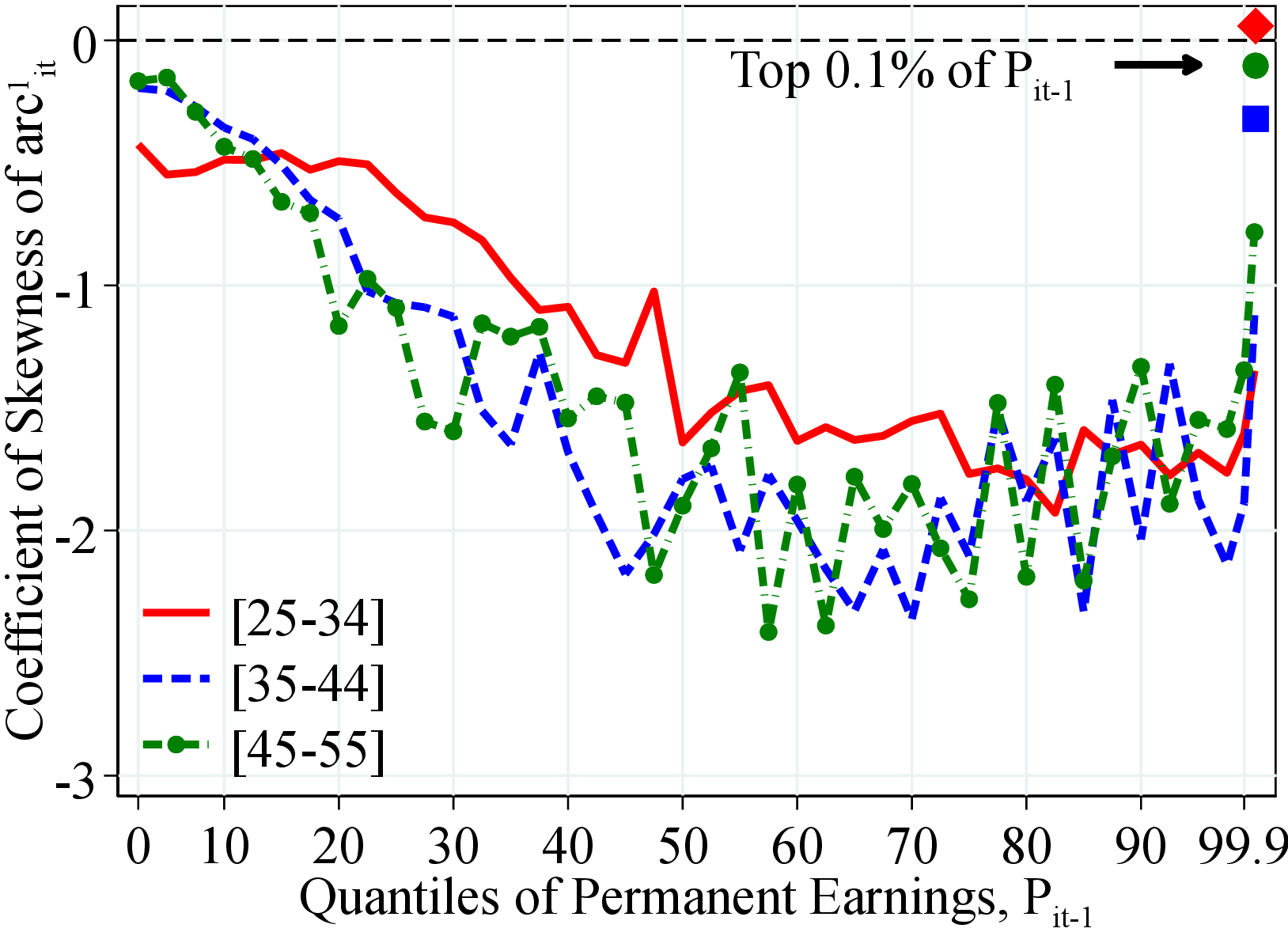

Figure: Figure 14 – Skewness of Log Earnings Growth by Fathers’ Resources

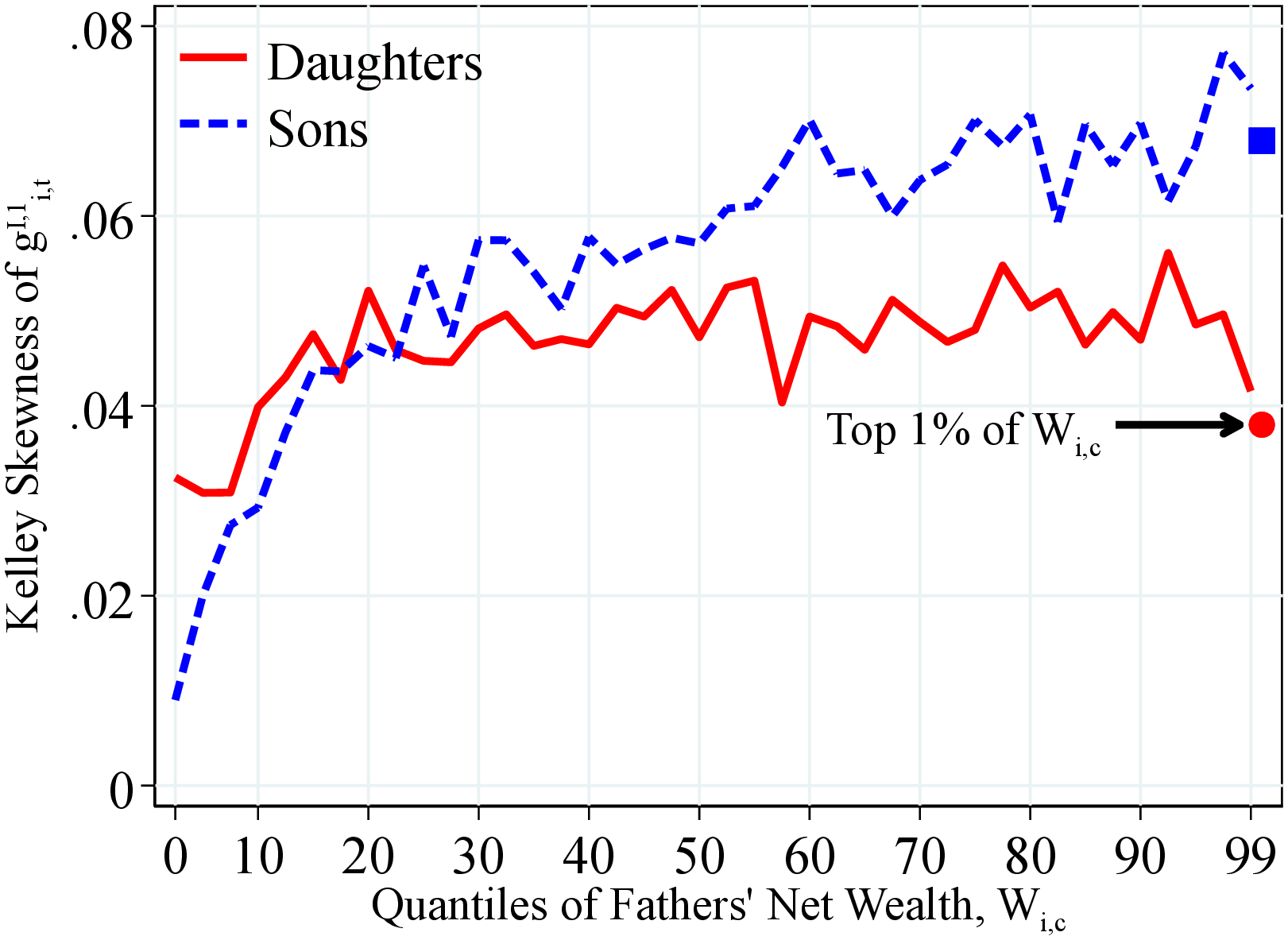

Notes: Figure 14 shows the Kelley skewness of one-year residual earnings growth for men and women within quantiles of fathers’ lifetime income distribution (Panel A) and fathers’ household net wealth distribution (Panel B) in 40 quantiles. The top 2.5% of the distribution is further separated into two groups (97.5th to 99th and 99th percentile and above) for a total of 41 quantiles. The markers identify the children of fathers at the top 1% of the lifetime income and wealth distributions. We show the average across annual moments between 1990 and 2012 as we require that individuals have non-missing one- and five-year changes.

