1 Introduction

Why is wage inequality significantly higher in the United States than in continental European countries (CEU)? And why has this inequality gap between the US and the CEU widened substantially since the 1970s (see Table 1)? More broadly, what are the determinants of wage dispersion in modern economies? How do these determinants interact with technological progress and government policies? The goal of this paper is to shed light on these questions by studying the impact of labor market (tax) policies on the determination of wage inequality, focusing on male workers and using cross-country data.

We begin by documenting two empirical relationships between wage inequality and tax policy. First, we show that countries with more progressive labor income tax schedules have significantly lower wage inequality at different points in time.1 The measure of wages we use is “gross before-tax wages” and can therefore be thought of as a proxy for the marginal product of workers.2 From this perspective, progressivity is associated with a more compressed productivity distribution across workers. Second, we show that countries with more progressive income taxes have also experienced a smaller rise in wage inequality over time, and this relationship is especially strong above the median of the wage distribution. These findings reveal a close relationship between progressivity and wage inequality, which motivates the focus of this paper. However, on their own, these correlations fall short of providing a quantitative assessment of the importance of the tax structure—e.g., what fraction of cross-country differences in wage inequality can be attributed to tax policies? For this purpose, we build a model.

| 1978–1982 | 2001–2005 | Change | |

| average | average | ||

| Denmark | — | 0.97 | — |

| Finland | 0.89 | 0.94 | 0.05 |

| France | 1.22 | 1.14 | –0.08 |

| Germany | 0.93 | 1.06 | 0.07 |

| Netherlands | 0.84 | 1.05 | 0.11 |

| Sweden | 0.73 | 0.87 | 0.14 |

| CEU | 0.92 | 1.01 | 0.06 |

| UK | 0.99 | 1.28 | 0.29 |

| US | 1.28 | 1.60 | 0.32 |

Specifically, we construct a life cycle model that features some key determinants of wages—most notably, human capital accumulation and idiosyncratic shocks. Individuals enter the economy with an initial stock of human capital and are able to accumulate more human capital over the life cycle using a Ben-Porath (1967) style technology (which combines learning ability, time, and existing human capital for production). Individuals can choose to either invest in human capital on the job up to a certain fraction of their time or enroll in school where they invest full time. We assume that skills are general and labor markets are competitive. As a result, the cost of on-the-job investment will be borne by the workers, and firms will adjust the wage rate downward by the fraction of time invested on the job.

We introduce two main features into this framework. First, we assume that individuals differ in their learning ability. As a result, individuals differ systematically in the amount of investment they undertake and, consequently, in the growth rate of their wages over the life cycle. Thus, a key source of wage inequality in this model is the systematic fanning out of the wage profiles.3 Second, we allow for endogenous labor supply choice, which amplifies the effect of progressivity, a point that we return to shortly. Finally, for a comprehensive quantitative assessment, we also allow idiosyncratic shocks to workers’ labor efficiency and model differences in consumption taxes and pension systems, which vary greatly across these countries.

The model described here provides a central role for policies that compress the wage structure—such as progressive income taxes—because such policies hamper the incentives for human capital investment. This is because a progressive system reduces after-tax wages at the higher end of the wage distribution compared with the lower end. As a result, it reduces the marginal benefit of investment (the higher wages in the future) relative to the marginal cost (the current forgone earnings), thereby depressing investment. A key observation is that this distortion varies systematically with the ability level—and, specifically, it worsens with higher ability—which then compresses the before-tax wage distribution. These effects of progressivity are amplified by endogenous labor supply and differences in average income tax rates: the higher taxes in the CEU reduce labor supply—and, consequently, the benefit of human capital investment—further compressing the wage distribution.

The main quantitative exercise we conduct is the following. We consider the eight countries listed in Table 1, for which we have complete data for all variables of interest. We assume that all countries have the same innate ability distribution but allow them to differ in the observable dimensions of their labor market structures, such as in labor income (and consumption) tax schedules and retirement pension systems. We then calibrate the model-specific parameters to the US data and keep these parameters fixed across countries. The policy differences we consider explain about half of the observed gap in the log 90-10 wage differential between the US and the CEU in the 2000s and 84% of the wage inequality above the median (log 90-50 differential). The model explains only about 24% of the difference in the lower tail inequality between the US and the CEU, which is consistent with the idea that the human capital mechanism is likely to be more important for higher ability individuals and, therefore, above the median of the distribution. We also provide a decomposition that isolates the roles of (i) the progressivity of income taxes, (ii) average income tax rates, (iii) consumption taxes, and (iv) the pension system. We find that progressivity is by far the most important component, accounting for about 2/3 of the model’s explanatory power.

The second question we ask is whether the widening of the inequality gap between the US and the CEU since the late 1970s could also be explained by the same human capital channels discussed earlier. One challenge we face in trying to answer this question is that the country-specific tax schedules that we derive in this paper are only available for the years after 2001 (due to data availability), whereas the tax structure has changed over time for several of the countries in our sample. Fortunately, for two countries in our sample—the US and Germany—we are also able to derive tax schedules for 1983, which reveal significantly more flattening of tax schedules in the US compared with Germany from 1983 to 2003 (see Figure 6). When these changes in progressivity and skill-biased technical change (SBTC) are jointly taken into account, the (recalibrated) model generates a much larger rise in inequality in the US than in Germany, in fact, slightly overestimating the actual widening of the inequality gap between these countries.

Finally, in section 6, we test some key implications of our model for lifecycle behavior using micro data. First, the model predicts that a country with a more progressive tax system should have a flatter age profile of average wages (by dampening human capital accumulation) compared with a less progressive one. Similarly, progressivity will imply a flatter profile of within-cohort wage inequality over the life cycle. We provide a comparison of the United States (using the Panel Study of Income Dynamics, PSID, data) and Germany (using the German Socio-Economic Panel, GSOEP) and find support for both predictions. We also discuss the predictions of the model for the levels of schooling and average labor hours for the countries in our sample.

1.1 Related Literature

Rodriguez (1998) and Moene and Wallerstein (2001) have documented that redistribution is larger in countries that have less (before-tax) wage dispersion.4 The political economy literature has proposed politico-economic models where small wage dispersion implies large redistribution (see, e.g., Hassler et al. (2003), Benabou (2000)). We propose an alternative theory where the wage dispersion is endogenous and progressive taxes imply less wage dispersion.

In terms of methodology, this paper is most closely related to the recent macroeconomics literature that has written fully specified models to address US-CEU differences in labor market outcomes. Prominent examples include Ljungqvist and Sargent (1998); Ljungqvist and Sargent (2008) and Hornstein et al. (2007), who focus on unemployment rates, and Prescott (2004), Ohanian et al. (2008), and Rogerson (2008), who study labor hours differences. Several of these papers rely on representative agent models and are, therefore, silent on wage inequality; and those that do allow for individual-level heterogeneity do not address differences in wage inequality. In terms of modeling choices, the closest framework to ours is Kitao et al. (2008), who study a rich life cycle framework with human capital accumulation and job search and model the benefits system. Their goal is to explain the different unemployment patterns over the life cycle in the US and Europe.

Finally, a number of recent papers share some common modeling elements with ours but address different questions. Important examples include Altig and Carlstrom (1999), Krebs (2003), Caucutt et al. (2006), and Huggett et al. (2011). Altig and Carlstrom (1999) study the quantitative impact of the Tax Reform Act of 1986 on income inequality arising solely from behavioral responses associated with labor supply and saving decisions and find that distortions arising from marginal tax rate changes have sizable effects on income inequality. Krebs (2003) studies the impact of idiosyncratic shocks on human capital investment and shows that reducing income risk can increase growth, in contrast to the standard incomplete markets literature, which typically reaches the opposite conclusion. Caucutt et al. (2006) develop an endogenous growth model with heterogeneity in income. They show that a reduction in the progressivity of tax rates can have positive growth effects even in situations where changes in flat-rate taxes have no effect. Another important contribution is Huggett et al. (2011), who study the distributional implications of the Ben-Porath model and estimate the sources of lifetime inequality using US earnings data. Finally, Erosa and Koreshkova (2007) investigate the effects of replacing the current U.S. progressive income tax system with a proportional one in a dynastic model. They find a large positive effect on steady state output, which comes at the expense of higher inequality. Although our paper has many useful points of contact with this body of work, to our knowledge, our combination of human capital accumulation, ability heterogeneity, progressive taxation, and endogenous labor supply is new, as is the attempt to explain cross-country inequality facts in such a framework.

The next section lays out the main model and explains the various channels through which tax policy affects wage inequality. Section 3 describes how the country-specific tax schedules are estimated and uses the estimates to document two new empirical relationships between taxes and inequality. Sections 4 and 5 discusses the parameterization and the main quantitative results. Section 6 examines a series of micro implications of the human capital mechanism proposed in this paper. Section 7 concludes.

2 The Model

We begin by describing the human capital investment problem. Using this environment, we discuss the various channels through which tax policy affects wage inequality. We then enrich this framework by introducing empirically relevant features (such as idiosyncratic shocks and labor market institutions) that are necessary for a sound quantitative analysis.

2.1 Human Capital Accumulation

Consider an individual who derives utility from consumption and leisure and has access to borrowing and saving at a constant interest rate, \(r\). Let \(\beta\) be the subjective time discount factor and assume \(\beta (1+r)=1\). Each individual has one unit of time in each period, which he can allocate to three different uses: work, leisure, and human capital investment. If an individual chooses to work, he can allocate a fraction (\(i\)) of his working hours (\(n\)) to human capital investment. At age \(s,\) new human capital, \(Q_{s},\) is produced according to a Ben-Porath technology:

\[ Q_{s}=A^{j}\left (h_{s}i_{s}n_{s}\right)^{\alpha}, \]

where \(h_{s}\) denotes the individual’s current human capital stock and \(A^{j}\) is the learning ability of individual type \(j\). We assume that skills are general and labor markets are competitive. As a result, the cost of human capital investment is completely borne by workers, and firms adjust the hourly wage rate, \(w_{s},\) downward by the fraction of time invested on the job: \(w_{s}=P_{H}h_{s}(1-i_{s})\), where \(P_{H}\) is the price of human capital; labor income is simply \(y_{s}=w_{s}n_{s}\). Finally, let \(\bar{\tau}(y)\) and \(\tau (y)\) denote, respectively, the average and marginal labor income tax functions. The problem of a type \(j\) individual can be written as

\[ \]

\[\begin{aligned} $$ \max _{\{c_{s},n_{s},a_{s+1},i_{s}\}} & \sum ^{S}_{s=1}\beta ^{s-1}u(c_{s},1-n_{s}) \\ \textrm{s.t.}\qquad c_{s}+a_{s+1} & =(1-\bar{\tau}(y_{s}))y_{s}+(1+r)a_{s} \\ h_{s+1} & =h_{s}+A^{j}\left (h_{s}i_{s}n_{s}\right)^{\alpha}\\ y_{s} & =P_{H}h_{s}(1-i_{s})n_{s}. $$ \end{aligned}\]\[ \]

The opportunity “cost of investment” (in human capital units) is equal to \(h_{s}i_{s}n_{s}\) and, using equation (1), it can be written as \(C_{j}(Q^{j}_{s})=\left (Q^{j}_{s}/A^{j}\right)^{1/\alpha}\), which will play a key role in the optimality conditions that follow.

A key parameter in the Ben-Porath technology is \(A^{j}\). Heterogeneity in \(A^{j}\) implies that individuals will differ systematically in the amount of human capital they accumulate and, consequently, in the growth rate of their wages over the life cycle. This systematic fanning out of wage profiles is the major source of wage inequality in this model.

2.2 Inspecting the Mechanisms

We are now ready to discuss how taxation of human capital can affect wage inequality. To this end, it is useful to distinguish between two cases.

Inelastic Labor Supply. First, suppose that labor supply is inelastic. Assuming an interior solution, the optimality condition for human capital investment is \[\begin{alignat} {1} \left (1-\tau (y_{s})\right)C^{\prime}_{j}(Q^{j}_{s})= & \{{\color{black}{\color{blue}{\color{black}\beta}\mathinner{\color{black}\left ({\color{black}1-\tau (y_{s+1}}\mathclose{\color{black})}\right)}}}+\beta ^{2}\left (1-\tau (y_{s+2})\right)+...+\beta ^{S-s}\left (1-\tau (y_{S})\right)\},\label{eq:FOC1} \end{alignat}\]

which equates the after-tax marginal cost of investment on the left hand side to the after-tax marginal benefit on the right.5 To understand the effect of taxes, first consider the case where taxes are flat rate (\(\tau '(y)=0,\:\forall y,\)). In this case, all terms involving taxes cancel out: \[\begin{alignat*} {1} C^{\prime}_{j}(Q^{j}_{s})= & \{{\color{blue}{\color{black}\beta}}+\beta ^{2}+...+\beta ^{S-s}\}. \end{alignat*}\]

Thus, flat-rate taxes have no effect on human capital investment. This is a well-understood insight that goes back to at least Heckman (1976) and Boskin (1977).6

Now consider progressive taxes, i.e., \(\tau '(y)>0\). We rearrange equation (4) to get: \[\begin{alignat} {1} C^{\prime}_{j}(Q^{j}_{s})= & \{{\color{blue}{\color{black}{\color{black}\beta}}\mathinner{\color{black}\frac{1-\tau (y_{s+1})}{1-\tau (y_{s})}}}+\beta ^{2}{\color{black}{\color{black}{\color{blue}\mathinner{\color{black}\frac{{\color{black}1-\tau (y_{s+2}}\mathclose{\color{black})}}{{\color{black}1-\tau (y_{s}}\mathclose{\color{black})}}}}}}+...+\beta ^{S-s}\frac{1-\tau (y_{S})}{1-\tau (y_{s})}\}.\label{eq:FOC2} \end{alignat}\]

With progressivity, as long as the individual’s earnings grow over the life cycle, the tax ratios in (5) will be strictly less than one, depressing the marginal benefit of investment, which in turn dampens human capital accumulation. Thus, these tax ratios capture the reduction in the value of future wage earnings compared with the forgone wage earnings today. This observation motivates our first measure of progressivity, what we refer to as the progressivity wedge, defined as:

\[ PW(y_{s},y_{s+k})\equiv 1-\frac{1-\tau (y_{s+k})}{1-\tau (y_{s})}, \]

between any two ages \(s\) and \(s+k\). A progressivity wedge of zero corresponds to flat taxes, and progressivity increases with the size of the wedge. In the next section, we empirically measure these wedges from the data.

To understand the effect of progressive taxes on wage inequality, note that the distortion created by progressivity differs systematically across ability levels. At the low end, individuals with very low ability whose optimal plan involves no human capital investment in the absence of taxes would experience no wage growth over the life cycle and, therefore, no distortion from progressive taxation. At the top end, individuals with high ability (whose optimal plan implies low wage earnings early in life and very high earnings later) face very large wedges, which depress their investment. Thus, progressivity reduces the cross-sectional dispersion of human capital and, consequently, wage inequality in an economy, even with inelastic labor supply.