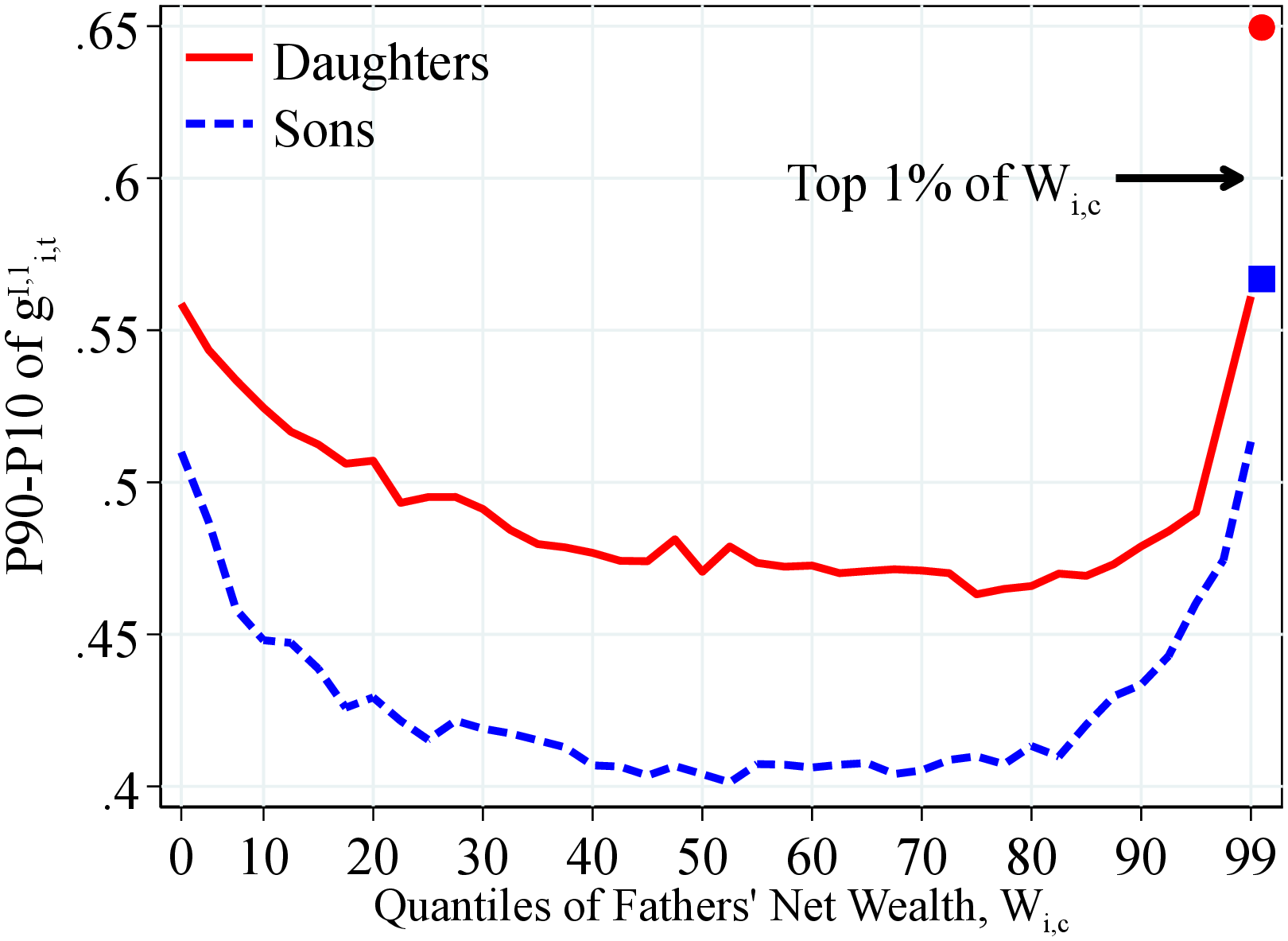

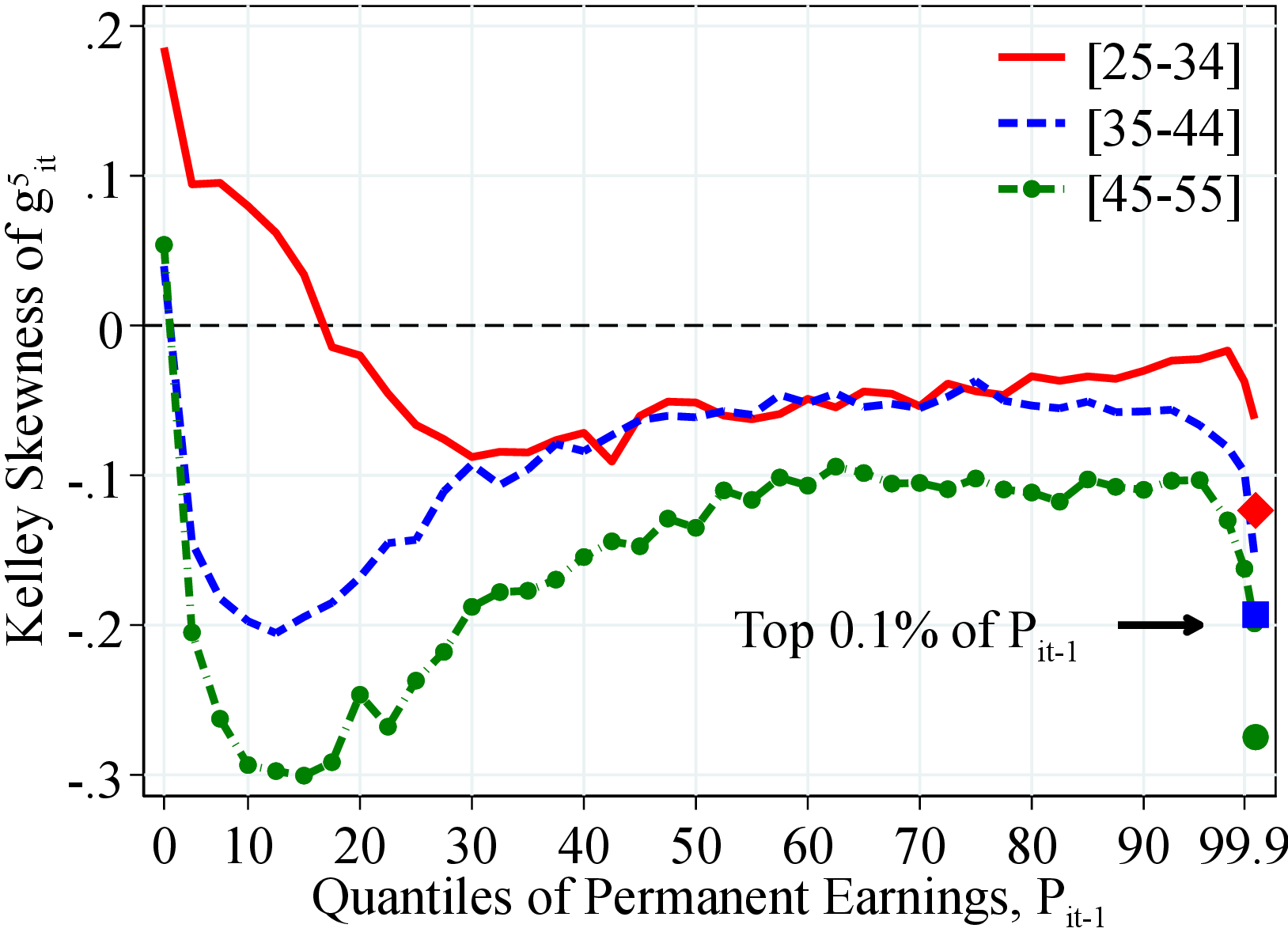

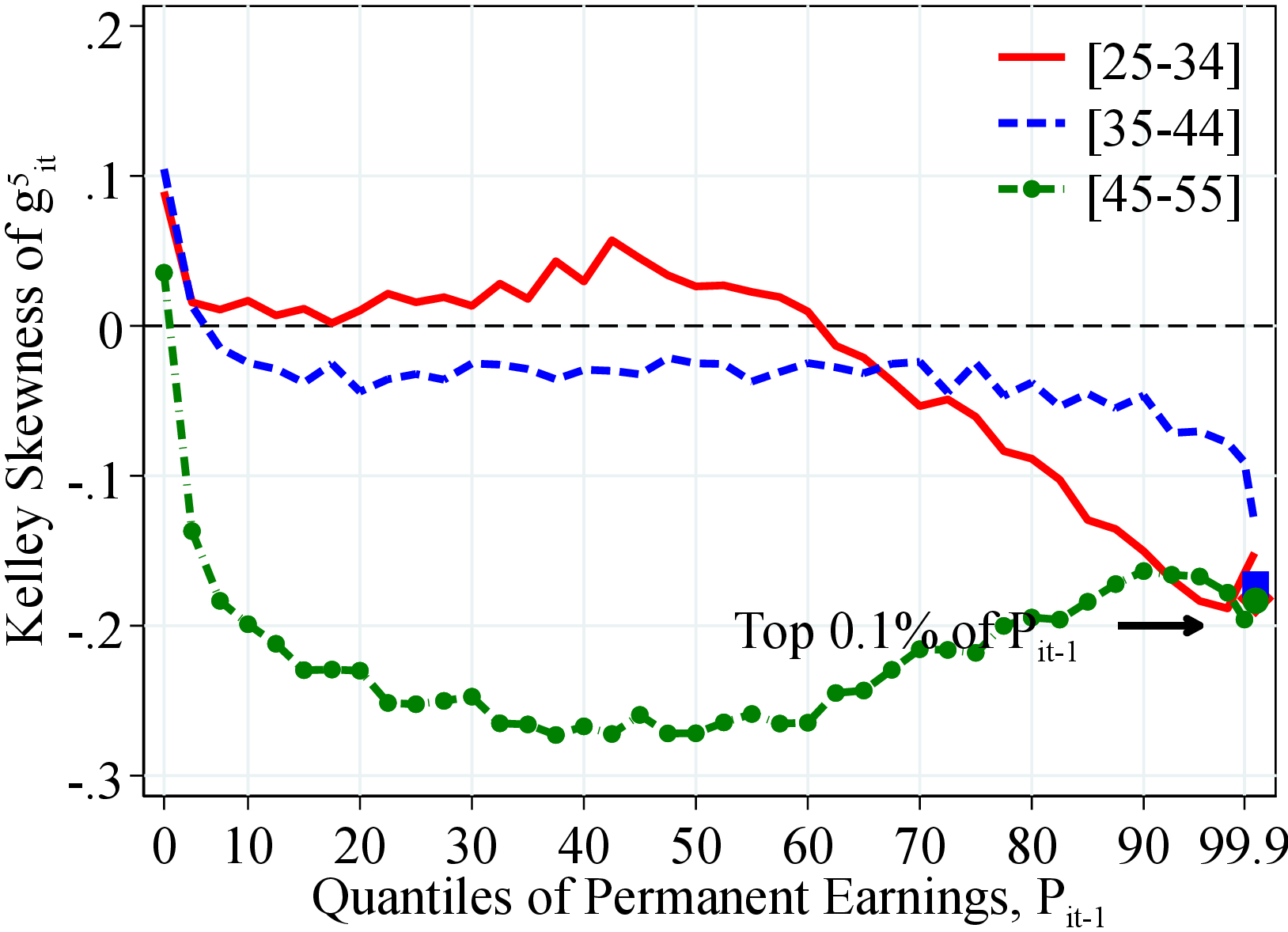

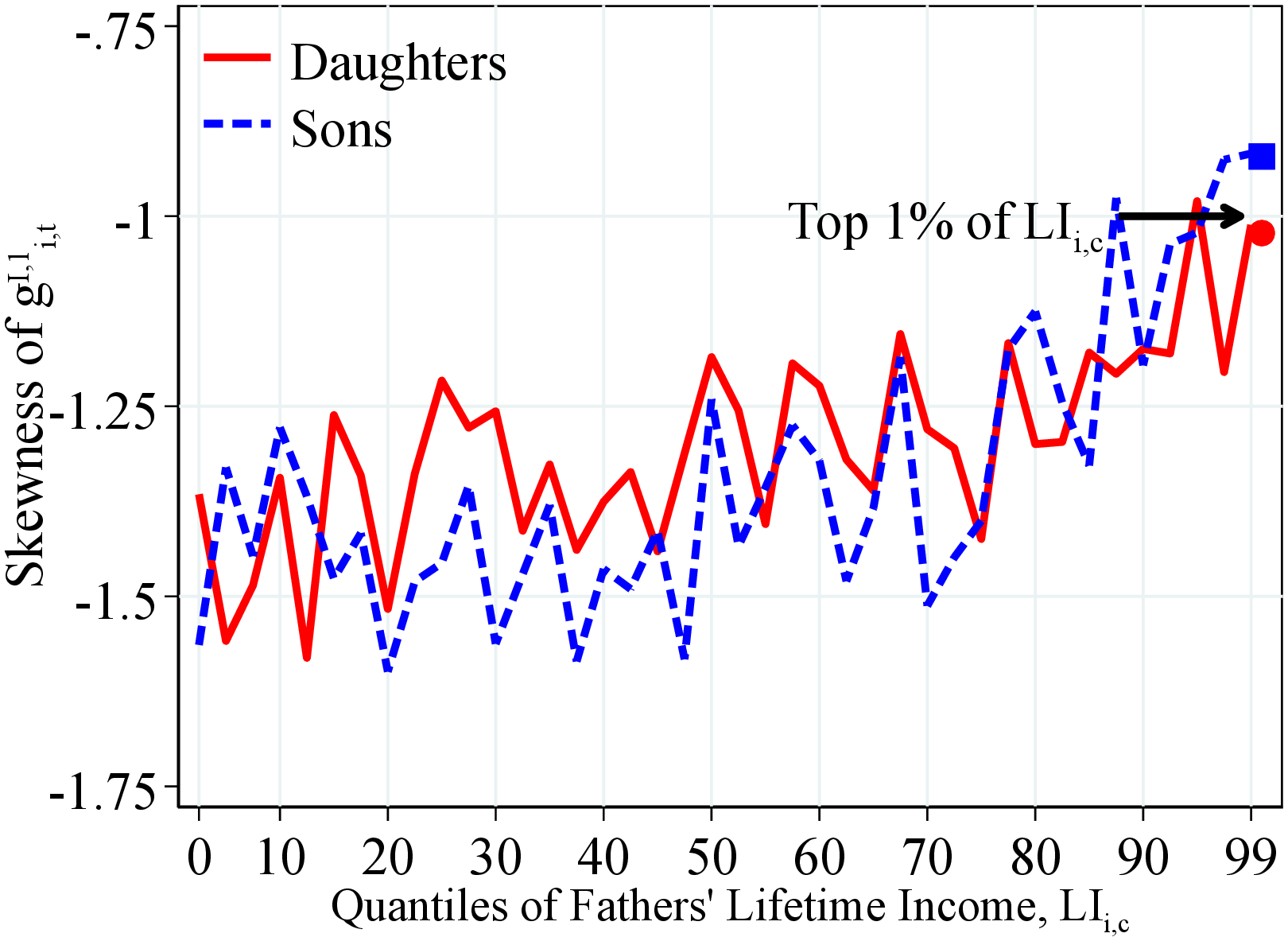

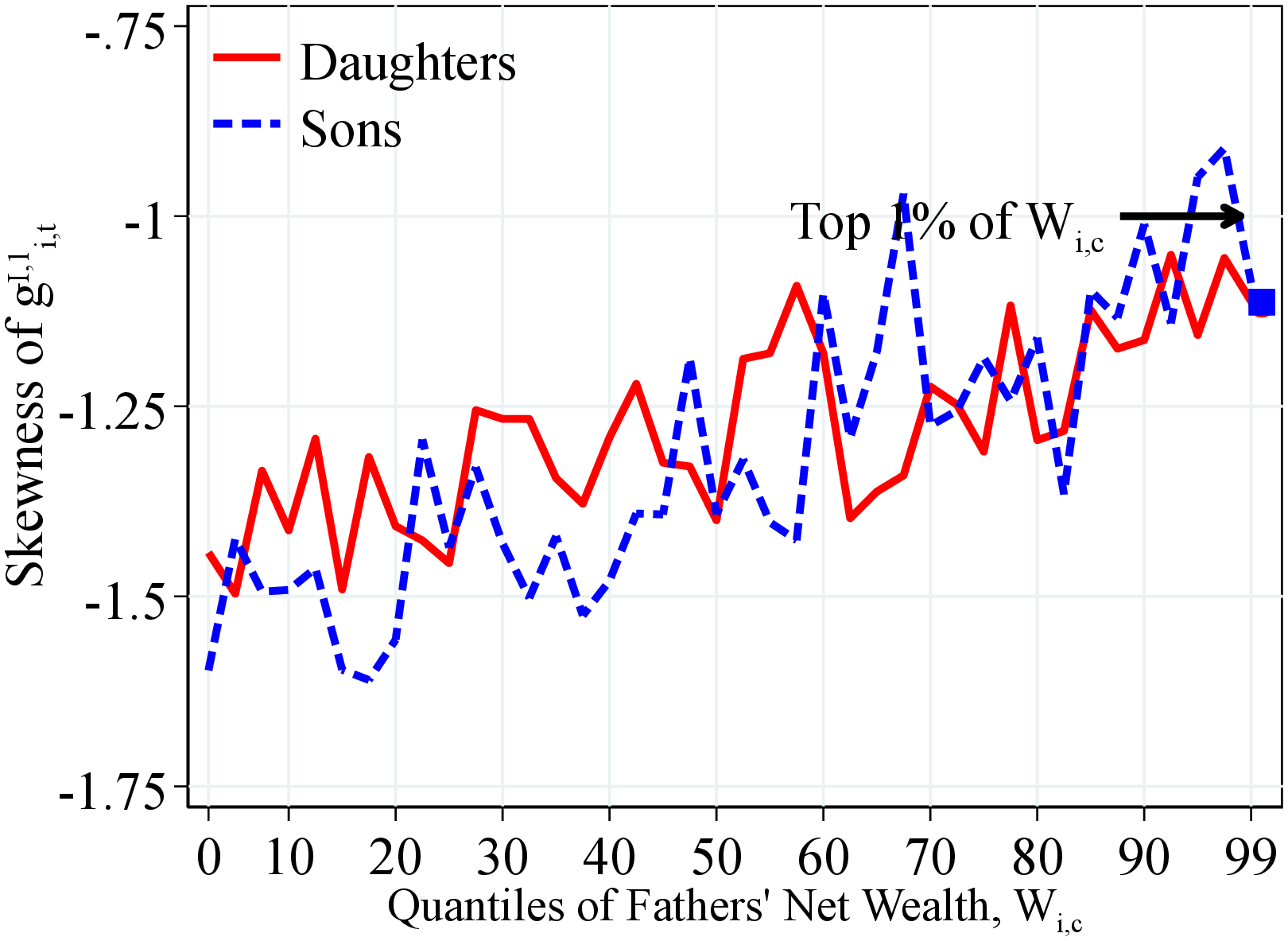

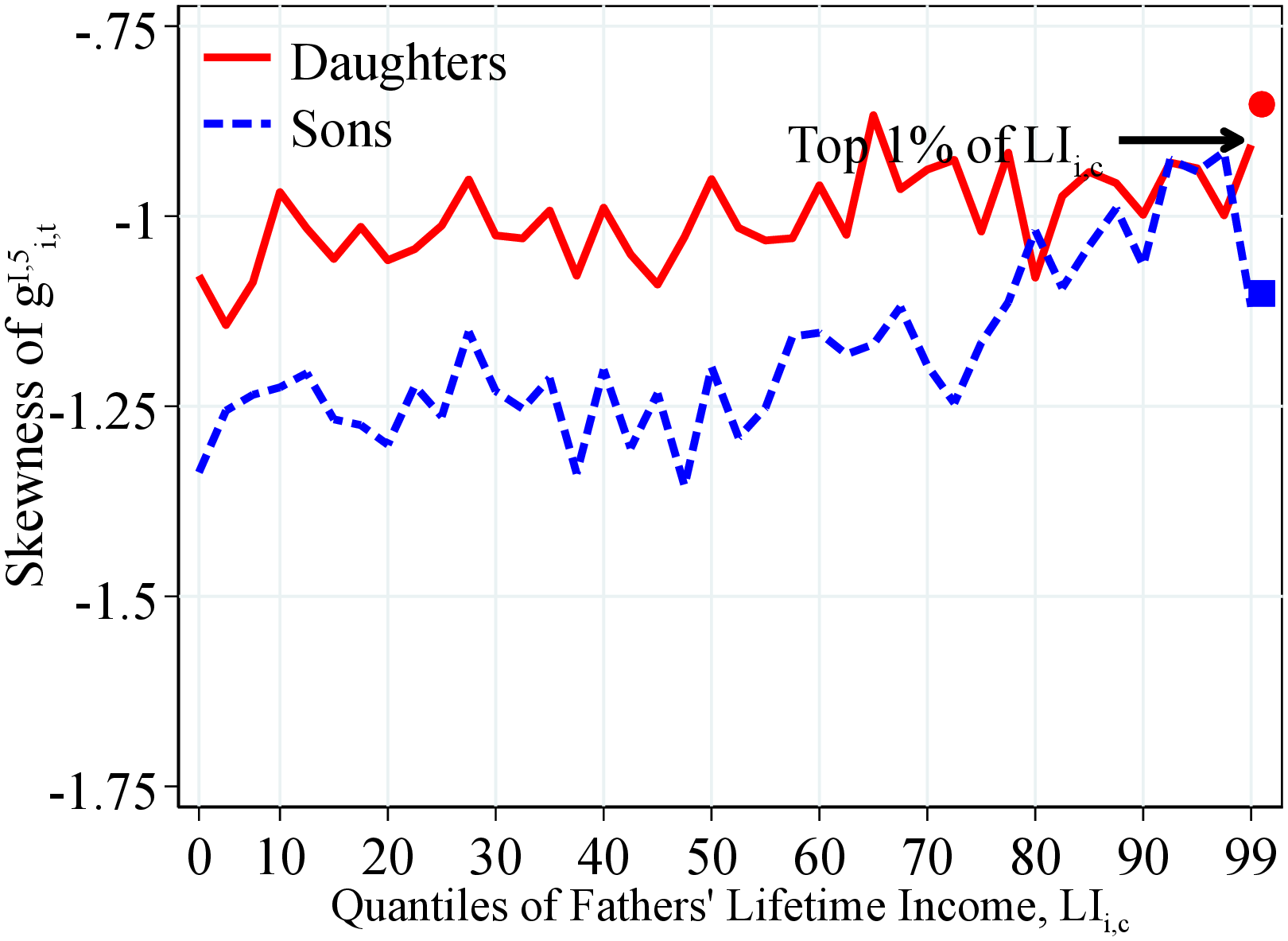

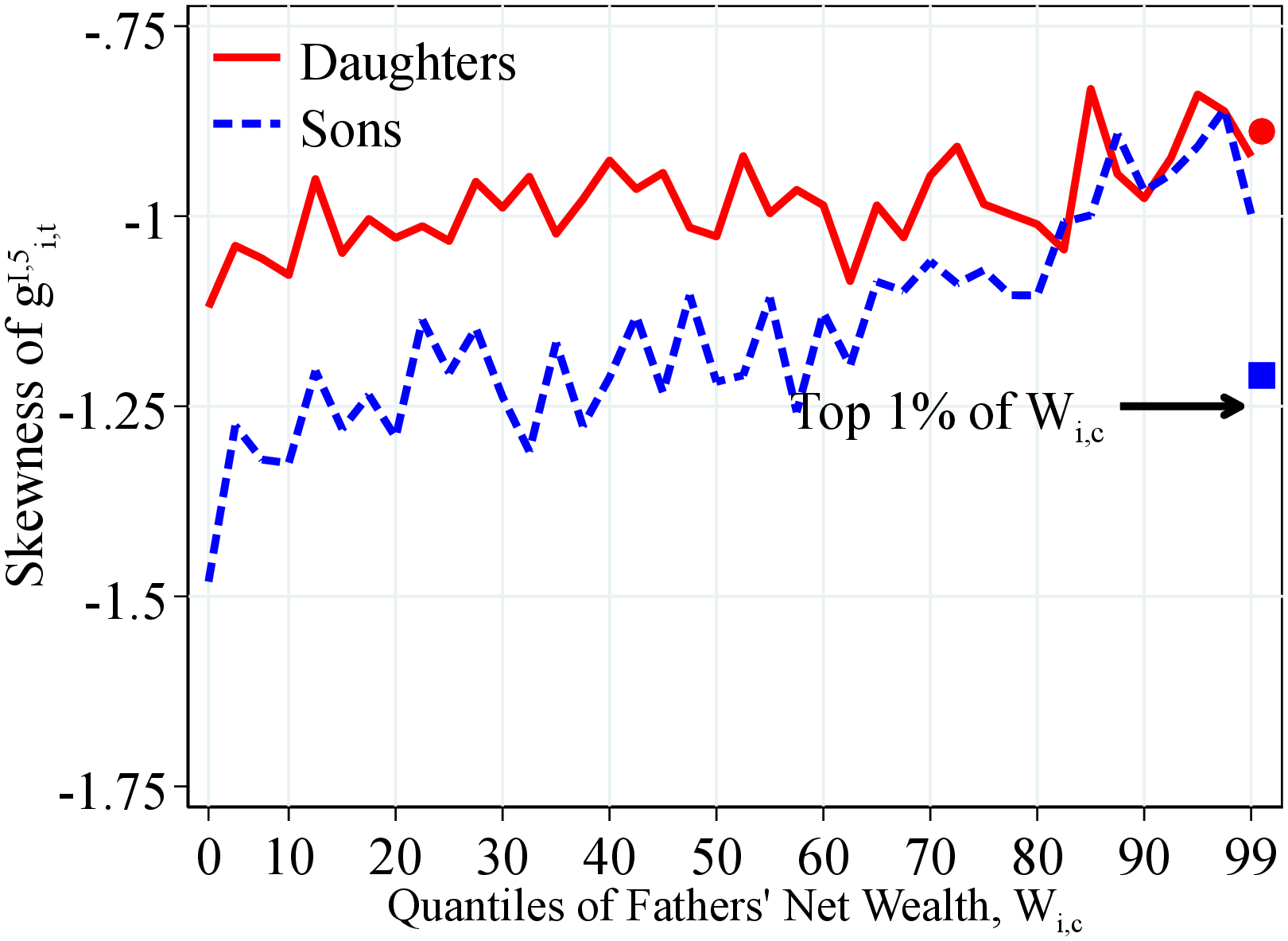

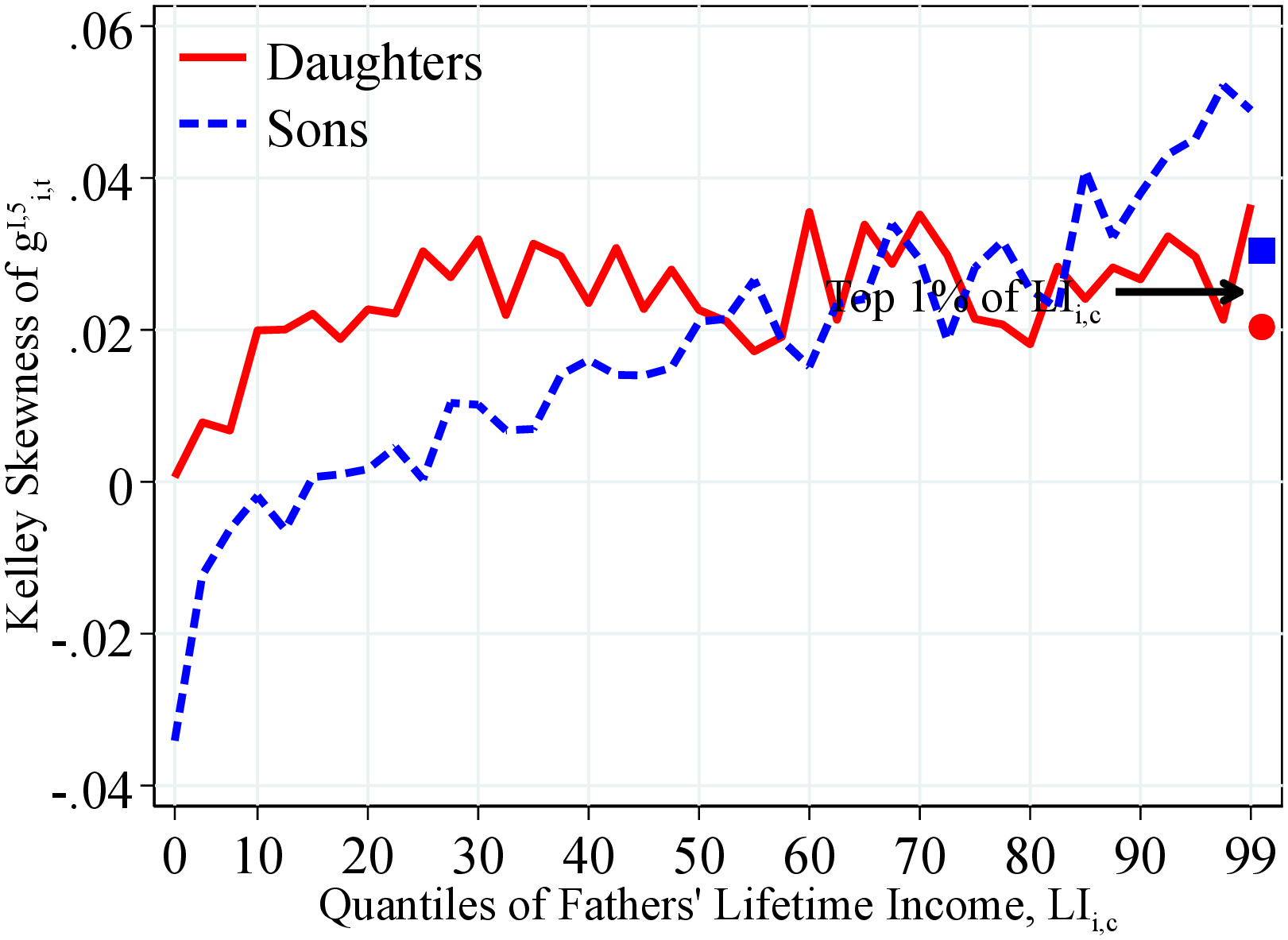

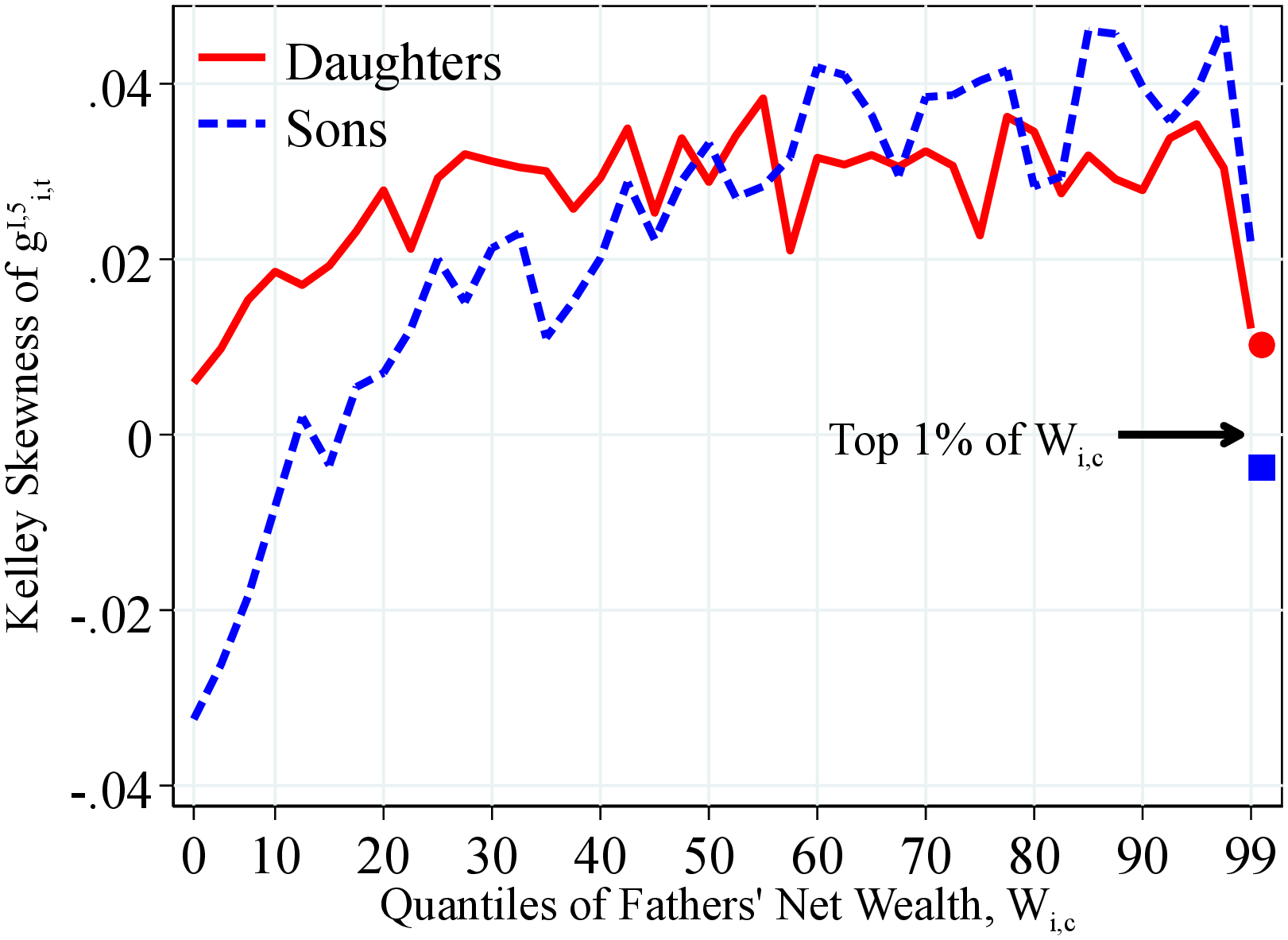

Skewness of Income Growth. We next turn to the variation in skewness of children’s income growth by the fathers’ lifetime income and wealth. Figure 14 shows that the distribution of income growth is right skewed regardless of fathers’ income and wealth. More importantly, we find that the distribution of income growth becomes increasingly more right skewed for both sons and daughters as we move from poorer to richer families.24 This finding suggests that children from more affluent families experience higher upside income potential, lower left-tail risk, or both. Differences between high- and low-resource fathers are substantial and economically significant.

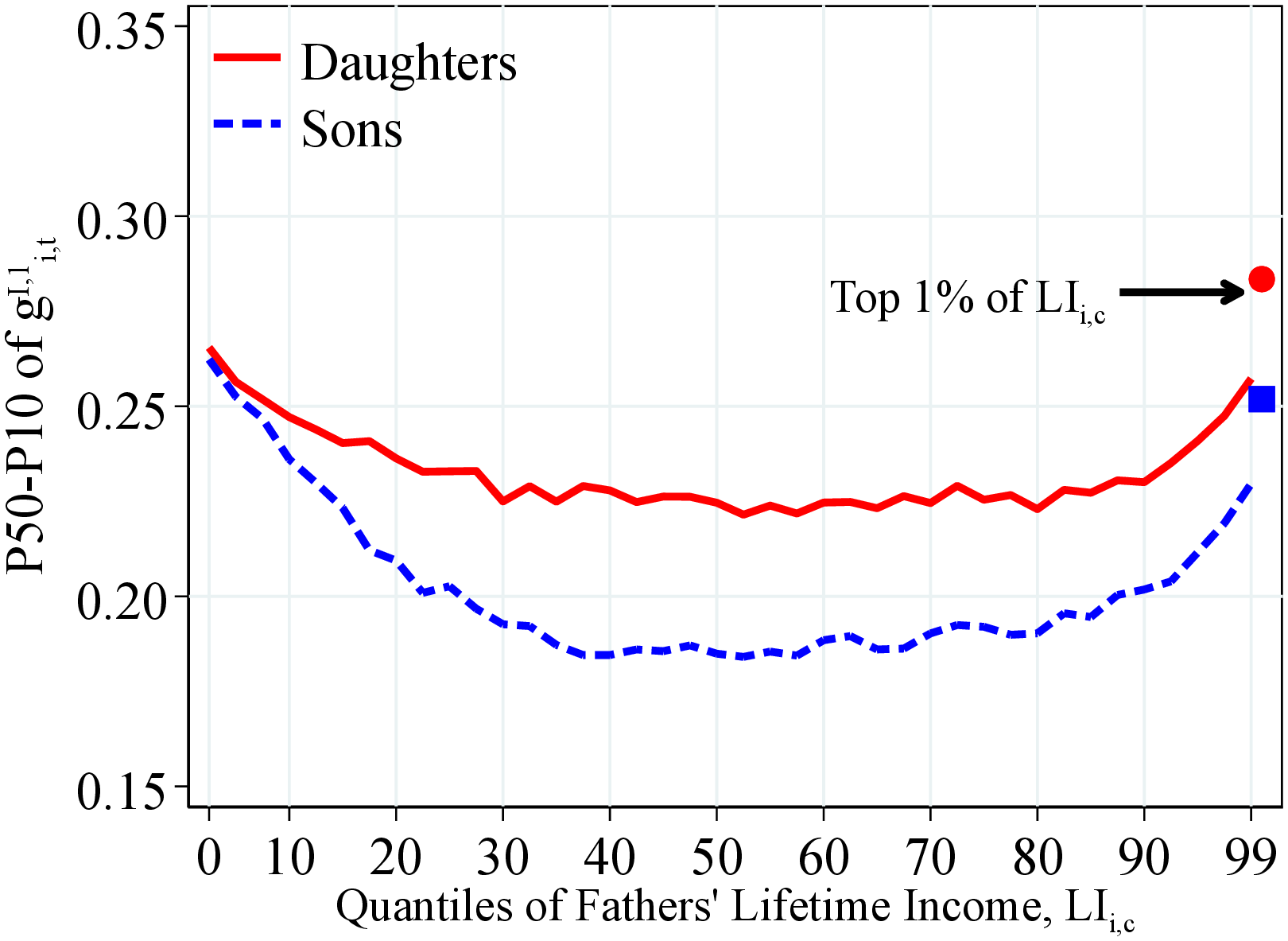

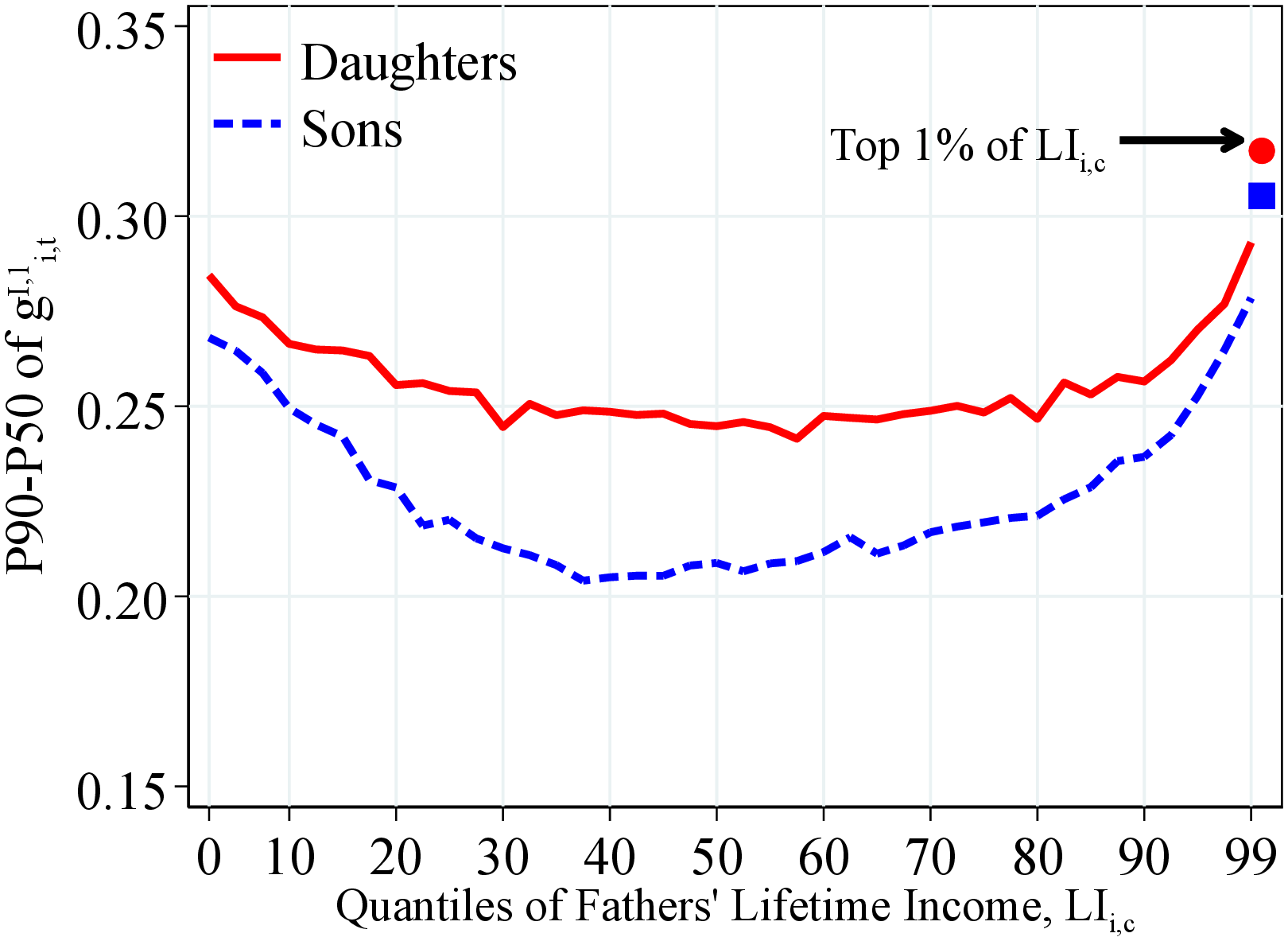

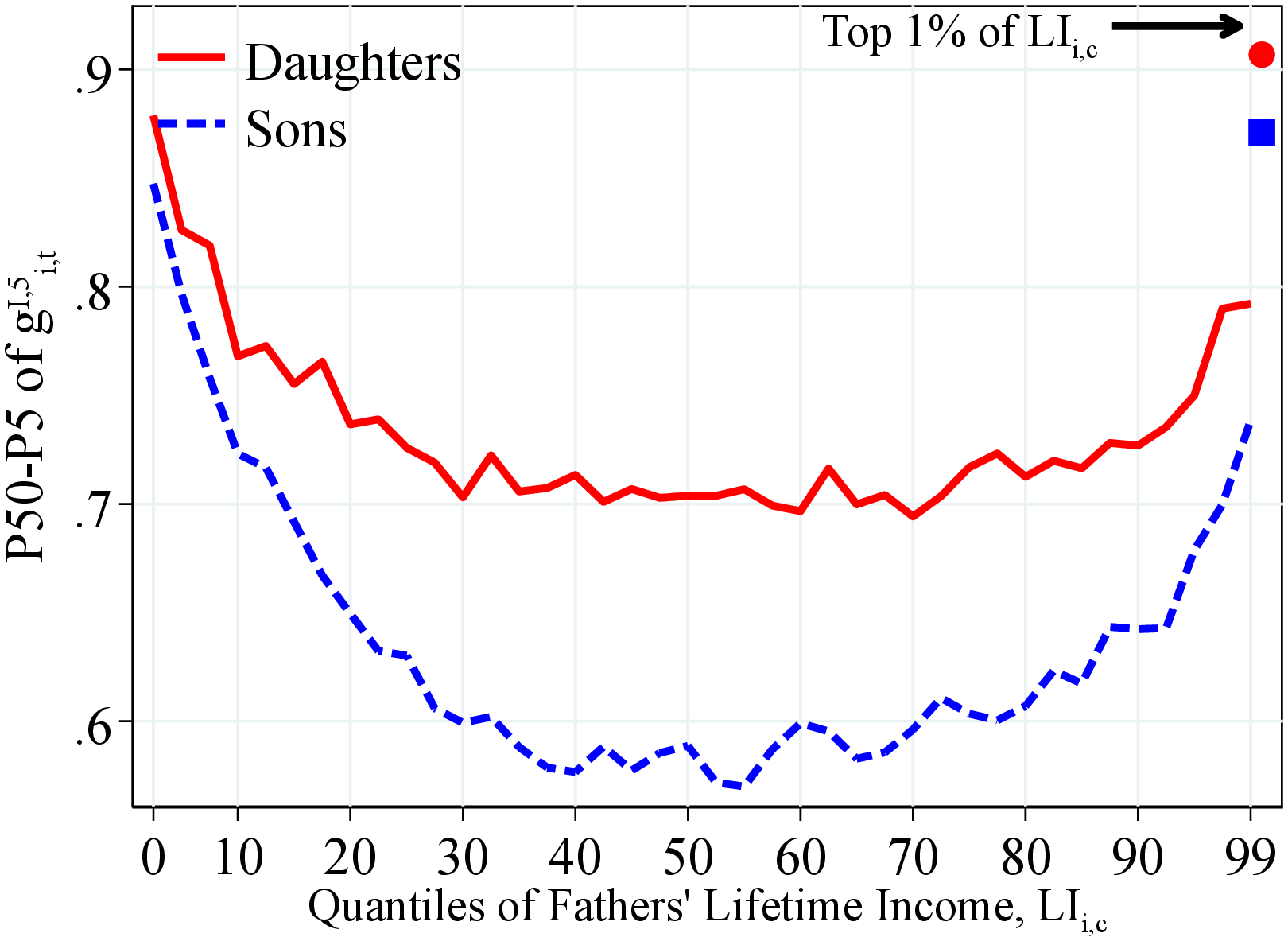

Notes: Figure 15 shows the P50-P10 and P90-P50 of the one-year residual earnings growth for men and women within quantiles of fathers’ lifetime income distribution in 40 quantiles. The top 2.5% of the distribution is further separated into two groups (97.5th to 99th and 99th percentile and above) for a total of 41 quantiles. We show the average across annual moments between 1990 and 2017. Markers show the average for children whose parents were at the top 1% of the corresponding distribution.

An important question is whether skewness becomes more positive over fathers’ resources because of a compression of the lower tail (less risk of large declines) or because of an expansion in the upper tail (more opportunities for large gains). To answer this question, we investigate how the left and right tails of the children’s income growth distribution change between poor and rich parents. In particular, Figures 15 and 16 show the P50-P10 and P90–P50 of children’s income growth. First, up to around the 85th percentile of the fathers’ income and wealth distributions, the decline in P90-P50 is relatively less pronounced than the compression of the lower tail as we move from poorer to richer parents. Therefore, the decline in income volatility in this range reflects somewhat more of a reduction in the left-tail risk of workers. However, beyond the 85th percentile, we see that both tails open up sharply, the upper tail even more so, thereby resulting in both an increase in volatility and an increase in positive skewness.

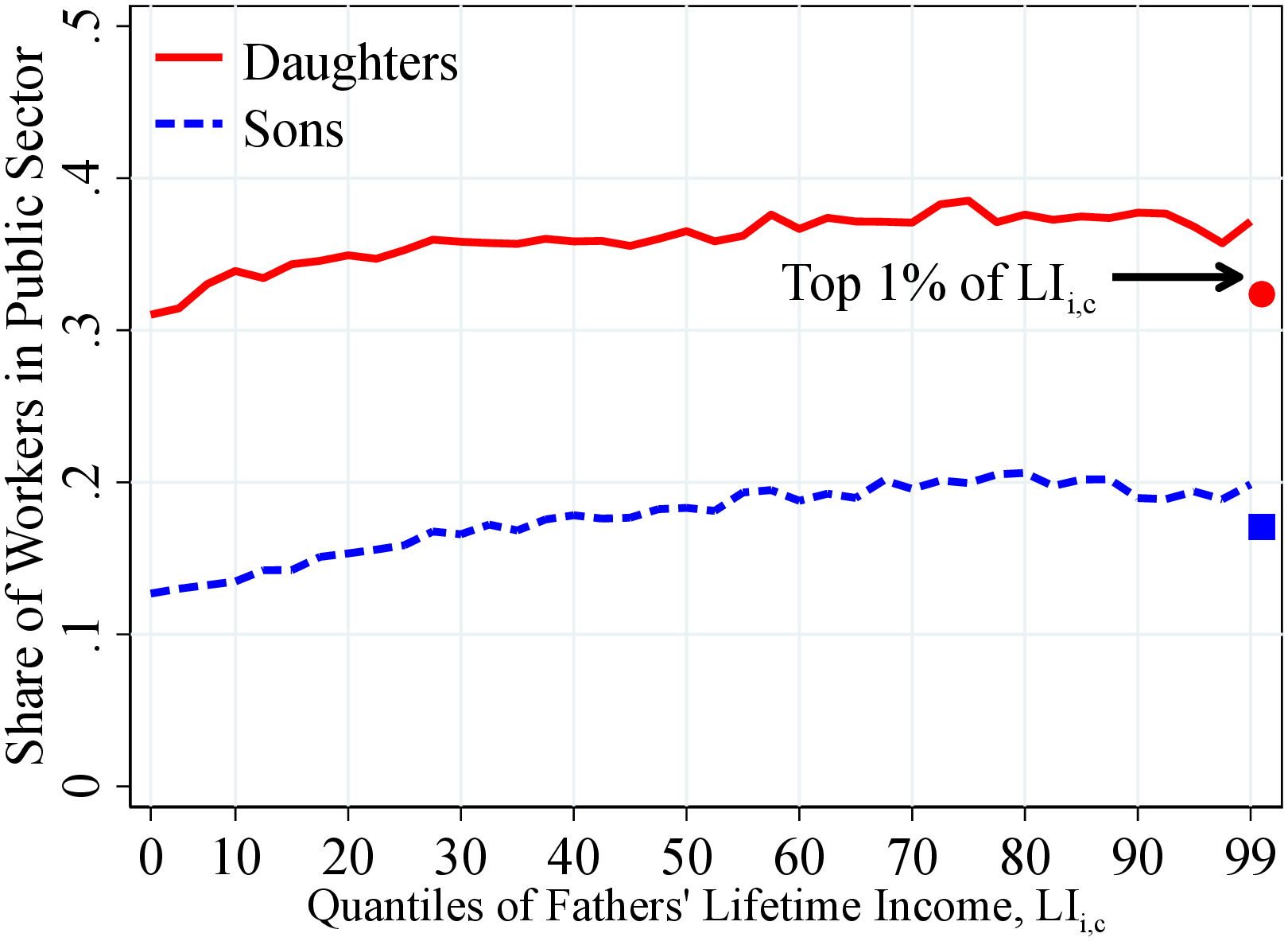

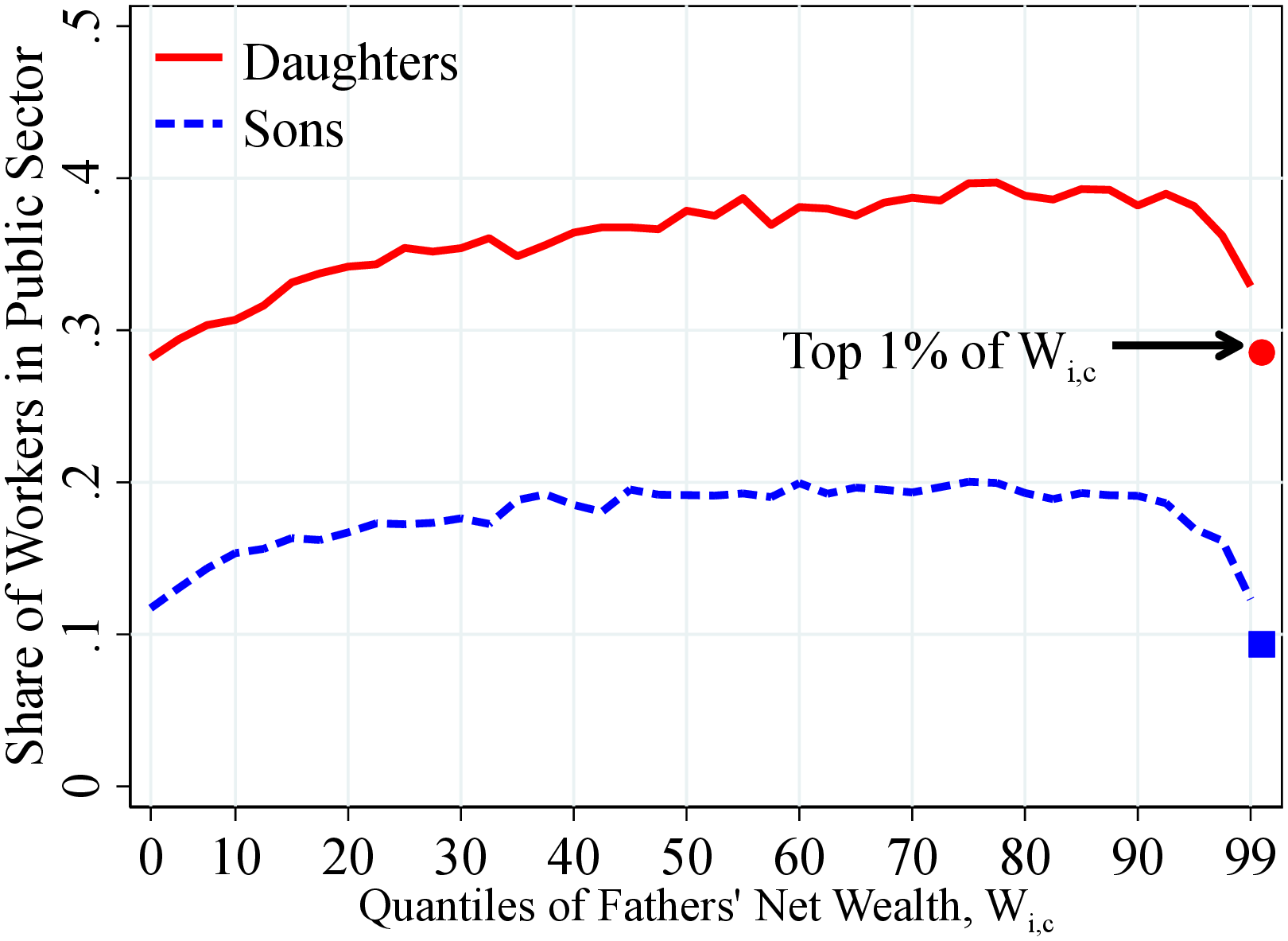

These findings are consistent with our conjecture that children from affluent families pursue high-risk high-return careers. Additional evidence from the data supports this conjecture as well. For example, we find that fraction of sons (daughters) employed in the public sector (i.e., in more stable, less risky jobs) increases from around 10% (30%) to 20% (40%) from families at the bottom of the distribution to upper-middle-class families, but then declines sharply at the top of the distribution (see Figure OA.III.8).

(a) Left-Tail Dispersion of \(g_{it}^{I,1}\)

(a) Left-Tail Dispersion of \(g_{it}^{I,1}\)  (b) Right-Tail Dispersion of \(g_{it}^{I,1}\)

(b) Right-Tail Dispersion of \(g_{it}^{I,1}\)

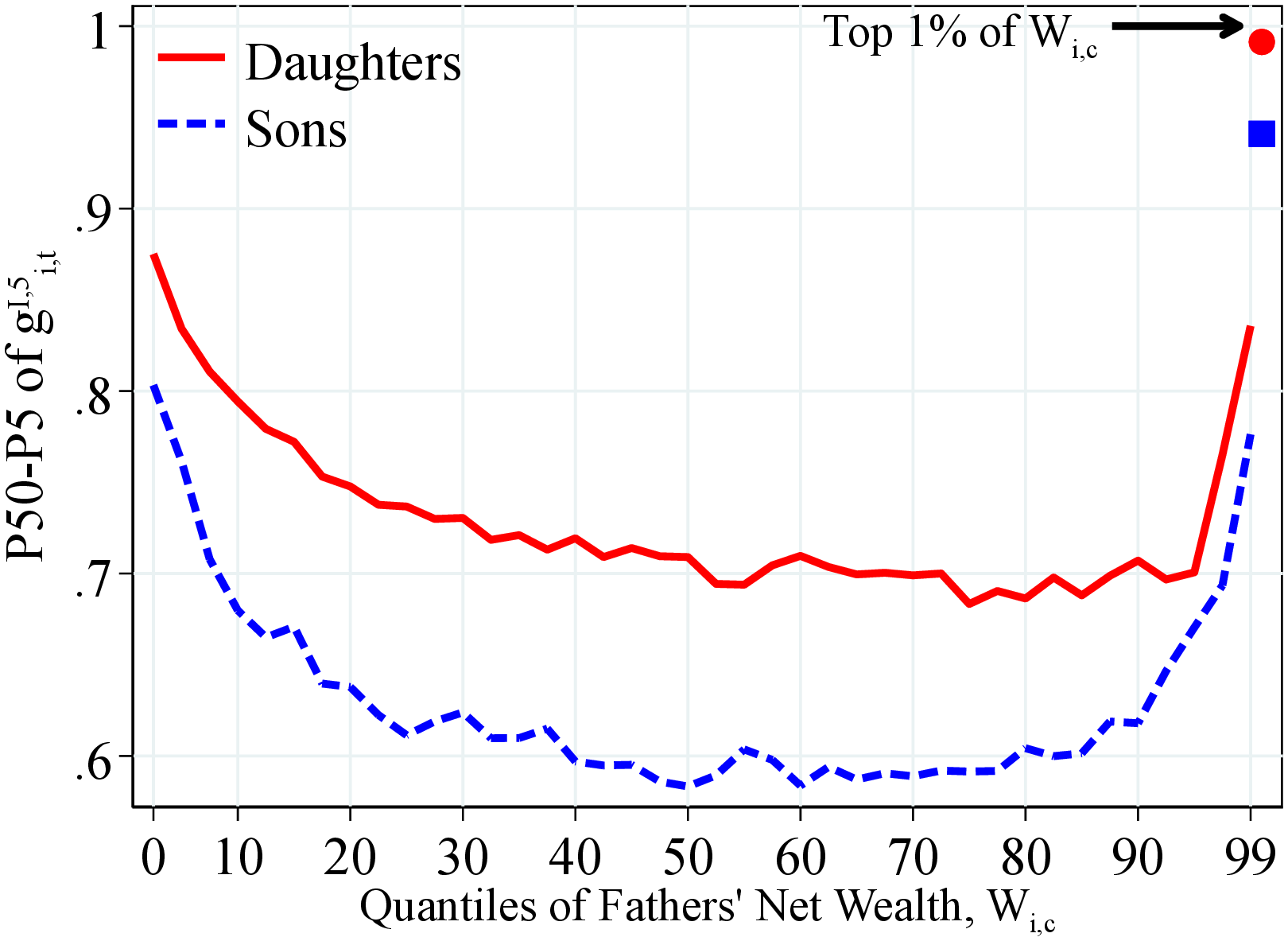

Figure: Figure 16 – Left- and Right-Tail Income Volatility by Fathers’ Wealth

Notes: Figure 16 shows the P90-P50 and P50-P10 of one-year residual earnings growth for men and women within quantiles of fathers’ household net wealth distribution in 40 quantiles. The top 2.5% of the distribution is further separated into two groups (97.5th to 99th and 99th percentile and above) for a total of 41 quantiles. We show the average across annual moments between 1990 and 2017. Markers show the average for children whose parents were at the top 1% of the corresponding distribution.