Endogenous Labor Supply. Second, consider now the the case with elastic labor supply. The first order condition can be shown to be (see Appendix A.1) as follows: \[\begin{alignat} {1} C^{\prime}_{j}(Q^{j}_{s})= & \{{\color{blue}{\color{black}{\color{black}\beta}}\mathinner{\color{black}\frac{1-\tau (y_{s+1})}{1-\tau (y_{s})}}}{\color{red}{\color{black}n}_{{\color{black}s+1}}}+\beta ^{2}{\color{black}{\color{black}{\color{blue}\mathinner{\color{black}\frac{{\color{black}1-\tau (y_{s+2}}\mathclose{\color{black})}}{{\color{black}1-\tau (y_{s}}\mathclose{\color{black})}}}}}}{\color{red}{n_{s+2}}}+...+\beta ^{S-s}{\color{blue}\mathinner{\color{black}\frac{1-\tau (y_{S})}{1-\tau (y_{s})}}}{\color{red}{n}_{{S}}}\},\label{eq:FOC3} \end{alignat}\]

where now the marginal benefit accounts for the utilization rate of human capital, which depends on the labor supply choice. Our second measure of progressivity is precisely motivated by this first order condition subject to a normalization:

\[ PW^{*}_{i}(y_{s},y_{s+k})=1-\frac{1-\tau (y_{s+k})}{1-\tau (y_{s})}\left (\frac{n_{i}}{{\displaystyle n_{\text{avg}}}}\right), \]

where \(n_{i}\) is the hours per person in country \(i\) and \(n_{\text{avg}}\) is the average of \(n_{i}\) across all countries in the sample.7

Now, once again, consider the effect of flat-rate taxes. The intra-temporal optimality condition for labor-leisure choice implies that labor supply depends negatively on the tax rate and positively on the level of human capital. A higher tax rate depresses labor supply choice (as long as the income effect is not too large),8 which then reduces the marginal benefit of human capital investment, which reduces the optimal level of human capital. But labor supply in turn depends on the level of human capital, which further depresses labor supply, the level of human capital, and so on. Therefore, with endogenous labor supply, even a flat-rate tax has an effect on human capital investment, which can also be large because of the amplification described here.

In summary, the baseline model studied here implies that countries with more progressive tax systems will have lower wage inequality. To the extent that labor supply is elastic (and the income effect is not too large), higher average tax rates can also lead to lower wage inequality. Finally, and as will become clear later, these countries will also experience a smaller change in wage inequality in response to technological changes (such as SBTC). In Section 3, we examine these predictions empirically.

2.3 Enriching the Basic Framework

As stated earlier, the main goal of this paper is to provide a quantitative assessment of the importance of the tax structure—e.g., what fraction of cross-country differences in wage inequality can be attributed to tax policies? For this purpose, we introduce several empirically relevant features.

Upper Bound on On-the-Job Investment. We impose an upper bound on the fraction of time that can be devoted to on-the-job investment: \(i\in [0,\chi]\), where \(\chi <1.\) Such an upper bound would arise, for example, when firms incur fixed costs for employing each worker (administrative burden, cost of office space, etc.) or as a result of minimum wage laws. Individuals can invest full-time by attending school (\(i=1\)) and enjoy leisure for the rest of the time. Thus, the choice set is \(i\in [0,\chi]\cup \{1\},\) which is non-convex when \(\chi <1\). Finally, human capital depreciates every period at rate \(\delta <1\).

Idiosyncratic Shocks. It is difficult to talk about wage inequality without any sort of idiosyncratic shock. In a human capital model, these shocks would interact with investment choice and can potentially affect the quantitative conclusions we draw from the analysis. Thus, we introduce idiosyncratic shocks to the efficiency of labor supply. Specifically, when an individual devotes \(\)\((1-i_{s})n_{s}\) hours producing for his employer, his effective labor supply becomes \(\epsilon n_{s}(1-i_{s})\), where \(\epsilon\) is an idiosyncratic Markov shock with a stationary transition matrix \(\Pi (\epsilon '\mid \epsilon)\) that is identical across agents and over the life cycle.9 Note that these shocks are not to the stock of human capital (as, for example, in Huggett et al. (2011)).10

Market Structure. A full set of one-period Arrow securities is available for trade at every date and state, allowing markets to be dynamically complete. An Arrow security that promises to deliver one unit of consumption good in state \(\epsilon '\) tomorrow costs \(q(\epsilon '|\epsilon)\) in state \(\epsilon\) today. Letting \(q=1/(1+r)\) be the price of a riskless bond, no-arbitrage implies that the price of an Arrow security is given by \(q(\epsilon '|\epsilon)=q\Pi (\epsilon '|\epsilon)\) for all \(\epsilon\) and \(\epsilon '\). Individuals completely insure themselves against consumption risk by trading these securities. Hence, all individuals of a given type \(j\) will have the same (and constant) consumption over the life cycle. However, individuals will have different realized paths of investment, human capital, labor supply, and wages.

We assume that the interest rate, \(r\), is fixed and the same for all countries, which is consistent with (at least) two separate environments. First, each country can be viewed as a small open economy with the same constant-returns-to-scale aggregate production technology, which takes aggregate physical and human capital as inputs. In this case, all countries will face the same world interest rate. In the second specification, suppose that all countries use the same aggregate production technology, which is linear in physical and human capital inputs. In both specifications, the aggregate human capital is given by the sum of \(h\times \epsilon n(1-i)\) over all individuals.

Pension Benefits. It is easy to see from the discussion above of equations (5) and (7) that the existence of a redistributive pension system will have an effect similar to progressive taxation. In addition, the retirement pension system represents a major use of tax revenues collected by governments. Therefore, modeling pensions is important for capturing how funds are returned to households.

During retirement, individuals receive constant pension payments every period. Essentially, the pension of a worker with ability level \(j\) depends on two variables: (i) the average lifetime earnings of workers with the same ability level (denoted by \(\overline{y}^{j}\)), and (ii) the total number of years the worker had Social Security eligible earnings by the time he retired, denoted by \(m^{S}\). The pension function is denoted as \(\Omega (\overline{y}^{j},m^{S})\).11

The Tax System and the Government Budget. The government imposes a flat-rate consumption tax, \(\bar{\tau}_{c}\), in addition to the (potentially) progressive labor income tax, \(\bar{\tau}(y)\).12 The collected revenues are used to finance the benefits system and any residual budget surplus or deficit, \(Tr,\) is distributed in a lump-sum fashion to all households.13 Because prices are exogenously given, the only general equilibrium effect here is through the government budget.

2.4 Individuals’ Dynamic Program

Individuals solve the following problem (ability type \(j\) is suppressed for clarity):

\[ \begin{aligned} V(h,a,m;\epsilon,s) & = & \max _{c,n,i,a'(\epsilon ')}\left [u(c,n)+\beta E\left (V(h',a'(\epsilon '),m';\epsilon ',s+1)|\epsilon \right)\right]\\ \textrm{s.t}. \\ (1+\bar{\tau}_{c})c+\sum _{\epsilon '}q(\epsilon '\mid \epsilon)a'(\epsilon ') & = & (1-\bar{\tau}(y))y+a+Tr,\\ y & = & \epsilon h(1-i)n,\\ h' & = & (1-\delta)h+A(hin)^{\alpha},\\ m' & = & m+1\{i<1\;\&\;n\geq n_{\min}\},\\ i & \in & [0,\chi]\cup \{1\}, \end{aligned} \]

for \(s=1,2,...,S.\) Equation (13) shows how individuals accumulate years of service, \(m\). Specifically, individuals get one more year of service credit if they are not in school (\(i<1\)) and are employed more than a certain threshold number of hours: \(n>n_{\min}.\)

After retirement, individuals receive a pension and there is no human capital investment. Since there is no uncertainty during retirement, a riskless bond is sufficient for smoothing consumption. Therefore, the problem at age \(s=S+1,..,T\) can be written as

\[ \]

\[\begin{aligned} $$ W^{R}(a,\overline{y}^{j},m^{S};s) & =\max _{c,a'}\left [u(c,0)+\beta W^{R}(a',\overline{y}^{j},m^{S};s+1)\right]\\ \textrm{s.t}\qquad (1+\bar{\tau}_{c})c+qa' & =(1-\bar{\tau}(y_{s}))y_{s}+a+Tr \\ y_{s} & =\Omega (\overline{y}^{j},m^{S}). $$ \end{aligned}\]\[ \]

The definition of a stationary recursive competitive equilibrium in this environment is standard, so the formal statement is relegated to Appendix A.

3 Progressivity and Inequality: Two Empirical Facts

This section has two purposes. First, we discuss the derivation of country-specific tax schedules that are used in the rest of the paper. Using these tax schedules, we construct empirical measures of the two progressivity wedges defined in (6) and (8) above. Second, with these wedges on hand, we go on to document two new empirical relationships between wage inequality and the progressivity of (labor income) tax policy that are consistent with the presented model and further motivate the quantitative analysis that follows.

3.1 Deriving Country-Specific Tax Schedules

For each country, we follow the procedure described here. First, the OECD tax database provides estimates of the total labor income tax for all income levels between half of average wage earnings (hereafter, AW) to two times AW. The calculation takes into account several types of taxes (central government, local and state, social security contributions made by the employee, and so on), as well as many types of deductions and cash benefits (dependent exemptions, deductions for taxes paid, social assistance, housing assistance, in-work benefits, etc.).14 Using these estimates, we calculate the average labor income tax rate, \(\bar{\tau}(y)\), for 50%, 75%, 100%, 125%, 150%, 175%, and 200% of AW. However, tax rates beyond 200% of AW are also relevant when individuals solve their dynamic program. Fortunately, another piece of information is available from the OECD: the top marginal tax rate and the corresponding top bracket for each country. As described in more detail in Appendix B.1, we use this information to generate average tax rates at income levels beyond two times AW. Then, we fit the following smooth function to the available data points:15 \[ \bar{\tau}(y/AW)=a_{0}+a_{1}(y/AW)+a_{2}(y/AW)^{\phi}. \]

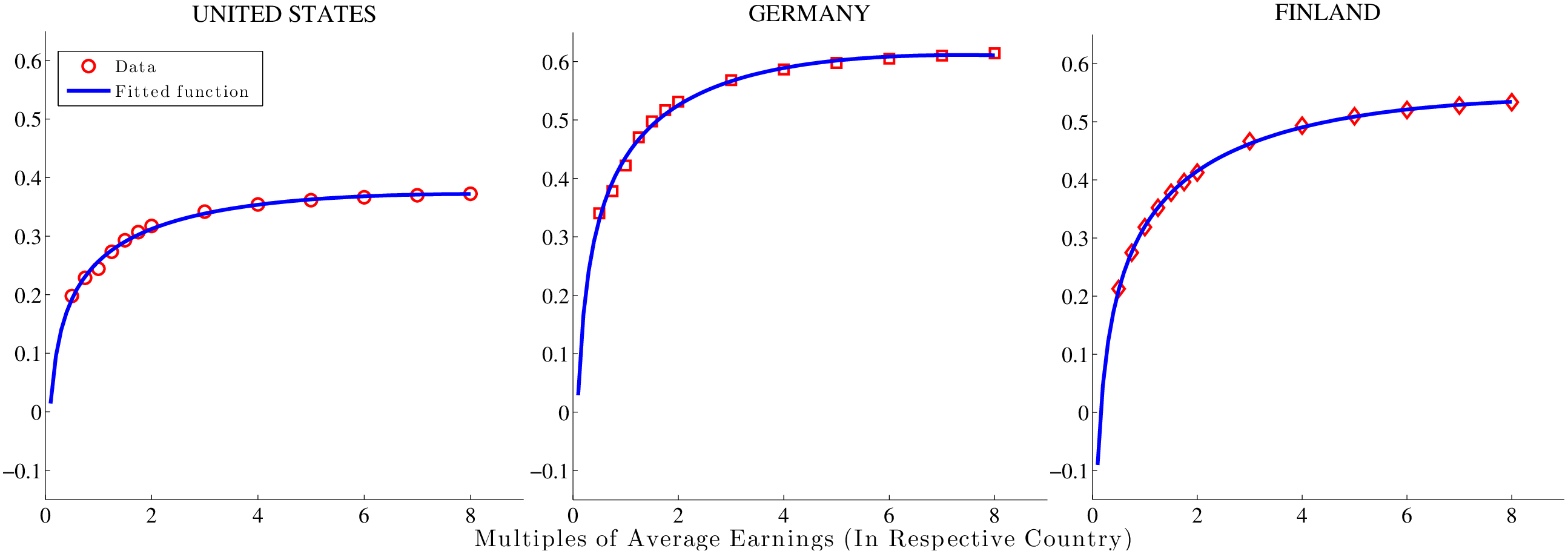

The parameters of the estimated \(\bar{\tau}(y)\) functions for all countries are reported in Appendix B.1, along with the \(R^{2}\) values. Although the assumed functional form allows for various possibilities, all fitted tax schedules turn out to be increasing and concave. The lowest \(R^{2}\) is 0.984 and the mean is 0.991, indicating a very good fit. In Figure 1, we plot the estimated functions for three countries: one of the two least progressive (United States), the most progressive (Finland), and one with intermediate progressivity (Germany).