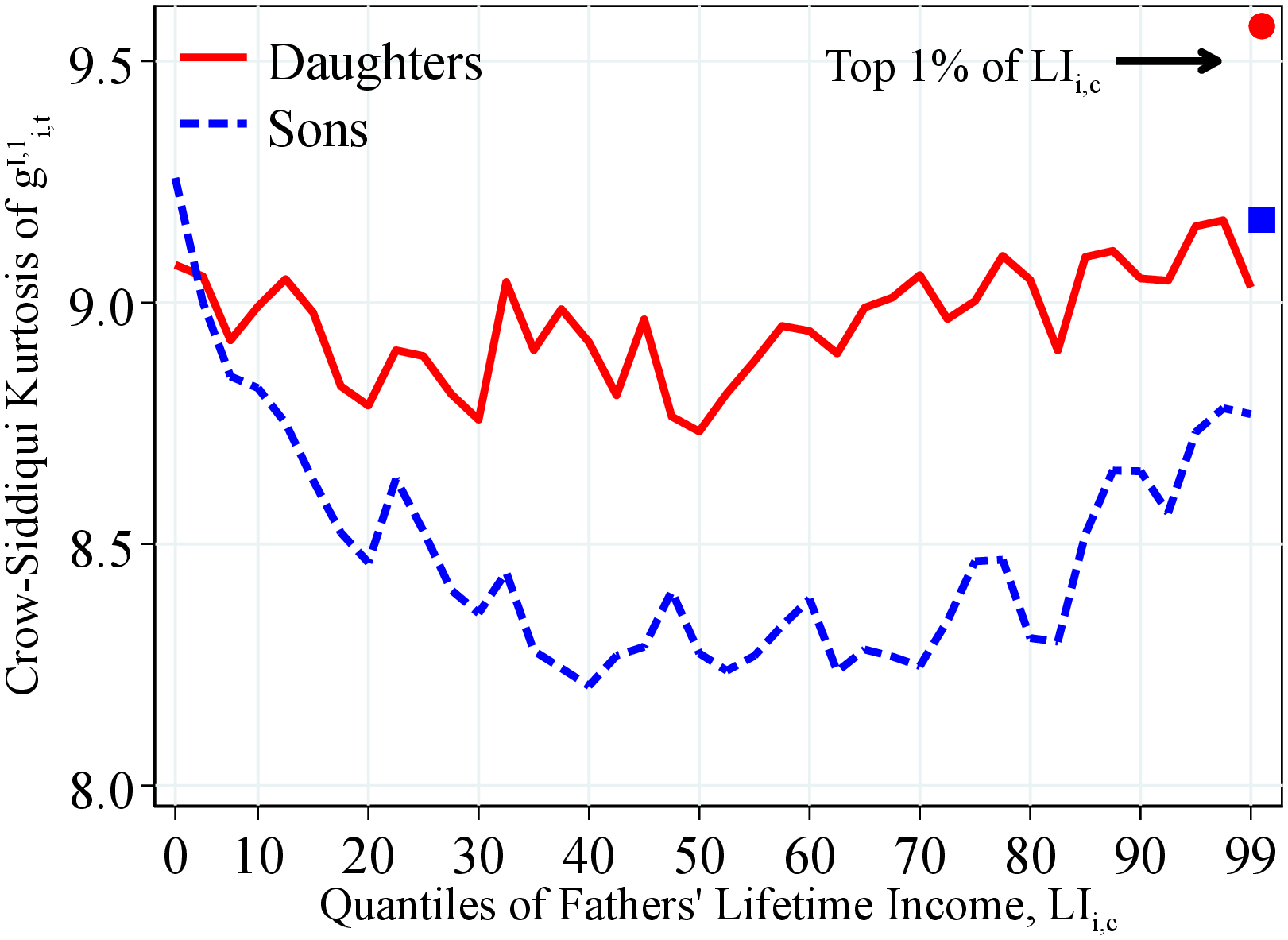

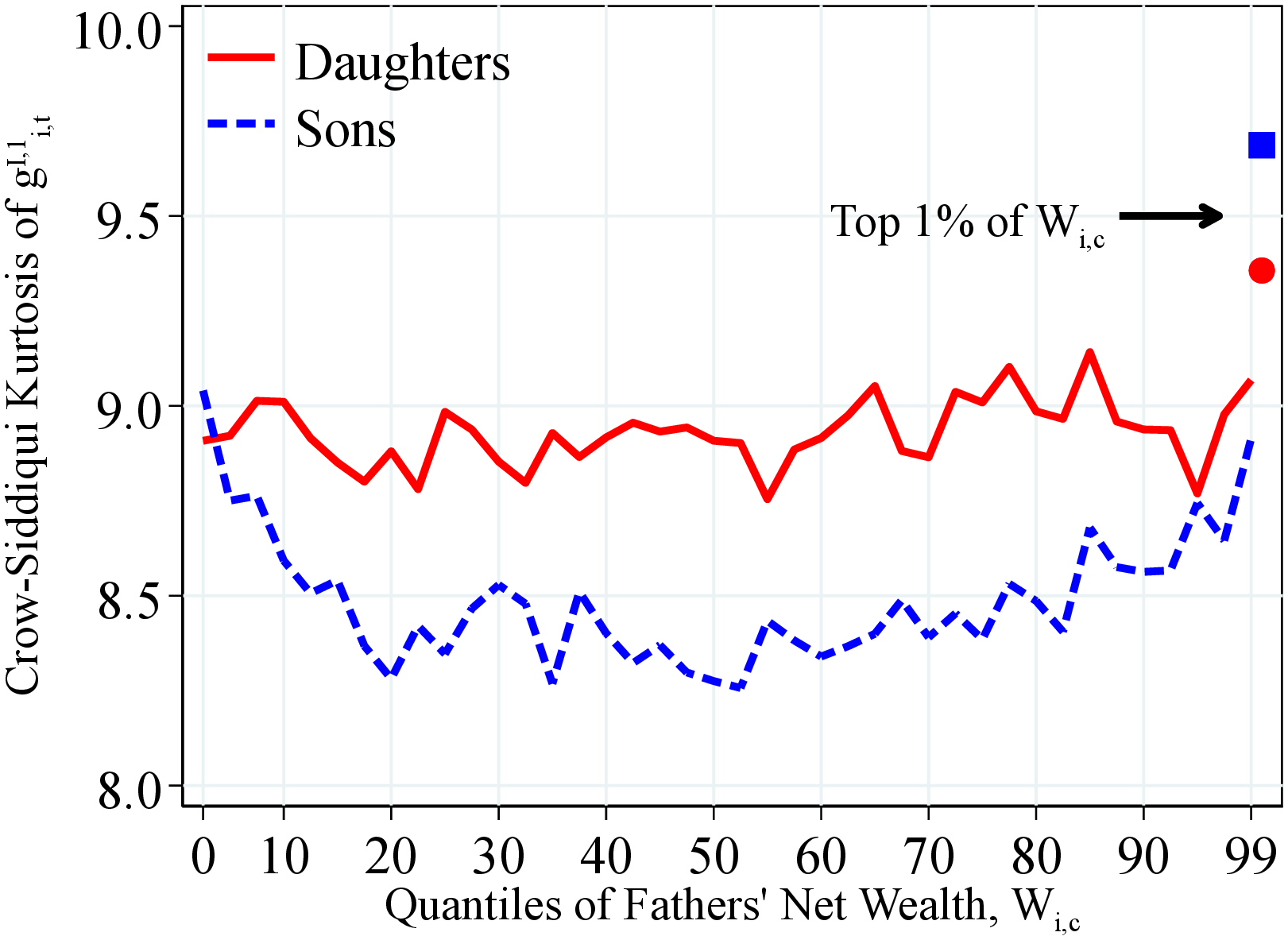

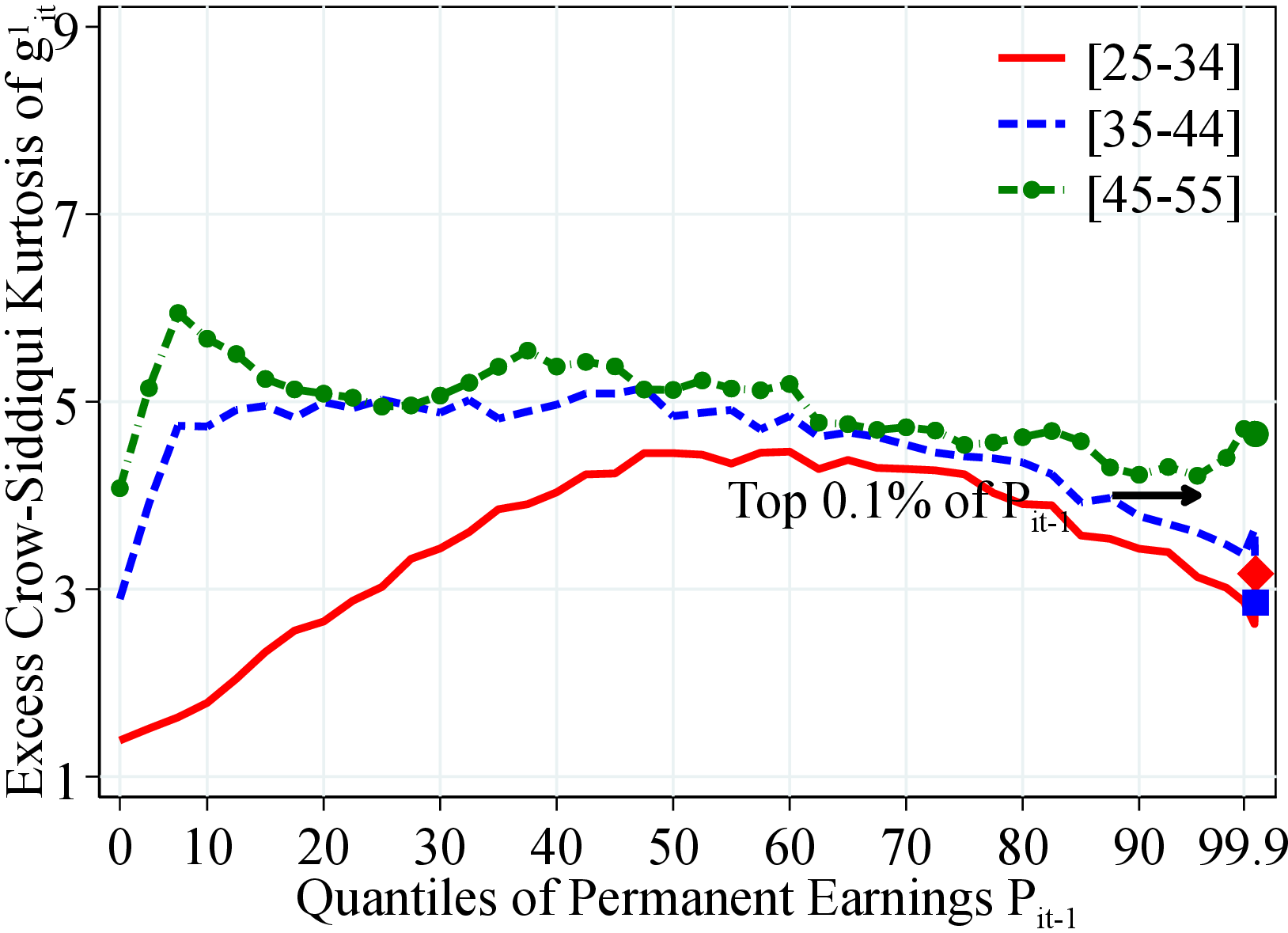

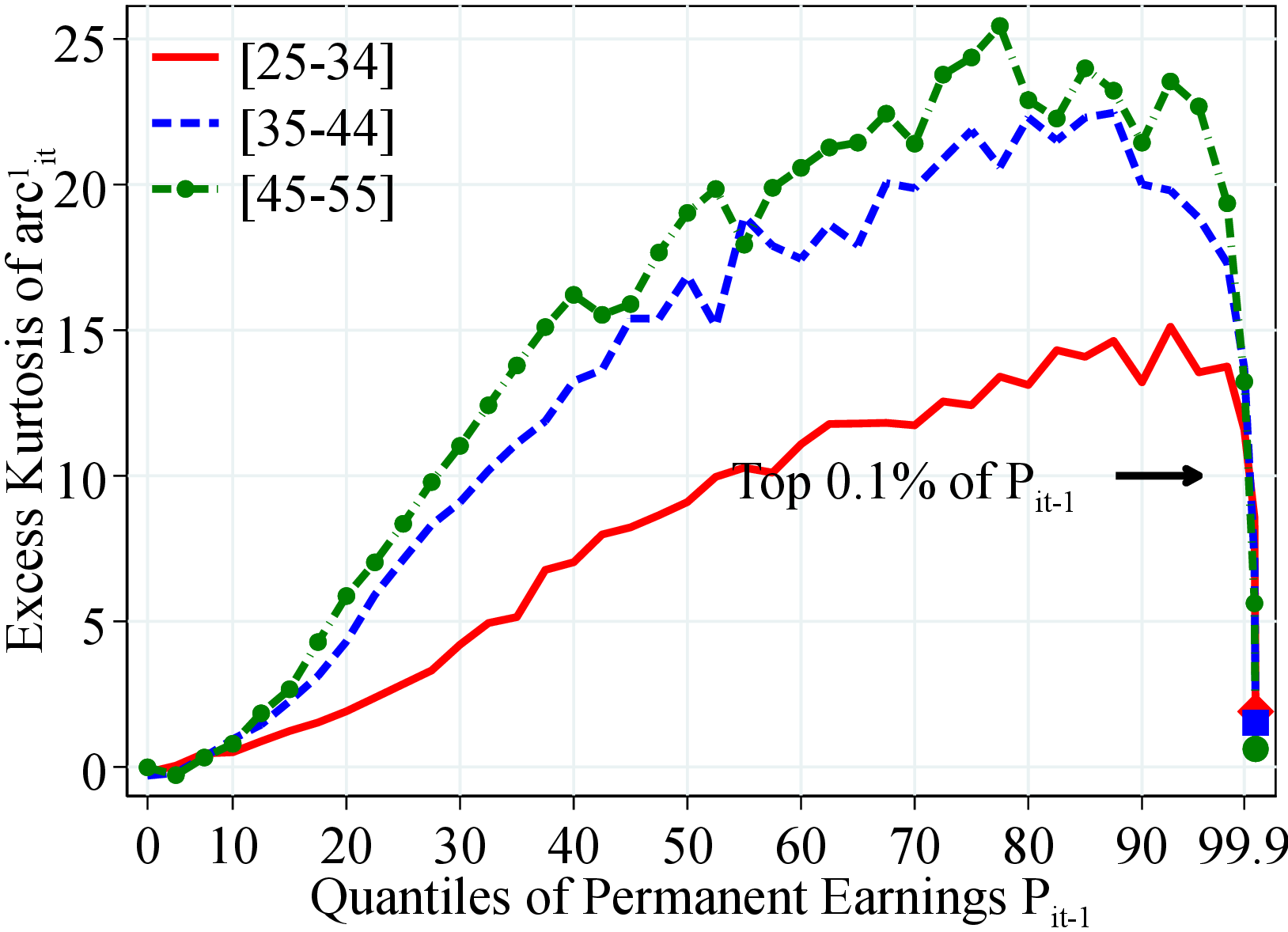

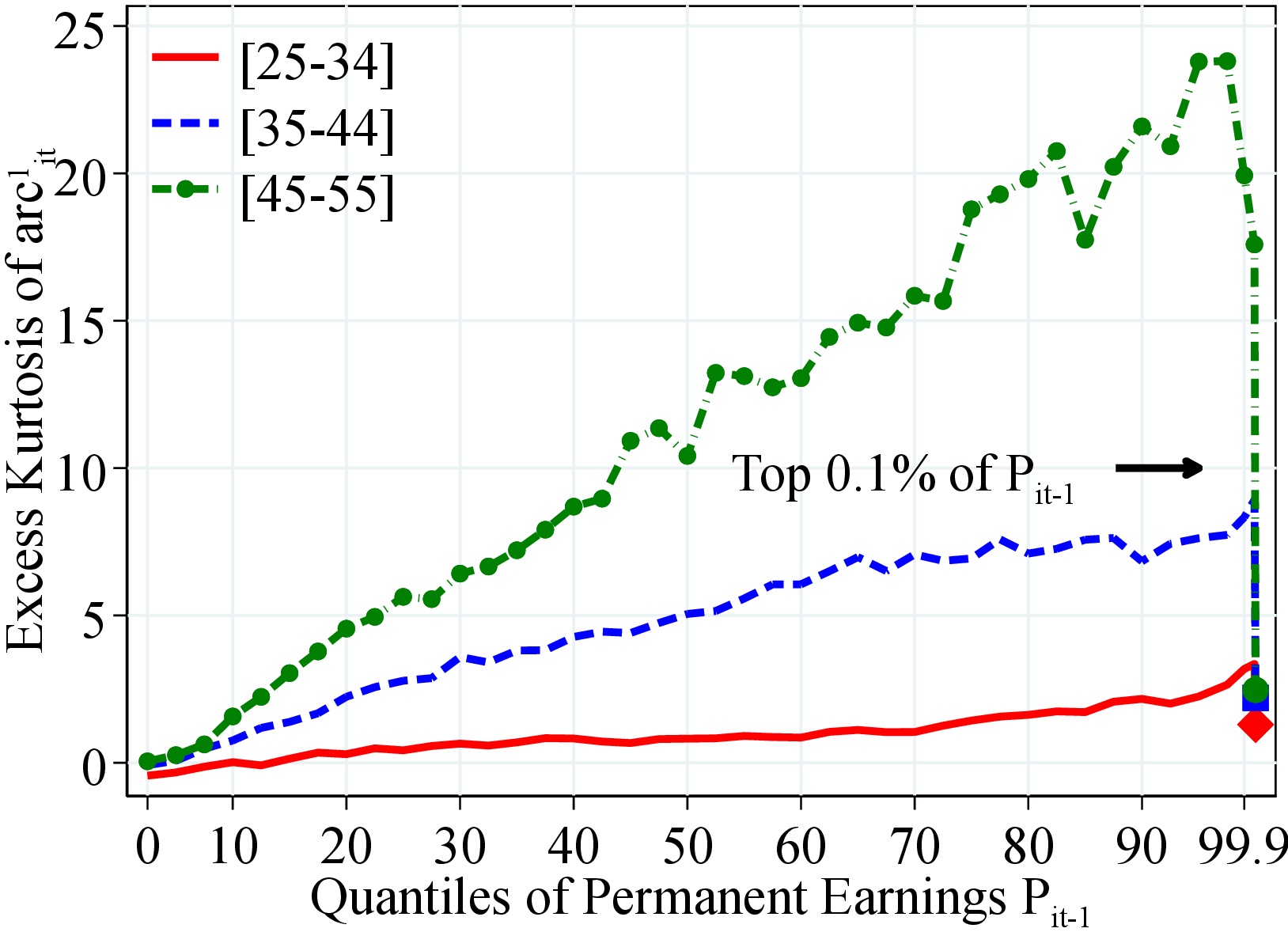

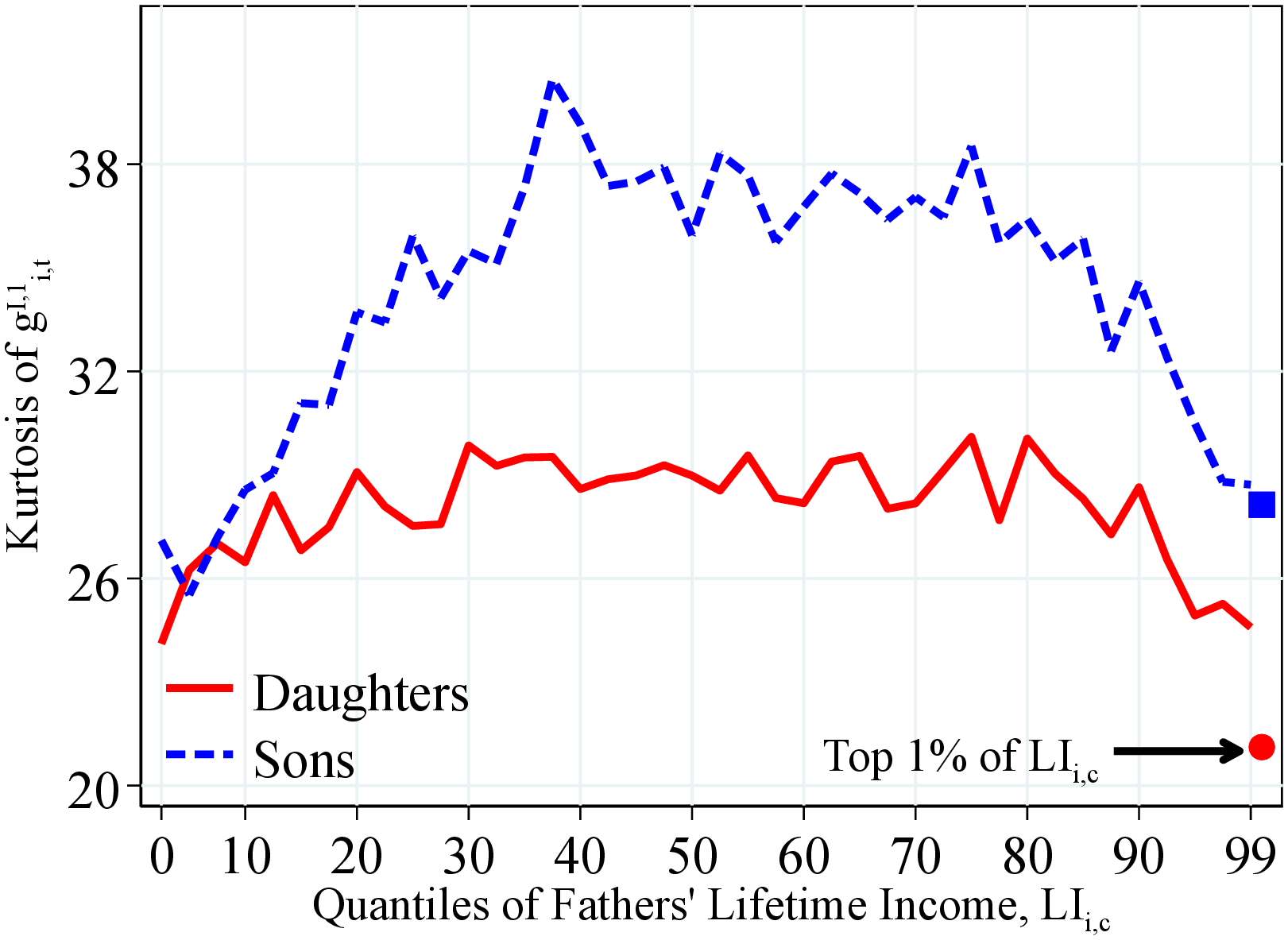

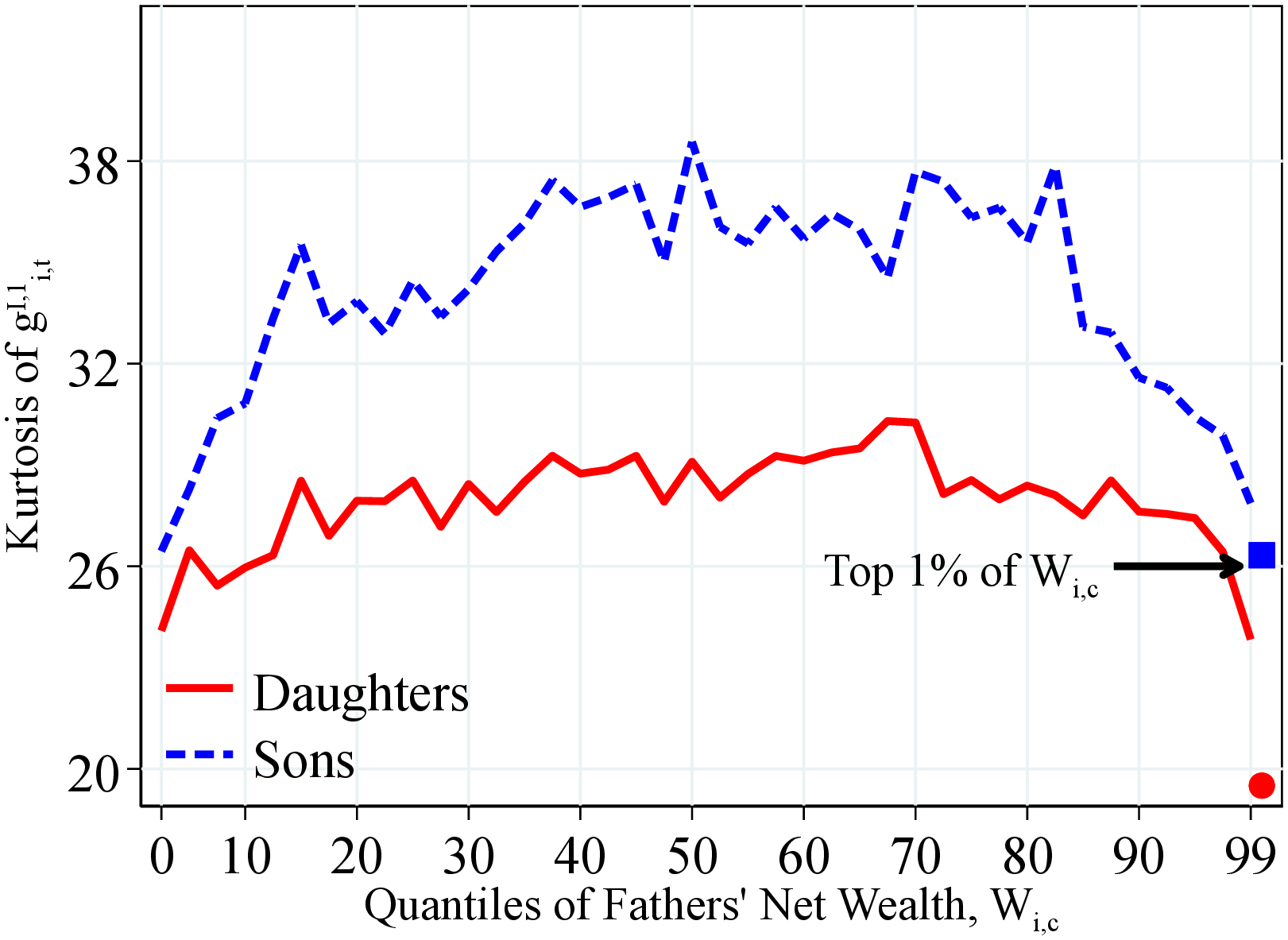

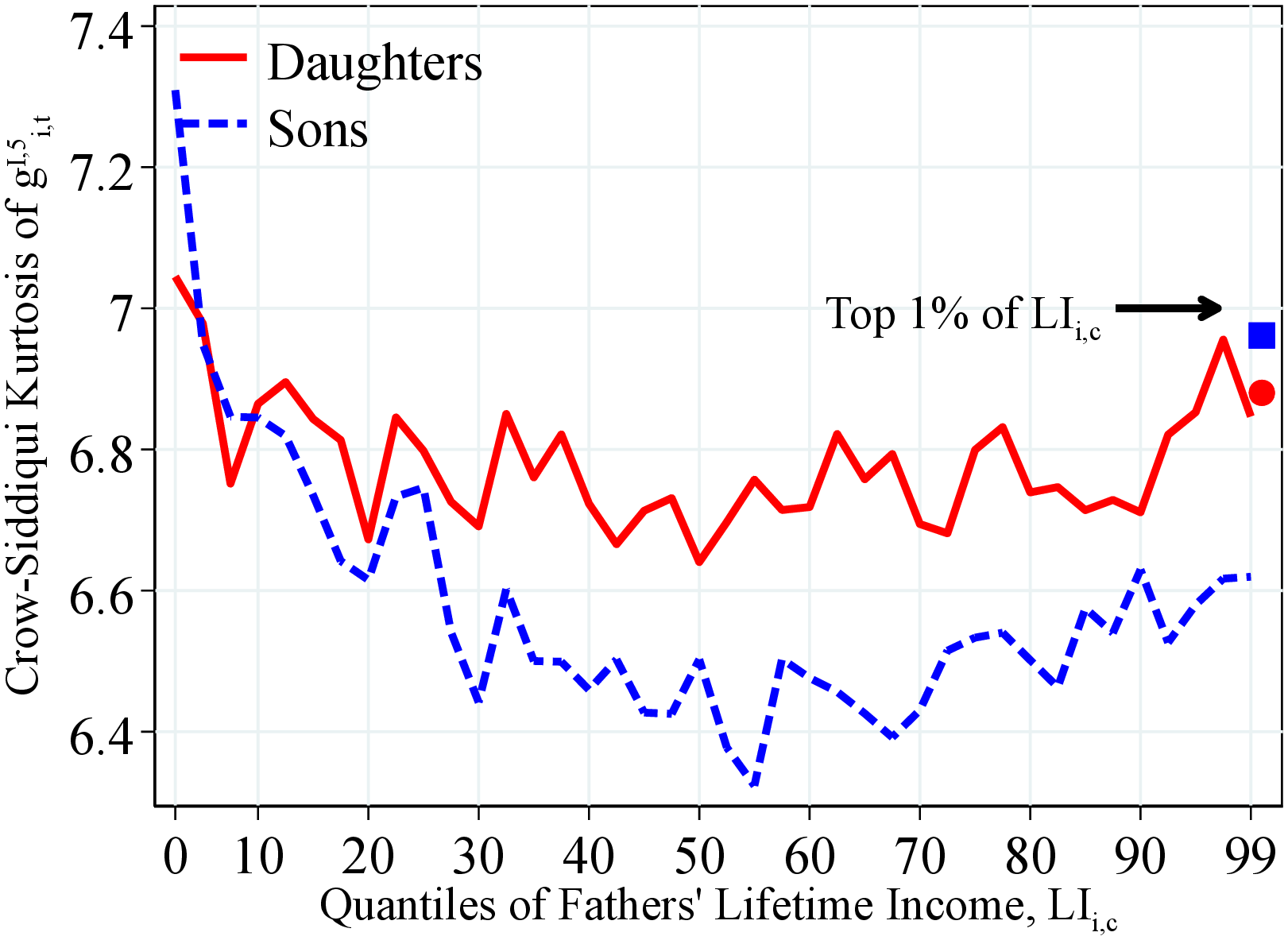

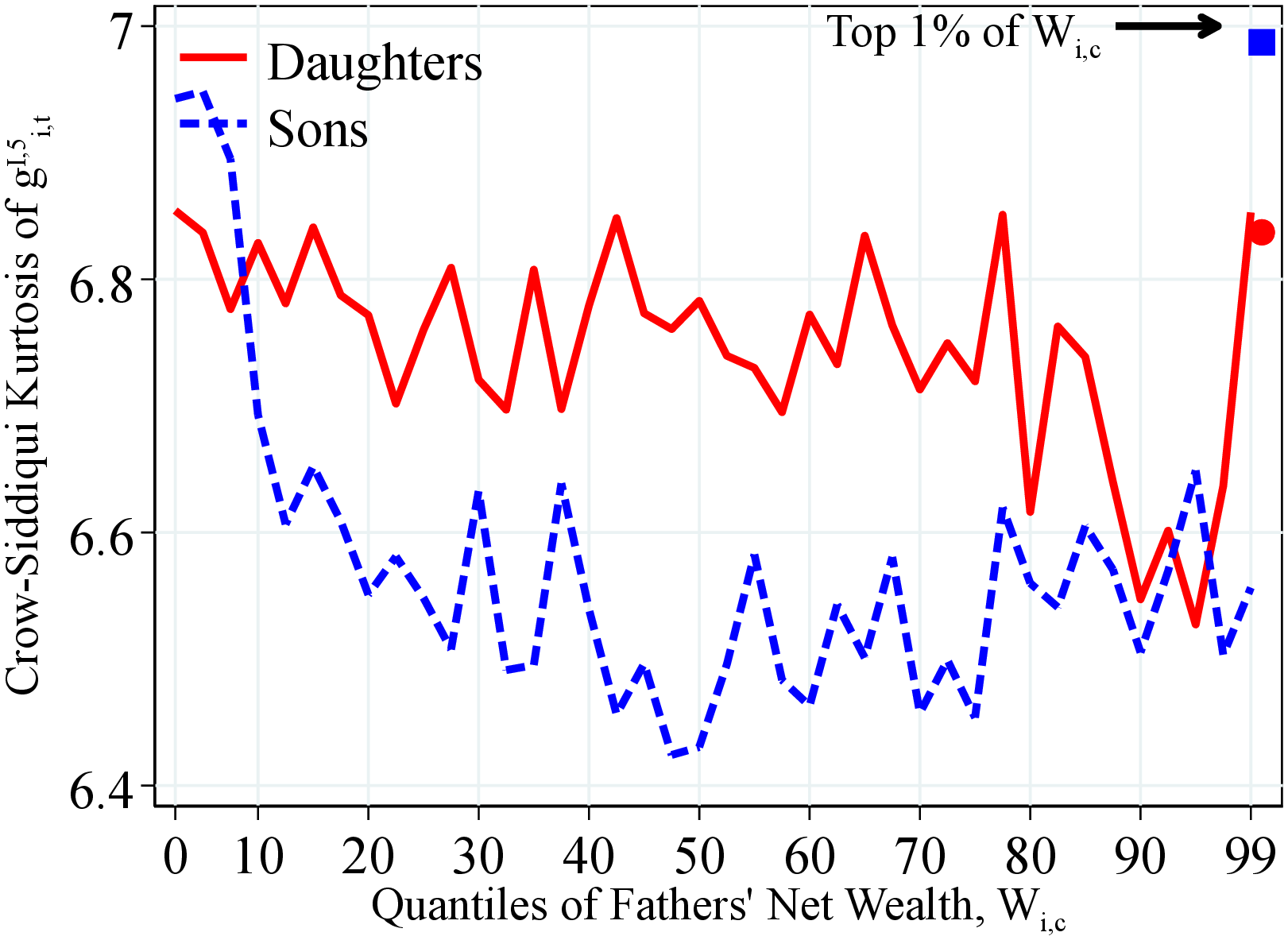

Kurtosis of Income Growth. Finally, Figure 17 shows the Crow-Siddiqui kurtosis of income growth conditional on fathers’ lifetime income and wealth. We find a U-shaped profile with low kurtosis of earnings growth among sons whose fathers are around the median lifetime income relative to those whose fathers were at the top or bottom of the lifetime income distribution. For daughters, we do not find any significant pattern. Children of the richest fathers face the most leptokurtic distribution of income changes. However, these results change significantly if we use the fourth standardized moment (Figure OA.III.7), which shows a hump-shaped profile with low kurtosis of earnings growth among children with bottom- and top-earning fathers relative to those from middle-income families. This result shows the importance of very large earnings changes in measurement of the higher-order moments.

(a) By Father’s Lifetime Income

(a) By Father’s Lifetime Income (b) By Father’s Net Wealth

(b) By Father’s Net Wealth

Figure: Figure 17 – Kurtosis of Log Income Growth by Fathers’ Resources

Notes: Figure 17 shows the excess Crow-Siddiqui kurtosis of the one-year residual earnings growth for men and women within quantiles of fathers’ lifetime income distribution (Panel A) and fathers’ household net wealth distribution (Panel B) in 40 quantiles. The top 2.5% of the distribution is further separated in two groups (97.5th to 99th and 99th percentile and above) for a total of 41 quantiles. We show the average across annual moments between 1990 and 2017. Markers show the average for children whose parents were at the top 1% of the corresponding distribution.

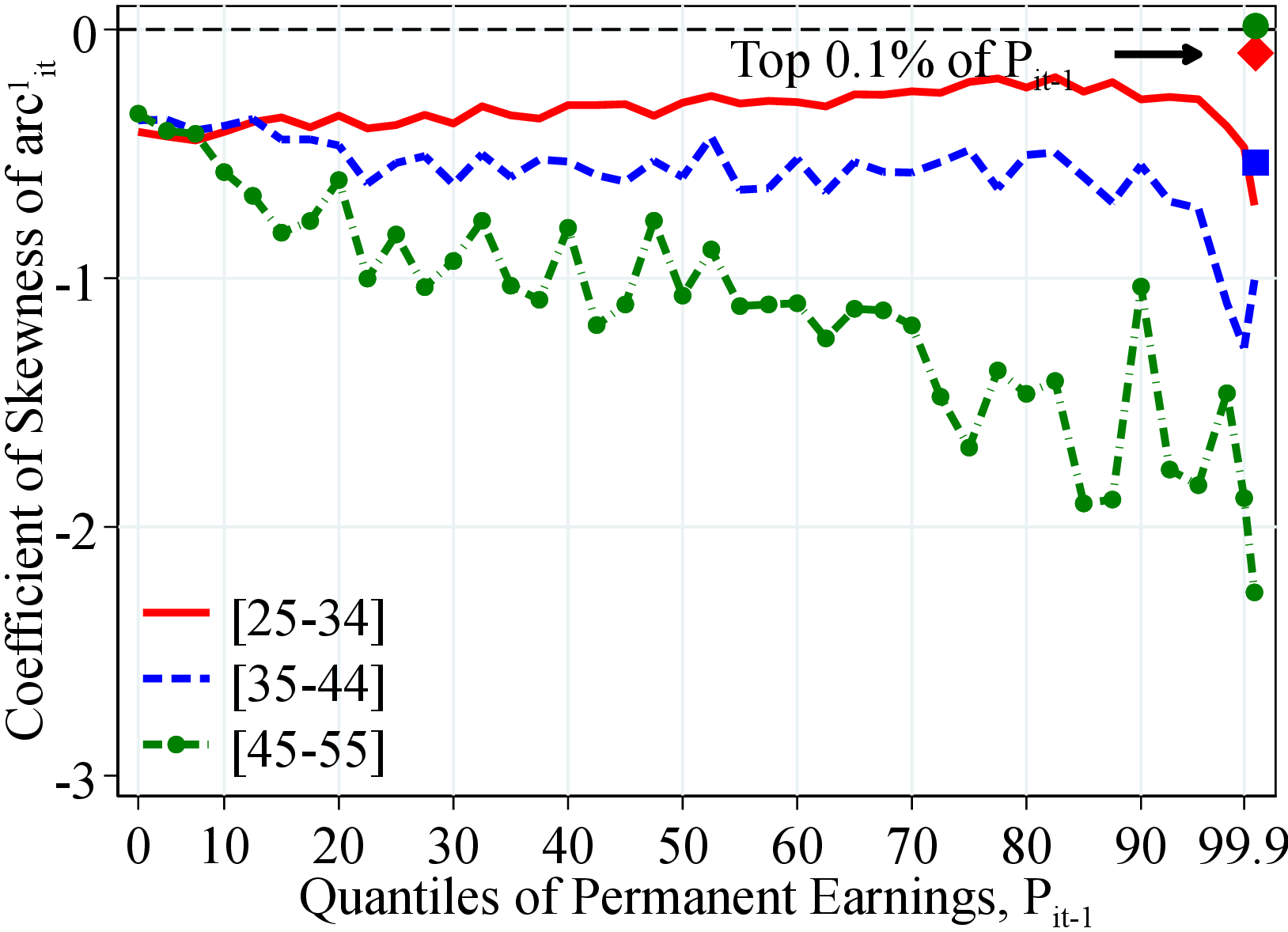

4.3 Fathers’ and Children’s Income Dynamics

Do fathers and children have income dynamics of similar properties (for example, because of similar risk attitudes or similar jobs and occupations)? To investigate this question, we again use a permanent income measure, \(\tilde{P}_{it}=\max \left \{Y_{t}^{min},\frac{1}{3}\sum _{j=0}^{2}Y_{it-j}\right \}\), the average income between periods \(t\) and \(t-2\) winsorized at the minimum income threshold (\(Y_{t}^{min}\)).25 Then, for each individual, we construct a time series of log permanent income growth (\(\Delta \tilde{P}_{it}=\log \tilde{P}_{it}-\log \tilde{P}_{it-1}\)) over their life cycle and compute the first three moments from this series. Given the relatively short length of the individual time series—between 20 and 40 years—we use percentile-based moments (the median, P90-P10, and Kelley skewness) to avoid having outliers drive our results. The results for the standardized moments display similar qualitative patterns (Appendix C.4).

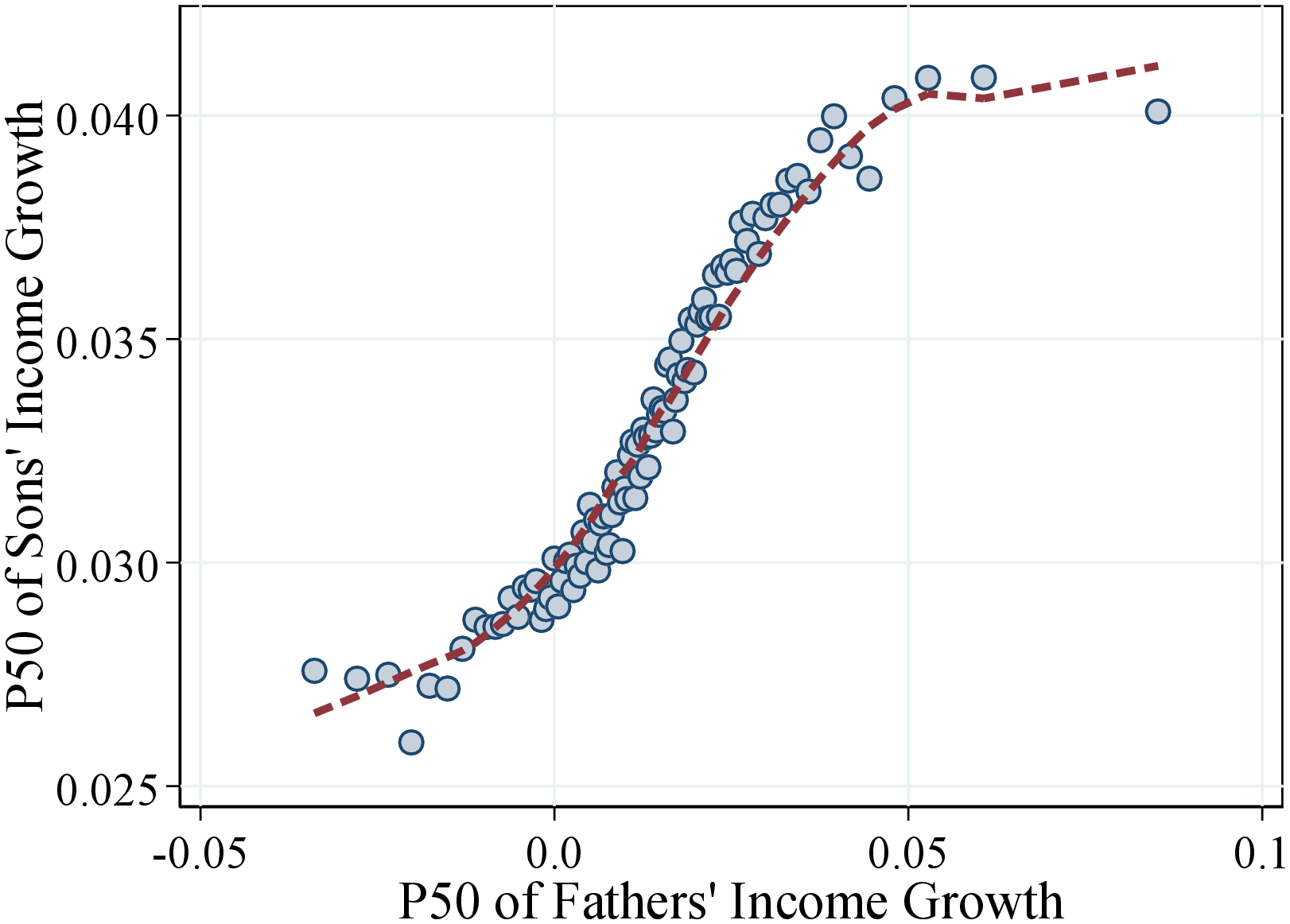

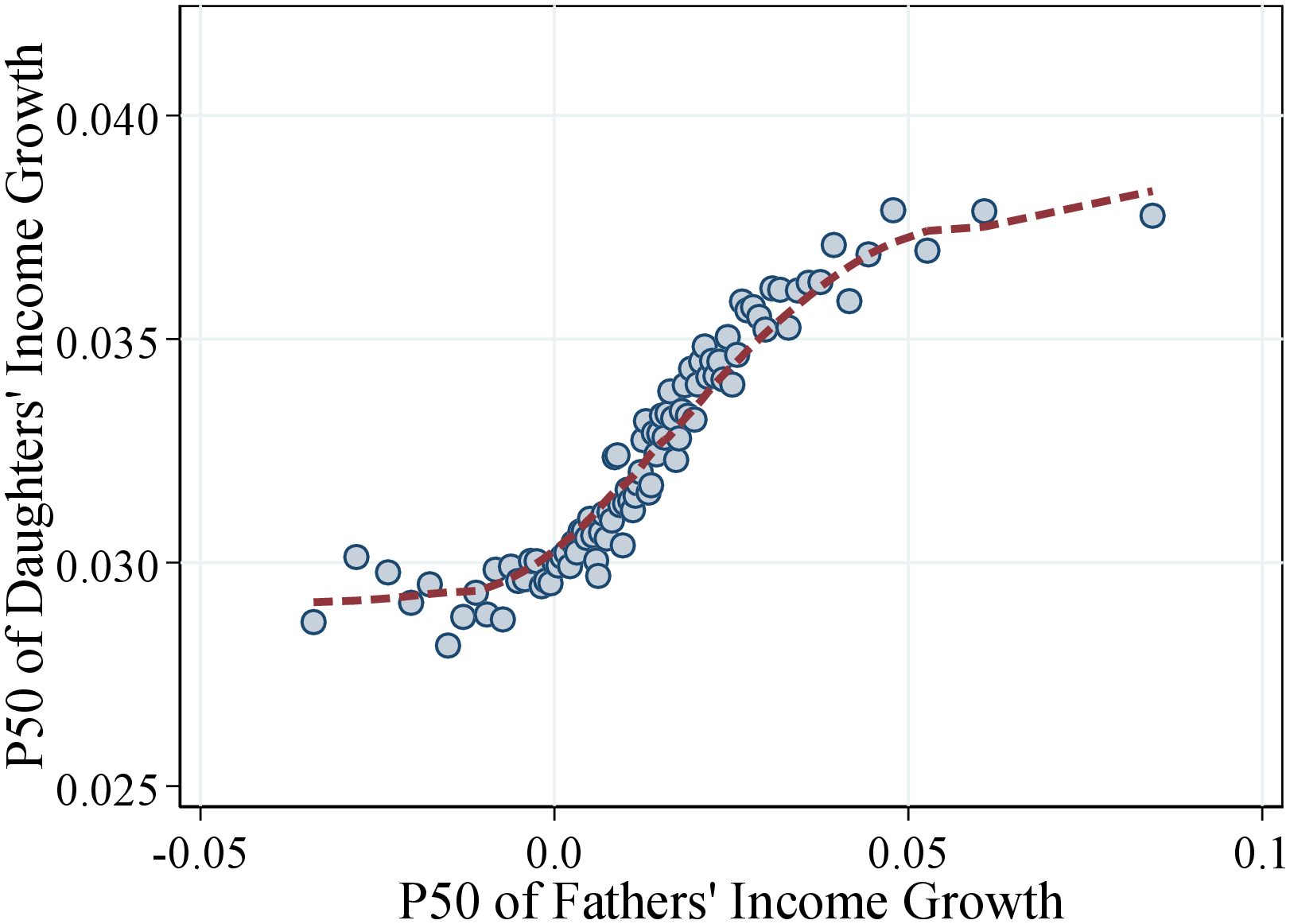

Median Income Growth. Figure 18 shows a binned scatter plot of the median log permanent income growth of fathers and sons (left panel) and fathers and daughters (right panel). We find a marked non-linear relation between fathers’ and children’s lifetime income growth. Fathers’ and children’s income growth does not seem to be strongly correlated for around 10%-15% of our sample when fathers have negative or very steep life-cycle income growth. In the rest of the sample, however, the children of fathers that experienced steeper income growth during their lifetime are more likely to experience high income growth. This correlation is also economically significant: An increase in a father’s median income growth from 0 to 5 log points results in an increase of roughly 1 log point in the son’s median income growth over the life cycle. For daughters, this number is slightly lower (around 0.8 log points) but still significant. The overall intergenerational elasticity of life-cycle income growth is 0.14 for men and 0.09 for women.26

(a) Sons

(a) Sons  (b) Daughters

(b) Daughters

Figure: Figure 18 – Median Income Growth of Fathers and Children

Notes: The scatter plot is based on a sample of 494,514 father-son pairs (left plot) and 471,229 father-daughter pairs (right plot). Each sample is divided into 100 bins. The dashed lines are calculated using a lowess smoothing regression.