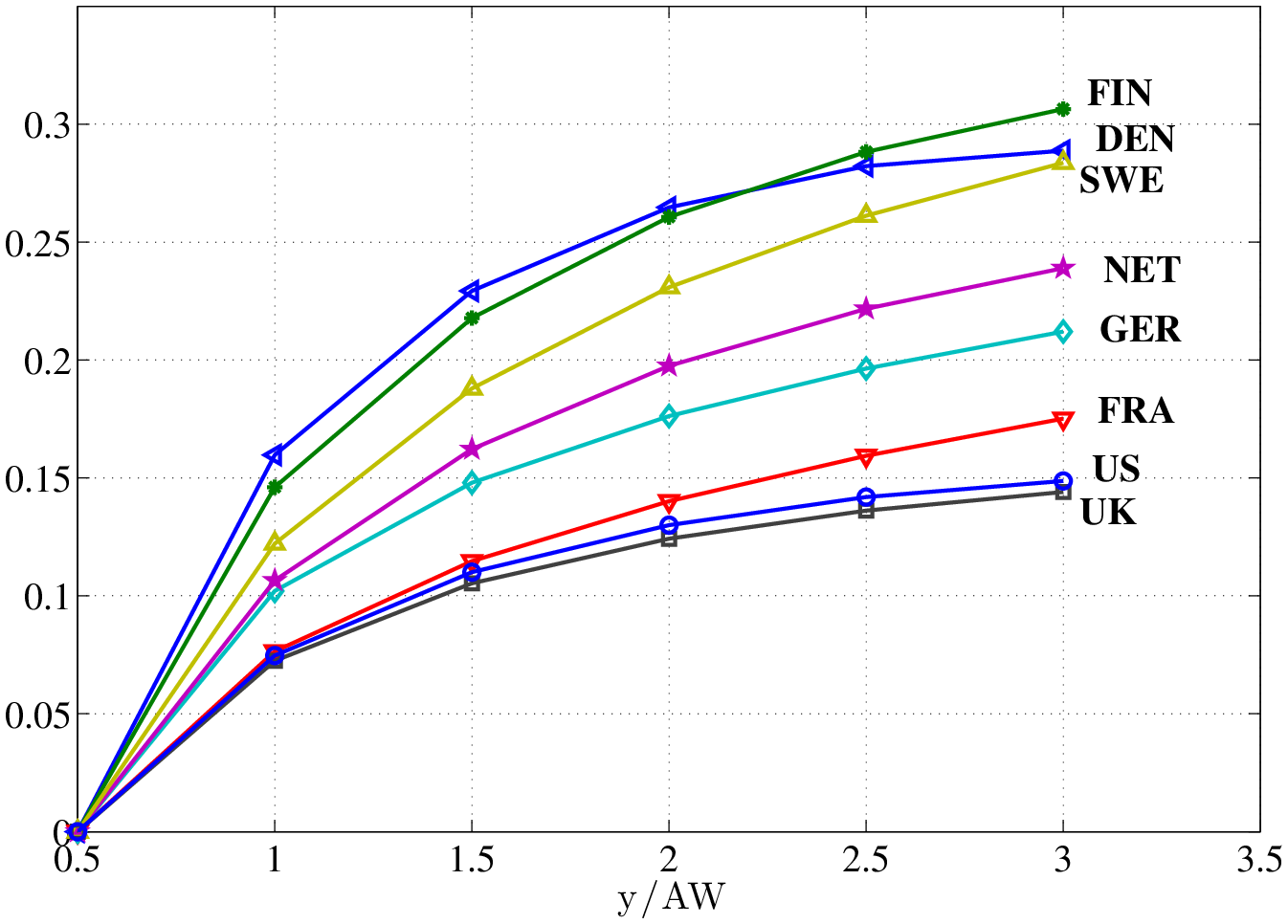

Figure 2 plots the progressivity wedges computed from the estimated tax schedules for all countries in our sample. Specifically, each line plots \(PW(0.5,0.5k)\) and \(k=1,2,...,6\), which are essentially the wedges faced by an individual who starts life at half the average earnings in that country and looks toward an eventual wage level that is up to six times his initial wage. As seen in the figure, countries are ranked in terms of their progressivity. Consistent with what one could conjecture, the US and the UK have the least progressive tax system, whereas Scandinavian countries have the most progressive ones, and larger continental European countries are scattered between these two extremes. The differences also appear quantitatively large (although a more precise evaluation needs to await the quantitative analysis in the next section): for example, the marginal benefit of investment for a young worker in the US who invests today when his wage is \(0.5\times AW\) and expects to earn \(2\times AW\) in the future is 13% lower than in a flat-tax system. The comparable loss is 27% in Denmark and Finland. These differences grow with the ambition level of the individual, dampening human capital investment, especially at the top of the distribution.

3.2 Taxes and Inequality: Cross-Country Empirical Facts

The wage inequality data come from the OECD’s Labour Force Survey database and are derived from the gross (before-tax) wages of full-time, full-year (or equivalent) workers.16 This is the appropriate measure for the purposes of this paper, as it more closely corresponds to the marginal product of each worker (and, hence, his wage) in the model. The fact that the inequality data pertain to before-tax wages is important to keep in mind; if the data were for after-tax wages, the correlation between progressivity and inequality would be mechanical and, thus, not surprising at all. Furthermore, we focus on male workers to avoid potential selection issues that may arise due to wide differences in female labor force participation rates across countries.

We normalize AW in each country to 1 and focus on \(PW(0.5,2.5)\) as the measure of progressivity. Similarly, when we calculate \(PW^{*}\) for a given country, we use the average hours per person in that country between 2001 and 2005 for \(n_{i}\) in equation (8), and the average of the same variable across all countries for \(n_{\text{avg}}.\)17 Finally, for brevity, in the rest of the paper we will refer to the “log 90-10 wage differential” simply as “L90-10,” and similarly for the other wage differentials.

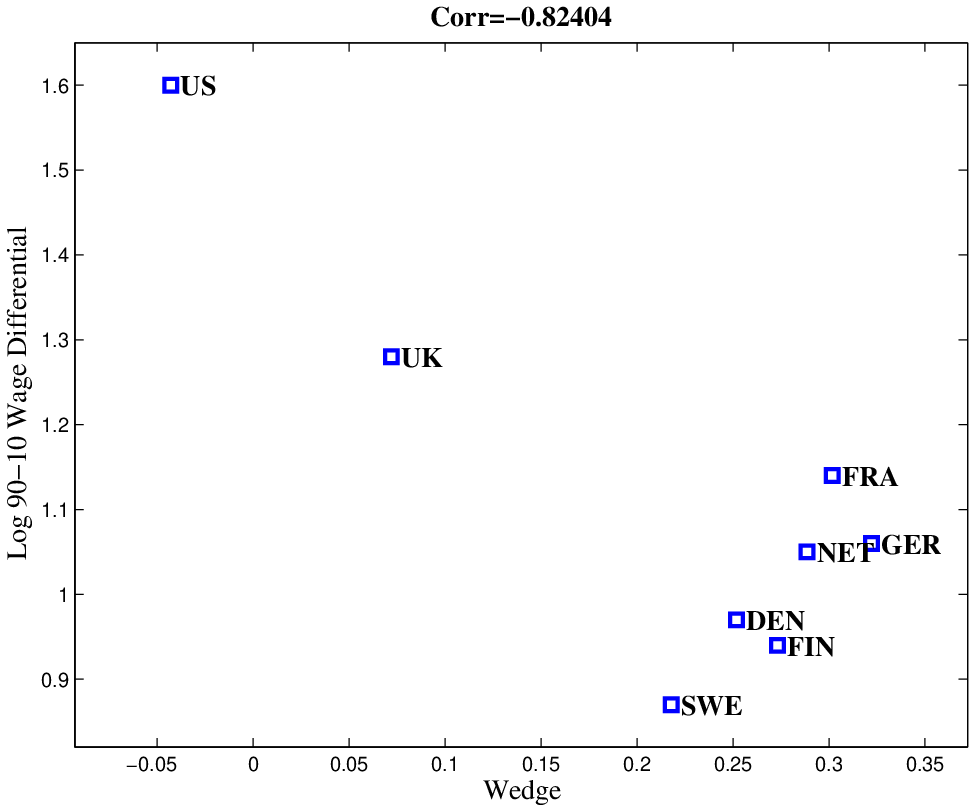

Figure 3 plots the relationship between L90-10 and the progressivity wedge in the 2000s. Countries with a smaller wedge—meaning a less progressive tax system and, therefore, a smaller distortion in human capital investment—have higher wage inequality. The relationship is also quite strong with a correlation of –0.82.18 (Repeating the same calculation using \(PW^{*}\) yields the same correlation.) Both relationships are consistent with the human capital model with progressive taxes presented above.

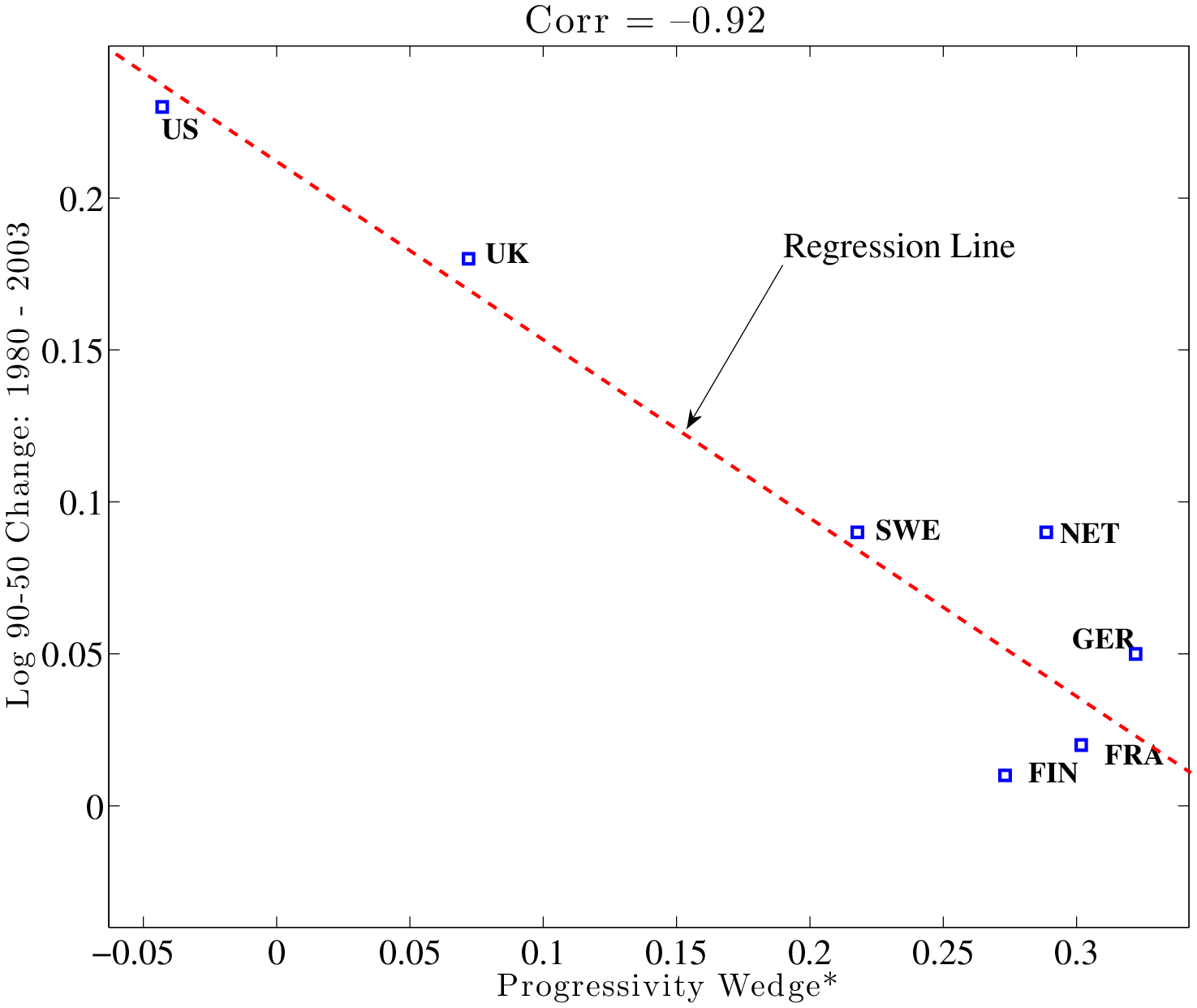

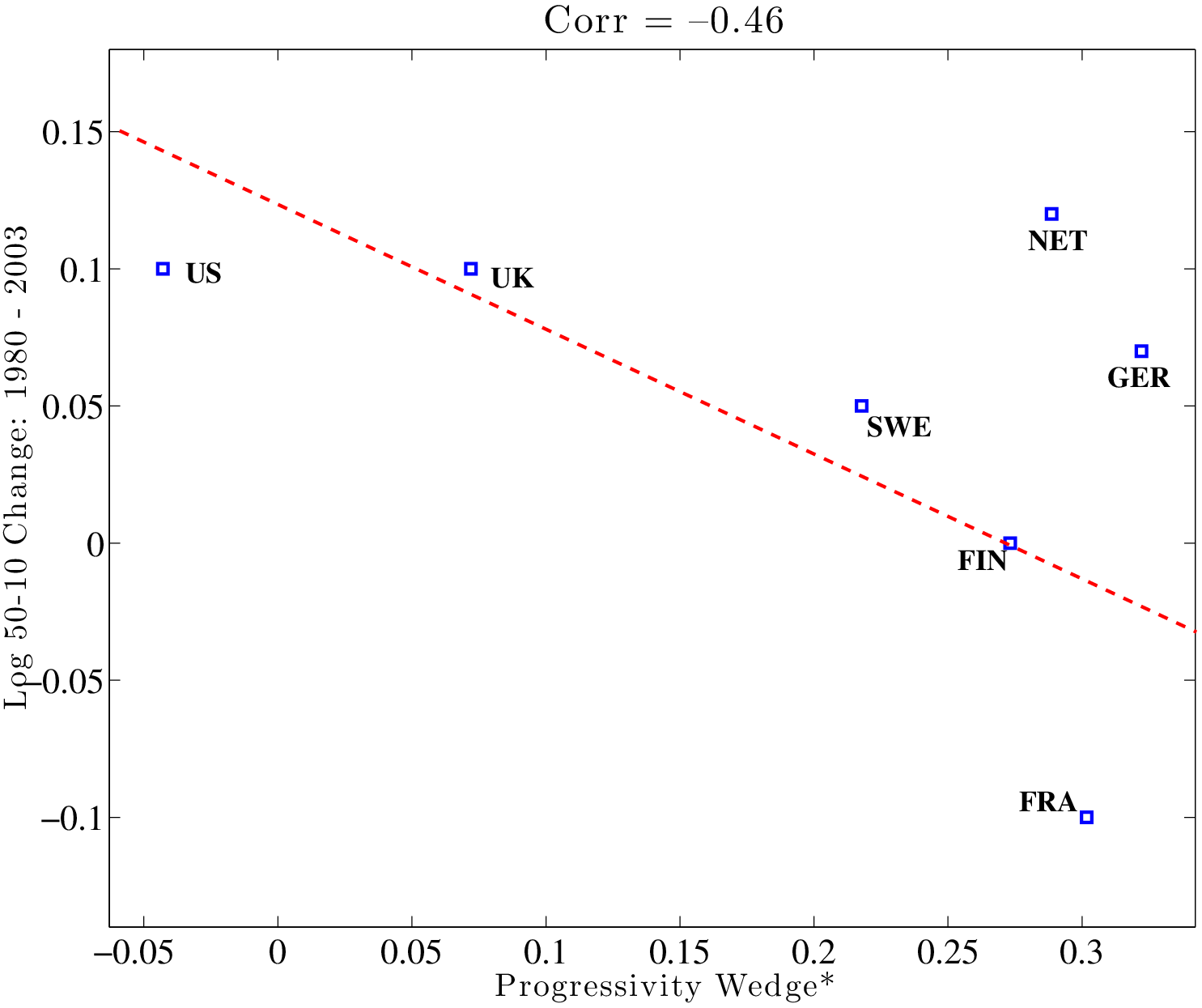

We next turn to the change in inequality over time. Figure 4 plots \(PW^{*}\) versus the change in L90-50 (left panel) and L50-10 (right panel). Countries with a more progressive tax system in the 2000s have experienced a smaller rise in wage inequality since the 1980s. The relationship is especially strong at the top of the wage distribution and weaker at the bottom: the correlation between progressivity and the change in L90-50 is very strong (\(-0.92\)), whereas the correlation with L50-10 is weaker (\(-0.46\)); see Figure 4. This result is consistent with the idea that the distortion created by progressivity is likely to be effective especially strongly at the upper end, where human capital accumulation is an important source of wage inequality, but less so at the lower end, where other factors, such as unionization, minimum wage laws, and so on, could be more important.