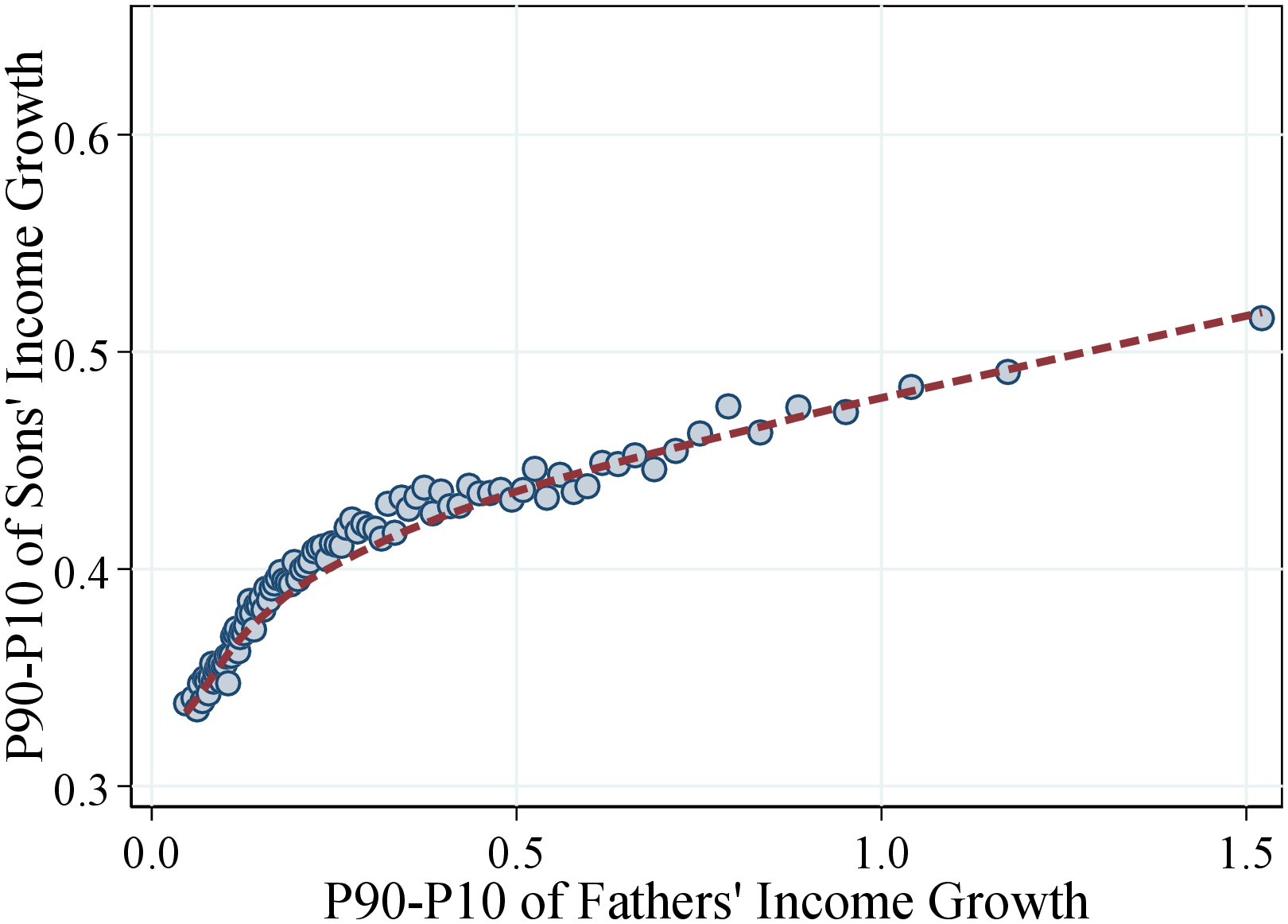

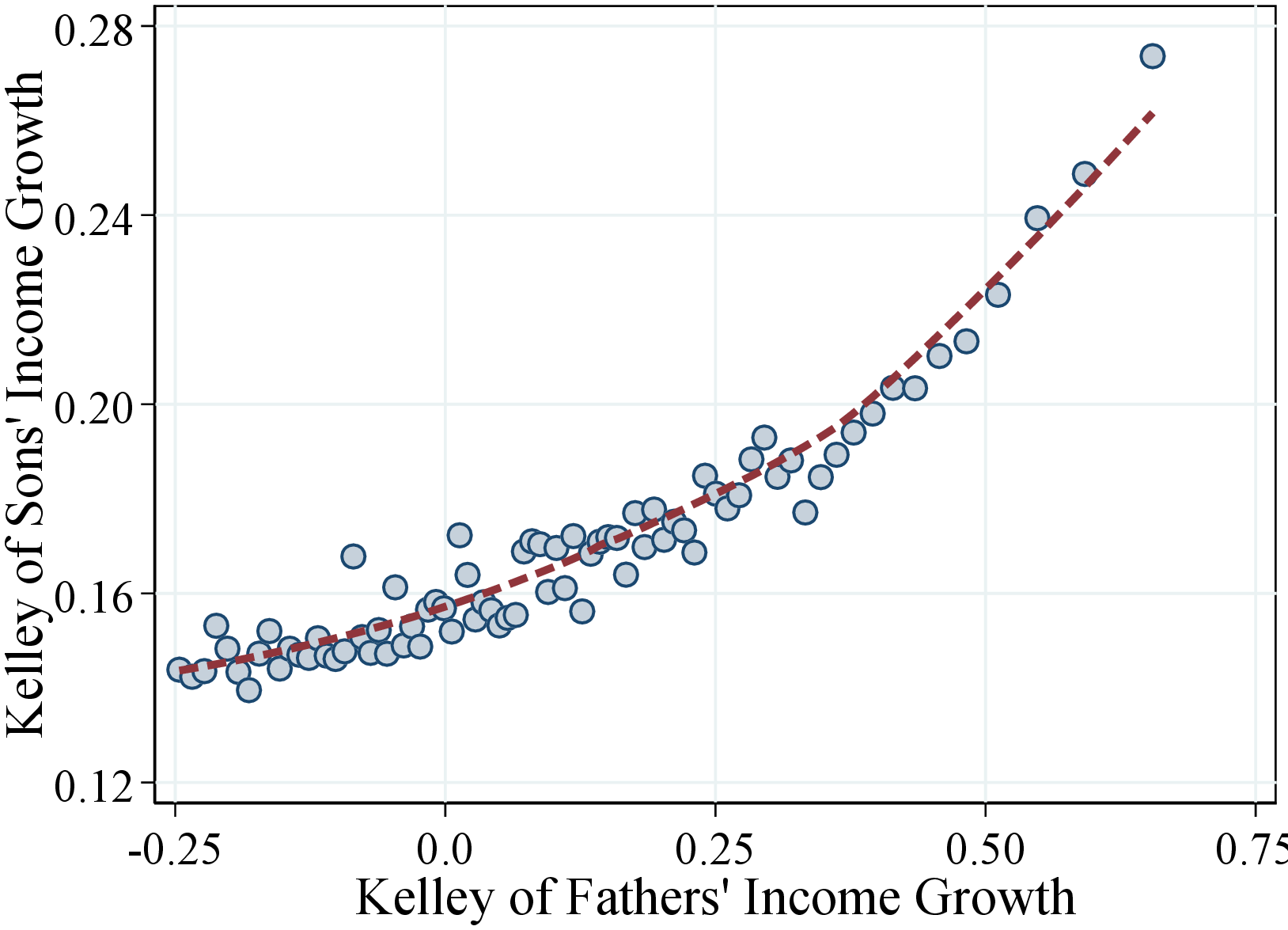

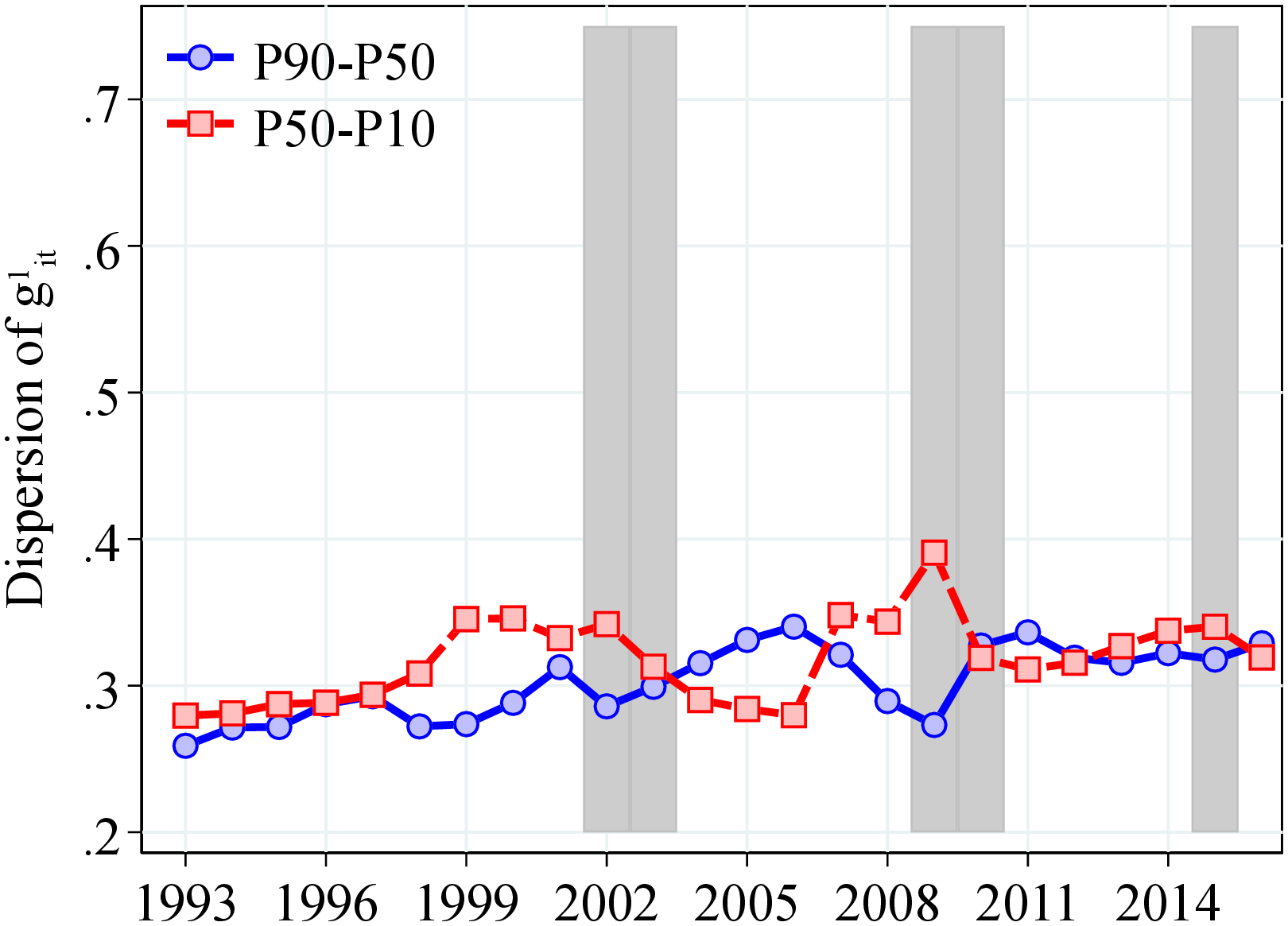

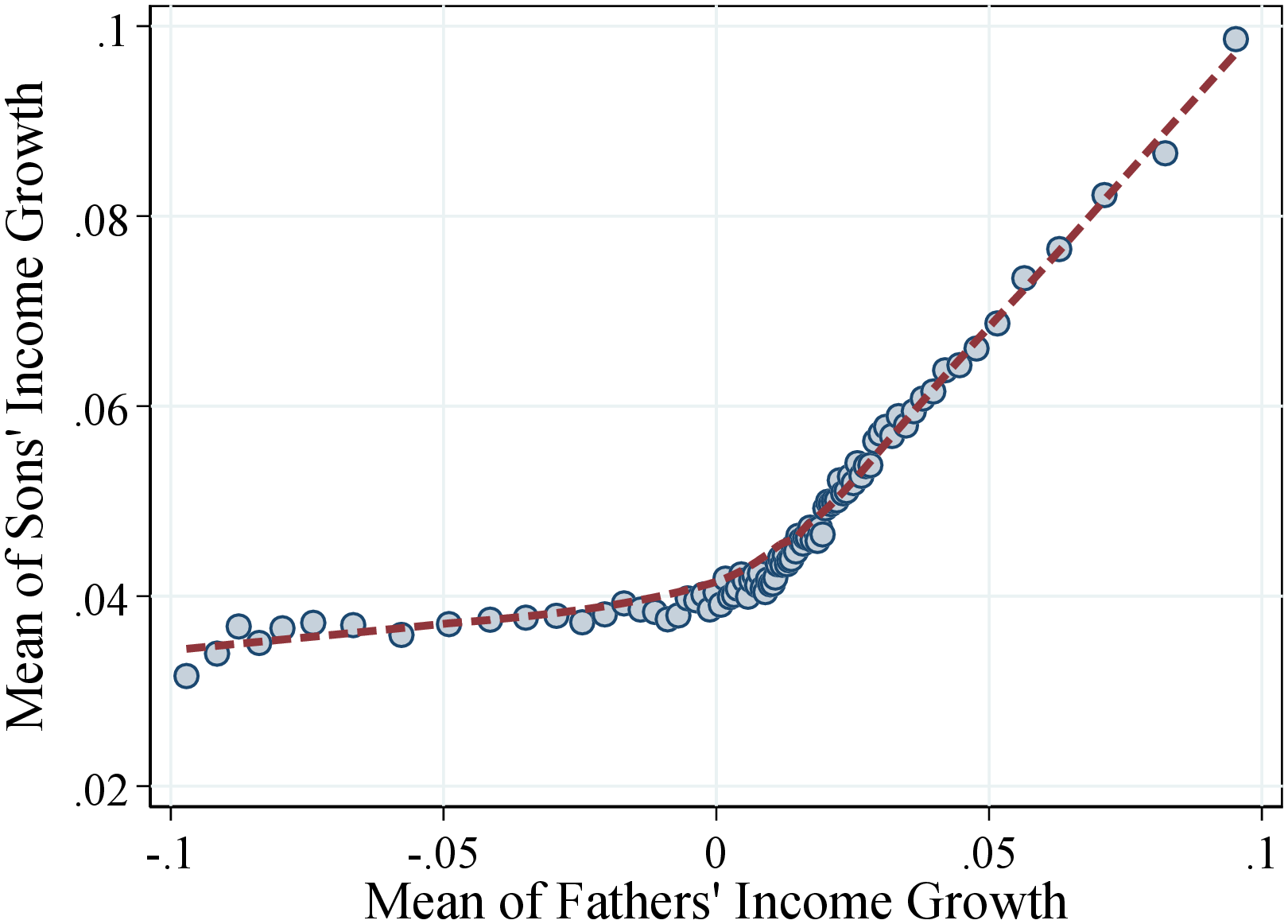

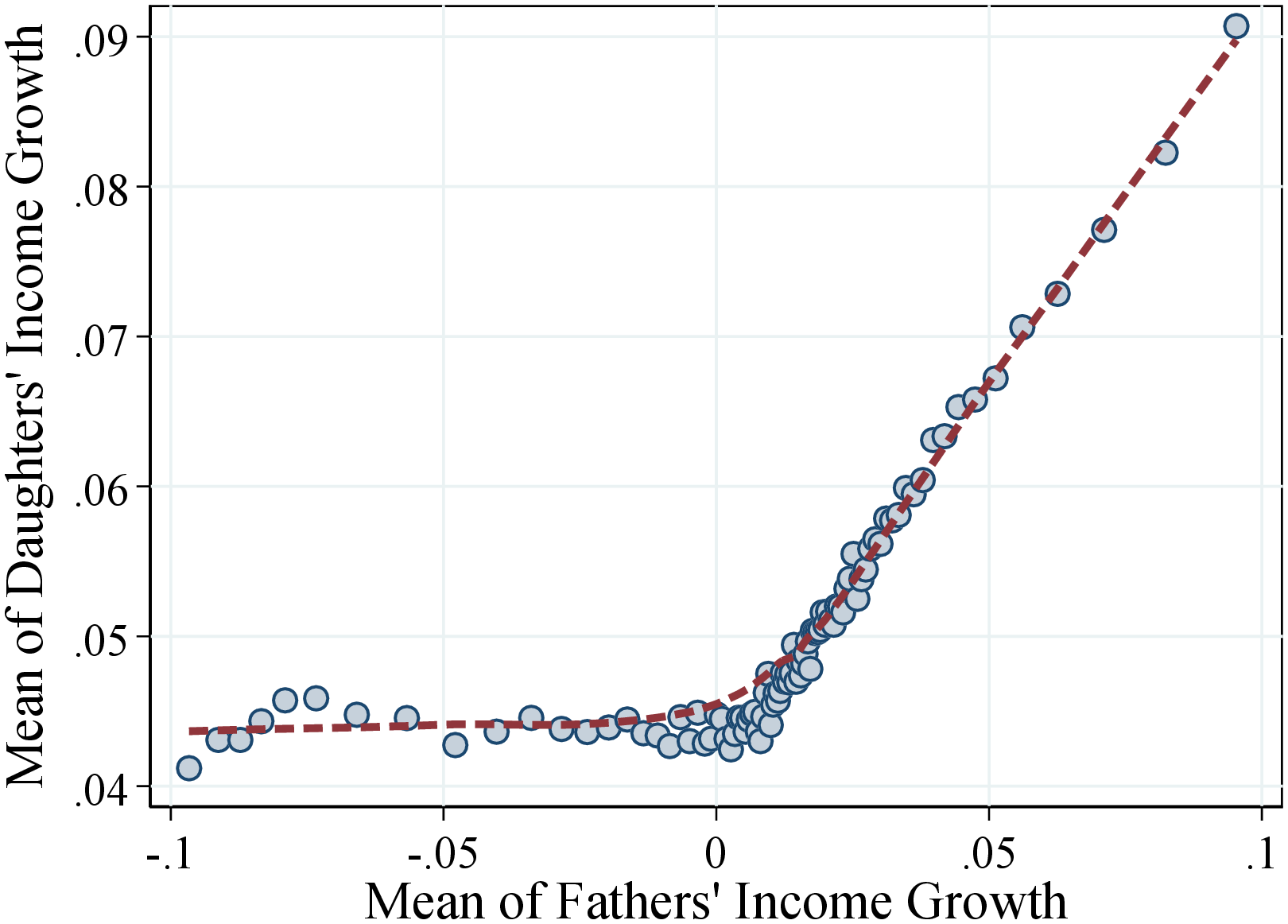

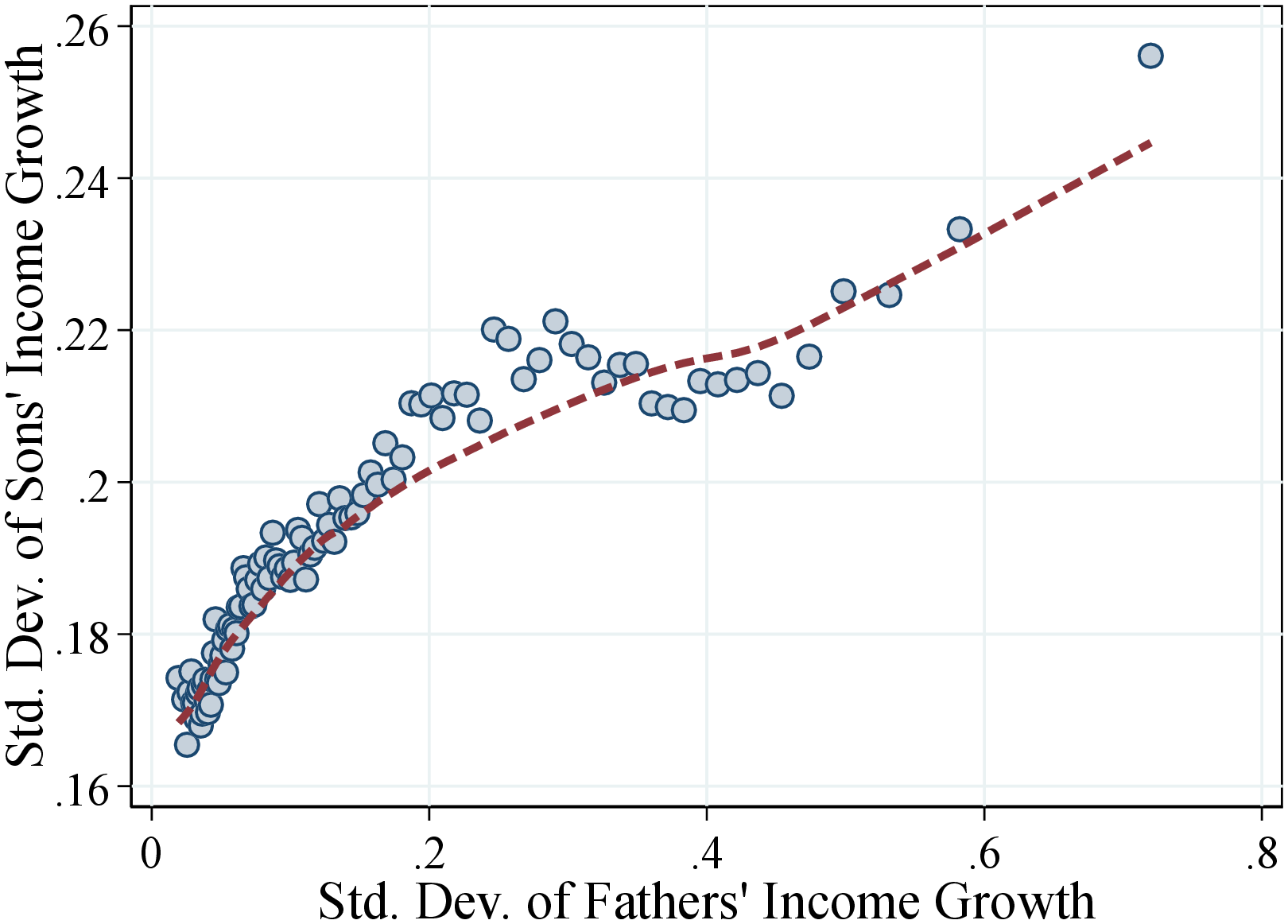

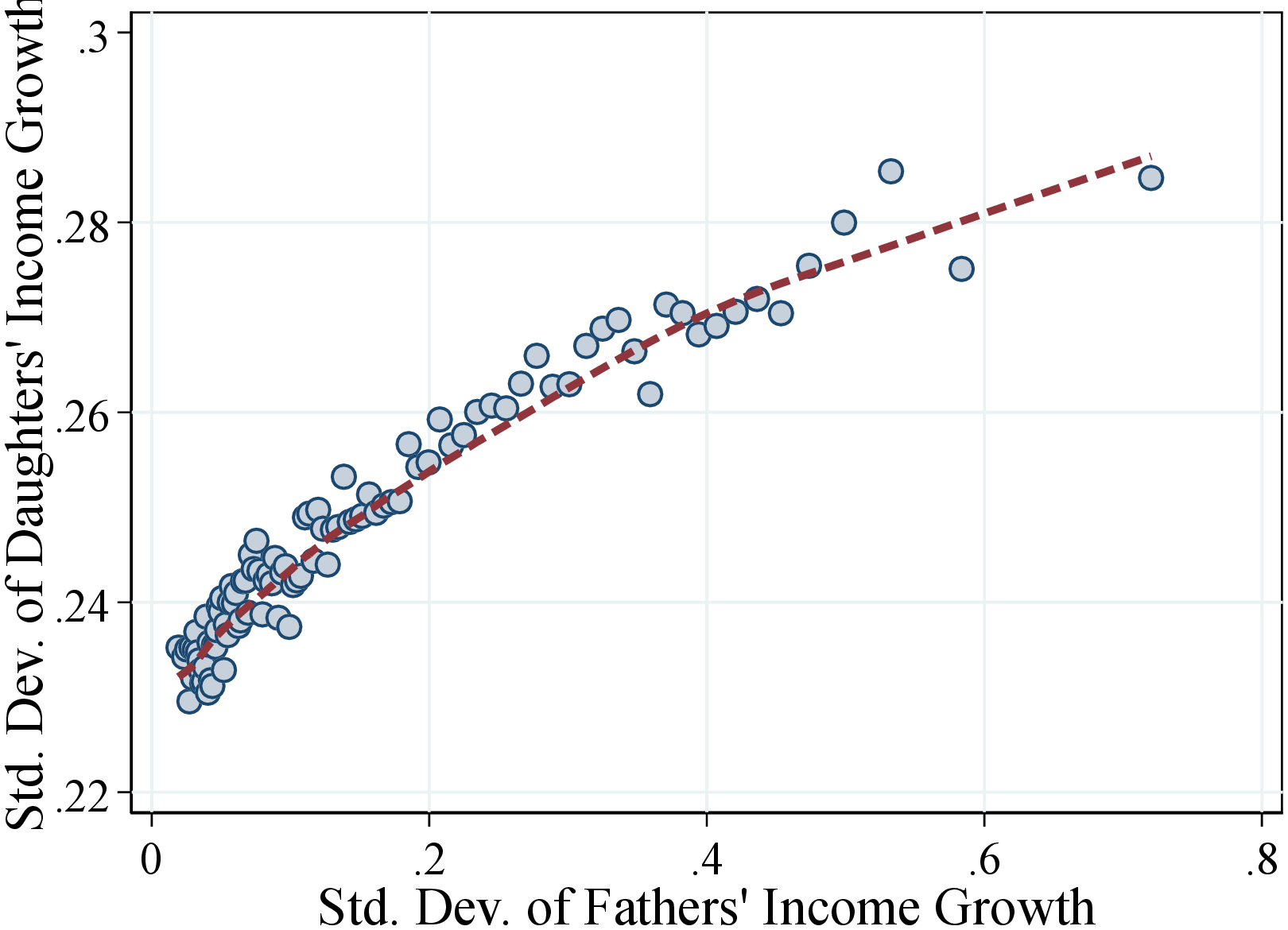

Income Growth Volatility. We now investigate whether the children of fathers with more volatile incomes also have riskier income streams. Figure 19 shows a binned scatter plot of the P90-P10 of fathers’ and children’s permanent income growth. We find a strong and economically significant correlation between fathers’ and children’s volatility of income. For example, when the father’s dispersion of income changes increases from 10 to 50 log points, where the bulk of the sample is, the son’s (daughter’s) P90-P10 of income growth increases roughly from 35 to 45 (45 to 55) log points. For more volatile incomes of fathers, the association becomes flatter, though still significant: An increase in the P90-P10 of fathers’ income from 50 to 150 log points is associated with an increase in children’s income volatility of roughly 10 log points. Together, these findings imply an elasticity between fathers’ and children’s income growth dispersion of 0.13 for sons and 0.11 for daughters.

(a) Sons

(a) Sons  (b) Daughters

(b) Daughters

Figure: Figure 19 – Dispersion of Income Growth of Fathers and Children

Notes: This plot is based on a sample of 494,514 father-son pairs (left plot) and 471,229 father-daughter pairs (right plot). Each sample is divided into 100 bins. The dashed lines are calculated using a lowess smoothing regression.

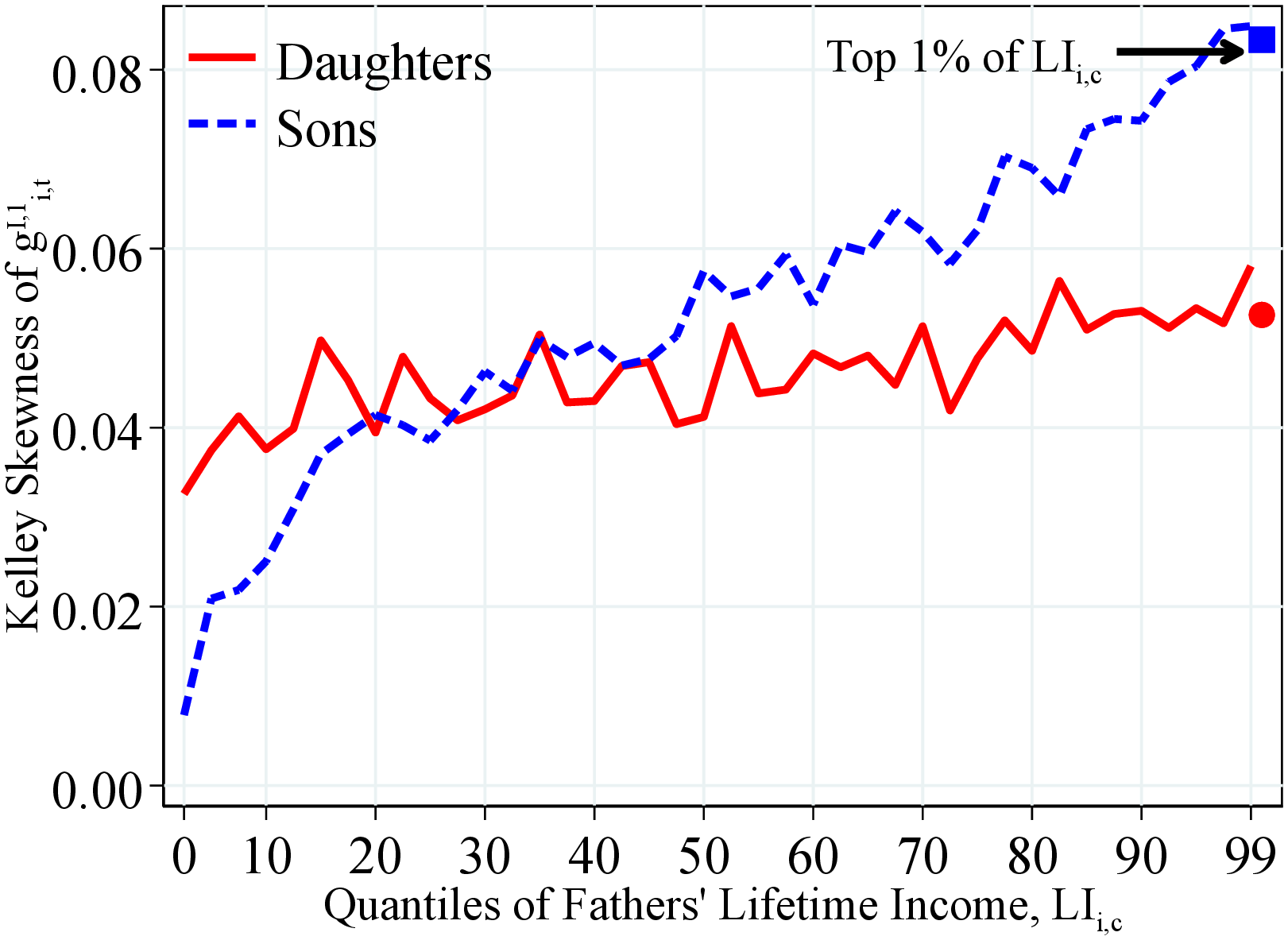

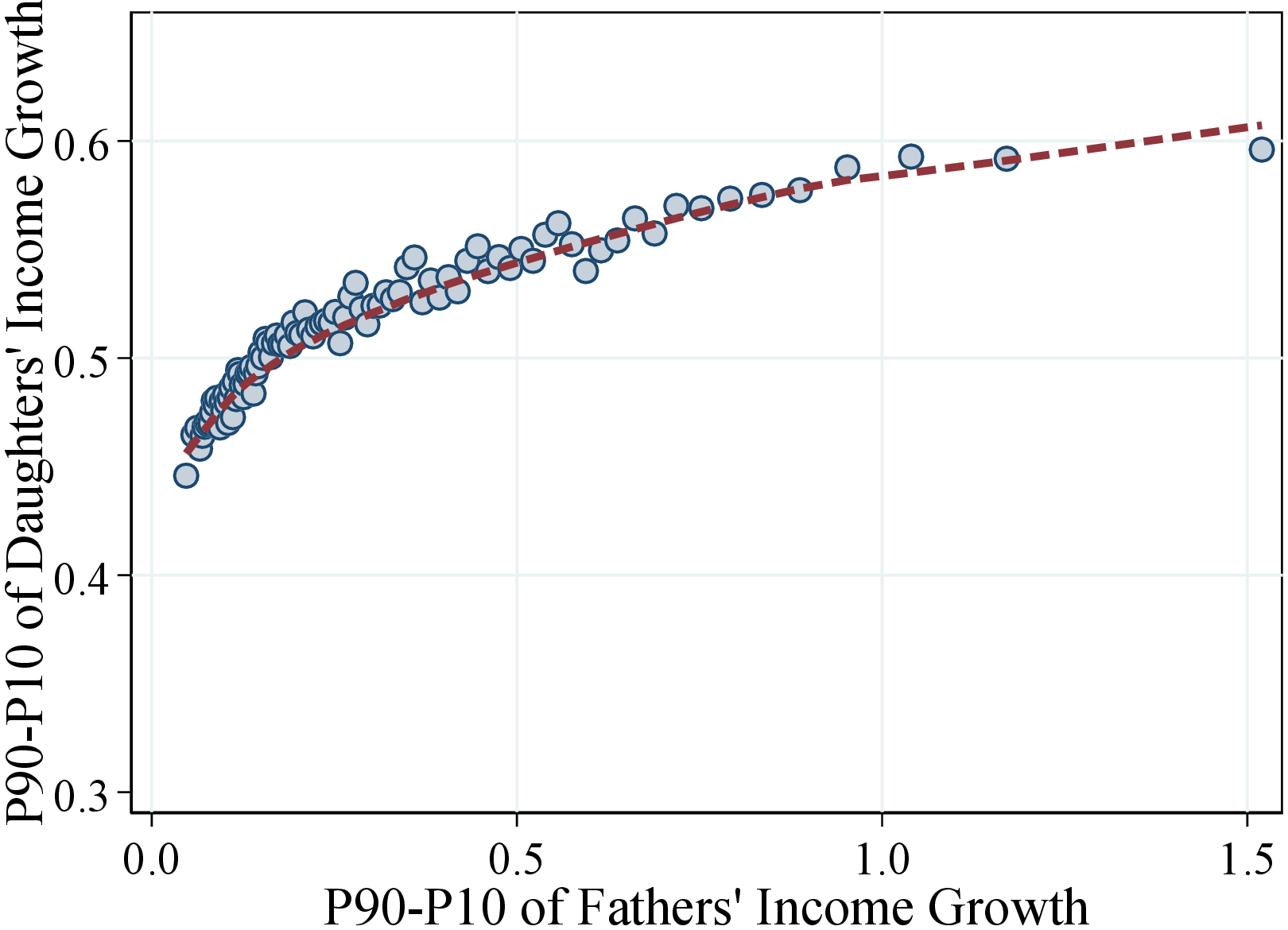

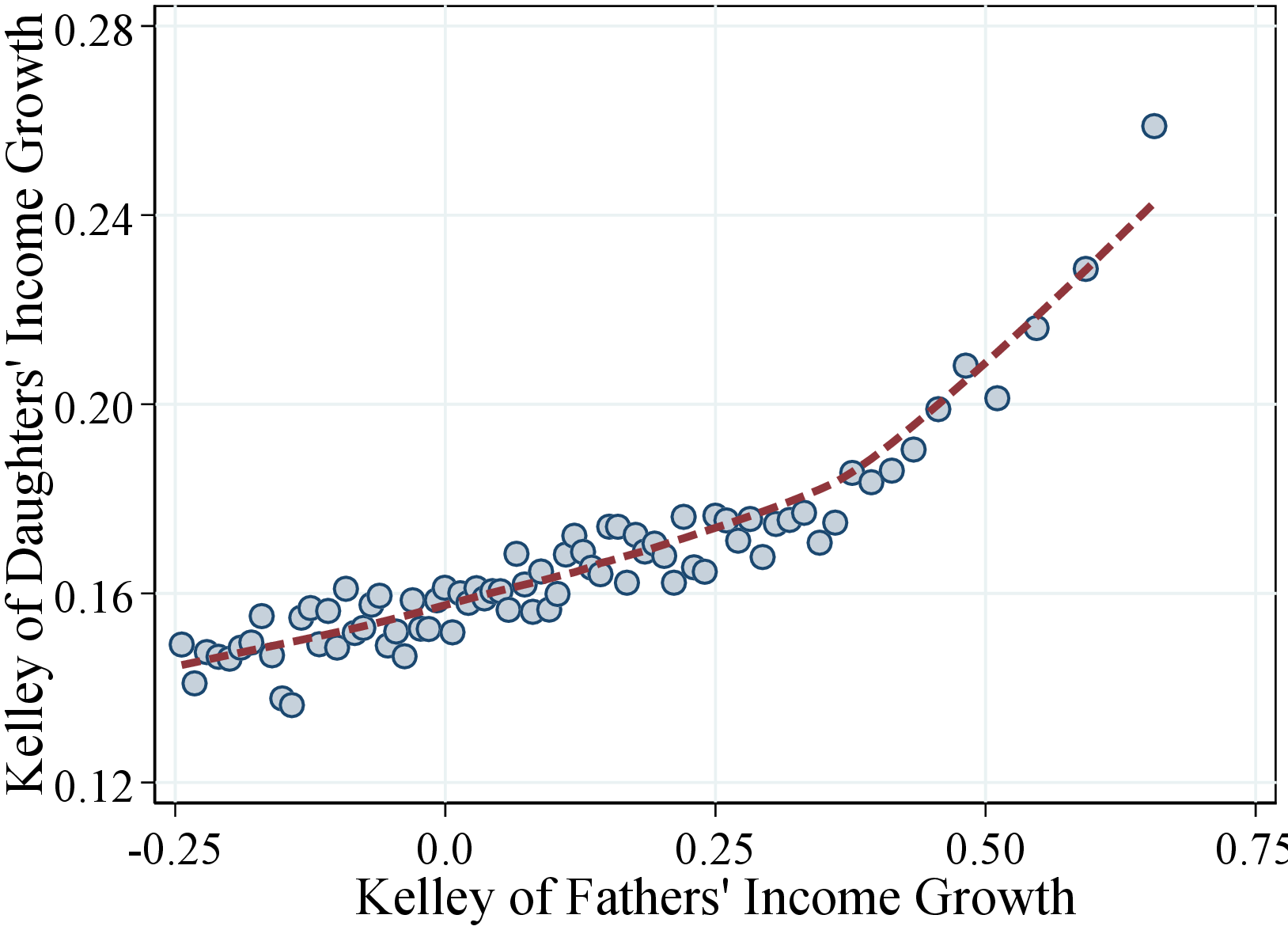

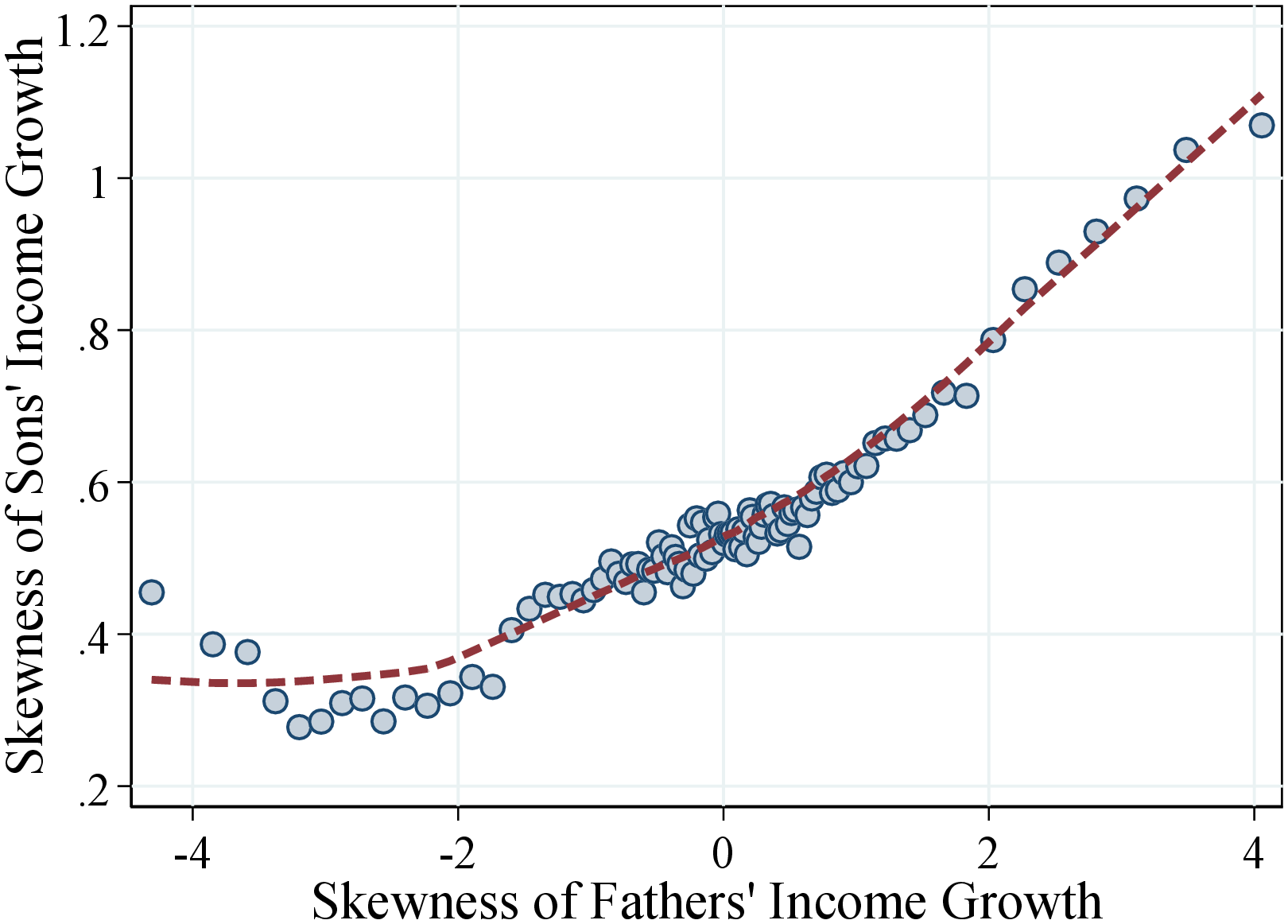

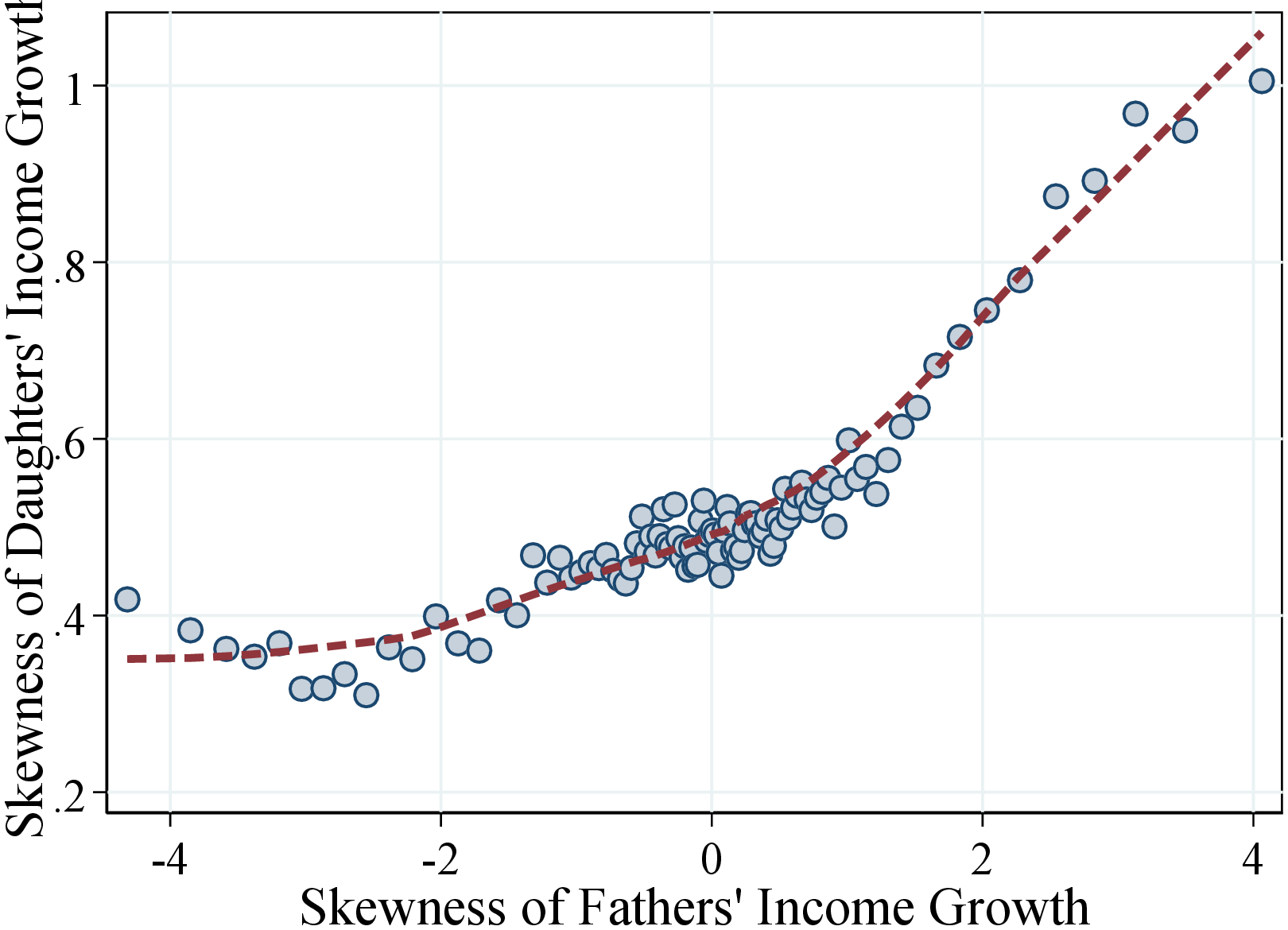

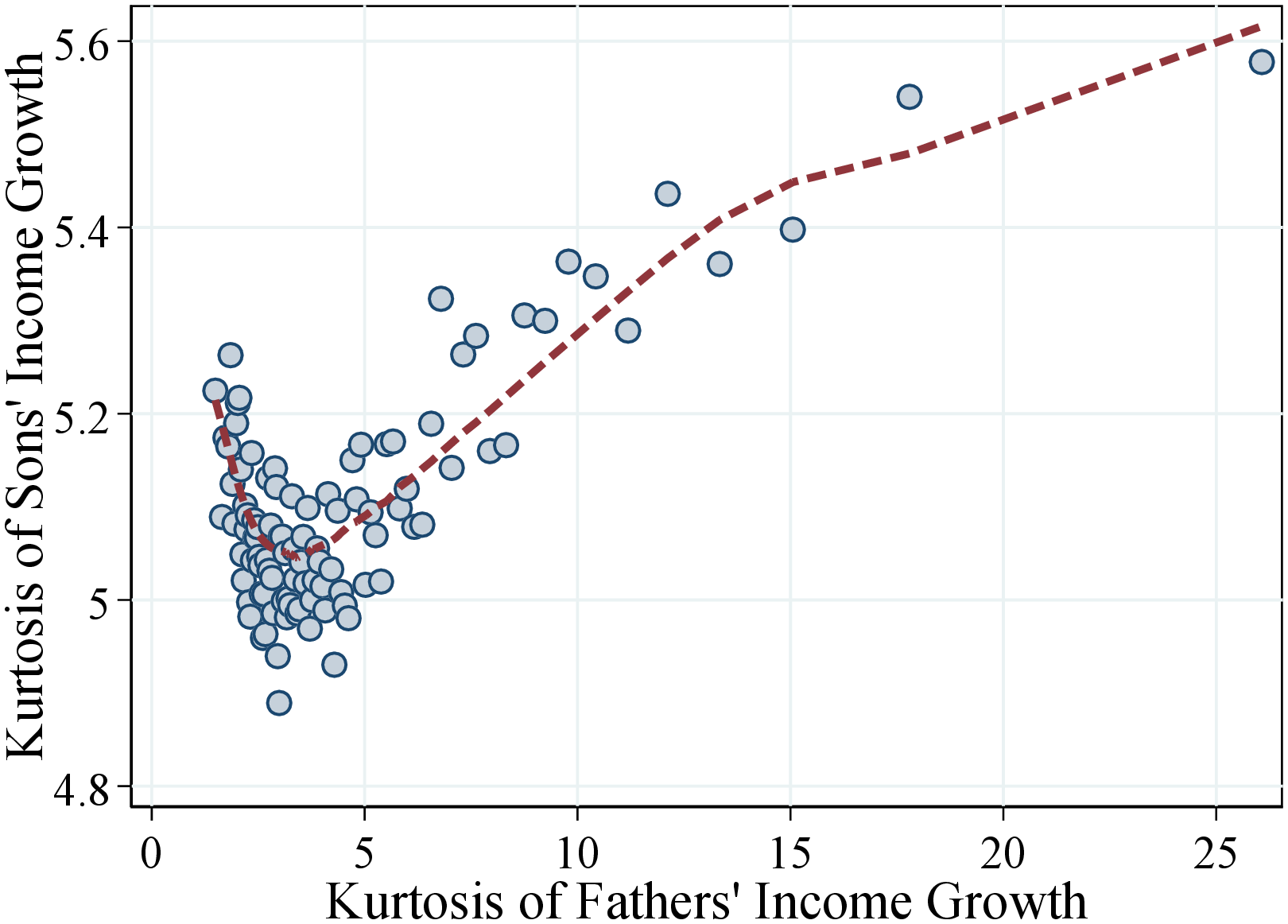

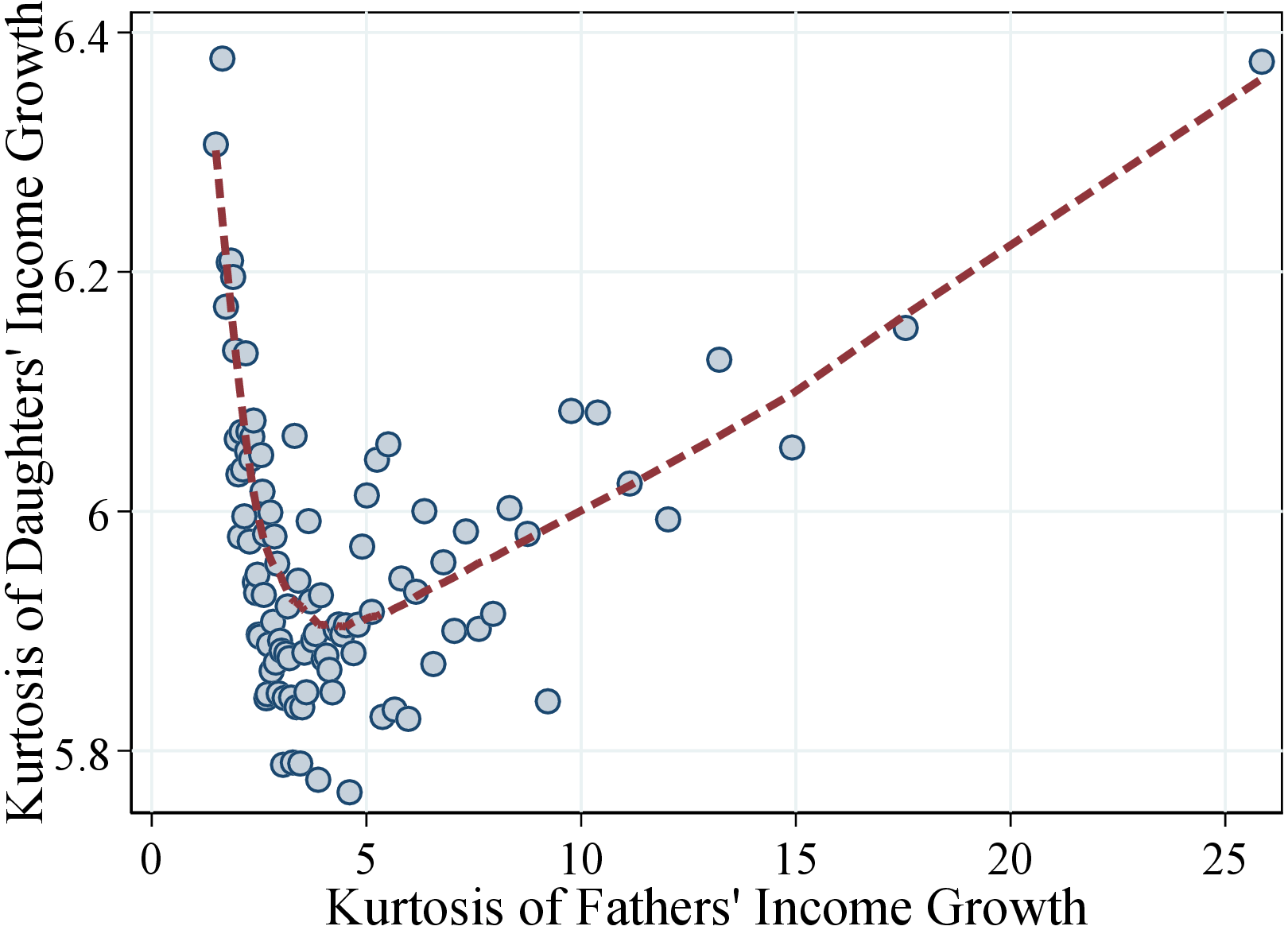

Skewness of Income Growth. Finally, we look at the relation between fathers’ and children’s skewness of income growth. Similar to the first two moments, Figure 20 shows a positive and strong correlation for Kelley skewness of income growth. Quantitatively, we find that an increase in fathers’ Kelley skewness from -0.25 to 0.25—where most of the distribution is found—is associated with an average increase of 0.04 (0.025) in the skewness of sons’ (daughters’) income growth.27

(a) Sons

(a) Sons  (b) Daughters

(b) Daughters

Figure: Figure 20 – Skewness of Income Growth of Fathers and Children

Notes: This plot is based on a sample of 494,514 father-son pairs (left plot) and 471,229 father-daughter pairs (right plot). Each sample is divided into 100 bins. The dashed lines are calculated using a lowess smoothing regression.

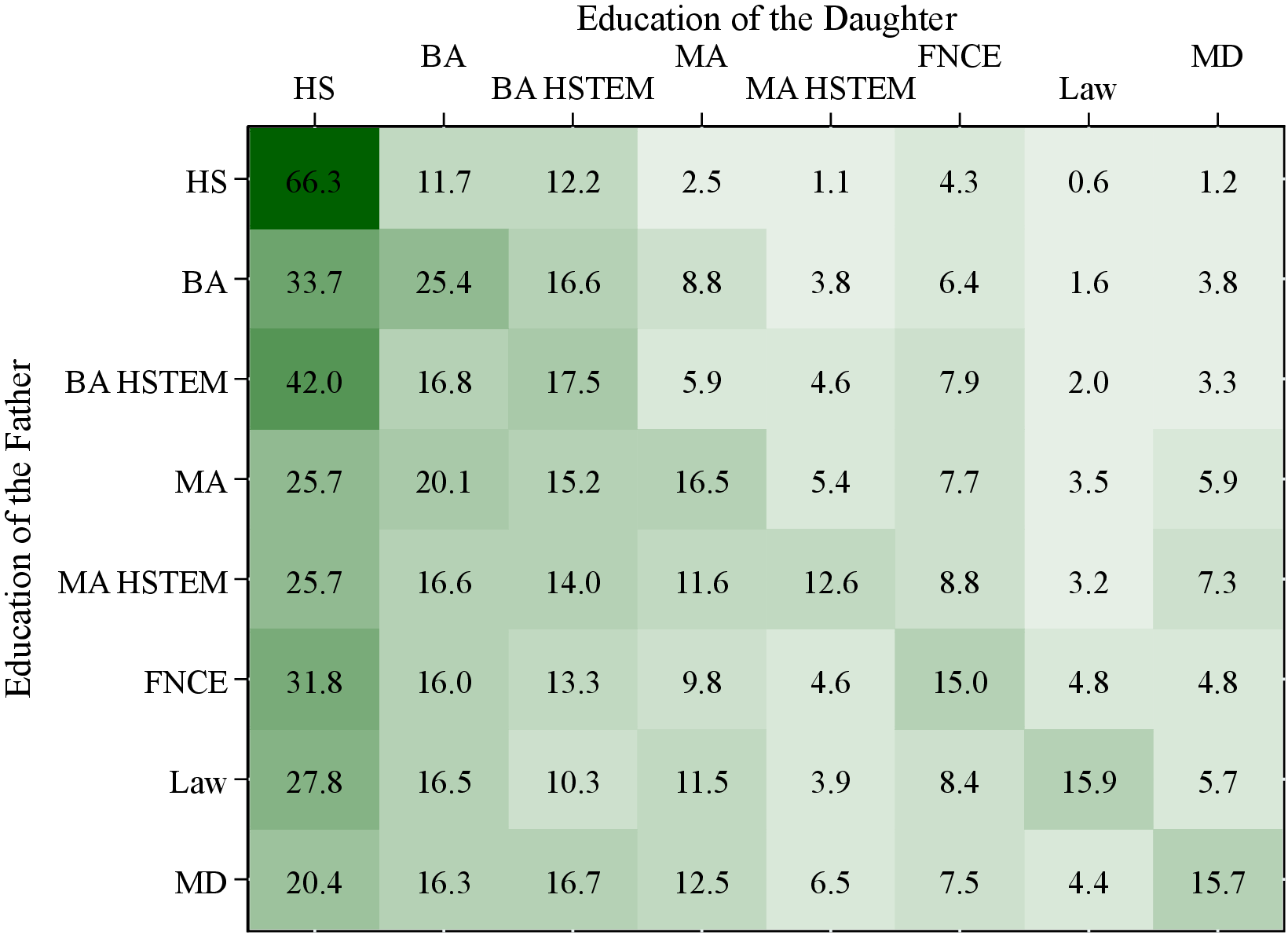

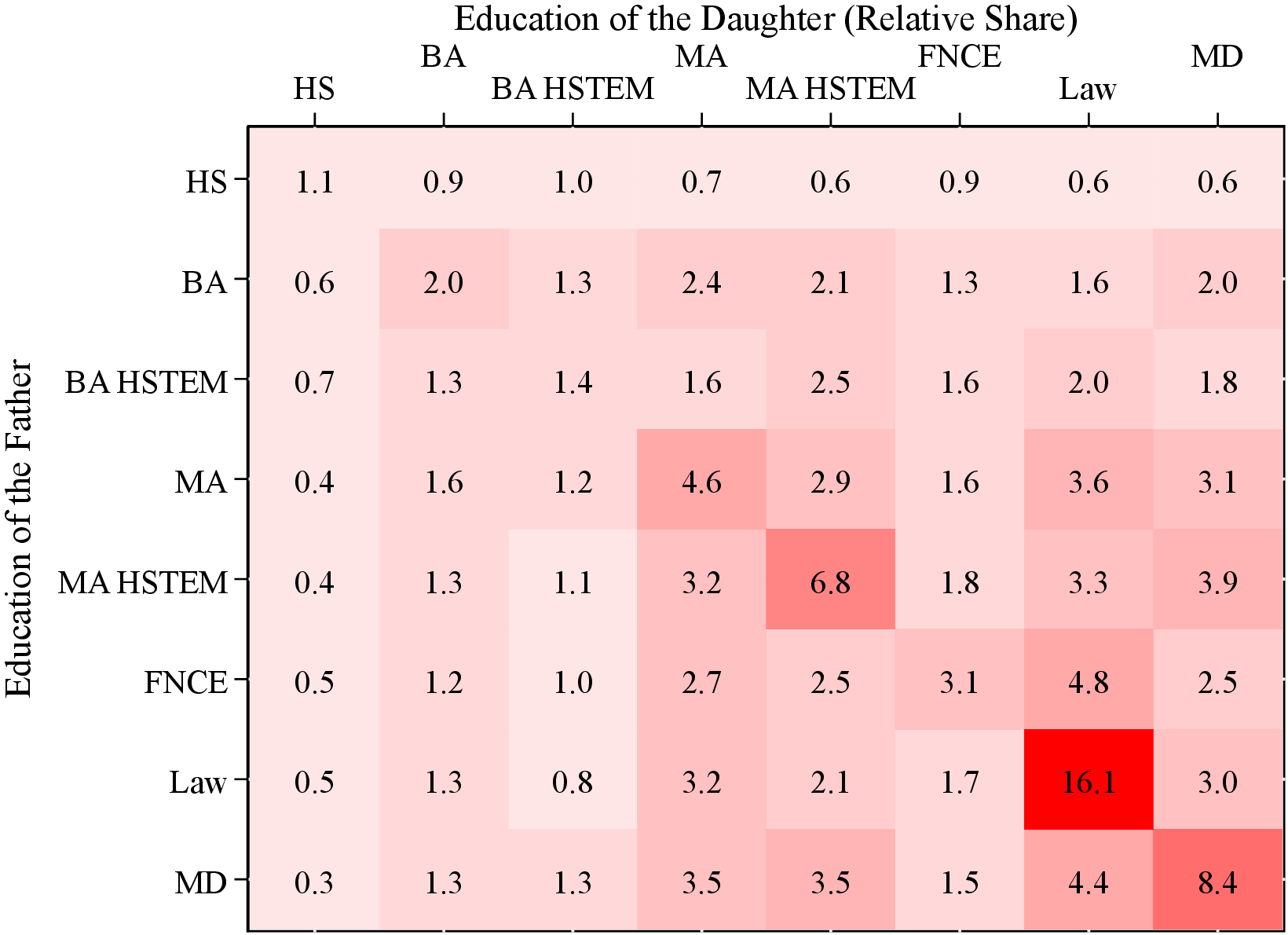

Occupational and Educational Intergenerational Mobility. One possible explanation for the findings in this subsection is that fathers and children have similar jobs and occupations, and therefore face similar income dynamics (see also Bello and Morchio (2017) and Boar and Lashkari (2021)). Despite the lack of information on occupations in our dataset, we know workers’ education at a detailed level. We investigate the intergenerational persistence in education using 47 categories of degrees, which range from primary education to post-graduate study in law (see Appendix C.4 for a full list).

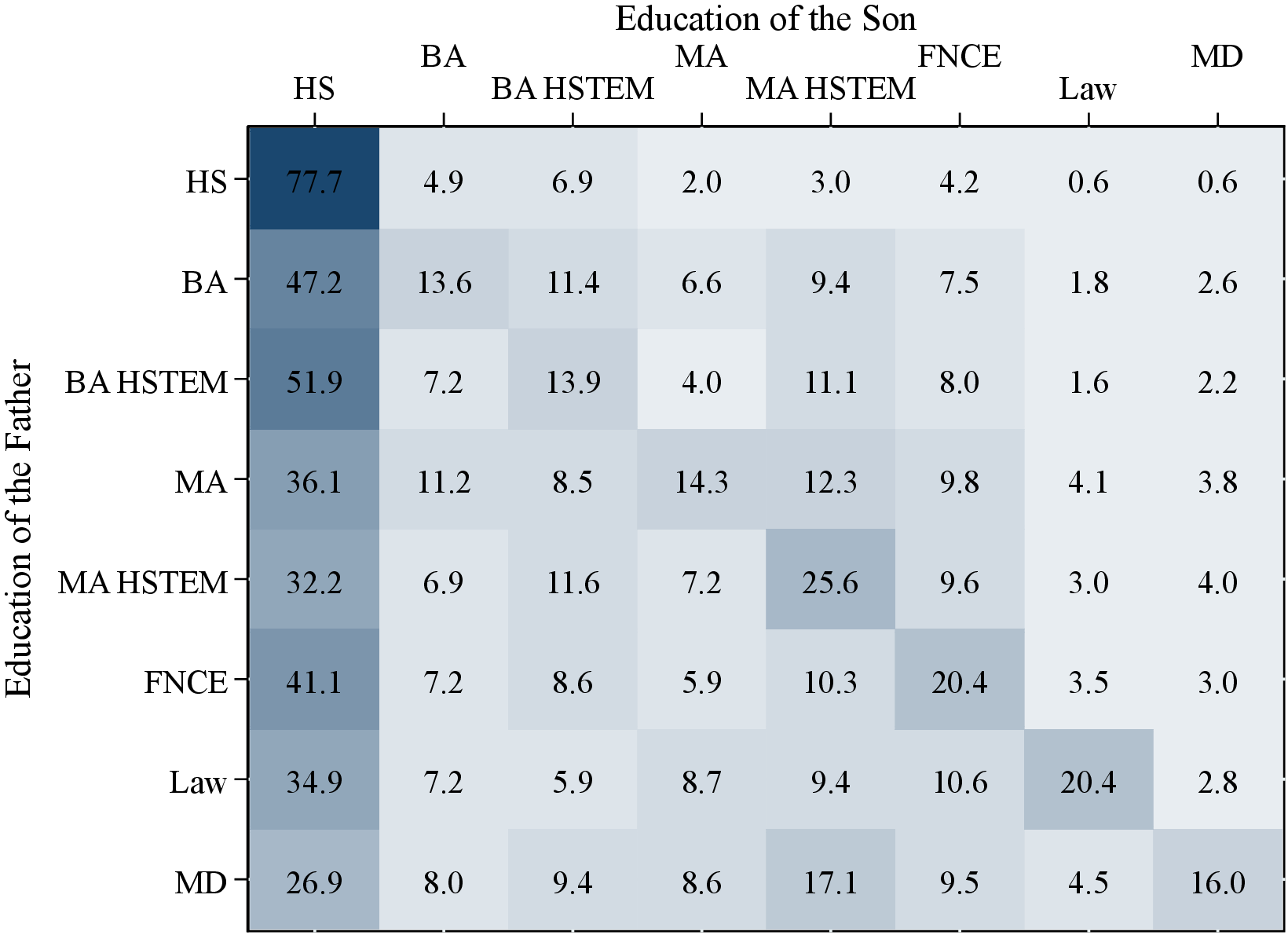

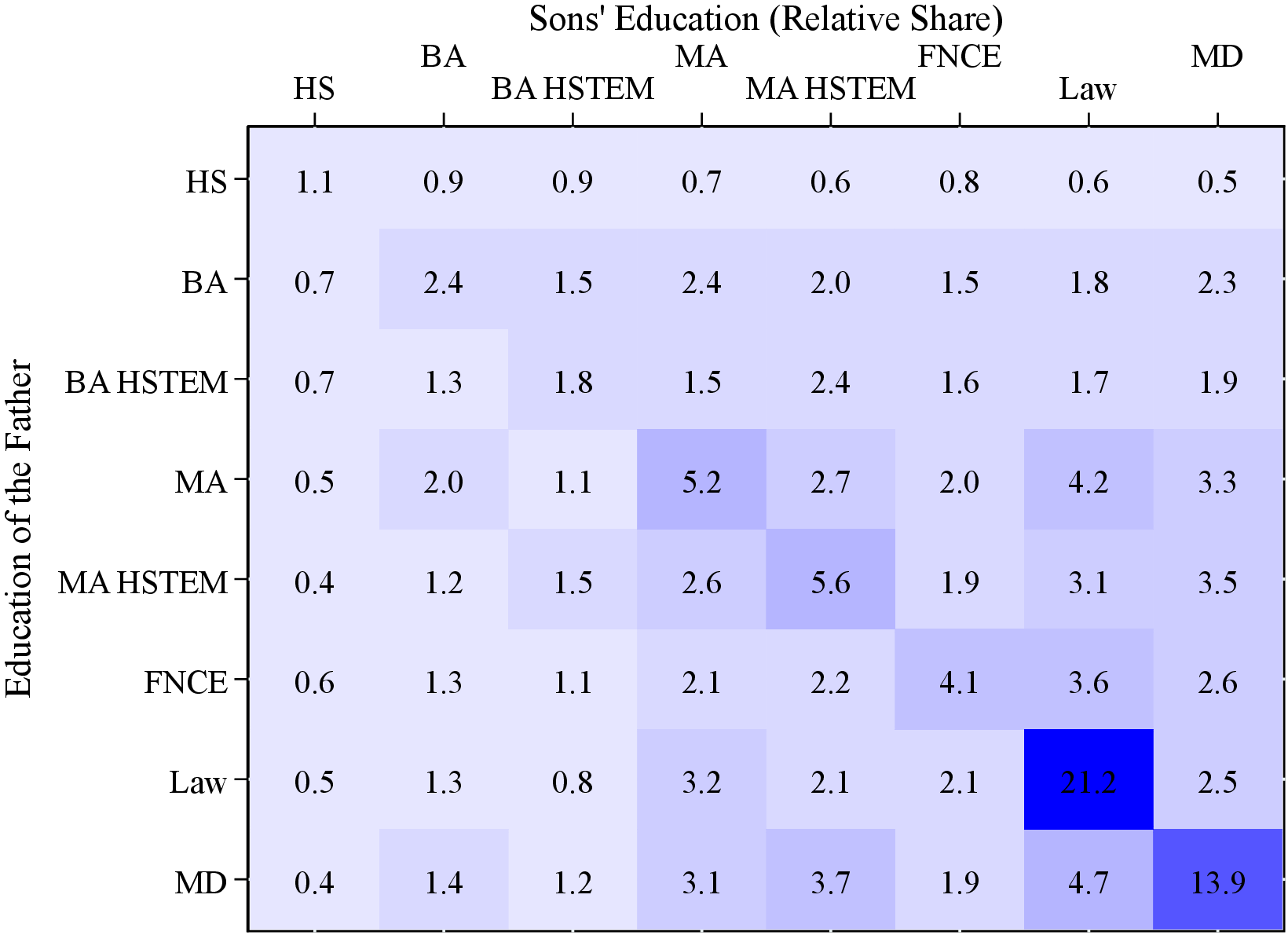