Finally, Table 2 gives a more complete picture of the differences between the two definitions of wedges. The top panel reports the correlation of each wedge measure with log wage differentials, which reveals that the adjustment for utilization rates through labor hours makes little difference in the correlations in 2003. Turning to the change in inequality over time (bottom panel), the simple wedge measure has a somewhat lower correlation with log wage differentials. However, adjusting for average hours per person strengthens these correlations to \(-0.77\) for the L90-10, and to \(-0.92\) for L90-50 (plotted in the left panel of Figure 4). We conclude that progressivity is strongly correlated with inequality both in the cross-section and over time, especially above the median of the distribution.

Overall, these findings reveal a close relationship between progressivity and wage inequality, which motivates the focus of this paper. However, on their own, these correlations fall short of providing a quantitative assessment of the importance of the tax structure. For this purpose, we now take the model to the data.

| Measure of Wedge: | ||

| \(PW(0.5,2.5)\) | \(PW^{*}(0.5,2.5)\) | |

| Wage differential | ||

| in 2003: | ||

| \(\quad\)L90-10 | \(-.82\) | \(-.82\) |

| \(\quad\)L90-50 | \(-.84\) | \(-.67\) |

| \(\quad\)L50-10 | \(-.72\) | \(-.85\) |

| \(\Delta\) Wage differential | ||

| from 1980 to 2003: | ||

| \(\quad\)L90-10 | \(-.45\) | \(-.77\) |

| \(\quad\)L90-50 | \(-.67\) | \(-.92\) |

| \(\quad\)L50-10 | \(-.16\) | \(-.46\) |

4 Parameter Choices

We now discuss the parameter choices for the model. First, our quantitative analysis focuses on steady states of the model described in Section 2. Second, we focus on male workers so as to avoid potential selection issues across countries related to different labor market participation rates for female workers. Our basic calibration strategy is to take the United States as a benchmark and pin down a number of parameter values by matching certain targets in the US data.19 We then assume that other countries share the same parameter values with the US along unobservable dimensions (such as the distribution of learning ability), but differ in the dimensions of their labor market policies that are feasible to model and calibrate (specifically, consumption and labor income tax schedules and the retirement pension system). We then examine the differences in economic outcomes—specifically in wage dispersion and labor supply—that are generated by these policy differences alone.

A model period corresponds to one year of calendar time. Individuals enter the economy at age 20 and retire at 65 (\(S=45\)). Retirement lasts for 20 years and everybody dies at age 85. The net interest rate, \(r\), is set equal to 2%, and the subjective time discount rate is set to \(\beta =1/\left (1+r\right)\). The curvature of the human capital accumulation function, \(\alpha,\) is set equal to 0.80, broadly consistent with the existing empirical evidence (see Browning et al. (1999), Table 2.3). In Appendix E, we conduct sensitivity analyses with respect to \(\alpha\) and consider cross-country variation in retirement age \(S\).

Utility Function. Preferences over consumption, \(c,\) and leisure time, \(1-n,\) are given by this common separable form: u(c,n)=(c)+.

This specification yields two parameters to calibrate: the curvature of leisure, \(\varphi,\) and the utility weight attached to leisure, \(\psi\). These parameters are jointly chosen to pin down the average hours worked in the economy, as well as the average Frisch labor supply elasticity. In 2003, the average annual hours worked by American males was 1,890 hours, or approximately 5.2 hours per day (Heathcote et al. (2010), figure 2). Taking the discretionary time endowment of an individual to be 13 hours per day, we get \(\overline{n}=5.2/13=0.4\).20

With power utility, the theoretical Frisch elasticity of labor supply is given by \((1-n)/(n\varphi).\) Because in this model, labor supply, \(n\), varies across individuals, there is a distribution of Frisch elasticities. We simply target the Frisch elasticity implied by the average labor hours, \(\overline{n}\). The empirical target we choose is 0.3, which is consistent with the estimates for male workers surveyed by Browning et al. (1999), which range from zero to 0.5.21 As will become clear in the sensitivity analysis conducted below, the model’s performance improves with a higher elasticity, so we opt for a more conservative value in our baseline calibration.

| Parameter | Description | Value | ||

| \(\varphi\) | Curvature of utility of leisure | \(5.0\) (Frisch = 0.3) | ||

| \(\psi\) | Weight on utility of leisure | \(0.20\) | ||

| \(\alpha\) | Curvature of human capital function | $0.$80 | ||

| \(S\) | Years spent in the labor market | \(45\) | ||

| \(T-S\) | Retirement duration (years) | \(20\) | ||

| \(r\) | Interest rate | \(0.02\) | ||

| \(\beta\) | Time discount factor | \(1/(1+r)\) | ||

| \(\delta\) | Depreciation rate of skills (annual) | \(1.5\%\) | ||

| \(E\left [h^{j}_{0}\right]\) | Average initial human capital (scaling) | \(4.95\) | ||

| Parameters calibrated to match data targets | ||||

| \(E\left [A^{j}\right]\) | Average ability | \(0.195\) | ||

| \(\sigma \left (h^{j}_{0}\right)/E\left [h^{j}_{0}\right]\) | Coeff. of variation of initial human capital | \(0.076\) | ||

| \(\sigma \left [A^{j}\right]/E\left [A^{j}\right]\) | Coeff. of variation of ability | \(0.396\) | ||

| \(\gamma\) | Dispersion of Markov shock | \(0.23\) | ||

| \(p\) | Transition probability for Markov shock | \(0.90\) | ||

| \(\chi\) | Maximum investment time on the job | 0\(.50\) | ||

Distributions: Learning Ability, Initial Human Capital, and Shocks. Agents have two individual-specific attributes at the time they enter the economy: learning ability and initial human capital endowment. We assume that these two variables are jointly uniformly distributed in the population and are perfectly correlated with each other.22 Although the assumption of perfect correlation is made partly for simplicity, a strong positive correlation is plausible and can be motivated as follows. The present model is interpreted as applying to human capital accumulation after age 20 and, by that age, high-ability individuals will have invested more than those with low ability, leading to heterogeneity in human capital stocks at that age, which would then be very highly correlated with learning ability. Indeed, Huggett et al. (2011) estimate the parameters of the standard Ben-Porath model from individual-level wage data and find learning ability and human capital at age 20 to be strongly positively correlated (corr: 0.792). Making the slightly stronger assumption of perfect correlation allows us to collapse the two-dimensional heterogeneity in \(A^{j}\) and \(h^{j}_{0}\) into one, speeding up computation significantly.

Therefore, this jointly uniform distribution of \((A^{j},h^{j}_{0})\) yields four parameters to be calibrated. \(E\left [h^{j}_{0}\right]\) is a scaling parameter and is simply set to a computationally convenient value, leaving three parameters: (i) the cross-sectional standard deviation of initial human capital, \(\sigma \left (h^{j}_{0}\right),\) (ii) the mean learning ability, \(E\left [A^{j}\right]\), and (iii) the dispersion of ability, \(\sigma \left (A^{j}\right).\) The idiosyncratic shock process, \(\epsilon,\) is assumed to follow a first-order Markov process, with two possible values, \(\left \{1-\gamma,1+\gamma \right \}\), and a symmetric transition matrix with \(\Pr (\epsilon '=x|\epsilon =x)=p\). This structure yields two more parameters, \(\gamma\) and \(p\), to be calibrated—for a total of five parameters. The sixth and last parameter is \(\chi\) (maximum investment allowed on the job). Finally, because there is measurement error in individual-level wage data, we add a zero mean i.i.d. disturbance to the wages generated by the model (which has no effect on individuals’ optimal choices).

Data Targets. Our calibration strategy is to require that the wages generated by the model be consistent with micro-econometric evidence on the dynamics of wages found in panel data on US households. Specifically, these empirical studies begin by writing a stochastic process for log wages (or earnings) of the following general form:

\[ \]

\[\begin{aligned} $$ \log \widetilde{w}^{j}_{s} & =\underset{\textrm{systematic comp.}}{\underbrace{\left [a^{j}+b^{j}s\right]}}+\underset{\textrm{stochastic comp.}}{\underbrace{z^{j}_{s}+\varepsilon ^{j}_{s}}}\\ z^{j}_{s} & =\rho z^{j}_{s-1}+\eta ^{j}_{s}, $$ \end{aligned}\]\[ \]

where \(\widetilde{w}^{j}_{s}\) is the “wage residual” obtained by regressing raw wages on a polynomial in age; the terms in brackets, \(\left [a^{j}+b^{j}s\right]\), capture the individual-specific systematic (or life cycle) component of wages that result from differential human capital investments undertaken by individuals with different ability levels, and \(z^{j}_{s}\) is an AR(1) process with innovation \(\eta ^{j}_{s}\). Finally, \(\varepsilon ^{j}_{s}\) is an iid shock that could capture classical measurement error that is pervasive in micro data and/or purely transitory movements in wages. For concreteness, in the discussion that follows, we refer to the first two terms in brackets as the “systematic component” of wages and to the latter two terms as the “stochastic component.”

We begin with \(\varepsilon _{s}\) and assume that it corresponds to the measurement error in the wage data. Based on the results of the validation studies from the US wage data,23 we take the variance of the measurement error to be 10% of the true cross-sectional variance of wages in each country, which yields \(\sigma ^{2}_{\varepsilon}=0.034\) for the United States. We then choose the following six moments from the US data to pin down the six parameters identified earlier:

- the mean log wage growth over the life cycle (informative about \(E(A^{j})\)),

- the ratio of minimum to mean wage (informative about \(\chi\)),

- the cross-sectional dispersion of wage growth rates, \(\sigma (b^{j})\) (informative about \(\sigma (A^{j})\)),

- the cross-sectional variance of the stochastic component (informative about \(\gamma\)),

- the average of the first three autocorrelation coefficients of the stochastic component of wages (informative about \(p\)), and

- L90-10 in the population (which, together with the previous moments, is informative about \(\sigma (h^{j}_{0})\)).

The target value for the mean log wage growth over the life cycle (i.e., the cumulative growth between ages 20 and 55) is 45%. This number is roughly the middle point of the figures found in studies that estimate lifecycle wage and income profiles from panel data sets, such as the Panel Study of Income Dynamics (PSID); see, for example, Gourinchas and Parker (2002) and Guvenen (2007). The second data moment is the legal minimum wage in the economy relative to the average wage of full-time workers, which, according to the OECD,24 was 0.29 for the US in the early 2000s. The third moment is the cross-sectional standard deviation of wage growth rates, \(\sigma (b^{j})\). The estimates of this parameter are quite consistent across different papers, regardless of whether one uses wages or earnings. We take our empirical target to be 2%, which represents an average of these available estimates (Baker (1997), Haider (2001), and Guvenen (2009)).

The next two moments capture key statistical properties of the stochastic component of wages in the data. These moments are (i) the unconditional variance of the stochastic component, (\(z_{s}+\varepsilon _{s}\)), as well as (ii) the average of its first three autocorrelation coefficients. The empirical counterparts for these moments are taken from Haider (2001), which is the only study that estimates a process for hourly wages and allows for heterogeneous profiles. The figure for the unconditional variance can be calculated to be 0.109 and the average of autocorrelations is calculated to be 0.33, using the estimates in Table 1 of Haider’s paper. Further details and justifications for these parameter choices are in Appendix D.25

Our sixth, and final, moment is L90-10 in 2003. Adding this moment ensures that the calibrated model is consistent with the overall wage inequality in the US in that year, which is the benchmark against which we measure all other countries. The empirical target value is 1.60 (from the OECD’s Labour Force Survey). Table 4 displays the empirical values of the six moments, as well as their counterparts generated by the calibrated model. As can be seen here, all moments are matched fairly well.

One point to note is that even though the average of the first three autocorrelation coefficients is pretty low (0.33), the stochastic component includes measurement error as well, which is i.i.d. The Markov shocks themselves have a first order annual autocorrelation of 0.80 (implied by \(p=0.90\), shown in Table 3).

| Moment | Data | Model |

| Mean log wage growth from age 20 to 55 | 0.45 | 0.44 |

| Ratio of minimum to mean wage rate | 0.29 | 0.30 |

| Cross-sectional standard deviation of wage growth rates | 2.00% | 2.03% |

| Cross-sectional variance of stochastic component | 0.109 | 0.106 |

| Average of first three autocorrelation coeff. of stochastic component | 0.33 | 0.34 |

| L90-10 in 2003 | 1.60 | 1.60 |

Benefits System and the Government Budget. Pension systems vary greatly across countries in their generosity, their duration, as well as in how much redistribution they entail. We provide the exact formulas for the pension system of each country in Appendix B.4. Whatever surplus (or deficit) remains in the budget after the benefits is distributed to (or collected from) individuals in a lump-sum manner.26

Consumption Taxes. The average tax rate on consumption is taken from McDaniel (2007), who provides estimates for 15 OECD countries for the period 1950 to 2003 by calculating the total tax revenue raised from different types of consumption expenditures and dividing this number by the total amount of corresponding expenditure. McDaniel (2007) does not provide an estimate for Denmark, so we set this country’s consumption tax equal to that of Finland, which has a comparable value-added tax (VAT) rate.

5 Quantitative Results

In this section, we begin by presenting the implications of the calibrated model for wage inequality differences across countries at a point in time. We then provide decompositions that quantify the separate effects of progressivity, average income tax rates, consumption taxes, and the pension system on these results. We next turn to the change in inequality over time and provide a comparison between the United States and Germany from 1983 to 2003. The model statistics below are computed from 10,000 simulated lifecycle paths for individuals drawn from the joint probability distribution of \((A^{j},h^{j}_{0})\).