Figure OA.III.21 in Appendix C.4 shows the intergenerational transition matrix for a select group of education categories (the full matrix is available at authors’ websites). Since the Norwegian workforce has become more educated and its educational composition has changed over time, we normalize these probabilities with the corresponding population averages among children. For example, 9.7% of sons of dentists also studied dentistry, but only 0.4% of all sons are dentists. Then the value for the intergenerational persistence of dentists in this matrix is \(\frac{9.7\%}{0.4\%}=22.5\), which implies that sons of dentists are 22.5 times more likely to be dentists relative to the population average.

All of the values on the diagonal of this matrix is significantly greater than 1, with an average of 6 for sons and 4.4 for daughters. For brevity, Table II shows this statistic for the five most and least persistent education categories. According to this measure, dentists, lawyers, and doctors display the strongest intergenerational persistence along with nurses and those with a higher degree in the social sciences (which includes economists). At the other extreme, we see substantial upward intergenerational socioeconomic mobility for children of relatively low-educated fathers. For example, fathers with only a primary education are among the least likely group to have children with a similar education (after already accounting for changes in educational composition across cohorts).

Strong intergenerational persistence in education supports our conjecture that fathers and children have similar occupations, thereby exhibiting correlated income risk. In the next section, we further investigate the determinants of the transmission of income risk.

| Least Persistent | Most Persistent | |||||||||

| Sons | ||||||||||

| Title | Low Sec. | Prim. | Tech | Sec ad | Voc. | Nurse | Soc. Sci | MD | Law | Dent. |

| Persistence | 1.1 | 1.3 | 1.5 | 1.6 | 1.7 | 8.2 | 10.3 | 19.4 | 21.2 | 22.5 |

| Pop. Share | 1.1% | 26.5% | 14.7% | 4.1% | 3.8% | 0.6% | 0.9% | 0.7% | 1.0% | 0.4% |

| Daughters | ||||||||||

| Title | Low Sec. | Sec adm. | Voc. | Prim | Up Sec. | Dent. | Soc. Sci | MS Eng. | MD | Law |

| Persistence | 1.2 | 1.2 | 1.2 | 1.3 | 1.4 | 8.5 | 8.9 | 9.7 | 14.5 | 16.1 |

| Pop. Share | 0.4% | 9.3% | 1.8% | 26.3% | 10.1% | 1.1% | 1.3% | 0.7% | 0.8% | 1.0% |

Notes: Table II shows the intergenerational persistence of educational categories between fathers and children. Persistence is calculated as the ratio between the proportion of children with a particular education whose fathers also have the same education normalized by the population share of that educational category (Pop. Share). This table shows the least and most persistent among 47 available categories. A full set of educational categories is available in Appendix C.4.

4.4 Determinants of the Transmission of Income Risk