5.1 Cross-Sectional Results: the 2000s

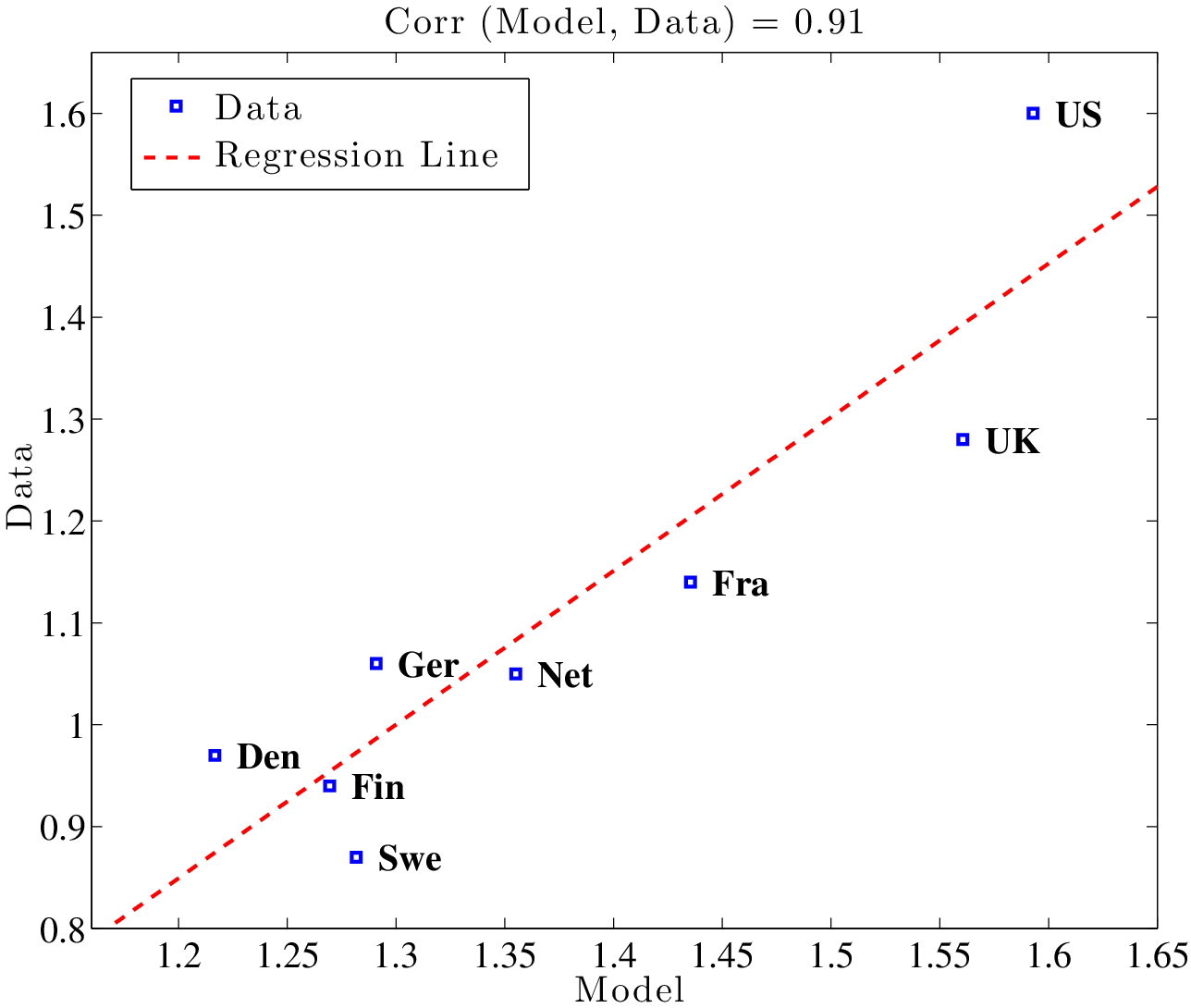

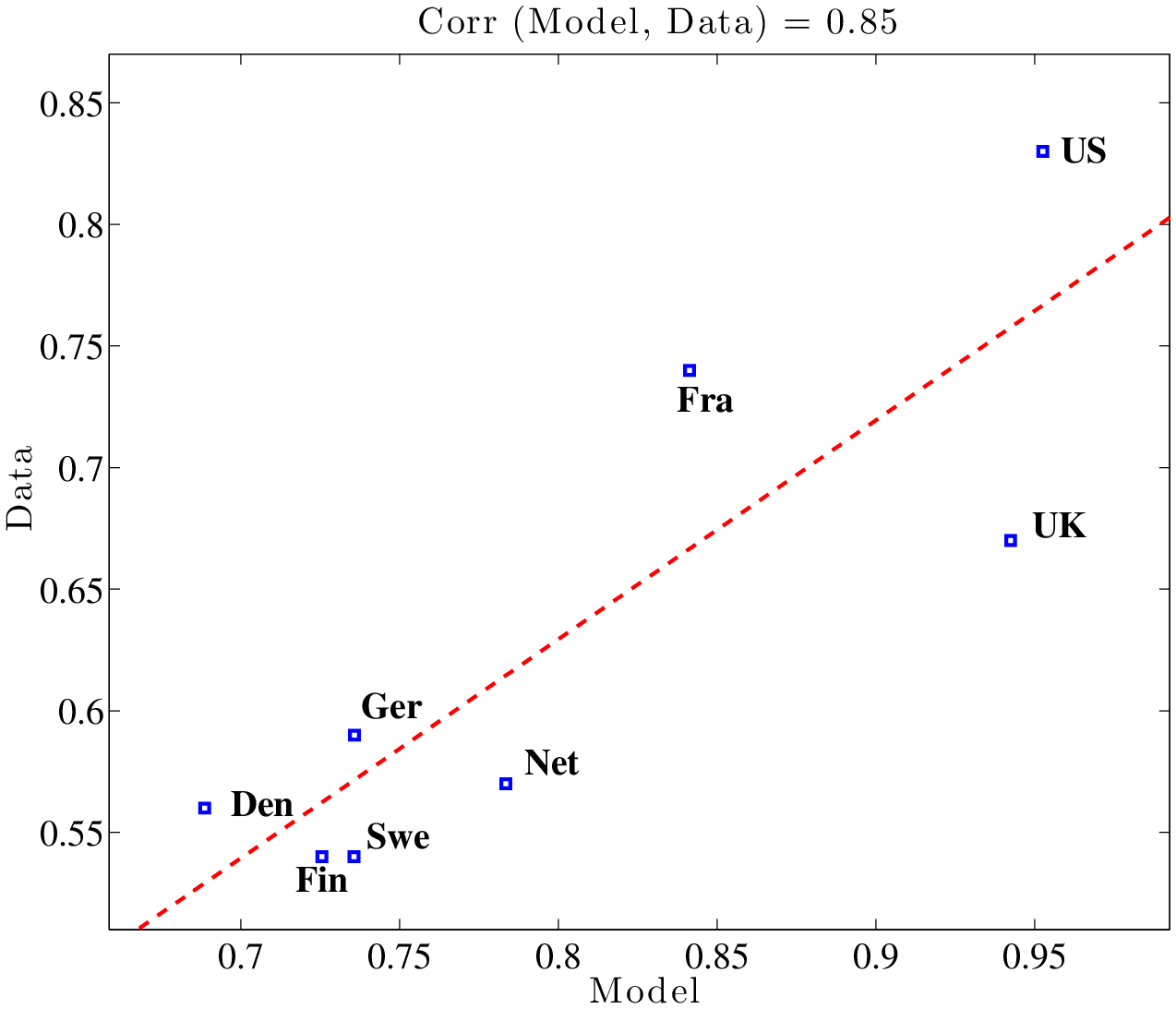

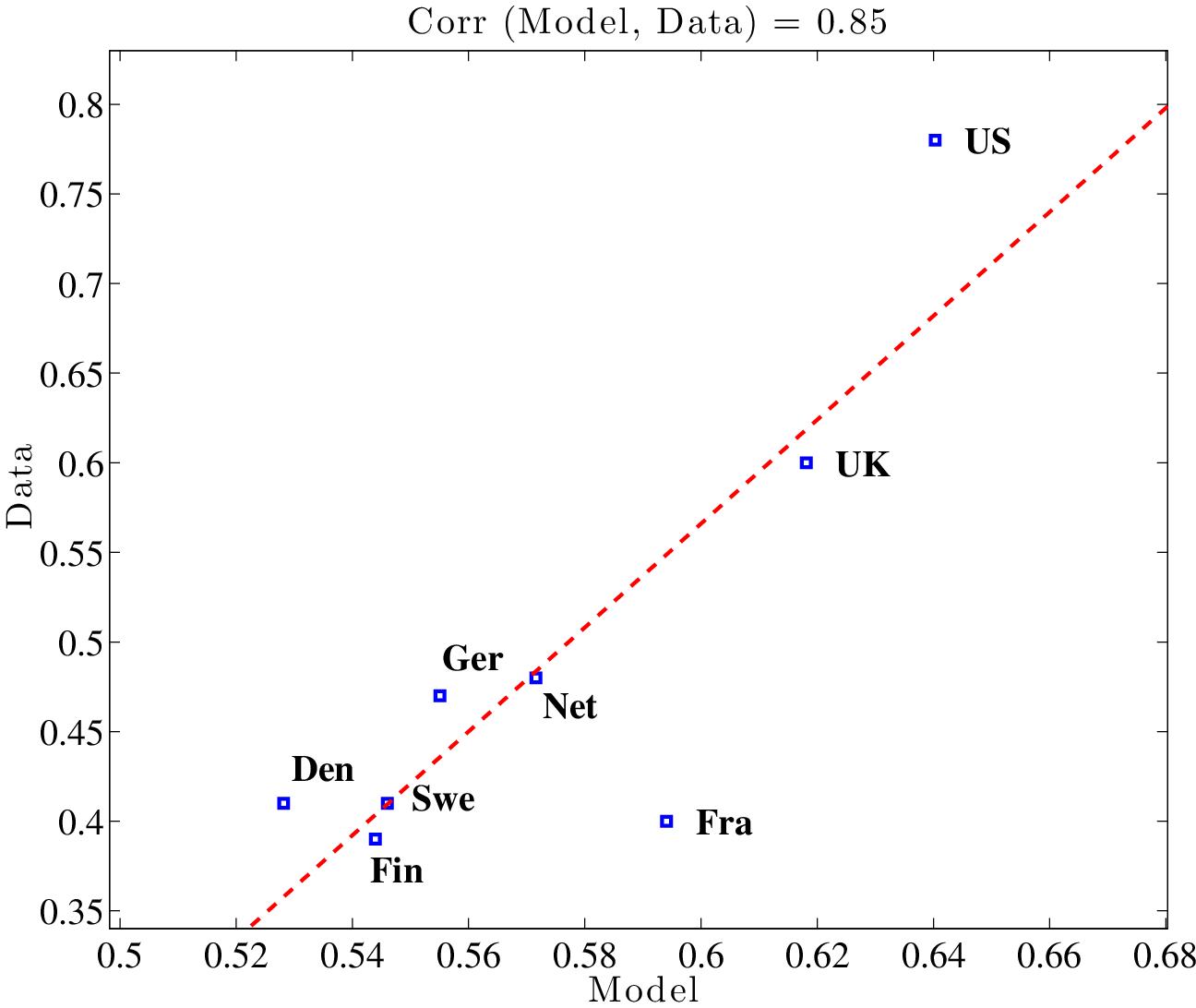

Figure 5 plots L90-10 for each country in the data against the value predicted by the calibrated model. The correlation between the simulated and actual data is 0.91 (and the countries line up nicely along the regression line), suggesting that the model is able to capture the relative ranking of these eight countries in terms of overall wage inequality observed in the data. To explore how the model fares at different parts of the wage distribution, the middle panel of Figure 5 repeats the same exercise for L90-50 and the bottom panel does the same for L50-10. In both cases, the model-data correlations are high: 0.85.

In Table 5, we quantify the importance of taxes for cross-country differences in inequality. The first two columns report L90-10 in the data for all countries, first in levels (second column) and then expressed as a deviation from the US, which is our benchmark country (third column). For example, in Denmark L90-10 is 0.97, which is 0.63 (i.e., 63 log points) lower than that in the US. The third and fourth columns display the corresponding statistics implied by the calibrated model. Again, for Denmark, the model generates an L90-10 that is 0.38 below what is implied by the model for the US. Therefore, the model accounts for 60% (\(=38/63\)) of the difference in L90-10 between the US and Denmark, reported in column (e). Similar comparisons show that the model does quite well in explaining the level of wage inequality in Germany but poorly in explaining the UK. The fraction explained by the model ranges from 35% for France to 56% for Germany. Overall, the model accounts for 48% of the actual gap in inequality between the US and the CEU in 2003.

To see which part of the wage distribution is better captured by the model, the next two columns display the same calculation performed in column (e), but now separately for L90-50 (f) and L50-10 (g). For all countries in the CEU, the model explains the upper tail inequality much better than the lower tail inequality. For example, for Denmark, the model explains 97% of L90-50 versus only 31% of L50-10. In fact, the model accounts for at least 65% of L90-50 for all countries in the CEU, averaging 84% across all countries, whereas it accounts for on average only 24% of L50-10. That our model does a better job at explaining inequality at the upper end (above the median) will be a recurring theme of this paper. This finding is consistent with the idea that progressive taxation affects the human capital investment of high-ability individuals more than others and, therefore, the mechanism is more effective above the median of the wage distribution.27 Finally, a notable exception to these generally strong findings is the UK, which is an important outlier: the model explains very little of the difference between the UK and US at the upper tail (6% to be exact) and only slightly more (13%) at the lower end.

| L90-10 | L90-50 | L50-10 | |||||

| Data | Model | % explained | % exp. | % exp. | |||

| Level | \(\Delta\) from US | Level | \(\Delta\) from US | (d)/(b) | |||

| (a) | (b) | (c) | (d) | (e) | (f) | (g) | |

| Denmark | 0.97 | 0.63 | 1.22 | 0.38 | 0.60 | 0.97 | 0.31 |

| Finland | 0.94 | 0.66 | 1.27 | 0.33 | 0.49 | 0.78 | 0.25 |

| France | 1.14 | 0.46 | 1.44 | 0.16 | 0.35 | 1.23 | 0.12 |

| Germany | 1.06 | 0.54 | 1.29 | 0.30 | 0.56 | 0.90 | 0.28 |

| Netherlands | 1.05 | 0.55 | 1.36 | 0.24 | 0.43 | 0.65 | 0.23 |

| Sweden | 0.87 | 0.73 | 1.28 | 0.31 | 0.43 | 0.75 | 0.26 |

| CEU | 1.00 | 0.59 | 1.31 | 0.29 | 0.48 | 0.84 | 0.24 |

| UK | 1.28 | 0.32 | 1.56 | 0.03 | 0.10 | 0.06 | 0.13 |

| US | 1.60 | 0.00 | 1.60 | 0.00 | – | – | – |

Decomposing the Effects of Different Policies. The baseline model incorporates several differences between the labor market policies of the US and those of the CEU countries. Here, we quantify the separate roles played by each of these components for the results presented in the previous section. We conduct three decompositions. First, we assume that countries in the CEU have the same retirement pension system as the US but differ in all other dimensions considered in the baseline model. This experiment separates the role of the tax system for wage inequality from that of the pension system. Second, we also set the consumption taxes of each country equal to that in the US, but each country retains its own income tax schedule as in the baseline model. This experiment quantifies the explanatory power of the model that is coming from the income tax system alone. Third, we go one step further and assume that each country keeps the same progressivity of its income tax schedule but is identical in all other ways to the US, including the average income tax rate. This experiment isolates the role of progressivity alone. In each case, we adjust the lump-sum transfers to balance the government’s budget.

Table 6 reports the results. First, in column 2, we assume that all countries have the same pension system as the US. In panel A, the correlation between the data and model is only slightly lower than in the baseline case for all parts of the wage distribution. Turning to panel B, the fraction of the US-CEU difference explained by the model goes down—but only slightly—indicating that more than 95% of the model’s explanatory power is coming from taxes (both income and consumption taxes). Next, in column (3), we also eliminate the differences in consumption taxes across countries. The model-data correlations go further down but, again, somewhat modestly. In panel B, the explanatory power of the model that is attributable to income taxes alone ranges from 75% to 80% for the three measures of wage inequality. The difference between columns 2 and 3 provides a useful measure of the role of consumption taxes, which account for about 17% (\(=96\%-79\%\)) of the model’s explanatory power for L90-10.

| Benchmark | All taxes | Lab. Inc. Tax | Progressivity | |

| Diff. from Benchmark: | (1) | (2) | (3) | (4) |

| Progressivity | — | — | — | — |

| Average income taxes | — | — | — | set to US |

| Consumption tax | — | — | set to US | set to US |

| Benefits institutions | — | set to US | set to US | set to US |

| A. Correlation Between Data and Model | ||||

| 90-10 | 0.91 | 0.90 | 0.85 | 0.88 |

| 90-50 | 0.85 | 0.87 | 0.85 | 0.87 |

| 50-10 | 0.85 | 0.84 | 0.78 | 0.81 |

| B. Fraction of US-CEU Difference Explained by Model | ||||

| 90-10 | 0.48 | 0.46 (96%) \(^{\textrm{a}}\) | 0.38 (79%) | 0.32 (67%) |

| 90-50 | 0.84 | 0.79 (94%) | 0.67 (80%) | 0.55 (66%) |

| 50-10 | 0.24 | 0.23 (96%) | 0.18 (75%) | 0.16 (67%) |

a The numbers in parentheses express the fraction explained by the model in each column as a percentage of the benchmark case reported in column (1).

Next, we investigate whether the power of income taxes comes from differences in the average rates across countries or from differences in the progressivity structure. In other words, if continental Europe differed from the US only in the progressivity of its labor income tax system—but had the same average tax rate on labor income—how much of the differences in wage inequality found in the baseline model would still remain? To answer this question, we proceed as follows. First, adjusting the average tax rate to the US level—without affecting progressivity—requires some care. We show in Appendix B.2 how this can be accomplished. Then, using these hypothetical tax schedules, we solve each country’s problem, assuming that all countries have identical labor market policies (set to the US benchmark) and their tax schedules generate the same average tax rate as in the US when using individuals’ choices made using the US income tax schedule. In panel B of column 4, we see that progressivity alone is responsible for 2/3 of the explanatory power of the model for L90-10.

Notice that the decomposition we conducted here is not invariant to the order in which different features are eliminated. So, a valid question is whether this conclusion—that average tax rate differences do not matter much—is robust to changing this order. To investigate this, we repeated the last experiment reported in column 4, but instead of eliminating average tax rate differences and keeping progressivity intact, we flipped the order (same progressivity as the US, but match each country’s average tax rate). In this case, the model only accounts for 14% of L90-10 differences, 20% of L90-50, and 10% of L50-10. This experiment confirms our previous conclusion that average tax rate differences are responsible for only a small fraction of the differences in wage inequality.

In summary, the pension system and consumption taxes together are responsible for about 20% of the model’s explanatory power. The more important finding concerns the role of progressivity, which, for all practical purposes, is the key component of the income tax structure for understanding wage inequality differences. Differences in the average income tax rate do not appear to be very important for inequality differences.

The Role of Labor Supply Elasticity. We now conduct two sensitivity analyses with respect to the value of labor supply elasticity: we consider (i) the case with a high Frisch elasticity of 0.5 and (ii) the case with only an extensive margin: \(n\in \{0,0.40\}\). In each case, the model is recalibrated to match the same six targets in Table 4. (Appendix E contains further sensitivity analyses with respect to the values of \(\alpha,\delta\), \(\chi\), \(G\), as well as the treatment of capital income taxes.)

| Frisch = 0.5 | Discrete hours: \(n\in \{0,0.40\}\) | |||||

| L90-10 | L90-50 | Log 50-10 | L90-10 | L90-50 | Log 50-10 | |

| (a) | (b) | (c) | (d) | (e) | (f) | |

| Denmark | 0.69 | 1.07 | 0.40 | 0.34 | 0.53 | 0.21 |

| Finland | 0.57 | 0.88 | 0.31 | 0.29 | 0.43 | 0.17 |

| France | 0.39 | 1.32 | 0.16 | 0.17 | 0.56 | 0.07 |

| Germany | 0.68 | 1.01 | 0.40 | 0.29 | 0.42 | 0.17 |

| Netherlands | 0.48 | 0.70 | 0.27 | 0.27 | 0.38 | 0.17 |

| Sweden | 0.52 | 0.87 | 0.33 | 0.22 | 0.38 | 0.15 |

| CEU | 57% | 94% | 31% | 26% | 44% | 16% |

| UK | 13 | 6 | 17 | 2 | –3 | 6 |

In the first experiment we set \(\varphi =3.0,\) which implies a Frisch elasticity of 0.5. Table 7 reports the counterpart of the analysis we conducted for the benchmark model and reported in Table 5. Comparing the two tables makes it clear that a higher Frisch elasticity improves the model’s explanatory power across the board. Now the model can explain 57% of the US-CEU difference in L90-10 (compared with 48% in the benchmark case) and 94% of the upper tail inequality (from 84% before). However, the improvement in L50-10 is modest, going from 24% in the benchmark case up to 31%.

To better understand the role of the intensive margin of labor supply, we now examine another case where workers can only choose between full-time employment at fixed hours (\(n=0.40\)) and nonemployment. The parameters of the utility function are the same as in the baseline case. The results are reported in the last three columns of Table 7. Without the amplification provided by an intensive margin—and the resulting dispersion in hours across countries—the explanatory power of the model falls and, in some cases, it falls significantly. For example, the model accounts for 26% of the difference in L90-10. For the upper-end inequality, the difference is even larger: the model now explains 44%, half of the baseline value, and also much lower than the 94% in the high Frisch case. Finally, the already low explanatory power at the lower tail falls further from 24% in the baseline case to 16%.

These findings underscore the importance of the interaction of endogenous labor supply choice (with an intensive margin) with progressive taxation for understanding wage inequality differences across countries, especially above the median of the distribution.

5.2 Inequality Trends over Time: 1983–2003

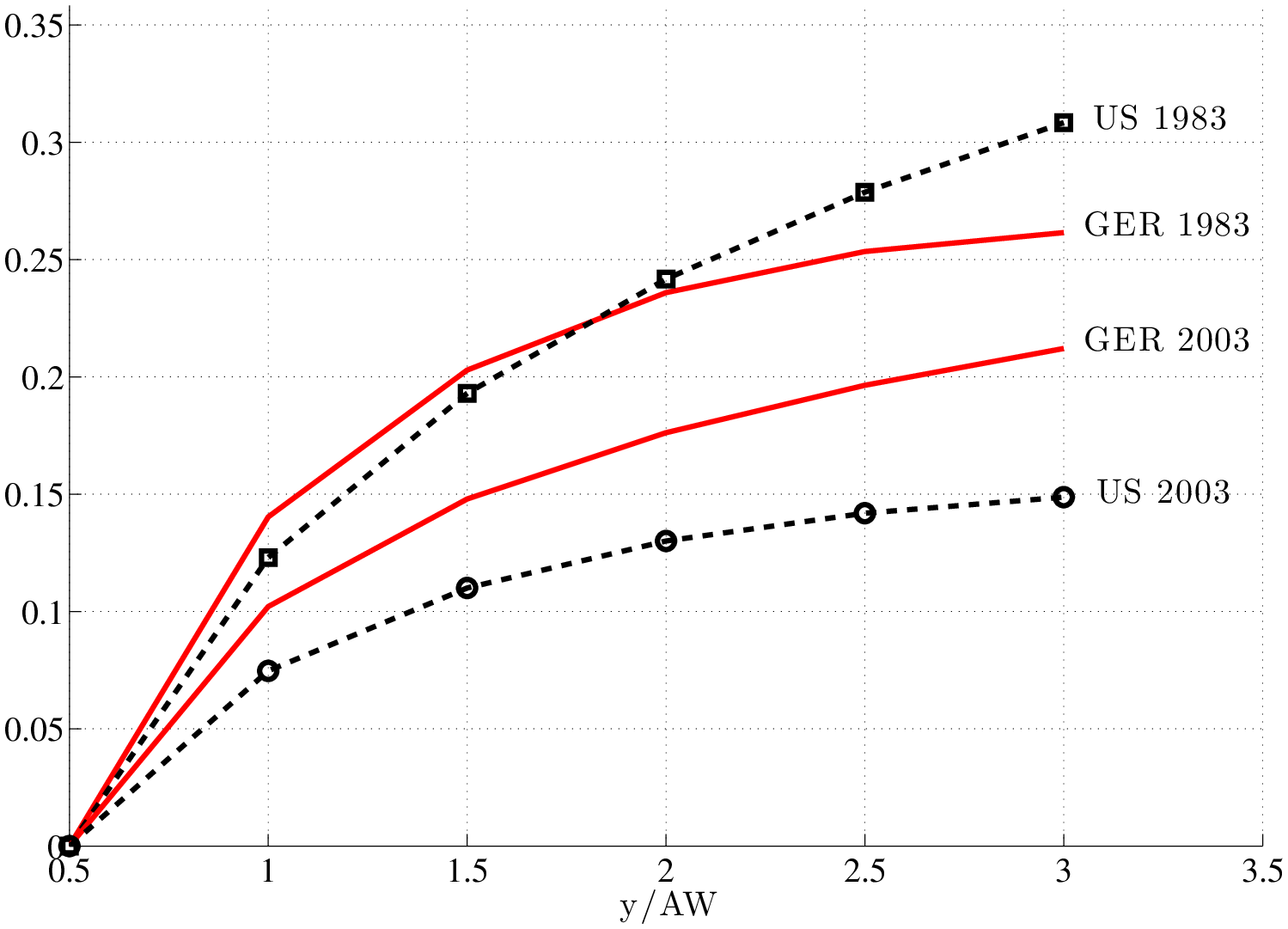

We now turn from levels in 2003 to the change in wage inequality over time. As shown in Table 1, from early 1980s to the early 2000s, wage inequality increased significantly more in the United States (by 32 log points) compared with the CEU (6 log points). Can the human capital mechanisms studied so far help us understand this “widening” of the inequality gap as well? One challenge we face in trying to answer this question is that the tax schedules we derived above are only available for the years after 2001, whereas the tax structure has changed over time for several of the countries in our sample. Fortunately, for two countries in our sample—the US and Germany—we are also able to derive tax schedules for 1983, which allows us to conduct a two-country comparison in this section.

How to Introduce SBTC? As noted earlier, in the standard Ben-Porath model studied so far, the price of human capital \((P_{H})\) was simply a scaling factor and had no effect on any implication of the model, which is why we normalized it to 1 above. This is an important shortcoming when the goal is to study the changes in human capital investment over time in response to changes in the value of human capital, due to, for example, SBTC. Guvenen and Kuruscu (2010) proposed a tractable way to extend the Ben-Porath model that overcomes this difficulty. This extension basically involves introducing a second factor of production—raw labor (\(\ell\))—in addition to human capital, \(h\). The key assumption is that, unlike human capital, raw labor cannot be accumulated over the life cycle (it is fixed). Individuals supply both factors of production for a total hourly wage of \(\left (P_{H}h_{s}+P_{L}\ell \right)(1-i_{s})\) at age \(s,\) where \(P_{L}\) is now the price (wage) of raw labor. With this two-factor structure, a rise in \(P_{H}\) does increase human capital investment. So SBTC could be modeled as a rise in \(P_{H}\) over time with \(P_{L}\) fixed. (All parameters other than \(P_{H}\) remain essentially unchanged in calibration.) The formal statement of this model along with the calibration of SBTC are presented in Appendix E.7.

Comparing the United States and Germany.

The procedure for constructing the 1983 tax schedules is described in Appendix B.3 and the resulting progressivity wedges are shown in Figure 6. As seen here, in 1983 the progressivity of the tax structure in the US and Germany was similar in both countries up to about twice the average earnings level. And above this point, the US actually had the more progressive system. Over time, the US became much less progressive, whereas the change in Germany was more gradual, making the US tax schedule much flatter than that of Germany over time.

Using these schedules, we conduct three experiments.28 In the first experiment, we assume that the tax schedules remained fixed throughout this period. We choose one parameter that controls the skill bias of technology, \(P_{H},\) to match the 32 log points rise in L90-10 in the US during the period. Note from column (1) of Table 8 that, in the data, L90-10 rose by only 13 log points in Germany during the same period. Turning to the model and assuming that Germany has been subject to the same SBTC as the US, the model generates a rise of 19 log points in L90-10 for Germany. Thus, whereas the inequality gap widens in the data by \(32-13=19\) log points, the model predicts \(32-19=13\) log points, explaining 68% (13/19) of the observed difference in the data.

| Data | Model | |||

| (1) | (2) | (3) | (4) | |

| Taxes: | Fixed | Changing | Changing | |

| SBTC: | Calibrated to US | Fixed | Calibrated to US | |

| Panel A: Change in L90-10 | ||||

| US | 0.32 | 0.32\(^{a}\) | 0.21 | 0.32\(^{a}\) |

| GER | 0.13 | 0.19 | 0.01 | 0.09 |

| \(\Delta\)(US-GER) | 0.19 | 0.13 | 0.20 | 0.22 |

| Panel B: Change in L90-50 | ||||

| US | 0.22 | 0.23 | 0.15 | 0.23 |

| GER | 0.05 | 0.14 | 0.01 | 0.06 |

| \(\Delta\)(US-GER) | 0.17 | 0.09 | 0.14 | 0.17 |

| Panel C: Change in L50-10 | ||||

| US | 0.10 | 0.09 | 0.06 | 0.09 |

| GER | 0.07 | 0.05 | 0.00 | 0.03 |

| \(\Delta\)(US-GER) | 0.02 | 0.04 | 0.06 | 0.06 |

Second, in column (3), we consider the case where the only change over time is in the tax schedules. We do not recalibrate any parameter to match targets in 1983. In the US, L90-10 rises substantially—by 21 log points—with no SBTC. Hence, the flattening of the tax schedule alone accounts for a significant fraction (about 2/3) of the rise in US wage inequality during this time. To our knowledge, this result is new in the literature. In contrast to the US, wage inequality barely changes (by 1 log point) in Germany. This experiment suggests that the dramatic fall in progressivity in the US and the small change in Germany alone could explain almost all of the widening inequality gap! Third, we now incorporate the change in tax schedules and re-calibrate SBTC such that we match the change in L90-10 for the US.29 Now, L90-10 rises by 9 log points in Germany. Thus, the model slightly over-explains—by 16% (\(=0.22/0.19-1.0\))—the widening gap in the data.

Panels B and C of the table explore how much of the widening gap has occurred at the top and bottom of the distribution. In the data, the L90-50 gap between the US and Germany rose by 17 log points, whereas the L50-10 gap increased by only 2 log points. Therefore, a remarkable fact is that virtually all of the rise in the inequality gap occurred because top-end inequality increased much more in the US (by 0.22) than in Germany (by 0.05). This observation strongly indicates that to understand the widening inequality gap, one needs to understand the economic forces that operate above the median of the wage distribution—and the human capital channels studied here provide one important candidate. To quantify these human capital effects, we turn to column (4): the model generates the same 17 log points rise in the L90-50 gap as in the data, and overstates the L50-10 gap observed in the data by 4 log points.

While these results are encouraging, a caveat must be noted. First, wage inequality in 1983 depends not only on the tax schedule in 1983, but also on the tax schedules that were in place several years prior, since the dispersion in human capital across individuals results from investments made in previous years. Clearly, the same comment applies to 2003. Although in our exercise we do not account for this fact, it is not clear which way this biases the results. This is because the US tax system was even more progressive before the Economic Recovery Tax Act of 1981, whereas the progressivity change in the years preceding 2003 (say, from 1990 to 2003) was more modest. Therefore, if we were to use a time average of tax schedules in our exercise (say, 1973 to 1983 and 1993 to 2003), we conjecture that the reduction in progressivity over time could be larger than we assumed in the experiment just described (which would attribute an even larger role to taxes). A more complete examination of this issue is an exciting topic for future research.

6 Microeconomic Evidence on the Mechanism

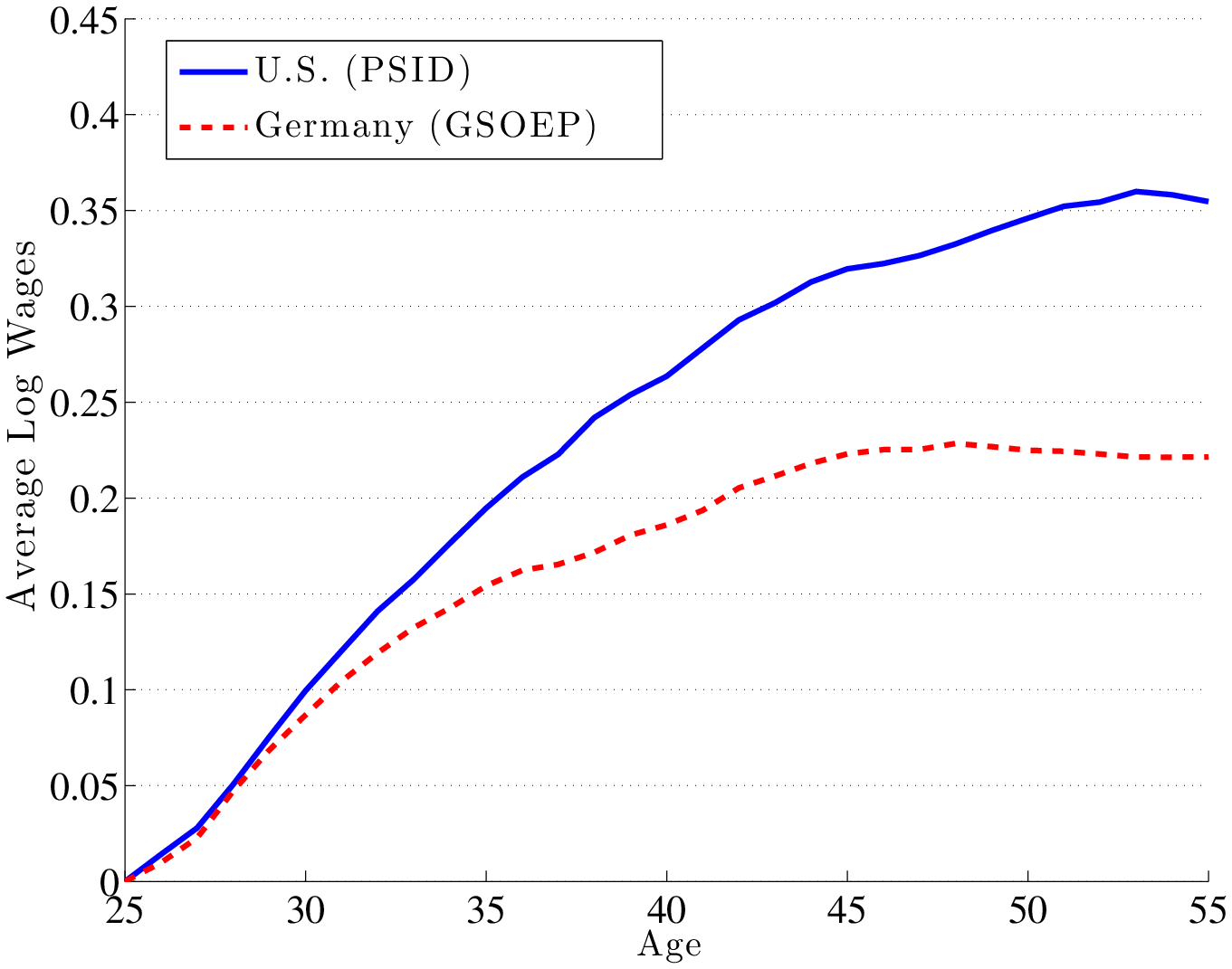

The model also makes predictions about how the lifecycle profiles of wages and hours vary across countries. In particular, because progressivity dampens human capital investment, average wages should grow more slowly over the life cycle in the CEU. Similarly, because progressivity compresses the cross-sectional distribution of human capital investment, wage inequality should rise less over the life cycle in the CEU. Testing these two predictions requires repeated cross-sectional data (or panel data) on wages (to disentangle the age profile from time or cohort effects), which is difficult to obtain on a comparable basis for the CEU countries in our sample.30 An exception is the German Socio-Economic Panel (GSOEP), which includes information on wages and hours of German individuals and is available to outside researchers. In this section, we make use of this data set and the PSID for the United States to provide a two-country comparison of lifecycle profiles.

6.1 Wages and Hours over the Lifecycle: US vs Germany

We focus on male workers who are between 25 and 55 years of age to minimize the effects of early retirement behavior and the consequent fall in employment rates at later ages. The PSID data cover 1968-1992 and the GSOEP data cover 1984 to 2007.

Wages. Figure 7 plots the lifecycle profile of mean log wages in the US and Germany. The profiles are extracted from panel data by cleaning cohort effects following the usual procedure in the literature; see Appendix G for details. As seen in the figure, from age 25 to 55 the average wage profile rises by 36 log points in the US, but by only 22 log points in Germany, consistent with the prediction of the model that a more progressive tax system generates a flatter average wage profile. The model counterparts of these numbers are also of interest. In the model, the rise in the mean log wages (from age 25 to 55) in the US exceeds the same statistic in Germany by 16 log points, which compares well with the 15 log points figure just reported in the data.

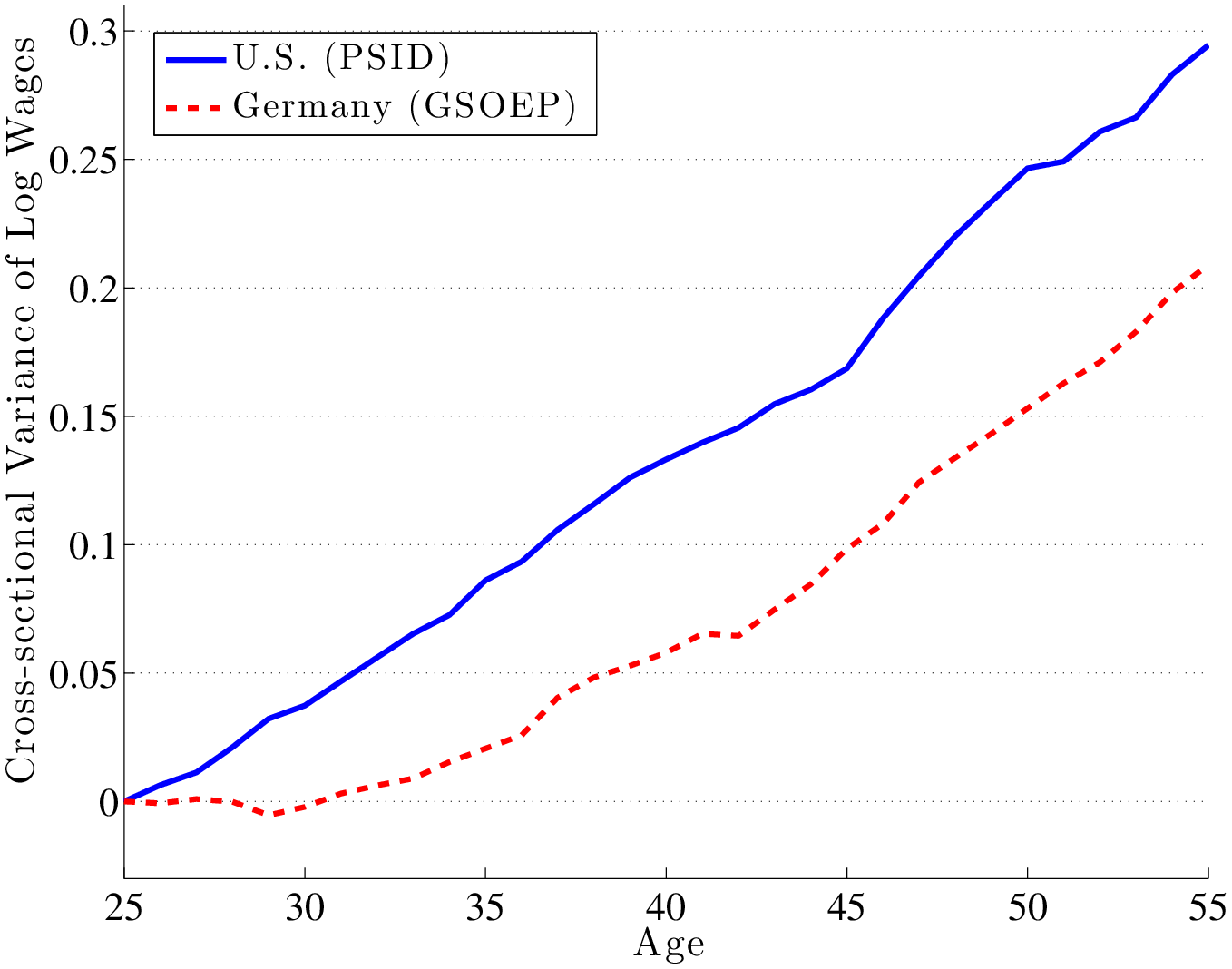

Next, the left panel of figure 8 plots the lifecycle profile of wage inequality (again controlled for cohort effects) for the two countries. In the US, the variance of log wages rises by 30 log points, compared with 21 log points for Germany. Again, inequality rises more over the lifecycle in the less progressive country, consistent with the mechanism in the model. Turning to the model, it predicts a 16 log point gap between the two countries, compared to 9 log points (\(=30-21\)) found in the data.

Although in figure 8 we normalized the intercept to zero to help visual comparison, a relevant question is, how much wage inequality is there at the time workers enter the labor market? To answer this question, we compute the variance of log wages for workers between ages 23 and 27 and find it to be very similar in both countries: 0.251 in the US and 0.260 in Germany.31 This implies that virtually all the difference in wage inequality between Germany and the United States documented in the previous section is generated by the faster rise of inequality over the lifecycle in the US compared to Germany and almost none is due to differences in initial inequality. This is also true in the model: the variance of log wages averages 0.133 for the US and 0.148 for Germany in the first five years of the lifecycle. This is a small gap compared to the 16 log points faster rise in wage inequality between ages 25 and 55.

Finally, instead of controlling for cohort effects as we did above, one can alternatively control for time effects. Using this approach, mean log wages rise by 0.37 in the US compared with 0.27 in Germany. Inequality rises by 0.12 in the US compared with only 0.02 in Germany. Thus, while the magnitudes change, the rankings of the two countries remain the same under this alternative approach.32

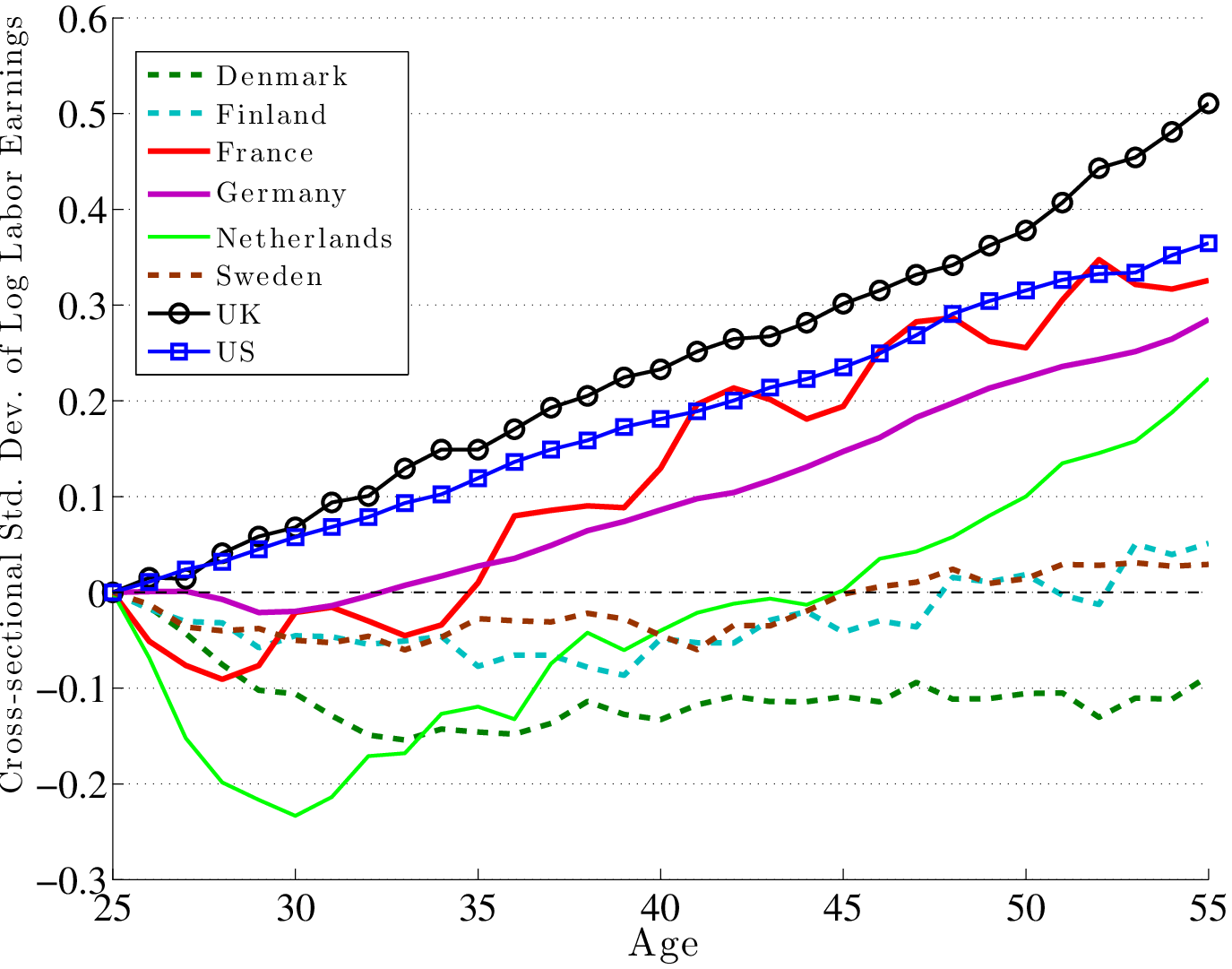

Earnings. Ideally, we would like to expand the comparison in the left panel of Figure 8 to all countries in our sample. However, this would require examining several distinct micro data sets—one for each country—which is beyond the scope of this paper. One option is to use the Luxembourg Income Study (LIS), which is a harmonized cross-country data set. One drawback of this data set is that it does not allow one to compute wages at different points in time, which is needed to clean cohort effects, as we did above. The data set does, however, contain earnings information at several points in time, which we use to construct life cycle profiles of earnings inequality for the six countries other than the US and Germany (right panel of Figure 8).33 For the US and Germany, we continue to use the PSID and GSOEP.

Three groups of countries can be discerned in the right panel. The UK and the US form the top group, with the largest rise in earnings inequality over the lifecycle. Scandinavian countries are concentrated at the bottom of the figure, with Sweden and Finland displaying increases of only 3 and 5 log points (in standard deviation), respectively, and Denmark recording a decline of 17 log points over the life cycle. Finally, the remaining three countries in western Europe—Germany, France, and Netherlands—line up in the middle. This ranking of countries is virtually the opposite of their ranking by progressivity (Figure 2) and is therefore consistent with the prediction of the model. We can also compute the model-data correlation for the change in the variance of log earnings between ages 25 and 55. This correlation is 0.86.

Labor Hours. We begin with the dispersion in hours. In Germany (GSOEP), the standard deviation of log hours is 0.369 compared with 0.324 in the United States (PSID).34 It is a well-known fact that incomplete markets models without preference heterogeneity severely understate the level of hours inequality (c.f. Erosa et al. (2009)) and our model is no exception. In the model, \(\sigma (\text{log}(n))=0.112\) in the US and \(0.128\) in Germany.35 Despite missing on the levels, the model is consistent with the fact that hours inequality is somewhat higher in Germany than in the US.

At first blush, it may seem surprising that the model implies higher dispersion in the more progressive country. The reason has to do with lump sum transfers, which happens to work in the opposite direction to progressivity in this two-country comparison. Specifically, the calibrated model implies that lump-sum transfers in Germany are more than twice as large as in the US. By their nature, these transfers create a larger wealth effect on low-income individuals (it is a larger fraction of their income) and, therefore, reduce their labor supply more than that of higher-income individuals. Thus, countries with higher lump-sum payments (or more redistributive government services), ceteris paribus, have higher hours inequality. To illustrate this point, we solve the model for Germany by fixing the lump sum transfers to the same fraction as in the US and assume the rest of the budget surplus yields no utility. The implied standard deviation of log hours falls from \(0.128\) to \(0.098\), which is now lower than in the US. Therefore, the predictions of the model regarding hours inequality is ambiguous, being driven by progressivity and the size of lump-sum transfers.

Overall, the lifecycle evidence on wages and hours documented in this section are in line with—and therefore provide further support to—the human capital mechanism that operates in our model.

6.2 Labor Productivity and Average Hours Across Countries

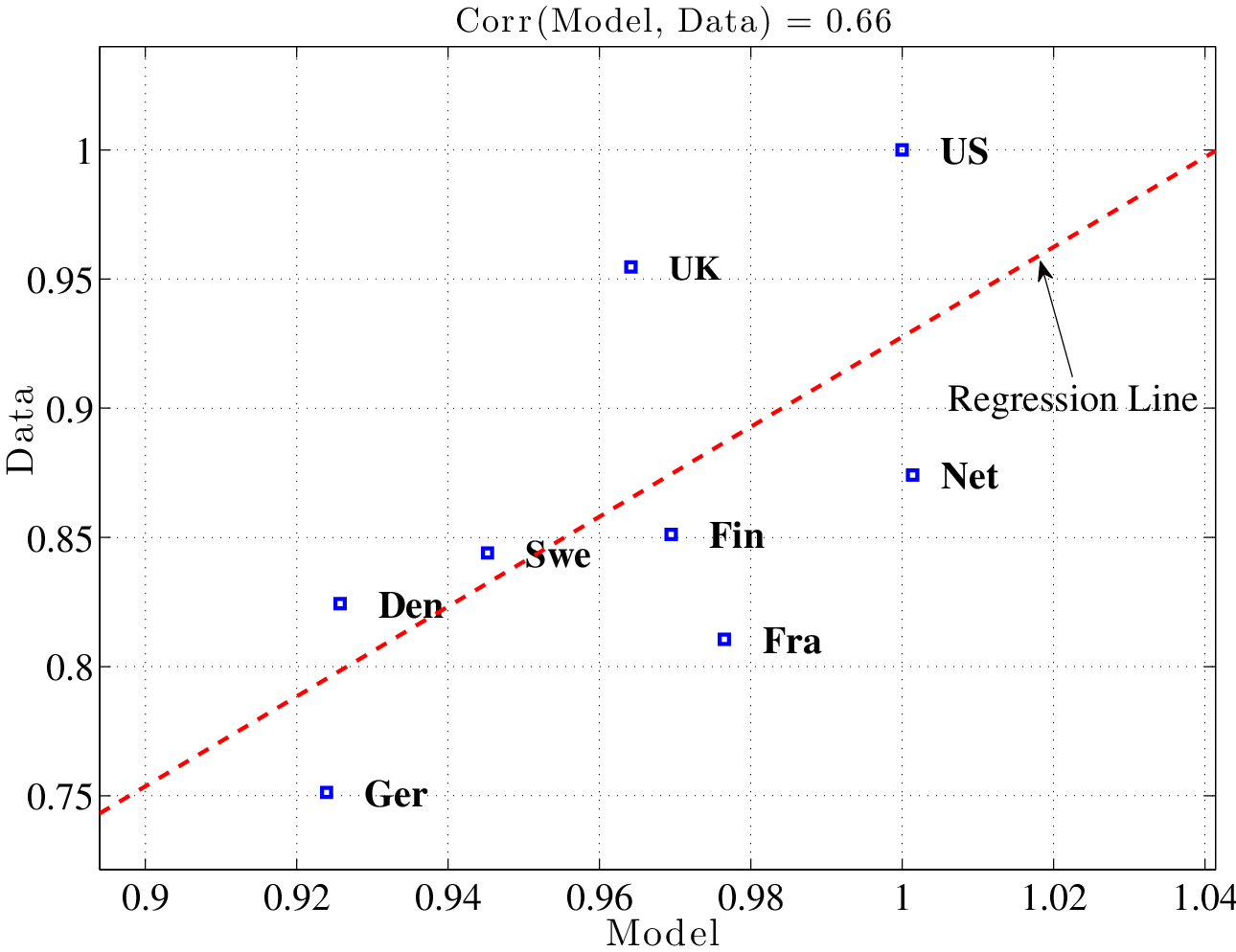

Hours Worked. We now turn to a comparison of average hours across countries. First, is well documented that Americans on average work much longer hours than Europeans (Prescott (2004), Ohanian et al. (2008)). Here we show that the same is true when we focus on males, and further examine if the variation is consistent with the variation in labor market policies captured by our model. The data are from Chakraborty et al. (2012), who provide average hours per male for a number of European countries by combining different data sources.36 The data are for males aged 25–54 in year 2000.

We begin by first comparing the US to Germany. An average German male works 25% fewer hours than his US counterpart (1467 hours versus 1952 hours per year). The model predicts a gap of 8%, and so explains only about a third of the empirical gap between these two countries.37 This is one statistic that clearly would be sensitive to the assumed Frisch elasticity. The alternative calibration with a Frisch elasticity of 0.5 discussed above (in Section 5.1) generates a 17% gap, which is closer to the data.

Next, we turn to a comparison of all 8 countries. We can also compute the average hours per male for the CEU. This statistic is 1612 hours, which is 17% lower than its US counterpart. The baseline model generates a small gap of 4% difference, whereas the high-Frisch model generates an 11% gap. Furthermore, one can also look at the average hours data, country by country, to see how well the model captures the variation across these 8 economies. Figure 9 plots the data against the model predictions. The model-data correlation is 0.66 for eight countries and is 0.73 when the UK is excluded. As before, raising the Frisch elasticity to 0.5 increases the correlation to 0.76.

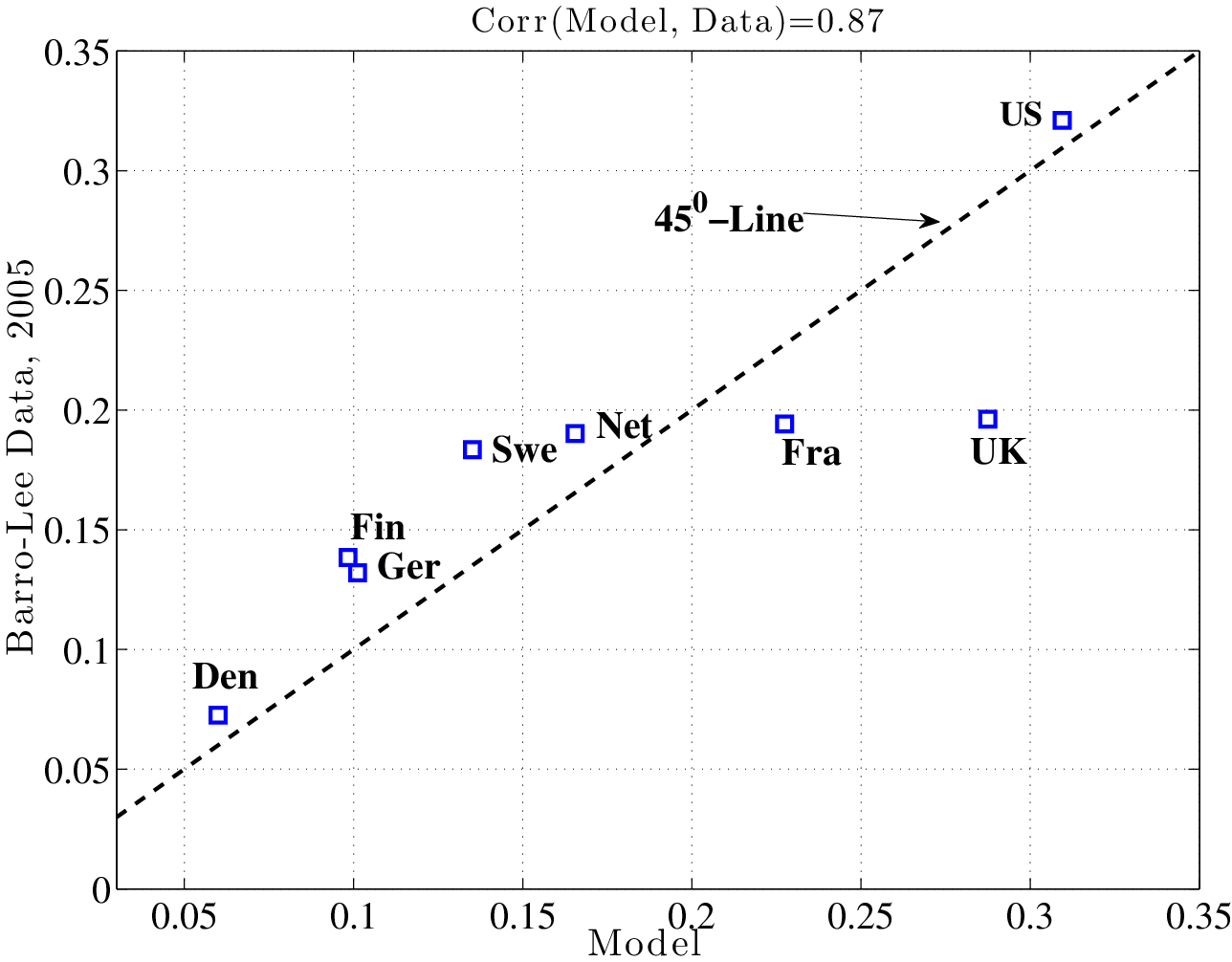

Labor Productivity. We now examine the predictions of our model for cross-country productivity differences, which is clearly an important topic. One challenge here is that our model is calibrated to data on males only, whereas the most common measure of labor productivity is measured for all workers, including females (GDP per hours worked). Computing male productivity would require data on GDP per male worker, which is difficult (if not impossible) to come by. With this important caveat in mind, we compare labor productivity in each country to GPD per (male) hour in the model. The data are obtained from the OECD StatExtract web site, and labor productivity is expressed as a percentage of the US level. The second row reports the model counterpart.

Starting from the last column Table 9, which reports the CEU average, the model predicts that labor productivity in the CEU is 83.2% of the US level; the actual figure is 90.4%, so the model under-predicts productivity in the CEU. Looking at each country, the model does quite well for Finland and Sweden, does reasonable well for France, and does less well for the remaining countries. The UK is still the only outlier, in the sense that the model significantly overpredicts labor productivity for that country.38

| GDP per hour worked (% of US) | |||||||||

| Den. | Fin. | Fra. | Ger. | Net. | Swe. | UK | US | CEU | |

| Data | 88.8 | 79.8 | 95.8 | 92.7 | 99.3 | 85.9 | 78.4 | 100 | 90.4 |

| Model | 78.7 | 81.0 | 90.4 | 81.6 | 85.0 | 82.0 | 98.8 | 100 | 83.2 |

6.3 Educational Attainment Across Countries